Welsh Income Tax Outturn Statistics: 2020 to 2021

Published 7 July 2022

© Crown copyright 2022

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/statistics/welsh-income-tax-outturn-statistics-2020-to-2021/welsh-income-tax-outturn-statistics-2020-to-2021

1. Overview

The aim of these Experimental Statistics is to provide users with information of interest in relation to net non-savings non-dividends (NSND) Income Tax for Welsh taxpayers. Information is also provided on Welsh Rates of Income Tax (WRIT) specifically.

This publication also shows:

- how many Welsh taxpayers are liable at each rate of tax

- the Outturn of Welsh NSND Income Tax revenue at each rate of tax

- an estimate for how much NSND Income Tax paid by Welsh taxpayers is collected via Pay As You Earn (PAYE) and how much via payments made in Self Assessment (SA)

Additionally, these tables also provide equivalent information for rest of UK (rUK) taxpayers on the same basis so comparisons can be made. References to tables throughout this bulletin refer to the statistical tables released alongside this bulletin, not the tables within the bulletin. References to tables labelled with letters pertain to the tables present within the bulletin.

Calculations in this bulletin (for example, on the average tax paid by taxpayers) are based on unrounded numbers so may not match calculations based on figures in the statistical release which are rounded.

1.1 What does it mean that these are Experimental Statistics?

Experimental Statistics are statistics that are within their development phase and are published in order to involve potential users at an early stage in building a high-quality set of statistics that meet user needs.

The Experimental Statistics label highlights to users that HM Revenue and Customs (HMRC) are still working on further developing the style and content for the tables and commentary in this publication.

It should be emphasised that the label of Experimental Statistics does not mean that the statistics are of low quality, but it does signify that the statistics are novel and what statistics are reported and how is still being developed.

2. Main Findings

2.1 NSND Income Tax for all Welsh Taxpayers

The total amount of NSND Income Tax paid by Welsh taxpayers in 2020 to 2021 was £4,896 million, an increase of 5.1% compared to 2019 to 2020.

- £3,686 million (75.3%) was at the basic rate

- £1,003 million (20.5%) was at the higher rate

- £208 million (4.2%) was at the additional rate

There were 1,372,400 Welsh taxpayers who contributed towards this by having some net Income Tax liability on their non-saving non-dividend (NSND) income, an increase of 1.9% compared to 2019 to 2020.

Of these:

- 1,266,700 (92.3%) were basic rate taxpayers

- 101,400 (7.4%) were higher rate taxpayers

- 4,300 (0.3%) were additional rate taxpayers

2.2 Welsh Rates of Income Tax

The final outturn of Welsh Rates of Income Tax (WRIT) is based on 10 percentage points (ppts) of each Income Tax band. See section 3.1 for more details on WRIT.

The final outturn of Welsh Rates of Income Tax (WRIT) in 2020 to 2021 was £2,140 million, an increase of 4.9% compared to 2019 to 2020.

Of this:

- £1,843 million (86.1%) was at the basic rate

- £251 million (11.7%) was at the higher rate

- £46 million (2.2%) was at the additional rate

The equivalent 10 ppt NSND Income Tax revenue for rUK was £60,672 million, an increase of 1.9% compared to 2019 to 2020.

Of this:

- £41,541 million (68.5%) was at the basic rate

- £11,421 million (18.8%) was at the higher rate

- £7,710 million (12.7%) was at the additional rate

3. Background

3.1 What are Welsh Rates of Income Tax?

From April 2019, the UK government transferred 10 percentage points (ppt) of each of the three main rates of Income Tax – basic, higher and additional rate – paid by Welsh taxpayers to the Welsh Government (WG). The Welsh Government now controls these three Welsh Rates of Income Tax (WRIT).

The combination of reduced UK rates plus the Welsh rates determines the overall rate of Income Tax paid by Welsh taxpayers.

The equivalent outturn for NSND Income Tax for Rest of UK (rUK) taxpayers in these statistics is used by HM Treasury to adjust the Welsh Government’s Block Grant, consistent with its fiscal framework agreement.

Tables 1, 2 and 4 (and the commentary around them) of the statistical release details all NSND Income Tax generated by Welsh taxpayers. Table 3 however pertains to WRIT, specifically.

3.2 Definitions of ‘non-savings non-dividends’ and ‘rUK’

The statistics in Tables 1 to 4 provide information on Income Tax due on non-saving non-dividend (NSND) income. NSND income includes earnings from employment, pensions, profits from self-employed sources and property. Only Income Tax due on NSND income is devolved to Wales. These tables provide a comparison of how total NSND Income Tax for Welsh taxpayers compares to that of taxpayers in rUK. As Income Tax due on NSND income is also devolved to Scotland, rUK is defined as England and Northern Ireland (ENI). HMRC publishes separate statistics on Scottish Income Tax.

Tax on NSND income in these tables is measured as the Income Tax liability expected to be collected by HMRC. The statistics also incorporate an adjustment to reflect reliefs which are not allocated to individual taxpayer accounts.

Taxpayers in these tables are defined as individuals who have some net NSND Income Tax liability due after reliefs have been deducted from their Income Tax bill.

In Tables 2 and 3, taxpayers have been assigned to a marginal tax rate (the Income Tax band that a taxpayer would pay their next pound of Income Tax into) based solely on their NSND Income Tax, however, it is possible that they have paid tax at a higher rate on their savings/dividend income.

3.3 Established liabilities and where tax is paid

Employers and pension providers must normally operate PAYE as part of their payroll. PAYE is HMRC’s system to collect Income Tax and National Insurance (NI) from employments and is largely paid in the same year as the taxable activity. When an employer pays their employees through payroll, they also need to make tax and NI deductions for PAYE. Employers are then obliged to report the amount of these payments and deductions to HMRC as well as paying the tax and NI deducted to HMRC.

An individual is required to file a Self Assessment (SA) return if they meet certain criteria. This is required even for individuals who also pay employment income into the PAYE system, if a requirement for filing in SA is met. SA returns are generally submitted in the year after the taxable activity has taken place, and the SA return filing deadline is typically nine months after the tax year has ended.

For the outturn calculation, an individual who files an SA return will have all their Income Tax liability established (reconciled) in SA when they submit their return, even if they have had some tax deducted through PAYE.

An individual who is not required to file in SA will have their liability established in PAYE when their tax information is reconciled by the National Insurance and PAYE Service (NPS).

Table 4 shows the system that established NSND Income Tax liabilities are paid through; that is ‘collected at source’ (PAYE) or paid through SA. This split in table 4 is different to the split of established liabilities in table 1, which is based on the system which the individuals’ liabilities are reconciled in.

For example, an individual earning income from an employment and additional sources may have their employment Income Tax deducted from their pay by their employer, whilst also paying Income Tax for additional income (e.g. property income) by filing an SA return. In this case, all Income Tax for this taxpayer is recorded in the SA Established component of the outturn as this is where the record will be reconciled. However, amounts paid will be split between PAYE and SA accordingly, as is reflected in table 4.

4. Welsh NSND Income Tax outturn and rUK comparison

4.1 Outturn components

Table 1 of the statistical release shows how each component of the outturn is combined to calculate total NSND Income Tax for Welsh taxpayers. The same breakdown is also available for Scotland and rUK. Please see section 7 for further information on the outturn components.

Overall, Welsh Income Tax grew more than rUK Income Tax (5.1% compared to 2.0%). Growth was especially strong in Welsh SA Established Liability (7.7%).

