DVLA's annual report and accounts 2015 to 2016

Updated 19 July 2016

© Crown copyright 2016

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/dvla-annual-report-and-accounts-2015-to-2016/dvlas-annual-report-and-accounts-2015-to-2016

1. Non-Executive Chair’s introduction

I am delighted to introduce you to the DVLA’s Annual Report & Accounts which sets out the agency’s performance and achievements for the year.

During the year the agency put more of its services online. The new services provide the customer with a simpler and more efficient way of using public services. DVLA’s digital business is moving at a fast pace and it will continue to do so over the coming years.

In 2015, DVLA successfully made a major change to its operating structure, transferring its previously outsourced IT to an in-house service. A major part of this significant project has been the transfer of skilled IT staff from the previous supplier to DVLA, providing business continuity and IT expertise into the business.

DVLA is one of the largest employers in South Wales, providing employment for around 5,430 staff in Swansea. Developing the IT skills of our staff in order to deliver our strategic plan is important to DVLA and we work with local universities to help achieve this. Swansea University has agreed to provide training for agency staff on their Computer Science Foundation course. In addition, 2 Cardiff Business School students successfully secured a 20 week placement at DVLA. During the year, 37 staff across the agency successfully completed apprenticeship schemes.

DVLA’s partnership with TechHub Swansea continues to provide a facility for future innovation and digital services. The TechHub moved to a new building during the year, which is part of an Urban Village regeneration scheme in Swansea‘s city centre. The TechHub partnership allows DVLA to offer placements and projects to undergraduates.

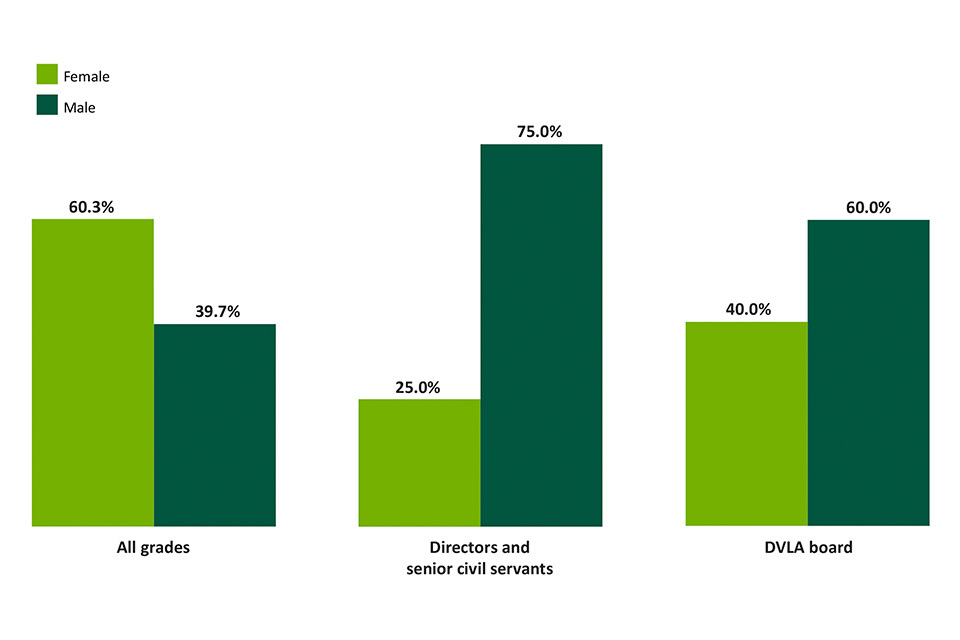

In 2015-16, the agency focused on increasing the percentage of women in our senior grades which currently stands at 25% across the agency and 40% on our Executive Board. We have been working on a number of initiatives to address this, including participating in cross civil service career development programmes aimed at under-represented groups.

We have been working with the Black, Asian and Minority Ethnic (BAME) community to attract more staff into the agency, representation currently stands at 0.9%. The agency has also been working with the Welsh Government Equality Network and the Regional Equality Group and local community groups to provide work placements, insight into recruitment and competency based vacancies.

This has been another successful year for the agency. There are exciting times ahead and I look forward to working with the Board, Executive Team and staff to build upon the successes of 2015.

Lesley Cowley OBE,

Non-Executive Chair

6 July 2016

2. Chief Executive’s message

The last year has been both a historic and exciting time for DVLA. Our transition from IT outsourcing to managing and delivering our IT in-house was an overwhelming success, a first at this scale in government.

The transition of our IT was carried out without any inconvenience to our customers and staff; this was as a result of both the hard work and commitment of our staff and the support of my Executive Team.

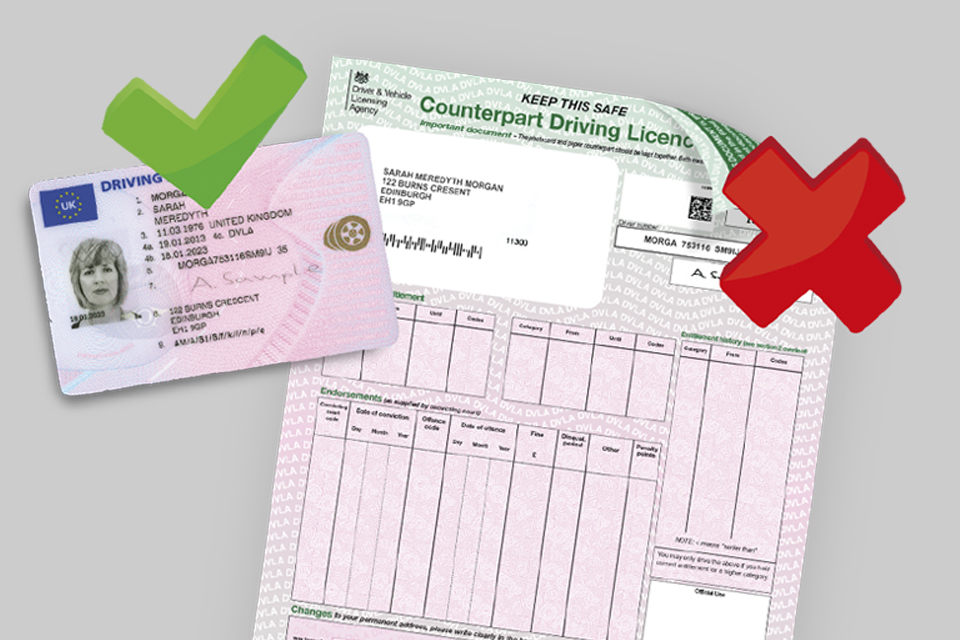

It was out with the old – abolition of the paper counterpart to the photocard driving licence and in with the new – the introduction of new online services for our customers.

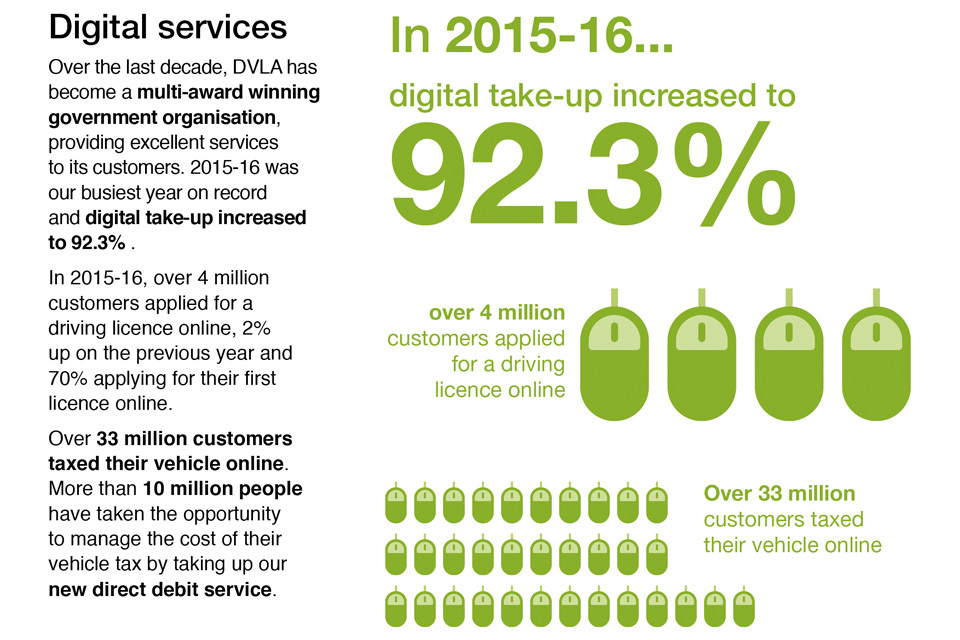

Continuous improvement and the introduction of new digital services has made it easier for customers to transact with us. Digital take-up has increased to 92.3% (87.8% in 2014-15).

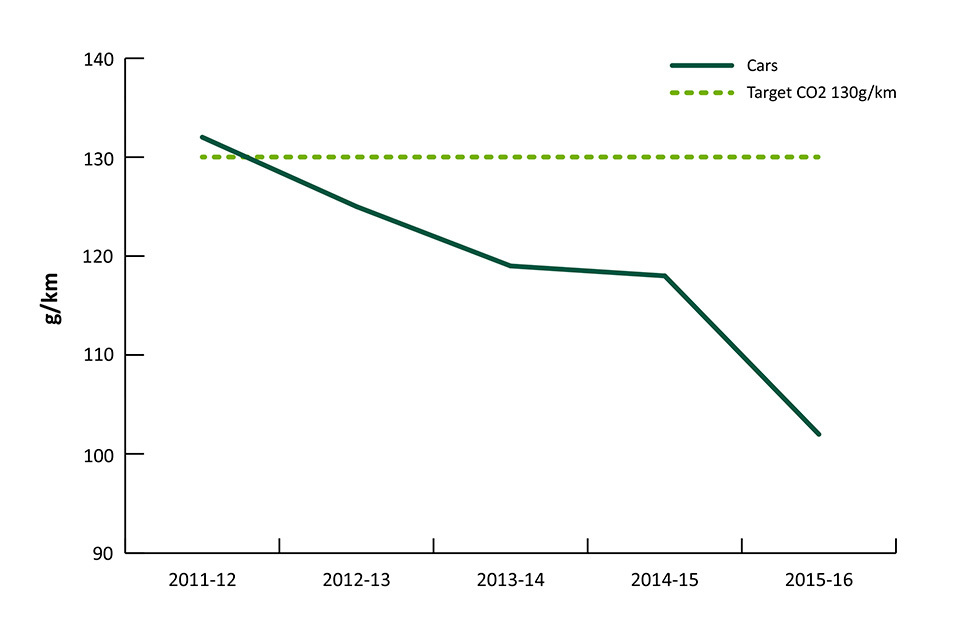

The Roadside Survey on VED evasion published in November 2015, estimated a compliance rate of 98.6%, a 0.8% reduction since the last survey in 2013. We have, however, collected more VED income than was forecast by the Office for Budget Responsibility (OBR) as detailed in the Section 2 Report in the accountability report. We have taken steps to look at why evasion levels have increased and are developing a strategy to address this.

