Cyber security sectoral analysis 2026

Published 12 May 2026

© Crown copyright 2026

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/cyber-security-sectoral-analysis-2026/cyber-security-sectoral-analysis-2026

Foreword

The UK’s cyber security sector continues to demonstrate why this country is one of the best places in the world to start and grow a cyber business. This year’s analysis shows a sector that is expanding in scale and capability, generating £14.7 billion in revenue, contributing £9.1 billion in Gross Value Added, and employing nearly 70,000 highly skilled people across more than 2,600 firms. These businesses protect our digital economy while creating high value jobs in every part of the UK.

At the heart of this success is talent. UK cyber businesses consistently highlight the strength of our engineering and security expertise as a key competitive advantage. Through programmes such as TechFirst, the government is helping to sustain the pipeline of specialist skills needed across cyber security and the UK’s wider frontier technologies. Alongside this, reforms to technical education and apprenticeships, and our continued focus on increasing the participation of women in tech, are helping to ensure that more people can access and benefit from the opportunities the cyber sector creates.

The UK is also a leading environment for cyber innovation. Our universities continue to generate new ideas, companies and intellectual property. Targeted accelerator programmes, including CyberASAP, are supporting researchers and founders to turn cutting edge research into commercially viable businesses, attracting private investment and strengthening the UK’s innovation pipeline.

Cyber security is a clear government priority. The Government Cyber Action Plan set out how we will strengthen resilience against cyber threats, and the Cyber Security and Resilience Bill will raise standards across critical national infrastructure and digital supply chains. As this report shows, public sector spending on cyber security continues to increase. Harnessing this demand to support UK capability, and to build stronger design partnerships between government, industry and investors, will be essential if more UK cyber firms are to scale into global leaders.

Artificial intelligence is reshaping the cyber security landscape. This report highlights the rapid growth of firms securing AI systems and using AI to identify vulnerabilities more effectively. The UK’s combined strengths in cyber security, AI and research position us well to lead in this next phase, securing our digital future while building globally competitive businesses at home.

Baroness Lloyd of Effra CBE

Parliamentary Under-Secretary of State (Minister for Digital Economy)

Department for Science, Innovation and Technology

Executive summary

Introduction

Ipsos and Perspective Economics were commissioned by the Department for Science, Innovation and Technology (DSIT) in May 2025 to undertake an updated analysis of the UK’s cyber security sector.

This analysis builds upon the previous UK Cyber Security Sectoral Analysis (published in March 2025) that provides a recent estimate of the size and scale of the UK’s cyber security industry. The research provides an assessment of:

-

the number of businesses in the UK supplying cyber security products or services

-

the sector’s contribution to the UK economy (measured through revenue and Gross Value Added, or GVA)

-

the number employed in the cyber security sector

-

the products and services offered by these firms

Project scope and summary of methodology

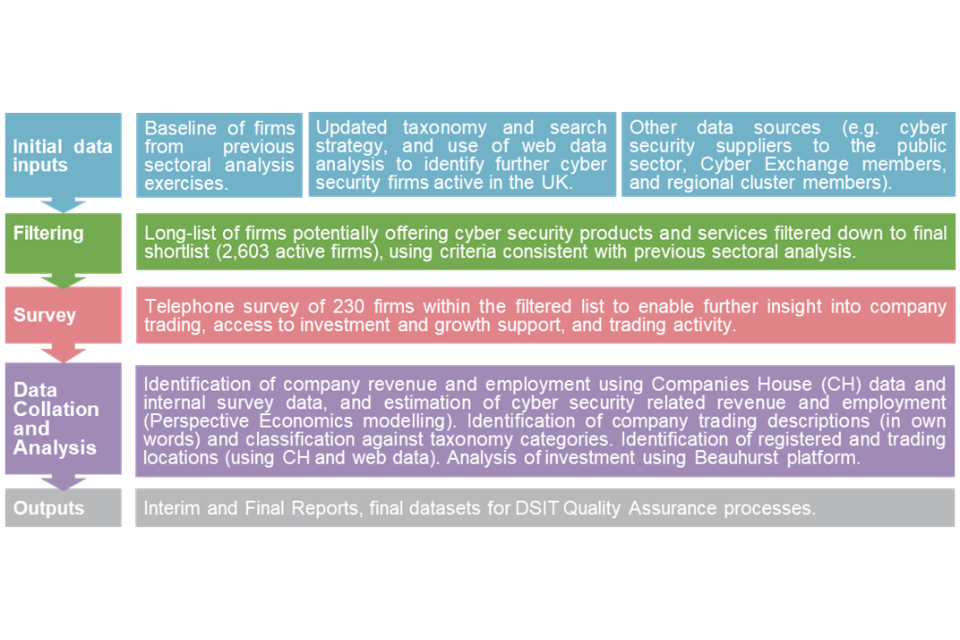

The diagram below sets out a summary of the research methodology used. This is consistent with previous studies to support a time-series analysis of the sector’s performance to date.

Source: Ipsos, Perspective Economics

Key findings

| Metric | Finding |

|---|---|

| Number of companies | We estimate that there are 2,603 firms currently active within the UK providing cyber security products and services. This is an increase of 438 firms (+20%) compared to the previous report, which identified 2,165 firms. |

| Sectoral Employment | We estimate there are approximately 69,600 Full Time Equivalents (FTEs) working in a cyber security related role across the cyber security firms identified. This reflects an estimated increase of c. 2,300 cyber security employee jobs within the last 12 months (an increase of 3%). |

| Sectoral Revenue | We estimate that total annual revenue within the sector has reached £14.7 billion within the most recent financial year. This reflects a nominal increase of c. 11% since last year’s study. |

| Gross Value Added | We estimate that total GVA for the sector has reached c. £9.1 billion — an increase of 17% since last year’s study. We estimate that GVA per employee has also increased from £116,200 to £131,200 (+13%). |

| Investment | In 2025, £184 million has been raised across 47 deals within dedicated cyber security firms. |

1. Introduction

1.1 Methodology and sources

This analysis builds upon the previous UK Cyber Security Sectoral Analysis 2025 (published in March 2025) that provides a recent estimate of the size and scale of the UK’s cyber security industry. This continues the time-series analysis undertaken by the research team since 2018. A full time-series analysis is set out within Chapter 4.

The research provides an assessment of the number of businesses in the UK supplying cyber security products or services; the sector’s contribution to the UK economy (measured through revenue and Gross Value Added, or GVA [footnote 1] ); the number employed in the cyber security sector; and an overview of the products and services offered by these firms.

The UK cyber security sector does not have a formal Standard Industrial Classification (SIC) code, and this study therefore closely aligns itself to that of the baseline analysis, to provide a time series analysis of how the sector has progressed since the baseline and subsequent annual studies.

The cyber security sector remains fast-moving, and continually subject to changes in products, services, and market approaches. This year’s study is fully consistent with the previous updated methodology set out within last year’s report. This includes a refined taxonomy to better identify and classify cyber security activity, continued use of a range of data sources[footnote 2], and an ongoing telephone and online survey of cyber security businesses in July to October 2025.

The following methodology and research sources were used to provide an overarching shortlist of UK cyber security businesses, and to estimate their economic contribution related to the sale of cyber security products or services.

The process by which we identify and measure the economic contribution of cyber security activity reflects a best estimate by the research team using agreed parameters for the inclusion of respective firms considered to be active in the field.

The key stages below are consistent with previous Cyber Security Sectoral Analysis exercises to enable a time series comparison.

Stage 1: Desk research

The research team conducted initial desk research to explore how the cyber security market had changed within the last 12 months. This included:

-

Engagement with UK cyber security regional networks and clusters, to gather local intelligence

-

A review of published reports regarding the output or activities of the sector (e.g., National Cyber Strategy, NCSC Annual Review, and wider landscape literature)

-

Recent investments or initiatives in the cyber security sector (including review of investments and acquisitions, and identification of industry initiatives and cohorts, e.g., Cyber Runway)

-

Any emerging trends in the market (including supply side and demand side), e.g., enhanced demand attributable to cloud security, or new product innovations requiring specific cyber security requirements (e.g., AI Security) — this is explored in Section 7

Stage 2: Initial data collection & gap analysis

The research team sought to identify potential active cyber security firms in the UK through:

-

A review of firms previously identified in the sectoral analysis (identifying current status and determining inclusion in the updated set)

-

A review of company participation within clusters, networks, and/or government supported initiatives

-

A cyber security market taxonomy has been used to inform a long list of firms (identified through use of web data and refined within DSIT workshops). This list was subject to automated and manual review, and refined to a final cyber security business list for analysis (n = 2,603)

The business metrics include (but are not limited to):

-

Company name, registered number, company status, and date of incorporation

-

Registered and trading locations (using official and web data)

-

Company website and contact details

-

Core description of company activities related to cyber security

-

Company size (Large / Medium / Small / Micro)

Stage 3: Cyber security sectoral survey

Ipsos conducted a representative survey of 230 cyber security firms from July to October 2025. The survey used the list of firms (n = 2,603) established in Stage 2 of this study as a sample frame from across the UK. The purpose of the survey was to understand firm-level performance, barriers, and collaboration in further detail.

It covered the following topics:

-

The categories of products and services offered across firms

-

The client sectors that cyber security firms work across

-

Revenue estimates (to supplement the other published data found in Stage 2)

-

Understanding areas of collaboration and reasons for working with cyber security partners

Stage 4: Qualitative consultations

This research has also been supported through 5 one-to-one consultations with investors in the cyber security sector. Participants were purposively sampled to reflect variation in size, location, product or service focus, maturity, and investment focus.

Stage 5: Data blending

In December 2025, the results of the cyber security sector survey were used to inform gaps within the list of identified cyber security sector firms e.g., the extent to which a firm provided cyber security products or services and attributed revenues accordingly. This stage involved data cleaning and augmentation from a range of previous sources (including company level accounts, web data, survey data, and wider desk review) to provide a final dataset of cyber security firms, including the development of firm-level metrics used for analysis within the report. Additional verification of web domains (to ensure active status) and Companies House was also undertaken to confirm active status at the time of analysis.

Stage 6: Data analysis and reporting

The final stage involved analysis of the final shortlist of firms to provide estimates of the total number of firms, products and services offered, whether firms are ‘dedicated or diversified’ with respect to how much of their activity related to cyber security provision, revenue/GVA/employment estimates, locations (registered, trading, and international presence), investment and survey feedback (anonymised at an individual level). Further analysis is also undertaken to explore AI security and software security providers operating in the UK market (as set out in Chapter 7).

