Digital Efficiency Report

Published 6 November 2012

© Crown copyright 2012

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/digital-efficiency-report/digital-efficiency-report

Executive summary

The size of the prize from bringing transactional services offered by central government online is considerable. On the basis of historic data looking at the savings already achieved by existing digital services over offline alternatives, this report estimates that between £1.7 billion and £1.8 billion could be realised as total annual savings to the government and service users. The savings made from greater digitisation of transactions, including their back-end processes, can be achieved whilst maintaining and ultimately improving service quality.

This report estimates that between £1.7 billion and £1.8 billion could be realised as total annual savings to the government and service users.

The Digital Efficiency Report is part of a process that began with the April 2012 Budget Statement (pdf, 707 KB). This committed the government to delivering online services that will go live only if the responsible minister can demonstrate that they themselves can use the service from 2014. In support of this, both cross-government and individual departmental digital strategies must be published by the end of 2012, setting out how new and redesigned services will meet this goal.

This report provides important supporting evidence for these documents, outlining the financial benefits of going digital to departments and the government as a whole. These figures, alongside other analyses, will ultimately help guide departmental strategies for 2013/14. The other benefits of going digital, including greater empowerment of the public and employability benefits, are more fully explained in the Government Digital Strategy.

Savings are likely to come from 4 key areas: the reduced staff time involved in processing digital transactions compared to offline alternatives; estates and accommodation; postage, packaging and materials; and the costs of supporting IT systems. They will not be made evenly across departments. Some departments are responsible for more services - and more individual transactions - than others. Some have digitised their services more comprehensively to date. Some of these savings may already have been accounted for in departments’ plans. And some services will require a greater investment of time, effort and money to fully realise the benefits of digitisation.

It is important to be clear that these figures do not account for the level of investment that may be needed to create or redesign digital services. The transitional costs of digitising services are not trivial. But the government’s new approach to procuring and embedding digital skills across departments, as set out in the Government Digital Strategy, should mean that the public sector will now be better able to take more control over the management of its online services.

Building world-class government digital services will take time. The savings potential from digital transactions will not be realised immediately, but digital has the potential to make a real impact during this Parliament. This report estimates that approximately £1.2 billion of savings could be created during the current spending review period.

This report estimates that approximately £1.2 billion of savings could be created during the current spending review period.

This report focuses on the savings potential of digital based on robust historic data. What it does not fully account for is the government’s new approach to digital. This could dramatically increase both the extent of savings, and the speed at which they can be realised. More digital skills across government, greater use of small and medium enterprise suppliers and the removal of the legislative blockers that impair digital service delivery will lead to even greater potential for digital transactions to save the public money and improve their user experience.

Moving to digital by default could save the government £1.7 billion to £1.8 billion every year.

Introduction

The way people connect with government is changing.

Twenty years ago, technology was very different. Communicating with public servants required filling in paper forms, arranging face-to-face meetings, or picking up a phone. Completing simple tasks often meant false starts, weeks of effort and wasted public money.

Today, digital services can harness the power and convenience of the web to make these interactions quicker, simpler and more secure. Millions of pounds have already been saved by bringing some public services online, with users also getting a better experience.

As the Government Digital Strategy explains, digitised transactional services present an unmissable opportunity for the UK. There is a strong body of evidence to support the idea that digital delivery of public services can produce a service at least as strong as that offered through other channels at a lower unit cost. For some government services, the average cost of a digital transaction is almost 20 times lower than the cost of a telephone transaction, about 30 times lower than the cost of postal transaction[footnote 1] and about 50 times lower than a face-to-face transaction. Digitisation is also likely to reduce the risk of failed transactions, and therefore the business cost of having to go through the same process multiple times.

Consumers have embraced online services in recent years, with almost two-thirds (pdf, 3.1 MB) (64%) of people saying they have used online banking services, and 86% of internet users having shopped online in 2011. As a consequence of this shift, some companies have achieved substantial cost savings. Government bodies are equally keen to digitise their public services and realise the potential efficiency gains. The City of Copenhagen estimates that digital transactions will cost less than 5% than the equivalent face-to-face interaction (pdf, 6.5 MB).

The future prize for government of going digital by default could be huge. From analysis of savings that can be robustly projected using historical data from existing digital services, it is estimated that a further £1.7 to £1.8 billion of total annual savings can be made by shifting the transactional services currently offered by central government departments from offline to digital channels.[footnote 2] Savings are likely to arise through reductions in staff, estates, materials and office equipment costs.

These figures are inclusive of any savings arising from digitisation that have already been included in departmental business plans. They also exclude any transitional or investment costs that may be required to release them. These costs are not insignificant. It will take time, effort and money to develop the flexibility and capability to do digital well across government. However, the figures do give a sense of scale to the huge efficiency potential that exists in digital services. This report explains how, when and where those savings could be made.

Conducting government services online is not just good for the public purse. It is also good for economic growth. Government estimates suggest that an hour spent interacting with government costs the average citizen £14.70.[footnote 3] Over 250 million transactions are still completed through offline channels every year. If half an hour were saved by digitising every transaction currently completed offline, the total savings to the economy could be up to £1.8 billion.[footnote 4]

The savings figures in this report are based on the best data available for savings already generated through digitising government services. As a result, they do not fully capture the effects the government’s new approach to digital. By embedding digital expertise across government, using a broader range of technology suppliers and redesigning policy frameworks, the government will have greater capacity to deliver world-class digital services that yield more efficiency savings, more quickly. After analysing savings estimates from future digital transformations, it appears likely that total annual savings from digitising transactional services could in fact be considerably higher. It should be noted that this report has not attempted to speculatively quantify these savings, and instead focuses on providing a robust estimate on the basis of existing historic data.

‘What does this report covers’ defines what is meant by ‘savings’ and ‘transactional services’, and clarifies the scope of this report.

‘The savings from digitising transactional services’ explains the methodology used to calculate the potential savings figures achievable through channel shift (moving from offline channels like post and phone to digital), and sets out the potential annual savings figures.

‘Where the savings will be found’ sets out which departments are expected to realise savings, where savings are likely to be made, and examples of the progress already made by public services towards digitisation.

Finally, ‘How long shifting to digital takes’ illustrates when potential savings could be realised, consolidates some of the lessons learned about the enabling factors needed to realise savings from digitisation of transactional services, and shows the potential in-year savings according to different speeds of digital take-up.

What this report covers

Defining transactional services

Transactional services cover a huge range of tasks, from paying car tax to applying for a passport, and they form a significant part of the government’s work. These services involve an exchange of money, goods, services, permissions, licences or information between the government and a service user, resulting in a change to a government system. This report focuses on what savings are achievable from conducting these services through digital channels rather than offline alternatives like phone, post or face-to-face conversations. Government departments and their agencies are directly responsible for managing over 650 transactional services.[footnote 5] The estimated total administration cost of managing these services in 2011/12 was approximately £6 billion to £9 billion.[footnote 6]

More than 300 transactional services have no digital channel available to their users.[footnote 7] Where transactional services currently possess a digital channel, many users still choose to carry out their transaction offline. Over 250 million transactions a year still take place through post, phone, face-to-face, or other offline channels.

Defining savings

This report has adopted the definition of cash-releasing savings as agreed by the Treasury and Cabinet Office.

