The effects of COVID-19 on IPS delivery and the trial site labour markets: Health-led Employment Trial Evaluation

Updated 8 April 2024

Applies to England, Scotland and Wales

© Crown copyright 2024

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/health-led-trials-impact-evaluation-reports/the-effects-of-covid-19-on-ips-delivery-and-the-trial-site-labour-markets-health-led-employment-trial-evaluation

August 2022

DWP research report no. 1038

A report of research carried out by Institute for Employment Studies on behalf of the Department for Work and Pensions.

Executive Summary

This report is part of a series of reports covering the implementation and outcomes of the health-led employment trials (HLTs). It provides detailed insights into the effects of the pandemic on the context of delivery for the HLTs. It is based on interviews with employment specialists delivering the trials, desk research documenting the pandemic and uses secondary data to explore the effects of the pandemic in the two labour markets. Additionally, interviews were undertaken with a range of stakeholders including individual placement and support (IPS) experts, Jobcentre Disability Employment Advisors (DEAs) and employers. The analysis demonstrated:

The pandemic affected the period in which outcomes were expected to be observed for the large cohorts who joined the trial in late summer and autumn 2019.

Some groups of people faced greater risks in the pandemic with demographic factors such as age, ethnicity and gender, and contextual factors such as living arrangements and multi generational households, presenting greater risks. Many disabled people and those with long term health conditions were required to shield by the government. Many of these factors intersected with the demographics and contextual situation of the trial population.

The support experience of recruits in the treatment group during the pandemic differed from earlier groups. In common with other IPS services, support moved to remote mode, using telephone or video-conferencing. Not all in the treatment group were able to make this transition due to their health conditions. Among those who continued to receive support, not all felt able to continue looking for employment, so the support instead focused on health and wellbeing. This was also common in other IPS services. Despite the challenges, employment specialists, DEAs and IPS experts indicated the pandemic had created opportunity in some specific occupations and the tight labour market meant that employers were more flexible in recruitment.

Labour market analysis indicated West Midlands Combined Authority (WMCA) had seen employment continue to grow, driven by higher participation for women. Sheffield City region [footnote 1] (SCR) saw employment fall overall, and signs of higher economic inactivity due to long term ill health and pandemic related reasons. Both regions saw some employment growth in relatively lower skilled jobs.

Employers recruited to the COVID-19 research discussed significant impacts on their operations, workforce and, crucially, recruitment. As with the national narrative, effects varied by sector and according to whether organisations were considered essential services. There were indications that the pandemic had increased focus on health and wellbeing policies within organisations.

Author’s credits

(Any errors or omissions in this report are the responsibilities of the authors.)

Jonathan Buzzeo is a Senior Research Fellow at the Institute for Employment Studies (IES). His work has primarily focused on: youth transitions, careers advice and guidance, educational and labour market disadvantage, and the links between these areas. He has worked for a range of clients on these topics including government departments and third sector organisations.

Billy Campbell, Research Officer, joined IES September 2021 shortly after completing an MA in Methods of Social Research. His interests include equality and diversity, education and the path to employment, and the higher education sector.

Rachel Cetera, Research Officer, joined IES in July 2021 having completed an MA in Legal and Political Theory at University College London (UCL) in 2021 and a BA in Economics and World Philosophies in 2019 at SOAS, London. She has reviewed grey literature on the barriers to employment progression for underrepresented workers and supported a ‘what works’ Rapid Evidence Assessment for the ReAct evaluation of prime providers delivering Department for Work and Pension’s Restart programme.

Rosie Gloster is a Principal Research Fellow at IES. She supported the management of the evaluation consortium and contributed to the process evaluation. She is a mixed-methods researcher specialising in employment and careers. She has authored several reports for DWP, including the Evaluation of Fit for Work.

Rahul Shukla, Research Intern, joined IES in September 2021 having graduated from his Master’s in Public Policy from UCL where he was a Chevening Scholar (FCDO, UK) from India in the 2020 to 2021 cohort.

Tony Wilson, Director of IES, has worked in employment policy and research for most of the last 20 years, in a range of roles spanning central government and independent institutes. He has particular expertise in labour market policy and analysis, the design, delivery and evaluation of employment and skills programmes, supporting organisations to understand and apply evidence of ‘what works’, devolution and local delivery, and leading complex programmes.

Becci Newton is Director of Public Policy and Research at IES and specialises in research on unemployment, inactivity, health, skills and labour market transitions. Becci has managed the evaluation since its design and contributed to the process evaluation. She has led multiple evaluations for DWP including of the 2015 Employment and Support Allowance (ESA) Reform Trials and the Work Programme.

Rebecca Duffy and Mandi Ramshaw are Project Support Officers at IES and proofread and formatted the report.

Glossary of terms

| Term | Definition |

|---|---|

| Employment specialists | Staff employed by the trials to undertake randomisation appointments, provide IPS support to the treatment group, and undertake employer engagement |

| Health-led employment trials | Two trials, funded by the Work and Health Unit, to test a new model of employment support for people with long term health conditions |

| Individual placement and support (IPS) | IPS is a voluntary employment programme that is well evidenced for supporting people with severe and enduring mental health needs in secondary care settings to find paid employment |

| Provider staff | Those working in provider organisations including employment specialists delivering IPS support, as well as managers and administrators |

| Randomised controlled trial | A study to test the efficacy of a new intervention, in which participants are randomly assigned to two groups. The intervention group receives the treatment, while the control group receives either nothing or the standard current treatment |

| Recruits | People who agreed to take part in the trials and who were randomised to either the treatment or control group |

| Site | The trials were delivered in two combined authorities, which are termed sites |

| Theory of change (ToC) | A description and illustration of how and why a desired change is expected to happen in a particular context. It sets out the planned major and intermediate outcomes and how these relate to one another causally |

| Thrive into work | The name given to the trial in West Midlands Combined Authority (WMCA) |

| Working win | The name given to the trial in Sheffield City Region (SCR) |

1. Introduction

The onset of the COVID-19 pandemic in February and March of 2020 coincided with the final months of trial delivery, and the period when employment outcomes would be expected for the largest cohorts in the trials (those that joined from late summer and autumn 2019). This report provides some insights into how this affected delivery of the IPS services as well as the trial site labour markets.

The report starts with an analysis of published evidence on the timeline and effects of the pandemic from February 2020, then turns to insights from a range of stakeholders to consider the effects the pandemic had on experiences of the trial and its possible effects on employment outcomes.

1.1 Methods and coverage

This study included desk research alongside several phases of primary research, including:

-

The desk research comprised a review of secondary labour market data across both the trial sites to understand the effect of the pandemic on employment and vacancies, as well as a review of published documents and other evidence recording the effects on the pandemic on the UK and its population.

-

In-depth interviews with 16 employment specialists across both trial sites (split evenly between WMCA and SCR) completed in July and August 2020. These interviews explored how the delivery model for IPS services in these areas changed with the onset of the pandemic, and the implications this had for service delivery, the treatment group and their outcomes.

-

In-depth interviews with four Disability Employment Advisers in WMCA and SCR in July and August 2021. These interviews covered the effects of the pandemic on the employment of disabled people and those with long term health conditions, including views on how the local labour markets were affected.

-

In-depth interviews with five IPS stakeholders in July and August 2021. These interviews covered how other IPS services adapted during the pandemic to understand how typical the changes observed in the trial were. Interviewees were drawn from other services as well as UK and international IPS resource centres based on recommendations from the Work and Health Unit, members of the evaluation consortium and ‘snowballing’ recommendations from interviewees.

-

In-depth interviews with 20 employers across a range of sectors and of varying sizes in July and August 2021. Interviews were spread across the two trial sites with 11 employers located in WMCA, and 9 in SCR. These interviews explored the effects of the pandemic on business operations, the workforce, and recruitment; and explored long-term changes in approaches to health and wellbeing that have been driven by the pandemic. The findings aimed to contextualise the employment outcomes achieved in both trial sites and see how the pandemic had affected local employers’ ability to hire and support those with long-term health conditions in the workplace. Table 1 below shows the make-up of the employer sample.

Table 1: Employer sample characteristics

| Characteristics | Number of employers | Sector | Number of employers | ||

|---|---|---|---|---|---|

| Area | SCR | 9 | Retail | 4 | |

| WMCA | 11 | Accommodation | 2 | ||

| Size | 11 to 25 | 4 | Food and beverage | 3 | |

| 26 to 50 | 6 | Public admin and defence | 1 | ||

| 51 to 250 | 8 | Education | 4 | ||

| 251 to 1000 | 1 | Human health activities | 6 | ||

| 1001 + | 1 |

Source: Sample information

1.2 Structure of this report

The coverage of this report is as follows:

-

Chapter 2 sets out the pandemic timeline and the effect this had on different sections of the UK population.

-

Chapter 3 presents findings from interviews with employment specialists describing how the IPS delivery model adapted during the early stages of the pandemic.