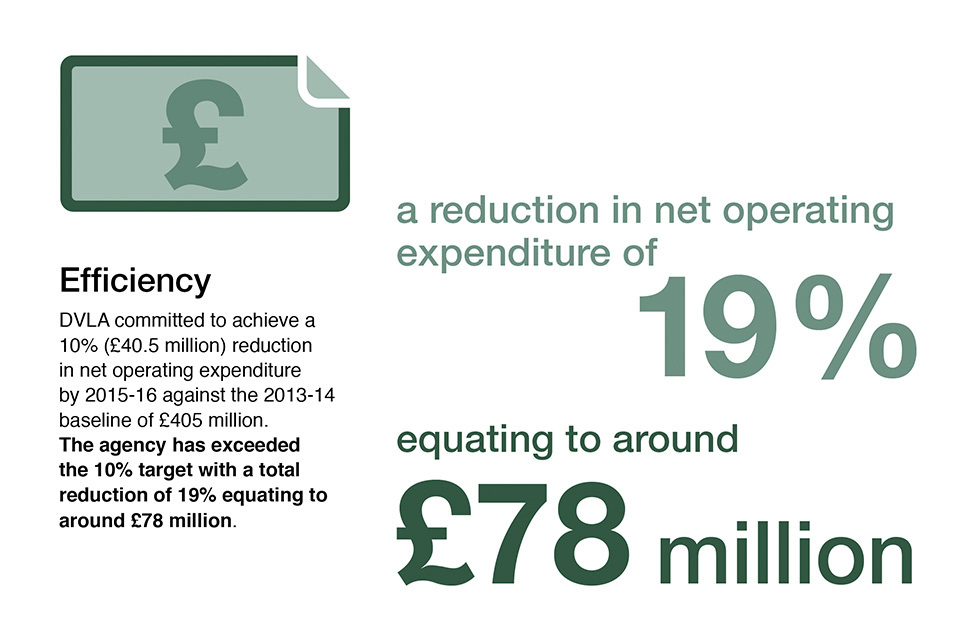

We exceeded our 10% efficiency saving for the year against the 2013-14 baseline of £405 million, with a total reduction of 19% equating to £78 million.

It was also a year of new opportunities. The significant improvements in our personalised registrations services took revenue over £100 million for the first time. We were successful in securing new business from Her Majesty’s Revenue and Customs (HMRC) to produce and mail 4 million tax return reminders. Our aim is to be recognised as a first class business provider and play a key role in delivering efficiencies and cost savings across government.

The numerous awards, recognition and accreditation that DVLA and staff have received over the year has been outstanding, I am proud to acknowledge them.

Next year will be even more challenging for DVLA. The digital world is fast paced and expectations from customers are growing. I am confident that we can continue to provide excellent services to our customers both digitally and through alternative service channels.

I look forward to next year.

Oliver Morley

Accounting Officer and Chief Executive, DVLA

6 July 2016

3. Highlights for the year

DVla have stopped using the paper counterpart to the photocard driving licence.

In 2015 to 2016, digital take up increased to 92.3%

DVLA introduced 10 new online services.

The agency secured work to produce and mail 4 million tax return reminders. The agency become the first in government to move away from a large scale IT contact

The agency exceeded the 10% target to reduce net operating expenditure by achieving a 19% reduction.

DVLA achieved the highest score of customer satisfaction across all sectors. The user experience testing lab was opened in 2015 to improve our services.

In 2015 to 2016 DVLA's personalised registrations scheme achived over £100 million for the first time in a financial year.

DVLA was voted fleet service company of the year. DVLA won 2 people managment awards.

DVLA contact centre achieved accreditation to the Customer contact association's new global standard 6. DVLA raised £43,578 for charity of choice LATCH. DVLA's communication team won best large in-house communucations team award.

4. Performance report

4.1 Who we are and what we do

DVLA is an Executive Agency of the Department for Transport (DfT) and forms part of the DfT Roads, Devolution and Motoring Group.

Our goal

Our goal is to get the right drivers and vehicles taxed and on the road as simply, safely and efficiently for the public as possible.

We are responsible for:

- maintaining over 47 million driver records

- maintaining over 39 million vehicle records

- collecting over £6 billion in Vehicle Excise Duty (VED).

We are also responsible for:

- recording driver endorsements, disqualifications and medical conditions

- issuing driving licences

- issuing vehicle registration certificates to vehicle keepers

- taking enforcement action against vehicle tax evaders

- registering and issuing tachograph cards

- selling DVLA personalised registrations

- helping the police and intelligence authorities deal with crime

- providing anonymised data to those who have the right to use the service.

DVLA digital services

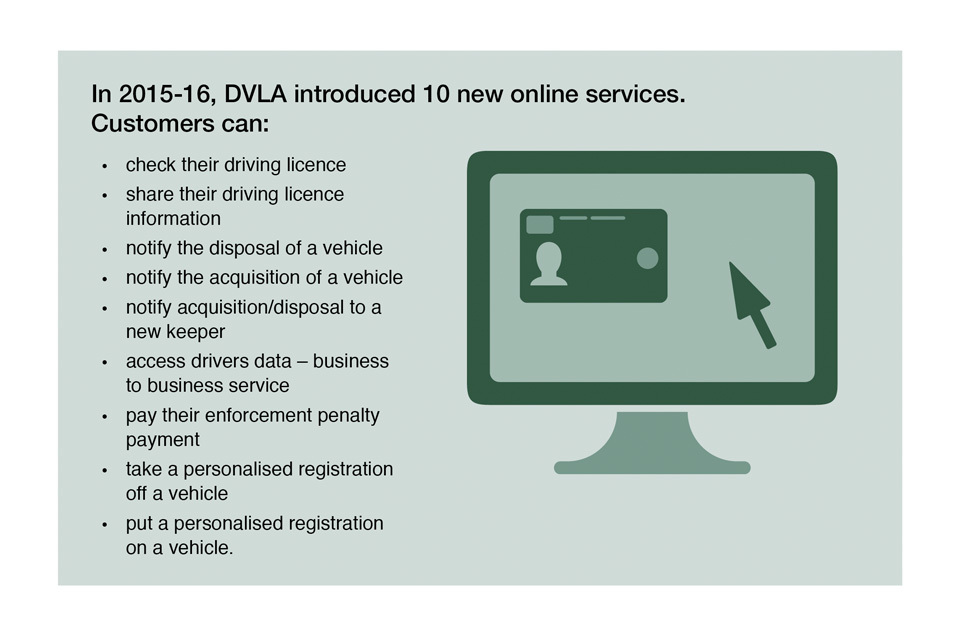

DVLA has a high reputation for providing innovative digital services. Over the last year we have introduced 10 new online services (see highlights for the year) and improved our current services. As a result of this, overall take-up has increased from 87.8 % in 2014-15 to 92.3% in 2015-16. Our online services include:

Vehicles online:

- pay your vehicle tax with the option to pay by direct debit

- vehicle management where customers can notify us that they have bought/sold a vehicle

- vehicle enquiry service to check if a vehicle is taxed

- personalised registrations where customers can transfer/retain their personalised registration

- pay your enforcement penalties online

Drivers online:

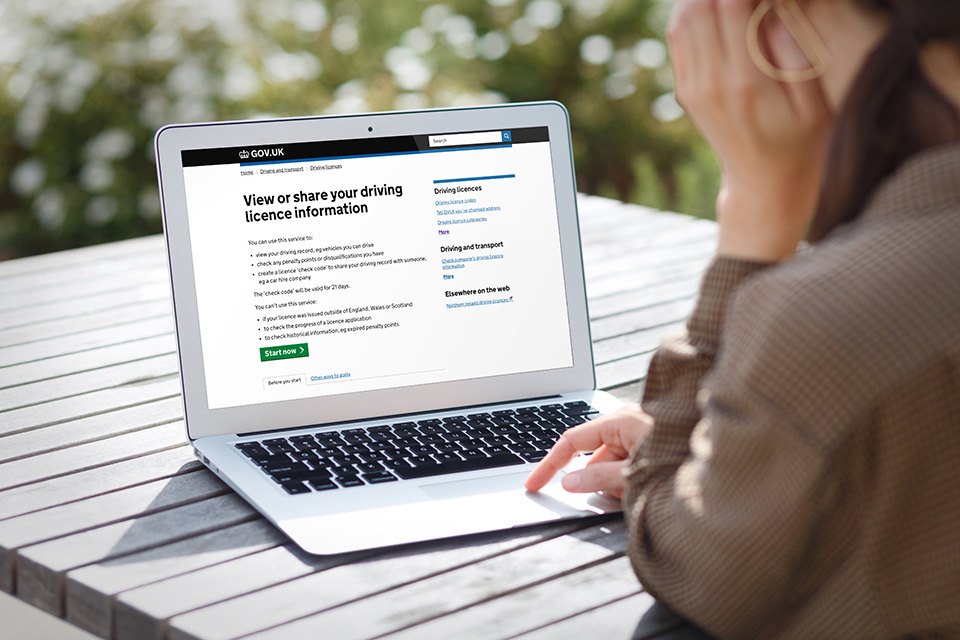

- view or share your driving record

- renew/replace your driving licence online

- my licence facility for drivers to give insurance companies permission to check entitlement to drive.

