2010 to 2015 government policy: UK energy security

Updated 8 May 2015

© Crown copyright 2015

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/2010-to-2015-government-policy-uk-energy-security/2010-to-2015-government-policy-uk-energy-security

This is a copy of a document that stated a policy of the 2010 to 2015 Conservative and Liberal Democrat coalition government. The previous URL of this page was https://www.gov.uk/government/policies/maintaining-uk-energy-security–2. Current policies can be found at the GOV.UK policies list.

Issue

Energy security is about making sure consumers can access the energy they need at prices that are not excessively volatile.

The UK has experienced strong energy security from a combination of its liberalised energy markets, firm regulation and extensive North Sea resources. According to the information available, the outlook for UK energy security remains positive.

While the UK’s energy system is relatively resilient to energy security challenges, it faces ongoing risks from severe weather, terrorist attacks, technical failure and industrial action. These risks can be mitigated but it is impossible to avoid them entirely.

The UK’s energy system also faces a great deal of change as existing infrastructure closes, domestic fossil fuel reserves decline and the system adapts to meet our low-carbon objectives. These changes will create new challenges for UK energy security in the years ahead.

Actions

We’re taking the following actions to make sure the UK’s energy system has adequate capacity and is diverse and reliable.

Reforming the electricity market

Our programme for Electricity Market Reform (EMR) will attract the £110 billion of investment needed to replace and upgrade the UK’s electricity infrastructure.

Removing barriers to competitive markets

We’re reforming the planning system for nationally significant infrastructure (like windfarms) to speed up the consents process and include new categories of commercial and business development.

- Read about the planning and consents process for nationally significant energy infrastructure projects.

Preparing for energy emergencies

We work with industry and regulators to strengthen the resilience of the UK’s energy networks and assets, prepare for all energy emergencies and maintain capability to lead response and recovery operations across government.

Increasing energy efficiency

Our Energy Efficiency Strategy sets out how we’re lowering UK energy security risks through various initiatives to improve the energy efficiency of appliances, businesses and public sector buildings, including the Green Deal and the Smart Meter programme.

Maximising cost-effective recovery of UK resources

To provide reliable energy supplies that are not exposed to international energy supply risks, we issue licences for domestic oil and gas exploration and production and we support development of the oil and gas industry through UK Promote, PILOT and Project Pathfinder.

Working internationally

Our international work aims to promote low-carbon technologies, encourage investment in UK oil and gas production, make sure global energy supply is reliable and enhance price stability. This work includes the EU security of supply regulations and implementation of the Third package on Electricity and Gas markets, which will improve market liberalisation.

Maintaining reliable networks

We are making sure the UK’s energy infrastructure can continue to deliver the energy people need and to where they need it. We’re also making sure that new energy generation infrastructure is incorporated in a secure, timely and cost-effective way.

Reducing carbon from UK energy supplies

We’re increasing the use of low-carbon technologies to reduce UK dependence on international oil and gas markets in the longer term and maintain diversity in the domestic energy sector.

Background

In response to the challenges affecting energy security in the UK, in December 2012 the Department of Energy & Climate Change (DECC) published the Energy Security Strategy.

The strategy:

- identifies cross-cutting risks to UK energy security

- assesses the main characteristics of energy security

- outlines work already happening to maintain the UK’s reliable energy supply

- sets out all of the actions we’re taking to maintain the UK’s energy supply

Who we consulted

Consultation on synergies and conflicts of interest arising from the Great Britain system operator delivering EMR

We soughtviews on potential conflicts of interest and synergies arising between the new role for the system operator in implementing EMR and National Grid’s existing roles and interests. The consultation closed on 29 January 2013.

Who we’re working with

The Office of the Gas and Electricity Markets (Ofgem) and DECC jointly publish the annual Statutory Security of Supply Report, with input from National Grid. The report provides forward-looking energy market information and identifies risks and the forces driving the market.

Appendix 1: future electricity networks

This was a supporting detail page of the main policy document.

Electricity networks are critical to achieving our energy and climate change objectives. Without the right network, for example, energy generated from renewable sources will not be able to reach customers.

The evolving nature of generation and demand for electricity brings new challenges to electricity networks. This particularly applies to how we prepare for, and manage, uncertainties in the future patterns of generation and demand. It also applies to how we work with new technologies. We will need to change where, when and how we establish electricity networks, how they operate and how we innovate.

Read ‘Electricity system: assessment of future challenges’.

The creation, maintenance and operation of electricity networks is a matter for network companies, overseen by the independent regulator, the Office of the Gas and Electricity Markets (Ofgem).

The Department of Energy & Climate Change (DECC) is responsible for setting the policy and legislative framework for the UK’s networks.

Our overall aims are to:

- ensure the timely, cost-effective and reliable connection of electricity generation to demand

- support a low-carbon, secure and affordable national system

Our specific objectives for future electricity networks are to:

- maintain electricity network reliability

- ensure new generation (renewables, nuclear and fossil fuels) and new demand (including electric vehicles and heat pumps) receive timely and affordable connection to the network

- use regulation to make sure networks are cost effective, competitive and using smarter technology

We will achieve these objectives by:

- ensuring timely grid access for new generation through the Connect and Manage regime

- making sure the regulatory framework allows for network charges, securities and transaction costs that are cost-reflective and proportionate

- ensuring the network is managed in a cost effective way including through temporary transmission constraint licence conditions on electricity generators

- identifying and helping to prepare for longer term challenges for the UK’s electricity network, particularly through the work of the Electricity Networks Strategy Group and Smart Grid Forum

- making sure the policy framework enables the assessment and delivery of transmission investment requirements in a cost-effective and timely manner

- co-ordinating our offshore network development programme

- producing an enduring offshore transmission regime that addresses operators’ concerns around how offshore transmission assets are commissioned under the generator build option within the regime

- encouraging network innovation

Building a smarter grid

The transition to a low-carbon economy will involve major changes to the way we supply and use energy. Transforming our electricity system is the most important part of these changes.

