Household below average income series: quality and methodology information report FYE 2020

Published 25 March 2021

© Crown copyright 2021

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/statistics/households-below-average-income-for-financial-years-ending-1995-to-2020/household-below-average-income-series-quality-and-methodology-information-report-fye-2020

Introduction

The Households Below Average Income (HBAI) report presents information on living standards in the United Kingdom and is the foremost source for data and information about household income, and inequality in the UK. It provides annual estimates on the number and percentage of people living in low-income households. Figures are also provided for children, pensioners, working-age adults and individuals living in a family where someone is disabled.

HBAI statistics incorporate widely-used, international standard measures of low income and inequality. They provide a range of measures of low income, income inequality, and material deprivation to capture different aspects of changes to living standards. The current series started in Financial Year Ending (FYE) 1995 and so allows for comparisons over time, as well as between different groups of the population.

The statistics are based on the Family Resources Survey (FRS), whose focus is capturing information on incomes, and as such captures more detail on different income sources compared to other household surveys. The FRS captures a lot of contextual information on the household and individual circumstances, such as employment, education level and disability. This is therefore a very comprehensive data source allowing for a lot of different analysis.

This report provides detailed information on key quality and methodological issues relating to HBAI data. Information on the FRS methodology is available in the FRS Background Note and methodology.

Comparing official statistics across the UK

All official statistics from the HBAI for the UK and constituent countries in this publication are considered by the Department for Work and Pensions (DWP) as “Fully Comparable at level A” of the UK Countries Comparability Scale (With the exception of measures estimated on a before housing cost (BHC) basis for Northern Ireland, due to differing treatment of water rates).

National Statistics

The regulatory arm of the UK Statistics Authority, the Office for Statistics Regulation, has designated the Family Resources Survey as National Statistics, in accordance with the Statistics and Registration Service Act 2007 and signifying compliance with the Code of Practice for Statistics (the Code).

National Statistics status means that official statistics meet the highest standards of trustworthiness, quality and public value and comply with all aspects of the Code. The Office for Statistics Regulation has undertaken this assessment to consider whether the statistics meet the required standard.

It is DWP’s responsibility to maintain compliance with the standards expected of National Statistics. If DWP becomes concerned about whether these statistics are still meeting the appropriate standards, we will discuss any concerns with the Office for Statistics Regulation. National Statistics status can be removed at any point when the highest standards are not maintained, and reinstated when standards are restored.

Further information about National Statistics can be found on the Statistics Authority website.

Acknowledgements

As in previous years, the DWP would like to thank the Institute for Fiscal Studies (IFS) for the substantial assistance that they have provided in checking and verifying the income data and grossing factors underlying the main results in this edition.

We are also grateful to HM Revenue and Customs (HMRC) for the provision of aggregated data from the Survey of Personal Incomes.

Users and uses

HBAI is a key source for data and information about household income and inequality, and is used for the analysis of low income by researchers and the Government. Users include: policy and analytical teams within the DWP, the Devolved Administrations, other Government departments, local authorities, Parliament, academics, journalists, and the voluntary sector.

The Department for Work and Pensions’ responsibilities include understanding and dealing with the causes of poverty rather than its symptoms, encouraging people to work and making work pay, encouraging disabled people and those with ill health to work and be independent, and providing a decent income for people of pension age and promoting saving for retirement. Progress towards these responsibilities will affect these results.

The key uses of the published statistics and datasets are:

-

to provide detail on the overall household income distribution and low income indicators for different groups in the population

-

for international comparisons, both within the EU and for OECD countries

-

for parliamentary, academic, voluntary sector and lobby group analysis. Examples include using the HBAI data to examine income inequality, the distributional impacts of fiscal policies and understanding the income profile of vulnerable groups

The following describes how HBAI statistics are included in the Welfare Reform and Work Act 2016.

The first three of the four income-related measures included in the Welfare Reform and Work Act 2016 are reported in HBAI.

The four measures cover the percentage of children in the United Kingdom:

a) who live in households whose equivalised net income for the relevant financial year is less than 60% of median equivalised net household income for that financial year.

b) who live in households whose equivalised net income for the relevant financial year is less than 70% of median equivalised net household income for that financial year, and who experience material deprivation.

c) who live in households whose equivalised net income for the relevant financial year is less than 60% of median equivalised net household income for the financial year beginning 1 April 2010, adjusted to take account of changes in the value of money since that financial year.

d) who live in households whose equivalised net income has been less than 60% of median equivalised net household income in at least 3 of the last 4 survey periods.

Definitions for relevant key terms in the Act are consistent with those given in the Glossary; Income Definition; Equivalisation; and Low income and material deprivation for children sections of this document.

Data for reporting against the fourth measure will be released via the Income Dynamics publication.

Further details of the uses of HBAI statistics are given in Annex 3

What do you think?

We are constantly aiming to improve this report and its associated commentary. In particular, this issue we have focussed on improving the data we deposit at the UK Data Service. We would welcome any feedback you might have, and would also be particularly interested in knowing how you make use of these data to inform your work. Please contact us by email: team.hbai@dwp.gov.uk.

New for this publication

Household Food Security Tables

This year’s HBAI statistics include new tables showing the level of household food security for individuals living in low income households (see tables 9.1 to 9.8).

Questions are asked of the person in the household who knows the most about buying and preparing food. In common with the rest of the FRS, the focus is on the period of 30 days leading up to interview. The questions are comparable to those used by other public bodies in the UK, and also internationally. From the questions, a ten-point household score is generated, and the household is given a food security status:

-

High food security (score = 0): The household has no problem, or anxiety about, consistently accessing adequate food

-

Marginal food security (score = 1 or 2): The household had problems at times, or anxiety about, accessing adequate food, but the quality, variety, and quantity of their food intake were not substantially reduced

-

Low food security (score = 3 to 5): The household reduced the quality, variety, and desirability of their diets, but the quantity of food intake and normal eating patterns were not substantially disrupted

-

Very low food security (score = 6 to 10): At times during the last 30 days, eating patterns of one or more household members were disrupted and food intake reduced because the household lacked money and other resources for food.

Households with high or marginal food security are “food secure”. Food secure households are considered to have sufficient, varied food to facilitate an active and healthy lifestyle. Households with low or very low food security are “food insecure”. The banner of food insecurity covers a wide range of circumstances; where there is risk of, or lack of access to, sufficient, varied food.

The individual level data in these tables are presented using the household food security status. This means that one household food security status is used across all individuals within a household. Experiences of food insecurity can vary within a household. This data should not be presented using the phrasing “individuals are food insecure”, but as “individuals living in food insecure households”.

The definition of a household used in the Family Resources Survey (FRS) is ‘one person living alone or a group of people (not necessarily related) living at the same address who share cooking facilities and share a living room, sitting room, or dining area’. So, for example, a group of students with a shared living room would be counted as a single household even if they did not eat together, but a group of bed-sits at the same address would not be counted as a single household. A household may consist of one or more benefit units, which in turn will consist of one or more people (adults and children).

It should be noted that the food security section of this publication excludes shared households (see definition below), such as a house shared by a group of professionals. These respondents may not have insight into the food security status of others in their household and may not regularly share financial information.

Revision to full Time Series due to treatment of Income from Child Maintenance

A minor methodological revision has been made to include within HBAI all income from child maintenance. In previous HBAI publications, child maintenance arranged directly between the parents or by court order was included, but child maintenance arranged via the Child Maintenance Service (or its predecessors) was not. From this year’s publication, child maintenance arranged via the Child Maintenance Service (or its predecessors) is now also included. This results in more income from child maintenance being included, in turn slightly increasing some household incomes and so tending to slightly reduce low income rates for families with children. The full back series (back to FYE 1995) has been revised – child maintenance arranged via the Child Maintenance Service or its predecessors added - so that all income from child maintenance income is included and comparisons over time are on a consistent basis across the full time series. This also means that figures for FYE 1995 to FYE 2019 in this year’s publication (FYE 2020 statistics) may be slightly different to the equivalent figures in previous publications. Please refer to the HBAI Quality & Methodology Report for more information.