The largest components of the outturn are SA and PAYE Established Liability. More NSND Income Tax liability is established through PAYE in Wales whilst more is established through SA in rUK.

This disparity is evident in Table 1 where 57.5% of rUK liabilities are reconciled in the SA Established component, whilst the equivalent figure is 36.7% for Wales. This is likely caused by a significantly higher proportion of Self-Assessment Returns being filed by rUK taxpayers in contrast to Welsh taxpayers

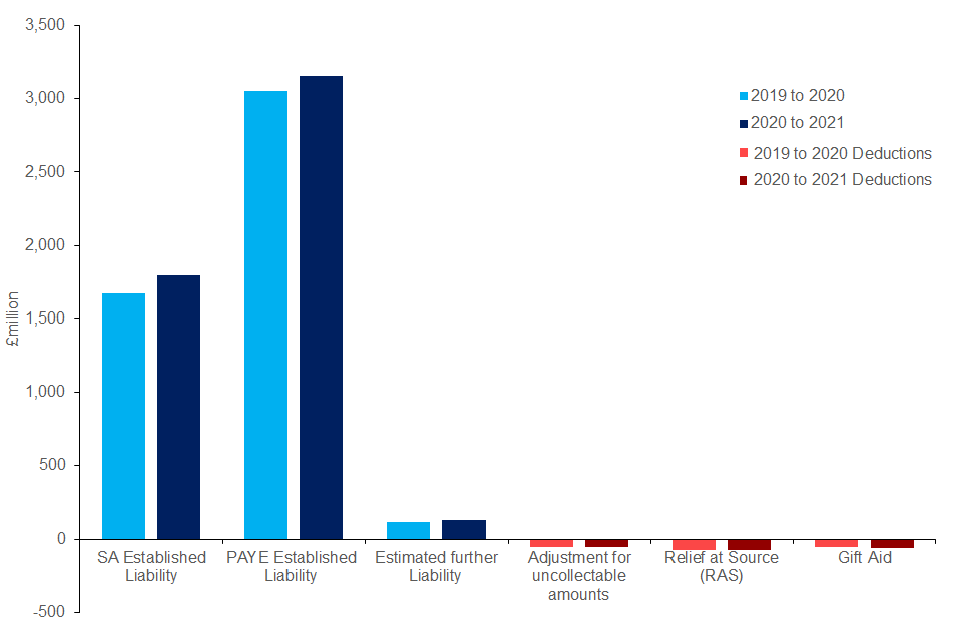

Figure 1: Breakdown of NSND Income Tax for Welsh taxpayers by component, 2019 to 2020 and 2020 to 2021

Table A: Breakdown of NSND Income Tax for Welsh taxpayers by component, 2019 to 2020 and 2020 to 2021

| 2019 to 2020 Welsh NSND Income Tax | 2020 to 2021 Welsh NSND Income Tax | |

|---|---|---|

| SA Established Liability | £1,670 million | £1,799 million |

| PAYE Established Liability | £3,055 million | £3,153 million |

| Estimated further Liability | £116 million | £129 million |

| Adjustment for uncollectable amounts | -£52 million | -£51 million |

| Relief at Source (RAS) | -£75 million | -£76 million |

| Gift Aid | -£54 million | -£58 million |

| Total | £4,660 million | £4,896 million |

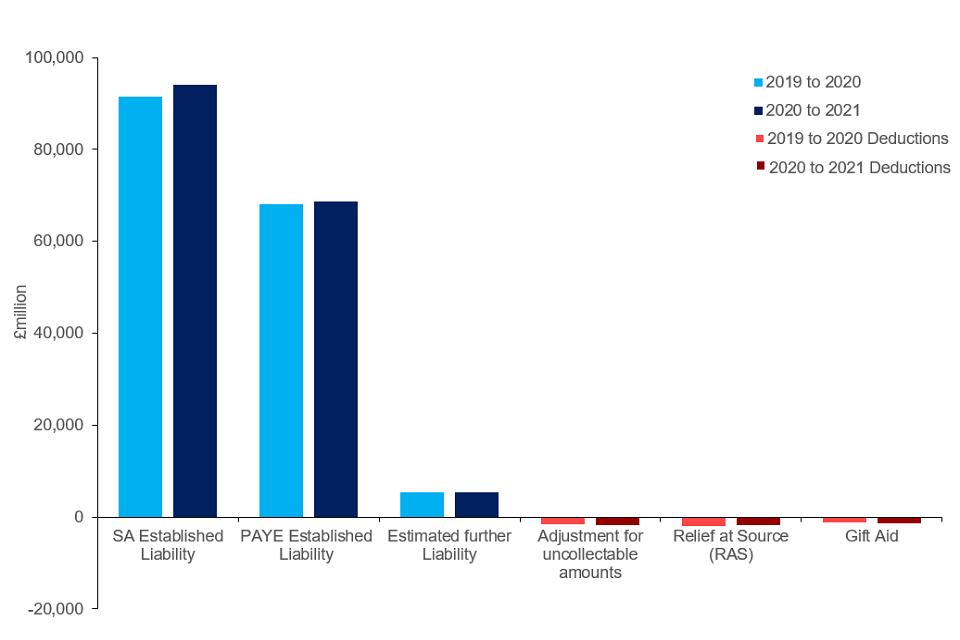

Figure 2: Breakdown of NSND Income Tax for rUK taxpayers by component, 2019 to 2020 and 2020 to 2021

Table B: Breakdown of NSND Income Tax for rUK taxpayers by component, 2019 to 2020 and 2020 to 2021

| 2019 to 2020 rUK NSND Income Tax | 2020 to 2021 rUK NSND Income Tax | |

|---|---|---|

| SA Established Liability | £91,454 million | £94,068 million |

| PAYE Established Liability | £68,177 million | £68,761 million |

| Estimated further Liability | £5,410 million | £5,461 million |

| Adjustment for uncollectable amounts | -£1,580 million | -£1,694 million |

| Relief at Source (RAS) | -£1,935 million | -£1,841 million |

| Gift Aid | -£1,221 million | -£1,294 million |

| Total | £160,305 million | £163,460 million |

Although the SA Established component constitutes the majority of reconciled rUK liabilities, the majority of NSND Income Tax is collected at source (through a PAYE scheme). Table 4 of the statistical release shows 85.0% of all rUK liabilities are collected through PAYE.

The equivalent split for Wales is 89.4% and 10.6% collected through PAYE and SA, respectively. Income Tax liabilities paid through SA have increased by £99 million or 22.5% between the 2019 to 2020 tax year and the 2020 to 2021 tax year

The lower proportion of tax collected at source in Wales compared to rUK is partially caused by a higher proportion of rUK taxpayers being required to submit SA returns compared to Welsh taxpayers.

Table C: Established Welsh NSND Income Tax by collection method, 2019 to 2020 and 2020 to 2021 inclusive

| 2019 to 2020 Welsh NSND Income Tax | 2020 to 2021 Welsh NSND Income Tax | |

|---|---|---|

| Collected at Source | £4,400 million (90.9%) | £4,540 million (89.4%) |

| Paid through SA | £442 million (9.1%) | £541 million (10.6%) |

| Total NSND Income Tax | £4,660 million | £4,896 million |

4.2 Tax liabilities by band – all NSND Income Tax

Table 2 of the statistical release provides breakdowns of all NSND Income Tax liabilities by tax band and taxpayer types (defined by their highest marginal rate; the Income Tax band that a taxpayer would pay their next pound of Income Tax into).