Integral to this transformation will be an electricity grid that is fitted with more information and communications technology over time. The result will be a ‘smarter’ grid that:

- gives a better understanding of variations in power generation and demand

- lets us use that information in a dynamic and interactive way to get more out of the system

Smart grid policy in the UK

Building a smarter grid is an incremental process of applying information and communications technologies to the electricity system, enabling more dynamic real time flows of information on the network and more interaction between suppliers and consumers.

Smart grids will make a key contribution to UK energy and climate goals. The UK is taking action now and investing in smart grid development and planning for the future:

- DECC published a vision document, Smarter Grids: the opportunity in December 2009, and the Electricity Networks Strategy Group (ENSG) published a vision and a Smart Grid Routemap, setting out a high-level description of the way in which a UK smart grid could be delivered

- DECC is rolling out smart electricity and gas meters to all UK homes by 2020. Smart meters can pave the way for a transformation in the way energy is supplied and used and are a key enabler of the smart grid

- Ofgem is providing £500 million over the next 5 years through the Low Carbon Networks Fund to support smart grid trials sponsored by the Distribution Network Operator companies.

- DECC provided £2.8 million to 8 smaller smart grid demonstration projects through the Low Carbon Investment Fund

- we worked with ENA to develop a framework for smart grid standards, focused on cyber security issues

Smart Grid Forum

DECC and Ofgem set up a Smart Grid Forum to:

- identify future challenges for electricity networks and system balancing, including current and potential barriers to efficient deployment of smart grids

- guide the actions that DECC/Ofgem are taking to address future challenges, remove barriers and aid efficient deployment

- identify actions that DECC/Ofgem, the industry or other parties could be taking to facilitate the deployment of smart grids

- facilitate the exchange of information and knowledge between key parties, including those outside the energy sector

- help all stakeholders better understand future developments in the industry that they need to be preparing for

- track smart grid developments and their drivers

- track smart grid initiatives in Europe and elsewhere

A particular achievement in the first year has been the construction of a Smart Grid Evaluation Framework, which can help assess the value of smart grid technologies. This uses analysis of likely penetration of low carbon technologies consistent with meeting the 4th Carbon Budget, and will inform network investment decisions. This framework showed that under a number of different scenarios savings could be shown as a result of delayed reinforcement.

More information about the Smart Grids Forum can be found on the Ofgem: DECC/Ofgem Smart Grid Forum site.

Appendix 2: maintaining security of electricity supply

This was a supporting detail page of the main policy document.

Electricity powers homes and businesses across the UK. We use it for many things such as lighting, heating, computing and charging our gadgets.

How does the electricity system work?

There are four main elements to the electricity system:

- Generation of electricity: we generate electricity in several different ways; examples include coal, gas, nuclear power and wind farms. We also import some electricity from other countries via interconnectors. Electricity cannot be stored efficiently so it is generated as it is needed. Supply and demand are then balanced on a second by second basis by the system operator.

- Transmission: the national transmission system carries electricity from generators to the distribution networks at high voltages.

- Distribution to homes and businesses: the distribution networks carry the electricity from the transmission system to homes and businesses at lower voltages.

- Suppliers: suppliers are companies who buy electricity from generators. They also buy the services of the transmission and distribution networks. They then supply individual consumers with power as they need it.

Capacity margins and system balancing

The electricity system is balanced on a second by second basis by National Grid who are the system operator. We often talk about capacity margins for electricity. At their simplest, they are the difference between the total generating capacity and the total demand.

The system operator balances the system by forecasting demand and matching supply to meet that demand. Matching supply to demand is done by turning power generation up or down or on or off. The UK is also increasingly using voluntary demand reduction. This is where large users can choose to reduce their demand to help balance the system.

This can be in return for payment if you are a large user. Reducing demand can include moving non-essential demand to off-peak times, for example you might run your dishwasher overnight instead of during the day. An example of this is the Marriott Hotel Chain.

Consumer behaviour can have a significant impact on balancing the system. Large numbers of people watching a popular television program or sporting event may cause demand spikes.

Risks to security of supply had been growing in recent years. This is because some older power stations have reached the end of their lives and need to close. But government, National Grid and Ofgem have now taken decisive action. This action will ensure we continue to benefit from the extremely high levels of security that we are used to.

What do these actions include?

- In November 2012, DECC published the Energy Security Strategy which set out the range of policies in place to deliver energy security and meet demand

- The government publishes a Statutory Security of Supply Report each year. This includes a response to the annual Electricity Capacity Assessment, which examines risks to security of supply over the next five years.

- National Grid are buying more back-up supplies for this winter and beyond so we are prepared to deal with unexpected events, such as a spike in demand or a power plant failure.

- Government is introducing a new tool called the Capacity Market to drive new investment in flexible power plants like gas and ensure enough existing power stations stay open.

- The reformed electricity market will deliver the low carbon energy and reliable supplies that the UK needs, while minimising costs to consumers.

- Contracts for Difference will provide long term price stabilisation for Low carbon plant.

