Tackling abuse and mismanagement 2014-15 - full report

Published 17 December 2015

Applies to England and Wales

© Crown copyright 2015

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/tackling-abuse-and-mismanagement-2014-15/tackling-abuse-and-mismanagement-2014-15-full-report

1. Introduction

1.1 Foreword from William Shawcross

Public trust in charities is high, but must never be taken for granted. Most charity trustees take their legal duties and responsibilities seriously. Only a small proportion of the 165,000 charities on our register ever become subject to an investigation or compliance case. Abuse or non-compliance of any kind in just one charity, however, can damage public trust in and the reputation of the entire charitable world, whether the abuse is deliberate or arises through mismanagement or neglect. The intense focus on charities over the course of this summer, caused by the exposure of shocking fundraising practices, and the collapse of some high-profile organisations, demonstrated how confidence can be affected.

William Shawcross Chairman, Charity Commission

A PDF version of the full foreword is available for download.

1.2 About the Charity Commission

The commission is the independent regulator of charities in England and Wales. Our role is to protect the public’s interest in charities and ensure that charities further their charitable purposes for the public benefit and remain independent from private, government or political interests. Parliament has given us 5 statutory objectives, and a wide discretion as to how to fulfil them. Our 5 objectives are to:

- increase public trust and confidence in charities

- promote awareness and understanding of the operation of the public benefit requirement

- promote compliance by charity trustees with their legal obligations in exercising control

- promote the effective use of charitable resources

- enhance the accountability of charities to donors, beneficiaries and the general public

An important part of our role is to prevent serious problems from arising in the first place, by providing online guidance that helps trustees understand and meet their legal duties and responsibilities in managing their charities.

Our strategic plan for 2015-18 explains how we will go about fulfilling our objectives over the next 3 years.

1.3 How we are strengthening our approach to tackling abuse and mismanagement

Our general approach to dealing with concerns about charities, including an explanation of the powers available to us, is explained in Annex 1, The Charity Commission’s approach to tackling abuse and mismanagement. You can read about the different kind of cases we can conduct into charities in Annex 2- Glossary.

We have significantly strengthened our work to prevent and stop abuse and mismanagement in charities over recent years. For example, we have:

- strengthened our registration processes to ensure that where we have concerns about a charity but are legally required to register it [footnote 1], our concerns are followed up after the charity is registered

- improved the way we proactively monitor charities that fall into certain risk categories and last year opened over 400 new monitoring cases

- significantly increased the number of inquiries into charities; in 2014-15, we opened 103 new investigations, compared to 15 in 2012-13

- started using our powers more swiftly, robustly, and effectively for example to require evidence on oath or require attendance in person, to freeze bank accounts or to remove or suspend trustees; last year, we used our powers on 1,200 occasions, compared to 216 in 2012-13

- carried out more proactive inspection and compliance visits

- improved our use of data to assess and respond to risks facing charities, for example by joining the fraud prevention service Cifas; since joining the service, we use it as an additional check on individual cases of concern and in 2014-15, we used it on over 200 occasions to identify matters requiring further scrutiny

- become more transparent about acting in the public interest, including by announcing new statutory inquiries, unless there are public interest reasons not to, and marking charities’ online register entries so that the public can identify charities under investigation

- engaged with charities that had previously reported serious incidents, to seek assurances that they have since acted on the regulatory advice we had given

- begun conducting themed reviews of charity accounts to monitor their compliance with reporting requirements, to promote high quality financial reporting and to identify concerns

You can read more about the ways in which we are becoming a more robust and proactive regulator in our Annual report for 2014-15 .

More recently, we have taken further steps to protect charities, by:

- convening a new Safeguarding Advisory Group, to help us ensure our work is joined up with that of the statutory bodies responsible for safeguarding vulnerable people

- building on a highly successful first national charity fraud conference hosted jointly with the Fraud Advisory Panel, we will explore the scope to host similar future events to raise awareness of fraud risks and good practice amongst charities

- launching a new Charity Sector Counter Fraud Group, bringing together charities, professional bodies and other key stakeholders to tackle current and emerging charity fraud threats; initial activities will focus on enhancing the professionalism of charities’ responses to fraud risks, including cyber fraud

- launching a consultation on allowing charities to file their annual accounts in a digital form (iXBRL), which in time will make it easier for the public to compare data about charities, and for us to identify patterns that may give rise to concern

