CFM96860 - Interest restriction: joint ventures: group ratio (blended) election: application of election

TIOPA10/S401-S404

There may be instances where a worldwide group has a relatively low group ratio but its investors have high group ratios. This can particularly happen in the circumstance in the context of a joint venture (JV) that has significant amounts of related party interest. This can lead to an interest restriction in the JV.

Here we allow the group to elect to have the group ratio profile of its investors. In this circumstance it will have access to a higher group ratio than that calculated in the JV group and the interest restriction can be reduced or in some cases eliminated.

The group ratio (blended) election also includes a debt cap calculation. See CFM96880 for further details.

To take this option, the reporting company of the group must make the election in the interest restriction return.

Who can elect into the group ratio (blended) election

Technically any worldwide group can make an election. However, only a group with a related party investor in the ultimate parent who has a higher group ratio than the group will benefit from making an election. This worldwide group would usually be an entity that is not consolidated into the investor’s worldwide group. For example, a joint venture company, an associated company, or a subsidiary held at fair value that is not consolidated into the worldwide group.

The group in the position of making a blended group ratio election is referred to below as the 'JV group'

How to calculate the Blended Group Ratio of a worldwide group

TIOPA10/S401 provides the rules for calculating a blended ratio of a group. Once an election is made the group ratio percentage of the JV Group does not apply. Instead it is replaced with the group ratio percentage as calculated in TIOPA10/s401(3).

This requires that each investor is considered separately and that the investor’s 'applicable percentage' is multiplied by the investor’s share in the JV group. The amounts are summed together to obtain the blended group ratio.

TIOPA10/s401(4) identifies the investor’s applicable percentage which is the higher of:-

- 30% (the fixed ratio percentage).

- The JV group’s actual group ratio.

- In the case where the investor is a related party, the group ratio of the investor’s worldwide group.

If it is not possible to ascertain the group ratio of a particular investor then the group would be able to use the investor’s applicable percentage, would be the higher of (i) 30% (the fixed ratio percentage); and (ii) the JV group’s actual group ratio as calculated.

TIOPA10/s401(6) applies when the investor has periods of account overlapping the period of account of the JV group. Here the group ratio of the investor is effectively averaged for the period which coincides with the JV group.