The data sources used to underpin the sectoral analysis included:

-

Web Data: Perspective Economics undertook extensive web review to identify new providers of cyber security products and services, with enriched company descriptions, activities and locations for identified company websites.

-

Bureau van Dijk FAME (and Companies House Data Product): This platform collates Companies House data and financial statements from all registered businesses within the UK.

-

Beauhurst: Beauhurst is a leading investment analysis platform, which enables users to discover, track and understand some of the UK’s high-growth companies e.g., identify investment, accelerator participation, and key information.

-

Tussell: Tussell provides market insight into public sector procurement through identifying key contracts, spend, buyers and suppliers.

-

Cyber Exchange: techUK’s Cyber Exchange directory enables cyber security providers to register an account and set out the products and services they provide to the market.

-

Representative survey of cyber security firms: in late 2025, Ipsos conducted a representative survey of cyber security firms. The feedback from 230 providers has been useful to understand the growth drivers and challenges for firms within the market.

-

One-to-one qualitative consultations: further, the team has also conducted 5 one-to-one consultations with investors to gather feedback on the growth and performance of the cyber security sector in the UK.

1.2 Consistency with the 2025 cyber security sectoral analysis

Our approach remains consistent with previous reports (and builds upon the methodology to identify and measure the contribution of the sector). As per previous studies, this report also explores firms that:

-

Have a clear presence within the UK market, through a UK registered business that reports to Companies House on an annual basis

-

Demonstrate an active provision of commercial activity related to cyber security (e.g., through the presence of a website / social media)

-

Provide cyber security products or services to the market (i.e., sell or enable the selling of cyber solutions to other customers)

-

Have identifiable revenue or employment within the UK

-

Appear to be active at the time of writing (i.e., have not, or are not in the process of dissolution)

-

Are not charities, universities, networks, or individual contractors (non-registered) — all excluded for analysis purposes

It also draws upon consistent sources, i.e., company accounts, longitudinal survey data, and Beauhurst for investment data. The financial analysis of firms is also consistent, as it uses company information from the most recent financial year of accounts (analysis undertaken in late 2025, with financial year 2024/25 as the modal year for published accounts) and the underpinning dataset sets out where employment, revenue, GVA and investment are either known or estimated (and the rationale underpinning this).

We note that a series of methodological updates have been undertaken including an update to UK company size thresholds (as set out previously), increased use and scoping of web data by the Perspective Economics research team, updated classification and categorisation (as set out in Section 2), and further research to identify AI and Software Security providers, following the 2025 research.

1.3 Interpretation of the data

Across this report, percentages from the quantitative data may not add to 100%. This is because:

-

We have rounded percentage results to the nearest whole number

-

At certain questions, survey respondents could give multiple answers

It is also important to note that the survey data is based on a sample of cyber sector firms rather than the entire population. Therefore, they are subject to sampling tolerances. The overall margin of error for the sample of 230 firms (within a population of 2,603 firms) is between c.4 and c.6 percentage points. The lower end of this range (4 percentage points) is used for survey estimates closer to 10% or 90%. The higher end (6 percentage points) is used for survey estimates around 50%. For example, for a survey result of 50%, the true value, if we had surveyed the whole population, is highly likely to be in the range of 44% to 56%.[footnote 3]

By contrast, the data from the qualitative consultations is intended to be illustrative of the key themes affecting the cyber security sector as a whole, rather than a statistically representative view of cyber sector investors.

1.4 Acknowledgements

The authors would like to thank the DSIT team for their support across the study. DSIT and the report authors would also like to thank those that participated within this research, including those that participated within the industry survey, the regional cyber security clusters, consultations, and shared data, knowledge, and feedback to help underpin this study.

Note: The cyber security sector continues to increase in size, scope, and specialisms. We are happy to receive comments and feedback regarding the methodology or findings herein, through contacting cybersecurity@dsit.gov.uk

2. Profile of the UK cyber security sector

Section summary: profile of the UK cyber security sector

-

We estimate that there are 2,603 firms currently active within the UK providing cyber security products and services. This reflects an increase of 438 firms (+20%) compared to the previous report, driven by newly registered companies, firms diversifying into cyber security, and improved identification through expanded web data and source coverage.

-

The majority of firms are small (19%) or micro (58%) in size. However, the sector contains a notably higher proportion of medium and large firms (22%) than the wider UK business population (c. 3%), indicating significant provider scale within the market.

-

Just over two-thirds (69%) of firms are dedicated (‘pure-play’) providers of cyber security. Micro firms are much more likely to be dedicated (84%), whereas large firms are predominantly diversified (83%), reflecting the tendency for major consultancies, managed service providers, and telecoms firms to establish cyber security practices alongside existing provision.

-

Analysis of company descriptions suggests that over 7 in 10 (72%) of firms are mainly involved in service provision (including managed services), and just under 1 in 3 (29%) are mainly involved in cyber security product development. This reflects a slight increase in product-led activity compared to the previous study.

2.1 Defining the UK cyber security sector

Within the National Cyber Strategy 2022, cyber security is defined as:

The protection of internet connected systems (to include hardware, software, and associated infrastructure), the data on them, and the services they provide, from unauthorised access, harm, or misuse. This includes harm caused intentionally by the operator of the system, or accidentally, as a result of failing to follow security procedures or being manipulated into doing so.

Therefore, this sectoral analysis seeks to identify businesses active within the UK that provide products or services that enable the protection of internet connected systems and their users.

In line with previous studies, this analysis is focused upon organisations that include all of the following attributes:

-

Have a clear presence within the UK market, through a UK registered business that reports to Companies House on an annual basis

-

Demonstrate an active provision of commercial activity (e.g., through the presence of an active website / social media presence)

-

Provide cyber security products or services to the market (i.e., sell or enable the selling of cyber solutions to other customers) — aligned to the taxonomy set out below

-

Have identifiable revenue or employment within the UK related to cyber security

-

Appear to be active at the time of writing (i.e., have not, or are not in the process of dissolution)

-

Are not charities, universities, networks, and individual contractors (non-registered) — which are all excluded for analysis purposes

The businesses included within this analysis are considered to provide one or more of the following products or services:

-

Cyber professional services, i.e., providing trusted contractors or consultants to advise on, or implement, products, solutions, or services for others.

-

Endpoint and mobile security, i.e., hardware or software that protects devices when accessing networks.

-

Identification, authentication, and access controls, i.e., products or services that control user access, for example with passwords, biometrics, or multi-factor authentication.

-

Incident response and management, i.e., helping other organisations react, respond, or recover from cyber attacks.

-

Information risk assessment and management, i.e., products or services that support other organisations to manage cyber risks, for example around security compliance or data leakage.

-

Internet of Things (IoT Security), i.e., products or services to embed or retrofit security for Internet of Things devices or networks.

-

Network security, i.e., hardware or software designed to protect the usability and integrity of a network.

-

SCADA and Information Control Systems, i.e., cyber security specifically for industrial control systems, critical national infrastructure, and operational technologies.

-

Threat intelligence, monitoring, detection, and analysis, i.e., monitoring or detection of varying forms of threats to networks and systems.

-

Awareness, training, and education, i.e., products or services in relation to cyber awareness, training, or education.

Section 2.3 sets out the type of cyber security products and services in further detail.

2.2 Number of cyber security firms active in the UK

We estimate that there are currently 2,603 firms active within the UK providing cyber security products and services. This reflects an estimate as of December 2025. Whilst this reflects an increase in the number of firms offering cyber security products and services (2,165 identified in the previous study), the research team emphasise that this is one metric among many to gauge the health of the sector. For example, this increase includes:

-

Newly registered companies offering cyber security products and services (often very early / small start-ups)

-

Previously registered companies that did not previously offer such services, but have established a product or team to do so recently (e.g., consultancies offering IT risk services)

-

Businesses now identified as providing a relevant cyber security product or service (e.g., identified through provision of an accredited scheme such as Cyber Essentials) where previous web-data matching did not flag such products or services

-

Businesses with limited web data reporting the provision of cyber security products or services, but which have been flagged through engagement with other sources (e.g., consultation with regional clusters)

Throughout this study, the research team emphasise the need to draw upon a wide range of existing sources, alongside the development and deployment of a cyber security taxonomy against Companies House data, analysis of relevant website domains, and in-depth regional engagement. Within the process, a ‘long list’ of several thousand businesses in the UK was identified as potentially relevant to the cyber security sector using keywords and web data. However, this long list was subsequently filtered to ensure each business demonstrated sufficient alignment to the research parameters and the market taxonomy. For example, web data can identify firms that may have an active registration with Companies House, have a website or social media presence, and meets the parameters of the taxonomy. However, further review of the presence may indicate a lagging status (e.g., the business may have no true employees or may not appear to be active for several years). The team therefore reviewed thousands of potentially relevant firms in detail and subsequently omitted organisations that may have mentioned security (e.g., offering a secure data centre service) but did not appear to tangibly offer security products or services to the end-market.

This yielded the 2,603 firms in scope, and the research team considers this to be an appropriate figure to gauge the health and composition of the sector whilst ensuring consistency with previous analysis.

We do however note, that as with all emerging sectors, subtle differences in definition can result in varying interpretations of the scope and composition of activity. In this respect, there may be other relevant cyber security use cases, which could in future meet the short list requirements (i.e., the 6 conditions set at the beginning of Section 2.1) and could therefore be included in future analysis. This might include, for example, firms involved in areas such as RegTech[footnote 4] or Safety Tech[footnote 5]. However, we provide these parameters to avoid duplication and provide DSIT with a health check regarding the overall cyber security market.

Further, we have improved our identification methodology. This analysis draws on an expanded range of data sources, including company accounts, web data, and wider secondary datasets, to inform our assessment of whether a firm can be considered in scope. We have also included signals such as Cyber Essentials certification and participation in accelerator programmes (e.g. Cyber Runway) to support identification of relevant firms. All web data is reviewed by the Perspective Economics research team to minimise omissions where automated scraping may not fully capture firm-level activity.

Overall, this process means that the 2,603 firms identified for analysis within this report have been assessed and verified as providers of cyber security products and solutions. We provide a high-level breakdown of this provision in subsequent chapters. Given the breadth of ‘cyber security’ as a term, we endeavour to be clear regarding what is in scope, what is being measured, and why this matters, for the sector and for the wider economy and society.

The following sub-sections set out an overview of the number of companies by size; the breakdown between companies that appear dedicated or diversified; and the products or services provided by each company. For the 2,603 cyber security firms, Figure 2.1 and Table 2.1 demonstrate breakdown by size. [footnote 6]

Figure 2.1: Number of registered cyber security firms by size

| Large | 240 |

| Medium | 343 |

| Small | 507 |

| Micro | 1,513 |

Source: Perspective Economics (n = 2,603)

Within the UK, the vast majority of all businesses are Small and Medium Enterprises (SMEs), and it is therefore to be expected that the majority of registered businesses within the cyber security sector are small (19%) or micro (58%) in size.