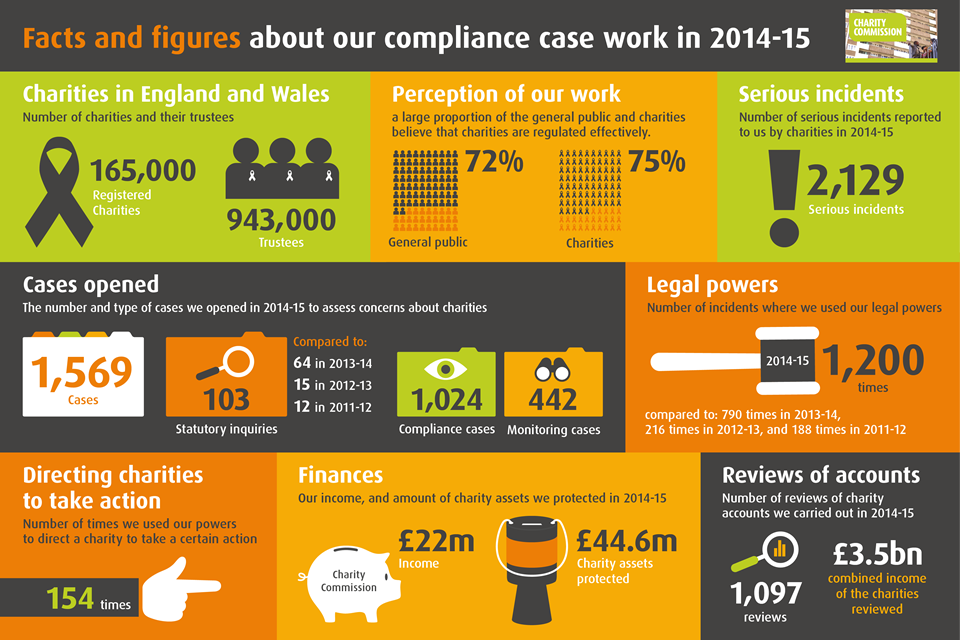

1.4 Key figures from our compliance case work in 2014-15

Charities in England and Wales

165,000 registered charities

943,000 trustees

Perception of our work

72% of the general public and 75% of charities believe that charities are regulated effectively.

Serious incidents

2,129 serious incidents reported to us by charities.

Cases opened

We opened 1,569 cases:

- 1,024 compliance cases

- 442 monitoring cases

- 103 statutory inquiries (compared to 64 in 2013-14, 15 in 2012-13 and 12 in 2011-12)

Legal powers

We used our legal powers 1,200 times. Compared to 790 times in 2013-14, 216 times in 2012-13 and 188 in 2011-12.

Directing charities to take action

We used our powers to direct a charity to take a certain action 154 times.

Finances

Charity Commission income: £22 million

Charity assets protected: £44.6 million

Reviews of accounts

We carried out 1,097 reviews of charity accounts in 2014-15. The combined income of the charities reviewed was £3.5 billion.

A PDF version of the Key figures from our compliance case work in 2014-15 is available for download.

For more statistical information about our compliance case work, see Annex 3, Statistical Analysis 2014-15.

2. Types of abuse and mismanagement

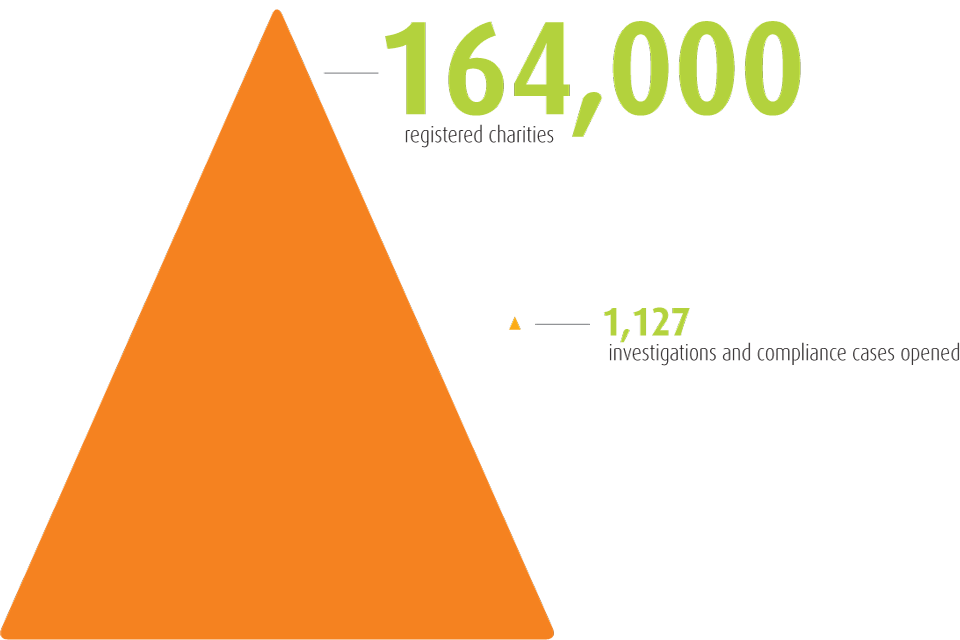

Only a small proportion of registered charities ever become subject to a compliance case or investigation by the commission. There are 164,000 charities but 1,127 investigations and compliance cases opened. But all charities can be vulnerable to abuse or mismanagement if their trustees have not put in place robust systems to protect their charity from harm.

This section sets out the types of abuse and mismanagement that occur in charities and links to case study examples of our case work in these areas.

The commission has identified 3 strategic risks facing charities:

- fraud, financial crime and financial abuse

- safeguarding issues

- abuse of charities for terrorist related purposes

Not all of these issues occur frequently in charities – but when they do occur, they can cause devastating damage, not just to the individual charity in question, but to wider public trust and confidence in the charitable sector. You can read about our strategic approaches to high-risk areas on the GOV.UK website.

In the following short video, Michelle Russell, the commission’s Director of Investigations, Monitoring and Enforcement explains the work of her teams and introduces key themes of the report.

2.1 Financial mismanagement and financial crime

Managing your charity’s resources responsibly is 1 of the 6 key duties of charity trustees, as explained in our core guidance, The essential trustee (CC3).

This duty means trustees must make sure the charity’s assets are only used to support its purposes and must avoid exposing the charity’s assets to undue risk.