- The Delivering UK Energy Investment report shows government progress to date and investment opportunities.

Appendix 3: maintaining security of gas supply

This was a supporting detail page of the main policy document.

The UK has one of the most liquid and largest gas markets in Europe with extensive import infrastructure and a diverse range of gas supply sources. We are therefore well placed to manage gas supply risks.

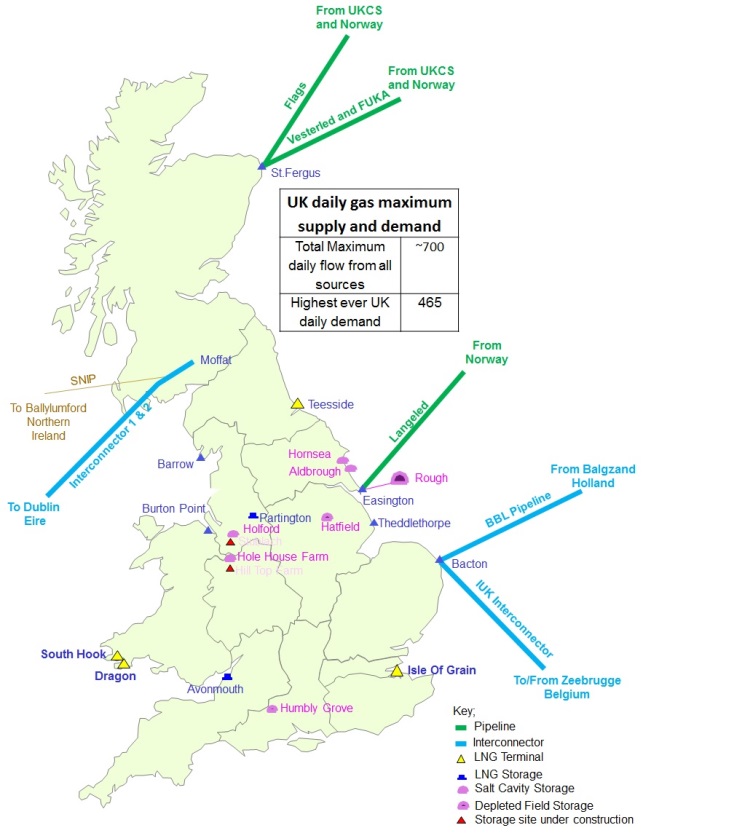

UK’s gas supply infrastructure

{kind=link}

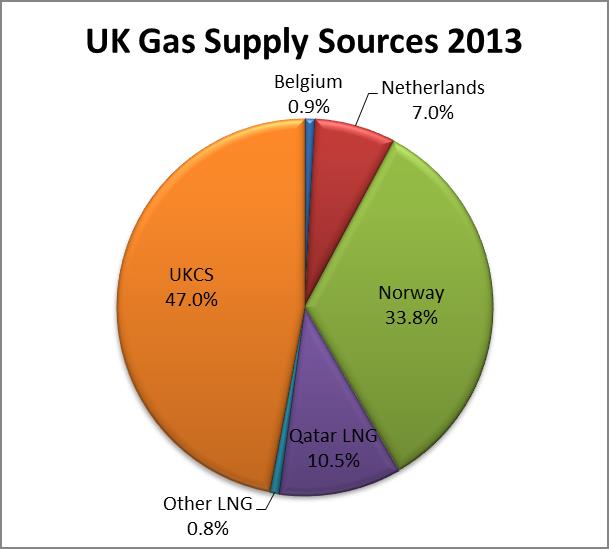

The UK Continental Shelf (UKCS) is a mature basin and production is declining. Despite this, the UK remains one of the major gas producing nations in Europe and during 2013, gas from our own indigenous production was sufficient to provide just under half of our gas demand. Our import infrastructure has significantly increased over the past decade reflecting the predicted decline of the UKCS and as a result, we have increased the diversity of supply sources and routes to our market. This flexibility means that, if there is a problem with one source, we have other sources to call upon, and gas can be delivered from the cheapest available source. We source gas from North Sea producers, pipelines from Norway, Belgium and the Netherlands, and shipments of Liquefied Natural Gas (LNG) from further afield, as well as from gas storage.

{kind=link}

Our infrastructure is able to deliver over 700mcm of gas per day – well over double average winter demand (243mcm/d in winter 2013/14) and over 50% more than the highest single day demand we have ever had in the UK (465mcm).

These diverse sources are capable of providing significant gas to meet the UK’s requirements and mean that UK gas market is resilient to all but the most extreme supply disruption events. There remains a risk of low probability but high impact events and the UK government takes this risk seriously.

Gas storage

Gas storage plays an important part in our gas system, but it is only one aspect alongside the import sources described above. Storage provides security of supply when demand is high, acting as a temporary balancing tool. Over winter 2013/14 storage withdrawal met 9% of our total gas needs, the remainder being met by other supply sources (Source: National Grid, DECC Energy Trends).

Given the constraints to the rate at which gas can be withdrawn from storage, it is misleading to calculate how many days of storage we have at any one time: our largest storage facility, called Rough, is only able to meet around 10% of peak winter daily demand but could do so continuously for around 80 days if starting from full.

Some countries on mainland Europe have more gas storage capacity than the UK but they don’t have the benefit of North Sea supply and our extensive range of import infrastructure.

Pricing

When demand is high and supply is not immediately available, prices rise to attract gas to the UK market. Higher prices are likely to trigger greater flows over our interconnectors with the continent or Norway, additional flows from storage, and attract LNG tankers to UK terminals.