The savings figures for digital channel shift based on historic data quoted in this report are:

- made specifically by the government, not the UK economy as a whole

- real cash savings from existing departmental and agency budgets, or where the service is managed by an agency run on a cost recovery accounting basis, cash savings passed on directly to service users. (Annex 2 sets out the split between cost recovery and public spending savings figures)

- achievable without substantial changes to existing legislation

- achievable without reducing the quality of service offered

The scope of this report

There are many sources of potential IT savings across the public sector. Shifting transactional service delivery to digital channels is the focus of this report because it has been identified as a definable source of potential savings to the government in the short- to medium-term. It is also the focus of the Government Digital Strategy. However, this does not mean that it represents the full range of savings that could be made from IT or digitisation.

Historical data has been used to calculate an estimated total annual savings figure for digitising transactional services. Because this figure is based on case studies, Departmental accounts and reasonable assumptions, as set out in Annex 4, it is reasonable to have confidence that the government can ultimately realise these through the digitisation of transactional services.

There is evidence to suggest that the savings achievable through shifting to digital channels could be multiplied when accompanied by a comprehensive transformation of the service’s business processes and back-end technical systems.

As the Government Digital Strategy explains, the government is putting in place the digital skills, support and standards needed to make these transformations both faster and more effective in driving both efficiency savings and take-up of online channels. To understand the savings potential of future digital transformations, business cases from a number of services about to embark on major transformations have been studied to compare their anticipated future savings with actual savings realised through past transformations. On this basis, it appears likely that the upper bound of potential savings from digitising transactions could be considerably higher.

Exploiting this additional potential will mean making difficult choices. Radical service transformation often requires extensive investment of time and resources, changes to primary legislation, and substantial re-engineering or replacement of the processes and technical systems that support a transaction. However, the rewards to both the government and the service users have the potential to be substantial.

In addition, there are areas of significant savings that have been treated as broadly out of scope for this report. The government is exploring ways of realising savings in each of these categories, and there is further explanation on some of these plans in the Government Digital Strategy.

Digitising the wider public sector

Central government’s transactional services cover a significant portion of public activity, but there are considerable areas of spending that do not fall within this definition. Services devolved from direct departmental control, such those run by local councils, the NHS and the police, are not counted in the savings figures quoted in this report.

Digitisation could substantially reduce costs across the public sector. Recently published estimates suggest between £134 million and £421 million could be saved annually through greater digitisation of local government transactions, while Department of Health analysis estimates annual savings in the region of £2.9 billion from digital deployment in the NHS.

Consolidating online publishing

In 2011, the government committed to consolidating all information publishing under a single government domain - the recently launched GOV.UK.

The replacement of Directgov and Businesslink - the previous homes of online publishing - is expected to yield annual savings of at least £36 million. To this should be added the cost of bringing departmental websites onto the GOV.UK domain which, over time, is expected to realise annual savings from departmental costs of between £25 million and £45 million for every year over the current spending review period to 2014 to 2015.[footnote 8]

Rationalising the government IT estate

The government runs a vast network of information technology systems. In 2011 to 2012, government procured over £6 billion of IT systems. This figure includes a huge range of equipment, from IT hardware used by public servants to large-scale data storage facilities. Rationalising this estate could potentially yield substantial savings that will be examined in the Government ICT Strategy, but one where the reality of doing so will be subject to multiple contractual arrangements. It is also likely to present a considerable logistical challenge, and will need to account for the lessons learned from previous government IT projects.

Digitising ‘back office’ and intra-governmental transactional services

The focus of this analysis is restricted to public-facing transactional services. As such, it rules out any transactions that take place between government bodies (such as exchanges of information within the criminal justice system) and those which relate to ‘back office’ functions (such as government accounting or recruitment).

Many of these processes are currently paper-based and run on a large scale, raising the possibility of future digital efficiency savings.

Savings from digitising transactional services

With transactional activity taking place across a range of diverse services, working out how much can be saved by conducting them digitally is not a simple task. To ensure that the findings of this analysis were robust, two separate methodologies for calculation were used to corroborate the findings: a bottom-up case study analysis, and a top-down analysis using aggregated government accounts.

Case study analysis

It is impractical to assess the savings potential of over 650 individual transactional services, so using a representative sample to provide an assessment for the full picture is essential. Every service was categorised using 4 significant factors of savings potential:

- volume of individual transactions per year

- service function (eg requesting a benefit or grant)

- customer type

- current level of digital take-up

17 case study services from across government were selected on the basis of covering a spread across the 4 factors, and used to provide data about the impact of each. They show that services will not be equal in the extent to which they can achieve savings.

Volume

Figure 1: Annual savings (£ millions) per 1% shift to digital - by volume

| Under 1 million | 0.06 |

| 1-8 million | 0.15 |

| Over 8 million | 0.32 |

Our analysis suggests that transaction volume is a good linear indicator of a service’s savings potential. Higher volume services appear to benefit from economies of scale that allow them to realise greater savings from each incremental improvement in digital take-up. Below a threshold of 1 million transactions each year, any economies of scale are smaller in terms of directly driving additional savings potential. However, they remain statistically significant, not least because of the sheer number of services with fewer than 1 million annual transactions provided by the government.

Function

Figure 2: Annual savings (£ millions) per 1% shift to digital - by function

| Function | Savings (£ millions) |

| Ordering goods | 0.39 |

| Providing information | 0.18 |

| Making a payment (taxes and fines) | 0.13 |

| Requesting benefits/grants/loans | 0.10 |

| Requesting a licence/authorisation | 0.07 |

| Booking an appointment | 0.06 |

Transactional services can be categorised into 6 broad function types. Function serves as a proxy for the complexity of a transactional service, as it implies certain things about its requirements including security, number of process steps, and links to other data stores. The analysis showed that more complex transactions, and particularly those that included a financial transfer, appeared to have greater potential for savings through channel shift than more straightforward registration or authorisation services.

It should be noted that more complex transactions may also be the most difficult to migrate to digital channels, and may require commensurately higher levels of investment. However, it is possible to take an incremental approach - even in services where full digitisation is not possible - and still make savings.

Customer type

Figure 3: Annual savings (£ millions) per 1% shift to digital - by customer type

| Customer type | Savings |

| Government to business | 0.18 |

| Government to consumer (challenged) | 0.15 |

| Government to consumer (mainstream) | 0.14 |

Government transactions cover a wide customer base. To simplify this, each of the 650-plus transactional services was categorised using 1 of 3 typical customer types; business users, mainstream consumer users, and less able consumer users. The analysis showed that type of customer was not a strong indicator of savings potential, though the potential savings from business-facing transactional services was slightly higher than those for consumer-facing services.

This report assumes a base case in which services shift to digital by default, defined as 82% take-up. This figure was chosen on the basis of the GDS ‘Digital Landscape Research’, which found that 82% of the UK adult population is online and able to use straightforward and convenient digital services. We acknowledge, however, that some services have a higher proportion of users who are less likely to be online (for example, older people, people with disabilities, people in lower socioeconomic groups), and therefore might find it more difficult to reach this level of take-up. We recognise that 82% take up is a challenging target for those services which predominantly serve audiences that are less likely than the general population to be online. In terms of how digital by default is defined, this figure will need to be revisited in the future as more evidence is gathered and people’s online behaviour evolves.