Commercial customers:

- automated first registration and licensing

- view vehicle record for fleet scheme members

- V5C on demand for fleet companies who choose to suppress the issue of the V5C

- selling/buying a vehicle to/from trade.

The purpose of this document

This Annual Report & Accounts sets out our performance and achievements for the year and should be read in conjunction with our business plan 2015-16.

4.2 Our strategic plan

We have completed the second year of our strategic plan 2014-17 (see paragraph 4.3 ‘Delivering against our business plan 2015-16’ in our performance report.

In 2015-16 we introduced new digital services and made significant improvements to our processes (see ‘Highlights for the year’) whilst focusing on our strategic goals of:

-

simpler licensing – simplify our policies and technology landscape to improve customer service

-

new opportunities – use our assets to grow new revenue, efficiency and opportunities across government

-

excellent services – build seamless, lean digital services that exceed expectations with more cost-effective channels, recognising and responding to different customer needs

-

the best of DVLA – develop our capabilities as a centre of excellence, building a unique culture which is commercial, confident and focused on our customers.

How we manage our organisation

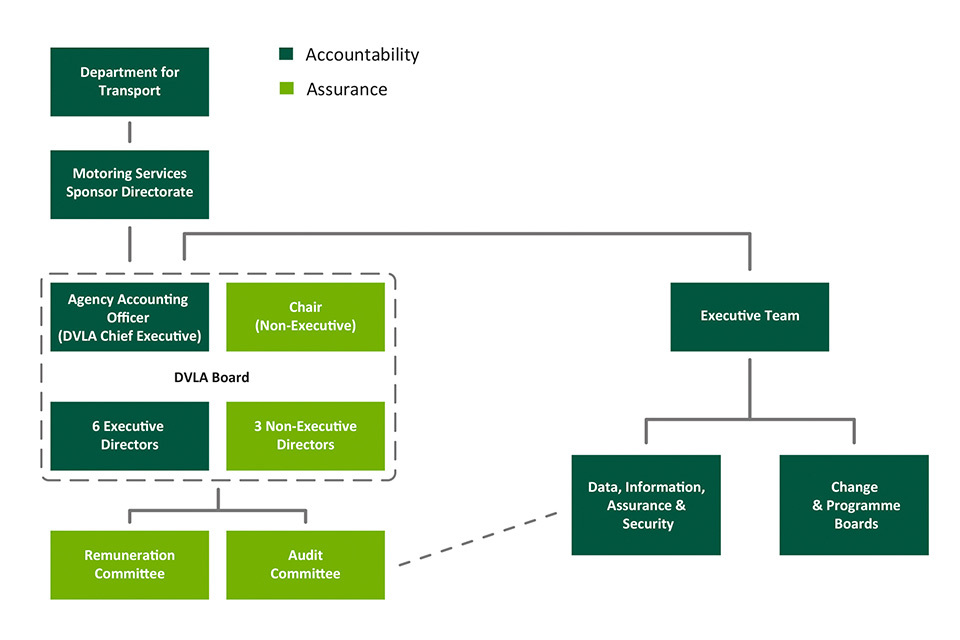

DVLA has a framework document agreed with the DfT, which establishes the governance, accountability, key relationships and financial management arrangements within which we operate. At the heart of these arrangements is the DVLA Board consisting of a Non-Executive Chair, Chief Executive (and Agency Accounting Officer), 3 Non-Executive Directors and 6 Executive Directors.

The DVLA Board establishes a clear control framework to support the effective management of risk, supported by delegations of authority and clear business processes, policies and procedures.

For more information about DVLA governance see the accountability report.

Risk management

Risk management continues to be important to DVLA. Details of the risks identified and addressed in 2015-16 are outlined in the governance statement.

Our key risks moving forward are:

- the ongoing risks relating to fraud, error and debt

- the related risks associated with data breaches and poor data quality

- the ongoing risks to IT security which are mitigated through the IT change agenda for example making new and existing systems as robust as possible in transition.

The risk management process has focused on increasing awareness and knowledge on how to effectively identify, manage and mitigate risks across the agency. This is to ensure there is a robust understanding of what risks affect our business, empowering staff to take accountability and responsibility for protecting the agency.

Social responsibility

The DVLA is committed to its corporate social responsibility policy and proactively supports initiatives that empower and benefit Welsh communities and individuals, giving as much back to the local area as possible. We have forged closer relationships with organisations in the region to share best practice and lessons learnt.

We have also played an active role around the digital economy. In November 2015, a digital innovation fund was launched by the Welsh government. This fund is being used to explore ways in which digital technology can help innovate public services in Wales. DVLA is one of the project partners.

DVLA is also a project partner with the new digital economy research centre in Swansea known as CHERISH-DE. This is one of the 6 world leading research centres announced by the Chancellor in the 2015 summer budget.

In 2015-16, DVLA software development community, continued to support local primary schools running code clubs in the Swansea area, teaching children aged 9 to 11 how to code. This is an ideal way to get children thinking more deeply about technology at a crucial age.

Since 2013, our approach to charitable giving has encouraged staff to annually vote for a charity of their choice – a selected charity to receive all fundraising proceeds from that year. Since launching the ‘Charity of choice’, we have seen a year-on-year increase in the amount of funds raised. A large part of this has been through the hard work, creativity and dedication of our staff.

2015 was a successful year for the agency’s fundraising efforts – staff ran marathons, entered raffles, shaved heads and participated in countless other events. Staff raised a total of £43,578 for the Welsh Children’s Cancer Charity LATCH, more than doubling the funds raised for 2014.

4.3 Delivering against our 2015-16 business plan

| 1. Reform | Measure | Result |

|---|---|---|

| 1.1 IT transformation – move to a new IT supply chain and digital service platform that provides customers with a 24/7 multi-channel service where appropriate | March 2016 | On 11 September 2015 DVLA moved away from its large IT supplier to deliver its IT services in-house. Integration of services onto the new digital service platform is under way |

| 1.2 Drivers medical reform – deliver actions agreed for drivers medical services reform as recommended in our strategic plan | March 2016 | We have improved our processes and introduced new online guidance to deliver actions agreed in our strategic plan (see ‘Drivers medical reform’ under paragraph 4.4) |

| 1.3 To deliver the facility to pay enforcement penalty payments online to provide a simpler, better, safer service to customers | Nov 2015 | On 26 March 2016, DVLA introduced a facility for customers to pay enforcement penalty payments online |

| 1.4 Stop issuing the paper counterpart to the photocard driving licence | June 2015 | DVLA stopped issuing the paper counterpart from 8 June 2015 |

| 1.5 Carry out a review of the impact of medical conditions on driving. Review and consult on the potential implications of raising the driving licence renewal age beyond the age of 70 | March 2016 | DVLA has reviewed older drivers with DfT and the Older Drivers Task Force. The findings of the review will be published in the summer of 2016 |

| 1.6 Review and develop a refined data sharing strategy | Dec 2015 | A data sharing strategy has been developed and is awaiting ministerial agreement |

| 2. Operational | Measure | Result |

| 2.1 Our total digital and automated transactions at March 2016 will | Exceed 75% | 92.3% |

| 2.2 To provide scheduled availability on: • electronic vehicle licensing • personalised registrations • driver licence online services |

98% | 99.97% |

| 2.3 To deliver in 8 working days a: ■ first driving licence ■ vocational driving licence ■ digital tachograph renewal |

98% of cases |

99.9% 99.4% 100% |

| 2.4 To answer calls queued to an advisor in 5 minutes | 95% of cases | 96.3% |

| 2.5 To maintain accuracy so that the registered vehicle keeper can be traced from details held on our record | 95% of cases | 92.6% |

| 2.6 Improve the accuracy of the driver records against the March 2015 outcome | 78% | 86.5% |

| 3. Customer service | Measure | Result |

| 3.1 Customer Service Excellence standard | Retain accreditation | Retained |

| 3.2 Customer Contact Association standard | Retain accreditation | Retained |

| 3.3 Improve our customer satisfaction results for key transactions against the March 2015 baseline: ■ I want to tax my vehicle ■ I want to amend my vehicle registration details ■ I want to renew my driving licence |

97.6% 88.1% 93.2% |

95.9% 92.4% 89.7% |

| 3.4 Develop a baseline for drivers medical customers satisfaction by March 2015 and improve by March 2016 | 76.8% | 76.6% |

| 3.5 Reduce the proportion of formal customer complaints not resolved at first contact by 10% against the 2014-15 baseline of 12.2% | 11% | 14.9% |

| 3.6 Comply with the Freedom of Information Act providing information within 20 working days | 93% | 99.9% |

| 3.7 Provide answers to questions asked in Parliament within the required timescales allowed | 100% | 100% |

| 3.8 Provide draft replies to ministerial correspondence within 7 working days | 100% | 99.6% |

| 3.9 Reply to official correspondence passed on from Whitehall within 20 working days | 80% | 99.7% |

| 3.10 Pay our invoices in 5 working days | 80% | 94.6% |

| 4. Finance and efficiency | Measure | Result |

| 4.1 Deliver an efficiency saving of 30% by March 2017 against the 2013-14 baseline net operational expenditure of £405 million | Deliver 10% | 19% |

| 4.2 Financial expenditure – manage our Departmental Expenditure Limit (DEL) total within plus or minus 10% (£128 million - £156 million) | March 2016 | £112 million |

| 4.3 Ensure by March 2016 DVLA full-time equivalents (FTEs) will number less than 4,900 | 5,554 | 5,430 |

| 4.4 Ensure the average number of working days lost (FTEs) due to sickness does not exceed | 7 days | 8.6 days |

| 5. Sustainability | Measure | Result |

| 5.1 Reduce greenhouse gas emissions (against 2009-10) | 25% | 28% |

4.4 Reform

IT transformation

On 11 September 2015, DVLA became the first in government to move away from a large scale IT contract. The seamless transition and minimal impact of the change to customers and employees has been acknowledged as a success for IT in government. The change is transforming the way in which DVLA delivers its business. Integration of services onto the new digital service platform is under way.