-

Chapter 4 describes how the labour markets of the trial sites were affected by the pandemic, based on secondary data.

-

Chapter 5 details how employers in different sectors in the two trial sites were affected and how their recruitment and workforce management practices changed as a result of the pandemic.

-

Chapter 6 contains concluding comments.

2. The pandemic timeline and the effect on the UK population

This chapter provides an account of the impact of the COVID-19 pandemic on the labour market from its onset through the end of the trial delivery period, focusing specifically on the sectors, geographic areas, and types of employment that were worst affected, and the intersection with demographic factors.

2.1 Timeline of events

The outbreak of COVID-19 from early 2020, and the lockdowns and other COVID-19 containment measures that followed, resulted in one of the biggest shocks to the labour market in the past 20 years. The UK experienced the largest economic contraction in 300 years (at 11.3%, Brewer, 2021a) with major effects for ways of working, including moves to remote working and new requirements for health protection. Nationally, the pandemic added to effects emerging from the UK’s negotiations with, and withdrawal from, the European Union.

On 20 March 2020, a few days before the first national lockdown commenced, the government announced the Coronavirus Job Retention Scheme (CJRS), which was intended to support employers to retain staff. While the CJRS meant redundancies were contained, the total number of jobs fell by the largest amount seen since 1992, reducing opportunities for people who were already unemployed or economically inactive for whom the CJRS did not apply. On the same day, the government also announced a £20 weekly uplift to the standard allowance of Universal Credit (UC). This boost remained in place for the duration of the trial delivery.

The CJRS was extended to enable employees to undertake some work in July 2020, when COVID-19 restrictions were eased temporarily and replaced by localised approaches. Starting with Leicester, local lockdowns were implemented in response to local infection rates throughout the summer and into the autumn of 2020. By the end of trial delivery, at the end of October 2020, the second national lockdown began. Evidence suggests that neither the local measures nor the November lockdown led to a significant deterioration of the labour market. Rather, they merely slowed down the UK’s recovery.

Alongside CJRS, when the government announced the first lockdown, it also issued ‘shielding letters’ so that those deemed clinically vulnerable would remain in their homes. This initially applied for 12 weeks and was later updated intermittently. However, the list of eligible individuals was developed iteratively, which led to differing advice on health conditions indicated for shielding.

2.2 Sectoral impact

The pandemic’s effect has been far from equally distributed across sectors. Much of the disparity across industries can be explained by sector-specific infection risks and the capacity of certain sectors and professions to adapt to remote working. Consistently throughout 2020, retail, hospitality, and leisure fared the worst. The vulnerability of these sectors in part derived from the general contraction of the UK economy, but also from higher risks of occupational transmission inherent to businesses including restaurants, bars, and personal care (O’ Donoghue et al, 2021).

In some cases, particularly within the creative industries, the pandemic accelerated the progressive disappearance of jobs already underway before 2020. In this sense, the CJRS protected a significant number of workers, with the arts, entertainment and recreation sector having the largest percentage of furloughed workers (34% against an average of 9% across industries, Office for National Statistics (ONS), 2020), and prevented the drop in employment from reaching the worst-case scenario. The European Economic Sentiment survey suggests that the drop in retail employment, for example, could have been 3% larger than it was.

However, the retail sector faced by far the most redundancies, and hospitality and food were worst affected by a drop off in vacancies. While some other sectors, such as finance and agriculture, reported facing uncertainty related to the exit from the European Union, evidence from the local lockdowns suggests that these did not suffer from the lockdowns’ spill-over effects which widened gaps seen across sectors. These inequalities were starker still when looking at differences across occupations. Even in less affected sectors, such as healthcare, the jobs created were mostly administrative and managerial (Williams et al, 2020). The sectoral inequalities intersected with demographic inequalities. For example, across the UK population, women were more likely to work in shut-down sectors and therefore be more affected by closures. However, this was only true for white ethnic groups, and minority ethnic British men were significantly more likely to work in shut-down sectors than their white counterparts (Platt and Warwick, 2020).

The implications are twofold. First, skilled and better-paid employment was more successfully protected from disruption and, in some cases increased. Second, those working in these roles were also protected from transmission risk as they were more likely to work from home. For lower skilled jobseekers, and those in key worker roles, their jobs led to a greater risk of exposure to the virus.

2.3 Spatial inequalities

There are widely held views that the pandemic emphasised existing and long standing inequalities (for example, Blundell et al, 2020; Local Government Association (undated)). In the UK, the north-south divide includes health and labour market inequalities and is longstanding. These inequalities were rising in the years prior to the pandemic (The Lancet, 2017). With an older population than the UK average, and a higher rate of disability benefit claimants (8.6% and 8% in former coalfields and older industrial towns respectively, compared to a UK average of 6%, Beatty and Fothergill, 2021), the north was hit hard by COVID-19.

The disparity became particularly evident into the summer of 2020, when local lockdowns were imposed. These started in Leicester and in the north west, expanding to the north east in September. The second national lockdown, in November, helped reduce the infection rate in the north. However, by the time the second-tier system replaced it, three-quarters of residents in the north and the Midlands faced the toughest restrictions, contrasting with only 10% of people living in the south (Butcher and Aitken, 2020). At the start of 2021, older industrial areas and former coalfields still had higher levels of infections (4,850 and 4,530 respectively per 100,000 residents, compared to a UK average of 4,060, Beatty and Fothergill, 2021).

However, and because of the exceptional experience in London, some commentators rephrased the divide as existing between rural and urban areas. Areas with high density housing were hit particularly hard at the onset of the pandemic, and larger urban centres particularly struggled in the recovery. Although cities benefitted from the ‘Eat Out to Help Out’ scheme introduced following the first lockdown, the positive impact on footfall was particularly strong in smaller towns.

As was the case across sectors, the impact of COVID-19 on different geographic areas was strongly mediated by differences in the ability to convert to working from home, which varied significantly across the country. The Centre for Cities estimated in 2018 (Magrini, 2020) that in the south-east and larger urban areas, homeworking would be possible for up to 50% of the workforce, contrasting with 20% in northern and Midlands cities. Those unable to work from home were more likely to work in a trade and possess few or no qualifications. These workers were more likely to be in northern cities, particularly those reliant on construction and manufacturing.

2.4 Quality of work inequalities

The relative effect of the pandemic varied strongly according to the kind of job workers performed, and specifically, whether it could be adapted to home-working. This played an accelerating role with respect to many existing inequalities, including income distribution. According to the ONS (2021), the income of the poorest fifth of households fell by 3.8% on average between 2017 and the end of 2020, while the income of the richest fifth continued to grow steadily throughout the pandemic. Over half of adults in the former group (54%) had to borrow more money in the first lockdown than they did before the onset of the pandemic, to cover essential costs such as food and housing (Brewer and Patrick, 2021). Low paid employees were hit particularly hard on many fronts. They were more at risk of infection, more than twice as likely to leave their jobs, and about two-thirds saw their hours reduced, even in the least affected sectors (Wilson and Buzzeo, 2021).

Secondly, the pandemic emphasised inequalities in flexible employment. For example, low-paid workers were less likely to be able to work from home, with two in five able to do so compared to four in five high earners (Cockett et al, 2021). While working from home brought complications, having the ability to do so was particularly important for those with health conditions and caring responsibilities. Conversely, the ‘have-nots’ in flexible employment were low-paid, working in riskier environments for transmission, and often denied furlough despite being more likely to see working hours reduced (Wilson and Buzzeo, 2021). Women balancing childcare responsibilities were particularly affected by the widespread reductions in working hours. However, men were hit the hardest by the fall in part-time work and self-employment (IES, 2021).

Flexible employment (whether that means working part-time, remotely, or on a temporary contract) does not necessarily imply worse quality work, and evidence suggests that up to 87% of individuals either work flexibly or would like to do so (Cockett et al, 2021). However, despite the growth in flexible vacancies brought on by the pandemic, the supply of these kinds of contracts (which reached 22% during the pandemic, Timewise, 2020) is far from meeting this demand.

Further, those who already had a flexible job in terms of hours at the beginning of 2020 did not fare well compared to their full-time counterparts. The flexible equivalent of the CJRS started later, in July 2020, and by then, 38% of part-time workers had temporarily left their jobs, and the number of part-time workers working fewer hours had increased by 10 times compared to the figure for the previous year (ibid). The difference with respect to full-time workers remained steady until the end of the trial period, with 38.7% of part-time employees remaining temporarily away from work, compared to 28.4% for their full-time counterparts (ibid).

The evidence strongly suggests that the effect of the COVID-19 pandemic on the labour market was multifaceted. To further understand the pandemic’s sectoral and geographical impact, and its intersection with flexible working during the trial period, the next section examines differences along demographic characteristics.

