CFM96810 - Interest restriction: joint ventures: interest allowance (non-consolidated investment) election: example 4: transparent JV

For visual illustration view diagram showing a transparent joint venture where profits and interest expenses flow through to investors

{kind=link}

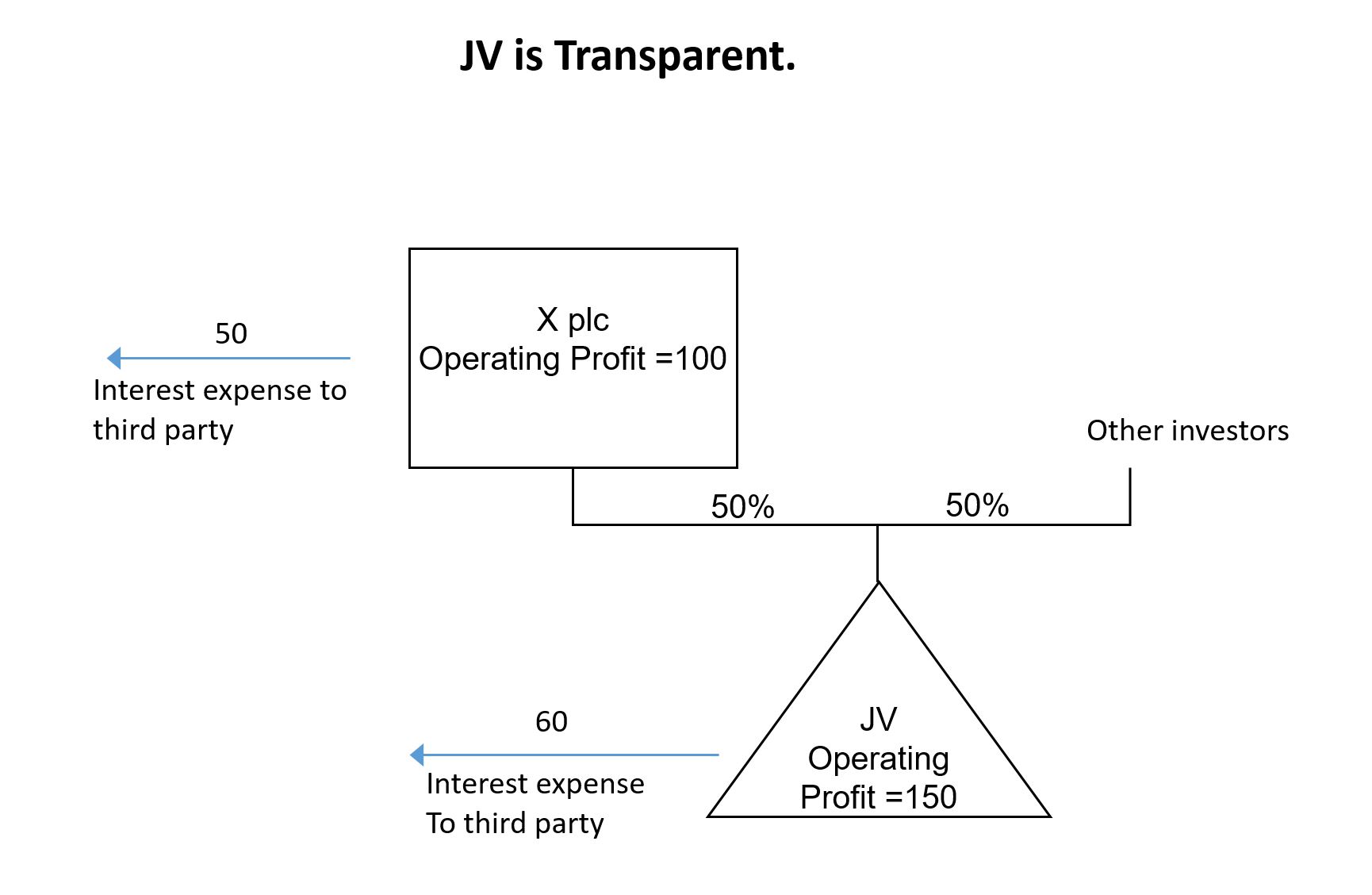

The diagram explains a transparent joint venture (JV). X plc has an operating profit of 100 and pays interest of 50 to a third party. X plc owns 50% of the JV alongside other investors. The JV has an operating profit of 150 and pays interest of 60 to a third party. Each investor is treated as receiving their share of the JV’s profit and expenses directly.

This has the same amount as the example in CFM96750 but in this case the JV is 'transparent' for tax purposes - for example it is a partnership. X plc makes an interest allowance (non-consolidated investment) election.

| Accounts | X plc | JV | X plc Group |

|---|---|---|---|

| Operating profit | 100 | 150 | 100 |

| 3rd party interest expense (QNGIE) | - 50 | - 60 | - 50 |

| Share of profits of JV | - | - | 45 |

| Profit before tax | 50 | 90 | 95 |

- X plc share of profits from JV - 50%

| Calculation of QNGIE | X plc |

|---|---|

| QNGIE in X plc | 50 |

| Share of JV QNGIE | 30 |

| Total QNGIE (A) | 80 |

| Calculation of group-EBITDA | X plc |

|---|---|

| Group-EBITDA of X plc group | 145 |

| Reduction in group-EBITDA from JV profits | - 45 |

| Share of JV's group-EBITDA | 75 |

| Group-EBITDA - (B) | 175 |

| Group ratio ( A/B) | 46% |

| Interest allowance | X plc |

|---|---|

| Tax-EBITDA of X plc (including its share of the JV's taxable profits before interest) | 175 |

| X plc group ratio | 46% |

| Interest allowance | 80 |

| Net tax-interest expense of X plc (including its share of the 60 interest expense of the transparent JV) | 80 |

| Less interest allowance | - 80 |

| Restriction | - |

The group ratio of X plc of 46% is the same as in example CFM96780. As the JV is transparent for tax purposes, X plc includes its share of the profits and net tax interest expense of JV in its tax figures. Therefore tax-EBITDA of X plc is 175 (100 + 50% of 150). The interest allowance is 80 which is equal to the net tax-interest expense in the X plc group so there is now no restriction.