Over 180 third party contracts were successfully completed or re-procured before the end of the contract. The work of the commercial exit programme was highly commended at the National GO Excellence in Public Procurement Awards in March 2016.

Commercial

DVLA’s commercial team led the implementation of a DfT contract management system, which acts as the repository of all contractual information. DfT central and 4 agencies are successfully using the system with more to follow in 2016-17.

Business development

In February, DVLA secured a contract with HMRC to produce and mail 4 million tax return reminders which will deliver cost savings and improved efficiency across government.

DVLA’s personalised registrations have achieved sales of over £100 million, a significant increase compared to £87 million in 2014-15, reflecting the upturn in the overall market.

Drivers medical reform

The service DVLA provide to customers is very important and we are always looking to improve the customer experience. During the year we introduced new measures and employed additional staff to contribute to improving road safety and reducing the time taken to process medical cases.

Over the last year, we have delivered a programme of work on drivers medical reform as set out in our strategic plan 2014-17. We have:

- introduced longer period licensing for drivers with epilepsy from 3 years to 5 years and for certain cases where the driver has Parkinson’s disease or Multiple Sclerosis

- improved our processes for vocational driver licence first applications, by reducing the initial contact from 35 days to 5 days. All applications where a medical condition has been declared, will either be issued a driving licence, be refused a licence or sent a medical form to complete

- made changes to the Medical Examiner Report (D4) for vocational drivers to reduce the number of forms rejected

- updated and improved our drivers medical pages on GOV.UK to make it easier for customers to use and understand

- improved our contractual costs and turnaround times with our external provider of specialist visual field tests delivering a 35% saving and reducing the time for visual test appointments by 2 days

- increased the number of completed reports received from the visual test by 27% returned within 15 days and 95% within 30 days. Completed reports are being returned 4 days earlier than 2014-15, improving road safety

- DVLA published new guidance for the medical profession in March 2016. The new guidance titled Assessing Fitness to Drive, forms part of the agency’s wide-ranging plans to improve its services for the medical profession and drivers.

Review of driving licence renewal age

To support the government’s commitment to improve road safety, DVLA has been working with DfT and their sponsored Older Drivers Task Force to evaluate available data and approaches to older drivers. The task force has carried out a review of older drivers and intend to publish their findings in the summer of 2016. Once the findings have been published, we will consider the recommendations and next steps.

Online penalty payments

DVLA has introduced a new online service for customers to pay their enforcement penalties. This new service will provide customers with the facility to pay vehicle-related enforcement penalties and any arrears of vehicle excise duty owed. This service supports the government’s digital by default agenda, making it easier for the customer to transact with us whilst reducing costs to the agency. For more information visit our website.

For customers who are unable to use our online service, DVLA will continue to provide alternative payment channels.

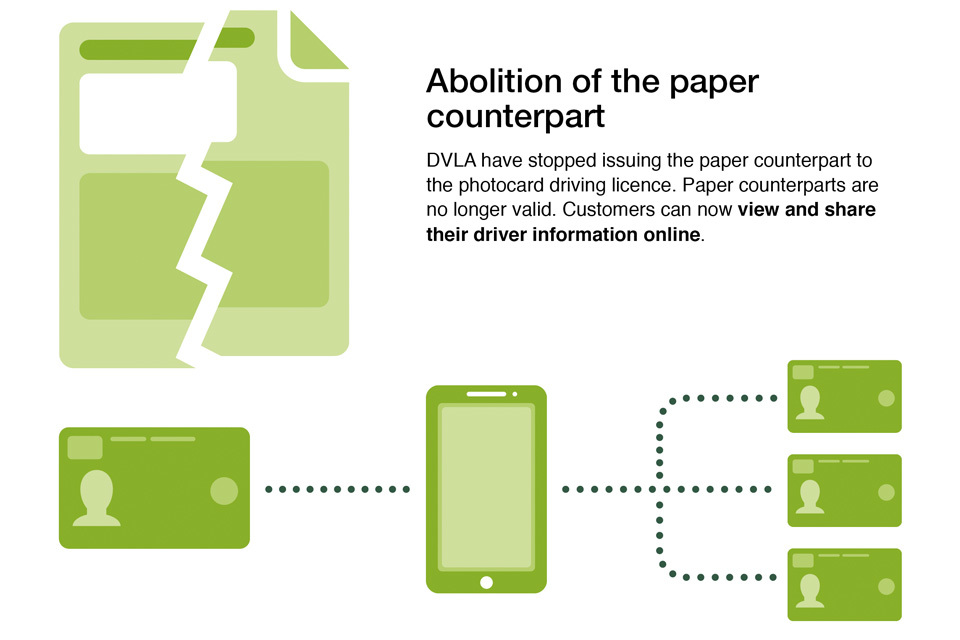

Abolition of the paper counterpart

On 8 June 2015, DVLA stopped issuing the paper counterpart to the photocard driver licence. The paper counterpart is no longer a valid document. This is part of the government’s commitment to cut red tape and remove unnecessary burden supported by DVLA’s strategy of simpler, better, safer services for our customers.

The abolition of the paper counterpart has contributed towards reducing the amount of paper we use in our operations, this equates to over 8 million counterparts per year.

Access to driving licence information is available on view or share your driving licence and is the digital alternative to the counterpart. Drivers in Great Britain can view their driver record online or share their details with third parties. This innovative range of services gives drivers control of their personal data and who they share it with. In 2015-16 over 12 million customers used this service.

Data strategy

During the year, DVLA carried out a review of its current data sharing activities to ensure that it fits with wider organisational objectives and our strategic direction.

We have taken into account the pressures on our current data sharing services. We have considered how best to improve services for existing customers. This included the assurance and audit of the release and use of data.

We will continue to engage with our customers to improve the technology that supports our digital services and focuses on potential changes to DVLA’s vehicle enquiry service. We will ensure that we include the necessary controls, audit arrangements and price structure for each service in line with our strategy and managing public money.

4.5 Operational

DVLA digital services

Over the last year we have introduced 10 new online services and made further changes to the digital services we offer. Our aim is to get as many customers as possible to transact with us digitally. Over the next few years we will put more of our services online. In 2015-16 take-up of our services available online continued to grow, achieving 92.3%.

DVLA Digital take-up 2014-16

| March 2014 | 74.8% |

|---|---|

| March 2015 | 87.8% |

| March 2016 | 92.3% |

Accuracy of DVLA records

During the period January 2016 to March 2016, a survey of 4,002 registered vehicle keepers was undertaken to determine the level of traceability of registered keepers from the details held on DVLA records. This survey is part of our ongoing activities to improve the accuracy of our vehicle records.

Historically, the accuracy of our vehicle records is high and our expectation for the year was to maintain vehicle accuracy at 95%. The results of our recent traceability survey showed that accuracy of the vehicle record continues to be high at 92.6% although under target.

The accuracy of our driver records has improved to 86.5% from the March 2015 outturn of 78%.

The increasing popularity of our online services has allowed customers to notify us sooner when they change their vehicle and driver licence details. This will contribute to improving the accuracy of both our driver and vehicle records. We have also updated information on our website to make it easier for the customers to understand how to notify us of changes to their details.

4.6 Customer service

Customer service standards

DVLA is committed to developing excellent services for our customers that are both meaningful to them and easy to use. DVLA is working closely with stakeholders, customers and other interested parties to ensure we provide services that suit their needs. For more information about our services visit our website.

Customer Service Excellence standard

In 2015 DVLA successfully achieved the Customer Service Excellence (CSE) standard, achieving continued accreditation since 2008. CSE accreditation demonstrates our commitment to achieve service excellence, putting our customers at the heart of our services.

DVLA contact centre

During the year DVLA’s contact centre continued to successfully support customers through changes, such as the abolition of the counterpart.

The contact centre achieved accreditation of the Customer Contact Association (CCA) Global Standard 6 in recognition of providing excellent customer service.

In March 2016, we introduced a new web chat facility to the existing telephone, email and social media channels. This will enhance the contact centre’s reputation as a multi-channel customer service provider against other leading public and private contact centres.

In the next year we will continue to modernise our contact centre. This will support and improve the quality of our customer service.

Customer satisfaction

During the year, DVLA built on its continuous improvement activities, focusing on customer expectations and satisfaction. Customer satisfaction levels are historically high, but our customers have expressed some dissatisfaction with our recent change to make vehicle excise duty non-transferable. We continued to achieve a high level of satisfaction from customers at 95.9%, slightly missing our target of 97.6%.

We narrowly missed the 93.2% customer satisfaction target for ‘I want to renew my driving licence’, achieving a satisfaction rate of 89.7%.

We achieved 76.6% satisfaction from our customers who have notified us of a medical condition. In 2016, we will introduce a new service for customers to notify us of their medical condition online. This will significantly improve the time it takes to process the application and contribute towards the improvement of customer satisfaction.

Our customer satisfaction results are based on a random sample of customers who have used the services during the year. As with any sampling of a population there will be a margin of error within the results. The table below sets out the 95% confidence interval based on the numbers sampled for each measure against each target.

| Customer Satisfaction Measure | Target | Result at 95% Confidence Interval |

|---|---|---|

| I want to tax my vehicle | 97.6% | 94.8% to 97.1% |

| I want to amend my vehicle registration details | 88.1% | 99.0% to 96.7% |

| I want to renew my driving licence | 93.2% | 87.7% to 91.6% |

| Drivers medical transactions | 76.8% | 72.2% to 81.0% |

DVLA user experience testing lab

As part of our commitment to deliver excellent digital services to our customers, we opened a user experience testing lab in 2015 to understand how customers use our services.

This new state of the art facility allows us to better test our services with our customers, giving us detailed feedback to help us improve our services. Our commercial customers are keen to explore this facility to help inform the development of their services.

Over the next year, we will be undertaking a best practice programme of user experience research, designed to accelerate the development of our driver and vehicles services.