2.5 Demographic factors

2.5.1 Age

Age emerged as an important factor in understanding the effects of COVID-19. Older workers were more vulnerable to the virus and had the most difficulty in returning to work when the first lockdown was lifted. In March 2020, the employment gap for workers aged 50 to 64 was 13 percentage points (ppts), and it grew by an additional percentage point (ppt) during 2020 (Centre for Ageing Better, 2021). While young people were generally less vulnerable to the virus, they too were disproportionately affected by the impacts on the labour market. Between September 2019 and September 2020, the youth claimant count increased in all UK local authorities, with some seeing a 7.6 ppt increase (Sutherland, 2020).

2.5.2 Disability and health conditions

Also in 2020, the disability employment gap grew to 29 ppts, and was largest for those aged 50 to 64 (Centre for Ageing Better, 2021). In August 2020, the government announced an extension to Access to Work, which included grants for special equipment enabling disabled people to work from home, access to mental health support, and financial support for transport for those who could not work remotely. The extension included a fast track for those deemed clinically extremely vulnerable. Conditionality for UC was suspended for all jobseekers initially for 3 months, along with face-to-face Jobcentre assessments and disability benefit reassessments. Conditionality was gradually reintroduced from July 2020. Additional positions for specialist Disability Employment Advisors were created in May 2021.

2.5.3 Race and ethnicity

Ethnic minority groups were hit particularly hard by COVID-19. According to the ONS (2020b), most had higher mortality rates than white ethnic groups, with South Asian older women the most vulnerable. Black and Asian men were more likely to work in settings susceptible to higher infection risk, or to live in urban or deprived areas, and people from South Asian backgrounds were more likely to live in multi-generational households, so being more exposed to transmission. Black ethnic groups were more likely to be hit harder financially, and less likely to have access to a private outdoor space. Individuals of Indian ethnicity reported a more significant deterioration of their mental health (ibid). Between the final quarter of 2019 and that of 2020, unemployment among ethnic minority groups rose by nearly two-thirds, compared to under a third for white workers (Trades Union Congress, 2021)

Implications for the trial

This chapter has explored some of the ways in which the COVID-19 pandemic affected workers and jobseekers during the 2020 trial delivery period. Some inequalities were particularly concerning given the characteristics of the trial population. Approximately one in four trial recruits were in the older, 45 to 55 age group, and almost one in five were aged 55 or above. Since trial recruits generally belonged to older cohorts, the switch to remote working, and the possibility of returning to the workplace after closures, would be more difficult. This is especially relevant given that the switch to working from home was more complex in the north and Midlands. Furthermore, a large majority of trial recruits reported having a mental health condition (84%) and low mental wellbeing (62%). As noted, older people and those long-term health conditions were particularly vulnerable to the virus and its labour market effects. The lockdowns and other containment strategies are likely to have had an aggravating effect on trial participants’ mental wellbeing.

There are also implications for the out of work (OOW) trial groups. In SCR, OOW recruits were more likely to be men. In WMCA, OOW recruits from an ethnic minority background made up a significant portion of recruits. Despite this, as the impact analysis (see the 12 month outcomes impact report) shows, there was no discernible effect on outcomes from the pandemic in either trial site.

3. How the IPS services in the trial adapted in the pandemic

This chapter explores how the COVID-19 pandemic changed the IPS services delivered by the trial, and how this might have affected outcomes of the treatment group. This was assessed through interviews that explored how the delivery model changed and the implications this had for service delivery, the treatment group and their outcomes. These findings were compared with the changes experienced by other IPS service providers and DEAs over the same period.

3.1 Approach

The research involved qualitative interviews with employment specialists and other trial staff in each trial site. The research took place in July 2020 and involved 16 in depth interviews in total (8 in each trial site). Interviews were also completed one year on in July and August 2021 with 4 Disability Employment Advisers (DEAs) and 5 IPS stakeholders, to see how the experiences of the trial sites compare to other services working with similar groups over this period.

3.2 Immediate effects on staff

Staff involved in delivering the trial reflected how their working lives were affected by the restrictions. Depending on their home circumstances, as with the general population they needed to adjust to home-schooling children alongside work. While employment specialists were used to working independently and spending time in the community, some found it challenging to adapt to working independently from home. Some described needing to consider how they best engaged and communicated with each other. Reduced travel time created more space for keeping in touch as a team and sharing knowledge, as well as discussing changes to the service caused by the pandemic. The IT skills of staff, and their willingness and ability to embrace changes to modes of working varied. While all employment specialists modified how they engaged with participants, and the content of the support they provided, some preferred interacting over the telephone and others via online platforms.

The trial had finished recruiting when the pandemic began, so employment specialists had prior relationships with participants from a face-to-face context and transferred these to modes of engagement, building on existing rapport and knowledge of clients. At the end of delivery, the size of adviser caseloads varied, depending on whether their colleagues had been redeployed as the trial was ending, or had left fixed term contracts during the final months of the service. While some advisers had considerable caseloads, others reflected that their caseloads were getting smaller during the trial period that coincided with the pandemic, which gave them more time to spend with individuals.

3.3 Transition of service delivery

The most immediate challenge posed by the pandemic was the need to change to a remote mode of delivery. Overall, employment specialists noted that switching to phone or video delivery went smoothly. It became evident that this change would be required a week or so before lockdown was implemented on 23 March 2020, so they began preparing in advance.

They used a combination of telephone and online approaches to keep in touch with the treatment group which included voice calls, video calls and text messages. The reasons for this were often related to the recruits’ access to smartphones or computers. Video calls were predominantly conducted using messaging apps on mobile phones. The treatment group’s access to computers was very varied, and those with computers often had to share them with others in their household. Their level of comfort with different technologies also varied, as did levels of anxiety caused by the pandemic, and both could affect the mode of delivery they selected.

Meeting at a distance meant employment specialists felt they could miss some body language cues during conversations. They found that where English was a second language for members of the treatment group it was more difficult to communicate in the remote mode. The phone approach also needed to be adapted for some in the treatment group, such as those with hearing impairments, and employment specialists found video appointments or support through an app were effective ways to support these clients remotely.

Employment specialists reported trying to encourage the treatment group to use video chats to increase familiarity with different technologies, which would have positive benefits both from developing skills that are useful for work, and keeping them connected to others, benefitting their mental health. There was one example of an employment specialist creating short videos to familiarise the treatment group with technologies. However, in common with experiences more generally in using online modes, the treatment group could experience anxiety at seeing themselves on screen, especially those with mental health conditions.

These experiences are similar to those expressed by staff involved in delivering other IPS services, outside of the trial sites. The IPS stakeholders confirmed that not all IPS recipients were equipped for remote working and using digital devices to connect, and this could cause anxiety and additional support needs. Some services put together new packs to support people during the pandemic, which included briefings on using digital devices to connect. There was also some evidence of centralisation of helplines and moves to maximise e-services given the remote working model.

At the time of the interviews with staff in the trial sites, SCR had risk assessed and was allowing face-to-face visits again where these would be beneficial to treatment group members and where social distancing guidelines could be followed. Employment specialists reported that this had re-invigorated the engagement of some in the treatment group. WMCA continued operating entirely in remote mode.

3.3.1 Engagement with the service

Overall levels of engagement among the treatment group remained high during the early phases of the pandemic, according to employment specialists, who made greater use of shorter but more frequent appointments to support this. A small number of people were reported to have left the trial, but employment specialists said it was because they had a history of low engagement. Some of the treatment group experienced a change in their employment specialist due to staff changes and redeployment over the lockdown and subsequent COVID-containment periods, which was also common within other IPS services according to IPS stakeholders. For employment specialists who were newly supporting this group, more work was required to keep them engaged with the service. Despite their best efforts, some felt that the changed mode permitted some participants to withdraw from full engagement with the support.

Some employment specialists emphasised that while most of the treatment group chose to remain in the trial, the degree of engagement in looking for job opportunities dropped initially, given the health risks posed by COVID-19, school closures, and the decline in recruitment activity during the early phases of the pandemic. It was also common for there to be interruptions to the support conversations, for example from children in the background, or other members of the household. Additionally, they said school closures were a major issue for the treatment group in March 2020 that encouraged a shift in focus away from employment support temporarily. For both those already in work and those seeking jobs, suddenly having children at home with no access to childcare meant they either had concerns about losing their jobs, were worried about having to work less, or were not able to look for work. Employment specialists said that some in the treatment group had no choice but to wait until their children returned to school in September 2020 before recommencing their job search or employment.

Employment specialists also observed that members of the treatment group faced initial difficulties in continuing to access community-based trial partners such as libraries and support groups, which were unable to continue operating throughout periods of lockdown. As a result, there were some gaps in both access and guidance on specific topics, requiring employment specialists to lead on a larger range of themes than they would usually. Employment specialists said they had received training and support within their teams to deal with these new and increasing fears since it was not always possible to meet these needs through signposting to other services.