Regarding the impact of the revision on levels of low income, the percentage of children in low income in FYE 2019 (previous publication) has been revised downwards by around 0.4 percentage points on an AHC basis and 0.2 percentage points on a BHC basis. Revisions in previous years are similar or slightly less and in most cases are unchanged rounded to the nearest percentage point. However, please note that the revisions are greater for family types with children who are more likely to receive income from child maintenance, in particular lone parent families. For example, the percentage of children in low income in lone parent families in FYE 2019 (previous publication) has been revised downwards by between 0.7 percentage points on an absolute BHC basis and 1.8 percentage points on an absolute AHC basis (the relative BHC and relative AHC downward revisions are 1.2 and 1.6 percentage points respectively).

Conversely, the impact on low income rates for families without children is far less than the 0.2 and 0.4 percentage point figures quoted above. Please note, however, that low income rates may have been revised by a very small amount even for some groups that do not have children receiving income from child maintenance e.g. pensioner households. Such revisions can happen because the low income line (60% of the median) will change if the median changes i.e. some other households receive extra income which raises the median and hence the low income line. Therefore, a very small number of household groups whose incomes are unchanged (they do not have child maintenance income via the Child Maintenance Service) may fall below the low income line because that low income line has increased slightly. As well as the relative low income lines, this also applies to the absolute low income lines (60% of the FYE 2011 medians BHC and AHC) because the revision has been applied to the full back series of data including FYE 2011. In summary, this means that, whilst low income rates have generally been revised slightly downwards for most groups with children, for groups without children (or specifically any group without child maintenance income via the Child Maintenance Service) it is possible that low income rates may have been revised very slightly upwards.

The impact of the revision on low income trends is even less than the impact on low income levels because the revision each year is in the same direction – more income for some households with children – and broadly similar in scale over time.

Reporting of Benefits in the FRS

As with all survey data, the source FRS data used in HBAI undergoes various quality assurance and editing processes each year to ensure its fitness for purpose. As a national statistic, and in line with the Code of Practice for Statistics (Value V4.1) DWP looks to improve the FRS, year on year.

In particular, benefit amounts are edited using a combination of manual and automated processes. We have previously advised users of our intention to match those taking part in the survey to their benefit records (across the range of administrative datasets available to DWP, for many different state benefits, and at the time of interview). This would enable a check on the accuracy of pound amounts reported during the interview, as well as the respondent’s eligibility for the various elements of state support.

For the current survey year (FYE 2020), the process to edit benefit amounts has involved the more-automated use of administrative data to edit FRS-reported Universal Credit (UC) amounts. This is necessary because:

-

It is generally more complicated to check UC amounts than for other benefits, owing to the number of different components of the UC calculation

-

The time taken to manually edit UC amounts is therefore greater than for other benefits

-

The range of possible amounts values is wider than any other state benefit, running from nil to several hundred pounds per week; and

-

There has been a substantial increase in the number of UC observations since the previous survey year (FYE 2019), more than doubling since then

Given the above factors, editing reported UC amounts data was a more challenging task than in previous surveys. Given the legal deadline to publish HBAI data by the end of March it is important to be efficient in survey processing. The process looked at instances where people stated that they were receiving some form of state support; and where the amount reported was in some way questionable. The information then retrieved included respondents’ (true) amounts of benefit received, which allowed a closer editing of benefit rates than would otherwise have been the case.

This more-automated UC amounts editing process has a minimal affect overall on household incomes. There is, however, likely to be a small impact on the income distribution, particularly in the bottom quintile where a greater proportion of income comes from income-related benefits.

The level of benefit caseload undercount varies by benefit and across survey years. The extent of this is shown clearly in the FRS Methodology tables, especially Table M.6a: Receipt of state support, FRS data and administrative data. Compared with FYE 2019, the main changes are increasing levels of undercount for Personal Independence Payment (PIP) and Housing Benefit (HB). The PIP undercount has increased from approximately 360 thousand to 690 thousand cases. For HB, a small over count (60 thousand) in FYE 2019 has become an undercount of 690 thousand in FYE 2020. However, some of this is due to the increased editing of UC cases noted above e.g. where an FRS respondent reported receipt of both UC and HB and the benefit editing showed that they were receiving their housing support within UC. Regarding the UC caseload undercount, the UC caseload itself approximately doubled between FYE 2019 and FYE 2020. Therefore, although the UC caseload undercount increased from 470 thousand to 660 thousand this was actually a slight decrease in relative terms (a decrease in caseload undercount from 39% to 32% compared with administrative data).

The impact on the income distribution of an increase in benefit caseload undercount is not possible to establish precisely: it depends on the reason for the increased undercount. If the cause of the undercount is that benefit recipients are responding to the survey but not reporting some or all of their benefits, then household incomes for these respondents, who tend to be in the bottom half of the income distribution, would be under-estimated. However, if the cause of the undercount is that a higher proportion of benefit recipients are not responding at all to the survey, then benefit recipients would be under-represented in the FRS sample and households not receiving benefits over-represented. Since households not receiving benefits tend to have higher incomes, this would mean household incomes overall would tend to be over-estimated.

Development of processes linking FRS data to administrative data will continue through 2021, in support of next year’s publication, and beyond. For more details please see the FRS Background Information and Methodology report.

Using and Interpreting HBAI Results

Guide to published tables

All the publication tables previously available within the report are available as ODS spreadsheets on the HBAI on GOV.UK. Data and tables are also available via Stat-Xplore.

In the summary tables, estimates of the percentage and number in low income that are statistically significant from the previous year are shown with an asterisk. Changes marked by an asterisk are unlikely to have occurred as a result of chance.

The series started in FYE 1995 and so allows for comparisons over time, as well as between different groups of the population.

What do we mean by average?

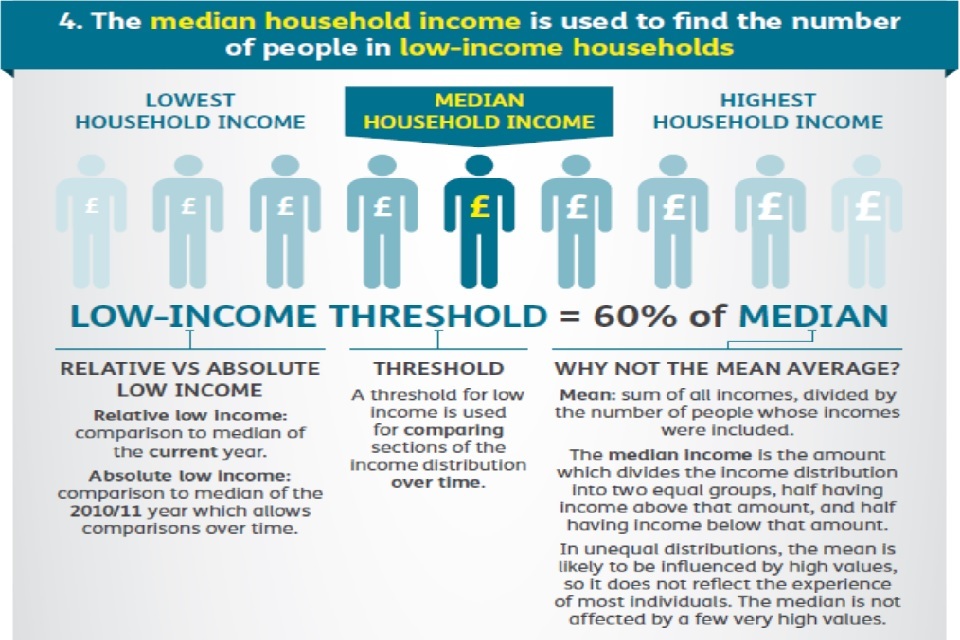

In HBAI, the term ‘average’ is used to describe the median. This divides the population of individuals, when ranked by income, into two equal-sized groups, and unlike the mean is not affected by extreme values.

HBAI measures

There are a range of measures of low income, income inequality, and material deprivation to capture different aspects of changes to living standards:

Relative low income

Relative low income measures the number and proportion of individuals who have household incomes below a certain proportion of the average in that year - and is used to look at how changes in income for the lowest income households compare to changes in incomes near the ‘average’. In the HBAI report we concentrate on those with household incomes below 60 per cent of the average. Information on those with household incomes below 50 and 70 per cent of the average is available in the detailed tables published on the HBAI web-pages.

