Tax-Free Childcare Statistics Commentary September 2020

Published 18 November 2020

© Crown copyright 2020

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/statistics/tax-free-childcare-statistics-september-2020/tax-free-childcare-statistics-commentary-september-2020

1. About this release

This is a quarterly publication of Tax-Free Childcare statistics. Tax-Free Childcare provides help with childcare costs for working parents.

For every £8 a parent pays into their Tax-Free Childcare account the government will add an extra £2, up to a maximum of £2,000 per child per year.

For disabled children the maximum is £4,000 per year. For more information about Tax-Free Childcare see the summary information in Annex 1 or guidance on Tax-Free Childcare on GOV.UK.

2. Summary

The key points from this release covering the period to 30 September 2020 are:

- 227,000 families used Tax-Free Childcare for 263,000 children in September 2020, this compares with 115,000 families using childcare for 130,000 children in June 2020

- this increase in Tax-Free Childcare account use coincides with the reopening of childcare settings following the end of the spring 2020 COVID-19 lockdown

- the government spent £26.5m on top-up for families in September 2020, £14.9m more than in June 2020

Publication information

This is an official statistics publication. Statistical tables to accompany this commentary are available in the accompanying spreadsheet

Coverage: United Kingdom

Frequency of release: Quarterly

Next Release: February 2021

For queries or feedback on this publication, please contact:

- Eleanor Woodward eleanor.woodward@hmrc.gov.uk

For press queries, please contact:

- HMRC Press Office 03000 585018

3. Families and children using Tax-Free Childcare

The number of families and children using Tax-Free Childcare in the latest quarter has increased strongly following the COVID-19 lockdown.

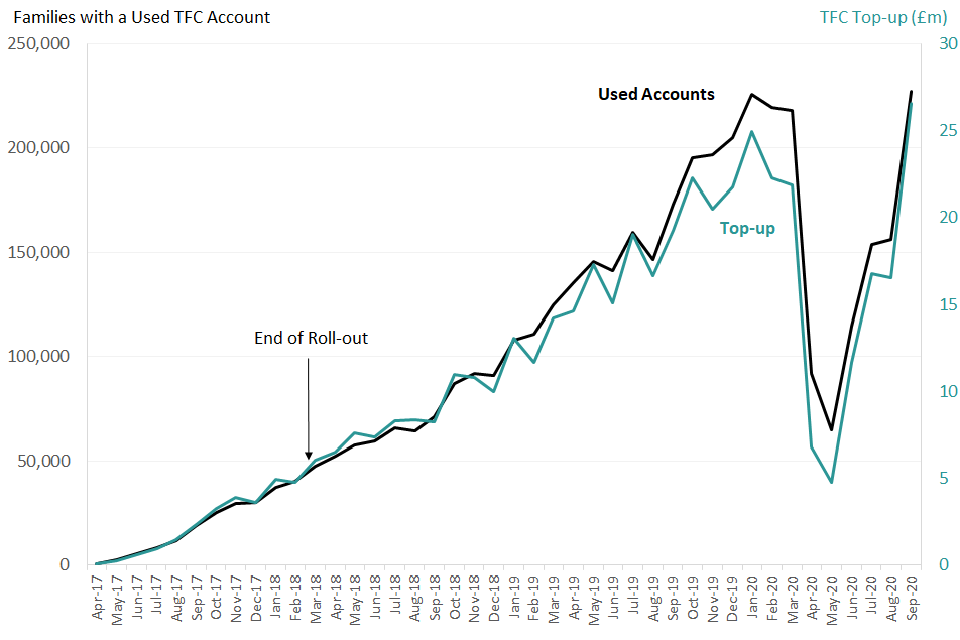

Figure 1: Families using TFC accounts and government top-up paid (£m), by month. The number of families using TFC accounts has increased strongly following the COVID-19 lockdown

fig-1

Figure 1 shows the number of families using TFC accounts each month, and total monthly government top-up. The key points to note from figure 1 are:

- the number of families using a Tax-Free Childcare account to make a payment to a childcare provider was on an increasing trend between the launch of the service and the start of the COVID-19 lockdown in March 2020

- the lockdown led to a sharp decline in Tax-Free Childcare account use in the quarter April-June 2020 following the closure of most childcare settings on 20 March (in response to the COVID-19 outbreak the government asked early years settings, schools and colleges to close to all children except those from priority groups: children of critical workers and those classified as vulnerable)

- account use in September has recovered to levels similar to those seen pre-lockdown

4. Self-employed Users of Tax-Free Childcare

Self-employed parents are eligible for Tax-Free Childcare but were not entitled to use childcare vouchers.