The IPS stakeholder interviews confirmed that these changes were also experienced by other IPS services. Some experienced reducing caseloads and drop-offs in referrals as recipients could not or did not want to work at different points. High levels of anxiety linked to the effects of the pandemic could mean they were reluctant to engage. The change to a remote mode could also be off-putting and affect the engagement of some recipients. Examples were given of people not answering their phones due to this reluctance or because the caller ID was withheld. For those that continued to engage, IPS stakeholders stated that it was common to focus on wellbeing rather than gaining work. This emphasis extended to employment specialists and other staff involved in these services. In this context, the team leader role was seen as pivotal in maintaining staff morale while also adapting the remit of IPS in response to COVID-19.

Following appropriate risk assessments and easing of restrictions, some employment specialists resumed face-to-face meetings with participants. These meetings initially tended to take place outdoors, such as walking through a park or the local area. Face-to-face engagement was reported to re-motivate members of the treatment group who had been less engaged in remote mode.

3.3.2 Delivery content

During March and April 2020 employment specialists focused more on supporting wellbeing and skill development rather than job applications, until restrictions began to lift in the summer of 2020, but by the summer there was a shift back to helping the treatment group become job-ready and find suitable local employment opportunities as the economy reopened.

However, health-related concerns associated with the risks posed by COVID-19 remained an additional barrier in reaching the delivery targets, according to many of the employment specialists who were interviewed. Due to the initial fall in business activity, it was more difficult for employment specialists to identify the jobs in the sectors that members of the treatment group wanted. Individuals were contacted to check if there were any other occupations and sectors of interest, but mostly they did not want to change and, in accordance with IPS principles, no pressure was applied, particularly when individuals had health and safety concerns. Of particular importance for those already working or entering work, was for employment specialists to be responsive to any changes due to the furlough scheme being used, or anxiety about travelling to and being at work.

While employment specialists believed there had been fewer employment outcomes during the pandemic, they commented that their IPS services had provided time and support throughout a challenging period and focused on intermediate outcomes such as engaging in skills development, managing mental wellbeing, and building IT skills and confidence. Staff anticipated that this would increase employability amongst the treatment group when vacancies returned.

Where the treatment group were in work, their support needs also changed. Employment specialists reported a need to prioritise: advice and support about the furlough scheme, and managing changes to working hours. For those in the treatment group who were working from home, there was an additional requirement for support on how to manage work life balance. For who were attending the workplace, managing safety was a common issue.

3.3.3 Benefits and challenges to remote working

The reduced need for travel, with the new ways of working, was identified by employment specialists as a major benefit of remote delivery, which was also confirmed by IPS stakeholders. It freed up time in their days, allowing them to focus on tasks such as increasing the number of appointments they had with the treatment group, completing more job search activities and being better able to complete administrative aspects of their role. Moreover, many felt that they spent more time on phone calls in response to the needs of the treatment group. Several staff reflected this made their management of their caseload more efficient. They identified benefits, for example, they could respond and support participants who contacted them because they had secured a job interview or who had an urgent problem or change of circumstances immediately. For future delivery, employment specialists felt their experience during the pandemic would make them think more creatively about how best to support participants.

The lack of face-to-face contact with individuals in the treatment group was, however, identified as the main disadvantage of the switch to remote working. This was not only inconvenient for some individuals and employment specialists, but also made some session activities more difficult to complete. Many employment specialists still preferred face-to-face delivery believing that engagement was more successful due to the ability to read non-verbal cues. Moreover, tasks that required the use of a computer, such as drafting a CV, were more difficult and could not be as individually led without a shared computer and screen. However, balancing this it was important to equip people for the new modes of work as during this time, aspects of the recruitment process, such as interviews, also increasingly took place online (in addition to online application forms).

Furthermore, the lack of access at home to the internet or computing devices for some of the treatment group proved to be a significant barrier. An employment specialist described the case of someone in the treatment group who was self isolating. They had previously used computers at the Jobcentre to look for work, so were no longer able to do so. For those in the treatment group with hearing impairments and without access to IT equipment, phone conversations with employment specialists did not provide a suitable solution, as due to the lack of a visual display individuals could not lip-read.

These experiences were shared by the DEAs and IPS stakeholders interviewed, who were working with similar customer groups. The DEAs noted that customers with learning difficulties or mental health issues could find it challenging to engage with any form of remote support. A consequence of this lack of interaction over the course of the pandemic was that these customers may lose confidence, which could set them back further in their search for employment. The DEAs interviewed also stated that face-to-face appointments were previously useful in encouraging customers to agree to additional support or provision that they had available (for example, a supported work placement). Often, they were able to introduce the customer to provider staff during their appointment, which gave them the chance to learn about the provision first-hand and discuss how it could benefit them before asking whether they would commit to taking part.

IPS stakeholders also noted that the switch to remote ways of working affected what activities employment specialists could complete with recipients. For example, active work on CVs at a computer was not possible during remote appointments. As a result, employment specialists did more of this work on behalf of recipients, rather than building capability. This could mean recipients were less invested in the support overall.

3.3.4 Engaging with employers

Initially, employment specialists found it challenging to undertake employer engagement. The approach switched from in person to remote mode. Some reported that employers’ priorities had shifted away from recruiting to protecting and adapting their existing workforce. Employment specialists recognised they needed to be sensitive to this, and to offer wider support beyond recruitment, to enable them to be well positioned to support employers when they next turned to recruitment. More broadly, they considered it was important to engage with employers on the implications of the pandemic for staff health and wellbeing, and for the treatment group particularly, to ensure appropriate adjustments were in place.

However, employment specialists needed to work at a distance on this, whereas prior to the pandemic they might have attended a face-to-face meeting and considered the implications based on the physical site. This placed further constraints on the nature and scope of their engagement with employers (the implementation and four-month outcome report contains further information on employer engagement in the trial).

IPS stakeholders also reported benefits and drawbacks in respect of employer engagement. The interviews took place around a year later than those with employment specialists and it seemed that services had adapted over time. Employer engagement in remote mode was reported to have advantages in terms of appointments being more readily accommodated by employers, and employment specialists being able to engage with more during a typical day due to reduced travel requirements. Amongst IPS stakeholders, there was discussion about how the IPS Fidelity Scale might need to be adapted to better allow for remote modes of working, including remote engagement of employers.

3.3.5 Employment and other outcomes

Employment specialists noted some employment outcomes were achieved from March 2020 onwards, but said that these were lower compared to the numbers they were achieving before the COVID-19 outbreak. The job outcomes achieved included entry level positions. Sectors with job vacancies changed in the early stages of the pandemic according to employment specialists. They reflected that initially there were increasing vacancies in supermarkets and the care sector. However, given the potential close contacts and perceived risks of the virus in these settings, many of the treatment group did not see these as suitable jobs. The IPS approach is client-led, with a focus on the work that clients are interested in. Where treatment group members had employment goals for sectors that were closed (such as hospitality), employment specialists worked with them to focus on skills development and work readiness to prepare for when the sector reopened. Overall, staff reported that there was more competition for job vacancies.

The labour market uncertainty meant that vacancies which were advertised were more likely to be fixed term, offering short-term or part-time opportunities which conflicted with preferences in the treatment group for permanent contracts and full time hours because of the increased certainty this offered on work hours and income.

Where outcomes were being achieved over 2020, employment specialists noted difficulties ensuring that the agreed workplace adjustments were put into practice by employers as often, due to staff shortages, employers had increased workloads to deal with and the adjustments could be unintentionally overlooked. There were extra hurdles in ensuring that treatment group members entering employment were satisfied with their commuting travel plans, and this led to them requiring a higher level of pre-entry support than staff provided previously.

IPS stakeholders presented a different view one year on which is more reflective of the outcomes observed for the trials which the employment specialists could not know at the time of the research. While some services had seen a dip at the start of the pandemic, and implementation of action plans with very specific targets for engagement and transparency in service goals, the situation had turned around and employment outcomes held up. Employer engagement was also seen as easier as people became more familiar with remote ways of working. Virtual contact methods worked well with busy diaries making employer engagement more seamless. Additionally, as travel time was no longer needed to meet in person at workplaces, it was possible to increase the number of employers engaged.

A stakeholder from the International learning centre, reported evidence (covering 25 countries) that employment outcomes were relatively resilient during the pandemic. The rate at the time of the interview with the relevant IPS stakeholder (September 2020) was 45.28%, which had recovered from a low of 41.52% in spring/summer 2019. This is attributed to employment specialists staying in role (some were redeployed but it was not a major issue for most services), complemented by the switch to virtual working that proved effective with many recipients and many employers.

3.3.6 Impact of COVID-19 on the labour market

Within the trials, employer engagement during the COVID-19 pandemic was limited through the early lockdown in March 2020, where instead the focus was on monitoring job advertisements. However, by the summer of 2020, employment specialists reported that they were again initiating proactive contact with employers through phone calls and emails.