Our case work shows that, too often, trustees fail to manage their charity’s resources responsibly, making the charity vulnerable to problems: financial mismanagement, financial abuse or financial crime are among the most frequent issues of concern arising in our case work.

Not all cases of financial mismanagement involve criminality. But when we uncover evidence of potential crime, we always share it with the police, and often work closely with them to help bring people who have committed crimes against charities to justice.

See our strategy for charity fraud, financial crime and financial abuse for more detail.

All types of financial abuse have the potential to be highly destabilising for the charity affected. Monetary losses only form part of the damage; financial abuse often causes wider harm, including to the charity’s reputation, and to morale among staff and volunteers.

Reporting serious incidents

Trustees must respond appropriately when problems do occur, including by making a serious incident report to us and taking steps to avoid a similar problem from occurring in future. In the following video, David Walker, Head of Investigations Development and Outreach, explains why it is in your charity’s interest to report serious incidents to the commission.

Case studies

The case studies below demonstrate the harm that can arise when trustees fail to put effective financial controls in place and the serious risks arising from individual trustees having inappropriate control over their charities finances.

Helping Hands for the Needy – statutory inquiry

We use our powers to restrict the charity’s bank accounts and suspend a trustee; our investigation concludes that significant sums of the charity’s money had been misused.

Children’s Cancer and Leukaemia Fund - monitoring case

Our proactive examination of this newly registered charity’s finances helps to bring a fraudster, who used the charity’s funds for personal gain, to justice.

Bethel United Church of Jesus Christ Apostolic UK – compliance case

We ensure that trustees improve the charity’s financial management after £190,000 was misappropriated by a former trustee, who was later convicted.

Academy for Talmudical Research – statutory inquiry

We ensure this charity accounts to the public for its income, after it failed to submit annual accounts for 2 consecutive financial years.

Case work statistics

In 2014-15 concerns about financial abuse and/or financial mismanagement featured in:

- 60 completed pre-investigation assessment cases

- 42 completed investigations (statutory inquiries and regulatory compliance cases)

- 398 completed operational compliance cases

In 2014-15 concerns about fraud and/or theft or the misapplication of funds featured in:

- 417 serious incidents reported by charities to the commission

- 255 completed operational compliance cases

What we do when we uncover financial abuse or mismanagement

Our role as regulator is to ensure that:

- trustees comply with their legal duty to manage their charity’s resources responsibly

- any financial abuse or mismanagement uncovered stops

- the trustees take steps to ensure the problems do not recur in the future

We always refer suspected criminality to the police or other law enforcement agencies to investigate and we work closely with them to bring fraudsters to justice.

As the case studies above make clear, our precise response will depend on the specific nature and level of concerns in each case, including the ability and willingness of trustees to take steps to put matters right.

If trustees do cooperate and are able to respond appropriately, our role might involve setting an action plan requiring the trustees, for example, to carry out a review or introduce new financial controls within a certain timeframe.

However, in some cases, someone in the charity, perhaps a trustee, may be implicated in deliberate or reckless abuse and in the most serious cases we may need to use our formal legal powers to protect the charity from further harm.

The case studies in this section exemplify the range of responses we might make. For an overview of our regulatory approach and powers, see Annex 1, The Charity Commission’s approach to tackling abuse and mismanagement.

What we do to prevent financial abuse and poor financial management in charities

As well as responding to concerns that arise in charities, and producing and updating online guidance for trustees, we are proactive in helping to prevent problems arising in the first place.

For example, we conduct themed reviews of charity accounts to monitor their compliance with reporting requirements, to promote high quality financial reporting and to identify concerns.

We also undertake proactive monitoring of charities that show certain risk factors; for example, last year, we undertook a project to review newly registered charities that had entered relationships with third party fundraising companies, as our experience shows these relationships can cause financial problems for charities. We have also proactively monitored charities that had reported receiving no income and making no expenditure, as this information could suggest the charity is either not operating and should come off the register, or is not properly reporting its accurate financial status.

How to ensure strong financial management mismanagement in your charity and help prevent against fraud and abuse

There are steps you and your fellow trustees can and should take to avoid poor decisions and accidental errors and to help protect the charity’s funds, which in turn helps protect a charity against financial crime such as theft or fraud :

- set a business plan and budget and keep track of income and spend against it

- have robust and effective financial controls in place including robust but proportionate policies and procedures about managing income and controlling expenditure

- ensure you and your charity’s senior management create the right culture, leading by example in adhering to the charity’s internal financial controls and good practice

- keep up-to-date and accurate records of all income and expenditure

- ensure trustees receive up to date, accurate and regular information about the charity’s finances

- prepare annual accounts and ensure they are audited and filed with the commission as required by law

- put in place appropriate safeguards for the protection of money, assets and staff if the charity operates outside of the UK

You can find more detailed information in our published guidance:

- The essential trustee (CC3)

- Internal financial controls (CC8) and accompanying checklist

- Charity reporting and accounting – the essentials

- Charity Finance Group Charity fraud guide

- Fraud and financial crime – chapter 3 of the online compliance toolkit, Protecting charities from harm

2.2 Concerns about safeguarding

Many charities work with children or with adults who are vulnerable because of their age, health, or their physical or mental abilities. The public rightly expects charities to be safe and secure places. When abuse against vulnerable people takes place within a charity, it not only harms the individual in question, but can result in a breakdown of hard-won trust in a charity.