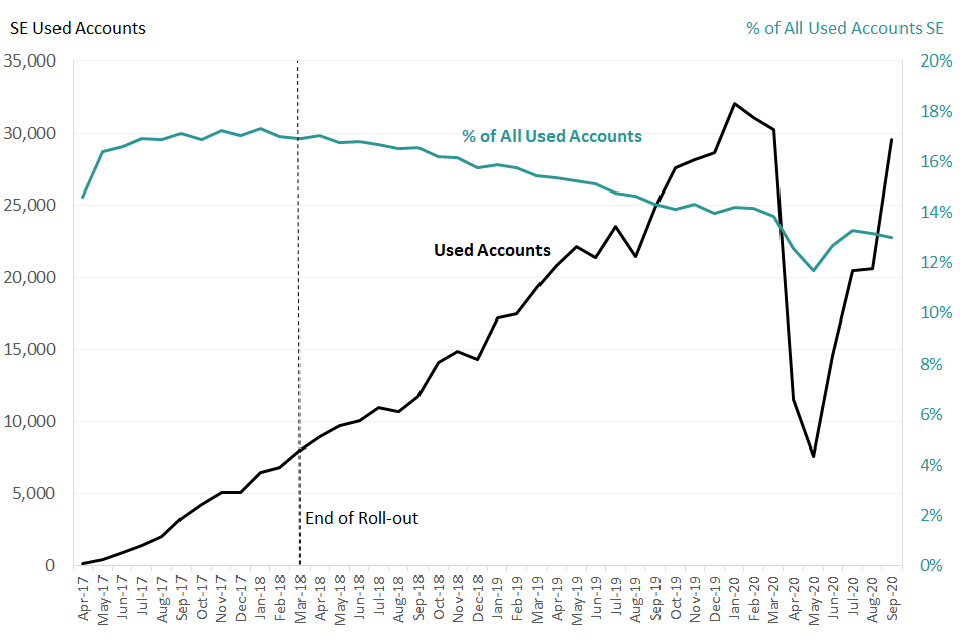

Figure 2: Families with a used Tax-Free Childcare account where at least one parent is Self-Employed, number and percentage of overall used accounts.

fig-2

Figure 2 shows the number of Tax-Free Childcare users in families with at least one self-employed parent. Key points to note are:

- the number of families with a self-employed parent using a Tax-Free Childcare account was on an increasing trend between April 2017 and February 2020

- in March 2020 there were 30,000 families with a self-employed parent using a Tax-Free Childcare account

- this fell steeply during the spring 2020 COVID-19 lockdown, to just 7,600 in May 2020, account use has recovered to close to pre-lockdown levels in September

- between March and May 2020, during the months of COVID-19 lockdown in the UK, there was a more pronounced decrease in the proportion of used accounts with a self-employed parent (75% decrease for families with a self-employed parent compared to 70% for all others)

- since May the percentage increase in account use by families with a self-employed parent has been greater than for families that don’t, although, because of the larger decrease during lockdown months, this leaves use by families with a self-employed parent down on levels seen before the COVID-19 lockdown

- there has been a slow declining trend in the proportion of used accounts with a self-employed parent since April 18, this could be due to early take up by this group compared to employed parents, who were more likely to have had access to childcare support before the scheme was rolled out