Absolute low income

Absolute low income measures the proportion of individuals who have household incomes a certain proportion below the average in FYE 2011, adjusted for inflation. It is used to look at how changes in income for the lowest income households compare to changes in the cost of living. In the HBAI report we concentrate on those with household incomes below 60 per cent of the average FYE 2011 income. Information on those with household incomes below 50 and 70 per cent of the average is available in the detailed tables published on the HBAI web-pages.

Rounding

Due to rounding, the estimates of change in percentages or numbers of individuals in low income or material deprivation may not equal the difference between the total percentage or number of individuals for any pair of years.

The publication and tables follow the following conventions:

| Symbol | Description |

|---|---|

| .. | not available due to small sample sizes (less than 100) |

| - | the estimate is less than 50,000 or the percentage is less than 0.5 per cent |

-

Population estimates are rounded to the nearest 100,000

-

Percentages are rounded to the nearest 1 per cent

Key Terminology

Income

This is measured as total weekly household income from all sources after tax (including child income), national insurance and other deductions. An adjustment called ‘equivalisation’ is made to income to make it comparable across households of different size and composition.

Median

Median household income divides the population, when ranked by equivalised household income, into two equal-sized groups. The median is the value at the very middle of the distribution.

Deciles and Quintiles

These are income values which divide the whole population, when ranked by household income, into equal-sized groups. This helps to compare different groups of the population.

Decile and quintile are often used as a standard shorthand term for decile/quintile group.

Decile groups are ten equal-sized groups - the lowest decile describes individuals with incomes in the bottom 10 per cent of the income distribution.

Quintile groups are five equal-sized groups – the lowest quintile describes individuals with incomes in the bottom 20 per cent of the income distribution.

Income distribution

The spread of incomes across the population.

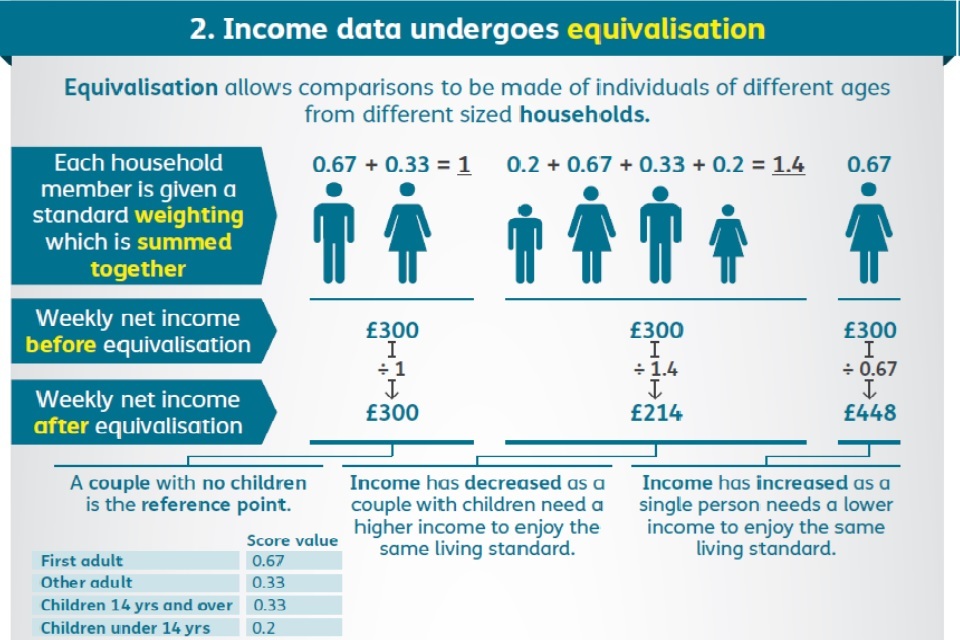

Equivalisation

Equivalisation adjusts incomes for household size and composition, taking an adult couple with no children as the reference point. For example, the process of equivalisation would adjust the income of a single person upwards, so their income can be compared directly to the standard of living for a couple.

Housing costs

Housing costs include rent, water rates, mortgage interest payments, buildings insurance payments and ground rent and service charges. A full list can be found in the glossary at the end of this document.

Benefit unit and households

HBAI presents information on an individual’s household income by various household and benefit unit (family) characteristics. There are important differences between households and benefit units.

Household

One person living alone or a group of people (not necessarily related) living at the same address who share cooking facilities and share a living room, sitting room or dining area. A household will consist of one or more benefit units.

Family or Benefit Unit

A single adult of couple living as married and any dependent children.

For example, a group of students with a shared living room would be counted as a single household even if they did not eat together, but a group of bed-sits at the same address would not be counted as a single household because they do not share living space or eat together.

A couple living with their young children and an elderly parent would be one household but two benefit units. The couple and their children would constitute one benefit unit, and the elderly parent would constitute another. It should be noted that the term ‘benefit unit’ is used as a description of groups of individuals regardless of whether they are in receipt of any benefits or tax credits.

A household will consist of one or more benefit units, which in turn will consist of one or more individuals (adults and children).

Other Terms

For more information on these and other terms used throughout the report, see the glossary at the bottom of this document, and the infographics explaining key terms.

Issues to consider

The following issues need to be considered when using the HBAI:

Lowest incomes

Comparisons of household income and expenditure suggest that those households reporting the lowest incomes may not have the lowest living standards. The bottom 10 per cent of the income distribution should not, therefore, be interpreted as having the bottom 10 per cent of living standards. Results for the bottom 10 per cent are also particularly vulnerable to sampling errors and income measurement problems. For HBAI tables, this will have a relatively greater effect on results where incomes are compared against low thresholds of median income. For this reason, compositional and percentage tables using the 50 per cent of median thresholds have been italicised to highlight the greater uncertainty. We have also presented money value quintile medians in Table 2.3ts on three-year averages to reflect this uncertainty.

Adjustment for inflation

As advised in a Statistical Notice published in May 2016, from FYE 2015 HBAI has made a methodological change to use variants of CPI when adjusting for inflation. Prior to the FYE 2015 HBAI publication variants of RPI were used to adjust for inflation.

This change follows advice from the UK National Statistician that use of RPI should be discontinued in statistical publications.

Full details on the likely impact on this methodological change, together with estimates for trends in income and absolute low income under both the old and new methodologies, are presented in Annex 4 to the FYE 2015 HBAI Quality and Methodology Report.

Benefit receipt

Relative to administrative records, the FRS is known to under-report benefit receipt. However, the FRS is considered to be the best source for looking at benefit and tax credit receipt by characteristics not captured on administrative sources, and for looking at total benefit receipt on a benefit unit or household basis. It is often inappropriate to look at benefit receipt on an individual basis because means-tested benefits are paid on behalf of the benefit unit. DWP published research (Working Paper 115) which explores the reasons for benefit under-reporting with the aim of improving the benefits questions included within the FRS. Table M.6a of the FRS publication presents a comparison of receipt of state support between FRS and administrative data. Methodology Table M.6b has been produced for the first time this year and compares the average weekly receipt of state support in the FRS FYE 2019 data, with the average weekly receipt of state support from the administrative data sources. Some benefit types have not been included in this analysis because no directly comparable administrative data source is available.

Self-employed

All analyses in the HBAI publication include the self-employed. A proportion of this group are believed to report incomes that do not reflect their living standards and there are also recognised difficulties in obtaining timely and accurate income information from this group. This may lead to an understatement of total income for some groups for whom this is a major income component, although this is likely to be more important for those at the top of the income distribution. There is little difference in the overall picture of proportions in low-income households when analysis is performed either including or excluding the self-employed.

Savings and investment

The data relating to investments and savings should be treated with caution. Questions relating to investments are a sensitive section of the questionnaire and have a low response rate. A high proportion of respondents do not know the interest received on their investments. It is likely that there is some under-reporting of capital by respondents, in terms of both the actual values of the savings and the investment income. This may lead to an understatement of total income for some groups for whom this is a major income component, such as pensioners, although this is likely to be more important for those at the top of the income distribution.

Methodological change for FYE 2020 (FRS savings and investments variable used in HBAI): The level of savings and investments, for some families (benefit units) and households has been estimated using a slightly different methodology in FYE 2020 than in previous years. The new method more accurately estimates savings in current accounts and basic bank accounts.