Retail prices of gas in the EU

{kind=link}

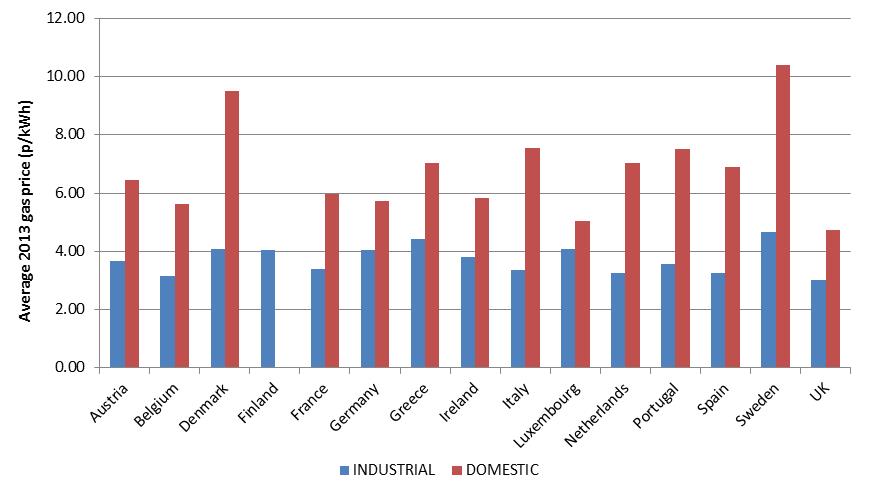

In recent months wholesale gas prices have fallen. While short term fluctuations in wholesale gas prices are unlikely to have a significant impact on consumers’ bills as energy suppliers buy gas on the forward markets gradually over time, which protects suppliers and thus consumers from the volatility of the commodity markets, we would expect that sustained changes in key fundamental costs are passed onto the consumer. Ofgem has referred the energy markets to the competition authorities to ensure there are no barriers to effective competition. The UK ranks favourably to other EU-15 countries with the lowest gas prices for domestic consumers, including taxes, as well as some of the lowest for industrial users in 2013 (Source; https://www.gov.uk/government/statistical-data-sets/international-domestic-energy-prices).

We know many consumers are really feeling the pinch due to rising energy prices, however, and the UK government has policies in place to help consumers, particularly the most vulnerable.

Multiple and significant losses to supply

Ofgem’s 2012 Gas Security of Supply report found that in a normal winter we would have to lose 50% of non-storage supplies for there to be an interruption to gas supplies to large industrial users and/or the power sector, and between 60% and 70% of all gas sources for there to be an interruption of supplies to domestic customers - equivalent to losing all LNG supply, all imports from the Continent and 50% of our production at the same time.

Nevertheless, in the unlikely event of a severe disruption to a number of sources of supply at a time of high demand, measures are in place to manage and minimise the potential impact on consumers. The owners and operators of the gas networks in the UK are required under established gas safety regulations to have adequate arrangements in place for dealing with supply emergencies. These arrangements aim to assure supplies to domestic consumers and to maximise an effective and timely response. As such industry is responsible for the operational management of the emergency and for notifying DECC as lead government department for the sector.

DECC would then be responsible for providing the interface between industry, central government, and other European countries, and for ensuring the public were kept well informed. It would also be responsible for understanding and managing the wider consequences that may arise from a major gas supply emergency and may have a role to play in the use of emergency powers in the very unlikely event these were needed.

Appendix 4: working internationally to maintain UK energy security

This was a supporting detail page of the main policy document.

Developments in international energy markets have major implications for the UK’s energy and economic security. As North Sea production declines, our dependency on imported oil and gas will grow and we will become increasingly exposed to the pressures and risks of global markets.

This will take place in a period of significant change. The next 2 decades will see global energy consumption increase substantially, driven by the rapid expansion of Asian economies. The patterns of trade are shifting accordingly and we are likely to face greater competition for more expensive resources. Global supply is also undergoing a quiet revolution as technological developments bring new resources into use.

The UK must stay ahead of these trends to secure reliable imports of oil and gas. Energy diplomacy plays a vital role in achieving this.

Increasing the use of low-carbon technologies and energy efficiency

To increase the use of low-carbon technologies and energy efficiency, which will in turn slow rising oil and gas demand, we work with a number of international organisations:

- Carbon Sequestration Leadership Forum

- Clean Energy Ministerial

- G20

- Global Carbon Capture and Storage Institute

- International Energy Agency

- International Partnership on Energy Efficiency Co-operation

- International Renewable Energy Agency

- Renewable Energy & Energy Efficiency Partnership

Read our policy on increasing the use of low-carbon technologies.

Read our policy on supporting industry, businesses and the public sector to become more energy efficient.

Encouraging global investment in oil and gas production

We encourage global investment in oil and gas production, and maximise UK commercial opportunities in doing so, through a range of bilateral relationships and multilateral initiatives.

We work with the International Energy Agency on analysis of investment needs and outlook. We also work with the Energy Charter Treaty on its rules to protect energy investments.

Ensuring reliable supplies

To ensure reliable supplies, we encourage greater liberalisation of energy markets and strengthened trading links and infrastructure, again working bilaterally and multilaterally. This includes work at a European level, in particular to implement the requirements of the Third Package of legislation on the internal energy market. This package aims to:

- establish a single market in energy across the EU

- help improve EU market integration and increase cross-border trade for both electricity and gas

It should also improve security of supply by reducing each country’s vulnerability to supply and price shocks.