Trustees have a duty of care to their charity. If you are a trustee of a charity working with vulnerable groups including children, this duty includes taking the necessary steps to safeguard and take responsibility for them. You must also make sure that, if an incident does occur, you deal with it quickly and responsibly.

Our role as regulator

We do not administer child protection legislation and we do not investigate individual instances of abuse – that is for the police and safeguarding authorities to lead on. Our role focuses on the work of trustees and the steps they take to protect the charity and its beneficiaries and comply with their duty to manage their charity responsibly.

See our strategy for dealing with safeguarding matters for more information.

Unfortunately, our case work shows that some trustees fail to put in place and implement the necessary policies and take the appropriate steps to protect children and vulnerable people and discharge their duty of care. The following case studies show what can go wrong when trustees do not take adequate steps, or do not respond appropriately when concerns have arisen.

Case studies

Hinckley Concordia – statutory inquiry

We ensure new trustees significantly strengthen the charity’s safeguarding policies and procedures, after finding that 2 former trustees knew the charity was employing someone with criminal convictions that would affect their suitability from a safeguarding perspective and failed to deal responsibly and appropriately with the matter.

Southwark Muslim Women’s Association – monitoring case

We step in to ensure trustees tighten governance, after an employee was convicted for historic sexual offences against minors – a fact that the trustees should have, but did not, report to us as a serious incident.

Poverty reduction charity – compliance case

We ensure the trustees addressed serious weaknesses in their safeguarding arrangements, after an employee broke restrictions on their activity following a conviction for sex offences.

Case work statistics

In 2014-15 concerns about current or historic safeguarding featured in:

- 1,042 reports of serious incidents

- 8 whistleblowing reports

- 151 operational compliance cases

- 14 completed pre-investigation assessment cases

- 6 completed investigations

- 2,350 disclosures took place between us and other agencies about charity related queries; of these, 437 related to fraud, money laundering or theft

What we do when we uncover safeguarding concerns

Concerns that an offence may have been committed are matters for the police. We do not investigate individual allegations of abuse or criminal harm. If we identify such concerns, we will always share the information with the police and relevant safeguarding authorities and work closely with other agencies to help protect the charity’s assets and reputation.

Our role is to ensure trustees comply with their duty to manage their charity’s resources carefully, which includes a duty of care and the need to avoid exposing the charity’s beneficiaries to undue risk. We also work to help ensure trustees know how to respond appropriately to concerns when they arise.

For more detail on our work to prevent and tackle concerns about safeguarding in charities, read our Strategy on safeguarding.

How we help ensure that safeguarding concerns are taken seriously in charities

Trustees of charities set up to work with children or vulnerable people are required to make a declaration, when the charity registers, that they have undergone a DBS check (Disclosure and Barring Service - previously CRB) and are suitable to serve on the board of a charity working with vulnerable beneficiaries.

A recent court case demonstrates how seriously the courts take it when people lie to us in their declarations.

Reviewing our safeguarding strategy and guidance for charities

We recently convened a new Safeguarding Advisory Group, bringing experts together from statutory agencies, charities and other organisations with specialist experience in safeguarding children and vulnerable adults. The group has given valuable advice on our current practice and ensuring our work is joined up with that of the statutory bodies responsible for safeguarding vulnerable people. With this group’s input, we are reviewing our strategy and guidance for charities on safeguarding to ensure that it reflects recent developments in safeguarding law and practice, including the findings of the Jimmy Savile inquiries, and signposts trustees to the relevant statutory guidance.

How to protect children and other vulnerable beneficiaries of your charity

Trustees have a duty of care towards their charity, which means that those whose charities work with vulnerable beneficiaries must take steps to protect them from harm. This involves putting in place internal procedures and policies that act as safeguards against abuse.

For example, a charity that works with children should

- have a child protection policy – a statement explaining how the charity protects children from harm

- have effective whistle-blowing procedures to ensure concerns can be raised

- put in place child protection processes which give clear, step-by-step guidance if abuse is identified

- carry out the appropriate level of DBS checks on staff, volunteers and trustees

- have policies and procedures to help prevent abuse happening in the first place, including around adult workers with one-to-one access to vulnerable people

Did you know?

Safeguarding induction training is now mandatory for all those who work directly with children, young people, their families and or their carers.

You can find further information about how to comply with safeguarding legislation and fulfil your duties as trustee in the guidance:

2.3 Abuse for terrorist related purposes

Charities and their work can provide important protection against extremism and terrorism. Schools, for example, can play a vital role in preparing young people to challenge extremism and the ideology of terrorism. Similarly, faith organisations can challenge ideology that claims religious justification for terrorism. Civil society, of which charities are a key part, is also an important place for the free exchange of views and debate which can inhibit propagandists of extremism and terrorism. This is why it is so important for us, and other government agencies, to collaborate meaningfully and effectively with charities and civil society on these issues.

However, some charities, like other types of organisations, can be at risk of being used for radicalisation and abused by extremists and terrorist groups. The level of risk facing individual charities will depend on the nature of their work and on where and how in the world they operate. If your charity provides aid in conflict zones, the risks may involve working in or close to areas in which armed or terrorist groups operate.