As this study focuses upon businesses with at least one member of staff, the following comparison is noted between the UK’s cyber security sector, and the broader UK business population. This highlights that, despite the cyber security sector containing a considerable proportion of micro and small businesses, there are many providers of scale operating within the UK market (i.e., 22% of businesses offering cyber security products and services to market are medium or large, compared to c. 3% of all businesses[footnote 7] in the UK).

Table 2.1: Comparison of the size of cyber security firms and wider business population

| Size | UK Business Population Estimates (2025) | Percentage[footnote 8] | Cyber Sectoral Analysis | Percentage |

|---|---|---|---|---|

| Large (250+) | 8,335 | <1% | 240 | 9% |

| Medium (50-249) | 38,435 | 3% | 343 | 13% |

| Small (10-49) | 220,085 | 16% | 507 | 19% |

| Micro (1-9) | 1,150,875 | 81% | 1,513 | 58% |

| All Businesses with at least 1 employee | 1,417,730 | 100% | 2,603 | 100% |

Change in Size

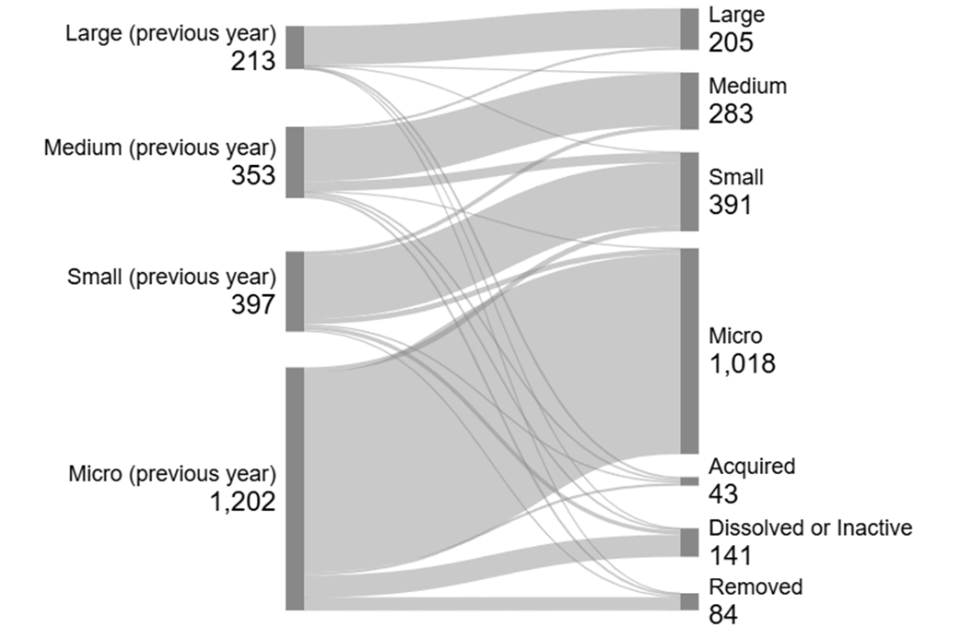

Following last year’s sectoral analysis, we have tracked the performance of each firm identified last year (n = 2,165 in the previous study) to understand how the size of cyber security firms has changed (where applicable) in the last 12 months.

The left side of the Sankey diagram (Figure 2.2) shows the size of cyber security firms as identified in the 2025 study, with the right side showing their updated size currently. The data highlights ongoing levels of dissolution or inactivity among micro and small providers. However, we note this study methodology has undertaken additional firm level checks to remove or mark firms as ‘inactive’ that no longer appear to be substantially trading, even if they are marked as ‘active’ with Companies House. For example, this includes the removal of ‘dead’ domain websites, and additional website quality reviews to remove firms without clear active market relevance or cyber security provision. As such, this improves the underlying dataset quality; however, results in the removal of ‘lower quality’ domains and entities (as marked by ‘removed’ in Figure 2.2).

Figure 2.2: Sankey flow chart — size (2025 study – 2026 study)[footnote 9]

Source: Perspective Economics (n=2,165)

Dedicated and diversified providers of cyber security products and services

Within this research, we attempt to categorise firms by whether they are either:

-

Dedicated (or ‘pure-play’), i.e., all or most of the business’ revenue or employment can be attributed to the provision of cyber security products or services.

-

Diversified, i.e., some, but not all of the business’ revenue or employment can be attributed to the provision of cyber security products or services.

These classifications are determined by the research team based on review of revenue, employment, and review of all products and services offered by the firm.

Figure 2.3: Dedicated and diversified providers

| Dedicated | 69% |

| Diversified | 31% |

Source: Perspective Economics (n = 2,603)

The rationale underpinning the need to provide this distinction between dedicated and diversified firms is because it is important to understand how firms solely providing cyber security, and firms providing cyber security as one product or service among others, vary with respect to size, scale, growth, and market activity.

Within the current dataset, just over two-thirds (69%) of firms are dedicated providers of cyber security products and services. This reflects a limited change from the previous study (68%). Disaggregating these firms by size also highlights that micro and small cyber security firms within this analysis are much more likely to be dedicated (84% and 64% respectively), whereas there are few large dedicated cyber security firms (17%).

In other words, this reflects the tendency for several large and medium sized companies in the UK to establish cyber security practices to complement existing provision, e.g., management consultancies, managed service providers, or telecoms firms developing a cyber security division that sells to the market. This also includes a range of larger diversified firms developing cyber security products or solutions tailored towards markets such as aerospace and defence, critical national infrastructure, and professional services.

Figure 2.4: Dedicated / diversified cyber security firms by size

| Size | Dedicated | Diversified |

|---|---|---|

| Large | 17% | 83% |

| Medium | 51% | 49% |

| Small | 64% | 36% |

| Micro | 84% | 16% |

Source: Perspective Economics (n=2,603)

2.3 Products and Services Provided

To understand the products and services provided by the UK cyber security sector, DSIT and the research team use a taxonomy (as summarised below) to categorise them.

This provides a high-level overview of the UK’s cyber security product and service offer. This taxonomy remains broadly consistent with previous years; however, the underlying keywords and terms have been revisited and updated. Further, the use of web data and manual review means firms can be classified into taxonomy areas through both the text available, and the analyst decision regarding key products and services. This means the following data reflects an interpretation of the key products and services offered. It is therefore indicative of the main solutions provided by the UK cyber security sector.

We take a top-down review of products and services using the text data available through web data review. This study draws on additional text data compared to previous studies; typically reviewing dozens of relevant web pages to ascertain products and services provided. Further, this year’s study has also reviewed products and services in the firm’s own words. The research team has considered almost 37,000 unique products or services mentioned by the cyber security providers identified.

Taxonomy definitions:

| Taxonomy Category | Agreed Definition |

|---|---|

| Cyber professional services | Providing trusted contractors or consultants to advise on, or implement, cyber security products, solutions, or services for others |

| Endpoint and mobile security | Hardware or software that protects devices when accessing networks |

| Identification, authentication, and access controls | Products or services that control user access, for example with passwords, biometrics, or multi-factor authentication |

| Incident response and management | Helping other organisations react, respond, or recover from cyber attacks |

| Information risk assessment and management | Products or services that support other organisations to manage cyber risks, for example around security compliance or data leakage |

| Internet of Things | Products or services to embed or retrofit security for Internet of Things devices or networks |

| Network security | Hardware or software designed to protect the usability and integrity of a network |

| SCADA and Information Control Systems | Cyber security specifically for industrial control systems, critical national infrastructure, and operational technologies |

| Threat intelligence, monitoring, detection, and analysis | Monitoring or detection of varying forms of threats to networks and systems |

| Awareness, training, and education[footnote 10] | Products or services in relation to cyber awareness, training, or education |

Source: Perspective Economics

Additionally, we also classify each company by whether they provide (as their main cyber security offering) products, services, and or managed security services:

-

Cyber security product(s): i.e., the business has developed and sells a bespoke product (hardware or software solution) to the market

-

Cyber security service(s): i.e., the business sells a service to the market e.g., cyber security advisory services, penetration testing etc

-

Managed Security Service Provider(s): i.e., the business offers other organisations some degree of cyber security support e.g., establishes security protocols, monitoring, management, threat detection etc — typically for a monthly or annual fee

This approach helps policymakers, industry, and investors understand how many companies there are focusing on a particular subsector of the market or offering new products or solutions accordingly.

Product and service provision

Figure 2.5 sets out an analysis of how many companies appear to be focused upon product or service provision. It is worth noting that there will be some overlap where firms provide both products and services; however, this approach selects one primary category per firm. Overall, analysis of company trading descriptions suggests that over 7 in 10 (72%) of firms are mainly involved in service provision (including managed services and reselling), and just under 1 in 3 (29%) are mainly involved in cyber security product development. This reflects a slight increase in product-led activity (from 26% in the previous study to 29% in this year’s study).

Figure 2.5: Number of registered cyber security firms by product/service focus

| Service | 1,216 |

| Product | 743 |

| MSSP | 644 |

Source: Perspective Economics (n = 2,603)

Taxonomy breakdown

Within this study, we have matched company descriptions (in their own words through website analysis) with the key terms within each taxonomy category, followed by a manual and automated check to assign companies to one (or more) taxonomy categories with respect to their product and service provision.

Figure 2.6 is based upon our analysis of trading descriptions, mapped against the taxonomy for all cyber security firms identified. This uses a ‘multiple-fit’ criteria (e.g. a firm may provide several products or services aligned to multiple taxonomy areas).

Figure 2.6: Number of registered cyber security firms by taxonomy offering

| Information Risk Assessment and Management | 80% |

| Cyber Professional Services | 80% |

| Network Security (including perimeter and application) | 52% |

| Threat Intelligence, Monitoring, Detection and Analysis | 45% |

| Training, Awareness and Education | 43% |

| Incident Response and Management | 38% |

| Identification, Authentication and Access Control | 29% |

| Endpoint Security (including Mobile Security) | 25% |

| IoT (including devices, automotive and connected home) | 10% |

| SCADA and ICS | 7% |

Source: Perspective Economics (n = 2,603)

Figure 2.7 sets out a range of the top product and service areas in cyber security mentioned by providers based on a review of web data. The research team has classified these into key groupings.