For current and basic bank accounts only, the new method avoids imputation of the account balance from interest paid, instead basing account balances on the figure given by the respondent. Approximately a third of all accounts are covered by this new methodology. Benefit unit respondents with reported savings and investments below £1,500 and above £20,000 are not asked to estimate the value of any of their accounts, other than current and basic bank accounts, so it is not possible to apply the new methodology to any other accounts.

This change has caused a large shift in the division of families (benefit units) and households between the two categories of (i) those with no savings at all to (ii) those with less than £1,500 in savings. This has produced estimates of savings in the relevant categories which are closer to those of other related surveys, but it should be noted that savings and investments breakdowns for FYE 2020 are not directly comparable with those for previous years.

Comparisons with National Accounts

Table 2.1tr shows comparisons between growth in Real Household Disposable Income and real growth in HBAI mean BHC unequivalised income. For some years, income growth in the HBAI-based series appears lower than the National Accounts estimates. The implication of this is that absolute real income growth could be understated in the HBAI series. Comparisons over a longer time period are believed to be more robust.

High incomes

Comparisons with Her Majesty’s Revenue and Customs’ Survey of Personal Incomes (SPI), which is drawn from tax records, suggest that the FRS under-reports the number of individuals with very high incomes and also understates the level of their incomes. There is also some volatility in the number of high income households surveyed. Since any estimate of mean income is very sensitive to fluctuations in incomes at the top of the distribution, an adjustment to correct for this is made to ‘very rich’ households in FRS-based results using SPI data. The median-based low-income statistics are not affected.

Working status

DWP and ONS have jointly investigated the reasons for the FRS consistently giving higher estimates than the Labour Force Survey (LFS) of the percentage of children in workless households. A report on this investigation found that the main reasons for the divergence were:

-

FRS unweighted data identifying a higher proportion of children in lone parent families, who have a much higher worklessness rate, than does LFS

-

FRS unweighted data showing a higher worklessness rate, in both lone parent and couple with-children families, than LFS

-

LFS employing a grossing regime which substantially reduces the proportion of children in lone parent households, and thereby in workless households; whereas the FRS grossing regime has less of an effect in reducing these proportions

-

the LFS grossing regime also reduces the worklessness rate in lone parent families; whereas the FRS grossing regime has less clear-cut effects

Gender analysis

The HBAI assumes that both partners in a couple benefit equally from the household’s income, and will therefore appear at the same position in the income distribution. Research has suggested that, particularly in low income households, the assumption with regard to income sharing is not always valid as men sometimes benefit at the expense of women from shared household income (see, for instance, Goode, J., Callender, C. and Lister, R. (1998) Purse or Wallet? Gender Inequalities and the Distribution of Income in Families on Benefits. JRF/Policy Studies Institute). This means is means that it is possible that HBAI results broken down by gender could understate differences between the two groups.

Students

Students Information for students should be treated with some caution because they are often dependent on irregular flows of income. Only student loans are counted as income in HBAI (with both the maintenance and tuition parts of the loan included), any other loans taken out are not. The figures are also not necessarily representative of all students because HBAI only covers private households and this excludes halls of residence.

Elderly

The effect of the exclusion of the elderly who live in residential homes is likely to be small overall except for results specific to those aged 80 and above.

Ethnicity analysis

Smaller ethnic minority groups exhibit year-on-year variation which limits comparisons over time. For this reason, analysis by ethnicity is presented as three-year averages.

Disability analysis

No adjustment is made to disposable household income to take into account any additional costs that may be incurred due to the illness or disability in question. This means that using income as a proxy for living standards for these groups, as shown here, may be somewhat upwardly biased. Analysis excluding Disability Living Allowance and Attendance Allowance from the calculation of income has been published as part of the suite of online HBAI ODS tables.

Regional analysis

Disaggregation by geographical regions (Regional information is at NUTS1 level) is presented as three-year averages. This presentation has been used as single-year regional estimates are considered too volatile. This issue was discussed in Appendix 5 of the FYE 2005 HBAI publication, where regional time series using three-year averages were presented. Although the FRS sample is large enough to allow some analysis to be performed at a regional level, it should be noted that no adjustment has been made for regional cost of living differences. It is therefore assumed that there is no difference in the cost of living between regions, although the AHC measure will partly take into account differences in housing costs.

Analysis at geographies below the regional level is not available from this data. Please see the Children in Low-Income Families publication for local level geographies.

Changes to deflators

Since the HBAI FYE 2018 publication, the Office for National Statistics (ONS) have made some very minor revisions to the bespoke Consumer Price Index (CPI) series we use to make real-terms income comparisons within and between survey years. However, because the effect of these revisions on low income measures is negligible no revisions have been made to the deflators used in HBAI. See the following ONS update for more details.

Survey Data

Most of the figures in the HBAI report come from the Family Resources Survey (FRS), a representative survey of over 19,000 households in the United Kingdom. The focus of the FRS is on capturing information on incomes and, as such, is the foremost source of income data and provides more detail on different income sources than other household surveys. It also captures a lot of contextual information on the household and individual circumstances, such as employment, education level and disability. This is therefore a very comprehensive data source allowing for a lot of different analysis.

Surveys gather information from a sample rather than from the whole population. The sample is designed carefully to allow for this, and to be as accurate as possible given practical limitations such as time and cost constraints. Results from sample surveys are always estimates, not precise figures. This means that they are subject to a margin of error which can affect how changes in the numbers should be interpreted, especially in the short-term. The latest estimates should be considered alongside medium and long-term patterns.

In addition to sampling errors, consideration should also be given to non-sampling errors. Non-sampling errors arise from the introduction of some systematic errors in the sample as compared to the population it is supposed to represent. As well as response bias, such errors include inappropriate definition of the population, misleading questions, data input errors or data handling problems – in fact any factor that might lead to the survey results systematically misrepresenting the population. There is no simple control or measurement for such non-sampling errors, although the risk can be minimised through careful application of the appropriate survey techniques from the questionnaire and sample design stages through to analysis of results.

HBAI is based on data from a household survey and so subject to the nuances of using a survey, including:

-

Sampling error: results from surveys are estimates and not precise figures. Confidence intervals help to interpret the certainty of these estimates, by showing the range of values around the estimate that the true result is likely to be within. In general terms the smaller the sample size, the larger the uncertainty. Statistical significance is an attempt to indicate whether a reported change within the population of interest is due to chance. It is important to bear in mind that confidence intervals are only a guide for the size of sampling error

-

non-response error: the FRS response rate each year is around 50 per cent. In an attempt to correct for differential non-response, estimates are weighted using population totals

-

Survey coverage: the FRS covers private households in the United Kingdom. Therefore, individuals in nursing or retirement homes, for example, will not be included. This means that figures relating to the most elderly individuals may not be representative of the United Kingdom population, as many of those at this age will have moved into homes where they can receive more frequent help

-

Survey design: the FRS uses a clustered sample designed to produce robust estimates at former government office region (GOR) level. The FRS is therefore not suitable for analysis below this level

-

Sample size: although the FRS has a relatively large sample size for a household survey, small sample sizes for some more detailed analyses may require several years of data to be combined in order to generate reliable estimates. From April 2011, the target achieved GB sample size for the FRS was reduced by 5,000 households, resulting in an overall achieved sample size for the UK of around 20,000 households for FYE 2012. We previously published an assessment concluding that this still allows core outputs from the FRS to be produced, though with slightly wider confidence intervals or ranges

-

Measurement error: the FRS is known to under-report certain income streams, especially benefit receipt. More detail can be found in Table M.6a and M.6b of the FRS report

Further methodological details relating to the FRS are given in the FRS Background Note and methodology.

Reporting Uncertainty

As above, survey results are always estimates, not precise figures and so subject to a level of uncertainty. Two different random samples from one population, for example the UK, are unlikely to give exactly the same survey results, which are likely to differ again from the results that would be obtained if the whole population was surveyed. The level of uncertainty around a survey estimate can be calculated and is commonly referred to as sampling error.