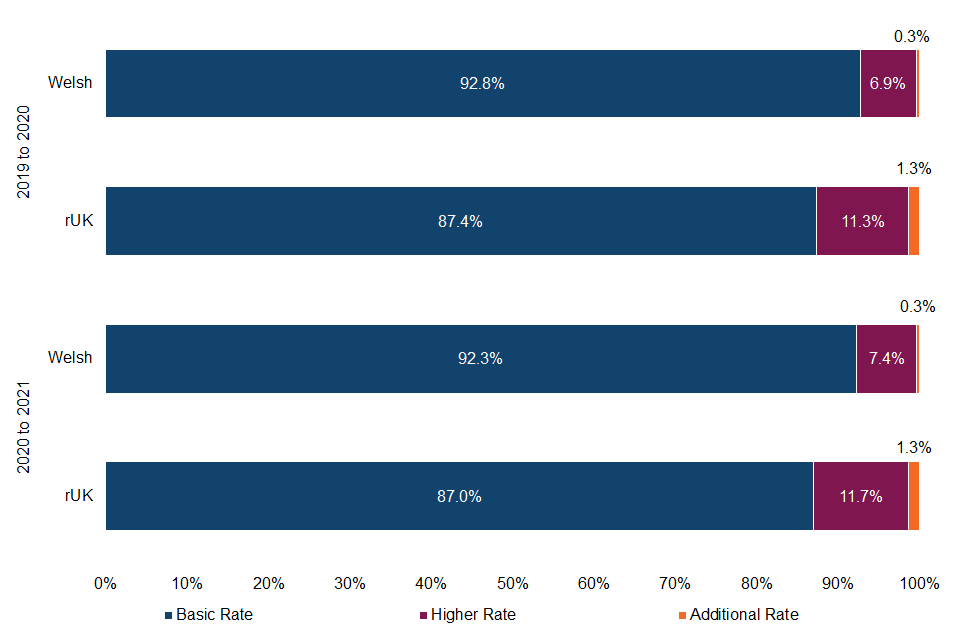

There was a slight increase in the proportion of higher rate taxpayers in Wales (7.4% in 2020 to 2021 compared to 6.9% in 2019 to 2020).

Figure 3: Share of Welsh and rUK taxpayers by their marginal tax rate, 2019 to 2020 and 2020 to 2021

Table D: Share of Welsh and rUK taxpayers classified by their marginal tax rate, 2019 to 2020 and 2020 to 2021

| 2019 to 2020 Welsh Taxpayers | 2019 to 2020 rUK Taxpayers | 2020 to 2021 Welsh Taxpayers | 2020 to 2021 rUK Taxpayers | |

|---|---|---|---|---|

| Basic Rate Taxpayers | 92.8% | 87.4% | 92.3% | 87.0% |

| Higher Rate Taxpayers | 6.9% | 11.3% | 7.4% | 11.7% |

| Additional Rate Taxpayers | 0.3% | 1.3% | 0.3% | 1.3% |

The table highlights that although higher rate or additional rate taxpayers make up a relatively small percentage of the total Welsh taxpayer population (7.7%), they are liable for over two fifths (40.7%) of NSND Income Tax in Wales. This figure (40.7%) is an increase of 0.8 ppts compared to the 2019 to 2020 tax year.

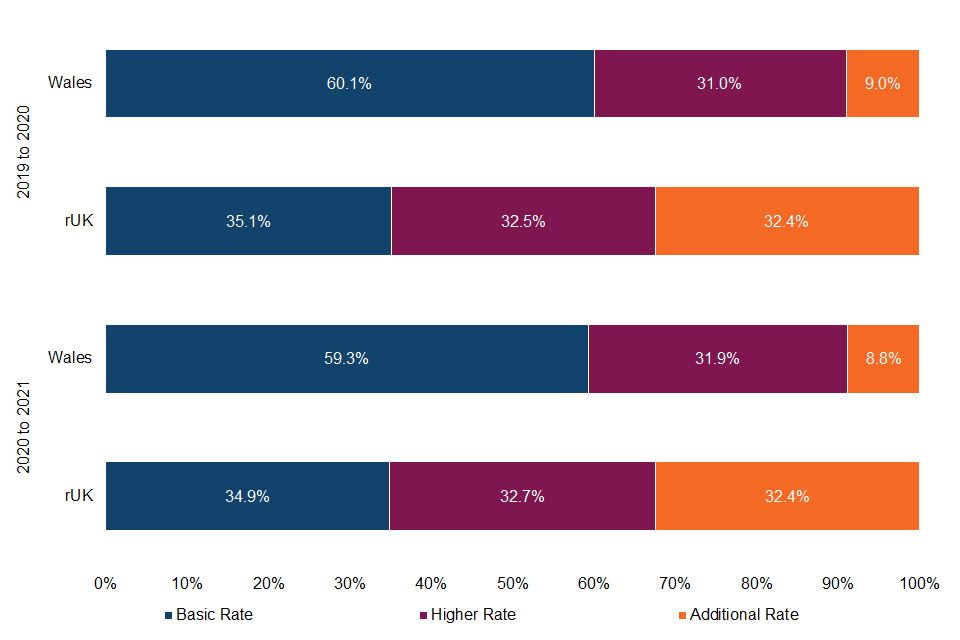

The breakdown of tax paid by different taxpayer types is very different in Wales and rUK. The majority of Welsh NSND Income Tax is paid by basic rate taxpayers (59.3%). Though this percentage has decreased from 60.1% in 2019 to 2020.

The most noticeable disparity is at the additional rate – as only 9 out of every 100 pounds of Welsh NSND Income Tax is paid by additional rate taxpayers. This figure has declined from the previous year, down from 9.0% to 8.8%. The equivalent figure for rUK is 32.4% in the 2020 to 2021 tax year.

Figure 4: Proportion of Welsh and rUK NSND Income Tax paid by each taxpayer type, 2019 to 2020 and 2020 to 2021

Table E: Proportion of Welsh and rUK NSND Income Tax paid by each taxpayer type, 2019 to 2020 and 2020 to 2021

| 2019 to 2020 Welsh Taxpayers | 2019 to 2020 rUK Taxpayers | 2020 to 2021 Welsh Taxpayers | 2020 to 2021 rUK Taxpayers | |