Employment specialists said that many in the treatment group believed that the pandemic made the labour market even more competitive. Fewer vacancies were available, and those that were advertised were filled quickly, with limited time to respond and develop suitable applications. There was a view that many employers were protecting the jobs of their current employees as a priority rather than leading new recruitment exercises, but that additional agency roles had become available from the summer of 2020. Employment specialists also said there had been an increase in vacancies in large supermarket chains, warehousing, construction and health and social care. Equally, they also saw a rise in work-at-home IT and marketing opportunities.

IPS stakeholders’ views were markedly different although probably as a result of these interviews taking place a year later than those with employment specialists for the trials. As became clear over time (eg IES, 2021 to 2022) the feared unemployment crisis did not emerge and instead there was a tightening of the labour market. IPS stakeholders argued that the large number of vacancies available in lower skilled occupations in the summer of 2021 could be well matched to needs of IPS recipients. As restrictions eased, the tight labour market was also seen to create opportunities for recipients of IPS, as employers were prompted to think differently about recruitment and to be more flexible in who they took on. While the range of jobs people can access has potentially narrowed, the international evidence also concurs with the thought that opportunity is created in a tight labour market.

4. The economic impacts of the pandemic in the trial site labour markets

4.1 Employment, unemployment and economic inactivity

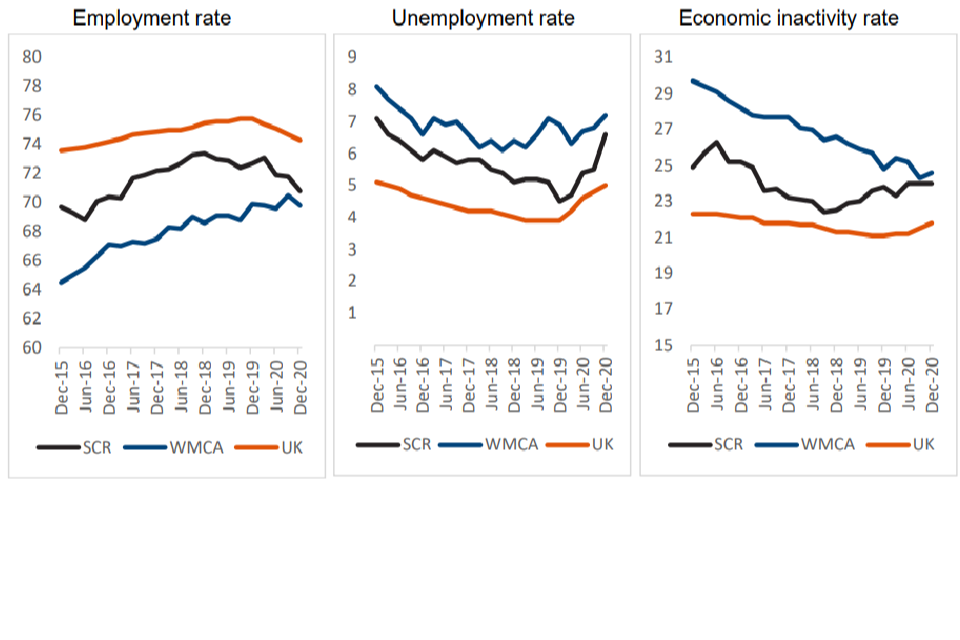

Both the WMCA and SCR had lower employment, higher unemployment [footnote 2] and higher economic inactivity [footnote 3] than the UK as a whole going into the pandemic, and this has remained the case since then. However, analysis of the Annual Population Survey (APS), set out in Figure 4.1 below, shows divergent trends between these three areas. While the UK employment rate has fallen back by around 2 ppts since the start of the pandemic, the fall for SCR has been far steeper while for WMCA employment has continued to rise.

Within SCR, the ‘gap’ between its employment rate and that of the UK as a whole had been narrowing sharply through to 2018 to 2019, but employment had actually started to deteriorate in advance of the pandemic. In all, the employment rate has fallen back by around 3 ppts over the last 3 years. The worsening picture in SCR appears to be explained by a large rise in economic inactivity in the year or so leading up to the pandemic, which had previously been falling sharply, and since the pandemic began, this appears to have fed through into higher unemployment.

WMCA by contrast has historically had a far lower employment rate and seen more gradual improvement in employment pre-pandemic. However, this improvement appears not to have slowed over the 18 months, meaning that its employment rate is now very close to SCR’s, and its employment gap with the UK as a whole is the narrowest that it has been in recent years. This is entirely explained by very steep falls in economic inactivity, while unemployment has remained stable (but still, relatively high).

Note that this analysis (and all other labour market analysis in this chapter) uses the APS, which generates estimates to local authority and combined authority level over rolling 12 month periods. The most recent data available on this survey covers the period July 2020 to June 2021, so after the end of the first lockdown, but only a very small part of the strong recovery that we have seen since the easing of restrictions in late spring. As such, this analysis tells the story of the impacts of the pandemic on the labour market, through to its nadir, rather than of the recovery. It should also be noted that Figure 4.1 uses truncated scales for the employment rate and economic inactivity rate, in order to more clearly illustrate the trends.

Figure 4.1: Employment, unemployment and economic inactivity, UK, SCR and WMCA (16 to 64s)

Source: IES analysis of Annual Population Survey. Dates denote the midpoint for that 12-month estimate (so the most recent data is for July 2020 to June 2021)

Impacts by local authority are set out below, starting with WMCA. Due to small sample sizes, changes in the data might be attributed to differences in the samples only. Hence, care should be taken in interpreting the figures.

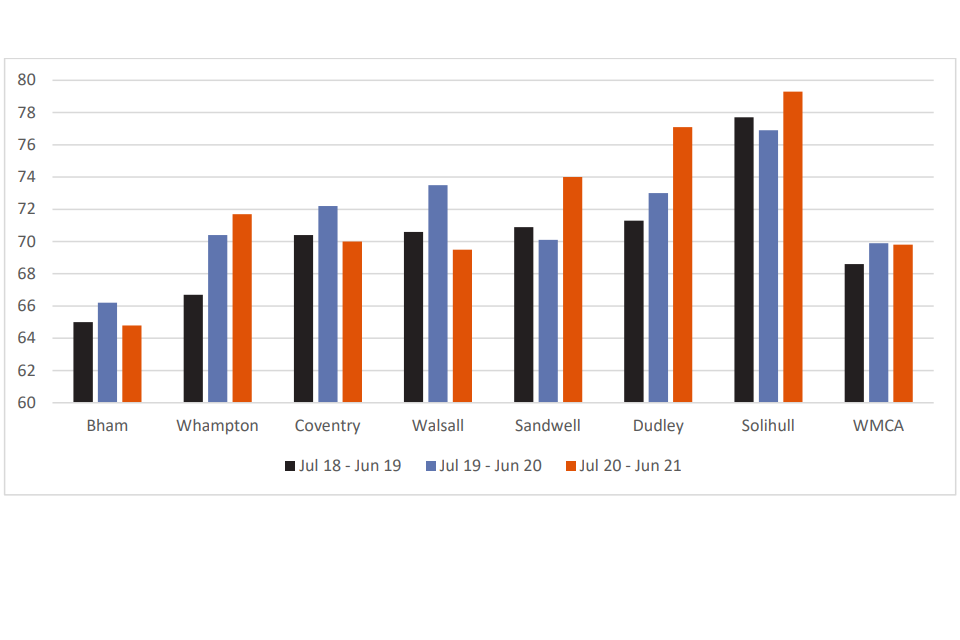

Nonetheless, Figure 4.2 shows that the relatively low employment rate overall for WMCA is explained by the outsized impact of Birmingham, which accounts for two fifths of the WMCA by population (and so is nearly the same size as SCR in its entirety). Employment in Birmingham has declined with the pandemic (albeit by slightly less than the national average), as it has in Coventry and Walsall (by somewhat more). Employment growth has been driven by Sandwell, Dudley, Solihull and Wolverhampton. This appears to at least in part reflect trends seen nationally, where employment impacts have been greater in those areas more reliant on office work, high street retail, hospitality, and leisure. In the case of WMCA, this has also meant that areas with lower employment pre-pandemic have generally seen more significant (negative) impacts from the pandemic.