Example

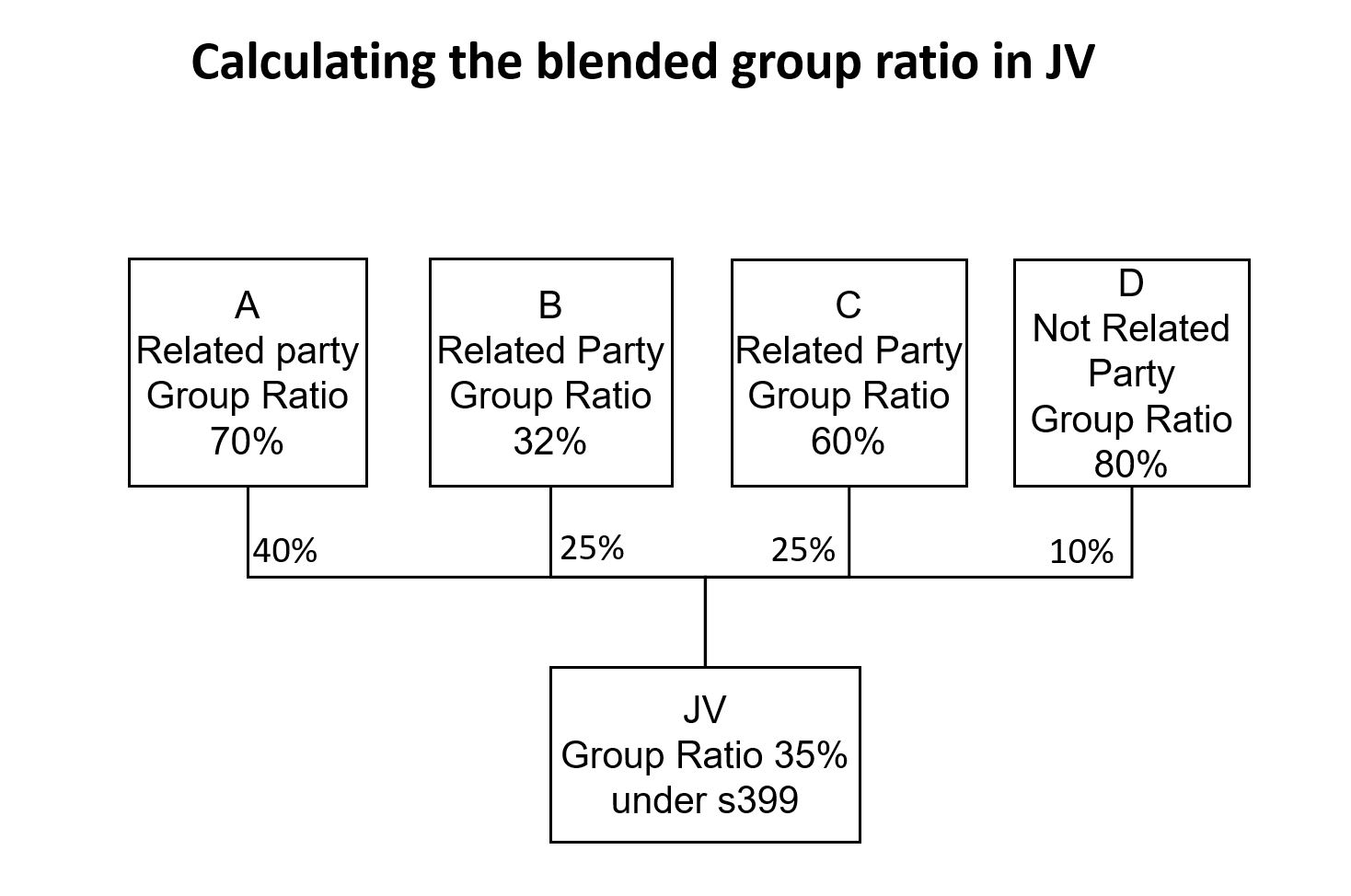

Consider JV that has investors A, B, C and D.

A is a related party, has a share of 40% of JV and a group ratio of 70%.

B is a related party, has a share of 25% of JV and a group ratio of 32%.

C is a related party, has a share of 25% of JV and a group ratio of 60%.

D is not a related party, has a share of 10% of JV and a group ratio of 80%.

JV has calculated its group ratio under TIOPA/s399 as 35%.

For visual illustration view diagram showing how a blended group ratio is calculated for a joint venture

{kind=link}

The diagram shows how the blended group ratio for a joint venture (JV) is calculated under section 399. Four investors participate in the JV. Three are related parties with group ratios of A 70%, B 32% and C 60%, holding interests of 40%, 25% and 25%. One investor D is not a related party, with a group ratio of 80% and a 10% interest. These interests are combined to give the JV a blended group ratio of 35%.

For Investor A the highest applicable percentage is at TIOPA10/s401(4)(c) which is the group ratio of investor A.

Contribution to Blended Group Ratio is 70% × 40% = 28%

For Investor B the highest applicable percentage is at TIOPA10/s401(4)(b) which is the group ratio of JV calculated under TIOPA10/s399 which is 35%

Contribution to Blended Group Ratio is 35% × 25% = 8.75%

For Investor C the highest applicable percentage is at TIOPA10/s401(4)(c) which is the group ratio of Investor C.

Contribution to Blended Group Ratio is 60% × 25% = 15%

For Investor D the highest applicable percentage is at TIOPA10/s401(4)(b) which is the group ratio of JV calculated under TIOPA10/s399 which is 35%. This is because investor D is not a related party.

Contribution to Blended Group Ratio is 35%* × 10% = 3.5%

These four values are summed together to obtain the blended group ratio of JV.

This is 28%+8.75%+15%+3.5% = 55.25%

In this circumstance it will be advantageous to make an election as the blended group ratio is higher than the group ratio as calculated under the normal rules.