As the humanitarian crisis in Syria has unfolded over the last few years, charities have been involved in delivering critical humanitarian aid and relief to those in need. Some people were motivated to go to conflict zones themselves as volunteers to assist, sometimes travelling on aid convoys. Many have good intentions, but some have used convoys as a means of moving people, funds and material for other motives. Some individuals did not return from Syria at the same time as their colleagues and may have been recruited by terrorist groups. We do not condone or support the use of aid convoys as an effective or safe way to deliver aid, and have issued alerts warning of the risks.

Whether your charity uses convoys, has staff on the ground or works through local partners, you as a trustee carry an important responsibility in ensuring that money and goods can be accounted for and reach those they are intended for, and do not get into the hands of others, including terrorist groups or used for terrorist purposes.

Our role in preventing and tackling the abuse of charity for terrorist purposes

Terrorist acts, the funding of and support for terrorist groups and activities are criminal matters. Whenever we identify concerns about possible terrorist-related issues, we work with the police and other agencies.

Our role as regulator is to help ensure trustees comply with charity law duties, take steps to protect their charities from being misused and to ensure that charity funds and property are used and applied properly.

See our counter-terrorism strategy for more information.

Charities working in the UK can also be vulnerable to abuse. People with extremist views, who encourage and support terrorism and terrorist ideology, have used charity events to make those views known, or used charities to promote or distribute extremist views or literature, including through online media. This can take various forms, such as through the use of a charity’s premises, through speakers at charity events, or use of a charity’s reach through internet use and social networking.

Activities may be carried out by someone involved in or connected to a charity, by individuals outside of it, or by other organisations. As trustees, you must protect your charity against such abuse. Charity law does not prevent charities, when furthering their lawful purposes, from promoting or supporting views that are controversial. But if your charity gives a platform, in whatever way, to radical and extremist views, you may be failing to fulfil your charity’s purposes for the public benefit and may be breaking the law.

Ensuring your charity carries out its purposes for the public benefit is 1 of the 6 key duties of charity trustees, as explained in our core guidance, The essential trustee (CC3).

Did you know?

Trustees must avoid activities that may place their charity’s funds, assets or reputation at undue risk.

Case study

Concerns were raised with us about a charity’s use of external guest speakers at its events. We advised the charity’s trustees about findings of our own research into individuals the charity had invited to one of its future events. We questioned whether the individuals in question were suitable to take part in the charity’s event because of comments attributed to them. We asked the trustees whether they had undertaken any due diligence before inviting the speakers and whether they had fully considered whether it was in the charity’s best interests for the individuals to take part. The trustees considered this and, in response to our concerns, revoked the invitations to the guest speakers concerned. We reviewed the charity’s policies and procedures for carrying out due diligence on invited guest speakers and the controls the charity had in place to manage events at which external speakers are invited. We found a number of weaknesses in the charity’s systems and provided the trustees with regulatory advice and guidance to help them better protect the charity from the risk of abuse arising from hosting external speakers. We will monitor the actions taken by the trustees in response to the regulatory advice and guidance we provided.

Case work statistics

In 2014-15, allegations made and concerns about abuse of charities for terrorist or extremist purposes, including concerns about charities operating in Syria and other higher risk areas, in which terrorist groups operate, featured in:

- 11 reports of a serious incident

- 32 pre-investigation assessment cases[footnote 2]

- 20 investigations[footnote 3]

We also carried out 80 visits and/or monitoring cases during the year to charities which are of greater risk and more susceptible to risk of terrorist or extremist abuse because of where they operate (eg in conflict zones) or due to their activities (eg because they regularly invite speakers to charity events). These were proactively identified by us, or identified as a result of serious incident reports, complaints, or concerns raised in the media.

Of the 11 serious incidents reported to us in 2014-15 that involved concerns about abuse of charities for terrorist or extremist purposes, 2 came from charities whose staff members or goods had been detained by terrorist groups.

- 2,350 disclosures took place between us and other agencies about charity related queries; of these, 506 related to terrorism and extremism queries or with agencies working with charities most affected by these risks

What we do to help charities prevent and protect themselves against terrorist-related abuse and how we respond to concerns raised

Our Counter-terrorism strategy explains our role and approach in the context of terrorist-related abuse of charities. We are not a criminal regulator, so it is not for us to investigate alleged crimes. But we have an important role in helping charities to prevent abuse from occurring in the first place, and in ensuring abuse is reported, stopped and the charity is better protected in the future.

We very much see this as a collaborative role. For example, we proactively work with charities working in high risk areas around the world, to help trustees understand how to prevent their charity’s assets being diverted or their reputations being harmed and pass on best practice in due diligence and monitoring.

We recently issued an alert to charities reminding them of the need to report any suspicions that their funds or assets may have been diverted to terrorist groups to the police, and to us. We did this because charities are telling us when we meet with them in our outreach work and inspection visits, that they are not aware of this legal duty. It is also important the public understand the difficult circumstances and increasing risks in which some charities operate. In some cases their staff and volunteers risk their lives to deliver humanitarian aid in hard to reach places.

How to protect your charity against abuse for terrorist related purposes

We expect trustees to be vigilant to ensure that their charity’s facilities, assets, staff, volunteers and other resources cannot be used for activities that may, or appear to, support or condone terrorist or extremist activities. The normal steps you take to ensure good governance and strong financial management will help protect you against all kinds of abuse, including this. So as a trustee, you need to consider what procedures should be put in place to prevent others from taking advantage of your charity. What that means in practice will depend on your charity’s individual circumstances. Trustees should also take all necessary steps to ensure their activities or views promoted cannot be misinterpreted.