Our commercial customers

Through engagement, extensive insight and a partnership approach, DVLA has changed the way it delivers its services to meet the differing needs of its customers.

During the year we continued to work closely with our corporate customers and stakeholders to strengthen our relationships and partnerships.

The motor trade, haulage, bus and fleet industries have all been active in working with us to create and test our new digital services. They have also used their communication channels and media to encourage customers to use our digital services.

In recognition of DVLA’s service to businesses, for the second year running, we have been voted Fleet Service Company of the Year in the 2015 Association of Car Fleet Operators (ACFO) Awards. This award is one we are most proud of as it recognises our achievements to deliver digital services to the fleet industry over the last twelve months.

Customer complaints

DVLA’s aim is to give the best possible service to its customers. We have to make difficult decisions as well as providing a high quality experience for our customers. It may not always be possible to meet customer expectations, as our decisions have to be made in line with relevant laws.

In 2015-16 the number of overall complaints reduced by 6.5% (12,775 compared to 13,660 in 2014-15). We failed to achieve the proportion of formal customer complaints not resolved at first contact against the 2014-15 baseline target of 11%, our final result was 14.9%. We have evaluated our processes and the evidence shows that the result was influenced by:

- major changes to vehicle licensing, involving the abolition of the tax disc and introduction of direct debit for VED

- delays in our drivers medical process early in the year meant that customers continued to write to seek explanations around the issue of their driving licence. We will continue to make improvements to our services to deliver drivers medical reform (see ‘Drivers medical reform’ under paragraph 4.4).

As a result, we have carried out a number of changes to the reported complaints process. We have commissioned a review using market research techniques and customer feedback on the clarity of the complaint process. We have also completed a review of the quality assurance process for complaint handling and initiated a professional complaint handling training programme. Customers now have direct access to our website to make a complaint.

For more information about our complaints procedures visit our website.

4.7 Finance and efficiency

DVLA’s accounts are made up of the business account and the trust statement.

Business account

The business account is segmented into:

- maintenance of the driver and vehicle database and related services

- sale of personalised registrations, which represents commercial income generated directly from the public. DVLA retains income to recover its costs in administering personalised registrations services with the excess paid to HM Treasury as consolidated fund extra receipts

- collection and enforcement of Vehicle Excise Duty (VED) including enforcement recoveries. Income stream from the collection of VED is accounted for in the trust statement

- services delivered to other government departments.

Financial results

DVLA’s total income for the year was £541 million against the £483 million forecast in our business plan 2015-16. The increase of £58 million is mainly due to:

- vehicles first registration volumes exceeding forecast by 9% which have generated an extra £15 million

- other fees and charges which include applications for replacement vehicle registration certificates and the transfer and assignment of personalised number plates to vehicles generating an increase of £26 million

- income from the sale of personalised registration numbers generating an additional £17 million. This is due to an increase of online sales from a forecast of around 600 per day to over 800. This reflects the upturn in the overall market.

Of the £58 million increase, £38 million has been surrendered to HM Treasury as consolidated fund extra receipts.

Total expenditure was £485 million against a business plan figure of £496 million. This is due to a number of variances:

- staff costs and ICT was £5 million less, following the move away from the IT contract

- expenditure on agents fees was £8 million lower than our business plan, as a result of customers moving to digital channels

- the cost of medical tests increased by £3 million against business plan, due to higher volumes of transactions being processed.

Departmental Expenditure Limit

As a government body, DVLA has budgets set at the start of the financial year in respect of its business account activities, known as the Departmental Expenditure Limit (DEL). The resource DEL outturn for the year is £112 million, £29 million under plan. Although expenditure has been steady, the additional income generated, as described above, resulted in a lower DEL requirement.

Trust statement

DVLA’s trust statement details the revenue in respect of VED, fines and penalties falling outside of the boundary of the agency’s business account.

Financial results

During the year the gross revenue amounted to over £6 billion, a decrease of £86 million on the restated 2014-15 results.

The net cost of collecting VED and the enforcement action taken as a result of non-compliance (brought to account in the business account) was £136 million, a decrease of £4 million against our business plan.

VED evasion

The Roadside Survey on VED evasion is carried out every 2 years to estimate the rate of evasion among vehicles seen on UK roads and the associated revenue loss. The survey is based on observing registration marks of vehicles in traffic carried out at 256 sites across the UK.

The Roadside Survey published in November 2015, estimated a compliance rate of 98.6%, a 0.8% reduction since the last survey in 2013. It is estimated that this may result in around £80 million in lost revenue for HM Treasury but some of this will have been recovered through enforcement activity.

There have been a number of changes to VED collection procedures since the 2013 survey which will have impacted on customer behaviour and these may also have contributed to the reduction in compliance.

-

Abolition of the tax disc – in October 2014 the paper tax disc, first issued in 1921, was abolished. As the last tax discs issued expired on 30 September 2015 it is likely that during the transitional period with customers becoming accustomed to the new tax changes that VED collection was affected. The agency has taken considerable steps to ensure that motorists are aware of the vehicle tax changes and have responded quickly where there have been issues.

-

Non-transferability of VED and automatic refunds – since 2014, vehicle tax ends when a vehicle changes ownership and the previous keeper is automatically refunded any full month of tax remaining. The new keeper is responsible for taxing the car immediately.

-

Direct Debit – the agency launched its Direct Debit scheme to manage the cost of VED in October 2014. There are around 10 million customers now using this service.

Once we have issued a new vehicle registration certificate V5C (log book) to a new keeper of a used vehicle, if they have not taxed that vehicle immediately, we write to remind them that VED is no longer transferable and that they must tax or notify us that their vehicle is kept off the road. Vehicle keepers who fail to tax receive a further reminder letter and those that still do not comply may have their vehicle clamped and/or impounded.

Efficiency

DVLA committed to achieve a 10% (£40.5 million) reduction in net operating expenditure by 2015-16 against the 2013-14 baseline of £405 million. The agency has exceeded the 10% target with a total reduction of 19% equating to around £78 million.

The savings have been achieved by realising the benefits from the following initiatives:

- abolition of the tax disc

- modernisation of DVLA’s network services

- centralisation of Northern Ireland vehicles services

- channel shift savings from the increased take-up of electronic vehicle licensing

- ICT Transformation including in-housing of our IT services.

4.8 Sustainability

Sustainability in DVLA

In 2015-16 the government extended the reporting period of the Greening Government Commitments (GGC) by one year. DVLA has exceeded all GGC targets with exceptional performance in reducing domestic flights and carbon from travel. Details of the performance against each commitment can be found below.

| Measure | Greening Government Commitment | 2009-10 Baseline | 2015-16 Target | Outturn 2015-16 | % Reduction Result 2015-16 |

|---|---|---|---|---|---|

| Greenhouse Gas Emissions | By 2015-16, reduce total carbon emissions by 25% of 2009-10 levels (tCO2e). | 18,261 | 13,696 | 13,125 | 28% |

| Greenhouse Gas Emissions | By 2015-16 reduce domestic business travel flight levels to 80% of 2009-10 levels (number of flights). | 1,747 | 1,397 | 102 | 94.2% |

| Waste | Reduce waste arising by 25% by 2015-16, relative to 2009-10 levels (tonnes) | 2,196 | 1,647 | 1,148 | 47.7% |

| Water | Reduce water consumption to an average of less than 6m3 per person per year (m3/FTE)(includes office accommodation only). | 4.58 | 6 | 3.84 | 16.2% |

| Administrative Paper | Reduce paper usage by 25% against the 2009-10 baseline by March 2015. For those organisations who had already achieved this level of reduction, to maintain the reduced levels achieved in 2011-12 (equivalent A4 reams). | 67,065 | 50,299 | 25,561 | 61.9% |

Further information is available in our Sustainability Report 2015-16. The following section details the minimum sustainability reporting requirements in accordance with the HM Treasury Public Sector Annual Reports: Sustainability Reporting Guidance 2014-15 and Greening Government Commitments Guidance.

Greenhouse Gas Emissions

Greenhouse Gas Emissions are made up of 2 components:

- emissions from travel

- emissions from the estate.

Emissions from travel

The emissions created by business travel have been reduced by 73.2%, between the baseline year of 2009-10 and this reporting year. This includes a reduction within the current year by a further 5% from 2014-15. A continued focus on reducing travel, changing modes of travel and procuring low emission DVLA fleet cars with the support of the Office for Low Emission Vehicles, have all contributed to the excellent performance against this target.

This was the final year of the Sustainable Operations on the Government Estate (SOGE) targets, GGC did not start until the following year.

Emissions from the estate

DVLA has achieved a decrease in emissions from the estate of 25.60% against the 2009-10 baseline, a marked improvement in performance from the end of last year. This has been achieved by introducing a more positive and agile way to managing our heating and cooling systems and by undertaking a number of other changes, such as fitting CO₂ sensors to automate management of air handling units. We have also installed variable speed drives to the main chiller pumps and are reviewing the lighting use across the estate and removing excess lighting.

| Years | 2009-10 | 2010-11 | 2011-12 | 2012-13 | 2013-14 | 2014-15 | 2015-16 |

|---|---|---|---|---|---|---|---|

| Scope 1 | 5579 | 5166 | 3662 | 4766 | 3218 | 3974 | 6224 |

| Scope 2* and 3 | 13290 | 13028 | 13308 | 12241 | 13061 | 11584 | 7146 |

| Total | 17290 | 17088 | 15818 | 15753 | 15080 | 14558 | 12864 |

| % Reduction | - | -1% | -9% | -9% | -13% | -16% | -26% |

(* Transmission losses emissions are included with Scope 2 (Grid Electricity Emissions))

Waste

In 2015-16 we saw a reduction in waste of 47.7%; this is almost a 2% improvement from the previous year. We continue to modernise our business, driven by our determination to reform our services and work in a way to make our services easier for customers to use. We are now realising the environmental benefits of initiatives such as abolition of the tax disc and the counterpart to the photocard driving licence.