Under requirements in the EU Security of Gas Supply regulation, we also share gas emergency and preventive plans with neighbouring member states to help mitigate and understand the impact of gas disruptions.

Enhancing energy price stability

To keep energy prices stable, we continue to support communication between producers and consumers and greater market transparency.

The UK is an active member of the International Energy Forum, which brings together all the main countries that produce oil and gas. We also work with the International Energy Agency on price data and analysis, and the G20 on increasing transparency in energy markets.

Appendix 5: Electricity Market Reform (EMR)

This was a supporting detail page of the main policy document.

The reformed electricity market will deliver the low carbon energy and reliable supplies that the UK needs, while minimising costs to consumers.

EMR introduces two key mechanisms to provide incentives for the investment required in our energy infrastructure.

- Contracts for Difference (CFD) provides long-term price stabilisation to low carbon plant, allowing investment to come forward at a lower cost of capital and therefore at a lower cost to consumers.

- The Capacity Market provides a regular retainer payment to reliable forms of capacity (both demand and supply side), in return for such capacity being available when the system is tight.

Stimulating the UK economy now and in the future

The UK faces very rapid closure of existing capacity as older, more polluting plants go offline, whilst UK electricity demand is expected to grow with our economy and as heat and transport systems are increasingly electrified. Attracting the investment to transform the UK’s electricity infrastructure will stimulate the economy, support the growth of UK supply chains and boost the jobs market. We will need a substantial increase in skilled professionals to design, plan, manufacture, construct and operate the projects across the UK. To achieve this investment we need to attract new sources of capital, and do so whilst keeping costs to consumers as low as possible.

Benefits of reform

The reformed electricity market will deliver the greener energy and reliable supplies that the country needs, while minimising costs for consumers in the long term. It will transform the UK electricity sector to one in which low-carbon generation can compete with conventional, fossil-fuel generation – ensuring we build a cleaner, more sustainable energy mix.

EMR is designed to:

- decarbonise electricity generation

- keep the lights on

- minimise the cost of electricity to consumers

Helping meet our carbon targets

To help us meet our legally binding carbon targets, it is critical that the power sector makes large reductions to its carbon emissions by the 2030s. Our reforms to the electricity market encourage investment in a range of low-carbon technologies so that they generate an increasing proportion of our electricity.

In addition to Contracts for Difference (CFDs), the Carbon Price Floor will indicate to the market our commitment to low-carbon electricity – as will the new Emissions Performance Standards, which will require any new coal-fired power station to be equipped with CCS.

Securing the UK’s energy supply

The risks to the security of the UK’s energy supply will increase, if there is not significant investment in the UK’s energy network. The Department of Energy & Climate Change (DECC) and the Office of Gas and Electricity markets (Ofgem) models suggest capacity margins will tighten towards the end of this decade, significantly increasing the risk to reliable supplies.

The Capacity Market will help keep the lights on by driving new investment in gas and demand side capacity, as well as getting the best out of our existing generation fleet as we transition to a low carbon electricity future.

By supporting all forms of low-carbon generation, CFDs will diversify the UK’s domestic energy supply. This will help improve the UK’s energy security and reduce reliance on energy imports. It will also ensure we keep the lights on and protect consumers against global spikes in fossil fuel prices.

Keeping bills down

The ultimate aim of these reforms to the electricity market is to create a competitive environment in which low-carbon technologies compete fairly on price and so deliver the best deal for the consumer. Our latest analysis suggests that EMR will reduce household electricity bills by £41 or 6 per cent per year on average over the period 2014-2030 compared to meeting the Government’s objectives using existing policy instruments.

Find out about reforms to the electricity market

Implementing Electricity Market Reform

Implementing Electricity Market Reform sets out the reforms and provides a comprehensive overview of EMR policy. The document includes chapters on the two main mechanisms that the Government is introducing to reform the electricity market: Contracts for Difference (CFDs) and the Capacity Market, as well as detail on measures to encourage greater energy efficiency through the Electricity Demand Reduction (EDR) programme.

EMR stakeholder bulletins

Stakeholders interested in Electricity Market Reform can be notified of new publications, announcements and upcoming events through our stakeholder bulletins.

If you would like to be added to the distribution list please contact harry.bannister@decc.gsi.gov.uk.

How the reformed market will work

Contracts for Difference (CFDs)

CFDs support new investment in low-carbon electricity generation. It has been designed to provide efficient and cost-effective price stabilisation by reducing exposure to the volatile wholesale electricity price.

CFDs require generators to sell energy into the market as usual but, to reduce exposure to fluctuating electricity prices and provide a variable top-up from the market price to a pre-agreed ‘strike price’. At times when the market price exceeds the strike price, the generator is required to pay back the difference, thus protecting consumers from over-payment.

CFDs will be implemented through a bilateral private law contract between the Generator and the Low Carbon Contracts Company Ltd (the ‘CFD Counterparty’). In order to be eligible to apply for a CFD contract, generators need to satisfy certain eligibility criteria. Please see the Contracts for Difference webpage for further details. Also see CFD Standard Terms and Conditions.

The payments to be made to generators will be calculated and paid out by the Low Carbon Contracts Company. The cost of CFDs will be met by consumers via the supplier obligation; a levy on electricity suppliers.

Five statutory instruments implementing CFDs set out how applicants can apply for a CFD and the detail of the allocation process; the criteria and eligibility for generators seeking a CFD; how a CFD contract may be drawn up, offered and publicised; establish the ‘supplier obligation’ mechanism, to meet the costs of CFDs; and set out a number of general provisions relating to the scheme.