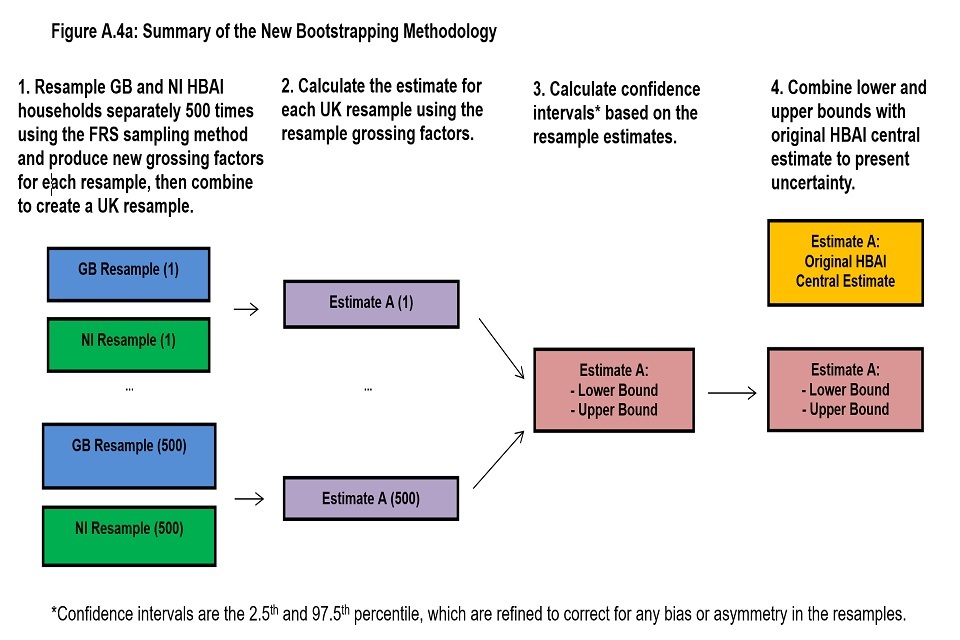

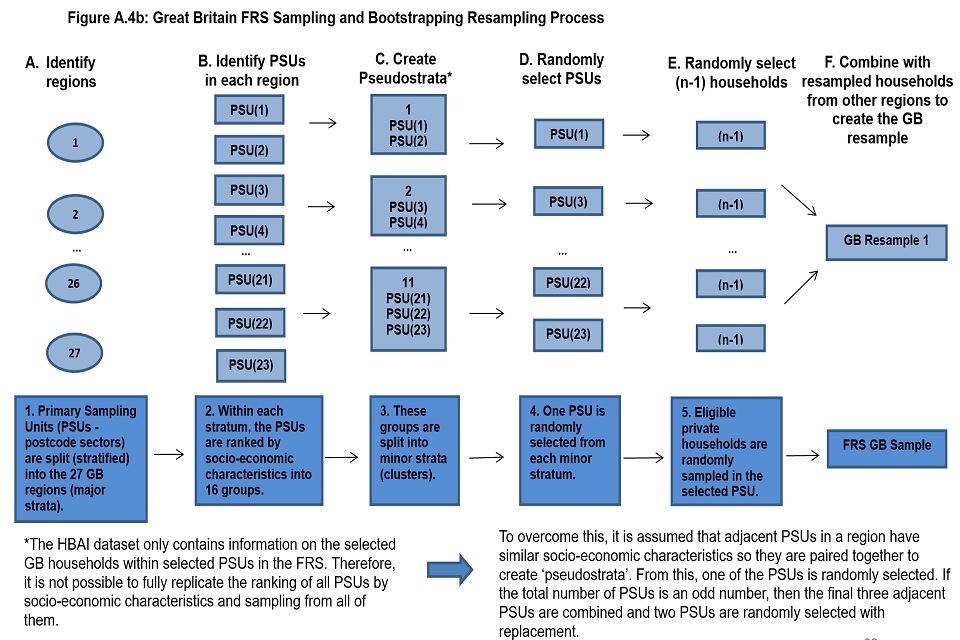

We can calculate the level of uncertainty around a survey estimate by exploring how that estimate would change if we were to draw many survey samples for the same time period instead of just one. This allows us to define a range around the estimate (known as a “confidence interval”) and to state how likely it is that the real value that the survey is trying to measure lies within that range. Confidence intervals are typically set up so that we can be 95% sure that the true value lies within the range – in which case this range is referred to as a “95% confidence interval”. Annex 4 of this document provides further details on the Bootstrapping methodology used to estimate confidence intervals in HBAI, alongside estimates of the sampling error.

Population

The analyses in the HBAI report are primarily based on the FRS. Households in Northern Ireland (NI) were surveyed for the first time in the FYE 2003 survey year. A detailed analysis of observed trends, together with results for NI and the UK for the first three years of NI data can be found in Appendix 3 of the FYE 2005 publication.

The FRS time series in this publication are presented with discontinuities in the years where there is a change from GB to UK. Prior to FYE 2015, for some tables, estimates for NI were imputed for the years FYE 1999 to FYE 2002. This allowed for changes since FYE 1999 to be measured at the UK level. For further details, see Appendix 4 of the HBAI FYE 2005 publication. This imputation is no longer carried out from the FYE 2015 publication.

The survey covers the private household sector. All the results therefore exclude people living in institutions, e.g. nursing homes, halls of residence, barracks or prisons, and homeless people living rough or in bed and breakfast accommodation. The area of Scotland north of the Caledonian Canal was included in the FRS for the first time in the FYE 2002 survey year and, from the FYE 2003 survey year, the FRS was extended to include a 100 per cent boost of the Scottish sample. This has increased the sample size available for analysis at the Scottish level.

A further adjustment is that households containing a married adult whose spouse is temporarily absent, whilst within the scope of the FRS, are excluded from HBAI. Similarly, prior to the FYE 1997 data, households containing a self-employed adult who had been full-time self-employed for less than two months were excluded. This exclusion is no longer made because of the improvements in the self-employment questions in the FRS.

Grossing

The published HBAI analysis presents tabulations where the percentages refer to sample estimates grossed-up to apply to the whole population.

Grossing-up is the term usually given to the process of applying factors to sample data so that they yield estimates for the overall population. The simplest grossing system would be a single factor, e.g. the number of households in the population divided by the number in the achieved sample. However, surveys are normally grossed by a more complex set of grossing factors that attempt to correct for differential non-response at the same time as they scale up sample estimates.

The system used to calculate grossing factors for HBAI mirrors that of FRS grossing with two differences described below.

The system used to calculate grossing factors for the FRS divides the sample into different groups. The groups are designed to reflect differences in response rates among different types of households . They have also been chosen with the aims of DWP analyses in mind. The population estimates for these groups, obtained from official data sources, provide control variables. The grossing factors are then calculated by a process which ensures the FRS produces population estimates that are the same as the control variables.

As an example, the grossed number of men aged 35-39 would be consistent with the Office for National Statistics (ONS) estimate (see Table 1). Some adjustments are made to the original control total data sources so that definitions match those in the FRS, e.g. an adjustment is made to the demographic data to exclude people not resident in private households. It is also the case that some totals have to be adjusted to correspond to the FRS survey year.

A software package called CALMAR, provided by the French National Statistics Institute, is used to reconcile control variables at different levels and estimate their joint population. This software makes the final weighted sample distributions match the population distributions through a process known as calibration weighting. It should be noted that if a few cases are associated with very small or very large grossing factors, grossed estimates will have relatively wide confidence intervals. There were some of these such cases in the FYE 2018 data, we have added footnotes to some tables where these large weights affect the results.

As stated above, the system used to calculate grossing factors for HBAI mirrors that of FRS grossing with two differences. The first difference with FRS grossing is that the sample of households is smaller for HBAI purposes because households with spouses living away from home are excluded (see Population section above). The second difference is that separate control totals are introduced for ‘very rich’ households, so that the top end of the income distribution is more accurately reflected, which is particularly important for estimates of mean income or inequality as measured by the Gini coefficient.

As with the FRS, the grossing regime for HBAI currently uses population and household estimates based on the results of the 2011 Census. Prior to FYE 2013, 2001 census based estimates were used. In addition, a review of FRS grossing was carried out on behalf of DWP by the ONS Methodological Advisory Service. In implementing the review recommendations, a number of relatively minor methodological improvements were implemented from FYE 2013.

The main changes implemented were as follows:

-

improvements to the categorisation of tenure control totals

-

a full breakdown of the total number of households into each of the English regions (in addition breakdowns for Scotland, Wales and Northern Ireland)

-

a new adjustment to account for the different rates of sampling in England and Wales, Scotland, and Northern Ireland

A back-series of grossing factors calculated using the new methodology was created for each year back to FYE 2003, and are used in the HBAI publication tables from FYE 2013 onwards. Further details and analysis of the impact of these methodological changes are published in the grossing methodology review.

