CFM96800 - Interest restriction: joint ventures: interest allowance (non-consolidated investment) election: example 3: JV group

For visual illustration view diagram showing interest allowance where a JV group makes a non consolidated holdings election

{kind=link}

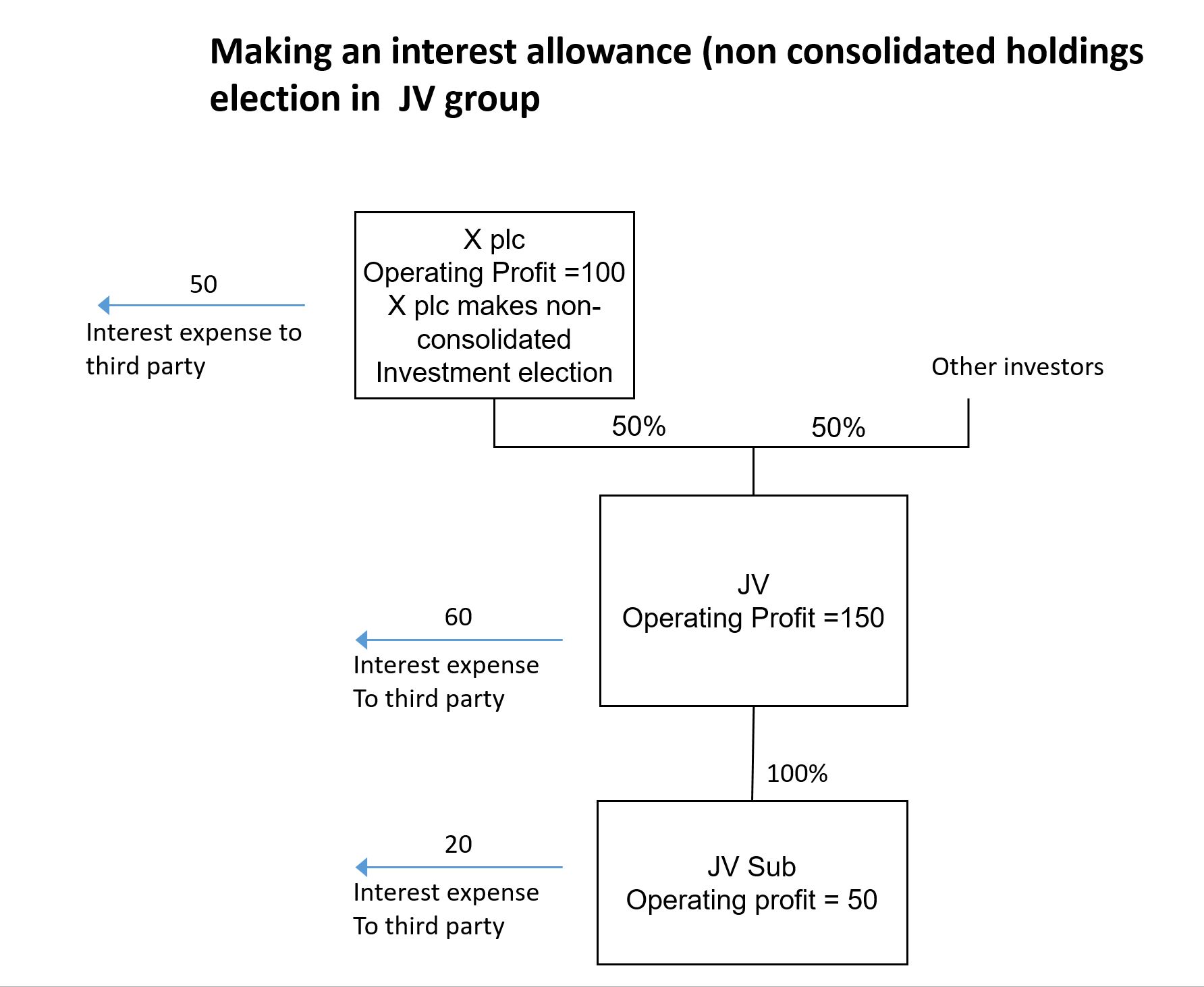

The diagram is showing how interest allowance is calculated where X plc has a non consolidated holdings election in a joint venture group, including X plc, the JV and its subsidiary, and their interest expenses.

Here the example at CFM96780 has been extended to a JV with a subsidiary which has operating profit of 50 and third party interest of 20. Applying the election requires that the results of the JV are consolidated and values can be included from qualifying net group-interest expense and group-EBITDA as before.

| Consolidating the JV group | JV | JV Sub | JV Group |

|---|---|---|---|

| Operating profit | 150 | 50 | 200 |

| 3rd party interest expense | - 60 | - 20 | - 80 |

| Profit before tax | 90 | 30 | 120 |

| Accounts | X plc | JV Group | X plc group |

|---|---|---|---|

| Operating profit | 100 | 200 | 100 |

| 3rd party interest expense | - 50 | - 80 | - 50 |

| Share of profits of JV group | - | - | 60 |

| Profit before tax | 50 | 120 | 110 |

- X plc group share of profits from JV - 50%

| Calculation of QNGIE | X plc Group |

|---|---|

| QNGIE in X plc | 50 |

| Share of JV Group QNGIE | 40 |

| Total QNGIE - (A) | 90 |

| Calculation of group-EBITDA | X plc Group |

|---|---|

| Group-EBITDA of X plc group | 160 |

| Reduction in group-EBITDA | - 60 |

| Share of JV group's group-EBITDA | 100 |

| Group-EBITDA - (B) | 200 |

- Group ratio - (A/B) - 45%

| Interest allowance | X plc |

|---|---|

| Tax-EBITDA | 100 |

| X plc group ratio | 45% |

| Interest allowance | 45 |

| Net tax-interest expense | 50 |

| Less interest allowance | - 45 |

| Restriction | 5 |

X plc gets a share of the JV group qualifying net group-interest expense of 40. However there is also a net increase of group-EBITDA of 40. In this case X plc can calculate its group ratio of 45% and for this example there is an interest restriction of 5.