Following on from the publication in April of the draft Contract for Difference (‘CFD’) contract and the successful passage of the EMR legislation through Parliament, the Government has published the final CFD contract and supporting notices. The final Allocation Framework and Notice followed.

For more detail see Chapter 2 of the Implementing EMR handbook

Capacity Market (CM)

The Capacity Market will enhance the security of our electricity supply by ensuring that sufficient reliable capacity is in place to meet demand.

The Capacity Market works by offering all capacity providers (new and existing power stations, electricity storage and capacity provided by demand side response) a steady, predictable revenue stream on which they can base their future investments.

In return for this revenue (capacity payments) they must deliver energy when needed to keep the lights on, or face penalties. The cost to consumers for this capacity will be minimised due to the competitive nature of the auction process which will set the level of capacity payments.

The first capacity auction will took place in December 2014. Capacity will be in place by the winter of 2018. In advance of this, the government will run two transitional auctions for demand side capacity in 2015 and 2016. This will help grow the demand side industry and ensure effective competition between traditional power plants and new forms of capacity; driving down future costs for consumers.

The Electricity Capacity Regulations 2014 establish a Capacity Market designed to ensure that sufficient electrical capacity is available to ensure security of electricity supply.

The Capacity Market Rules provide the detail for implementing the operating framework set out in the Regulations. The Rules focus on the technical and administrative rules and procedures for how the Capacity Market will operate.

For more detail see Chapter 3 of Implementing EMR handbook.

EMR State Aid

The European Commission confirmed State Aid approval of the Capacity Market, the CFD for Renewables and 5 FID Enabling for Renewables offshore wind projects on 23 July 2014. As part of the State Aid approval process, it has been necessary to make some changes to the schemes. The details of all the changes are set out in the 1 August stakeholder bulletin.

The full text of the European Commission’s decisions on these State Aid cases is now available.

Delivery Plan

The first EMR Delivery Plan was published in December 2013. It set out the administrative strike prices for renewable technologies under Contracts for Difference commissioning in the period 2014/15-2018/19 including the robust methodology which provided the basis for the strike prices. It also set out and the reliability standard for the GB electricity market, which has been used to inform the amount of capacity to be contracted.

Electricity Demand Reduction Pilot

The purpose of the Electricity Demand Reduction (EDR) Pilot is to understand whether capacity savings resulting from the installation of more efficient electrical equipment (which provide lasting rather than temporary reductions), could also form part of the Capacity Market and to learn lessons for the Government and wider stakeholders about the delivery of any final scheme. EDR projects could contribute to the Capacity Market as they reduce the demand placed on the system and in turn lower the amount of generation capacity that needs to be delivered to meet that demand.

Visit the Electricity Demand Reduction page for more information.

For more detail see Chapter 4 of the Implementing EMR handbook.

Participation

CFD allocation and pre-qualification: National Grid

National Grid has been appointed as the Delivery Body for Contracts for Difference, responsible for publishing CFD application/allocation guidelines and running the CFD allocation process.

To access pre-qualification information and guidelines or to submit a supply chain plan please see the Supply chain guidance page or go to the National Grid EMR portal.

CFD Contract Management and Supplier Obligation: Low Carbon Contracts Company

The Low Carbon Contracts Company is new government-owned company which will now act as a counterparty to a CFD contract. Its principal functions are to manage Contracts for Difference, and to administer the collection and payment of monies under the supplier obligation for the CFD regime. For more detail see Chapter 2 of the Implementing EMR handbook.

Generators wishing to apply for a CFD and Suppliers seeking information on the supplier Obligation can find further details on the Low Carbon Contracts Company website.

Capacity Market Settlement: Electricity Settlements Company

The Electricity Settlements Company is responsible for the administrative functions associated with the collection and verification of bid bonds and collateral in respect of the Capacity Market. It will make capacity payments and retain accountability and control of the Capacity Market settlement process. Key documents relating to the CM settlement process can be found on the Electricity Settlements Company website.

Low Carbon Contracts Company & Electricity Settlements Company framework documents

Low Carbon Contracts Company Ltd framework document

Electricity Settlements Company Ltd framework document

These framework documents set out the relationship between the Electricity Settlements Company and the Low Carbon Contract Company and their sole shareholder, the Secretary of State for Energy and Climate Change, and the broad framework within which they will each operate.

Follow these links for more information on the Electricity Settlements Company and the Low Carbon Contracts Company

For more detail see Chapter 1 of the Implementing EMR handbook.

EMR Budget

Technology Groupings and Competition

Our ultimate aim is that all technologies should move to competitive allocation as soon as it is appropriate to do so, with the eventual aim of technology neutral auctions for all low carbon generation.

We recognise that not all technologies are currently at the same level of development. So a technology neutral auction at this point would result in high levels of deployment of a small number of technologies with technologies which are currently more expensive, but which have the potential for further industry development and cost reduction, unlikely to secure CFDs and deploy.

We are introducing competition within two groupings: established and less established technologies. The move to immediate competition reflects the need to manage the budget effectively, ensure value for money and bring the scheme in line with EU guidance on renewables and new State Aid guidelines.

The government’s policy on technology groups and competitive allocation can be found on the Further consultation on allocation of Contracts for Difference page.