|---|---|---|---|---|

| Basic Rate Taxpayers | 60.1% | 35.1% | 59.3% | 34.9% |

| Higher Rate Taxpayers | 31.0% | 32.5% | 31.9% | 32.7% |

| Additional Rate Taxpayers | 9.0% | 32.4% | 8.8% | 32.4% |

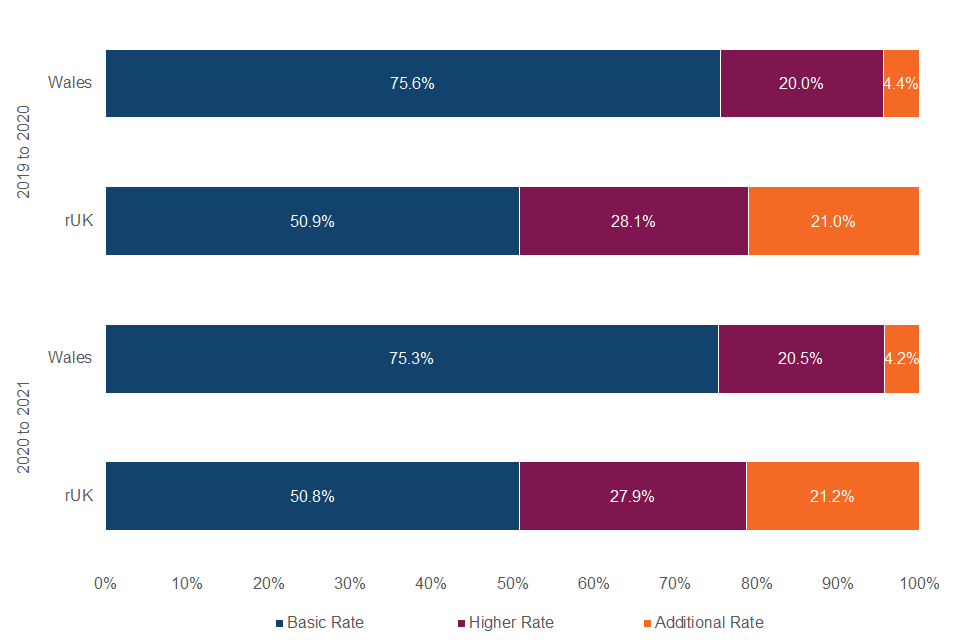

At the Income Tax band level, the share of NSND Income Tax is more orientated towards the lower Income Tax Bands in Wales. In the 2020 to 2021 tax year, 75.3% of Welsh NSND Income Tax was liable at the basic rate, with 20.5% at the higher rate and 4.2% at the additional rate.

This contrasts to rUK where the split is more even, with 50.8% of rUK NSND Income Tax revenue paid at the basic rate, 27.9% at the higher rate and 21.2% at the additional rate in the 2020 to 2021 tax year.

For both regions, this split is relatively consistent between the 2019 and 2020 and 2020 and 2021 tax years.

Figure 5: Share of Welsh and rUK NSND Income Tax by Income Tax band, 2019 to 2020 and 2020 to 2021

Table F: Share of Welsh and rUK NSND Income Tax by Income Tax band, 2019 to 2020 and 2020 to 2021

| 2019 to 2020 Welsh NSND Income Tax | 2019 to 2020 rUK NSND Income Tax | 2020 to 2021 Welsh NSND Income Tax | 2020 to 2021 rUK NSND Income Tax | |

|---|---|---|---|---|

| Basic Rate | 75.6% | 50.9% | 75.3% | 50.8% |

| Higher Rate | 20.0% | 28.1% | 20.5% | 27.9% |

| Additional Rate | 4.4% | 21.0% | 4.2% | 21.2% |

4.3 Average Amounts of NSND Income Tax Liability

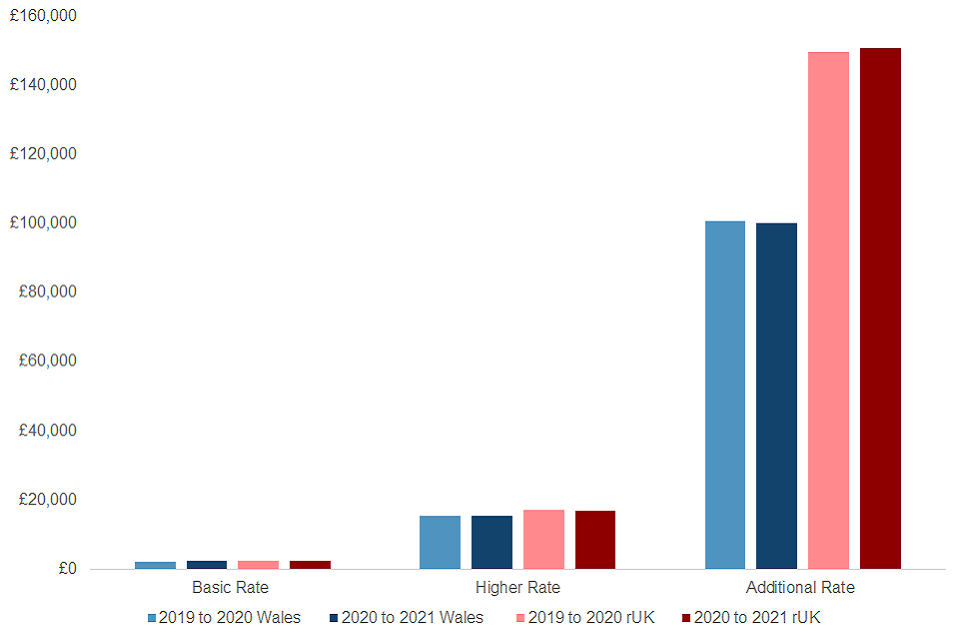

Overall, the average NSND Income Tax paid by Welsh taxpayers increased by £108 and by £95 for rUK taxpayers between the 2019 to 2020 and 2020 to 2021 tax year.

While the total NSND Income Tax paid by Welsh additional rate taxpayers has increased by around £10 million in the 2020 to 2021 tax year, the average NSND Income Tax paid by Welsh additional rate taxpayers has decreased by £681 due to the higher number of additional rate taxpayers. The equivalent figure for rUK is an increase of £1,216.

Figure 6: Average NSND Income Tax paid by each taxpayer type, 2019 to 2020 and 2020 to 2021

Table G: Average NSND Income Tax paid by each taxpayer type, 2019 to 2020 and 2020 to 2021

| 2019 to 2020 Welsh NSND Income Tax | 2019 to 2020 rUK NSND Income Tax | 2020 to 2021 Welsh NSND Income Tax | 2020 to 2021 rUK NSND Income Tax | |

|---|---|---|---|---|

| Basic Rate Taxpayers | £2,240 | £2,392 | £2,292 | £2,428 |

| Higher Rate Taxpayers | £15,455 | £17,155 | £15,424 | £16,927 |

| Additional Rate Taxpayers | £100,793 | £149,648 | £100,112 | £150,864 |

| All Taxpayers | £3,460 | £5,958 | £3,568 | £6,053 |

4.4 Tax liabilities by band – Welsh Rates of Income Tax

Table 3 of the statistical release provides breakdowns of WRIT NSND Income Tax liabilities grouped by both Income Tax band and Marginal taxpayer types. It compares this 10ppts wedge with the comparable wedge in rUK tax liabilities. These WRIT and corresponding rUK figures are used by HM Treasury to determine adjustments to the Welsh Government’s Block Grant.

The total WRIT figure grew by 4.9% in the 2020 to 2021 tax year, compared to 1.9% in the comparable rUK wedge.

Table H: WRIT and comparable rUK NSND Income Tax, 2019 to 2020 and 2020 to 2021

| 2019 to 2020 WRIT | 2019 to 2020 Comparable rUK NSND Income Tax | 2020 to 2021 WRIT | 2020 to 2021 Comparable rUK NSND Income Tax | |

|---|---|---|---|---|

| Basic Rate | £1,761 million | £40,765 million | £1,843 million | £41,541 million |

| Higher Rate | £233 million | £11,263 million | £251 million | £11,421 million |

| Additional Rate | £45 million | £7,494 million | £46 million | £7,710 million |

| Total | £2,040 million | £59,222 million | £2,140 million | £60,672 million |

Since WRIT only accounts for 10ppts per tax band, a higher proportion of WRIT comes from tax at the basic rate compared to all NSND Income Tax from Welsh taxpayers as the basic rate is 20%.