5. Disabled Children using Tax-Free Childcare

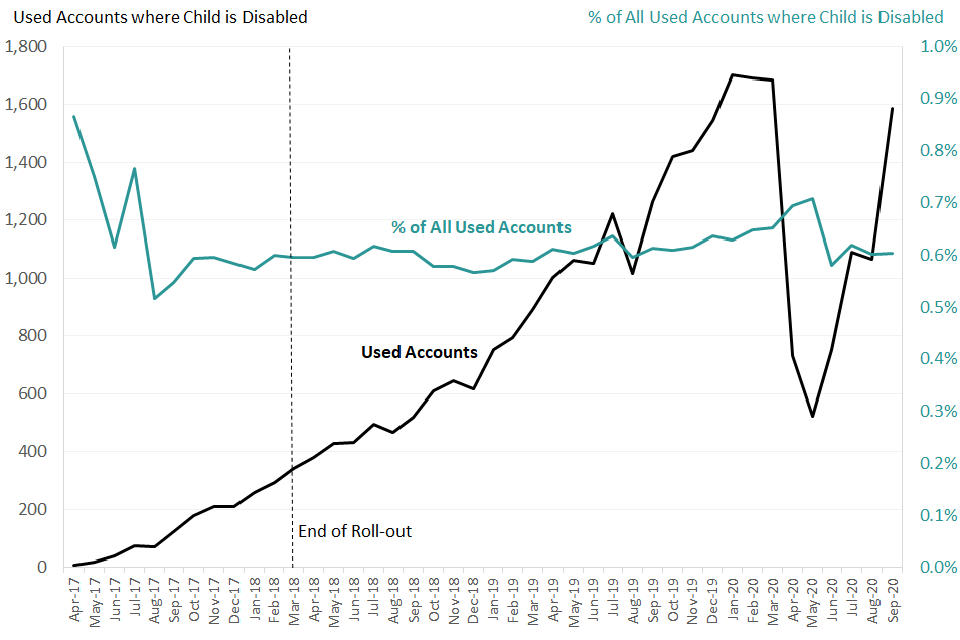

Disabled children are eligible for Tax-Free Childcare up to the age of 16 and can get up to a maximum of £4,000 top up per year. Families with a disabled child have been able to apply for Tax-Free Childcare since its launch in April 2017.

Figure 3: Disabled Children with a used TFC Account, Number and Percentage of Overall Children with Used Accounts.

fig-3

Figure 3 shows the number of disabled children with a used TFC account, and disabled children as a percentage of all children with used accounts. The key points to note from figure 3 are:

- the number of used Tax-Free Childcare accounts for disabled children was on an increasing trend until early 2020 but fell sharply during the COVID-19 lockdown in April and May

- account use has recovered to close to pre-lockdown levels in September

6. Account Use by Age of Child

There has been recovery in account use following the COVID-19 lockdown in all age groups, although this has been more pronounced for pre-school aged children, aged 3 and under.

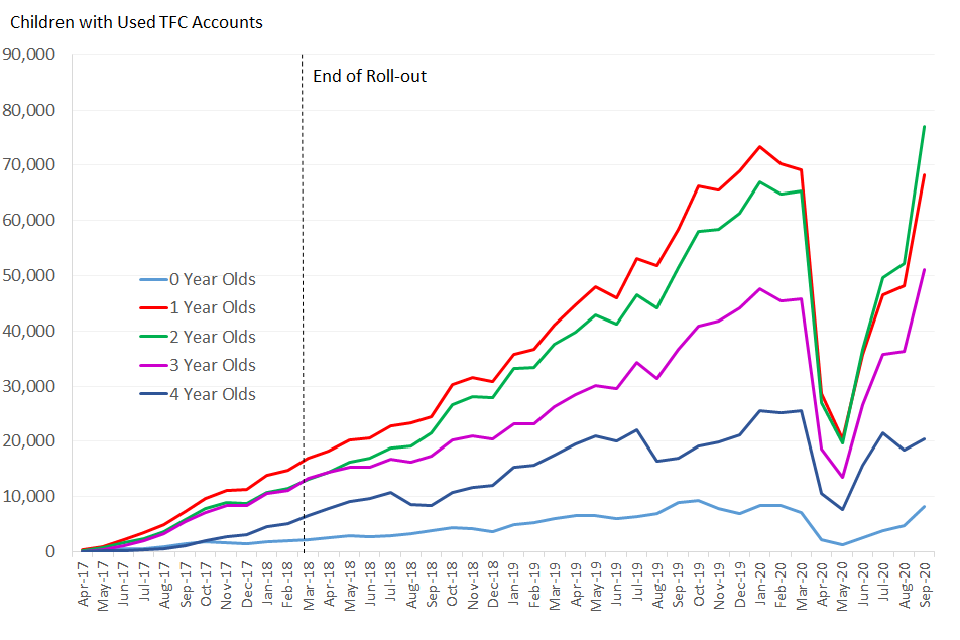

Figure 4: Children aged 0 to 4 using TFC accounts, by month and child age. There has been a recovery in account use following the COVID-19 lockdown.