In developing the grossing regime, careful consideration has been given to the combination of control totals and the way age ranges, Council Tax bands and so on, have been grouped together. The aim has been to strike a balance so that the grossing system will provide, where possible, accurate estimates in different dimensions without significantly increasing variances.

There are some differences between the methods used to gross the Northern Ireland sample as compared with the Great Britain sample:

-

local taxes in Northern Ireland are collected through the rates system, so Council Tax Band as a control variable is not applicable

-

Northern Ireland housing data are based largely on small sample surveys. It is not desirable to introduce the variance of one survey into another by using it to compute control totals; therefore, tenure type has not been used as a control variable

Details of the grossing regime for Northern Ireland are shown in Table 2.

Table 1: HBAI grossing regime for Great Britain

| Control totals for Great Britain | Groupings | Original Source | Adjustments made by DWP |

|---|---|---|---|

| Private household population by region, age, and sex | Regions: North East, North West, Yorkshire and the Humber, East Midland, West Midlands, East of England, London, South East, South West, Wales, Scotland. Sex and Age: Males aged 0-9, 10-19 dependents, 16-24 non-dependents, 25-29, 30-34, 35-39, 40-44, 45-49, 50-59, 60-64, 65-74, 75-79, 80+; Females aged 0-9, 10-19 dependents, 16-24 non-dependents, 25-29, 30-34, 35-39, 40-44, 45-49, 50-59, 60-69, 70-74, 75-79, 80+ | Mid-year population estimates. Office of National Statistics | ONS total population figures are adjusted for private household estimates using data supplied by ONS directly to DWP. 16-19-year-old dependents and non-dependents are split using data supplied by HMRC directly to DWP. |

| Benefit Units with children | Region: England and Wales, Scotland | Families in receipt of child benefit. HM Revenue and Customs | |

| Lone parents | Sex: Males, Females | Lone parent estimates. Labour Force Survey | Adjusted for FRS survey year (April-March) |

| Households by region | Region: North East, North West, Yorkshire and the Humber, East Midlands, West Midlands, East of England, London, South East, South West, Wales, Scotland | Households by region. Office for National Statistics (England) / Welsh Government (Wales) / Scottish Government (Scotland) | Adjusted for FRS survey year (April-March) |

| Households by tenure type | Tenure (Social Renters, Private Renters, Owner Occupied) | Dwellings by tenure type. Ministry of Housing, Communities and Local Government | Household control totals are calculated using dwellings data published by MHCLG, Welsh Government, Scottish Government. Adjusted for FRS survey year (April-March) |

| Households by council tax band | Council Tax Band (NVS and A, B, C and D, E to H) | Dwellings by council tax band published by Valuations Office Agency. Dwellings by council tax band. Published by the Scottish Government | Household control totals are calculated using dwellings data published by VOA / Scottish Government, adjusted for FRS survey year (April-March). Estimates for properties not-valued-separately (NVS) based on FRS sample proportions. |

| Households containing ‘Very Rich’ people | Pensioners, Non-pensioners | HMRC Survey of Personal Incomes (SPI) |

Table 2: HBAI grossing regime for Northern Ireland

| Control Totals for Northern Ireland | Groupings | Original Source | Adjustments made by DWP |

|---|---|---|---|

| Private household population by age and sex | Sex and Age: Males aged 0-9, 10-19 dependents,16-24 non-dependents, 25-29, 30-34, 35-39, 40-44, 45-49, 50-59, 60-64, 65-74,75-79, 80+; Females aged 0-9, 10-19 dependents, 16-24 non-dependents, 25-29,30-34, 35-39, 40-44, 45-49, 50-59, 60-69, 70-74, 75-79, 80+ | Private household estimates. Department for Social Development in Northern Ireland. | |

| Households | Household estimates. Department for Social Development in Northern Ireland | ||

| Lone Parents | Lone Parent Estimates. Department for Social Development in Northern Ireland. | ||

| Households containing ‘Very Rich’ people | Pensioners, Non-pensioners | HMRC Survey of Personal Incomes (SPI) |

Adjustment for individuals with very high incomes

An adjustment is made to sample cases at the top of the income distribution to correct for volatility in the highest incomes captured in the survey. This adjustment uses data kindly supplied by HM Revenue and Customs’ statisticians from HM Revenue and Customs’ Survey of Personal Incomes (SPI) to control the numbers and income levels of the ‘very rich’ while retaining the FRS data on the characteristics of their households. The methodology defines a household as ‘very rich’ if it contains a ‘very rich’ individual and it adjusts pensioners and non-pensioners separately. Thresholds have been set at the level above which, for each group, the FRS data is considered to be volatile due to small numbers of cases.

From the FYE 2010 publication, the SPI adjustment methodology was changed to be based on adjusting a fixed fraction of the population rather than on adjusting the incomes of all those individuals with incomes above a fixed cash terms level. This is intended to prevent an increasing fraction of the dataset being adjusted. The adjustment fraction was set at the same level as the fraction adjusted in FYE 2009. There was also a movement to basing all SPI adjustment decisions on gross rather than a mixture of gross and net incomes. These changes only have a very small effect on the results as presented.

The numbers of ‘very rich’ pensioners and non-pensioners in survey estimates are matched to SPI estimates by the introduction of two extra control totals into the grossing regime. One is for the total number of pensioners above the pensioner threshold and the other for the number of non-pensioners above the non-pensioner threshold. The grossing factors for individual cases are only marginally changed as a result of this adjustment. In addition, each ‘very rich’ individual in the FRS is assigned an income level derived from the SPI, as the latter gives a more accurate indication of the level of high incomes than the FRS. Again this adjustment is carried out separately for pensioners and non-pensioners.

The latest SPI data available when we carried out our analysis was the FYE 2018 SPI, which was projected forward to cover the FYE 2020 Family Resources Survey year.

Equivalisation

HBAI uses net disposable weekly household income, after adjusting for the household size and composition, as an assessment for material living standards - the level of consumption of goods and services that people could attain given the net income of the household in which they live. In order to allow comparisons of the living standards of different types of households, income is adjusted to take into account variations in the size and composition of the households in a process known as equivalisation. HBAI assumes that all individuals in the household benefit equally from the combined income of the household. Thus, all members of any one household will appear at the same point in the income distribution.

The unit of analysis is the individual, so the populations and percentages in the tables are numbers and percentages of individuals – both adults and children.

Equivalence scales conventionally take an adult couple without children as the reference point, with an equivalence value of one. The process then increases relatively the income of single person households (since their incomes are divided by a value of less than one) and reduces relatively the incomes of households with three or more persons, which have an equivalence value of greater than one. The infographic below illustrates the process of equivalisation, Before Housing Costs.

Consider a single person, a couple with no children, and a couple with two children aged twelve and ten, all having unadjusted weekly household incomes of £300 (BHC). The process of equivalisation, as conducted in HBAI, gives an equivalised income of £448 to the single person, £300 to the couple with no children, but only £214 to the couple with children.

The main equivalence scales now used in HBAI are the modified OECD scales, which take the values shown in Table 3. The equivalent values used by the McClements equivalence scales are also shown for comparison alongside modified OECD values. The McClements scales were used by HBAI to adjust income up to the FYE 2005 HBAI publication.

In the modified OECD and McClements versions, two separate scales are used, one for income BHC and one for income AHC. The construction of household equivalence values from these scales is quite straightforward. For example, the BHC equivalence value for a household containing a couple with a fourteen-year-old and a ten-year-old child together with one other adult would be 1.86 from the sum of the scale values:

0.67 + 0.33 + 0.33 + 0.33 + 0.20 = 1.86

This is made up of 0.67 for the first adult, 0.33 for their spouse, the other adult and the fourteen-year-old child and 0.20 for the ten-year-old child. The total income for the household would then be divided by 1.86 in order to arrive at the measure of equivalised household income used in HBAI analysis.