We note that this is based upon text classification of almost 37,000 unique products and services identified within company web data. This is reliant upon sufficient web coverage and a rapid classification of products and services into relevant categories identified by the research team. This should therefore be considered as indicative of the most commonly mentioned products and service areas, rather than an exhaustive coverage. Further, this is based upon estimated count of terms mentioned across providers, rather than a full assessment of all values as set out in Figure 2.6. As such, there may be some minor variance between taxonomy estimates, and product and service estimates. However, this chart is included to provide a more granular assessment of key solutions cited by vendors.

Figure 2.7: Products and services identified within the cyber security sector

| Security Consulting & Advisory | 63% |

| Governance Risk & Compliance | 62% |

| Security Operations & Monitoring | 46% |

| Incident Response & Recovery | 46% |

| Security Awareness & Training | 40% |

| Vulnerability Management | 38% |

| Data Security & Privacy | 36% |

| Penetration Testing & Red Teaming | 35% |

| Threat Intelligence | 32% |

| Identity & Access Management | 30% |

| Security Certifications | 29% |

| Network Security | 29% |

| Cloud Security | 26% |

| Endpoint & Device Security | 25% |

| Application Security | 21% |

| Email & Communication Security | 16% |

| AI Security, Assurance and Governance | 13% |

| Physical & Hardware Security | 11% |

| Backup & Data Protection | 11% |

| Industrial & OT Security | 10% |

| Secure Development | 7% |

| Fraud & Financial Security | 7% |

| IoT Security | 6% |

Source: Perspective Economics review of web data (n = 2,494 providers with product and services identified)

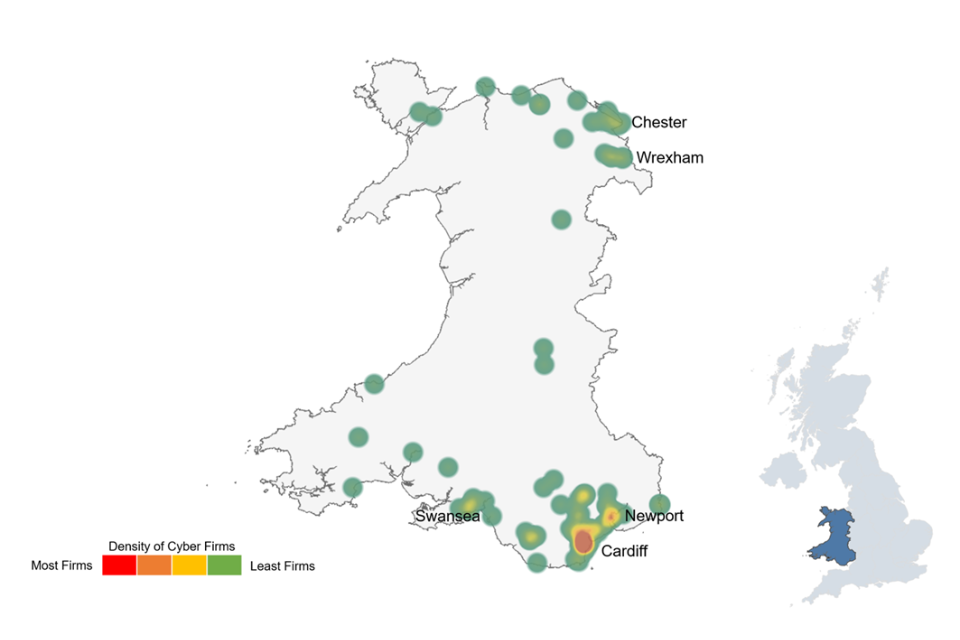

3. Location of cyber security firms

Section summary: location of cyber security firms

-

We have identified 5,374 active office locations for the 2,603 firms in this study. London (33%) and the South East (16%) are the 2 largest regions; however, just over half (51%) of UK office locations are based outside these 2 regions.

-

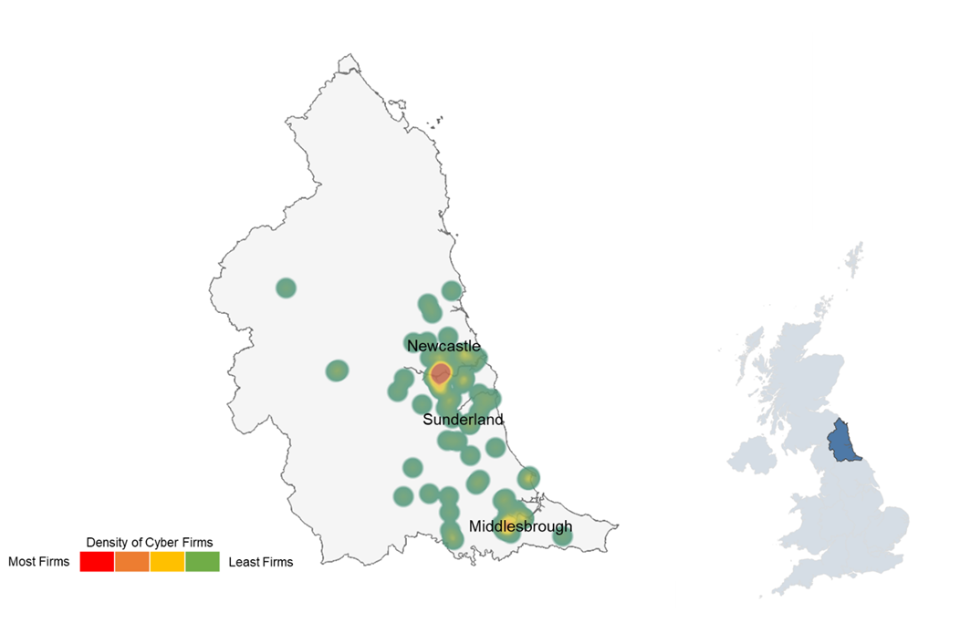

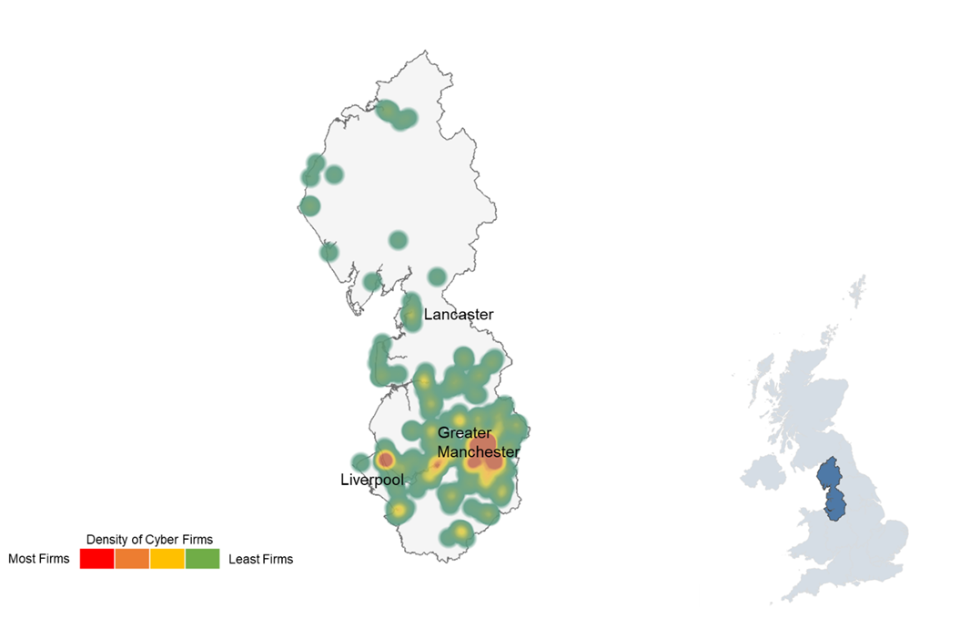

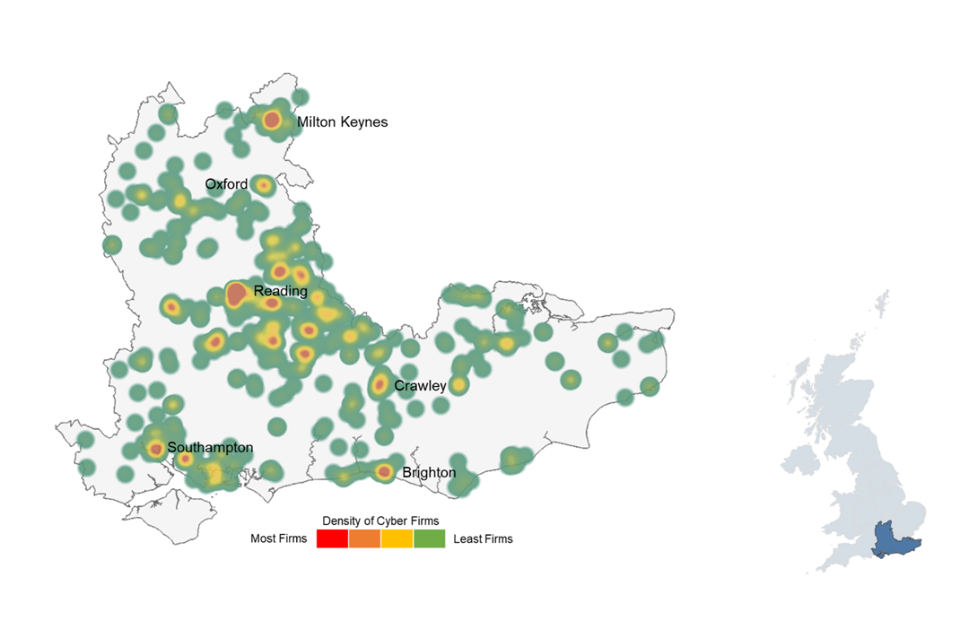

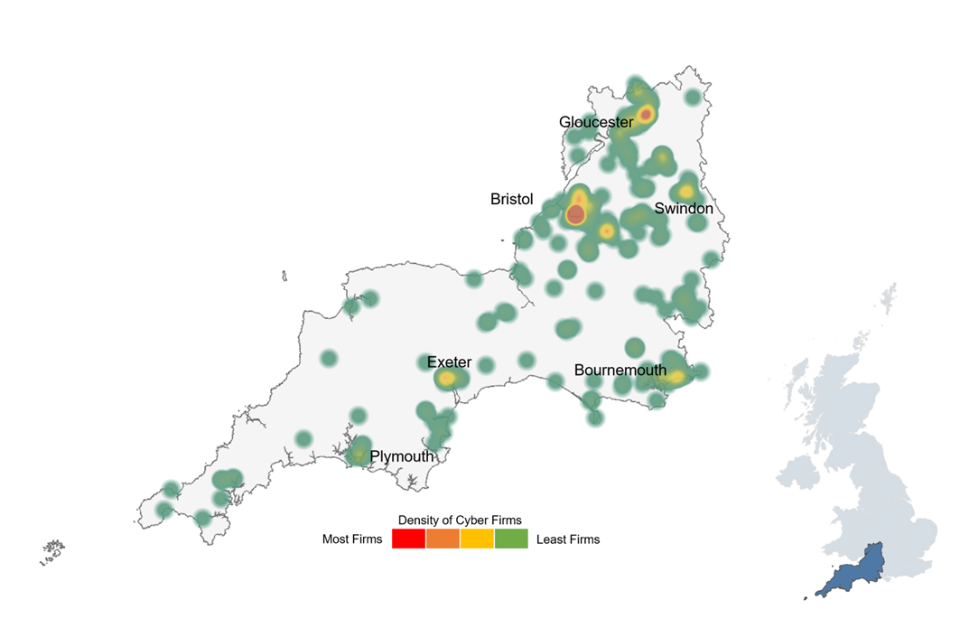

The data highlights sustained hotspots in areas such as Greater Manchester, Bristol and Bath, Cheltenham, Belfast, Glasgow, Edinburgh, Newcastle, and the Oxford–Cambridge Growth Corridor. No substantial proportional changes at the regional level were observed compared to the previous report.