fig-4

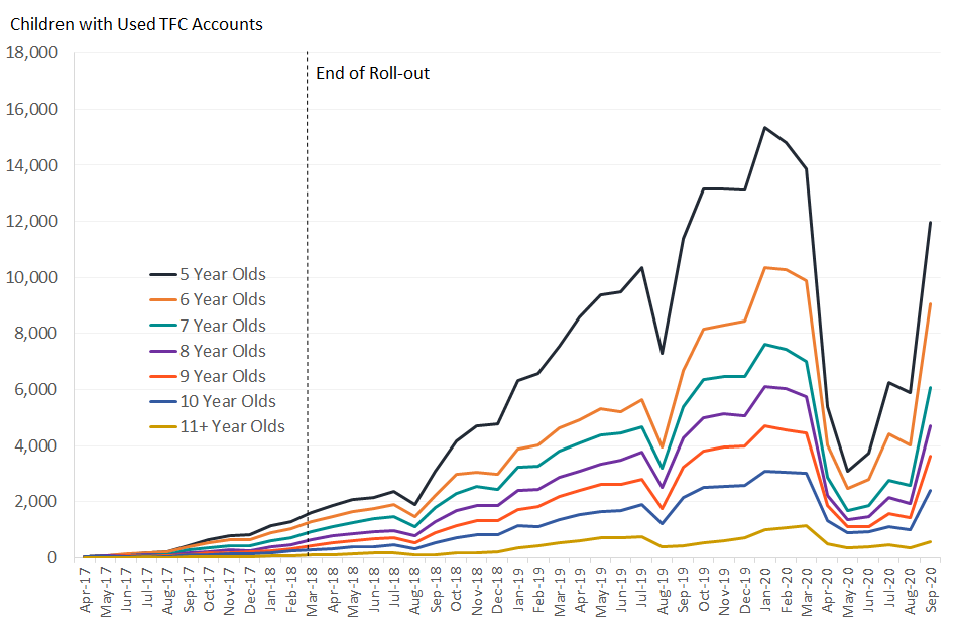

Figure 5: Children aged 5 to 16 using TFC accounts, by month and child age. Recovery in account use following the COVID-19 lockdown has not been as strong for school age children as for pre-school children.

fig-5

Figure 6: Quarter on quarter percentage change in TFC account use, split by children aged 0 to 3, 4 , and 5 and over. TFC use fell between March and June for all age groups and recovered between June and September. Children aged 0 to 3 TFC use in September was higher than in March, children aged 4 and over the number of used accounts in September remained below March levels.

| Period | age 0 to 3 | age 4 | age 5+ |

|---|---|---|---|

| Change in number of accounts used between March and June (%) | -46% | -39% | -73% |

| Change in number of accounts used between June and Sept (%) | 101% | 30% | 213% |

| Change in number of accounts used between March and Sept (%) | 9% | -20% | -15% |

Figure 4 shows the number of children aged 0 to 4 years using TFC accounts by month and child age, figure 5 shows the same for children aged 5 years and over. Figure 6 shows the quarterly percentage change in TFC account use since March 2020.

The key points to note from figures 4, 5 and 6 are:

- the impact of the COVID-19 lockdown was considerable for all age groups

- account use has recovered strongly between June and September for children in pre-school settings, age 0 to 3 years

- the increase in account use for 4 year olds is less strong in September, this may be because of the move of these children into school settings, and associated changes in childcare arrangements

- growth in account use in school age children was slower than for pre-school children in months to August, there has been a large increase for all ages 5 years and above in September, although use is still below levels seen pre-lockdown

- in general the number of children aged 5 and above with used Tax-Free Childcare accounts is substantially lower than those aged 0 to 4 years

- one likely factor is that children of school age generally have lower childcare costs and hence parents are less incentivised to take-up Tax-Free Childcare