Table 3: Comparison of modified OECD and McClements equivalence scales

| OECD rescaled to couple without Children=1 | OECD ‘Companion’ Scale to equivalise AHC results | McClements BHC | McClements AHC | |

|---|---|---|---|---|

| First Adult | 0.67 | 0.58 | 0.61 | 0.55 |

| Spouse | 0.33 | 0.42 | 0.39 | 0.45 |

| Other Second Adult | 0.33 | 0.42 | 0.46 | 0.45 |

| Third Adult | 0.33 | 0.42 | 0.42 | 0.45 |

| Subsequent Adults | 0.33 | 0.42 | 0.36 | 0.40 |

| Children aged under 14 years | 0.20 | 0.20 | 0.20 | 0.20 |

| Children aged 14 years and over | 0.33 | 0.42 | 0.32 | 0.34 |

Notes:

-

all scales presented to two decimal places

-

for the McClements scale, the weight for ‘Other second adult’ is used in place of the weight for ‘Spouse’ when two adults living in a household are sharing accommodation, but are not living as a couple. ‘Third adult and ‘Subsequent adult’ weights are used for the remaining adults in the household as appropriate. In contrast to the McClements scales, apart from for the first adult, the OECD scales do not differentiate for subsequent adults

-

The McClements scale varies by age for children; appropriate averages are shown in the table

Income Definition

The income measure used in HBAI is weekly net (disposable) equivalised household income. This comprises total income from all sources of all household members including dependants.

Income is adjusted for household size and composition by means of equivalence scales, which reflect the extent to which households of different size and composition require a different level of income to achieve the same standard of living. This adjusted income is referred to as equivalised income.

In detail, income includes:

-

usual net earnings from employment

-

profit or loss from self-employment (losses are treated as a negative income)

-

state support - all benefits and tax credits

-

income from occupational and private pensions

-

investment income

-

maintenance payments

-

income from educational grants and scholarships (including, for students, student loans and parental contributions)

-

the cash value of certain forms of income in kind (free school meals, free school breakfast, free school milk, free school fruit and vegetables, Healthy Start vouchers and free TV licence for those aged 75 and over)

Income is net of the following items:

-

income tax payments

-

National Insurance contributions

-

domestic rates / council tax

-

contributions to occupational pension schemes (including all additional voluntary contributions (AVCs) to occupational pension schemes, and any contributions to stakeholder and personal pensions)

-

all maintenance and child support payments, which are deducted from the income of the person making the payment

-

parental contributions to students living away from home

-

student loan repayments

Housing costs

Income After Housing Costs (AHC) is derived by deducting a measure of housing costs from the above income measure.

Housing costs include the following:

-

rent (gross of housing benefit)

-

water rates, community water charges and council water charges

-

mortgage interest payments

-

structural insurance premiums (for owner occupiers)

-

ground rent and service charges

For Northern Ireland households, water provision is funded from taxation and there are no direct water charges. Therefore, it is already taken into account in the Before Housing Costs measure.

In the FYE 1996 and subsequent datasets, a refinement was made to the calculation of mortgage interest payments to disregard additional loans which had been taken out for purposes other than house purchase.

Negative incomes

Negative incomes BHC are reset to zero, but negative AHC incomes calculated from the adjusted BHC incomes are possible. Where incomes have been adjusted to zero BHC, income AHC is derived from the adjusted BHC income.

State support

The Government pays money to individuals in order to support them financially under various circumstances. Most of these benefits are administered by DWP. The exceptions are Housing Benefit and Council Tax Reduction, which are administered by local authorities. Tax Credits are not treated as benefits, but both Tax Credits and benefits are included in the term State Support.

Income-related benefits for United Kingdom include:

-

Council Tax Reduction

-

Employment and Support Allowance (income-related element)

-

Extended Payments (Council Tax Reduction and Housing Benefit)

-

Housing Benefit

-

Income Support

-

Jobseeker’s Allowance (income-based element)

-

Pension Credit

-

Social Fund – Funeral Grant

-

Social Fund – Sure Start Maternity Grant

-

Universal Credit

Non-Income-related benefits for United Kingdom include:

-

Armed Forces Compensation Scheme

-

Attendance Allowance

-

Bereavement or Widowed Parent’s Allowance

-

Bereavement Support Payment

-

Carer’s Allowance

-

Child Benefit

-

Disability Living Allowance (both mobility and care components)

-

Employment and Support Allowance (contributory element)

-

Guardian’s Allowance

-

Incapacity Benefit

-

Industrial Injuries Disablement Benefit

-

Jobseeker’s Allowance (contributory element)

-

Maternity Allowance

-

Personal Independence Payment (Daily Living and Mobility components)

-

Severe Disablement Allowance

-

State Pension

-

Statutory Maternity/Paternity/Adoption Pay

-

Statutory Sick Pay

-

Winter Fuel Payments

Income-related benefits for Northern Ireland include:

-

Northern Ireland Other Rate Rebate

-

Northern Ireland Rate Rebate through energy efficient homes

-

Northern Ireland Rate Relief

-

Rates Rebate

Non-Income related benefits for Northern Ireland include:

-

Northern Ireland Disability Rate Rebate

-

Northern Ireland Lone Pensioner Rate Rebate

Interpreting low income measures

Relative low income

Relative low income sets the threshold as a proportion of the average income, and moves each year as average income moves. It is used to measure the number and proportion of individuals who have incomes a certain proportion below the average.

The percentage of individuals in relative low income will increase if:

-

the average income stays the same, or rises, and individuals with the lowest incomes see their income fall, or rise less, than average income; or

-

the average income falls and individuals with the lowest incomes see their income fall more than the average income

The percentage of individuals in relative low income will decrease if:

-

the average income stays the same, or rises, and individuals with the lowest incomes see their income rise more than average income; or

-

the average income falls and individuals with the lowest incomes see their income rise, or fall less, than average income, or see no change in their income

Absolute low income

Absolute low income sets the low income line in a given year, then adjusts it each year with inflation as measured by variants of the CPI. This measures the proportion of individuals who are below a certain standard of living in the UK (as measured by income).

The percentage of individuals in absolute low income will increase if individuals with the lowest incomes see their income fall or rise less than inflation.

The percentage of individuals in absolute low income will decrease if individuals with the lowest incomes see their incomes rise more than inflation.

Income inequality

Income inequality, measured by the Gini Coefficient, shows how incomes are distributed across all individuals, and provides an indicator of how high and low-income individuals compare to one another. It ranges from zero (when everybody has identical incomes) to 100 per cent (when all income goes to only one person). The 90:10 ratio is the average (median) income of the top 20 per cent (quintile 5) divided by the average income of the bottom 20 per cent (quintile 1). The higher the number, the greater the gap between those with the highest incomes and those with the lowest incomes.

Before Housing Costs (BHC)

Before Housing Costs (BHC) measures allow an assessment of the relative standard of living of those individuals who were actually benefiting from a better quality of housing by paying more for better accommodation, and income growth over time incorporates improvements in living standards where higher costs reflected improvements in the quality of housing.

After Housing Costs (AHC)

After Housing Costs (AHC) measures allow an assessment of living standards of individuals whose housing costs are high relative to the quality of their accommodation. Income growth over time may also overstate improvements in living standards for low-income groups, as a rise in Housing Benefit to offset higher rents (for a given quality of accommodation) would be counted as an income rise.

Therefore, HBAI presents analyses of disposable income on both a BHC and AHC basis. This is principally to take into account variations in housing costs that themselves do not correspond to comparable variations in the quality of housing.

Low income and material deprivation for children

Material deprivation is an additional way of measuring living standards and refers to the self-reported inability of individuals or households to afford particular goods and activities that are typical in society at a given point in time, irrespective of whether they would choose to have these items, even if they could afford them.

A suite of questions designed to capture the material deprivation experienced by families with children has been included in the FRS since FYE 2005. Respondents are asked whether they have 21 goods and services, including child, adult and household items. Together, these questions form the best discriminator between those families that are deprived and those that are not. If they do not have a good or service, they are asked whether this is because they do not want them or because they cannot afford them.

The original list of items was identified by independent academic analysis. See McKay, S. and Collard, S. (2004). Developing deprivation questions for the Family Resources Survey, Department for Work and Pensions Working Paper Number 13. The questions are kept under review and for the FYE 2011 Family Resources Survey, information on four additional material deprivation goods and services was collected and from FYE 2012 four questions from the original suite were removed.