-

For dedicated providers, we have identified 414 UK-headquartered businesses with a physical presence in international markets. The United States and European Union / European Economic Area are the core markets for international trading (each 62%), with key European markets including Germany, Netherlands, Spain, France, and Ireland.

-

A further 530 cyber security businesses active in the UK appear to be headquartered or originate from outside the UK, with key nations (by count) continuing to include the US, India, Canada, Israel, France, Germany, Australia and Ireland.

3.1 Introduction

This chapter explores the registered location (i.e., where each business has located its registered address with Companies House), and the active office locations (i.e., where each business has a trading presence or office across the UK) of cyber security firms.

Understanding the registered and trading addresses of cyber security firms in the UK enables regional analysis and supports the evidence-based identification of notable clusters or hotspots of activity. We have identified 5,374 active office locations for the 2,603 firms identified within this study.

These have been identified using identification of 2,603 registered locations (via Companies House) and a further 2,771 UK office locations with web data (for example, where a cyber security firm has multiple sites across the UK).

3.2 Location of cyber security firms in the UK

Figure 3.1 sets out the breakdown of firms by number of UK office locations identified in each of the 12 regions. This highlights the importance of identifying local units of activity in the UK (marked in blue below) when seeking to understand regional activity, as registered locations can be skewed towards London and the South East.

Overall, the data suggests that just over half (51%) of UK office locations are based outside of London and the South East regions. Further exploration of regional office data suggests no substantial proportional changes at the regional level (proportional to overall size of the UK market) compared to the previous report.

Figure 3.1: Percentage of cyber security firms by location

| London | 33% |

| South East | 16% |

| North West | 9% |

| South West | 8% |

| Scotland | 7% |

| East of England | 7% |

| West Midlands | 6% |

| Yorkshire and The Humber | 5% |

| East Midlands | 3% |

| Wales | 2% |

| Northern Ireland | 2% |

| North East | 2% |

Source: Perspective Economics (n=5,374)

Active (local offices)

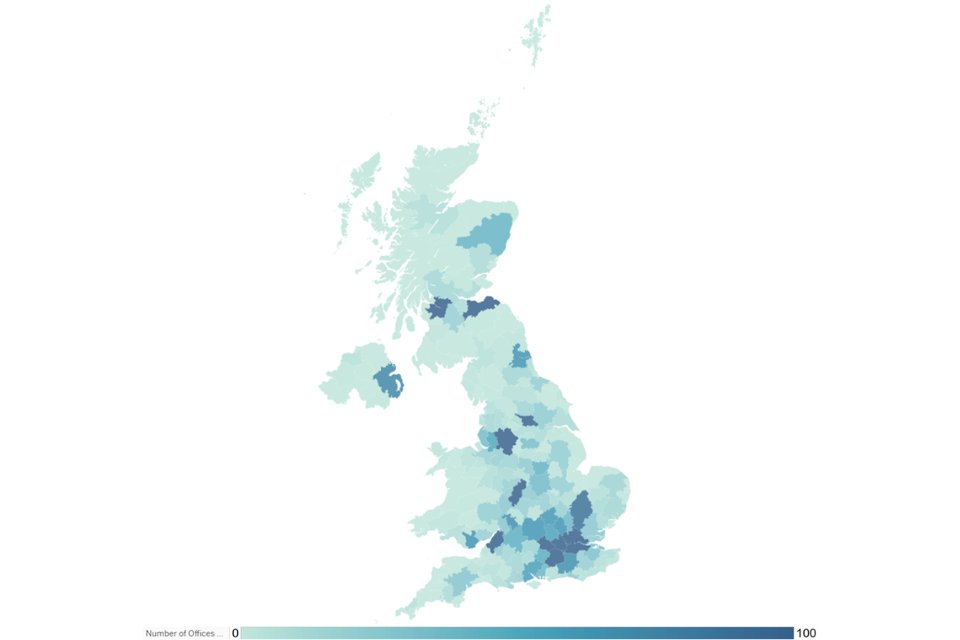

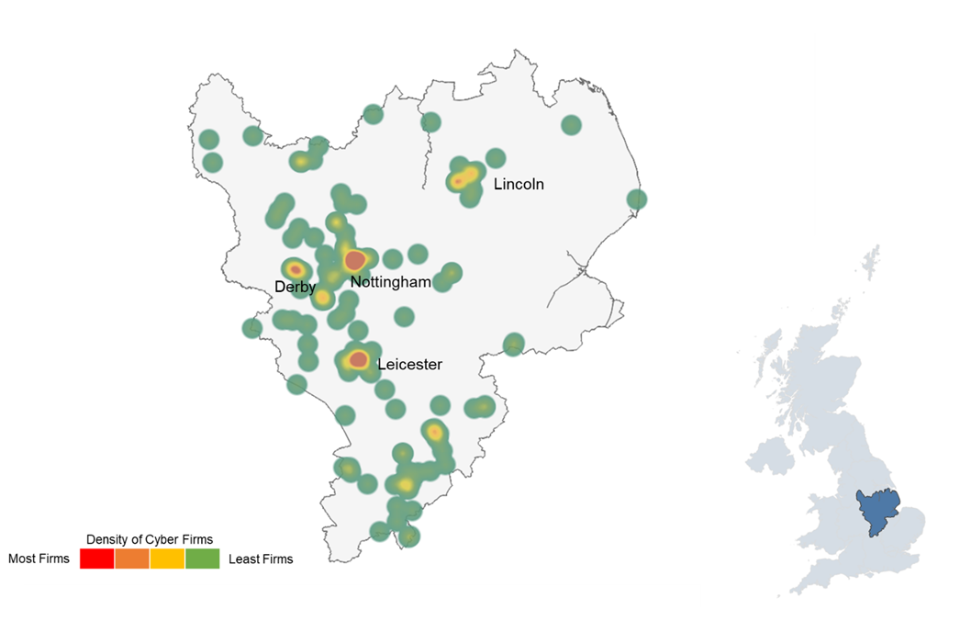

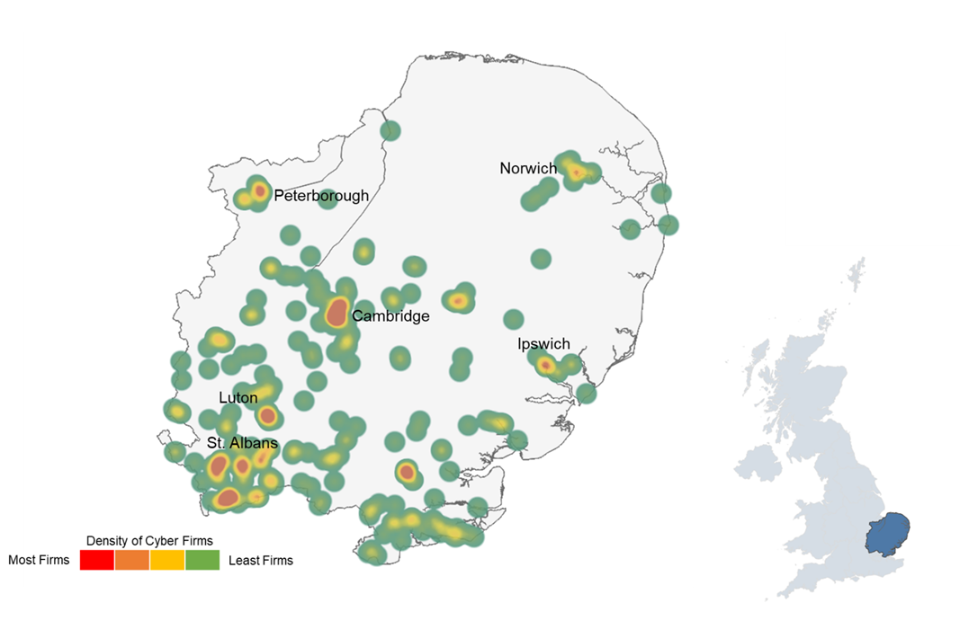

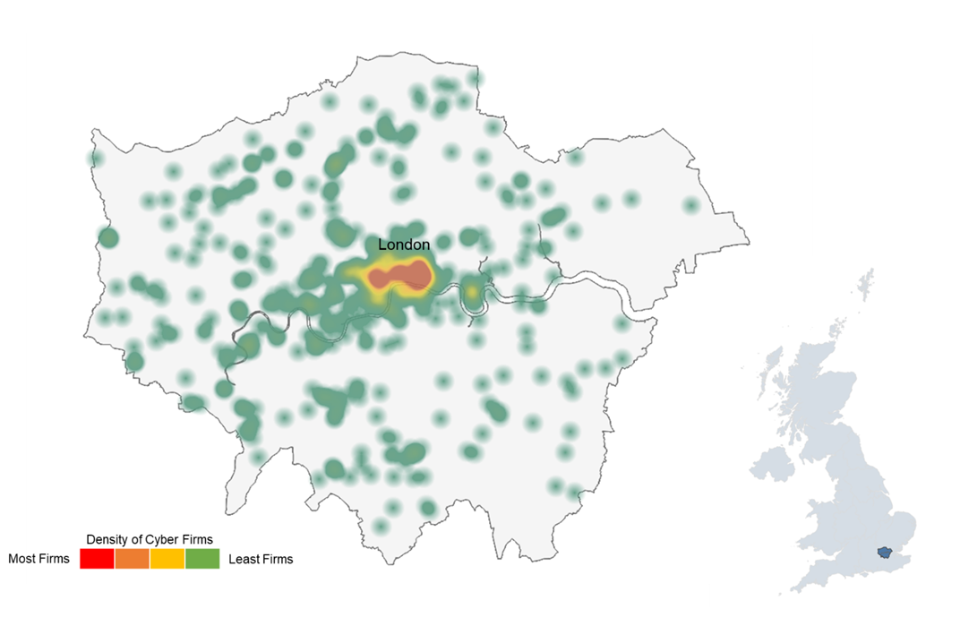

Figure 3.2 also highlights the number of active offices by Travel to Work Area (TTWA)[footnote 11], and emphasises sustained hotspots in areas such as Greater Manchester, Bristol and Bath, Cheltenham, Belfast, Glasgow, Edinburgh, Newcastle, and the Oxford-Cambridge Growth Corridor.