- looking back most of the age groups aged 5 years and above show a dip in used accounts in both August 2018 and August 2019, this is likely due to a difference in childcare arrangements in school summer holidays

- there was a small decrease between July and August in 2020 but this is less pronounced due to the impact of the unwinding of lockdown

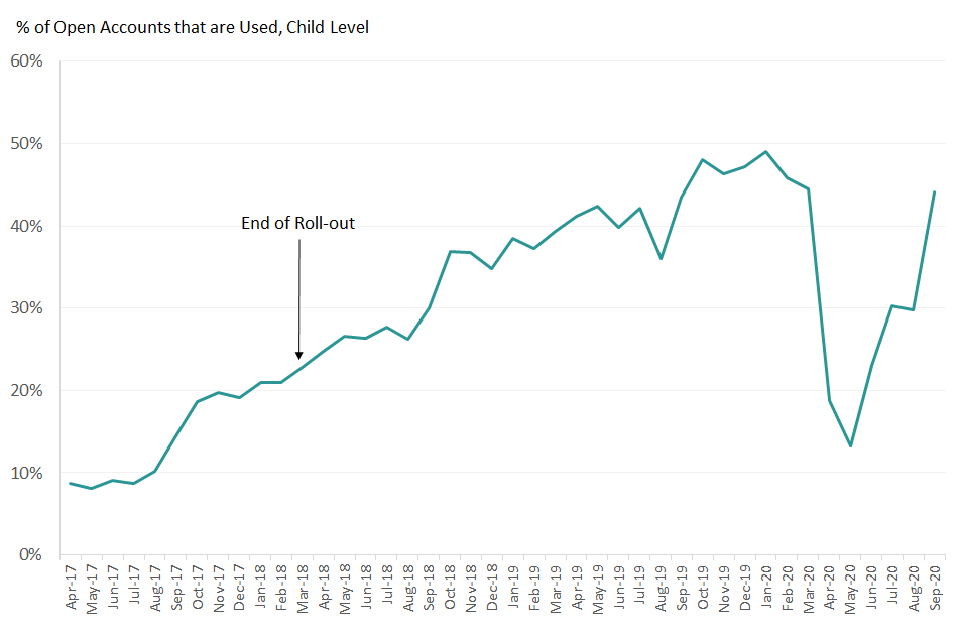

7. Percentage of Open Accounts which are used

Not all Tax-Free Childcare accounts that are opened are used. There are a number of reasons for this, including:

- some families will open an account for a child and then decide not to use it

- some families will open a TFC account for one child which they go on to use, and at the same time open accounts for other children in the family which are not used

- in applying for 30 hours free childcare, many families find that they are also eligible for Tax-Free Childcare and an account is opened for them, although they may not use the account at the time

Figure 7: Percentage of open accounts which are used, by month. There has been a recovery in the percentage of open Tax-Free Childcare Accounts that are used since the COVID-19 lockdown.

fig-6

Figure 7 shows the percentage of open accounts which are used each month. The key points to note from figure 7 are:

- the percentage of open accounts which are used was on a generally increasing trend until March 2020 but fell sharply in April 2020

- there was a significant decrease in account use during the COVID-19 lockdown but the decrease in open accounts was less pronounced leading to a fall in the percentage of open accounts that were used, dropping from 44.5% in March 2020 to 13.2% in May 2020

- during the latest quarter as account use has increased so too has the percentage of open accounts that are used, up to 44.1% in September 2020

Annex 1 – Background to Tax-Free Childcare

Tax-Free Childcare was launched to the public in April 2017 with a phased roll out by age of the youngest child in a family, completed in February 2018. The full roll-out schedule is shown below.

Comparisons should not be made between months before March 2018, when roll-out was complete, and more recent months. Since roll-out was phased by age of the youngest child in a family, older children appearing in the tables may have joined Tax-Free Childcare before their apparent roll-out date.

Children must be aged 11 or under, or 16 and under if they have a disability, to be eligible for Tax-Free Childcare. Families with a disabled child up to the age of 16 were able to sign up for Tax-Free Childcare in April 2017.