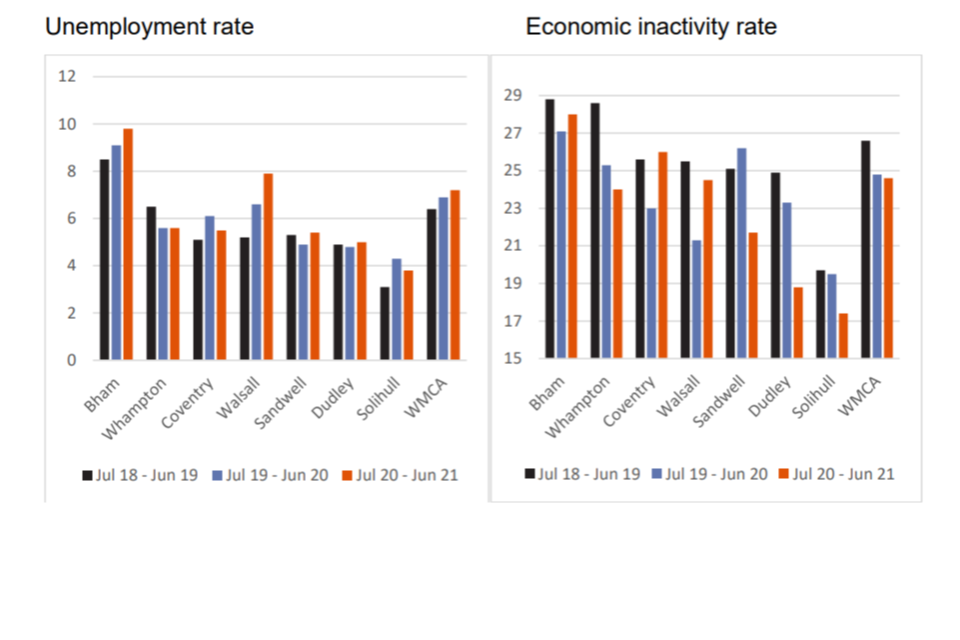

Figure 4.3 then sets out changes in unemployment and economic inactivity. This shows that those areas with falling employment have all seen economic inactivity increase, while Birmingham and Walsall have also seen unemployment rise quite significantly – so not all of the fall in employment is explained by withdrawal from the labour market. Areas with rising employment have generally seen unemployment staying stable and in some cases economic inactivity falling. Note that the graphs below (and in the subsequent SCR analysis) again use truncated scales for employment and inactivity.

Figure 4.2: Employment rates by local authority, WMCA, 2018/19 to 2020/21

Source: IES analysis of Annual Population Survey

Figure 4.3: Unemployment and economic inactivity rates by local authority, WMCA, 2018/19 to 2020/21

Source: IES analysis of Annual Population Survey

The same analysis for the SCR area similarly shows that the overall fall in employment is driven particularly by the impacts of Sheffield, its largest local authority (also accounting for two-fifths of population). The fall in employment in Sheffield is around twice the UK average, with Doncaster also seeing a significant decline (slightly higher than the national average). Rotherham on the other hand has seen strong employment growth, moving it from having the lowest employment rate in the region area to the highest. It should be noted though that all 4 local authorities entered the pandemic with employment above 70%.

The reasons for these changes are likely to be similar to those seen in other parts of the country. That is, the difference in experience between large commercial and business centres and areas with more dispersed populations and/ or market towns. Interestingly though, because of the very different starting points in SCR compared with WMCA, the pandemic has served to narrow (and in fact reverse) the differences between areas with lower and higher employment pre-pandemic.

Figure 4.4: Employment rates by local authority, SCR, 2018/19 to 2020/21

Source: IES analysis of Annual Population Survey

Analysis of unemployment and economic inactivity also illustrates that the sharp rise in unemployment in SCR is particularly driven by Sheffield and Doncaster, with Sheffield also seeing economic inactivity tick up. Barnsley has seen a small rise in economic inactivity despite employment rising slightly too, while Rotherham has seen inactivity fall and unemployment rise – so the labour pool in the last year appears to have grown even more than the increase in employment.

Figure 4.5: Unemployment and economic inactivity rates by local authority, SCR, 2018/19 to 2020/21

Source: IES analysis of Annual Population Survey

4.2 Benefit receipt by local authority area

Administrative data on UC can also give us useful insights into the relative impacts of the pandemic on different areas. UC receipt increased markedly (by 75% overall) between March and May 2021, as over two million people made initial claims for benefits following job loss or their business halting. This also served to accelerate the ‘migration’ of claimants of prior (‘legacy’) benefits, and UC volumes have declined only slowly overall since then (although somewhat more quickly in recent months for those required to search for work).

Figure 4.6 below shows the growth in the proportion of residents (aged 16 to 64) claiming UC and recorded as not being in work. The relative position of each local authority largely reflects the labour market picture set out above. For WMCA, Birmingham and Wolverhampton have the highest rates of benefit receipt. With then Dudley, Walsall and Sandwell in a middle group (along with the average for WMCA as a whole), and then Coventry and Solihull with far lower rates (in line with the average for Great Britain). Coventry has relatively low employment and low benefit receipt, which may well reflect its large student population. For SCR, Sheffield has consistently the lowest rate of benefit receipt, Barnsley and Doncaster are both highest, and Rotherham is in between.

Overall, both WMCA and SCR entered the pandemic with higher rates of UC receipt than the country overall. This was especially so in the WMCA. At local authority level, all areas have seen very similar patterns of growth (that is, similar ppts increases), which reflects the relatively broad-based nature of the pandemic. However, this means that areas that had lower claimant rates before the pandemic saw higher percentage growth, with Sheffield (78%) and Coventry (71%) seeing the highest growth and Birmingham (45%) and Wolverhampton (48%) the lowest. (By the same token, the two combined authorities overall started the pandemic with higher claimant rates than the national average and so also saw smaller percentage increases. 64% in SCR and 52% in WMCA, compared with 75% across Britain.)

Nonetheless, the percentage differences between places were not large enough to lead to higher ppts rises in areas with lower unemployment, with for example Birmingham, the area with the highest pre-pandemic rate and the lowest percentage increase still seeing its claimant rate increase by 4.0 ppts. While Sheffield, with the lowest pre-pandemic rate and largest percentage increase seeing its rate rise by only 3.2 ppts. As a result, the gaps between those areas with the lowest and highest rates actually widened between March 2020 and September 2021. Only slightly in SCR (from 3.5 to 3.7 ppts), but significantly in WMCA from 4.3 to 6.4 ppts).

This picture of widening gaps in claimant rates in WMCA and broadly stable gaps in SCR largely reflects the story from the Annual Population Survey data set out above. However, in other respects there are only very slight if any signs in the UC data of the differences between places that are seen in the survey estimates. For example, Dudley and (to some extent) Solihull do appear to have fared relatively better than other areas in the WMCA, and Sheffield perhaps slightly worse than others in SCR, but otherwise trends are largely similar. This could mean that there are labour market factors not well captured in the UC data. For example, the known growth in student numbers or falling participation among older people who may not be on benefit (both explored in more detail below), or that there are non-labour market reasons why UC caseloads have not fallen faster, for example to do with the recording of self employment or Work Capability Assessment backlogs.

Figure 4.6: Proportion of population (16 to 64) claiming Universal Credit and not in work by local authority, WMCA, SCR and GB average

Source: IES analysis of Stat-Xplore and Annual Population Survey

Source: IES analysis of Stat-Xplore and Annual Population Survey

Finally, a further important factor in understanding the picture relating to benefit receipt is the proportion of residents claiming ‘legacy’ benefits that are no longer open to new claimants and who have not yet been assessed for eligibility for UC. These benefits (Employment and Support Allowance, Incapacity Benefit and Income Support) are largely only paid now to people who have been out of work for a long time due to long-term ill health, and so recipients are predominantly economically inactive and not seeking work. The most recent data (for May 2021) is set out in Figure 4.7 below and shows that nearly every area is higher than average, and that (unsurprisingly) ex-industrial areas have the highest rates of receipt (especially in SCR, despite it having higher employment and lower economic inactivity than WMCA).

Figure 4.7: Proportion of population (16 to 64) claiming Employment and Support Allowance, Incapacity Benefit or Income Support by local authority, WMCA and SCR, May 2021

Source: IES analysis of StatXPlore

4.3 Factors affecting labour market (non) participation

4.3.1 Reasons for economic inactivity

While rates of economic inactivity have started to converge between WMCA and SCR, underneath this there are very different factors explaining both non-participation and changes during the pandemic. Figure 4.8 sets out for both areas the share of those economically inactive, by the reason given [footnote 4]. This shows firstly that those economically inactive in WMCA are much more likely to be students and somewhat more likely to be looking after their family or home (that is, usually parents of young children), while those in SCR are much more likely to have long-term ill health and somewhat more likely to have retired early. This clearly reflects the demographics of the two regions, with WMCA a younger, more urban population and SCR somewhat older and ex-industrial. Compared with national figures (not shown on the graph), student figures are higher in WMCA and lower in SCR than average, while long-term ill health is lower in WMCA and higher in SCR .

The graph also illustrates that there are differences in how the composition of economic inactivity had changed in the run-up to and during the pandemic. WMCA has seen a large fall in the share of economic inactivity explained by family or home caring, with offsetting small rises in other categories, which is broadly similar to the pattern found in the UK as a whole (albeit with a somewhat larger fall in family or home caring in WMCA). For SCR by contrast, the share of economic inactivity due to being a student has actually fallen through the pandemic, caring has declined only slightly, and long-term ill health is broadly unchanged. The most stark difference has been in those economically inactive for ‘other’ reasons, where national increases have been smaller but assumed to be explained by people not looking because of factors related to COVID-19 (like shielding or a job temporarily ending).