Water

In 2015-16 we continued to achieve good practice consumption figures for our water consumption at 3.84m³ per FTE (good practice is between 4-6m³ per FTE). This is based on office space only. Our total consumption has reduced since the baseline year by around 10%. For more information see our Sustainability Report 2015-16.

Procurement

DVLA recognises the impact that its procurement decisions have on sustainability outcomes and continues to look for areas to improve our performance in this area. This year we have developed a specific action plan to focus on improvements, have a representation on the government-wide sustainable procurement group and continue to be committed to meeting the Government Buying Standards (GBS) best practice specifications wherever possible. More information on sustainable procurement can be found in our Sustainability Report 2015-16.

Transparency commitments

| Climate change adaptation | One of DVLA‘s properties is at risk of flooding. The local council has taken mitigating actions within the area and we have business continuity plans in place to reflect this risk. There are ongoing discussions about the longer-term future of this site for operational purposes. |

|---|---|

| Biodiversity and natural environment | The work that we have undertaken over the past few years as part of our focus on increasing the biodiversity of our sites is starting to show positive results. This year we have recorded 9 Section 42 species. |

| Procurement of food and catering services | Procurement of our food and catering services is done through our PFI contract. We undertake an annual check of this and the current supplier. The results of this annual check can be seen in our SD report. |

| Sustainable construction | No construction activities have been undertaken in the past 12 months. |

| People | More details on our social responsibility can be found in our SD report. |

Oliver Morley

Accounting Officer and Chief Executive, DVLA

6 July 2016

5. Accountability report

5.1 Corporate governance report

Directors’ report

Purpose of the Directors’ report

This report is presented in accordance with the requirements of the Companies Act 2006 (Strategic Report and Directors’ Report) Regulations 2013.

Members of the Board

Full disclosure of the serving directors for 2015-16 is available in the governance statement of this document. Directors have declared that they hold no significant third party interests that may conflict with their board duties.

Pension liabilities

The employees of DVLA are civil servants to whom the conditions of the Superannuation Acts 1965 and 1972 and subsequent amendments apply.

The Principal Civil Service Pension Scheme (PCSPS) and the Civil Servant and Other Pension Scheme (CSOPS, known as ‘alpha’) are unfunded multi-employer defined benefit schemes. DVLA is unable to identify its share of the underlying assets and liabilities. Provision is made in Note 11 of the business account to meet early retirement costs payable by DVLA up to employees’ normal retirement age.

Employees

Information about our policies and arrangements relating to staff is shown in the staff report.

External auditors’ remuneration

The external auditors did not undertake any non-audit work in the year.

Disclosure of audit information

The Accounting Officer has taken all steps that he ought to have taken to make himself aware of any relevant audit information and to establish that the agency’s auditors are aware of any relevant information.

Sickness absence data

The agency’s sickness absence measure is shown in the performance report.

HM Treasury cost allocation and charging requirements

Full disclosure of the agency’s compliance with the cost allocation and charging requirements of HM Treasury is reported within Note 2 of the financial statements.

Personal data related incidents

Full disclosure of the agency’s data controls is made through the Governance statement in the accountability report.

Future developments

The agency’s future developments are detailed in our strategic plan 2014-17 and business plan 2016-17.

Statement of Accounting Officer’s responsibilities

Business Account

Under the Government Resources and Accounts Act 2000, HM Treasury has directed DVLA to prepare for each financial year a statement of accounts in the form and on the basis set out in the Accounts Direction. The accounts are prepared on an accruals basis and must give a true and fair view of the state of affairs of the DVLA and of its comprehensive net expenditure, cash flows and changes in taxpayers’ equity, for the financial year.

In preparing the business account, the Accounting Officer is required to comply with the requirements of the Government Financial Reporting Manual and in particular to:

- observe the Accounts Direction issued by HM Treasury, including the relevant accounting and disclosure requirements and apply suitable accounting policies on a consistent basis

- make judgements and estimates on a reasonable basis

- state whether applicable accounting standards as set out in the Government Financial Reporting Manual have been followed and disclose and explain any material departures in the financial statements

- prepare the financial statements on a going concern basis.

The Permanent Secretary of DfT has appointed the Chief Executive of DVLA as Accounting Officer of the agency. The responsibilities of an Accounting Officer, including responsibility for the propriety and regularity of the public finances for which the Accounting Officer is answerable, for keeping proper records and for safeguarding the DVLA’s assets, are set out in Managing Public Money published by HM Treasury.

Trust statement

Under the Exchequer and Audit Departments Act 1921, HM Treasury has directed the DVLA to prepare, for each financial year, a trust statement detailing the revenue and expenditure in respect of Vehicle Excise Duty (VED), fines and penalties falling outside of the boundary of the agency’s business account. The trust statement is prepared on an accruals basis and must give a true and fair view of the collection and allocation of VED, fines and penalties, including the revenue and expenditure, financial position and cash flows. Whilst DVLA is concerned with compliance, the trust statement does not estimate the duty foregone because of non-compliance with the VED regime.

In preparing the trust statement, the Accounting Officer is required to comply with the requirements of the Government Financial Reporting Manual and in particular to:

- observe the Accounts Direction issued by HM Treasury, including the relevant accounting and disclosure requirements and apply suitable accounting policies on a consistent basis

- make judgements and estimates on a reasonable basis

- state whether applicable accounting standards as set out in the Government Financial Reporting Manual have been followed and disclose and explain any material departures in the trust statement

- prepare the financial statements on a going concern basis.

HM Treasury has appointed the Permanent Secretary of DfT as Principal Accounting Officer of the Department. The Chief Executive of DVLA holds the role of Accounting Officer for the purposes of the trust statement. The Accounting Officer is also responsible for the fair and efficient administration of the VED regime including the assessment, collection and proper allocation of VED revenue.

5.2 Governance statement

Introduction

The Permanent Secretary of the DfT has appointed me as Accounting Officer and Chief Executive for DVLA. As Accounting Officer, I have responsibility for the proper, effective and efficient use of public funds and may be required to appear before Parliamentary Select Committees. I am accountable to the Minister for the performance of DVLA in accordance with the framework document, which sets out the accountability and key relationships between DVLA and the DfT. I am also required as Accounting Officer by HM Treasury’s Managing Public Money and the Government Financial Reporting Manual to provide a statement on how I have discharged my responsibility to manage and control the resources for which I am responsible during the year.

DVLA is sponsored by DfT’s Roads, Devolution and Motoring Group which is also sponsor to the Driver and Vehicle Standards Agency (DVSA) and the Vehicle Certification Agency (VCA). DVLA is responsible for providing driver licensing services in Great Britain and the registration of vehicles and collection of VED throughout the UK. Regular meetings are held with Ministers to discuss the agency’s current issues and general progress. These are attended by the DVLA’s Non-Executive Chair, Chief Executive and the DfT sponsor as required.

Driver licensing in Northern Ireland is a devolved power and is undertaken by the Driver and Vehicle Agency (DVA), sponsored by the Department of Infrastructure in Northern Ireland. However, responsibility for licensing and registering of vehicles in Northern Ireland lies directly with the DfT Secretary of State.

Governance framework

I have ensured that the agency’s governance framework is designed to comply with the good practice guidance laid down in HM Treasury Corporate Governance in Central Government Departments: Code of Good Practice 2011. This has been supported by a Governance review undertaken by the Government Internal Audit Agency (GIAA) during 2015-16.

DVLA is managed by a Board and an Executive Team. The DVLA Board is chaired by a Non-Executive Director and has both strategic and business oversight responsibilities supported by the Audit and Risk Committee and the Remuneration Committee. The Executive Team is responsible for the day-to-day management of the agency in delivering its commitments to the government and the public as set out in the annual business plan. The agency’s high level governance structure is given below.

Governance structure

DVLA Board

The DVLA Board comprises a Non-Executive Chair, the Chief Executive, 6 Executive Directors and 3 independent Non-Executive Directors and focuses on the agency’s strategic direction. The Board gives assurance to the Secretary of State for Transport on the effectiveness with which the agency is run and is meeting its objectives and holds the Executive Team to account for the delivery of those objectives. The Non-Executive Chair is appointed by the Secretary of State. I appoint the Executive Directors with approval from the Permanent Secretary. Non-Executive Directors are recommended for appointment by the Chair to the DVLA Board, in partnership with the Director General of Roads, Devolution and Motoring at DfT. There is a clear demarcation between the DVLA Board and the Executive Team.

The DVLA Board meets formally each month to consider:

- the strategic direction and plans of the agency, including oversight of the agency’s change agenda and progress against the business plan

- oversight of the key risks and issues identified by the Executive Team and the effectiveness with which they are mitigated.

DVLA Executive Directors have specific areas of functional responsibility and accountability as below:

- Operations & Customer Services: Tony Ackroyd

- Human Resources and Estates: Phil Bushby

- Technology: Iain Patterson to 29 February 2016

- Strategy, Policy and Communications: Julie Lennard

- Finance: Rachael Cunningham

- Commercial and Business Development: Andrew Falvey

The Non-Executive Chair and the 3 Non-Executive Directors act through the monthly board meetings and as members of the Audit and Risk Committee and Remuneration Committee and have private sector backgrounds:

- Lesley Cowley, Non-Executive Chair (appointed 2014) in leadership and digital transformation

- Mike Brooks, Audit and Risk Committee Chair (appointed 2009, resigned 2015) in accountancy, audit and finance

- Jeremy Boss, Audit and Risk Committee Chair (appointed 2016), in accountancy, audit, finance and IT

- Christopher Morson (appointed 2013) in strategy and digital service transformation

- Emma West (appointed 2014) in talent management and organisational development

Executive Team

The Executive Team meets formally each week and has responsibility and accountability for delivering the agency business plan together with day-to-day management of the business. I chair this meeting and its membership is drawn exclusively from the agency’s executive directors.

The focus of these meetings changes every week over a 4 week cycle:

- Week 1 – Change Portfolio Delivery and Investment Decisions

- Week 2 – Operations

- Week 3 – Finance and Commercial

- Week 4 – Human Resources, Estates, Policy and Communications.

This regular and consistent rhythm builds a strong team ethic and a keen focus on business issues driving productivity and delivering change.