Figure 3.2: Active cyber security offices by travel to work area (TTWA)

Source: Perspective Economics (n=5,374) (Darkest blue denotes any TTWA with >100 active offices)

3.3 International activity

This section outlines where UK registered cyber security firms have an established physical presence in another country. This helps to inform a further understanding of where firms are exporting, are engaged in international markets, or where multinational firms have a presence in the UK. For the dedicated providers of cyber security products and services, we have identified:

-

414 UK-headquartered dedicated cyber security businesses with a physical presence in international markets (denoted by an office presence);

-

A further 530 cyber security businesses (dedicated and diversified) active in the UK appear to be headquartered or originate from outside the UK.

For the 414 UK-headquartered dedicated cyber security businesses, the following chart sets out the main trading regions (totalling to more than 100%, since firms have offices across multiple locations):

Figure 3.3: Regions with an international presence (by UK-headquartered cyber security firms)

| United States | 62% |

| EU/EEA | 62% |

| India | 14% |

| Australia | 14% |

| United Arab Emirates | 11% |

| Canada | 9% |

| Singapore | 7% |

| South Africa | 6% |

| Japan | 4% |

| Israel | 4% |

Source: Perspective Economics (n = 414)

As with previous years, the United States and European Union / European Economic Area are core markets for international trading [footnote 12], with key markets including Germany, Netherlands, Spain, France, and Ireland. In recent years, the UK has also been a clear international destination for foreign direct investment (FDI) in cyber security. We have also identified where international firms (n = 530) have set up a physical presence in the UK (related to cyber security). We find that key nations (by count) continue to include the US, India, Canada, Israel, France, Germany, Australia and Ireland.

4. Economic contribution of the UK cyber security sector

Section Summary: Economic Contribution of the UK Cyber Security Sector

-

We estimate that total annual revenue within the sector has reached £14.7 billion, reflecting a nominal increase of c. 11% since last year’s study. The majority (70%) of revenue is earned by large firms; however, average cyber security revenue among small firms has increased by approximately 25%, and there are now 241 firms with over £10 million in annual revenues (up from 105 two years ago).

-

We estimate there are approximately 69,600 Full Time Equivalents (FTEs) working in a cyber security related role, an increase of c. 2,300 (3%). This is the lowest recorded growth rate since the series began in 2018, suggesting a significant softening in workforce growth.

-

Total GVA for the sector has reached c. £9.1 billion (+17%), with estimated GVA per employee increasing from £116,200 to £131,200 (+13%). The GVA-to-turnover ratio has also improved (from 0.59 to 0.62), suggesting increasing levels of productivity within the cyber security ecosystem.

-

Most of the employment growth within the sector over the last 12 months has been driven by product-based firms (rising to 27,164 FTEs, 39% of the total), while service and MSSP related employment has effectively stabilised at c. 42,400.

-

The average size of a cyber security team has reduced from 31 to 27 staff (and from 204 to 180 in large enterprises), potentially highlighting workforce efficiencies throughout some of the largest employers in the market.

4.1 Estimated revenue

In the most recent financial year, annual cyber security revenue within the sector is estimated at £14,735 million (rounded to £14.7 billion). This reflects an increase of 11%[footnote 13] from last year’s study (£13.2 billion). This figure is estimated using:

-

Revenue figures available for dedicated (pure-play) cyber security firms that publish annual accounts

-

Revenue figures available for diversified cyber security firms (multiplied by the estimate of the proportion of the firm’s activity related to cyber security, typically based upon headcount or reported proportions in annual accounts or survey responses)

-

Estimated cyber security revenue within the cyber sector survey (for most recent financial year)

-

Where gaps exist, employment has been sourced or estimated, with revenue estimated using ‘revenue per employee’ (estimated by size using known data) multiplied by ‘number of employees’ to provide an estimated revenue figure on a firm-by-firm basis. These modelled estimates are subject to wider variance than figures drawn directly from company accounts.

This revenue estimate relates to revenue attributable to cyber security activity only. The following subsections set out revenue by size, revenue by size and dedicated/diversified categorisation, and revenue by key company offer. Please note that as the analysis was undertaken in late 2025, we use the most recent financial year reporting data where possible, which means that much of the revenue will have been achieved through work delivered and billed in 2024 (e.g., if a company has a financial year ending March 2025, those accounts will reflect billed work from April 2024 – March 2025).

Revenue by firm size

We estimate that the majority (£10.4 billion, 70%) of all UK cyber security revenue is earned by large firms (which further demonstrates the earning power of these firms given that they reflect 9% of all market providers). This includes several very large firms in telecommunications, aerospace, defence and security, and consultancies for which the size and scale of their respective cyber security product and service divisions reflect a considerable proportion of the wider market. Analysis of these 240 large providers also highlights that:

-

153 large firms are UK headquartered with estimated UK cyber security revenue of £6.1 billion

-

87 are international firms (headquartered outside of the UK) but have a registered presence in the UK market with estimated UK cyber security revenue of approximately £4.2 billion

Medium firm revenues have sustained their revenue share in relative and absolute terms, at 19% (compared to 21% last year) with £2.9 billion generated in the last 12 months.

Small firms have encouragingly increased revenues over this period (from £790 million to £1,269 million). The average cyber security related revenue among small firms has increased from approximately £2 million in the previous study (2025) to £2.5 million in the last 12 months (an average increase in revenue by approximately 25% among small firms). Further, we estimate that micro firms have generated £251 million in this period.

Figure 4.1: Total cyber security revenue by size of firm

| Large | £10,363M |

| Medium | £2,852M |

| Small | £1,269M |

| Micro | £251M |

Source: Perspective Economics (n=2,603)

Segmentation of revenue by both size and by whether the firm is understood to be ‘dedicated’ or ‘diversified’ also provides an overview of which firms are driving the revenue within the sector.

This highlights that ‘diversified’ firms continue to generate significant revenues through their cyber security offer. However, for Small and Medium Enterprises (SMEs) including micro firms, dedicated cyber security firms generate the greatest proportional revenue (i.e., c. 83% of revenues for each of the SME categories[footnote 14]).

Figure 4.2: Total cyber security revenue by size by dedicated / diversified status

| Size | Dedicated | Diversified |

|---|---|---|

| Large | £4,748M | £5,614M |

| Medium | £2,307M | £546M |

| Small | £1,119M | £150M |

| Micro | £221M | £30M |

Source: Perspective Economics (n = 2,603)

Review of firm level cyber security related revenue also highlights that the UK market has:

-

Approximately 32 large, diversified ‘anchor’ firms generating over £50 million in cyber security revenues (up from 28 last year). Although cyber security may often represent a small proportion of their overall business (for example, a multinational consultancy with £1 billion in total revenue and a £50 million cyber practice), these firms account for a substantial proportion of the UK cyber sector’s total revenue.

-

A significant growing middle market: There are now 241 firms (an increase from 219 in 2025, and more than twice the figure of 105 firms in 2024) that we have identified as providers of cyber security with over £10 million in annual revenues.

Further, segmentation of revenues by size and by those companies that either provide (as a core role) cyber security products or services is set out in Figure 4.3 below.

Overall, service providers including Managed Service Providers (MSPs) and Managed Security Service Providers (MSSPs)[footnote 15] are generating approximately £8.4 billion in cyber security related revenues (up from £7.4 billion last year). The revenue of product companies has also increased to c. £6.4 billion (up from £5.6 billion last year).

Figure 4.3: Total cyber security revenue by size and by offering

| Offering | Large | Medium | Small | Micro | Total |

|---|---|---|---|---|---|

| Services (including MSSPs) | £6,087M | £1,328M | £768M | £200M | £8,383M |

| Product | £4,276M | £1,524M | £501M | £63M | £6,364M |

Source: Perspective Economics (n = 2,603)[footnote 16]

4.2 Estimated employment

We estimate that there are 69,589 Full Time Equivalents (FTEs) working in a cyber security related role across the 2,603 cyber security firms identified.

This reflects an increase of 3% (up from 67,299 last year) in employee jobs within the last 12 months. This growth is the lowest recorded growth rate in employment within the sector since this study began in 2018 and suggests a significant softening in workforce growth. We set out estimated cyber security sectoral employment by year in Figure 4.4, as set out within previous sectoral analysis reports.

Figure 4.4: Cyber security employment (annual estimates)

| 2020 | 46,683 |

| 2021 | 52,727 |

| 2022 | 58,005 |

| 2023 | 60,689 |

| 2024 | 67,299 |

| 2025 | 69,589 |

Source: Perspective Economics

Factors shaping employment and workforce activity are explored further in the annual DSIT Cyber Security Skills in the UK Labour Market research.

Company level employment is initially estimated at the registered office location level (i.e., this suggests concentrated employment within Greater London and the South East is 72% of the UK figure). As a result, this has the effect of underestimating employment for the other regions, because employers often have employees across the UK. As such, in Figure 4.5, we provide the estimated employment breakdown by region. This estimate draws upon Perspective Economics modelling[footnote 17] of key regional employers, and regional cyber security workforce estimates. These are explored in further detail in the annual DSIT Cyber Security Skills in the UK Labour Market research, but include assessment of regional workforce roles, multiple office locations, regional market intelligence, vacancy data, and review of wider estimates such as Annual Population Survey / Labour Force Survey.