Tax-Free Childcare Roll-out Dates by Age of youngest Child

| Age | Date eligible |

|---|---|

| 0 to 3 years | 21 April 2017 |

| 4 years | June 2017 |

| 5 years | 24 November 2017 |

| 6 to 8 years | 15 January 2018 |

| 9 to 11 years | 14 February 2018 |

Families with a Tax-Free Childcare account receive 20% top up on childcare costs up to a total of £2,000 per year per child (£4,000 for a disabled child).

Tax-Free Childcare is run by HMRC with their delivery partners National Savings & Investments. Accounts are fully online for the large majority of users. Parents pay into and make payments to childcare providers out of the same account. Parents are able to withdraw money for other purposes, but lose the government top-up on anything removed.

An individual family may register for a Tax-Free Childcare account for multiple children. Separated or Divorced parents cannot register an account separately for the same child.

In order to qualify for Tax-Free Childcare families must have all adults earning the equivalent of at least the national minimum or living wage for 16 hours per week, with income below £100,000 a year. They must not be claiming tax credits or universal credit in any form or other disqualifying benefits such as Job Seeker’s Allowance.

Since September 2017, families in England have also been able to use the government’s offer of 30 hours free weekly childcare for children aged 3 or 4. Families can access this offer provided all parents are earning at least the equivalent of the national minimum or living wage for 16 hours a week, and don’t have a taxable income over £100,000 annually.

Unlike Tax-Free Childcare, families are eligible for 30 free hours if they receive tax credits or universal credit or childcare vouchers. Applications for the 2 offers are linked and accessed through the same online portal on GOV.UK.

When a family applies for 30 hours free childcare and also meets the additional eligibility criteria for Tax-Free Childcare, a Tax-Free Childcare account is automatically opened, and vice versa. This leads to a discrepancy between ‘open’ and ‘used’ Tax-Free Childcare accounts which can be seen in the tables accompanying this publication.

Tax-Free Childcare is replacing the childcare voucher and directly contracted childcare schemes, which closed to new entrants in October 2018. Tax-Free Childcare is available to families where one or more parents are self-employed. This is different to the employer supported childcare schemes, which are only available from some employers.

With childcare vouchers, a basic rate taxpayer can salary sacrifice up to £55 per week, with a maximum benefit of £933 per year per parent, whilst a higher rate payer can get up to £28 a week in vouchers.

Whether a family is better off under Tax-Free Childcare or childcare vouchers will depend on their circumstances.

Following the closure of childcare vouchers, parents who change employer and new parents will no longer be able to receive childcare vouchers but may be eligible for Tax-Free Childcare. This should lead to an increase in take up of Tax-Free Childcare in the longer term, as these families look for childcare support.

Whether a family can access Tax-Free Childcare may also depend on their preferred childcare provider. Childcare providers need to be signed up to Tax-Free Childcare before a family can make payments to them.

Annex 2 – Glossary and Methodological Notes

Open account

An open Tax-Free Childcare account is one where a family has met the eligibility criteria and is within their eligibility period according to data held by HMRC on their administrative systems.

The eligibility period is the period where families receive top-up on any payments made through their account and usually lasts around 3 months. At the end of this period families are required to reconfirm their eligibility, and the period starts anew.

For the purposes of these statistics monthly open account figures in table 1 are calculated as the number of families with an open account on the last day of each calendar month. A similar calculation is done for table 2 but counting the number of children.

Annual open account figures in tables 1 and 2 are calculated as the numbers with an open account on the last day of any of the 12 months April to March.

Using this measure, families or children are likely to have open accounts in multiple months but will only be counted once in the annual figures. This means that the annual number of open accounts will not equal the sum of the 12 months in the year.

Used account

A used account is one where a payment is made from the account to a childcare provider within the month or year according to transactions data provided to HMRC by National Savings and Investments.

For table 1 this is calculated as the number of families making a payment in the period. For table 2 it is calculated as the number of children whose parents make a payment to a childcare provider on the child’s behalf.

Because families or children have used accounts in multiple months this means that the annual number of used accounts will not equal the sum of the 12 months in the year.

Identifying a child and a family

Families who register for Tax-Free Childcare are assigned a unique claim identifier within HMRC’s internal data. Children whose parents register are also given a unique identifier. It is therefore possible to link data across multiple children where they belong to the same family.