The trends table 4.5tr available on the Children web page shows figures using the original suite of questions up to and including FYE 2011, and the new suite of questions from FYE 2011 onwards. FYE 2011 data is presented on both bases as figures from the old and new suite of questions are not comparable.

See Appendix 3 of the FYE 2011 HBAI publication for a discussion of the implications of changing the items.

A prevalence weighted approach has been used, in combination with a relative low-income or severe relative low-income threshold. Prevalence weighting is a technique of scoring deprivation in which more weight in the deprivation measure is given to families lacking those items that most families already have. This means a greater importance, when an item is lacked, is assigned to those items that are more commonly owned in the population.

For each question a score of 1 indicates where an item is lacked because it cannot be afforded. If the family has the item, the item is not needed or wanted, or the question does not apply then a score of 0 is given. This score is multiplied by the relevant prevalence weight. The scores on each item are summed and then divided by the total maximum score; this results in a continuous distribution of scores ranging from 0 to 1. The scores are multiplied by 100 to make them easier to interpret. The final scores, therefore, range from 0 to 100, with any families lacking all items which other families had access to scoring 100.

A child is considered to be in low income and material deprivation if they live in a family that has a final score of 25 or more and an equivalised household income below 70 per cent of contemporary median income, Before Housing Costs.

A child is considered to be in severe low income and material deprivation if they live in a family that has a final score of 25 or more and an equivalised household income below 50 per cent of contemporary median income, Before Housing Costs. A technical note giving further background to this measure is available.

From the FYE 2009 edition of the HBAI publication, we moved to using the prevalence weights relative to the survey year in question, rather than fixed FYE 2005 weights, which were used in previous publications. The prevalence weights are shown in Table 5 below.

Table 5: Material deprivation scores used for children in FYE 2019

| Material deprivation questions | Weights | Final Scores | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| For children | |||||||||||

| Outdoor space or facilities nearby to play safely | 0.936 | 5.61 | |||||||||

| Enough bedrooms for every child of 10 or over of a different sex to have their own bedroom | 0.846 | 5.07 | |||||||||

| Celebrations on special occasions such as birthdays, Christmas or other religious festivals | 0.965 | 5.79 | |||||||||

| Leisure equipment such as sports equipment or a bicycle | 0.887 | 5.32 | |||||||||

| A family holiday away from home for at least one week a year | 0.684 | 4.10 | |||||||||

| A hobby or leisure activity | 0.760 | 4.56 | |||||||||

| Friends around for tea or a snack once a fortnight | 0.667 | 4.00 | |||||||||

| Go on school trips | 0.889 | 5.33 | |||||||||

| Toddler group/nursery/playgroup at least once a week | 0.719 | 4.31 | |||||||||

| Attends organised activity outside school each week | 0.709 | 4.25 | |||||||||

| Fresh fruit and vegetables eaten by children every day | 0.931 | 5.58 | |||||||||

| Warm winter coat for each child | 0.986 | 5.91 | |||||||||

| For adults | |||||||||||

| Enough money to keep home in a decent state of decoration | 0.800 | 4.79 | |||||||||

| A holiday away from home for at least one week a year, whilst not staying with relatives at their home | 0.614 | 3.68 | |||||||||

| Household contents insurance | 0.665 | 3.99 | |||||||||

| Regular savings of £10 a month or more for rainy days or retirement | 0.667 | 4.00 | |||||||||

| Replace any worn out furniture | 0.639 | 3.82 | |||||||||

| Replace or repair major electrical goods such as a refrigerator or a washing machine, when broken | 0.725 | 4.32 | |||||||||

| A small amount of money to spend each week on yourself, not on your family | 0.719 | 4.40 | |||||||||

| In winter, able to keep accommodation warm enough | 0.925 | 5.61 | |||||||||

| Keep up with bills and regular debt payments | 0.919 | 5.57 | |||||||||

| Sum of all weights | 16.679 | 100 |

Material deprivation for pensioners

A suite of questions designed to capture the material deprivation experienced by pensioner families has been included in the Family Resources Survey since May 2008. Respondents are asked whether they have access to 15 goods and services. The list of items was identified by independent academic analysis. See Legard, R., Gray, M. and Blake, M. (2008), Cognitive testing: older people and the FRS material deprivation questions, Department for Work and Pensions Working Paper Number 55 and McKay, S. (2008), Measuring material deprivation among older people: Methodological study to revise the Family Resources Survey questions, Department for Work and Pensions Working Paper Number 54. Together, these questions form the best discriminator between those pensioner families that are deprived and those that are not. Note that this measure is only available for pensioners aged 65 or over.

Where they do not have a good or service, they are asked whether this is because:

-

they do not have the money for this

-

it is not a priority on their current income

-

their health or disability prevents them

-

it is too much trouble or tiring

-

they have no one to do this with or help them

-

it is not something they want; it is not relevant to them

-

other

A pensioner is counted as being deprived of an item where they lack it for one of the following reasons:

-

they do not have the money for this

-

it is not a priority on their current income

-

their health or disability prevents them

-

it is too much trouble or tiring

-

they have no one to do this with or help them

-

other

The exception to this is for the unexpected expense question, where the follow up question was asked to explore how those who responded ‘yes’ would pay. Options were:

-

use own income but cut back on essentials

-

use own income but not need to cut back on essentials

-

use savings

-

use a form of credit

-

get money from friends or family

-

other

Pensioners are counted as materially deprived for this item if and only if they responded ‘no’ to the initial question.

The same prevalence weighted approach has been used to that for children, in determining a deprivation score. Prevalence weighting is a technique of scoring deprivation in which more weight in the deprivation measure is given to families lacking those items that most pensioner families already have. This means a greater importance, when an item is lacked, is assigned to those items that are more commonly owned in the pensioner population.

For each question a score of 1 indicates where an item is lacked because of the reasons outlined on the previous page. If the pensioner family has the item, the item is not needed or wanted, or the question does not apply then a score of 0 is given. This score is then multiplied by the relevant prevalence weight. The scores on each item are summed and divided by the total maximum score; this results in a continuous distribution of scores ranging from 0 to 1. The scores are multiplied by 100 to make them easier to interpret. The final scores, therefore, range from 0 to 100, with any families lacking all items which other families had access to scoring 100. The prevalence weights are shown in Table 6 below.

Table 6: Material deprivation scores used for pensioners in FYE 2019

| Material deprivation questions | Weights | Final Scores | |||||

|---|---|---|---|---|---|---|---|

| For pensioners aged 65 and over | |||||||

| At least one filling meal a day | 0.987 | 7.14 | |||||

| Go out socially at least once a month | 0.813 | 5.88 | |||||

| See friends or family at least once a month | 0.952 | 6.89 | |||||

| Take a holiday away from home | 0.612 | 4.42 | |||||

| Able to replace cooker if it broke down | 0.920 | 6.65 | |||||

| Home kept in a good state of repair | 0.968 | 7.00 | |||||

| Heating, electrics, plumbing and drains working | 0.984 | 7.12 | |||||

| Have a damp-free home | 0.952 | 6.88 | |||||

| Home kept adequately warm | 0.976 | 7.06 | |||||

| Able to pay regular bills | 0.982 | 7.10 | |||||

| Have a telephone to use, whenever needed | 0.954 | 6.90 | |||||

| Have access to a car or taxi, whenever needed | 0.915 | 6.62 | |||||

| Have hair done or cut regularly | 0.918 | 6.64 | |||||

| Have a warm waterproof coat | 0.991 | 7.17 | |||||

| Able to pay an unexpected expense of £200 | 0.904 | 6.54 | |||||

| Sum of all weights | 13.826 | 100 |

A pensioner is considered to be in material deprivation if they live in a family that has a final score of 20 or more. For children, material deprivation is presented as an indicator in combination with a low-income threshold. However, for pensioners, the concept of material deprivation is broad and very different from low income, therefore it is appropriate to present it as a separate measure.

A technical note giving a full explanation of the pensioner material deprivation measure is available.

Material deprivation weighting methodology

We currently recalculate the prevalence weights each year based on the question responses from that year. The maximum possible material deprivation score for each year is then rescaled to 100 for ease of interpretation, and children in a family with a score of at least 25, or pensioners with a score of 20 or more, are classed as being materially deprived. If over time more families can afford a certain item, then a family lacking such a good will see an increasing overall deprivation score, and will be considered as becoming more materially deprived.