CFM96880 - Interest restriction: joint ventures: group ratio (blended) election: blended net group-interest expense

Under the Group Ratio Method the interest allowance is normally set as the lower of:-

- The group ratio percentage applied to the aggregate tax-EBITDA of the group for the period; or

- The group ratio debt cap for the period.

By making the group ratio (blended) election, this allows the interest allowance to be calculated using a blended group ratio. However, when calculating the interest allowance, the group ratio debt cap also needs to be considered. This is particularly important in circumstances where there is a large amount of related party interest expense as the group ratio debt cap will be the limiting factor for the interest allowance.

Referring to the example at CFM96870 if we apply the normal group ratio debt cap then the qualifying net group-interest of the JV will be the third party interest expense of 35. This is lower than the interest allowance calculated under TIOPA10/s398(a) using the blended ratio and so the interest capacity in the example at CFM96870 will be 35. In this case it would cause there to be an interest restriction of 30.

The situation is potentially more restrictive in the situation where the group which makes a blended election has interest expense that consists entirely of related party interest. In this case the qualifying net group-interest expense would be nil so without specific provision the group ratio (blended) election would be ineffective. The group would have to rely on the fixed ratio method and potentially a large interest restriction may happen.

TIOPA10/s402 works in a complementary way to TIOPA10/s401 where a group ratio (blended) election has been made.

Application of the blended net group-interest expense

TIOPA10/S402 modifies the application of the group ratio debt cap where a group (JV group) makes a Group Ratio (Blended) election.

Instead of using the qualifying net group-interest expense of the group for the period, the blended net group-interest expense of the group for the period is used. This requires the blended net group-interest expense to be calculated in accordance with TIOPA10/S402(3)-(4).

To calculate the blended net group-interest expense each investor in the JV group should be considered in turn.

For each investor it needs to be determined how the applicable percentage is determined for the blended group ratio (see CFM 96860). For each investor determine whether step 1, step 2 or step 3 applies. Only one step will apply for each investor.

- Step 1 applies if the fixed ratio percentage of 30% is used for that investor (TIOPA10/S401(4)(a)). Under this step the adjusted net group-interest expense of the group is multiplied by the investor’s share in the group.

- Step 2 applies if the actual group ratio of the group is used for that investor (TIOPA10/S401(4)(b)). Under this step the qualifying net group-interest of the group is multiplied by the investor’s share in the group.

- Step 3 applies if the actual group ratio of the investor’s worldwide group is used for that investor (TIOPA10/S401(4)(c)). Calculating the amount in this step requires consideration of TIOPA10/s402(4) to (8):

- TIOPA10/s402(4) determines the applicable net group-interest expense of the investor’s worldwide group. This looks at loans or other financial arrangements in the investor’s worldwide group that create qualifying net group-interest expense which are then used to fund (directly or indirectly) loans, or other financial arrangements, to the group making the blended election. Therefore if third party finance is taken out and wholly used to fund the JV group all of the gross amounts of qualifying net group interest expense from the third party finance is the applicable net group-interest expense.

- TIOPA10/s402(7)-(8) consider the situation where loans or other arrangements are used to part fund the JV group and part fund another purpose. In this case the applicable net group-interest expense is determined by how much of the qualifying net group interest expense is referable to the funding of the JV group on a just and reasonable basis. Therefore if the investor group takes out a third party loan that has 100 of qualifying net group-interest expense and it is determined that half of this loan is used to fund the JV and the other half is used to fund another purpose then the applicable net group interest expense will be 50.

Once these amounts have been calculated for each investor step 4 adds together the amounts for each investor together and this is the blended net group-interest expense for the group making the group ratio (blended) election.