Figure 4.5: Estimated cyber security employment by region

| Region | Estimated | Registered |

|---|---|---|

| London | 30% | 49% |

| South East | 13% | 23% |

| North West | 10% | 7% |

| South West | 9% | 5% |

| West Midlands | 8% | 3% |

| Scotland | 7% | 2% |

| East of England | 7% | 5% |

| Yorkshire and The Humber | 5% | 2% |

| Northern Ireland | 4% | 1% |

| East Midlands | 4% | 1% |

| Wales | 3% | 1% |

| North East | 3% | 1% |

Source: Perspective Economics (n = 69,589 FTEs, estimate)

Analysis of estimated cyber security employment by company size (Figure 4.6) demonstrates that, in line with last year’s findings, most cyber security employment remains concentrated within large firms (62%).

Based on review of company level data, we estimate that the average size of a cyber security team within the sector has reduced since last year’s study, from 31 staff to 27 staff. Further, the average size of a cyber security team within large enterprises (firms with over 250 employees) has reduced from 204 cyber security staff in the previous study to 180 staff (an average reduction of 12%) potentially highlighting workforce efficiencies throughout some of the largest cyber security employers in the market. As set out in Section 4.3, this has resulted in higher levels of reported productivity (as measured through Gross Value Added) per employee within the sector.

Figure 4.6: Estimated cyber security employment by size of firm

| Large | 43,310 |

| Medium | 15,871 |

| Small | 6,897 |

| Micro | 3,511 |

Source: Perspective Economics (n=69,589)

Figure 4.7 sets out employment segmented by ‘Dedicated’ and ‘Diversified’ firms. In contrast to the previous year, the latest data suggests that dedicated cyber security firms are driving the majority of employment growth. Dedicated firms added an estimated 2,100 FTEs (+5%), compared to fewer than 200 (<1%) in diversified firms. We estimate that 60% of sectoral employment takes place within dedicated firms.

Figure 4.7: Estimated cyber security employment by dedicated / diversified

| Dedicated | 41,872 |

| Diversified | 27,717 |

Source: Perspective Economics (n=69,589)

Figure 4.8 also sets out cyber security related employment segmented by company core offering. Just under two-thirds (61%) of employees work within a company that primarily offers cyber security services or managed services, compared to 39% that work primarily within a product environment.

In previous years, the number of cyber security staff working within product companies had increased (from 15,278 in 2021, 33% of cyber security staff) to 23,952 FTEs in last year’s report. This trend has continued, growing to 27,164 FTEs (39% of cyber security staff), particularly as firms seek to develop products or integrate tooling into platforms for end-customer use.

Service and MSSP related cyber security employment has effectively stabilised at 42,425 FTEs[footnote 18] (from 42,232 last year), after growing 14% in the previous year (2024). This suggests a potential cooling down in service related employment. Further, this means that most of the employment growth within the cyber security sector captured within the study over the last 12 months has been driven by product-based firms.

As set out in Figure 4.8, cyber security product firms typically operate with larger teams than their service counterparts, with an average of 37 FTEs compared to 23 for services, and a median of 5 FTEs for product firms compared to 2 for services. This may reflect the prevalence of smaller independent consultancies and advisory practices within the service segment.

Figure 4.8: Estimated cyber security employment by offering

| Services (including MSSPs) | 42,425 |

| Product | 27,164 |

Source: Perspective Economics (n=69,589)

4.3 Estimated Gross Value Added (GVA)

Gross Value Added (GVA) is used as a measure of productivity (at a firm level, or above). It captures the sum of a firm’s Gross Profit, Employee Remuneration, Amortisation and Depreciation. In this respect, any increase in GVA can highlight an improvement in the performance of a firm or a sector, as evidenced through higher profitability or enhanced earnings.

We estimate that within the most recent financial year, cyber security related GVA (for the 2,603 firms) has reached £9.1 billion (£9,131 million). This is a significant increase of £1.3 billion (+17%) since last year’s report from £7.8 billion.

Figure 4.9 sets out an overview of GVA (compared to revenue) by size of firm. Overall, this data suggests an increased GVA-to-turnover ratio of 0.62:1 (i.e., for every £1 of revenue the sector generates, 62p in direct GVA is generated, compared to 59p last year and 54p in the prior year). This suggests increasing levels of productivity within the cyber security ecosystem.

Table 4.2 also sets out the estimated GVA per employee at approximately £131,200 per employee. This is an increase of 13% from the previous year’s estimate of £116,200). GVA per employee provides an estimate of labour productivity in the sector, as it typically captures remuneration and profitability.

Figure 4.9: Total cyber security revenue and GVA by size of firm

| Size | Estimated Revenue | Estimated GVA |

|---|---|---|

| Large | £10,363 million | £6,459 million |

| Medium | £2,852 million | £1,744 million |

| Small | £1,269 million | £728 million |

| Micro | £251 million | £200 million |

Time-series analysis

The table below sets out the key metrics for the cyber security sector, as tracked by each sectoral study since 2020.

Table 4.1: Key sector metrics (since 2020)

| Year | Number of Firms | Change | Employment | Change | Revenue | Change | GVA | Change | Investment (Dedicated) | Change |

|---|---|---|---|---|---|---|---|---|---|---|

| 2020 | 1,483 | +21% | 46,683 | +9% | £8,878m | +7% | £4,003m | +6% | £821m | +169% |

| 2021 | 1,838 | +24% | 52,727 | +13% | £10,146m | +14% | £5,326m | +33% | £1,013m | +23% |

| 2022 | 1,979 | +8% | 58,005 | +10% | £10,462m | +3% | £6,228m | +17% | £302m | -70% |

| 2023 | 2,091 | +6% | 60,689 | +5% | £11,859m | +13% | £6,450m | +4% | £271m | -10% |

| 2024 | 2,165 | +4% | 67,299 | +11% | £13,234m | +12% | £7,820m | +21% | £206m | -24% |

| 2025 | 2,603 | +20% | 69,589 | +3% | £14,735m | +11% | £9,131m | +17% | £184m | -11% |

| Estimated CAGR (2020–25)[footnote 19] | 11.9% p.a. | 8.3% p.a. | 10.7% p.a. | 17.9% p.a. | — |

4.4 Summary

The table below sets out the key findings regarding the economic contribution of the UK’s cyber security sector, as per this year’s analysis (2025).

Table 4.2: Summary of cyber sector economic contribution (2025)

| Size | Number of Firms | Estimated Revenue | Estimated GVA | Estimated Employment (FTE) | Revenue per Employee | GVA per Employee |

|---|---|---|---|---|---|---|

| Large | 240 | £10,363m | £6,459m | 43,310 | £239,268 | £149,136 |

| Medium | 343 | £2,852m | £1,744m | 15,871 | £179,713 | £109,891 |

| Small | 507 | £1,269m | £728m | 6,897 | £183,982 | £105,568 |

| Micro | 1,513 | £251m | £200m | 3,511 | £71,481 | £57,001 |

| Grand Total | 2,603 | £14,735m | £9,131m | 69,589 | £211,741 | £131,219 |

Source: Perspective Economics

5. Investment in the UK cyber security sector

Section summary: investment in the UK cyber security sector

-

In 2025, £184 million has been raised across 47 deals within dedicated cyber security firms. This represents a reduction of 11% compared to 2024 (£206 million across 59 deals), though the rate of decline has softened compared to the previous year.

-

In contrast to 2024, where medium sized firms accounted for 69% of investment value, 2025 has seen a shift towards smaller firms. Small firms accounted for the largest share by value (£84 million, 46%), and micro firms also saw increased investment (£43 million, 23%), suggesting growing investor appetite for earlier-stage opportunities.

-

London is the top performing region for cyber security investment (£103 million, 56%). In 2025, 37% of investment raised was across the 10 regions outside of London and the South East, above the levels seen in 2022 (25%) and 2023 (35%), though below the 49% recorded in 2024.

-

Investor consultations highlight AI security and post-quantum cryptography as key investment themes. Investors reported improved deal flow and founder quality but cited procurement barriers and the availability of UK growth stage capital as ongoing concerns.

5.1 Introduction

This section draws upon the Beauhurst platform which tracks announced and unannounced investments in high-growth companies from across the UK. Our team has matched Company Registration Numbers and Company Names identified within this current analysis with the platform to identify 1,077 fundraisings[footnote 20] associated with 318 cyber security companies. This chapter focuses on investment activity within the full year of 2025 (1st January – 31st December), and typically explores investment raised by dedicated cyber security firms.

5.2 Investment to date

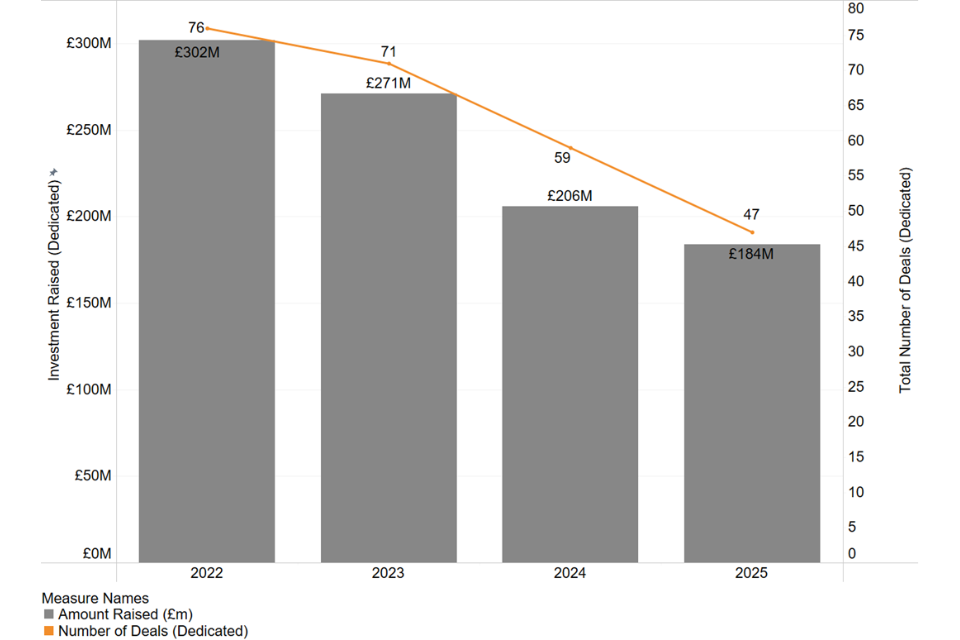

The investment timeline (Figure 5.1) demonstrates that 2025 has remained challenging for cyber security investment compared to previous years. This includes £184 million raised across 47 deals within dedicated cyber security firms.

As set out with the previous report, since 2022, external investment into private firms has reduced across sectors, as interest rates have risen, and as firm-level valuations have been revised. The Beauhurst State of UK Investment H1 2025 Update[footnote 21] highlights that, for example, the amount raised by UK private companies across all sectors in H1 2025 (£8.6 billion) is 34% lower than that raised in H1 2024 (£13.1 billion). The research conducted by Beauhurst notes that it is “increasingly clear we may be settling into a lower baseline for investment activity. The sharp peaks of previous years, including the post COVID-19 investment boom in 2021 and 2022, have given way to a flatter, more cautious landscape.”