While these are changes in the proportions economically inactive by reason, there are very similar findings when looking at the estimated levels. For example, family caring falling by a quarter over two years in WMCA (compared with 13% in SCR), long-term ill health rising by 8% in SCR compared with 4% in WMCA, and ‘other’ reasons up by three-fifths in SCR but broadly unchanged in WMCA.

Figure 4.8: Reasons for economic inactivity, WMCA and SCR, 2018/19 to 2020/21

Source: IES analysis of Annual Population Survey

Analysis of UC data also gives some indications of the relative impacts of the pandemic on different groups, and to some extent backs up the analysis above. As Figure 4.9 shows, since the start of the pandemic:

-

just over half (55%) of the growth in UC claims among those out of work has been in the ‘searching for work’ group, which covers all of those who do not have health conditions that significantly limit their ability to work or who do not have primary caring responsibility for a child aged 4 and under.

-

just over a third (37%) of the growth in UC claims is in those with ‘no work requirements’ among those out of work meaning that they have a health condition or impairment that very significantly affects or prevents them from working

-

of the UC claims among those out of work, 8% have some work requirements, meaning either a less significant health condition or caring responsibilities for a child aged 1 to 4

Within WMCA, a greater proportion of the growth is among those in the searching for work group, and a smaller proportion in no work requirements, which we would expect to see given the falls in economic inactivity overall, even though long-term ill health appears to have risen as a reason for inactivity. Within SCR, however, a substantially larger share of the growth in UC has been among those with no work requirements, which reflects a far greater incidence of economic inactivity due to long-term ill health. However, it is notable that the share of the growth in ‘searching for work’ in SCR is relatively low, despite the large increase in unemployment in the last year.

Figure 4.9: Share of total growth in UC by each conditionality group for out of work claimants, March 2020 to September 2021, WMCA, SCR and GB

Source: IES analysis of Stat-XPlore

| Searching for work | No work requirements | Preparing for work | Planning for work | |

|---|---|---|---|---|

| GB | 55% | 37% | 6% | 2% |

| WMCA | 58% | 33% | 7% | 2% |

| SCR | 54% | 41% | 4% | 1% |

4.3.2 Participation rates by gender

The differing trends in economic inactivity (and its inverse, labour market participation) are also reflected in data on gender and age, set out below. First on gender, the difference in participation rates between women and men is far greater in WMCA than SCR (as Figure 4.10 sets out), which is likely largely explained by the far higher rate of economic inactivity due to home or family care in the WMCA. In fact, across all local areas, participation rates for men and women are close to or above 80% (and on average higher in the WMCA).

This gap is particularly noticeable in Birmingham, and across the region there is far more variation in activity rates for women than there are for men. Interestingly though, participation has fallen overall for men while it has risen for women (again reflected in lower economic inactivity due to caring), which in turn has narrowed the participation gap from 12.2 to 7.6 ppts. In other words, rising participation for women is driving the overall growth in employment in WMCA, even as participation has fallen for men. Birmingham, Sandwell and Dudley saw the largest rises in activity rates for women.

There are similar trends evident in SCR, with higher participation rates for women overall, a narrower gap pre-pandemic, and a further narrowing, albeit less pronounced, over the most recent year (from 8.9 to 6.9 points). In SCR however, higher participation among women has not been enough to offset the falls for men, leading to employment declining overall.

Figure 4.10: Economic activity rates by gender and local authority, WMCA and SCR, 2019 to 2020 and 2020 to 2021

Source: IES analysis of Annual Population Survey

4.3.3 Participation rates by age

On age, Figure 4.11 shows that SCR has higher economic activity rates across age groups, with lower participation in WMCA among young people explained by the larger share of the population that are non-working students, and lower participation among people aged 25 to 49 due to fewer women in the labour force. Activity rates are similar among those aged 50 to 64.

Over the most recent two years, within WMCA the most significant changes have been higher participation for people aged 25 to 34 (particularly women), and an apparent fall in the most recent year among young people (more students). Within SCR, participation is broadly flat, with the slight declines among those aged over 35 likely reflecting the rises seen in economic inactivity for ‘other’ reasons and (to a lesser extent) long-term ill health.

Figure 4.11: Economic activity rates by age, WMCA and SCR, 2018 to 2019, 2019 to 2020 and 2020 to 2021

Source: IES analysis of Annual Population Survey

For completeness, Figure 4.12 shows the share of growth by age group (again for out of work claimants only) but does not point to any significant differences between the two regions (nor to differences from the national average).

Figure 4.12: Share of total growth in UC by age band for out of work claimants, March 2020 to September 2021, WMCA, SCR and GB

| 16 to 24 | 25 to 34 | 35 to 49 | 50 and over | |

|---|---|---|---|---|

| GB | 10% | 27% | 35% | 28% |

| WMCA | 11% | 28% | 35% | 26% |

| SCR | 11% | 29% | 33% | 27% |

Source: IES analysis of Stat-XPlore

4.3.4 Employment gaps for disabled people and ethnic minority groups

Data on employment rates for disabled people suggests that the recent rises in employment have not led to any appreciable narrowing of the employment rate ‘gap’ in the WMCA, while falling employment has not led to any widening of the gap in SCR. This is set out in Figure 4.13 below. Sample sizes are small so care should be taken in interpreting short-term changes. In both regions, the gap appears to be broadly similar to the UK average. Unsurprisingly, a higher proportion of the working age population are disabled in SCR (at 25%) than in WMCA and the UK (20%), which reflects the higher incidence of long-term ill health in the region.

Figure 4.14 shows the estimated employment rate ‘gap’ for people from ethnic minority groups, and the trends are less clear. In both regions, the gap tends to be larger than for the UK as a whole. In the case of the WMCA, one-third of all working age residents are from ethnic minority groups (note the confidence interval is around 4 ppts). For SCR around 1 in 11 people are from an ethnic minority group and confidence intervals are wide, at around 13 ppts. Due to small samples, definitive statements are hard to make but broadly, it appears that the gap is wider in SCR than in WMCA.

Figure 4.13: Gap between employment rate of disabled people and non-disabled people, SCR, WMCA and UK

Source: IES analysis of Annual Population Survey. Dates denote the midpoint for that twelve-month estimate (most recent data is for July 2020 to June 2021)

Figure 4.14: Gap between employment rate of ethnic minority groups and white people, SCR, WMCA and UK

Source: IES analysis of Annual Population Survey. Dates denote the midpoint for that twelve-month estimate (most recent data is for July 2020 to June 2021).

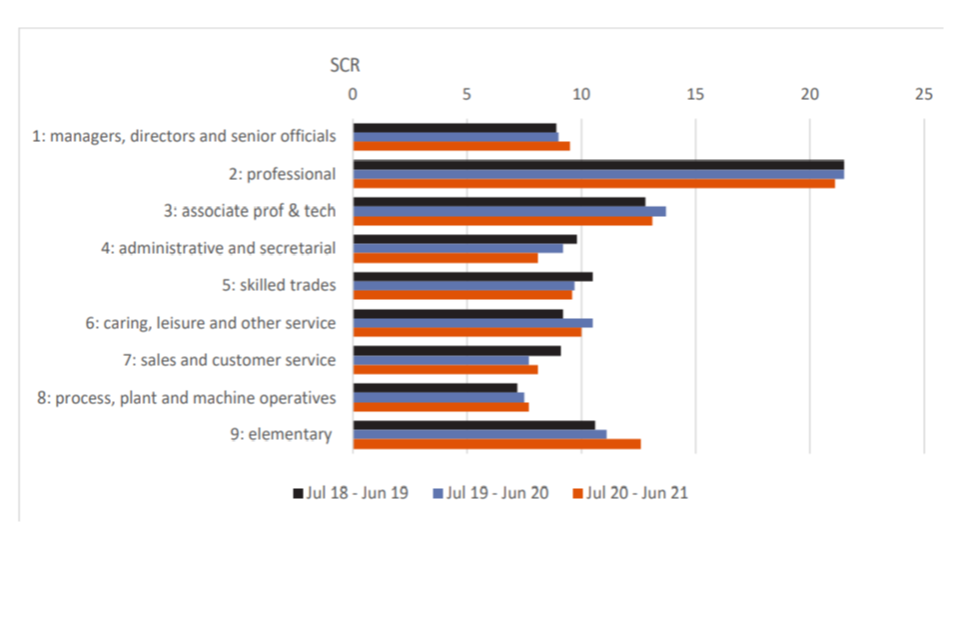

4.4 Trends in employment by occupation

The pandemic saw significant changes nationally in employment by occupation, with large falls in lower skilled work, (particularly driven by hospitality, cleaning and taxi driving), falls in skilled trades (especially construction related), but also increases in professional and scientific jobs, including technology and pandemic related work, and in public service administration. Many of these effects were directly due to lockdowns and the response to the pandemic. However, there are also signs of more lasting changes, and in particular a continued shift towards higher skilled work.