You can find further information about how to protect your charity in our published guidance:

- Charities and terrorism – chapter 1 of the online compliance toolkit, ‘Protecting charities from harm’

- Protecting charities from abuse for extremist purposes and managing the risks at events and in activities – chapter 5 of the online compliance toolkit, ‘Protecting charities from harm’

- Due diligence monitoring and end use of funds – chapter 2 of the online compliance toolkit, ‘Protecting charities from harm’

- Holding moving and receiving funds safely in the UK and internationally – chapter 4 of the online compliance toolkit, ‘Protecting charities from harm’

- Regulatory alert reminding trustees of the requirement under section 19 of the Terrorism Act 2000 to report certain terrorist financing offences

2.4 Serious governance failures

Resulting in unmanaged conflicts of interest, unauthorised trustee benefits, breaches of governing document and other serious problems

A significant proportion of serious concerns we encounter result from a basic failure of trustees to fulfil their 6 key duties, leading to poor governance. Good governance is not an ‘optional extra’ in a charity. Without it, trustees put their charities at serious risk of abuse and also risk harming the quality of service the charity offers to beneficiaries.

Did you know?

Deliberate abuse is more likely to occur and less likely to be detected in a charity with poor governance.

The importance of collective decision making

Good, collective trustee decision making is at the heart of good governance. Good decision making involves, among other things, acting in good faith and exclusively in the charity’s interests, acting within your powers, managing conflicts of interest, informing yourself properly and seeking appropriate advice where relevant.

Our casework shows that a breakdown of collective decision making by charity boards is often at the root of poor governance and serious mistakes or indeed mismanagement. Sometimes, this breakdown occurs because individuals or groups of individuals – often including staff members – become too dominant and make decisions that are for the board as a collective body to make.

In the following short video, Richard Black, senior caseworker at the commission, explains why it spells problems for a charity if a small group of individuals become too dominant – and how to prevent this from happening in your charity.

Sometimes, dominant individuals have ulterior motives and go on to abuse a charity for personal gain. Sometimes they use an opportunity they have been given because no-one challenges them or they have too much control for their own advantage or gain. But that is not always the case; sometimes, the individuals in question mean well in their work for the charity. But as some of the following case studies demonstrate, it is never healthy for strategic decisions to be made without the active involvement of the full board.

Concerns around unauthorised personal benefit

Another serious governance problem we see too often is unauthorised private benefit. This arises when a trustee or someone connected to a trustee – for example a family member – benefits from their charity in a way that is not appropriate and/or not authorised. This authorisation must be either by:

- the charity’s governing document

- the commission

- the courts

Even when personal benefits are authorised, it is important that trustees manage any resulting conflict of interest carefully. For example, if a trustee benefit relates to services that the trustee’s company provides at a competitive rate to the charity, it is important to ensure that the trustee in question does not take part in discussions or decisions about whether and on what terms that arrangement should be continued.

Not all cases of unauthorised personal benefit involve deliberate abuse. Sometimes, the problem arises from good intentions, and the charity in fact benefits from the arrangement, perhaps because it receives goods or benefits at a discount. But even in such situations, the law is clear that if a benefit is not authorised, the trustee in question may need to account for their profit and repay the sums involved, which is why it is so important to ensure that any benefits you receive are authorised.

A charity’s reputation can also be seriously damaged if trustees are seen to act outside their powers or take advantage of their position in a charity in granting themselves personal benefits.

In the following short video, Harvey Grenville, who leads one of the commission’s investigation teams, explains what unauthorised personal benefits are – and why they can lead to serious problems.

Case studies

Air Ambulance Service – compliance case

Our involvement ensures the trustees improve their oversight of the charity, after concerns were raised with us about a failed fundraising event and a significant loan to a staff member.

Police Dependants’ Trust– compliance case

We set the trustees an extensive action plan, after identifying weaknesses in the charity’s governance and in collective decision making by the trustees.

Holmewood Animal Rescue Charitable Trust – monitoring case

Our proactive case ensures the trustees address concerns about the charity’s management that we had identified at registration stage.

House the Homeless– compliance case

We get involved to ensure the charity addresses concerns about alleged conflict of interest.

Raleigh Limited – statutory inquiry

Among other outcomes, our investigation ensures the charity recovers money that had been expended on unauthorised private benefit.

Whitehorse Stables – statutory inquiry

Our investigation ensures the trustees take steps to manage conflicts of interest and improve accounting procedures.

Khalsa Centre – statutory inquiry

We appoint an interim manager to protect the charity’s assets and interests, and to restore adequate governance after identifying serious risks to the charity resulting from an ongoing dispute.

Society Network Foundation – compliance case

We identify concerns about the charity’s use of restricted funds for general charitable purposes; the charity notified us during our case that it was winding up.