As shown in Figure 5.1, investment levels into the UK cyber security sector have reduced year on year since 2022, and this has continued into 2025. We estimate there has been a reduction in the overall investment raised by UK dedicated cyber security firms in the most recent year (reducing from £206 million in 2024 to £184 million in 2025, a decrease of 11%). However, this is a softer decline than seen between 2023 and 2024 (a decrease of 24%) which may indicate some levelling off in activity. Further, this has been raised across 47 investment deals, with a range of investors still highly engaged with the sector, particularly among domestic funds, such as Osney Capital’s Fund 1[footnote 22], a cyber security specialist seed fund focused on early-stage UK cyber security. Section 5.5 explores some of the views among the investment community.

Figure 5.1: Total external investment

Source: Perspective Economics analysis of Beauhurst data

5.3 Investment by location

Figure 5.2 sets out an overview of investment performance within cyber security by UK region, with respect to value and volume of investment.

In 2025, London is the top performing region for cyber security investment, with £103 million raised (56%) across 22 deals. In London, notable fundraisings this year include Inforcer (£26 million raised in July 2025 to help MSPs standardise Microsoft 365 security policies), Maze (launching with $25 million (£18.4 million) in Series A and $6 million prior investment to scale AI cloud security agents). Yorkshire and the Humber also saw the second highest value of activity (£23 million), via a deal driven by Optalysys, which builds photonic computers for secure encrypted data processing. Further, Sitehop (based in Sheffield, with a registered address in London) secured £7.5 million in October 2025 to help ‘future-proof networks against quantum threats’.

Further, the data highlights some encouraging activity across the regions in the UK. The South East recorded 6 deals worth £12.8 million, including Cybaverse (£5 million) and Adarga (£4.3 million), while the North West saw 7 deals totalling £10.5 million, with firms such as Zally (£2.8 million) and usecure (£3 million) securing funding. Scotland also attracted £7.3 million across 3 deals, notably Approov’s £5 million Series A for mobile app security.

London and the South East collectively account for 28 deals (60% of the UK total). However, 2025 continued to see investment activity spread across UK regions, with deals recorded in the South West (Blueskytec, £1.5 million), West Midlands (SecureCloud+, £5 million), and North East (GoDefend), £250,000). However, given the reduction in overall number of deals among dedicated cyber security firms at a UK level, some smaller regions had reduced, or no investments were identified within the Beauhurst investment data.

Increasing access to investment across the regions remains a key tenet of national cyber security and economic strategy, as set out in the Industrial Strategy (2025). In 2025, 37% of investment raised was across the 10 regions outside of London and the South East. Whilst this is lower than the 49% recorded in 2024, it remains above the levels seen in 2023 (35%), 2022 (25%), and significantly higher than the 9% recorded in 2021. This suggests that regional investment activity, supported by schemes such as Cyber Runway and regional investor networks, continues to broaden access to capital for cyber security firms across all regions.

Figure 5.2: Total investment by region (2025)

| Region | Amount Raised | Number of Deals |

|---|---|---|

| London | £103.2M | 22 |

| Yorkshire and the Humber | £23.4M | 1 |

| East of England | £19.6M | 2 |

| South East | £12.8M | 6 |

| North West | £10.5M | 7 |

| Scotland | £7.3M | 3 |

| West Midlands | £5.4M | 2 |

| South West | £1.6M | 2 |

| North East | £0.3M | 2 |

Source: Beauhurst

5.4 Investment by size

Figure 5.3 sets out the volume of investment by company size within the cyber security sector in 2025. This data suggests that in 2025:

-

Small firms (10 to 49 employees) raised £84 million (46%) across 18 deals

-

Medium sized firms (50 to 249 employees) raised £57 million (31%) across 10 deals

-

Micro firms (1 to 9 employees) raised £43 million (23%) across 19 deals

In contrast to 2024, where medium sized firms accounted for 69% of investment value, 2025 has seen a shift towards smaller firms. Small firms accounted for the largest share of investment by value, raising £84 million (46%) compared to £35 million (17%) in 2024. Micro firms also saw increased investment, raising £43 million (23%) compared to £29 million (14%) in 2024. This suggests growing investor appetite for earlier stage opportunities, particularly in emerging areas such as post-quantum security and AI security.

Figure 5.3: Total investment by company size (2025)

| Medium (50-249 employees) | £57M |

| Small (10-49 employees) | £84M |

| Micro (1-9 employees) | £43M |

Source: Beauhurst

5.5 Investor views

Across the investor consultations undertaken by Ipsos in late 2025, investors were also asked about their main criteria for investing in cyber security businesses in the UK, the role of AI in cyber security, their view on the UK as a ‘destination’ for cyber security investment (including regional and national considerations), changes over the last year and how they expect the landscape to develop, and any other feedback on where additional support would help to catalyse further investment. We set out some key feedback below. Please note that this is a small sample, covering indicative sentiment. It is not considered representative of the full investment community but does provide insight into key areas.

Market outlook and investment criteria

Several investors, particularly at angel and pre-seed levels, reported an uptick in deal flow compared to 2024, with an increase in potential investment opportunities compared to the previous year, and improved assessment of long-term growth opportunities. AI has been reported as a key component of investment theses, both for AI-powered cyber security solutions and for securing AI systems directly. However, investors noted that they were carefully scrutinising AI claims to distinguish genuine innovation from more generic use cases.

“We’re seeing no shortage of deal flow, with 3 or 4 companies [reviewed] every couple of weeks.” — Angel Investor

“The prices for the sector have gone up. I think there’s people getting more excited about [cyber] again and multiples are up.” — Venture Capital Investor

“Every single company I meet now has some sort of AI story. You can’t get away from it. From a sector perspective, it creates new opportunities for new companies to be disruptive to established players.” — Venture Capital Investor

“We spend quite a bit of time, particularly if companies are saying they’re using AI within their products, to really get under the skin of that. Is that genuine innovation or are they just putting a skin on a large language model?” — Angel Investor

Key investment areas identified within consultations included:

-

AI security: Agentic AI (creating new risk categories), securing AI workloads, monitoring AI use, and explainable AI

-

Quantum and post-quantum cryptography: Heightened interest following NCSC guidance on migrating to post-quantum technology, though investment timelines remain uncertain

-

Market Consolidation: Private equity interest in bundling MSSPs and niche solutions into direct platforms

-

Recovery and incident response solutions driven by high-profile breaches

-

Hardware security and semiconductor security, including memory safety at chip level

“Agentic AI is a whole new set of risks and family of risks that we’re not used to dealing with. When we talk about agents, we’re talking about groups of systems with different accesses to data that can tell each other to do things. I would say that is a 2025 new problem.” — Venture Capital Investor

“Post-quantum cryptography is now becoming more urgent. In the last 12 months the NCSC have published their guidance around migrating to post-quantum technology ahead of Q-Day.” — Angel Investor

Innovation pipeline and early-stage support

The UK’s innovation ecosystem was viewed positively, with investors noting a significant improvement in the quality of founders. Universities remain central to the ecosystem, and increasing specialisation within cyber security has created more investment opportunities. Government-backed accelerator programmes, particularly Cyber Runway and CyberASAP, were highlighted as valuable contributors to the pipeline.

“In the last 12 months, there’s been a big step up in quality of entrepreneurs looking at starting cyber businesses…in 2025, the number of really great early companies that I’ve met has been great.” — Venture Capital Investor

“Innovation happens in many places across the UK. From a university perspective, we’ve seen quite a bit come out of the CyberASAP programme.” — Angel Investor

Government role and market development

Government support for the early-stage ecosystem was valued, with investors highlighting programmes such as CyberASAP and deployment of capital through the National Security Strategic Investment Fund. Investors encouraged continued and expanded support in this area.

However, investors identified procurement as a significant barrier. Government procurement rules and requirements were seen as providing some obstacles for smaller cyber security SMEs to grow. Investors would like to see the UK government buy more from cyber start-ups.

“[Government] need to open that space up for those SMEs to succeed, which means changing how they engage with their suppliers… actually, we’re going to give our people the freedom to engage with the right suppliers on set terms and trust them to execute on that.” — Venture Capital Investor

“We want to be doing more cyber investing. We’re finding it hard to work out where the best place to play is partly because of the funding journeys that they go on and partly because of the later stage markets. It’s a sector that I think has enormous potential. It’s just we collectively need to find a better way to unlock it, to make sure that UK innovation is funded in the UK rather than snapped up at an early stage.” — Venture Capital Investor

Market challenges and funding environment

The investment landscape has faced uncertainty, with investors discussing macroeconomic and policy factors. Some investors advocated for more strategic deployment of grant funding, particularly focusing on initial product development or commercial progress. A key concern raised was the availability of growth capital in the UK. Investors cited challenges with UK public markets and the availability of private equity at later stages. A related point was a need to promote visible role models for building large UK cyber security companies.

Talent gaps in go-to-market functions were also highlighted. The UK was described as strong in technical talent but weaker in sales capability, with top commercial talent often attracted to the US market.

“The UK public markets need to invest in it. The ability to raise real growth capital within the UK is what will really enable some of these businesses to go big.” — Venture Capital Investor

“I think the market is maturing slightly. Certainly, if I go back 5, even 10 years, there were very few people who are good at selling cyber security. I think there are more now, but they’re still few and far between.” — Venture Capital Investor

Regional development and investment distribution

Investors reported continued and strengthening regional diversity in the cyber ecosystem. Belfast, Cheltenham, Edinburgh and Manchester were highlighted as particularly strong hubs. This has been stimulated by universities, investment in local ecosystems (with CyberASAP cited), and remote working patterns. However, London continues to exert gravity for cyber firms as a source of capital and proximity to major customers according to respondents.

“There has been far more diversity from a geographic perspective. I’d say almost everywhere has grown, at least from the deal flow we see. When I first started, we were heavily dependent on Golden Triangle relationships and I say that’s definitely not the case at the moment.” — Venture Capital Investor

“Probably mostly linked to the universities, their investment into cyber and the ecosystem’s built up around that. My view is that Belfast as a cyber hub is mostly a function of a concerted effort to develop talent and support companies in that city.” — Venture Capital Investor

“It’s just the natural course of growth and business and pursuing opportunity means that you have to be in close proximity to your customers and your sources of private capital… and that means being in London.” — Venture Capital Investor

International positioning