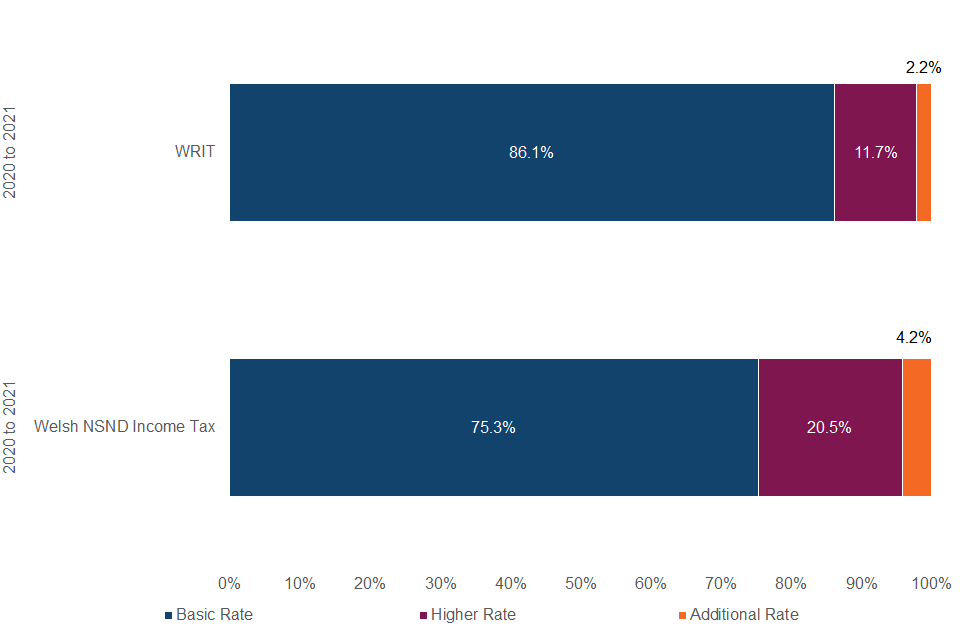

Figure 7: Comparison of WRIT and Welsh NSND Income Tax proportions by Income Tax Band, 2020 to 2021

Table I: Comparison of WRIT and Welsh NSND Income Tax proportions by Income Tax Band, 2020 to 2021

| 2020 to 2021 WRIT | 2020 to 2021 All Welsh NSND Income Tax | |

|---|---|---|

| Basic Rate | 86.1% | 75.3% |

| Higher Rate | 11.7% | 20.5% |

| Additional Rate | 2.2% | 4.2% |

5. Indicative In-Year Welsh Income Tax

5.1 Background

HMRC provides in year monitoring data for Welsh Income Tax from RTI data, to the Welsh Government (WG) and the Office for Budget Responsibility (OBR) each month.

Table 5 of the statistical release shows the Income Tax statistics that HMRC shares as a monthly time series. It shows the amount of UK Income Tax withheld by employers on behalf of their employees (as reported in RTI) and the proportion of tax from Welsh taxpayers. The table also contains amounts of Income Tax withheld on behalf of Scottish taxpayers.

The Income Tax measure in Table 5 is not equivalent to that presented in Tables 1 to 4 as Income Tax in RTI will include amounts for reserved charges other than NSND Income Tax. For example, any tax code adjustments to account for Savings and Dividend Income or High Income Child Benefit Tax charge (HICBC), which are not devolved to the Welsh government. See section 7.7 for more detail on the caveats of RTI figures.

However, it is a useful guide of the in-year Income Tax paid by Welsh taxpayers prior to the publication of the Outturn statistics.

Welsh taxpayers are identified using the Welsh indicator variable provided by NPS (see section 6.1 for more details of how Welsh taxpayers are defined in NPS).

Although, the tax figures are updated for each month during the in-year monthly process. The final RTI monthly time series will generally not be updated following the end of the tax year.

5.2 Income Tax reported as withheld from RTI

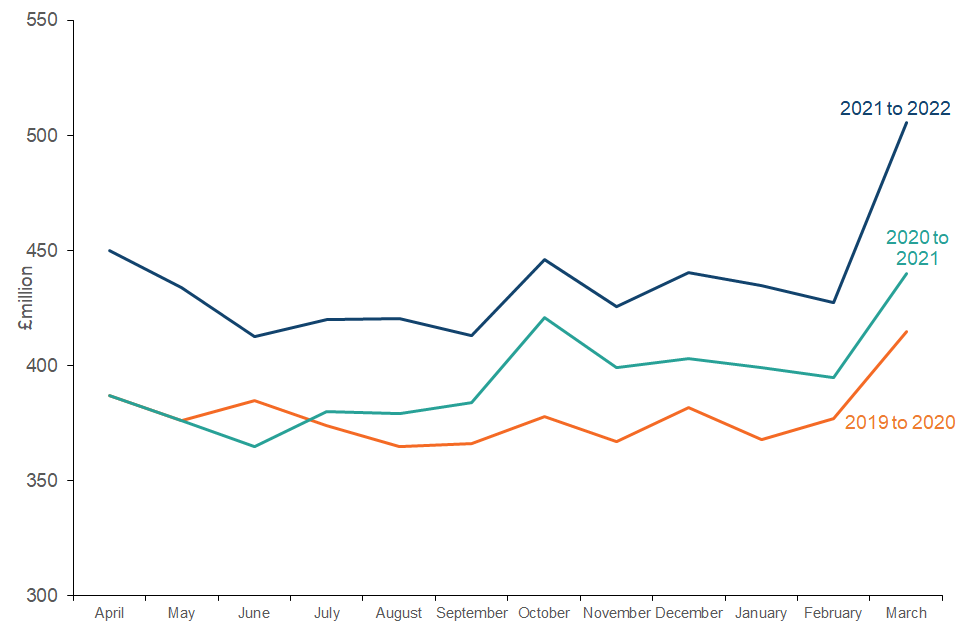

The monthly time series of tax withheld in RTI is relatively similar for Welsh and rUK taxpayers. There is a clear spike in tax in March each year and this reflects when bonuses are generally paid, at the end of the tax year.

Smaller spikes throughout the tax year may be caused by in-year bonuses and redundancies.

Figure 8: RTI Income Tax reported as withheld for Welsh taxpayers, 2019 to 2020, 2020 to 2021 and 2021 to 2022