Current digital take-up

Figure 4: Annual savings (£ millions) per 1% shift to digital - by current digital take-up

| Current digital take-up | Savings (£ millions) |

| 0 - 20 | 0.13 |

| 20 - 40 | 0.13 |

| 40 - 60 | 0.25 |

| 60 - 80 | 0.22 |

| 80 - 100 | 0.15 |

Many government transactional services have already begun the process of digitisation. However, there is a wide range in the level of take-up across services that already possess a digital channel. This analysis shows that savings can be realised at all stages of channel shift. The expected amount of savings increases as the level of take-up goes beyond 40%, before slowing steadily as services approach full digitisation. A fuller explanation of the bottom-up methodology is set out in Annex 4.

Top-down analysis

The top-down approach is based on estimates of the transaction related expenditure associated with each department. These estimates used data taken from published departmental and agency accounts. For transaction focused agencies (eg Land Registry), all costs from the total agency expenditure unrelated to transactional activity (eg grants, non-cash costs) were deducted, based on data from the annual reports, before being aggregated at departmental level.

For departments or agencies whose main purpose is not transactional (eg Foreign and Commonwealth Office (FCO)), the major transaction-related cost categories were identified using departmental and agency annual reports, and included categories such as staff and other costs of service delivery (eg telephone, printing and postage, and rents). Cost categories clearly unrelated to transactions, such as capital outlay on infrastructure or expenditure on non-transactional services like the police, were excluded.

For each department, the number of digital transactions by channel was estimated using data available in some transactional services. For services known to be digital but lacking data on the percentage of digital take-up, an average figure was used based on take-up in services for which the data was available.

Unit cost ratios by channel and by department, based on data from the case studies and external benchmarks (eg local government)[footnote 9], were applied to the transaction-related costs by department. Cost ratios were tailored to the type of services provided by each department where it was believed that the benchmarks did not appropriately represent cost savings potential (for example, the switch to digital would have a limited impact on costs for process-heavy services such as passport applications). This analysis was carried out for the 13 departments responsible for the largest volume of transactions. They covered more than 99% of transactions across central government. A fuller explanation of the top-down methodology is in Annex 5.

Estimates of total annual savings

In this report, all quoted savings figures assume a base case defined as all services processing over 10,000 transactions each year shift to 82% digital take-up.[footnote 10] The bottom-up methodology yields an annual saving estimate from this shift to digital by default as £1.8 billion. The equivalent top-down figure is £1.7 billion.

Figure 5: Projected total annual savings, split by public spending / cost recovery receipt of savings

| Projected Total Annual Savings | Fiscal | Cost Recovery | Total |

|---|---|---|---|

| Bottom-up | 1.162bn | 0.612bn | 1.78bn |

| Top-down | 1.1bn | 0.623bn | 1.72bn |

As mentioned previously, our analysis estimated that the total transaction-related spend across government as being £6 billion to £9 billion. In the historical case study data examined for this report, a channel shift towards digital by default therefore reduces the total transactional costs across government by around a fifth.

When this result is examined against the evidence for the relative cost of digital channels compared to offline alternatives, it implies that the full benefits of digitisation have not necessarily been realised in the past. This could be attributed to a number of factors, including technological improvements in recent years, legislative obstacles, and a relative lack of digital skills across government. In business cases for redesigned transactional services just beginning the process of radical business transformation alongside digitisation (or new digital services being created to replace existing transactions, such as Universal Credit), costs are expected to fall by an even greater proportion. However, given the relative lack of supporting data, this report has not attempted to quantify these savings.

Where the savings will be found

The story so far

Some services have already made substantial savings from digitisation. Based on the historic case study data examined for this report, it is anticipated that digital savings will primarily be made in the following areas:

- total employment costs of those providing the service, including training

- estate and accommodation

- postage, printing and telecommunications

- office equipment, including technology systems

The chart below shows a breakdown of the sources of savings based on a “time and materials” model of savings.[footnote 11]

Figure 6: Sources of savings, by estimated % of total saving

| Percentage | Category |

|---|---|

| 78% | Staff costs |

| 12% | Accommodation |

| 7% | Printing and postage |

| 4% | IT and equipment |

The evidence from specific case studies supports these findings. The Driving Standards Agency started offering an online channel for booking practical driving tests in 2003. More than three-quarters of almost 2 million transactions are now digital, with only 23% of people still booking via phone. As people have migrated to digital, costs have fallen. The principal sources of savings have been reductions in employee numbers and accommodation costs. One of 2 dedicated contact centres closed in 2008, while the total number of employees working on the transaction has fallen from 400 in 2003 to 75 in 2012. Stationery and postage costs have also been removed from the digital channel.

Last year, digital take-up across all 4 main business taxes (Self Assessment, PAYE, Corporation Tax and VAT) was over 80%, equivalent to tens of millions of transactions.

HMRC first offered online tax return filing in 2000, with the pace of take-up accelerating following the Carter Review in 2006. Last year, digital take-up across all 4 main business taxes (Self Assessment, PAYE, Corporation Tax and VAT) was over 80%, equivalent to tens of millions of transactions. Dramatically reduced volumes of paper applications has meant fewer people are required to process them (resulting in a full-time equivalent (FTE) reduction of over 2,700 over the last 5 years), a corresponding reduction in the need for their accommodation, less space to store the paper forms (cumulative savings of almost £5 million), less stationery (cumulative savings of £34 million) and a smaller spend on postage.

Responsibility for transactional services is not split evenly across government departments and their agencies. Some departments are responsible for many different services, but the majority of those have relatively low annual volumes of activity. Others are responsible for fewer services, but some of them involve millions of individual transactions every year.

Different departments will face different challenges. Those responsible for managing a small number of bigger services (such as Department for Work and Pensions (DWP)) are likely to have to manage significant risks in the process of transforming them, as failure to deliver a smooth transition will have major impact on users. Other departments (such as Department for Business, Innovation and Skills (BIS)), responsible for a large number of transactional services, face the challenges of making investment cases for lower volume services where savings per service will be relatively small, as well as managing multiple simultaneous transformation projects across many different agencies and arm’s length bodies. In addition, in some situations it may be that the overhead costs of, for example, a network of local offices, are not reduced by shifting transactions online, and so digitisation may not on its own release significant savings from estates in all cases.

The graphs overleaf display the difference between a split of services and transaction volumes by department. Both of these graphs indicate that there are some departments that are unlikely to find many savings through channel shift, simply because they are responsible for very few services or individual transactions.

Figure 7: Number of transactional services by department

| Number of transactional services by department | Digital Not Available | Digital Available | Total |

|---|---|---|---|

| BIS | 142 | 97 | 239 |

| Defra | 57 | 37 | 94 |

| Home Office | 31 | 14 | 45 |

| DfT | 24 | 31 | 55 |

| DECC | 22 | 31 | 53 |

| DWP | 15 | 6 | 21 |

| HMRC | 11 | 28 | 39 |

| MOJ | 6 | 6 | 12 |

| DCMS | 6 | 43 | 49 |

| AGO | 3 | 2 | 5 |

| DfE | 2 | 23 | 25 |

| FCO | 1 | 4 | 5 |

| DFID | 1 | 4 | 4 |

| DCLG | 1 | 1 | 2 |

| MOD | 0 | 3 | 3 |

Figure 8: Volume of completed transactions by department[footnote 12]

| Number of transactional services by department | Non Digital | Digital | Total |

|---|---|---|---|

| HMRC | 93 | 547 | 640 |

| DWP | 53 | 2 | 55 |

| DfT | 49 | 42 | 91 |

| BIS | 16 | 36 | 52 |

| HO | 11 | 5 | 16 |

| Defra | 13 | 10 | 23 |

| MOJ | 10 | 2 | 12 |

| DCMS | 5 | 9 | 14 |

| DECC | 1 | 1 | 2 |

| DfE | 1 | 2 | 3 |

| AGO | 0 | 0 | 0 |

| DCLG | 0 | 1 | 1 |

| DFID | 0 | 0 | 0 |

| FCO | 0 | 0 | 0 |

| MOD | 0 | 0 | 0 |

The future potential

The future additional savings potential for specific departments is dependent on 4 things:

- the number of transactional services the Department is responsible for

- how those services are classified against the 4 factors of savings potential (as set out in Section 2

- the size of transitional costs involved in releasing savings

- the extent to which digital savings have already been accounted for in business plans

The estimates below show an approximated range for the total potential annual savings by department, assuming a shift to the base case for digitisation set out above. They are based on the top-down methodology explained earlier, using estimates of total transactional service spend, channel mix and cost per transaction to calculate the potential savings from a shift to digital services. Although these savings estimates have been calculated on the basis of aggregated digital take-up by department, the purpose of the calculation is to understand the potential savings from making each individual service digital by default.

