CFM96790 - Interest restriction: joint ventures: interest allowance (non-consolidated investment) election: example 2: opaque JV with loan from the principal worldwide group

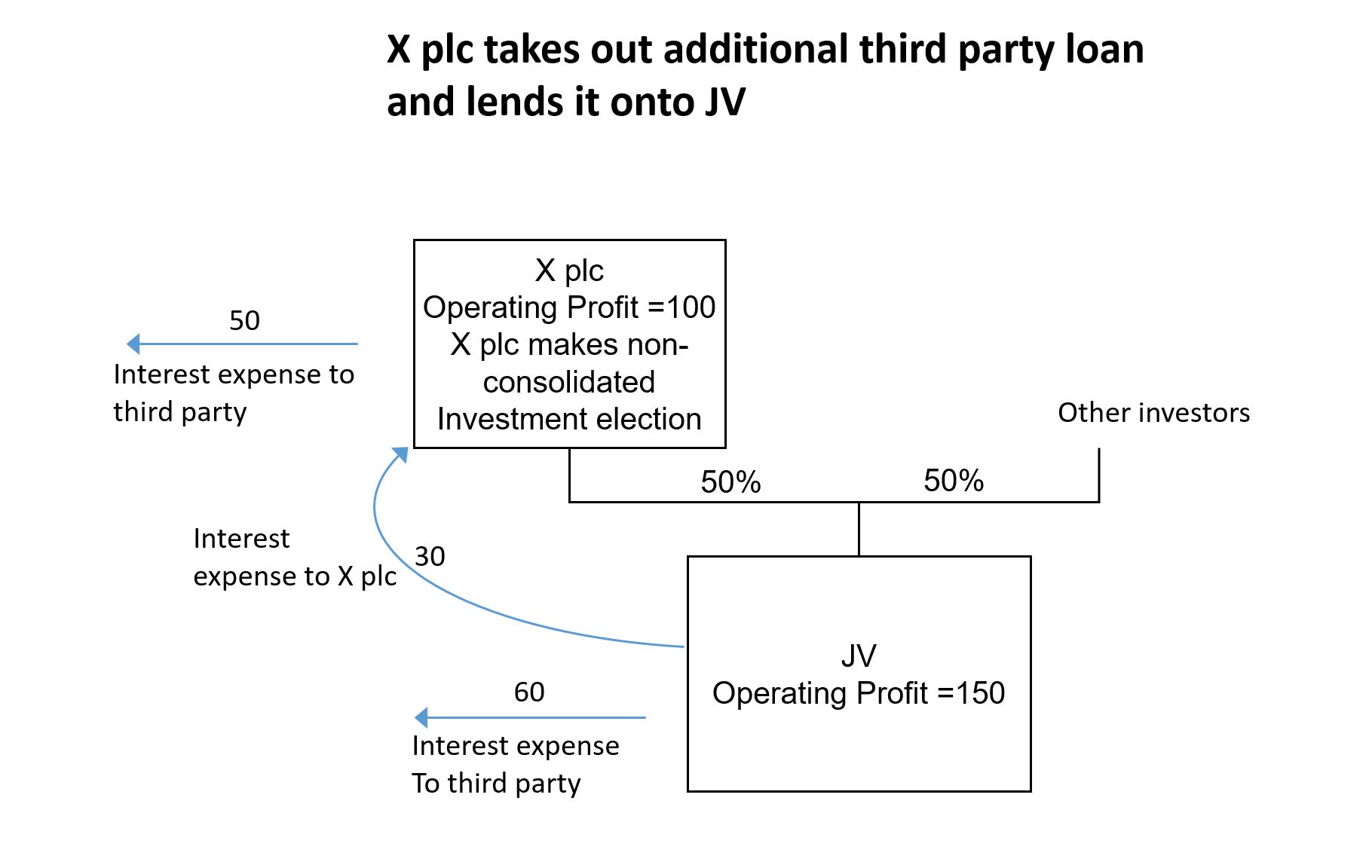

For visual illustration view diagram showing how X plc funds a joint venture using a third party loan

{kind=link}

The Diagram is showing X plc taking out an additional third‑party loan and lending it to a joint venture it owns 50% of, with interest flows between X plc, the joint venture and third‑party lenders.

Here the amounts are the same as the previous example at CFM96780, but X plc has taken out additional third party interest which it has on-lent to the JV.

In this situation TIOPA10/s427(3)(a) and TIOPA10/s428(5) apply to the loan from X plc to the JV. Therefore the election effectively ignores these amounts featuring in the financial statements of the principal worldwide group and the associated worldwide group. These amounts do not form part of adjusted net group-interest expense in either the principal worldwide group or the associated worldwide group.

The net effect of this is to ignore the 30 of adjusted net group-interest expense of the JV and to ignore the 30 of corresponding interest income in the calculation of adjusted net group-interest expense in X plc. This means that X plc has 80 of adjusted net group-interest expense and similarly for qualifying net group-interest expense because none of this is offset by any interest income from the JV.

| Accounts | X plc | JV | X plc group |

|---|---|---|---|

| Operating profit | 100 | 150 | 100 |

| 3rd party interest (expense) | - 80 | - 60 | - 80 |

| Related party interest (expense)/income | 30 | - 30 | 30 |

| Share of profits of JV | - | - | 30 |

| Profit before tax | 50 | 60 | 80 |

| Profit before tax ( ignoring loan) | - | 90 | - |

| Share of profits of JV (ignoring loan) | - | - | 45 |

- X plc group share of profits from JV - 50%

| Calculation of QNGIE | X plc Group |

|---|---|

| QNGIE in X plc | 80 |

| Share of JV QNGIE | 30 |

| Total QNGIE - (A) | 110 |

| Calculation of group - EBITDA | X plc Group |

|---|---|

| PBT of X plc group (pre-election) | 80 |

| Remove interest on loan to JV | - 30 |

| Remove share of JV's profits | - 30 |

| PBT of X plc group after adjustments | 20 |

| Addback NGIE (excluding loan to JV)) | 80 |

| Group-EBITDA of X plc group (before share of JV (before share of JV group-EBITDA) | 100 |

| Share of JV's group-EBITDA | 75 |

| Group-EBITDA - (B) | 175 |

- Group ratio - (A/B) - 63%

| Interest allocances | X plc |

|---|---|

| Tax-EBITDA | 100 |

| X plc group ratio | 63% |

| Interest allowance | 63 |

X plc has a net tax-interest expense of 50 (tax-interest expense of 80 less tax interest income of 30). All of its third party interest of 80 is qualifying net group-interest expense to use in its group ratio. The group interest income from JV is ignored for the purposes of TIOPA10/S427. It obtains a further qualifying net group-interest expense of 30 by its share in the third party interest of the JV. The group ratio is 63% and as there is an interest allowance of 63 there is no restriction of the net tax-interest expense in X plc.