Case work statistics

In 2014-15 serious governance concerns featured in:

- 130 reports of serious incidents

- 72 whistleblowing reports

- 5 completed pre-investigation assessment cases

- 2 completed investigations

Concerns about mismanagement or maladministration featured in:

- 58 completed operational compliance cases

- 13 completed pre-investigation assessment cases

- 41 completed investigations

General concerns about poor governance featured in:

- 113 completed operational compliance cases

Concerns about unmanaged conflicts of interest and/or trustee benefits featured in:

- 3 completed pre-investigation assessment cases

- 3 completed investigations (statutory inquiries and regulatory compliance cases)

- 53 completed operational compliance cases

Concerns about breaches of governing document featured in:

- whistleblowing reports

- 55 completed operational compliance cases

What we do to prevent and tackle serious governance concerns

Enabling trustees to run their charities in line with the law is 1 of the 4 priorities set out in our strategic plan 2015-18.

We are becoming more proactive in raising awareness of and ensuring trustees understand their legal duties and responsibilities, for example through the review and extensive dissemination of our core guidance for trustees, The essential trustee. For example, we conduct monthly social media campaigns focused around specific areas of charity management or trustee responsibility. We also issue a quarterly newsletter to all trustees for whom we hold email addresses.

How we respond to incidents of poor governance depends on individual circumstances; we take a risk-based and proportionate approach: often, trustees recognise that poor governance or failures on their part have brought about problems and are eager to work with us to put matters right. However, when trustees have been negligent leading to significant loss to the charity or are unwilling or unable to respond appropriately, we do not shy away from using our powers to protect the charity. The case studies above demonstrate the range of responses we can make to governance failures in charities.

How to prevent serious governance failures arising in your charity

You can dramatically reduce the risk of serious mismanagement or abuse occurring in your charity by fulfilling your 6 key duties and putting robust governance controls in place.

The 6 key duties of trustees are:

- ensure your charity is carrying out its purposes for the public benefit

- comply with your charity’s governing document and the law

- act in your charity’s best interests

- manage your charity’s resources responsibly

- act with reasonable care and skill

- ensure your charity is accountable

The essential trustee (CC3) explains what these duties mean in practice.

You also find further information in our other governance guidance:

- Hallmarks of an effective charity (CC10)

- It’s your decision: charity trustees and decision making (CC27)

- Conflicts of interest (CC29)

- Managing charity assets and resources (CC25)

- Reporting serious incidents – guidance for trustees

2.5 Concerns about charities’ independence

By definition, charities cannot have a political purpose. This is one aspect of ensuring a charity’s independence. To be a charity, an organisation must be established for exclusively charitable purposes for the public benefit. This is a fundamental principle of charity law, and it is trustees’ responsibility to ensure their charity carries out its purposes for the public benefit.

Campaigning and political activity can be a valuable way for charities to support the delivery of their charitable purposes. But political activity alone cannot become an end in itself, that is to say the sole reason for the charity’s existence. Trustees must also ensure they protect their charity’s independence, ensuring that any involvement it has with political parties is balanced.

Trustees must not use the charity as a vehicle to express their own personal views, political or otherwise. They must act exclusively in the best interests of the charity.

Charities must be especially careful in the run-up to an election.

Did you know?

Charities must never give support or funding to a political party, a candidate or politician.

Concerns about charities’ campaigning or political activity do not arise very frequently in our case work, but when they do arise, they can be by nature high profile and have the potential to undermine public understanding of and trust in charity.

This year, we monitored charities’ political activity in the run up to the 2015 general election. The outcomes of this case work are published on GOV.UK. In addition, concerns about campaigning and political activity featured in 13 completed operational compliance cases.

Case studies

The Badger Trust – compliance case

We ensure the charity takes measures to distance itself from a campaign that appeared to have party-political elements.

Global Warming Policy Foundation – compliance case

We assess complaints that the charity was promoting views of a political, rather than educational nature; our involvement ensures the trustees took steps to focus the charity’s work on its educational objects.

Oxfam – compliance case

The trustees agree to review the charity’s social media work, after concerns were raised with us about an advertisement and a tweet published by the charity.

Institute of Public Policy Research – compliance case

We assess concerns that the charity’s actions lent support to a political party.

What we do to prevent and tackle concerns about charities’ independence

We take all concerns about charities’ political campaigning activity very seriously, because of their potential impact on public trust and confidence.

Vigilance at registration stage is an important facet of our work to help prevent charities from engaging in inappropriate political or propagandist activity or being perceived as such, or as being party politically biased. When organisations whose objects are educational or that plan to carry out public campaigning activity apply for registration, we take steps to ensure the trustees understand the limitations that charitable status brings and the duties and responsibilities that fall to the trustees of charities.

We work hard to ensure that trustees of all charities understand the rules, especially in the run-up to elections, including by taking part in events and raising awareness of our guidance, including through social media.

How to ensure you maintain your charity’s independence

When thinking about carrying out campaigning or political activity, trustees must ensure that the charity stays within our guidance. Trustees must carefully weigh up the possible benefits against the costs and, in particular, any associated risks to be satisfied that the campaign of activity will be the best possible way of supporting the delivery of their charity’s purposes.

When designing your campaign, it can be acceptable to use emotive or potentially controversial material, so long as it is lawful and justifiable in the context of the campaign, and the material is accurate and has a well-founded evidence base. This can be a high risk area for trustees and requires careful consideration.

When undertaking campaigning or political activity, trustees must also ensure they comply with other relevant guidance, such as that produced by the Electoral Commission.

You can find further information in our guidance:

- Speaking out: Campaigning and political activity by charities (CC9)

- Charities, elections and referendums

- It’s your decision: charity trustees and decision making

- The essential trustee: what you need to know (CC3)

- Electoral Commission guidance on Charities and Campaigning

2.6 Concerns about charities abusing their charitable status

By law, we have to register organisations that are established for exclusively charitable purposes for the public benefit.