These figures are inclusive of any savings arising from digitisation already included in departmental business plans, and exclude transitional or investment costs required to release them. As a result, the upper bound of the range is likely to represent an exaggeration of the full savings potential. The estimates of transactional costs are based on an assessment of the total spending from departments on their services, both in the customer-facing part of the service and the back-end processes needed to support it. This means that the estimated savings are a combination of savings made from greater digitisation of the entire transaction, including the back-end processes.

Figure 9: Range of projected total annual savings (£ millions) by department[footnote 13]

| Department | Projected savings (upper) | Projected savings (lower) |

| DWP | 430 | 260 |

| BIS | 350 | 230 |

| HMRC | 270 | 240 |

| Home Office | 240 | 180 |

| Defra | 230 | 160 |

| DFT | 190 | 80 |

| DFE | 130 | 35 |

| DCMS | 75 | 30 |

| MOJ | 50 | 30 |

| DECC | 35 | 15 |

| FCO | 3 | 2 |

| AGO | 2 | 1 |

| DCLG | 0 | 0 |

| DFID | 0 | 0 |

| MOD | 0 | 0 |

This report does not set out specific details about how and where departments may realise savings and efficiencies, as this would require detailed investigation beyond the scope of the analysis. The actual savings potential will be as set out in departmental digital strategies published at the end of 2012. Individual projects for the digitisation or redesign of services will of course need to develop fully costed business cases and be managed according to the principles set out in ‘Managing Public Money’. We recognise that by using historic 11/12 financial data to develop our savings estimates they may not fully reflect future policy changes, such as the effects of Universal Credit. These changes are likely to impact on the savings potential of specific departments. A fuller explanation of how expected savings were calculated for each department is set out in Annex 5.

Realising savings through digitisation is unlikely to happen without some level of transition costs. Building or redesigning transactional services is not a trivial activity, and likely to require investment. departments are already looking for ways to maintain service quality whilst reducing their expenditure, and are operating under severely constrained budgets. However, the case studies provide examples of services where the business benefits of digital have already outweighed the upfront costs. Looking forward, the investment case for digital is likely to be strengthened as government adopts a more agile approach to digital development and sources technology from a broader range of smaller suppliers, thereby reducing the levels of required expenditure.

The Civil Service Reform Plan indicated that the number of civil servants would fall from 2010 levels by around 23% to 380,000 by 2015 as the way that government delivers its services changes. Furthermore, the Public Accounts Committee (pdf, 253 KB) has advised that the savings already achieved in staff costs across the Civil Service “will not be sustainable unless departments now complete long-term operating models for their businesses”. Digital services will form a core element of future government service models and are likely to thereby contribute to such headcount reductions.

The historical data reveals that a significant proportion of the savings realisable through digitisation are achieved through a reduction in staff costs. It is worth noting that these can often be difficult to realise in practice. But crucially, the evidence suggests that digitisation could enable the government to reduce these costs while maintaining the quality of service that is provided to users.

If the proportion of savings estimated to relate to staff costs (from Fig. 6) is applied to the total estimated annual savings and then divided by an average cost per FTE, this amounts to a total FTE savings estimate of at least 40,000.[footnote 14] This represents the number of FTEs that could be saved if a shift towards digital transactions right across government were achieved.[footnote 15] For the avoidance of doubt, this estimate is inclusive of any staff savings already presented in departmental business plans and those departments which have developed digital services have generally made assumptions about the impact of digital services on their future workforce requirements, so that these are managed over time.

How long shifting to digital takes

The figures quoted thus far in this report represent potential total annual savings - the difference between the total annual cost of running a transactional service at its current level of digitisation and the total annual cost of running the same service after a shift to digital by default.[footnote 16]

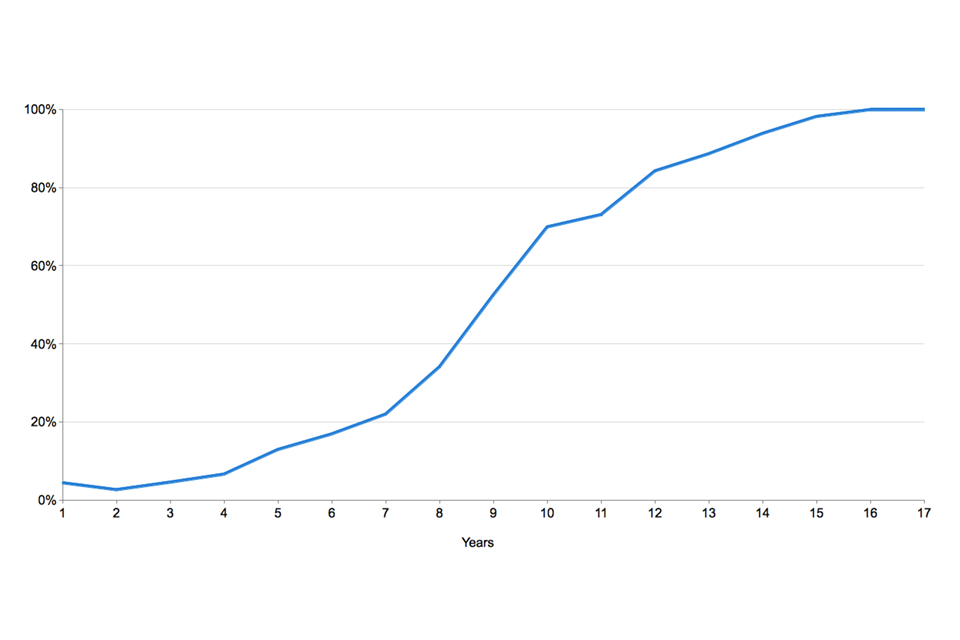

To understand the trajectory for realising the benefits from digitisation, it is helpful to look at the historical take-up of digitised transactional services. The data showing take-up rates for the 17 case studies has been consolidated to create a generic path for the digitisation of transactional services.[footnote 17]

Figure 10: Digital take-up curve, averaged across case study data

Fig. 10: Graph showing digital take-up curve, averaged across case study data

Evidence from the case studies demonstrates public services exhibiting a typical technology adoption S-curve. For services at around 20% digital take-up, the rate of adoption tends increases as they become increasingly accepted by the mainstream, often reaching 80% take-up within 3 to 5 years. The pace of change could be further increased where digitisation is driven by a process of fundamental service redesign focused on meeting user needs.