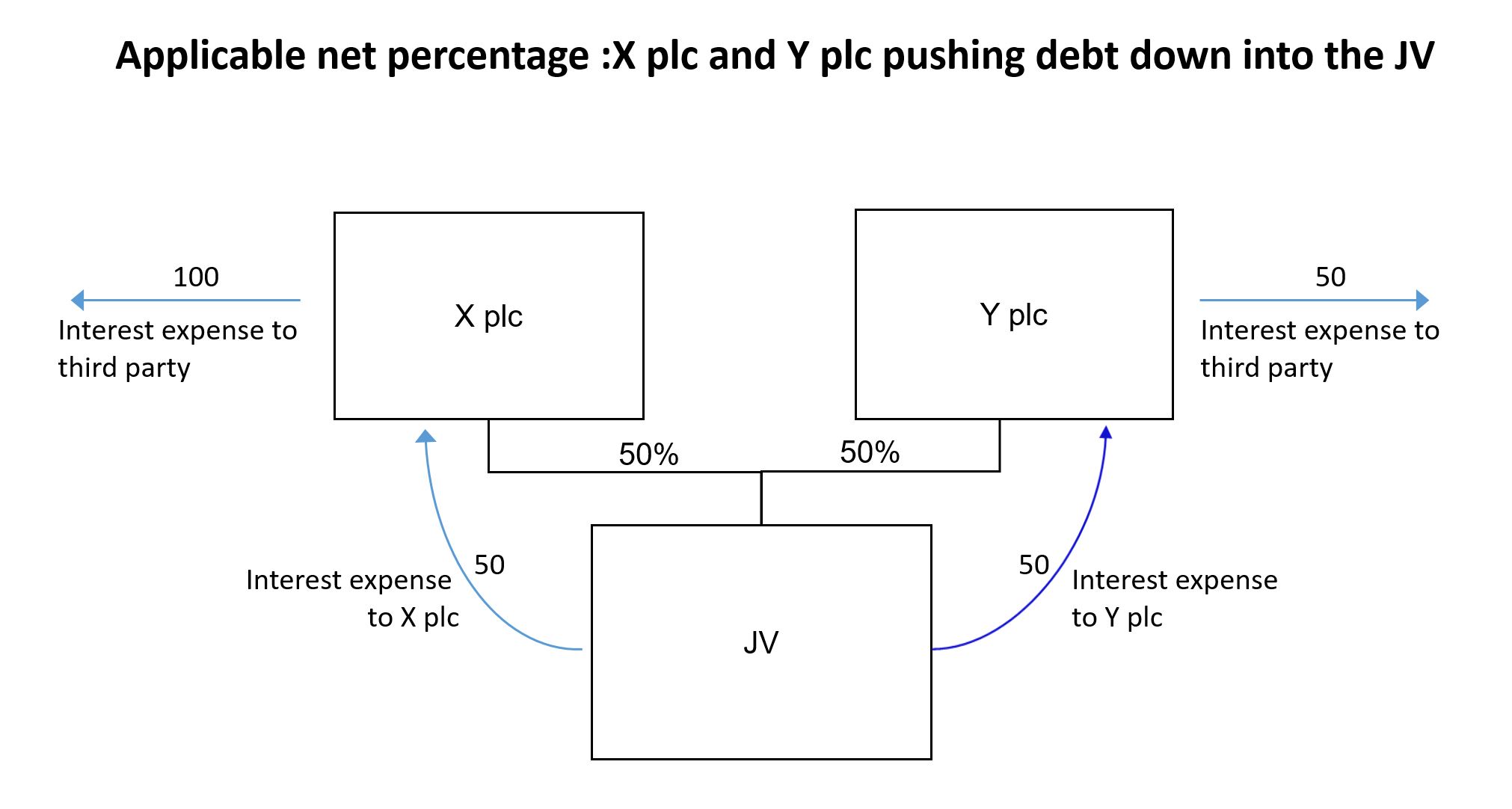

Example: Investors push down debt into a JV

For visual illustration view diagram showing X plc and Y plc pushing debt down into a joint venture

{kind=link}

The diagram shows X plc and Y plc each holding a 50% interest in a joint venture (JV) and pushing debt down into the JV. X plc incurs interest expense of 100 payable to a third party, and Y plc incurs interest expense of 50 payable to a third party. The JV pays interest of 50 to X plc and 50 to Y plc.

X plc has a gross amount of qualifying net group-interest expense of 100 from a third party loan. However only part of the third party loan is invested in JV. It can be determined that 50 of this third party interest relates to the investment of funds in in JV. Therefore the applicable net group-interest expense is 50 in this case.

Y plc has a gross amount of qualifying net group-interest expense of 50 from a third party loan and all of the third party loan is invested in JV. Therefore the applicable net group interest of Y plc is 50.

Combining the results of X plc and Y plc mean that here the blended net group-interest expense of JV is 100 which is the group ratio debt cap for this example.