The relationship between Tax-Free Childcare and 30 hours free childcare

In September 2017 the government launched its offer of 30 free hours of childcare in England for children aged 3 and 4 (although parents were able to apply for and therefore open a 30 hours account from April 2017).

Parents apply and have their eligibility checked for 30 hours free childcare via the childcare service, the online application for Tax-Free Childcare and 30 hours free childcare. If a parent is found to be eligible, they will be given a 30 hours eligibility code.

A parent should take this code along with their national insurance number and their child’s date of birth to their chosen childcare provider. The provider will either directly, or via their local authority, use the Department for Education’s Eligibility Checking System (ECS) to confirm the validity of the code.

Once the 30 hours eligibility code has been validated via the ECS, the child will be able to take up their 30 hours place.

In applying for 30 hours free childcare, many families find that they are also eligible for Tax-Free Childcare and a Tax-Free Childcare account is also opened for them. This contributes to the discrepancy between open and used Tax-Free Childcare accounts that is seen in the data in the tables accompanying this release.

For this reason, used accounts are considered as the best measure of take up of Tax-Free Childcare.

How the figures for 30 hours free childcare in this publication differ from other sources

Department for Education publish their own data on the numbers of children benefiting from funded early education, including those in a 30 hours place. Statistics about education provision for children under 5 years of age are published by DfE on GOV.UK

Because Tax-Free Childcare statistics only publishes numbers of open 30 hours free childcare accounts where they also have an open Tax-Free Childcare account, this publication should not be used as the lead source for 30 hours free childcare data.

Additionally, HMRC’s 30 hours data only shows where an account has been opened, and is within its eligibility period and not all of these families will necessarily be making use of the 30 hours offer.

This is because the Tax-Free Childcare system allows parents to renew eligibility for a 30 hours account until the start of the term following the child’s 5th birthday - to ensure children who defer school entry are able to access 30 hours free childcare.

In some cases, this may mean that the child retains an open 30 hours account in HMRC’s data, even though they have started school and will therefore be unable to use the 30 hours offer.

Government top up and how is it calculated

Families who are signed up to Tax-Free Childcare and then make a payment to a registered childcare provider receive a top up of 20% and are able to receive up to £2000 per child per year (£4000 for a disabled child).

The monthly and annual top up amounts are the total top up that the government has spent in this period. Annual totals are equal to the 12 months in the year. The monthly totals also include some backdated payments to families who did not initially receive their expected top-up.

Self-employed status

Self-employed parents were not eligible for childcare vouchers but are eligible for Tax-Free Childcare. Families with a self-employed parent are defined according to a flag that exists on HMRC’s Tax-Free Childcare administrative data. This is based on details provided by parents during their application, including their unique taxpayer reference (UTR).

For monthly data, the latest record on a parent’s self-employed status is looked at the end of each calendar month. For annual data, the monthly data sets are combined so that the annual number of families with a self-employed parent and open or used account, are any families with a self-employed parent and open or used account in any of the months in the year.

This method reflects the fact that parents may change whether they are self-employed throughout the year.

Disability flag

Children with a disability are defined according to a flag that exists on HMRC’s Tax-Free Childcare administrative data. HMRC has access to Department for Work and Pensions records to confirm where disability living allowance (DLA) or personal independence payments (PIP) are received for a child, or a child has a Certificate of Visual Impairment (CVI).

For monthly data, the latest record on a child’s disabled status is looked at the end of each calendar month. For annual data, the monthly data sets are combined so that the annual number of disabled children with an open or used account, are those with an open or used account at any month in the year.

Geographical allocation

In order to allocate a family to a region parents details are linked to the postcode held on the HMRC central repository of address information. This data receives information from other HMRC tax and benefit administrative systems and from Department for Work and Pensions.

For annual data presented in table 6, a family’s latest available address record within the 12 month period is used. The sum of all regions in the tables may not equal the United Kingdom total because it has not been possible to allocate all families or children to a region. Families or children not allocated to a region are still counted within the United Kingdom total.

Calculating children’s ages

Children’s ages are calculated using the child’s date of birth which HMRC holds on its administrative Tax-Free Childcare data. Ages are calculated on the last day of each calendar month, so where a child has a birthday in a particular month, they will be assigned to the older age category.

Revisions

Figures will be revised only if an error is discovered. No changes have been made this quarter.