Table J: RTI Income Tax reported as withheld for Welsh taxpayers, 2019 to 2020, 2020 to 2021 and 2021 to 2022

| Month | 2019 to 2020 | 2020 to 2021 | 2021 to 2022 |

|---|---|---|---|

| April | £387 million | £387 million | £450 million |

| May | £376 million | £376 million | £434 million |

| June | £385 million | £365 million | £413 million |

| July | £374 million | £380 million | £420 million |

| August | £365 million | £379 million | £420 million |

| September | £366 million | £384 million | £413 million |

| October | £378 million | £421 million | £446 million |

| November | £367 million | £399 million | £426 million |

| December | £382 million | £403 million | £441 million |

| January | £368 million | £399 million | £435 million |

| February | £377 million | £395 million | £427 million |

| March | £415 million | £440 million | £505 million |

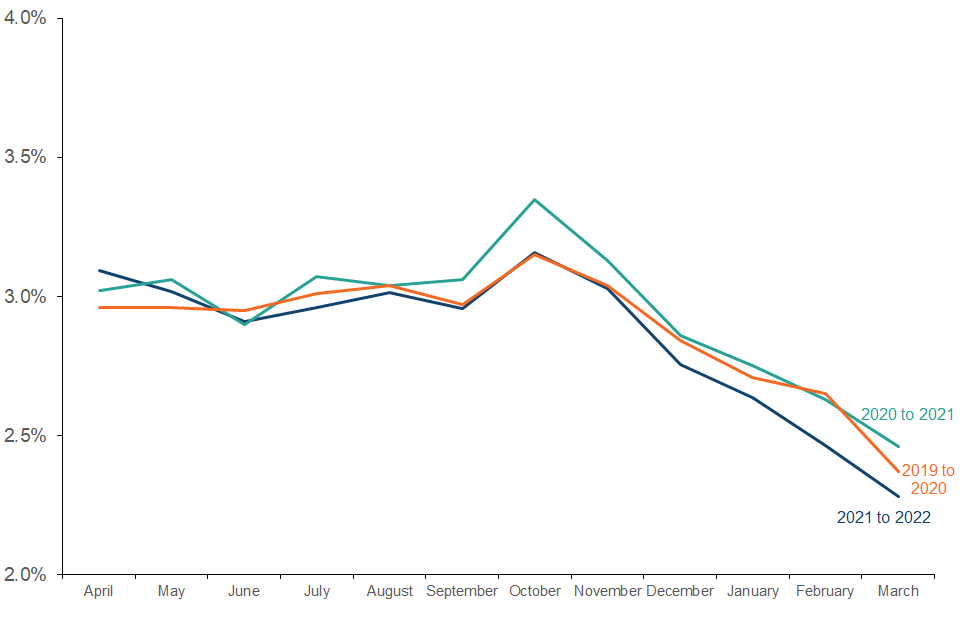

The Welsh share of whole UK RTI Income Tax has followed a similar trend in 2021 to 2022 compared to previous tax years. The share is relatively consistent across most of the year but decreases towards the end of the tax year.

In-year peaks may arise when businesses largely based in Wales pay bonuses or redundancy payments.

Following on from the October peak, the Welsh share exhibits a gradual decline up until it reaches a low point of around 2.3% in March. This likely reflects bonus payments forming a smaller proportion of remuneration for Welsh employees compared to rUK.

This overall share has reduced to 2.82% in 2021 to 2022 compared to a high of 2.92% in the 2020 to 2021 tax year.

Figure 9: Welsh share of RTI Income Tax reported as withheld, 2019 to 2020 through to 2021 to 2022

Table K: Welsh share of RTI Income Tax reported as withheld, 2019 to 2020 through to 2021 to 2022

| Month | 2019 to 2020 | 2020 to 2021 | 2021 to 2022 |

|---|---|---|---|

| April | 2.96% | 3.02% | 3.09% |

| May | 2.96% | 3.06% | 3.02% |

| June | 2.95% | 2.90% | 2.91% |

| July | 3.01% | 3.07% | 2.96% |

| August | 3.04% | 3.04% | 3.01% |

| September | 2.97% | 3.06% | 2.96% |

| October | 3.15% | 3.35% | 3.16% |

| November | 3.04% | 3.13% | 3.03% |

| December | 2.84% | 2.86% | 2.75% |

| January | 2.71% | 2.75% | 2.64% |

| February | 2.65% | 2.63% | 2.47% |

| March | 2.37% | 2.46% | 2.28% |

| Average | 2.87% | 2.92% | 2.82% |

6. Definitions

6.1 Who is a Welsh taxpayer?

The definition of a Welsh taxpayer is based on where an individual resides in the course of a tax year. Welsh taxpayer status applies for a whole tax year – it is not possible to be a Welsh taxpayer for part of a tax year.

For most taxpayers, the location where they live will be obvious, but there will be less straightforward cases – for example, where people have more than one home, or have moved into or out of Wales during the year. HMRC has provided guidance to help in these circumstances.

The location of a person’s employer is not relevant. So, for example, someone who works in Wales, but has their home elsewhere in the UK, will not be a Welsh taxpayer.

Detailed guidance to whom Welsh Income Tax will apply

6.2 How do the tax systems on NSND income compare for Welsh and rUK taxpayers?

From April 2019, the UK government transferred 10 percentage points (ppt) of each of the three main rates of Income Tax – Basic, Higher and Additional rate – paid by Welsh taxpayers to the Welsh Government (WG). The Welsh Government now controls these three Welsh Rates of Income Tax (WRIT).

The combination of reduced UK rates plus the Welsh rates determines the overall rate of Income Tax paid by Welsh taxpayers – meaning that Welsh taxpayers and rUK taxpayers currently pay the same Income Tax rates.

Table L: Welsh and rUK Income Tax Thresholds, 2020 to 2021

| Tax Band Threshold | Welsh Income Tax 2020 to 2021 | Rest of UK 2020 to 2021 |

|---|---|---|

| Personal Allowance | £12,500 | £12,500 |

| Higher rate threshold | £50,000 | £50,000 |

| Additional rate threshold | £150,000 | £150,000 |

Table M: NSND Income Tax rates for Welsh, WRIT and rUK Income Tax, 2020 to 2021

| Tax Rates | UK Government Rates in Wales 2020 to 2021 | WIRT 2020 to 2021 | Overall Income Tax Rates 2020 to 2021 |

|---|---|---|---|

| Basic Rate | 10% | 10% | 20% |

| Higher Rate | 30% | 10% | 40% |

| Additional Rate | 35% | 10% | 45% |

6.3 Why are we producing these statistics?

The WRIT outturn in HMRC’s Annual Report determines the WG’s Income Tax revenues whilst the equivalent outturn for Income Tax on NSND income for rUK taxpayers in these statistics (Table 3 of the statistical release) is used by HMT to determine adjustments to the WG’s Block Grant. For Block Grant purposes the total outturn figures presented in HMRC’s Annual Report and this publication are final.

These statistics are being published to give more information about NSND Income Tax paid by Welsh taxpayers.

6.4 What is the relationship between these statistics and other personal tax statistics and information?

There are other publications which show similar statistics to what is shown in this publication. It is important to understand how these other statistics relate to what is being released here and highlight differences in coverage or data used to compile each set of statistics.

The following publications are explained below:

- Devolved tax and spending forecasts (OBR)

- Personal Income Statistics from the Survey of Personal Incomes

- Earnings and Employment Statistics from PAYE Real Time Information

- Income Tax Receipts Publication

OBR: Devolved tax and spending forecasts

The OBR was established in 2010 to provide independent and authoritative analysis of the UK’s public finances. Alongside the UK Government’s Budgets and other fiscal statements, they produce forecasts for the economy and the public finances. They publish these in their Economic and Fiscal Outlook (EFO).

The OBR publish devolved tax and spending forecasts alongside each EFO that are consistent with their main UK forecasts. HM Treasury draws on the OBR’s tax forecasts when making spending settlements for the Welsh Government in accordance with their fiscal framework. The OBR also publishes updated forecasts for the devolved taxes in Wales alongside the Welsh Government’s budgets in its Welsh Taxes Outlook (WTO).

In the EFO, the OBR forecast based on the national accounts, with SA recorded in the year in which it is received. This contrasts to the OBR Devolved tax and spending publication and in the statistics set out here, where SA is recorded on a liabilities basis (i.e. in the year in which the tax liability arose).