Based on this historic S-curve, total in-year savings are expected to rise to approximately £0.6 billion in 2014 to 2015 and £1.0 billion in 2016 to 2017. The total savings made over the remainder of the current spending review period are approximately £1.2 billion.

Figure 11: Estimated cumulative savings (£ billions) by year, based on historic S-curve

| Year | Cumulative savings (£ billions) |

| 2012/13 | 0.16 |

| 2013/14 | 0.48 |

| 2014/15 | 0.60 |

| 2015/16 | 0.89 |

| 2016/17 | 1.04 |

The time frame of this S-curve starkly contrasts with what is delivered by today’s high-performing transactional services. It is reasonable to believe that the historic S-curve is not reflective of the pace of digitisation possible today.

Making savings through digital can be a challenging process. The services studied for this report overcame potential blockers in their progress towards digitisation. As well as overcoming these blockages, these services have used tools and techniques to improve the success of channel shift, and increase the speed of digitisation.

Rewarding digital users

Using differential prices (eg for ordering official copies of Land Registry documents), submission deadlines (eg HM Revenue and Customs (HMRC) self-assessment return) or levels of assistance (eg Companies House pre-populating digital forms), between digital and offline channels have effectively encouraged customers to move away from using less cost-effective channels. This has proved an effective tactic not only for generating savings, but also for the powerful message it sends to users.

Raising customer awareness

Some organisations, such as Companies House, have successfully driven up digital take-up through campaigns based on customer insight gained from primary research. Digital take-up was accelerated through emphasising the benefits of digital; improved security; faster confirmation of success; quicker payment mechanisms; and access to immediate online help.

Effective internal engagement

Like all major organisational changes, shifting to digital needs to be handled sensitively. When transforming their services, departments and agencies have found early engagement with unions and staff important and effective. In anticipation of any headcount reductions, effective communication, recruitment freezes and cross-organisation planning have avoided the need for compulsory redundancies, minimising the disruptive effects on staff and productivity.

Overcoming legislative barriers

Some organisations’ experience of introducing digital services or trying to drive higher take-up by withdrawing offline channels has involved lengthy consultation and approval processes. To make substantial savings from digital, the time and amount of bureaucracy involved in gaining the relevant approvals needs to be minimised wherever possible.

Managing security risks

Digital services bring unique challenges in making sure users’ personal information and identity is protected. Identity assurance will create a simple, trusted and secure environment for users to access digital public services. The identity assurance approach is based on standards and is technology neutral, reducing the complexity and cost for government, while creating new opportunities for reducing fraud through collaboration between the public and private sectors.

Working with partner organisations

Digital services are often more dependent on partner organisations than offline channel equivalents. To deal with this, services have built a level of tolerance into their processes to avoid the failure of one component breaking the entire transaction. For example, the Driving Standards Agency can continue to serve customers booking a practical driving test online even if links to the databases confirming the applicant’s provisional licence and the theory test status are unavailable, by holding applications in stasis until links are restored. Similarly, Companies House and HMRC have engaged with software providers to enable the integration of their service within the programmes, processes and systems business customers use to file returns.

Increased digital capability

By employing staff with specific responsibility for service provision and quality who have a high level of digital skills, government organisations are in a stronger position to monitor and iteratively improve the performance of their transactional services. The Government Digital Strategy sets out the steps for increasing the level of these skills across government in order to build world-class transactional services that encourage faster user take-up.

Looking forward, it is reasonable to assume that these lessons learn d, in combination with the new approach to digital set out in the Government Digital Strategy, would result in a compressed S-curve, representing a faster pace of more comprehensive digitisation that goes beyond a 82% digital uptake rate. This would be expected to yield higher savings more quickly. The in-year savings shown below are consistent with a digital take-up curve twice as fast as one based on historic data. This has been chosen to illustrate the effect of faster digitisation on potential in-year savings, rather than in expectation that this specific rate of take-up will be achieved.

Figure 12: Estimated cumulative savings (£ billions) by year, based on compressed S-curve

| Year | Cumulative savings (£ billions) |

| 2012/13 | 0.49 |

| 2013/14 | 0.92 |

| 2014/15 | 1.35 |

| 2015/16 | 1.96 |

| 2016/17 | 2.17 |

Annex 1: List of case studies

| Department - Agency | Service | Volume | % digital | Customer | Function |

|---|---|---|---|---|---|

| BIS - ACAS | Booking a training course | 8,000 | 40% | Businesses | Booking an appointment |

| BIS - Companies House | Filing accounts | 2,060,000 | 41% | Businesses | Providing information |

| BIS - Companies House | Annual Returns filing | 2,263,000 | 97% | Businesses | Providing information |

| BIS - Intellectual Property Office | Patent Renewal | 381,000 | 86% | Businesses | Making a payment |

| BIS - Land Registry | Ordering official copies | 9,321,000 | 95% | Businesses | Ordering goods |

| DfE | Free School Meal applications | 858,000 | 40% | Challenged consumers | Requesting benefits /grants / loans |

| DfT - Driving Standards Agency | Practical Driving Test booking | 1,942,000 | 77% | Mainstream consumers | Booking an appointment |

| DfT - DVLA | Vehicle excise duty | 43,630,000 | 47% | Mainstream consumers | Making a payment |

| DfT - DVLA | First application for driving licence | 954,000 | 28% | Mainstream consumers | Requesting authorisation |

| DfT - DVLA | Driving Licence: Photo Renewal | 2,406,000 | 17% | Mainstream consumers | Requesting authorisation |

| DWP | Job Seekers’ Allowance new claims | 3,415,000 | 39% | Challenged consumers | Requesting benefits / grants / loans |

| HMRC | Corporation Tax | 1,658,000 | 96% | Businesses | Making a payment |

| HMRC | PAYE (end of year returns) | 8,948,000 | 100% | Businesses | Making a payment |

| HMRC | Self-Assessment (end of year returns) | 9,845,000 | 80% | Businesses | Providing information |

| HMRC | VAT | 7,753,000 | 81% | Businesses | Making a payment |

| MoJ - National Offender Management Service | HMPS Visit Booking service | 1,550,000 | 15% | Challenged consumers | Booking an appointment |

| Defra - Rural Payments Agency | Single Payments Scheme | 43,000 | 41% | Businesses | Requesting benefits /grants / loans |

Annex 2: Recipients of savings

Some of the government’s transactional services are paid for directly through departmental budgets, whilst others are paid for by customers of those services.

This means that some of the savings from digitising transactional services will benefit the government and some will directly benefit consumers (since the savings would be passed on to them in lower prices for the service). In this report savings to government are described as “cash-releasing”, fiscal savings and savings to customers are described as cost recovery savings.

The split between the two types of savings is shown in Fig. 5.