Budget notice

Final CFD budget notice for the autumn 2014 CFD allocation round

This document is the CFD budget notice that the Secretary of State has given to the EMR Delivery Body, National Grid, ahead of the first allocation round that occured in October 2014. This followed on from the draft budget notice which was released three months ahead of the round opening to provide visibility and certainty for investors, enabling them to prepare their applications.

The budget notice set out what is required of the Delivery Body for the allocation round, as per the allocation regulations 2014; and is accompanied by explanatory notes with respect to biomass conversion, future allocation rounds and remaining budget, maxima and minima, and Scottish Islands Onshore wind projects. The budget notice should be read in conjunction with the explanatory notes.

£300million will be allocated to renewables projects this autumn in the first CFD auction. This is a near 50% increase of the £205 million indicative budget announced in July. This budget will be split between two “pots”: one for more established technologies, such as onshore wind and solar PV, and one for less established technologies such as offshore wind.

This means that we are releasing budget as follows for the first allocation round commencing 16 October 2014:

-

Pot 1 (established technologies): we intend to release for allocation in the 2014 allocation round £50m for projects commissioning in 2015/16, and an additional £15m for projects commissioning from 2016/17 onwards.

-

Pot 2 (less established technologies): we intend to release for allocation in the 2014 allocation round £155m for projects commissioning in 2016/17 onwards, and an additional £80m for projects commissioning from 2017/18 onwards.

-

Pot 3: No budget released in 2014. Decisions on budget for the 2015 allocation round will be taken in 2015.

While we have increased the CFD budgets since our indicative budget in July, the increase in budget comes within the Levy Control Framework cap – and so does not have impacts on bills in addition to those already announced.

Levy Control Framework

The Levy Control Framework (LCF) sets annual limits on the overall costs of all DECC’s low carbon electricity levy-funded policies to control public expenditure paid for through consumer energy bills. The LCF was extended to 2020/21 specifically for low carbon electricity policies to inform decisions on new mechanisms, and has been set at a level which will enable us to cost-effectively meet our low carbon and renewables ambitions.

For more detail see Chapter 1 in the Implementing EMR handbook.

Route to Market under CFDs

Independent renewable generators play an important role in delivery investment in renewables: they have a significant pipeline of projects and support competition and innovation.

DECC has developed the Offtaker of Last Resort mechanism to provide independent renewable generators with access to a ‘backstop PPA’ at a minimum price. The OLR guarantees eligible renewable CFD generators a route-to-market, reducing the risks that they face, and in doing so:

- reduces the cost of investment in renewable electricity generation,

- boosts competition, and

- ultimately lowers costs to consumers.

For more detail see Chapter 2 in the Implementing EMR handbook.

The institutional framework

A number of parties are involved in the delivery of the market reforms:

- Government – Sets the policy framework, provides sponsorship, leads design and legislative action.

- Ofgem – Regulates the electricity market, provides design advice, analysis and regulation.

- National Grid – Delivery Body, administrator of CFD allocation and the Capacity Market auction and provides advice to the Government.

- Low Carbon Contracts Company (the CFD Counterparty) – Administers and acts as counterparty to the CFD, manages the supplier obligation.

- Electricity Settlements Company (the Capacity Market Settlement Body) – Makes capacity payments and retains overall accountability and control of the Capacity Market settlement process.

- Devolved Administrations – Oversee implementation and monitoring of EMR with DECC.

- Generators – Participants and parties to CFD and Capacity Market agreements.

- Suppliers – Contributors to CFD and Capacity Market funding arrangements.

For more detail see Chapter 1 in the Implementing EMR handbook.

Transitional Arrangements

Final Investment Decision Enabling for Renewables

Some of the CFD budget was released early to successful projects in the FID Enabling for Renewables process in order to avoid an investment hiatus ahead of the full implementation of the enduring regime.

Eight renewables projects were awarded Investment Contracts under the Final Investment Decision (FID) Enabling for Renewables process in April 2014. Investors are committing up to £12 billion of investment, backed by new Contracts for Difference (CFDs) which provide them with greater certainty about the income that they will receive in the market. In accordance with the Energy Act 2013, the signed contracts were laid before Parliament in both Houses on 4 June 2014.

These projects include biomass conversion, dedicated biomass with combined heat and power and offshore wind. The contracts awarded in April will bring forward:

- up to 15 TWh/y of generation. This will be enough generation to power the equivalent of up to three million homes;

- approximately 4.5GW of renewables capacity across offshore wind farms, coal to biomass conversion plant and dedicated biomass plant with combined heat and power. This is around 14 per cent of the UK’s 2020 renewable energy target; and

- a reduction of about 10MtCO2 from the UK power sector per annum compared to fossil fuel generation.

The Investment Contracts have been published on the Future electricity networks page.

Read the latest on Final Investment Decision Enabling for Renewables: Updates 1, 2 and 3.

Transition from the Renewables Obligation

The government is committed to supporting investment in renewables in order to maintain investor certainty and confidence, and with the aim of preventing an investment hiatus ahead of implementation of Electricity Market Reform, we have put in place robust transitional arrangements from the Renewables Obligation (RO) to the new support mechanism. In July 2013, the government published a consultation paper setting out proposals for the operation of the RO during the transition period to the new Contracts for Difference (CFD) support mechanism. A further consultation was published in November 2013 proposing detailed arrangements for the eligibility criteria and lengths that would apply to the grace periods to be offered at the point of RO closure. The Government published its response to both consultations on 12 March 2014.

Key points include: that the new renewable generating capacity will have a choice of scheme that should take place at the point of application for the RO or CFD; that operators of dual scheme facilities would be expected to treat the capacity in each scheme as distinct and separate; and there are some technology-specific requirements for biomass plants and offshore wind.