The latest OBR devolved forecasts of WRIT were published in March 2021. This shows the OBR forecast of WRIT for 2019 to 2020 to be £2.0bn. The latest full WTO publication was published in December 2020, this was updated in June 2021 with no change to the WRIT forecast.

OBR March 2022 Devolved Tax and Spending Forecast

SPI: Personal Income Statistics

HMRC release an annual publication from the Survey of Personal Incomes (SPI) which shows statistics for taxpayers’ personal incomes. This publication provides breakdowns to highlight the number of individuals with different sources of income and subject to certain reliefs.

In March 2022 HMRC published the annual Personal Income statistics for 2019 to 2020 which are based on the SPI. The data used in the SPI publication is different to the data used in this publication.

The SPI is a sample of around 800,000 individuals in either SA or PAYE. The SPI is designed to measure total income and the total tax impact on the Exchequer and therefore includes the tax impact of RAS payments to pension providers and Gift Aid payments to charities. It also measures liability and takes no account of some tax not being collected.

There is a further HMRC publication, ‘Income Tax Statistics and Distributions’, which provides projections for future tax years based on the SPI. The projections in that publication reflect announced changes to the Income Tax system and use determinants from the OBR to model tax liabilities in future years. The latest publication of this series was released in June 2022 and provides projections for tax years 2019 to 2020 to 2022 to 2023.

Income Tax Statistics and Distributions

The statistics presented in these two publications are not expected to be consistent with what is shown in this publication. This is due to sampling variation, the measurement differences described above and the fact that projections are a forecast of how tax liabilities may evolve for future years.

RTI: Earnings and Employment Statistics

Since April 2020 HMRC and the Office for National Statistics (ONS) have jointly released monthly statistics on earnings and employment statistics using data from PAYE RTI. The aim of this publication is to provide users with information on the number of individuals receiving pay from PAYE, their mean and median pay as paid through PAYE and the total amount of pay from PAYE in each country or region of the UK.

UK Real Time Information Experimental Statistics

The statistics in the RTI earnings and employment publication are different to the RTI statistics shown in Table 5 of this statistical release, although both are compiled from the same source of data.

The RTI publication presents information relating to employees only and excludes data on payments made to occupational pensioners while this publication includes tax collected from occupational pensions as well as employments

In addition, the RTI publication only presents statistics for number of employees and their pay. This release shows tax collected via PAYE, which may include collection of tax due on other income collected via the PAYE tax code. This can arise from savings or dividend income and other charges such as the HICBC.

Income Tax Receipts Publication

HMRC publish an annual National Statistics publication on Income Tax Receipts. The statistics presented in this publication show tax liabilities for specific tax years.

Income Tax Receipts Statistics

Liabilities are amounts of tax due on incomes arising in a given tax year, whereas receipts show amounts paid and collected in a given year. Due to lags in the Income Tax payment regimes, particularly for SA, liabilities and receipts for the same year can differ significantly.

Liabilities and receipts will also differ for other reasons, for example when over or underpayments occur which are repaid or recovered in a later year altering total receipts in that year in a way unrelated to tax liabilities for that year.

7. Outturn data methodology

The methodology set out in this section reflects the methodology for calculating the outturn which has been agreed between the WG and HMRC.

The final outturn figures reflect accrued revenue and have been calculated using actual liabilities data together with some estimation where actual data is unavailable. Details of this for each of the 6 components of the outturn figure is explained below.

Total NSND outturn =

- +SA Established liability

- +PAYE established liability

- +Estimated further liability

- -Adjustment for uncollectable amounts

- -Relief at source (RAS) pension relief

- -Gift Aid

7.1 SA Established Liability

Income Tax liability is established for all individuals in SA once their SA return has been received and their tax calculation has been conducted.

This includes any individual who is required to file an SA return who also has an employment or occupational pension for which tax is deducted at source through PAYE.

The established liability for those who submit an SA return is calculated for each taxpayer identified in SA by summing the Income Tax due at each tax rate on NSND income and then reducing it by a share of reliefs.

Reliefs

Income Tax reliefs reduce the total amount of Income Tax an individual is liable to pay.

Some reliefs, such as relief for qualifying distributions and refinance relief for landlords, can only be claimed when an individual has a specific source of income. In calculating the SA established liability such reliefs are prioritised to the appropriate stream of income before any excess is apportioned to other streams of income.

All other reliefs, such as marriage allowance, married couples’ allowance and relief for gift aid payments, can be claimed irrespective of what income sources an individual has. These ‘generic’ reliefs are applied proportionately to tax due on savings/dividend income and tax due on NSND income based on the level of gross Income Tax liability.

Other SA charges and CRCs

There are other charges which can be raised against an individual in SA through investigations/assessments or via a ‘Create Return Charge’ when an individual has failed to submit their return.

These additional charges, if known when data is being compiled, are also included when determining the SA established Income Tax liability.

The charge may include other tax liabilities (for example Capital Gains Tax). The share of the charge that relates to Income Tax is therefore estimated. This is based on the share of total liability relating to Income Tax for taxpayers who have submitted their return.

Welsh share

The total SA established Welsh liability is then calculated by summing the NSND liability, net of reliefs, across each Welsh taxpayer in SA. This is done at a by band level.

Welsh taxpayers are defined by having a Welsh tax calculation in the SA system or being included in the Welsh NPS extract explained below.

The rUK established SA liability is calculated in a similar way but summing across all rUK taxpayers where rUK taxpayers are all taxpayers not included in the Scottish or Welsh NPS extracts.

Taxpayers who have indicated they were non-resident in their SA return will be counted as rUK taxpayers.

7.2 PAYE Established Liability

PAYE established liability includes:

- liabilities for individuals who are reconciled in PAYE

- PAYE settlement agreements

Individuals reconciled in PAYE

For individuals who are in PAYE but have not been issued with a notice to file in SA, their Income Tax liability is established when their PAYE account is reconciled.

A bespoke data extract of all Welsh and rUK taxpayer accounts in NPS for each tax year was commissioned specifically to assist in compiling the outturn figures.

This provided the liability for NSND income, net of reliefs, for all Welsh and rUK taxpayers by tax rate.

PAYE settlement agreements

The established PAYE amount includes a share of liabilities raised through PAYE Settlement Agreements (PSA).

A PSA allows an employer to make one annual payment to cover all the tax and National Insurance due on minor, irregular or impracticable expenses or benefits for their employees.

The expenses and benefits reflected in the PSA are not recorded through payroll and are not required to be included on end of year P11D forms, in which other employment expenses and benefits are reported to HMRC.

The Welsh share is determined by using RTI data to determine the share of tax collected by employers through PAYE schemes which have a PSA. RTI data is also used to determine how the tax is distributed across tax bands for Welsh and rUK taxpayers.

7.3 Estimated further liability

In addition to the established liability the final outturn figure includes an estimate for:

- liabilities from late filed SA returns

- liabilities realised from compliance activity

- liabilities from unreconciled PAYE cases

Late filed SA returns

The value of late filed SA returns has been estimated for each tax year by examining historic SA data to determine the pattern of SA filing in the preceding five tax years. It is assumed that the average growth of liabilities for these years will be similar to how the liabilities will grow for the years presented in these statistics.

This is performed separately for Welsh and rUK taxpayers. Taxpayers with a Welsh postcode were used as a proxy for Welsh taxpayers in these years, as no Welsh indicator exists before WRIT was introduced.