Annex 3: Sensitivity analysis

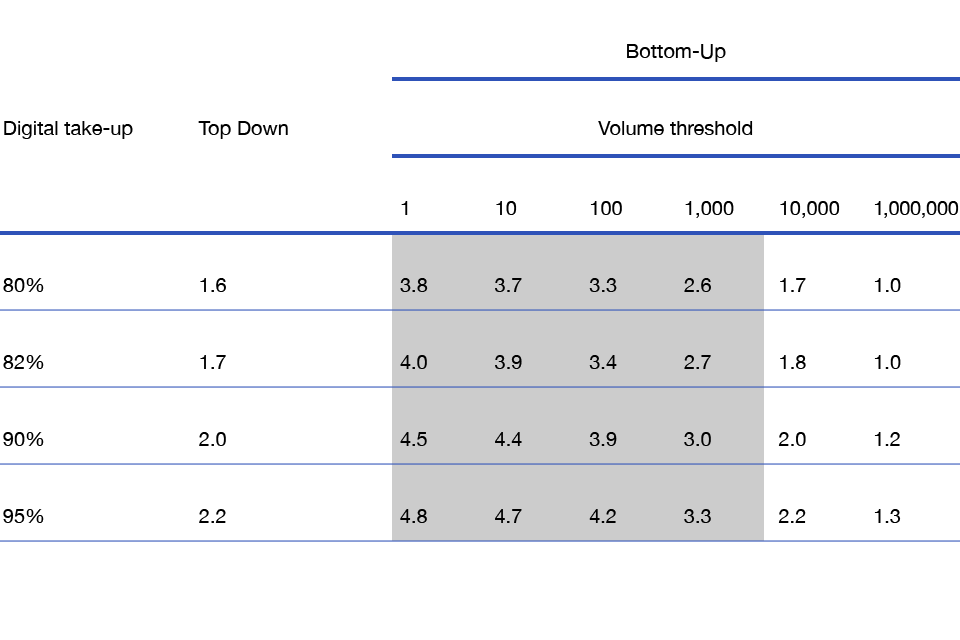

Throughout this report, base case assumptions have been made about the level of digital take-up defined as digital by default and about the size of transactional service below which savings are assumed not to be generated. The figures highlighted below in bold relate to the base case estimates quoted thus far in the report, for a digital by default take-up rate of 82% digital, and a volume threshold of 10,000 transactions each year.

The figures that have been greyed out in the grid below are considered less reliable estimates for potential savings. This is because all quoted savings figures are gross of any investment required to realise them. For lower volume services, such as applying for a permit for burial at sea, the level of investment needed for successful digitisation is likely to exceed the savings returned as a result until transaction platforms are developed. Common technology platforms that fit a standard transaction type will reduce the need for building new digital services from scratch, and may ultimately make digitising smaller transactional services economically viable. However, savings from these much smaller services are unlikely to be realisable during the current spending review period (up to 2014/15).

Figure 13: Estimated total annual savings (£ billion), based on different levels of digital take-up and size of services digitised.

Figure 13: Table showing estimated total annual savings (£ billion), based on different levels of digital take-up and size of services digitised

Annex 4: Bottom-up methodology

Understanding the savings indicators

The analysis started with hypotheses about the aspects of transactional services that may be linked to the potential for savings. It was hypothesised that four variables may play this role. In this report, these variables are referred to as indicators of savings potential.

- volume

- level of digital take-up

- function

- customer type

This hypothesis was tested using data from the 17 case studies. The relative impact of each of these is explained in section 2 of the main report.

Alongside this analysis, a database was compiled of all the transactional services across central government within the scope of the report. Every transactional service was categorised using the 4 indicators of savings potential, using real data for digital take-up where available, and an average take-up figure when it was not.[footnote 18] This allows the total savings for each percentage point shift towards digital by default[footnote 19] across government to be calculated.

Any transactions which have a volume of less than 10,000 are excluded from the calculation. This is based on the fact that for services below this size, the investment and transition costs are likely to be significant in relation to savings.

Confidence intervals

To test how statistically significant the indicators of savings potential are, 95% confidence intervals on each indicator were calculated. This produced relatively large ranges for the potential savings generated per percentage shift to digital, probably because the standard deviation of the savings is large from transaction to transaction and the sample sizes to determine the savings associated with each indicator are relatively small.

Nevertheless, the confidence intervals support the hypothesis that volume is strongly linked to savings potential: a transaction with a volume of over 8 million will offer greater savings than one with fewer.

Figure 14: 95% confidence intervals on potential annual savings per 1% shift to digital - by volume

| Number of transactional services by department | Low | Medium | High |

|---|---|---|---|

| Under 1 million | -£0.04m | £0.06m | £0.17m |

| 1 - 8 million | £0.11m | £0.15m | £0.19m |

| Over 8 million | £0.21m | £0.29m | £0.37m |

Function also has a significant impact. However, we cannot prove to 95% confidence, on the basis of their function alone, that some of the simpler transactions will offer the potential for any savings.

Figure 15: 95% confidence intervals on potential annual savings per 1% shift to digital - by function

| 95% confidence intervals on potential annual savings per 1% shift to digital - by function |

Low | Medium | High |

|---|---|---|---|

| Ordering Goods | £0.31m | £0.39m | £0.48m |

| Providing Information | £0.10m | £0.18m | £0.26m |

| Making a payment (taxes and fines) | £0.05m | £0.11m | £0.18m |

| Requesting benefits/grants/loans | £0.00m | £0.10m | £0.21m |

| Requesting a license/authorisation | £0.05m | £0.07m | £0.19m |

| Booking an appointment | -£0.02m | £0.06m | £0.13m |

The analysis of digital penetration shows some variation in savings at different levels, but it is not possible to say with 95% confidence that the savings vary by level. This allows the methodology to use the assumption that the savings potential for each percentage take-up of digital could be broadly constant.

Figure 16: 95% confidence intervals on potential annual savings per 1% shift to digital - by digital take-up

| Digital take up - confidence | Low | Medium | High |

|---|---|---|---|

| 0 - 20% | 0.07 | 0.13 | 0.20 |

| 20 - 40% | 0.05 | 0.12 | 0.20 |

| 40 - 60% | 0.13 | 0.23 | 0.33 |

| 60 - 80% | 0.14 | 0.22 | 0.31 |

| 80 - 100% | 0.07 | 0.15 | 0.22 |

The same goes for customer type; there is some variation but the confidence intervals are large.

Figure 17: 95% confidence intervals on potential annual savings per 1% shift to digital - by customer type

| Customer type - confidence | Low | Medium | High |

|---|---|---|---|

| business | 0.13 | 0.18 | 0.22 |

| mainstream consumer | 0.06 | 0.12 | 0.19 |

| challenged consumer | 0.03 | 0.15 | 0.28 |

In contrast to the confidence intervals on the individual indicators of savings potential, the confidence on the total estimate is tighter. This means that it has been established, with a probability of 95%, that the savings potential lies in the range £1.4 billion to £2.2 billion, with £1.8 billion the expected figure.

The reason for this is that the total estimate is calculated from a larger sample size – all of the years for all of the case studies – whereas the savings for the individual attributes are calculated from a subset of data points.