Board and Audit and Risk Committee attendance

Figures denote meetings attended (meetings available to attend) between 1 April 2015 and 31 March 2016.

| Name | DVLA Board | Audit and Risk Committee |

|---|---|---|

| Lesley Cowley, Non-Executive Chair | 11/(11) | N/A |

| Oliver Morley, Chief Executive | 11/(11) | 3/(4) |

| Rachael Cunningham | 10/(11) | 3/(4) |

| Phil Bushby | 10/(11) | N/A |

| Iain Patterson (to 29 February 2016) | 6/(8) | N/A |

| Tony Ackroyd | 11/(11) | N/A |

| Julie Lennard | 11/(11) | N/A |

| Andrew Falvey | 10/(11) | N/A |

| Mike Brooks, Non-Executive Director and Audit and Risk Committee Chairman (to 30 September 2015) | 6/(6) | 2/(2) |

| Jeremy Boss, Non-Executive Director and Audit and Risk Committee Chairman (from 21 January 2016) | 2/(3) | 1/(1) |

| Christopher Morson, Non-Executive Director | 11/(11) | 4/(4) |

| Emma West, Non-Executive Director | 10/(11) | 4/(4) |

| Paul Rodgers, DfT Non-Executive Director | N/A | 4/(4) |

| Sarah Scullion, DWP Non-Executive Director | N/A | 4 /(4) |

The ET has met 50 times in the year with non-attendance agreed in advance on an exceptional basis.

DVLA Board effectiveness

The Chair meets regularly with the Non-Executive Directors to discuss their performance and to ensure the agency gains greatest value from their external perspectives and experience.

The Board periodically undertakes self assessment reviews of its performance against Cabinet Office, National Audit Office and external good business practice guidance. The latest review was undertaken in September 2015. Whilst the review concluded there were no significant issues to address, the Board agreed a number of continuous improvement activities in the areas of strategic planning and development, external stakeholder engagement and Non Executive Director appraisal, development and performance reporting. Some outputs from the review have already been implemented with the remainder being worked on for the forthcoming year.

As Chief Executive, my role is to formally agree specific targets and success criteria with each Executive Team member at the start of each year, directly from the agency’s published business plan and I review progress against these objectives with them at face-to-face monthly meetings.

Remuneration Committee

The role of the Remuneration Committee is to make final recommendations to DfT and myself on all aspects of remuneration decisions for DVLA’s Executive Team (including the Chief Executive) in accordance with current pay guidance and with particular regard to equal opportunities.

It also considers the wider talent in the organisation and ensures visibility in respect of potential successors into agency senior civil service positions. It is chaired by the DVLA Chair and met on 2 occasions during the year.

Audit and Risk Committee

The DVLA Audit and Risk Committee has formally agreed terms of reference which is reviewed on an annual basis. The Committee provides advice and support to the Chief Executive in delivering the Accounting Officer role for the agency.

The Audit and Risk Committee is comprised of 3 Non-Executive Directors and 2 independent members who are senior civil servants in DfT and the Department for Work and Pensions. The 5 members are:

- Mike Brooks Audit and Risk Committee Chair (appointed 2009, resigned 2015)

- Jeremy Boss Audit and Risk Committee Chair (appointed 2016)

- Christopher Morson (appointed 2013)

- Emma West (appointed 2014)

- Paul Rodgers* accountancy and commercial (appointed 2012)

- Sarah Scullion* human resources (appointed 2013).

(* Senior civil servants with the DfT and the Department for Work and Pensions respectively)

I attend along with the Finance Director and Head of Internal Audit as observers, National Audit Office and KPMG as sub-contracted auditors to National Audit Office. Other Executive Team members attend as observers by rotation and when the Committee has asked to discuss matters for which they are accountable. Representatives of DfT Finance have a standing invitation to attend every meeting.

The Audit and Risk Committee has access to all internal audit reports, major project assurance reports, external reviews, risk registers and management reports. The agenda follows a cyclical pattern for external reporting but consider the following at each of their 4 meetings:

- progress against assurance plans; adequacy of response to the risk register and that correct risks have been identified

- management responses and action progress against assurance reviews

- response to fraud and bribery threats

- ICT security and any breaches reported.

The Audit and Risk Committee considers and approves the agency Management Assurance Statement, the Governance Statement and the Annual Report & Accounts.

Wider governance

The DfT Sponsor helps ensure sufficient priority is afforded to operational delivery, progress towards business plan performance measures and the management of risk through regular challenge meetings with myself and the Director of Finance.

The agency contributes monthly to DfT transparency reporting on progress towards financial targets and cash forecasting, expenditure and contracts in respect of our own activities. The DVLA reports, together with emerging escalated risks and issues, are aggregated with those of other agencies and considered at the DfT Executive Committee and Group Audit and Risk Committee as appropriate.

Managing our risks

The agency risk policy is updated on an annual basis to ensure the risk management framework and approach to risk appetite is appropriately defined and remains effective. The current agency risk policy is published on DVLA’s internal Intranet site and remains aligned to the overarching DfT policy.

Risks are identified and managed at several levels across the agency and captured on a standard reporting template. Current risks are reviewed by the Executive Team on a monthly basis along with a quarterly review by the DVLA Board and Audit and Risk Committee.

The Executive Team and agency Board consider potential new risks that the agency faces on an ongoing basis. A specific risk identification exercise was undertaken in January 2016 identifying risks to be included on the Corporate Risk Register.

The main risks to the agency at the 2015-16 year end included a number of inherent risks that the agency will always need to monitor. Such risks include ensuring robust business continuity plans being in place to address a range of potential disruptive scenarios; and the ongoing risks based around the move to more digital services ensuring these changes minimise the risk of fraud and any potential data breaches. The agency has in place specialist registers for the areas of business continuity, counter fraud, information assurance and health and safety ensuring these risks are continually monitored and actions are put in place to mitigate against such risks occurring. The agency has a continuous focus on data quality for all stakeholders and customers. Data Governance Board monitors and reviews all data and information risks across the agency.

Significant risks are escalated as appropriate to DfT in accordance with requirements set by the Department and HM Treasury.

The effectiveness of the agency’s risk management framework has been reviewed during the year:

- our internal audit service has performed an independent and objective review on the existence and effectiveness of controls over the agency’s risk management framework. The review confirmed that a sound framework was in place but that the agency could benefit from some further improvements to enhance the effectiveness of the framework of risk management within the IT Directorate to reflect the post out-sourced IT environment

- a risk maturity assessment has been conducted by independent assurance reviewers and aligned with the internal audit review which was conducted in parallel. Last year the assessment concluded the agency continues to make progress in the area of risk management with increasingly mature risk management practices. This maturity assessment supported the review performed by internal audit.

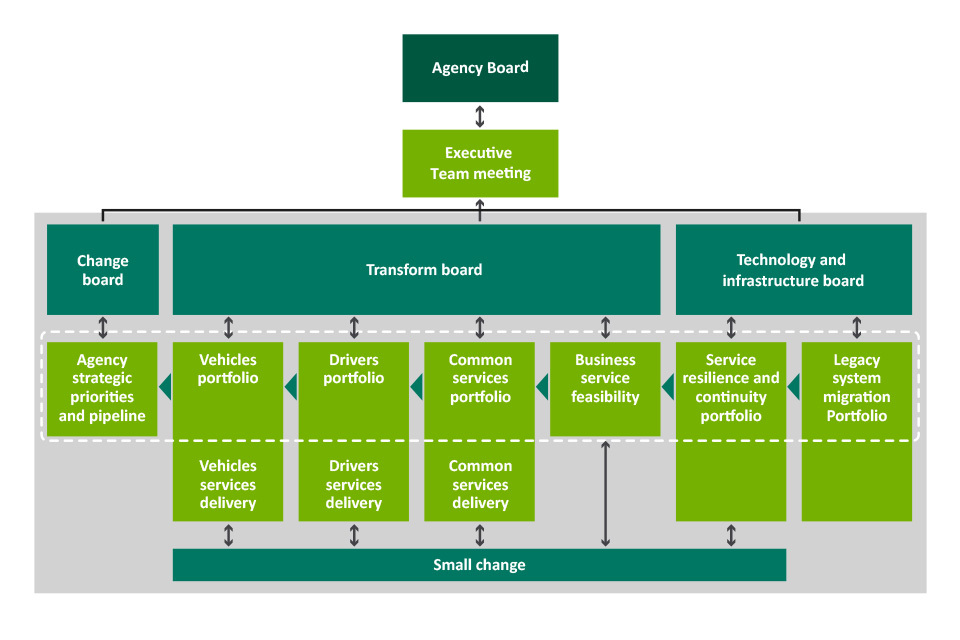

Managing the business – change and investment

The agency manages the introduction and prioritisation of change through the strategic pipeline. The key features of this process are:

- a rolling 24 month pipeline of change including contracts, business as usual and Business Development activities.

- a fortnightly Change Board consisting of the Executive Team and Finance, which acts as the first decision making forum in the pipeline process

- a fortnightly Business Impact Panel (BIP) consisting of representatives from across the agency. This panel assesses the potential impact on the agency and allocates funds of up to £50,000 to initiate discovery work to ensure there is a clearly identified need and that any proposal is value for money

- the agency business case process determines the appropriate governance route for each investment. A 3-stage business case process (following HM Treasury Green Book guidance) is undertaken for changes with a lifecycle cost greater than £1 million with smaller value investments requiring a Cost Benefits Analysis

- all business cases are subject to internal specialist review (by key individuals across the business) and approval at the appropriate board depending on value (i.e. Programme, ET, agency Board)

- change progress and portfolio finance update is reported to week 1 ET meeting. During the year a continuous assurance function has been set up to provide assurance on the delivery confidence of projects. This function provides assurance reporting to the ET and Audit and Risk Committee.

Governance Model - portfolio structure

Cabinet Office spending controls

In addition to the rules set out in Managing Public Money, Cabinet Office operates a set of additional spending controls. Nine areas of spend require specific Cabinet Office approval. They are:

- advertising, marketing and communication

- strategic supplier management

- digital technology

- consultancy

- property, including facilities management

- commercial models

- redundancy and compensation

- external recruitment

- learning and development (Civil Service Learning).

