CFM96870 - Interest restriction: joint ventures: group ratio (blended) election: example

If there is third party and related party interest in the example shown in CFM96860 the effect of a blended group ratio can be demonstrated.

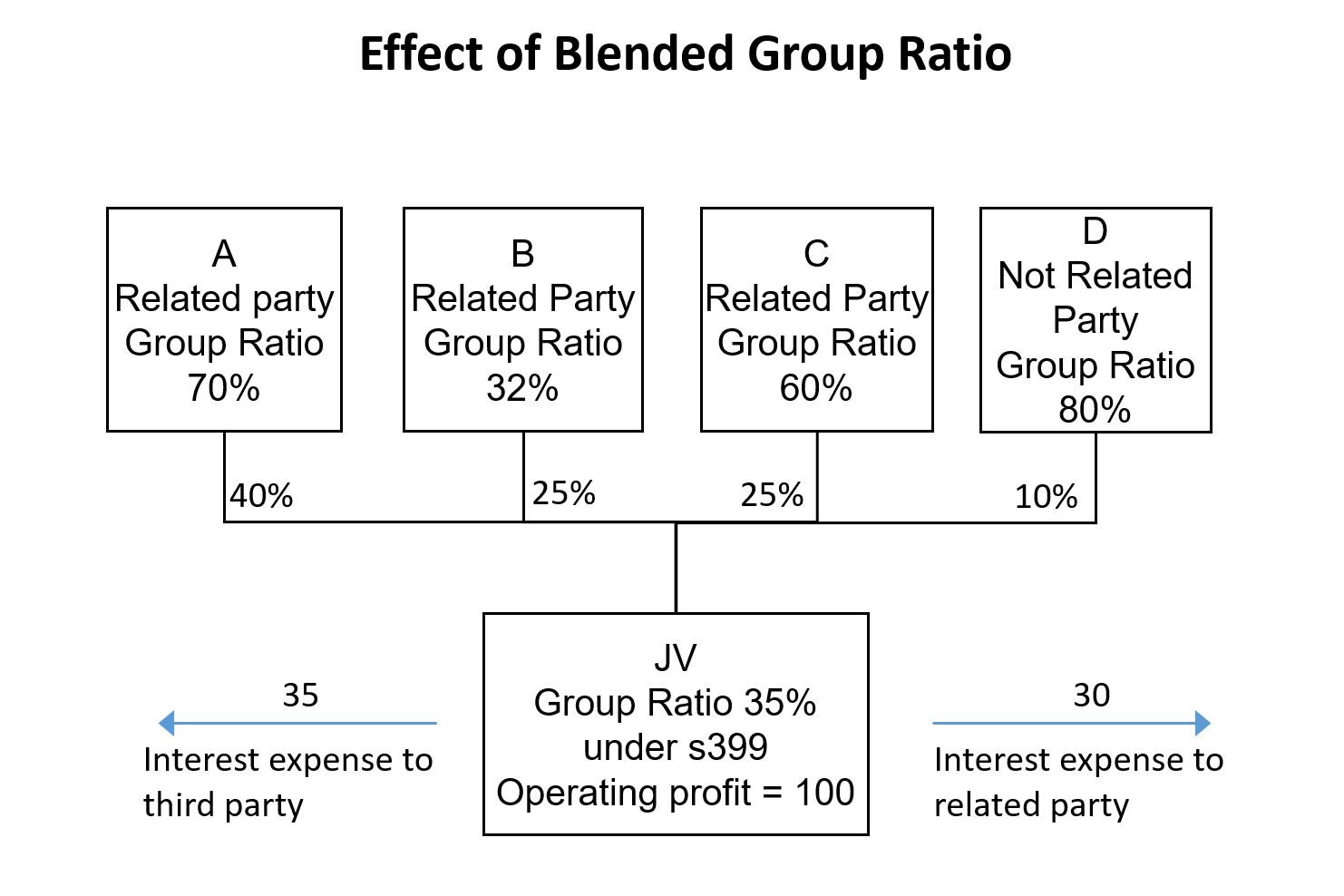

For visual illustration view diagram showing the effect of a blended group ratio on a joint venture

{kind=link}

The diagram shows the effect of applying a blended group ratio to a joint venture (JV) under section 399. The JV has four investors. Three are related parties with group ratios of A 70%, B 32% and C 60%, holding interests of 40%, 25% and 25%. One investor D is not a related party, with a group ratio of 80% and a 10% interest. These interests give the JV a blended group ratio of 35%. The JV has operating profit of 100, with interest expense of 35 paid to a third party and 30 paid to a related party.

Election not made

| Accounts | JV |

|---|---|

| Operating profit | 100 |

| Third party interest expense (QNGIE) | - 35 |

| Related party interest | - 30 |

| Profit before tax | 35 |

| Calculation of adjusted net group-interest expense | JV |

|---|---|

| Third party interest expense | 35 |

| Related party interest expense | 30 |

| Adjusted net group-interest expense | 65 |

| Calculation of group ratio | JV |

|---|---|

| Qualifying net group-interest expense | 35 |

| PBT for the JV | 35 |

| Add back adjusted net group-interest expense | 65 |

| Group-EBITDA | 100 |

| Group Ratio | 35% |

| Interest allowance | JV |

|---|---|

| Tax-EBITDA | 100 |

| X plc group ratio | 35% |

| Interest allowance | 35 |

| Net tax-interest expense | 65 |

| Less interest allowance | - 35 |

| Restriction | 30 |

When the election is not made the group ratio of the JV is calculated under TIOPA10/s399 which works out at 35%. As the related party interest does not contribute to the group ratio there is a restriction of 30 in the JV

Blended group ratio election made

| Accounts | JV |

|---|---|

| Operating profit | 100 |

| 3rd party interest expense (QNGIE) | - 35 |

| Related party interest | - 30 |

| Profit before tax | 35 |

| Calculation of adjusted net group-interest expense | JV |

|---|---|

| Third party interest expense | 35 |

| Related party interest | 30 |

| Adjusted net group interest expense | 65 |

- Blended Group Ratio from example in CFM96860 - 55%

| Interest allowance | JV |

|---|---|

| Tax-EBITDA | 100 |

| Blended group ratio | 55% |

| Interest allowance | 55 |

| Net tax-interest expense | 65 |

| Less interest allowance | - 55 |

| Restriction | 10 |

If this situation is compared to the circumstance where no election is made the restriction is reduced to 10. Therefore, in this circumstance it is advantageous to make a group ratio (blended) election.