Figure 18: 95% confidence intervals on total annual savings estimates (£ billions)

| Confidence | Estimated annual savings (£ billions) |

|---|---|

| Low confidence interval | 1.4 |

| Mid case | 1.8 |

| High confidence interval | 2.2 |

In-year savings

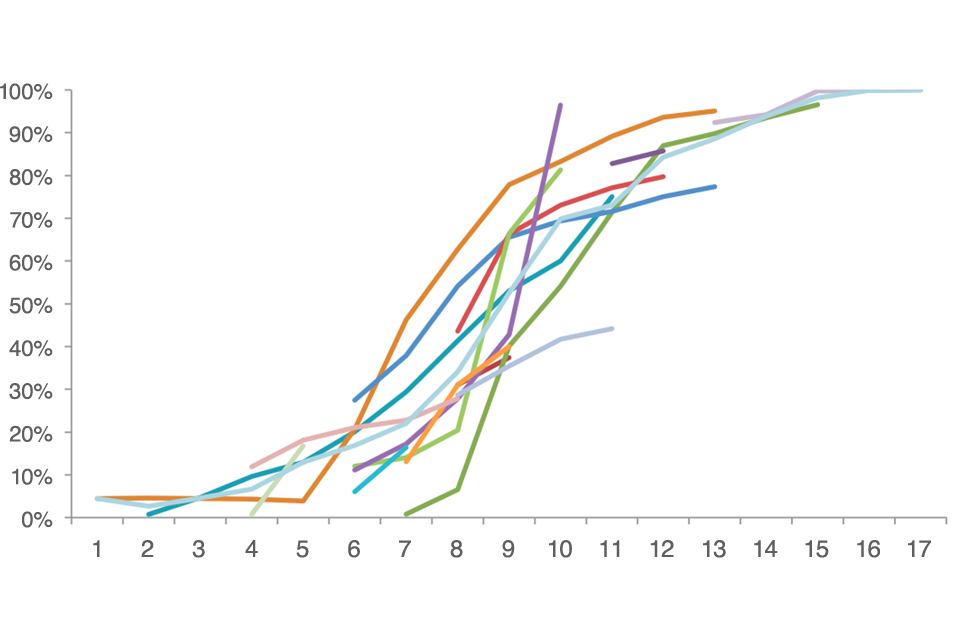

For each of the case studies, digital penetration has been tracked over time.

Figure 19: Digital take-up curves (year by year) for individual case study services

Figure 23: Table showing overview of channel cost benchmarking data

Putting these historic curves together gives a generic take-up curve for Government services. It forms an S-curve which is typical of the take-up of various technologies (Fig 10).

This S-curve enables the calculation of in-year savings. The position of each service on the curve was established. Where the penetration for a service was not known, the average across all services was used. To calculate the in-year annual savings, each transaction was moved along the curve year by year. This approach was used to calculate the increase in digital penetration, which was then multiplied by the annual savings per percentage point.

Annex 5: Departmental savings methodology

Overview of the approach

Three inputs drive the estimate of potential departmental cost savings

-

Transactional service costs Estimates of transactional service costs are based on departmental and agency accounts, supplemented by further details from case studies ands other publicly available information. Further details on this are in Section 2 of the main report.

-

Transactional service channel mix (% digital) Where data was available, actual figures for the service channel mix were used. Where data was not available, it was assumed that the % digital take-up for services was 46% - based on an average of the known digital take-up rates across government services. It was assumed that the remaining offline transactions were split by 80% phone and 20% face-to-face. We recognise that this ratio will vary across departments, depending on the nature of transactional services they offer.

-

Cost savings % resulting from a shift from an offline to digital channel A variety of benchmarks for relative channel cost were used. These are explained in further detail below.

The analysis shows a high degree of sensitivity to cost ratios used.

Sensitivity to estimated transaction-related costs

The sensitivity of estimated potential cost savings to estimated transaction costs by department is linear. Every 10% change in estimated transaction-related costs for each department would result in a 10% change in the same direction to estimates of potential cost savings for that department.

Sensitivity to channel split

There are a relatively small number of transactions corresponding to services for which we are using the assumed digital take-up figure. Consequently, the total estimated potential cost savings are quite insensitive to the variable. However, such sensitivity may be higher for individual departments with a disproportional number of transactions with unknown digital take-up.

Figure 20: Sensitivity to % digital take-up assumptions where a service is known to offer a digital channel with unknown take-up

| % used | Potential cost savings (bn) | Comment |

|---|---|---|

| 70.5% | £1.55 | Simple avg. including services that are 100% digital |

| 50.6% | £1.68 | Weighted avg. of the same 40 services below for our base case |

| 46.1% | £1.71 | Base estimate; simple avg. of the 40 services with known digital take-up of more than 0% and less than 100% |

| 12.8% | £1.86 | Simple avg. including services that are 0% and 100% digital (including blanks which were assumed to be 0% digital) |

Figure 21: Sensitivity to assumed channel split for non-digital transactions[footnote 20]

| % split by channel for non-digital transactions | Potential cost savings (bn) |

|---|---|

| 50% phone / 50% face-to-face | £1.87 |

| 70% phone / 30% face-to-face | £1.76 |

| 80% phone / 20% face-to-face | £1.71 |

| 90% phone / 10% face-to-face | £1.66 |

| 100% phone / 0% face-to-face | £1.63 |

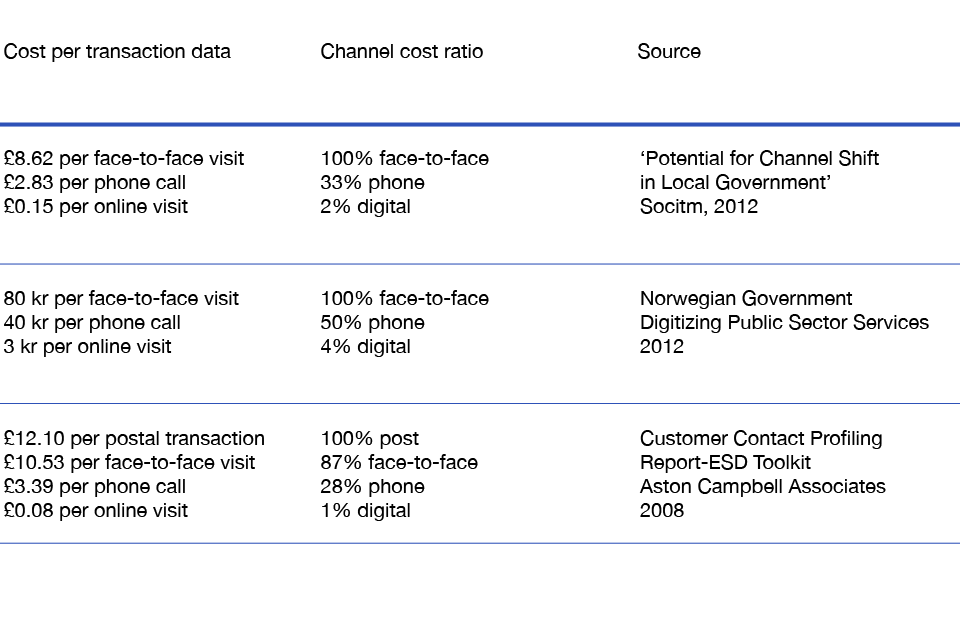

Sensitivity of cost saving to channel cost ratios

The sensitivity analysis shows a high degree of sensitivity to the channel cost ratios used. We have further analysed sensitivity of the model and the potential cost savings estimate to some of the key variables. Departmental figures will be much more sensitive than the total figure to each of those variables.

Figure 22: Sensitivity of total annual savings to channel cost ratios

| Relative cost per channel, per transaction | Potential total annual savings | Source | |

| 3% digital / 33% phone / 100% face-to-face | £3.7bn | Adjusted estimates from ‘Potential for Channel Shift in Local Government’ (Socitm, 2012). | [footnote 21] |

| Balanced mix varied by department according to data where available and benchmarks | £1.7bn | Base estimate; mix of channel cost benchmarks and case study data. | |

| 36% digital / 66% phone /100% face-to-face | £1.4bn | Average of % savings taken from case study data |

Figure 23: Overview of channel cost benchmarking data

Figure 19: Graph showing digital take-up curves (year by year) for individual case study services

As indicated by the ranges of the estimated transaction costs by department and the sensitivity analysis to other key estimates and assumptions, potential cost savings estimates can be strengthened to reduce variability. The estimates present the best available external view.The next step would be to reduce the number of estimates and assumptions that have been made based on judgement, and replace them (wherever possible) with factual data. An iterative process would result in better-informed and more customised estimates for every service agency and department, but require a considerable degree of additional analysis.