This comprehensive transition policy will ensure a smooth shift from the RO to the CFD for renewable generators, suppliers and consumers alike. We are giving the renewables industry the assurance and comfort needed to ensure ongoing investment, and ensuring value for money for consumers.

We have also published the Government Response to the consultation on changes to financial support for Solar PV under the Renewables Obligation (RO) and Feed in Tariffs (FITs).

For more detail see Chapter 1 in the Implementing EMR handbook.

EMR in the Devolved Administrations

Throughout the development of these reforms we have sought to ensure that the approach to incentivising investment in low carbon generation is applicable and usable by all financiers and investors, and beneficial to all UK consumers. The Northern Ireland Executive, Scottish and Welsh governments have been closely involved in the development of the reforms and this collaboration will continue throughout their delivery.

For more detail see Chapter 1 in the Implementing EMR handbook.

EMR Panel of Technical Experts

To ensure the information underpinning the policy making is robust, the Government has put in place an independent Panel of Technical Experts (PTE). Their role is to impartially scrutinise and quality assure the analysis carried out by National Grid in its role as Delivery Body, the choice of models and modelling techniques employed, the inputs to that analysis (including the inputs provided by DECC) and the outputs from that analysis scrutinised in terms of the inputs and methods applied. An independent Panel of Technical Experts for the enduring regime was appointed in February 2014.

Energy Intensive Industries Exemption

The government consulted on eligibility for schemes designed to provide relief to electricity intensive industries from the indirect costs of renewables. This comprises of compensation from the renewable obligation (RO) and feed-in tariffs (FIT), which was announced in Budget 2014, and re-consults on Electricity market reform: contracts for difference costs exemption eligibility- CFDs which ran from 4 July 2013 to 30 August 2013.

A further consultation on EII implementation has been published, seeking views on several proposed changes to the CFD supplier obligation: the implementation of exemptions from CFD costs for electricity intensive industries and imported renewable electricity; and minor and technical amendments to the CFD Supplier Obligation regulations. Published alongside the consultation are draft Regulations, an updated Impact Assessment and the Vivid Economics and Cambridge Econometrics report ‘Impact of exemptions from the CFD’.

More information on EIIs can be found on the main EII page.

The Emissions Performance Standard

The Energy Act 2013 established an Emissions Performance Standard (EPS) to limit carbon dioxide emissions from new fossil fuel power stations. The Government has now consulted on draft regulations that will fully implement the EPS.

The consultation, titled ‘Implementing the Emissions Performance Standard: Further Interpretation and Monitoring and Enforcement Arrangements in England and Wales’ was launched on the 25 September. The consultation ran until the 6 November 2014. On 15 January 2015 the government published their response to the consultation, together with an impact assessment.

EMR policy development archive

All publications, meeting group and event papers, reports and presentations published in the EMR development and implementation phase can be accessed on the National Archives version of this page.

Appendix 6: UK Promote

This was a supporting detail page of the main policy document.

On 1st April 2015 certain functions passed from the Department of Energy and Climate Change (DECC) to the Oil and Gas Authority (OGA) a newly created Executive Agency of DECC

In 2001 the Department for Trade and Industry (now the Department of Business Innovation & Skills) launched UK Promote – an initiative to attract new companies to explore and develop the UK Continental Shelf (UKCS). The UKCS is a 200-mile zone around the UK in which the government has the right to exploit resources such as oil and gas.

The Oil and Gas Authprity now manages UK Promote.

Overall investment in North Sea oil and gas is increasing with new drilling programmes and significant field development plans for the UKCS.

Our objective

UK Promote aims to attract 2 types of new entrants:

- independent oil companies with the resource to drill wildcat exploration wells and exploit the full value chain from exploration to development

- niche developers and smaller companies, particularly those with the skills to develop previously undeveloped discoveries through technically innovative and best-cost solutions

UK Promote 2015

Promote licence

The Promote licence is a variant of the Seaward Production Licence. It is designed to give small and start-up companies a production licence first so they can then attract the necessary operating and financial capacity later.

The Promote licence offers:

- a 90% reduction in the annual rental rate for 2 years

- no requirement for applicants to prove technical/environmental competence or financial capacity before the licence is awarded (but they must do so within 2 years of its start date if they are to keep the licence)

- a mandatory relinquishment (the surrender of acreage that the licensee does not intend to work) of 50% at the end of the initial term

Licence terms:

The terms of the licence are:

- initial term – 4 years

- second term – 4 years

- third term – 18 years

UK Promote’s other work

UK Promote also:

- establishes standard legal agreements to stimulate competition in the exploration and appraisal market

- encourages re-investment in fallow areas through the Fallow Acreage Initiative, (found in “Summaries of the regulatory, administrative and operational practices in the UK” in “Prospectivity of the UK Continental Shelf: North Sea and West of Britain opportunities” below) by making licensees ‘drill or drop’ within a set timeframe

- provides data for potential investors including field approvals and start up data, geoscientific data and relinquishment reports

- maps potential exploration and development opportunities in the North Sea and west of Britain

Related guidance

Read more about oil and gas licensing and regulation:

- Oil and gas: petroleum licensing guidance

- Oil and gas: fallow blocks and discoveries

- Oil and gas: fields and field development

- Environmental regulation of offshore oil, gas and carbon dioxide storage activities

- Oil and gas: taxation

- Oil and gas: decommissioning of offshore installations and pipelines