This is performed at a total level and a tax band level. The estimated value of late filed SA returns at each tax band is then scaled to the total estimated value.

Liabilities from compliance activity

Included in the estimated further liability is an amount to reflect Contract Settlement Agreements which are raised as part of compliance investigations. The Welsh and rUK NSND share (as well as the split between tax bands) of this is assumed to be the same proportion as observed in the SA established liability.

As many Contract Settlement Agreements will be raised in the tax years following the outturn, this amount is estimated. The estimate is forecast based on the total value of Contract Settlement Agreements in previous tax years and OBR’s forecast of future SA Income Tax.

For the 2020 to 2021 outturn, the forecast was slightly adjusted to take into account below average Contract Settlement Agreement receipts in the 2021 to 2022 tax year caused by COVID-19.

Liabilities from unreconciled PAYE cases

Almost all PAYE cases are reconciled within 12 months of the end of the tax year. However, complex tax affairs or operational changes means that HMRC occasionally delays some customers’ end of year reconciliations to prevent them receiving an incorrect tax calculation or accounting update.

The Income Tax liabilities for these unreconciled cases has been estimated by using data from RTI.

7.4 Adjustment for uncollectable amounts

Uncollected SA amounts

An initial amount of uncollected debt for the current outturn year is calculated by using current SA data.

The proportion of this debt that will be collected in the future is estimated by using the same historic SA data over the previous five tax years used to establish the late filed SA returns for the ‘Estimated further liability’. The average growth in the collection rate of SA liabilities observed in this historic data is applied to the initial amount of uncollected debt in the current outturn year. This is completed separately for Welsh and rUK taxpayers to calculate specific uncollected amounts for each.

This is performed at a total level and a tax band level. The estimated value of uncollected amounts at each tax band is then scaled to the total estimated uncollected amount.

Uncollected PAYE amounts

Not all tax due is collected by HMRC and some is subsequently remitted or written off when it cannot be recovered.

This component reflects the amount written off from PAYE employers when they have failed to pay all the Income Tax they were expected to.

The uncollected amount is based on HMRC PAYE Income Tax write-offs/remissions data. The data is used to calculate the value of write-offs/remissions that have already taken place for the outturn year and to forecast the value of future write-offs/remissions. These are combined to give an estimate of how much PAYE Income Tax (at a UK level) is expected to be remitted or written off in total for the outturn year. RTI PAYE data is then analysed for each PAYE scheme with a write-off/remission to calculate what proportion of total tax collected by these schemes is in respect of Welsh taxpayers.

RTI data is also used to determine how the tax is distributed across tax bands for Welsh and rUK taxpayers.

For the 2020 to 2021 outturn, a slight adjustment to the methodology was applied to estimate these uncollected amounts to account for the impact COVID-19 may have on the profile of write-offs related to the 2019 to 2020 and 2020 to 2021 tax years.

The total proportion of uncollected PAYE NSND Income Tax was assumed to be in-line with the amounts observed in pre-COVID outturn figures.

7.5 Relief At Source (RAS) pension relief

When an individual pays into a pension scheme the scheme treats this as being received net of Basic rate tax and reclaims that basic rate tax relief back from HMRC to add to the member’s pension pot.

This adjustment in the outturn calculation reflects the Basic rate tax being passed to the pension provider and no longer held as Income Tax by the exchequer.

The RAS for pension contributions in this calculation is determined by using information from annual returns made by pension schemes which show the amount of gross contributions made by scheme members in the appropriate tax year.

The proportion relating to Welsh taxpayers is calculated by identifying individual contributions made by scheme members who have a Welsh postcode held on the pension contribution data.

7.6 Gift Aid

When a taxpayer makes a charitable donation, the charity can claim Basic rate tax relief from HMRC on the value of the donation.

This adjustment in the outturn calculation reflects the Basic rate tax being passed to the charity and no longer held as Income Tax by the exchequer.

Charities can back date claims for this Basic rate tax by up to four years. Therefore, the value which will ultimately relate to a specific tax year has been estimated using previous years data.

The Welsh share has been estimated as an average of Wales’ share of the UK population and Wales’ share of total UK Income as measured by the SPI. Welsh cases were identified based on postcode as the Welsh indicator did not exist before WRIT was introduced.

7.7 HMRC RTI for PAYE methodology

The estimates in Table 4 have been sourced from data held on HMRC’s PAYE RTI administrative system. The RTI administrative system covers all individuals who have a live employment or occupational pension open on a PAYE Scheme.

Most people pay Income Tax through PAYE. This is the system that employers or pension providers use to take Income Tax and National Insurance contributions before they pay an employee’s wages or pension. An employee’s tax code tells the employer how much Income Tax to deduct.

Under RTI, employers are required to send HMRC information about tax and other deductions made through the PAYE system every time an employee is paid. Since April 2014, all employers have been required to report in real time through RTI. This provides HMRC with a very rich source of data, which can be used to better inform public understanding of the labour market.

Individuals who pay tax through the SA system are included in these statistics if they are also employed and paid via PAYE. Individuals with more complex financial affairs (for example the self-employed or those who have a high income) may also pay or be refunded Income Tax and NI through SA. Individuals in SA who are not in the PAYE system will not be included in these statistics.

Production of in-year monitoring of Welsh Income Tax withheld in RTI, provided in Table 4 of this publication, has the following caveats:

- the sum of these figures will not equate to the final outturn and are only intended to be an indication of part of the outturn (from employments covered by PAYE)

- RTI data does not include all income reported through Self Assessment such as profits from self-employment or income from property and thus only provides a partial picture of NSND Income Tax liabilities in Wales.

- Income Tax due on other sources of income such as savings interest may be collected through PAYE using a process known as coding out. This process is also used to collect amounts due for some non-Income Tax charges, such as the HICBC. Coded out tax amounts are included in RTI data and therefore appear in these figures

- RTI data in-year is subject to amendments throughout the year, and any end-of-year updates that may occur are not included

- these figures are pre-reconciliation and provisional

- the NPS flag is taken as a snapshot in time and this means that as taxpayers change residential address during the year, their status and therefore the figures may change

7.8 Revision in relation to non-resident taxpayers

In 2021, inconsistencies in the regional classification of a small number of SA taxpayers were discovered in HMRC’s NPS and SA systems.

These taxpayers had Welsh/Scottish residency flags in HMRC’s NPS records and were thus identified as Welsh/Scottish taxpayers for the purpose of the Outturn.

However, the flag indicator variable in HMRC’s SA database for these taxpayers showed as rUK. An examination of tax returns for a sample of these individuals was conducted and it was discovered that these taxpayers were non-resident for tax purposes.

It is not possible to be a WRIT or SIT taxpayer while being non-resident so the NSND Income Tax revenue generated from these non-resident taxpayers should have been allocated to rUK.

The process of producing the outturn figures has been revised for the 2020 to 2021 outturn. The figures from previous outturn years have also been revised accordingly in this statistical release.

Overall, this leads to an average yearly reduction of SIT outturn of £8.9 million (-0.08%) over the period 2016 to 2017 to 2019 to 2020, for WRIT this represents a one-time reduction of £1.5 million (-0.07%) in 2019-20.

Through further analysis, we have accounted for these adjustments in the Income Tax paid through Self Assessment and PAYE (Table 3) and the by band breakdown of NSND Income Tax (Table 2).