Sometimes, we see reason to question whether those applying to register an organisation plan to use the charity to facilitate non-charitable activities. If, after examining an application, we find we are legally required to register the organisation, but have concerns, we will monitor the new charity to make sure it is being run for exclusively charitable purposes for the public benefit.

We are vigilant: an organisation which is a sham cannot be a charity in law and will not be entered onto the register of charities. We are robust in our assessment of charitable status and will investigate any organisations where the real intention is to gain unlawful or inappropriate gain or benefit. As well as assessing the information provided by applicants, our registration team conducts independent research into applications, reviews information against our intelligence database and works with other authorities where appropriate to identify issues of concern. Where there is evidence of wrongdoing, applications are rejected and the organisation and individuals concerned are referred to the police and/or other prosecuting authorities such as HMRC.

We occasionally come across systematic abuse that calls into question whether the charity in question was in fact set up for nefarious purposes in the first place. It might have been set up in way where the real intention is to obtain gain unlawful or inappropriate gain or benefit. If we conclude that it should not have been registered in the first place, we will take the charity off the register if necessary.

Concerns about charities set up for non-charitable purposes featured in 43 operational compliance cases concluded in 2014-15.

Case studies

Children’s Cancer and Leukaemia Fund – monitoring case

Our proactive examination of this newly registered charity’s finances helps to bring a fraudster, who used the charity’s funds for personal gain, to justice.

Melton Arts and Crafts Trust – compliance case

We remove the charity from the register on the grounds that it does not operate, after identifying concerns that it was being used as a tool to avoid paying national non-domestic rates at a number of industrial units.

2.7 Concerns about fundraising

Our research demonstrates that fundraising practices have a crucial bearing on public trust and confidence in charities. For example, ‘using fundraising techniques I don’t like’ is one of the most common reasons people cite for trusting certain charities less than others.

And, in recent months, there has been a great deal of public and media focus on charities’ fundraising activities, after newspapers uncovered practices that many considered unethical and unsavoury. These events have highlighted how visible charities’ fundraising activities are, and how significant an impact fundraising can have on public perceptions of charities. They have also demonstrated that damage to one charity’s reputation can harm public confidence in the ‘charity brand’.

It is therefore vital that trustees fulfil their legal duties and responsibilities in overseeing their charity’s fundraising. That involves:

- making the strategic decisions

- informing themselves regularly and fully

- taking swift action when concerns arise

As a trustee, you must always ensure your fundraising is lawful and done in a way that encourages public trust and confidence, whether the fundraising is done in-house, or with the help of a professional fundraiser.

Our role in regulating fundraising by charities

Charity fundraising is self-regulated by the charity sector. But we can and do intervene in some cases involving fundraising concerns. The nature of our intervention will depend on the seriousness of the concern.

The self-regulatory system for charity fundraising is changing as a result of the recent revelations and a new single self-regulatory body is being developed. We will work with the new organisation to help ensure the public regains trust in charity fundraising.

Case work statistics

In 2014-15 concerns about fundraising issues featured in:

- 16 serious incidents reported to the commission

- 41 concluded operational compliance cases

- 9 concluded investigations or pre-investigation assessment cases

- 18 monitoring cases

Case study

Aiding Children – monitoring case

After concerns were raised with us about the charity’s fundraising methods and practices, we conclude that it was an organisation set up for private benefit and remove it from the register.

What we do to prevent and tackle concerns about charities’ fundraising activity

Fundraising practices are self-regulated (see Our role in regulating fundraising by charities), but we have an important role in ensuring that trustees fulfil their duties and responsibilities towards their charities in the context of fundraising. Some of our cases dealing with fundraising issues involve serious concerns about unmanaged conflicts of interest involving trustees and third-party fundraising organisations. Our role in such situations will involve ensuring that trustees are fulfilling the 6 core trustee duties set out in The essential trustee, when making decision about their charity’s fundraising.

Where trustees’ actions or failings present a serious risk to the charity, we are likely to regard this as misconduct or mismanagement.

You can read more about our role in our strategic statement on the regulation of fundraising.

How to ensure you fulfil your legal duties when making decisions about fundraising

Acting with reasonable care and skill is 1 of the 6 key duties of charity trustees. This is sometimes called the ‘duty of care’, and it means that, as a trustee, you must make use of your skills and experience when making decisions for your charity, and that you must take advice when necessary. You should also dedicate enough time, thought and energy to your role.

This principle applies to decision-making about fundraising as it does to any other activity a charity may be involved in.

We are currently consulting on a new version of our guidance on Charities and fundraising. We revised the guidance to help ensure trustees understand what we expect of them in the context of fundraising. Have your say on the updated guidance by taking part in our consultation.

Footnotes

-

Charity status depends on a statutory test. To qualify for charitable status, an organisation must have exclusively charitable purposes for the public benefit. We cannot turn down an organisation for registration if it meets that test but we have concerns about its management or ability in the future to comply – but we can and do follow up significant concerns once the charity is on the register. ↩

-

These include cases that may have been opened or have been ongoing during the year 2014-15. These are not necessarily completed cases. ↩

-

There were no cases completed in 2014-15. This statistic relates to cases that may have been opened or have been ongoing during 2014-15. ↩