Estimates of transaction related costs

The top-down approach was built by estimating the transaction-related expenditure associated with each department. For the transaction-focused agencies, we deducted all non-transaction related costs from the total agency expenditure (eg grants, non-cash costs) from the annual reports, and aggregated these at a department-level to estimate transaction-related expenditure. For all other departments/agencies whose main purpose is not transactional in nature, the major transaction-related cost categories were identified using departmental and agency annual reports, and included categories such as staff and other costs of service delivery. This analysis was carried out for the 13 largest departments, out of a total of 15 relevant departments and covered 99.9% of total transactions (some departments with a small number of transactions were excluded as they are primarily non-transactional in nature).

Figure 24: Estimates of transaction related costs and savings by department.

| Department Transactions (millions) | Est. transaction related costs | Est. savings (cost recovery % ) | . |

|---|---|---|---|

| HM Revenue and Customs (HMRC) | 640.2 | £720m-870m | £240-270m (0%) |

| Department for Work and Pensions (DWP)[footnote 22] | 54.1 | £2.5-4.1bn | £260-430m (0%) |

| Home Office | 16.1 | £750m-£1bn | £180-240m (80%) |

| Department for Transport (DfT) | 90.8 | £320-770m | £80-190m (100%) |

| Department for Business, Innovation and Skills (BIS) | 52.0 | £560-760m | £230-350m (50%) |

| Department for Environment, Food and Rural Affairs (Defra) | 23.2 | £520-760m | £160-230m (10%) |

| Department for Communities and Local Government (DCLG) | 0.6 | £210-340m | £0m (0%) |

| Department for Education (DfE) | 2.8 | £65-230m | £35-130m (0%) |

| Department for Culture, Media and Sport (DCMS) | 13.9 | £70-115m | £30-75m (100%) |

| Ministry of Justice (MoJ) | 11.6 | £60-80m | £30-50m (0%) |

| Department of Energy and Climate Change (DECC) | 2.3 | £40-60m | £15-35m (0%) |

| Foreign and Commonwealth Office (FCO) | 1.5 | £5-8m | £2-3m (100%) |

| Attorney General’s Office | 0.1 | £2-5m | £1-2m (0%) |

| Ministry of Defence | 0.0 | n/a | n/a |

| Department for International Development (DFID) | 0.0 | n/a | n/a |

The cost recovery % figure estimates, to the nearest 10%, the proportion of savings that will be passed on directly to service users. The estimates savings are also shown in Fig 9.

Figure 25: Mid-range estimates of total potential annual savings by department (£m), split by public spending / cost recovery realisation

| Mid-range estimates of total potential annual savings by department (£m), split by public spending / cost recovery realisation | Public spending | Cost recovery | Total |

|---|---|---|---|

| HMRC | 255 | 0 | 255 |

| DfT | 0 | 116 | 166 |

| DWP | 326 | 0 | 326 |

| BIS | 164 | 176 | 340 |

| DEFRA | 177 | 16 | 193 |

| HO | 41 | 187 | 227 |

| DCMS | 0 | 63 | 63 |

| MoJ | 49 | 0 | 49 |

| DfE | 83 | 0 | 83 |

| DECC | 27 | 0 | 27 |

| DCLG | 0 | 0 | 0 |

| FCO | 0 | 2 | 2 |

| AGO | 2 | 0 | 2 |

| DFID | 0 | 0 | 0 |

| MoD | 0 | 0 | 0 |

As in Figure 9, these savings estimates are based on historic 11/12 financial data. New policy initiatives, such as Universal Credit, are likely to affect both the total savings potential of specific departments. The actual savings potential will be as set out in departmental digital strategies published at the end of 2012.

Footnotes

-

Driving Standards Agency data, 2011/12: £6.62 post, £4.11 telephone, £0.22 digital per transaction. ↩

-

Of this, £1.1 - £1.3 billion (approximately 65%) will accrue directly to the government accounts as cash-releasing fiscal savings for the taxpayer. The remainder will be passed on directly as savings to service users. This split is explained in further detail in Annex 2. ↩

-

HMRC, Costing Customer Time Research Paper, 2009. In the 2009 report ‘Champion for Digital Inclusion’ (RaceOnline, PwC), it was stated that people could save between £3.30 and £12.00 for every Government transaction they completed digitally instead of offline. ↩

-

These savings may alternatively be claimed as leisure time. ↩

-

These services account for over half of the 1.5 billion transactions that take place across the whole of government. ↩

-

This estimate is based on analysis of published government accounts to identify costs specifically related to the delivery of transactional services. More detail on the top-down methodology used to produce this figure is set out in Section 2 of this report. ↩

-

Government Digital Service analysis, 2012 ↩

-

Government Digital Service analysis, 2012 ↩

-

SOCITM Insight, Potential for channel shift in local government (Engand), 2012. £8.62 face-to-face, £2.83 telephone, £0.15 digital per transaction. ↩

-

The choice of 82% digital take-up is made on the basis of the Government Digital Service Digital Landscape Research, published alongside the Government Digital Strategy (2012). The research found that only 18% of people either very rarely use the internet, or not use it at all. ↩

-

Estimates based on time spent per transaction in a non-digital channel by service and cost per FTE per minute. The model also includes estimates for rent, IT, and materials per transaction. ↩

-

This graph includes automated electronic transactions (as digital) and Job Seekers Allowance claim transactions (as non-digital). However, these have been excluded from the aggregated departmental figures when calculating savings estimates because they distort the savings potential that exists from making individual transactional services digital by default. This should not detract from the significant efficiencies that electronic transactions have generated ↩

-

The lower / upper bounds reflect the range of estimates for total transaction costs across departments. ↩

-

This estimate assumes a full FTE average cost of approximately £36,000. This figure is based on Cabinet Office analysis of the average annual FTE cost across government. ↩

-

The majority of these FTEs are expected to be civil servants, though a proportion will be employees of companies responsible for outsourced government services. ↩

-

‘Digital by default’ is defined as the base case scenario set out earlier - a shift to 82% digital take-up for all services with over 10,000 transactions per year. ↩

-

The take-up rates for each specific case study are illustrated in Annex 4. ↩

-

It is likely that using this average figure overestimates the digital penetration of some services, which will lead to a smaller estimate of the potential savings. ↩

-

As explained in the main report, the choice of 82% digital take-up is made on the basis of the Government Digital Service Digital Landscape Research, published alongside the Government Digital Strategy ↩

-

This sensitivity calculation excludes departments where specific estimates on channel split were based upon published data or information disclosed through the case studies. ↩

-

The SOCITM study estimated average UK council costs per transaction of 15 pence, £2.83, and £8.62 for transactions done digitally, by phone, or face to face, respectively. Such costs would result in cost ratios of 2%, 33%, 100%. However, we used a 30 pence cost assumption for digital transactions as suggested by other studies with similar ranges for telephone and face-face costs. ↩

-

The savings calculation for DWP includes data from Jobcentre Plus published accounts that includes the cost of face to face Fortnightly Job Reviews (FJRs) for Jobseekers Allowance. The Jobcentre Plus accounts do not include a disaggregation for FJRs so these are included in the estimated transaction costs for DWP. Approximately 40 million FJRs are carried out every year, so the inclusion of these costs may inflate the cost per transaction figure used for the purposes of this report. ↩