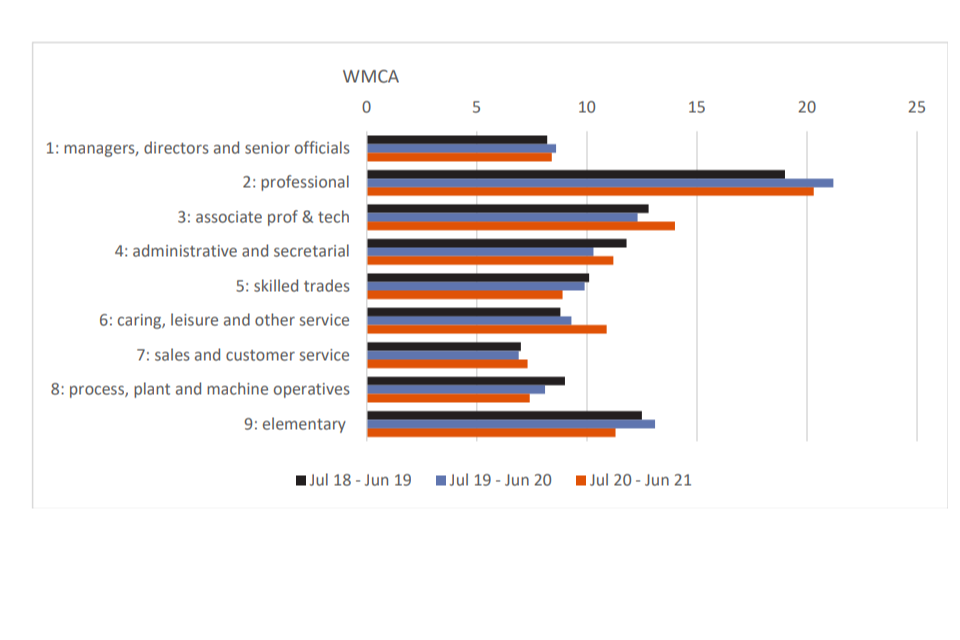

Within WMCA and SCR, analysis by main occupational group (Standard Occupational Codes 1 to 9) suggests a broadly similar picture, albeit with important differences between the regions. Figure 4.15 below illustrates this. The top panel, for WMCA, shows in common with the UK as a whole there were significant declines in employment in lower skilled work and in skilled trades. However, WMCA also saw significant growth in care jobs, which was not seen nationally over the same period.

For SCR (the bottom panel), there were some appreciably different trends, in particular a growth in ‘elementary’ jobs (explored in more detail below), no growth in administrative work or caring, but a smaller fall in skilled trades. Employment in more highly skilled professions also declined, and in both regions was less positive than for the UK as a whole.

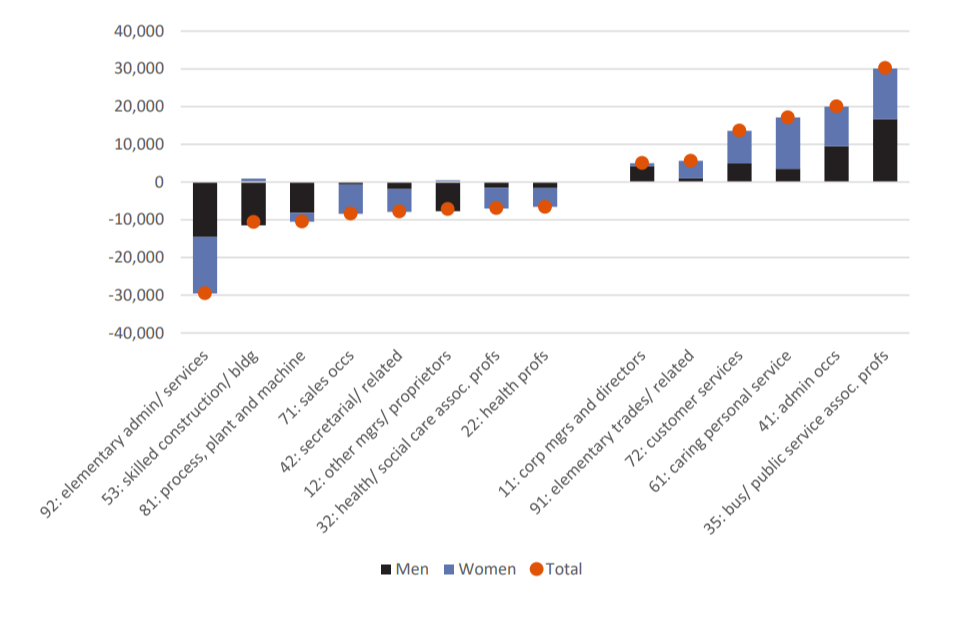

More detailed analysis by two-digit code is set out in Figure 4.16 for WMCA and in Figure 4.17 for SCR. These present occupations with the largest falls and rises, with the cut-off being those falls and rises that account for more than about 5% of the total change in employment. These data should be treated with caution due to sample sizes, but do give some more pointers to what may have been driving the relative performance of the two regions.

In the WMCA the largest fall was in elementary administration and services, which includes most bar and restaurant staff as well as cleaners. This also shows that the falls related to construction particularly affected men, while falls in secretarial work and some health professions were primarily among women (counterintuitively, the pandemic overall has seen employment fall in a number of health professions including nursing). At the same time, the occupations with highest growth appear to have benefited women more than men, in administrative roles, customer services and social care.

SCR also saw falls in health professions (affecting both women and men), as well as large declines in jobs related to leisure and transport (likely taxi drivers). However, unlike WMCA, jobs in administration and customer service appeared to decline, while sales jobs, elementary administration and services actually increased. On the latter category, given the disproportionate impact of the pandemic on hospitality, this suggests that other jobs within this group rose by enough to offset this, perhaps including industrial cleaning or storage (for example, related to online deliveries).

In the context of the HLTs, this analysis suggests that in both regions there will have been real challenges for entry level employment, which would have been further exacerbated by the fact that many ‘employed’ people were off work on furlough.

Real-time vacancy data suggest that job openings remained well below pre-pandemic levels until early 2021. Nonetheless, the apparent strong growth in some categories for example, in ‘elementary’ jobs in SCR, and social care in WMCA, suggests that both labour markets continued to create opportunities through the pandemic in the sorts of roles that have in the past been filled by people supported through employment programmes.

Figure 4.15: Employment by broad occupation group, WMCA and SCR, 2018 to 2019, 2019 to 2020 and 2020 to 2021 (%)

Source: IES analysis of Annual Population Survey

Figure 4.16: Occupations (two-digit standard occupational classification (SOC)) with largest falls and largest rises, 2019/2020 to 2020/2021, WMCA

Source: IES analysis of Annual Population Survey

Figure 4.17: Occupations (two-digit SOC) with largest falls and largest rises, 2019/2020 to 2020/2021, SCR

Source: IES analysis of Annual Population Survey

4.5 Flows out of claimant unemployment

All of the analysis presented above sets out levels (and changes in levels) of employment, rather than the underlying flows into work. Unfortunately, there is no reliable data on labour market flows to local levels, but it is possible to use the ‘Alternative Claimant Count’ data to construct an estimate of the rate of off-flow from the searching for work conditionality group. This shows the proportion of those who are in the benefit group who went on to leave the benefit group in the following month. It does not tell us whether that exit was to work or to another benefit group, but if there is no change in rates of off-flow to non-work destinations then it is reasonable to infer that any changes in the trend overall reflect changes in the rate of exits to work.

Figure 4.18 below sets out the estimated off-flow rates for the two trial sites and nationally, since 2019. This suggests that off-flow rates averaged around 15% a month nationally prior to the pandemic, but were at barely half this rate through until April 2021 (with the peak in June likely reflecting people leaving benefit after the introduction of the Self Employed Income Support Scheme, and the slight recovery in October possibly reflecting a slight recovery in the labour market between lockdowns). Since April, off-flow rates have improved slightly but remain well below pre-pandemic levels.

Regarding the two labour markets, WMCA had far lower off-flow rates pre-pandemic and has lower off-flow rates now, with no sign of an appreciably different trend. SCR on the other hand has seen off-flow rates deteriorate rather more than for the UK as a whole. This could reflect either administrative or labour market factors, but if it is the latter it would suggest that UC claimants have not particularly benefited from the apparent growth in employment in elementary and sales jobs in the region.

Figure 4.18: Off-flow rate from Universal Credit ‘searching for work’ group, WMCA, SCR and GB

Source: IES analysis of Stat-XPlore. Off-flow rate calculated by dividing the number of people flowing out of the UC Searching for Work group by the stock of people in that group in the prior month

4.6 Conclusion