Relevant areas within the agency have been assigned specific responsibility for assuring the spending requests submitted to the Cabinet Office.

The agency has worked with DfT and Cabinet Office spend approval teams (for digital and technology spend) to develop a more effective spend control process. This has been based on an assessment of the agency’s ability to manage its digital and technology spend approval. Initial assessment by the Cabinet Office has been positive and discussions are ongoing on how this will work in practice. The agency’s change pipeline is key to this process by giving a clear forward view of plans.

Financial controls

Review of operational budgets and project affordability takes place at the monthly finance ET meeting with confirmation of affordability given by the Finance Director. Budgetary controls are supported by a robust and formal full monthly planning and re-forecasting cycle, monitoring volume and change demand. The results are reported monthly to the DVLA Board for action and forward decisions.

As the Accounting Officer, I hold a letter of Financial Delegation issued by the Permanent Secretary of the DfT. I sub-delegate financial delegations to Executive Directors and key finance staff.

Staff who have been allocated a delegation must ensure that they have completed the mandatory training programme and been assessed to ensure competence to fulfil the role.

The agency has developed and implemented a strategy and framework for the analytical assurance of both business case models and statistic reports. The framework details roles and responsibilities and ensures the agency enshrines the principles of the Macpherson Review in the day-to-day operation of its business and will ensure a robust body of documentation is available for audit. Analytical assurance statements are produced as standard reflecting best practice. Specialist review sign-off of business cases ensures analytical assurance is undertaken prior to investment decisions being made. A periodic review is undertaken assessing the organisation’s business models against DfT criteria to establish if the model in question is classified as ‘business critical’. At present we do not have any models classed as ‘business critical’.

Shared Services

DfT divested its Shared Service Centre (which provides back office services including HR, Payroll and Finance) to arvato on 1 June 2013 and established the government’s first Independent Shared Service Centre 1 (ISSC1). DVLA, as part of the DfT family, contracts with arvato through a call-off contract under a framework agreement managed by the Cabinet Office.

Since divestment, arvato has provided legacy SAP services to DVLA. Work continued to migrate the DfT family, including DVLA, to Tier 2 platform during 2015-16.

In November 2015, DfT and the Cabinet Office agreed that DfT would lead in agreeing a way forward for DfT in respect of their relationship with arvato. The Cabinet Office remained the framework authority for ISSC1 and the new ISSC1 governance arrangements were agreed by the Cabinet Office and DfT. This enabled DfT to fulfil certain responsibilities under the framework agreement during the commercial negotiation phase. As the framework authority, the Cabinet Office Accounting Officer remained responsible for providing DfT and DVLA, with assurance that ISSC1 was meeting its contractual obligations. The Cabinet Office Accounting Officer was supported in this role by a dedicated Shared Service Audit Committee.

The commercial negotiations with arvato have been concluded in principle. DfT has secured agreement with arvato on revisions to the DfT call-off contract that will ensure continuity of service and prove good value for money for the taxpayer.

In early 2016, the Comptroller and Auditor General approved plans for a National Audit Office report into the government’s Next Generation Shared Services programme, focusing primarily on progress on its 2 Independent Shared Service Centres. The NAO report was published on 20 May 2016 and was subject to a Public Accounts Committee hearing on 27 June 2016.

DfT has received an International Standards of Assurance Engagement (ISAE) 3402 report, produced by Ernst and Young on arvato’s operation of the control environment at ISSC1. DfT has also received a number of internal audit reports from the Cabinet Office on ISSC1 risk controls. DVLA has placed reliance on these reports for assurance over ISSC1’s control environment during the 2015-16 financial year.

Commercial controls

As a central government body, the agency’s commercial activity is governed by legislation within the Public Contracts regulations 2015. In the agency, governance and control of commercial activity is administered by the Commercial Directorate and overseen by the Commercial Director.

Commercial Directorate is responsible for ensuring that commercial practice at the agency is compliant with the Regulations. In line with the government’s Transparency Agenda, all tender opportunities are published, including Single Tender Actions and Contracts over £10,000.

Commercial Directorate has developed Commercial Procedures and a Commercial Policy which act as the 2 primary control documents governing commercial activity at the agency.

Contractual Authority emanates from me as Accounting Officer and is delegated to individuals in specific posts (primarily Commercial Director, Head of Procurement and senior commercial managers) and is not transferable. Only those with Contractual Authority are allowed to commit the agency to any commercial activity. Contractual Authority is distinct from Financial Authority and no individual is permitted to exercise both for the same requirement.

The agency has developed an efficient and effective practice whereby all contracts are sponsored at Executive Team level. This is supplemented by making day-to-day contract management the shared responsibility of a business owner and a professional Commercial Advisor from within Commercial Directorate, who are supported by a professional Financial Advisor.

As an additional tier of governance, all major agency procurements are subject to scrutiny by the DfT Procurement Approval Board prior to award of contract.

Data controls

There have been significant changes to the agency data control framework since the exit in September 2015 of the IT outsource contract Partners Achieving Change Together (PACT) and bringing the responsibility for many of our IT Services in-house. In addition provision of online services has grown significantly.

The existing governance arrangements have worked well during these transitions with the Senior Information Risk Owner (SIRO) who is also the Director of Strategy, Policy and Communications, being accountable for information risk. The SIRO is supported by the DVLA Chief Information Security Officer (CISO) who is accountable for security across the agency estate.

Data control and risk is co-ordinated through a Data Governance Board (DGB) chaired by the SIRO and attended by subject matter experts from across the organisation. The Chief Executive Officer also attends this Board.

We have had 21 incidents of personal data breaches; none of which have required escalation to the Information Commissioner. Whilst this is a slight increase on the previous year (18 breaches 2014-15), it is still low level in terms of the 168 million transactions processed annually by the agency.

The agency has delegated authority to accredit its IT system from DfT to our CISO, who is also the DVLA Accreditor. The approach has been revised and simplified in line with new government guidance; this approach is the responsibility of the DVLA Accreditor and has been agreed at the DGB. Our systems are now being assessed against this new framework.

There has been a programme of security events across the agency to maintain awareness and ensure the correct behaviours are adopted by staff to protect our information. Our Information Asset Owners (IAOs) who have responsibility for specific data sets attend regular briefings on current trends in security and risks.

Fraud, error and debt

The management of fraud, error and debt is a critical part of good governance. Losses and recoveries are reported to Cabinet Office. Overall responsibility for the agency’s management of this area sits with the Director of Strategy, Policy and Communications, supported by a cross-agency Steering Group.

Counter fraud initiatives and fraud investigations are taken forward by the Counter Fraud and Intelligence Team, often in liaison with DVLA’s operational Criminal Intelligence Officers. The GIAA provides support and input to fraud investigations, advising on aspects of control and risk management.

The Department launched the updated Whistleblowing Policy in May 2015. It makes clear how to raise a concern, the process to follow, and who to contact. DVLA collate and maintain a register which is used to populate a DfT centralised register.

Accounting Officer assurance

The system of internal control is designed to manage risk to a reasonable level, rather than to eliminate all risk. It should provide reasonable and not absolute assurance of effectiveness. The system of internal control supports the achievement of DVLA’s policies, aims and objectives, whilst safeguarding the funds and assets of the organisation, in accordance with HM Treasury’s Managing Public Money.

As Accounting Officer for DVLA, I have responsibility for reviewing the effectiveness of the systems of internal control. This is primarily informed by the agency’s Internal Audit reviews, along with the management assurance reporting of the managers within the agency who are responsible for the development and maintenance of the internal control framework.

Twice a year, a Management Assurance Statement review is undertaken to review all facets of management assurance, policy and practice. The 2015-16 Management Assurance Statement review asked agency senior managers to provide performance commentary and evidence on the application of 34 aspects of assurance. There were 28 areas of substantial assurance, 4 areas of assurance that were classed as moderate and 2 areas that had limited assurance level (which are access to system and IT technical resilience), where significant weaknesses were identified in the framework of governance. Responses were reviewed and agreed by subject matter experts, Internal Audit, ET, DfT and signed off by Audit and Risk Committee. The areas with limited assurance correspond with those highlighted within the Head of Internal Audit opinion and an action plan is being drafted to address these going forward.

Audit and Risk Committee

The DVLA Board and Audit and Risk Committee assist in developing and overseeing governance assurance processes and the plans to address any identified weaknesses. This ensures that continual improvement of the systems remains a priority.

These processes apply to all agency activities and transactions in the business account and trust statement. The Chair of the Audit and Risk Committee reports regularly to the agency Board on the Audit and Risk Committee’s views on the effectiveness of the agency’s governance, risk management and internal control arrangements.

Internal audit

The DVLA internal audit team transitioned into the GIAA as of 1 November 2015. This move increases the independence of the Internal Audit function and follows wider government priorities for Internal Audit Services within the Civil Service. Benefits include greater consistency and joined up working for the provision of Internal Audit services across government.

GIAA carries out the internal audit reviews for the DVLA. This team operates to prescribe Public Sector Internal Audit Standards and complies with procedures and standards set by the GIAA. The internal audit report provides me with an independent and objective opinion on the adequacy and effectiveness of the agency’s system of internal control, together with recommendations agreed to by management for improvement.

The Head of Internal Audit has unfettered access to the Chair of the Audit and Risk Committee and as Accounting Officer, I also work closely with the DfT Head of Internal Audit within GIAA. The audit plan for the year is informed by the main risks to the agency’s business and encompasses a broad range of internal controls. This includes assurance over the security and use of DVLA data, as well as contractual commitments and data protocols for those organisations that interact with DVLA.

Head of Internal Audit opinion

On the basis of the evidence obtained during 2015-16, the Head of Internal Audit was able to provide a moderate level of assurance that the DVLA’s framework of governance, risk management and control is appropriately defined and working effectively.

The Head of Internal Audit has advised that this opinion reflects the maturity of the agency’s Risk Management Framework; and the continued focus by the agency on further strengthening existing governance arrangements.