Section 3 - Off-payroll and Disguised Remuneration

Published 23 April 2020

© Crown copyright 2020

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/independent-loan-charge-review-summary-of-evidence/section-3-off-payroll-and-disguised-remuneration

Off-payroll and DR

The off-payroll working rules, sometimes known as ‘IR35’, can apply if a worker provides their services through an intermediary and have been in place since 2000. An intermediary will usually be the worker’s own personal service company (PSC), but it could also be a partnership, a managed service company, or an individual.

The rules make sure that workers, who would have been an employee if they were providing their services directly to the client, pay broadly the same Income Tax and National Insurance contributions (NICs) as employees. The rules do not apply to the self-employed.

Broadly, for each engagement the worker enters into the PSC should make an employment status determination to see if the off-payroll working rules apply. If they do, the PSC should calculate a ‘deemed employment payment’. This is the amount deemed to be the income of the worker, after some deductions and employer NICs have been removed. The PSC should then pay the Income Tax and Class 1 NICs to HMRC.

Non-compliance with the off-payroll working rules is widespread. We estimate around 90% of PSCs in scope of the rules do not comply with them, costing the Exchequer around £700 million in 2016 to 2017.

In April 2017, the government reformed the rules so that public sector organisations who take on contractors are responsible for making sure they and their workers pay the right tax. At Budget 2018, the government announced its intention to bring the operation of the rules for medium and large organisations outside the public sector in line with the public sector. The reform to the off-payroll working rules will raise almost £3bn to 2024.

Following the introduction of IR35 in 2000, contractors were required to pay employment taxes and argue they were pushed into using DR schemes to ensure they continued not to pay employment taxes. We recognise that some schemes were sold as being ‘IR35 compliant’, which may have been attractive to some individuals. DR schemes ensure that the off-payroll working rules do not apply because individuals become employees of the company set up for the purposes of the scheme, and there is no doubt about their employment status.

However, the government is clear that there are no policy, or legislative, links between the 2 measures. Individuals working through their own PSC were able to comply with the off-payroll working rules without entering into contrived avoidance. Seeking to avoid complying with tax obligations is not an excuse for entering into a contrived tax avoidance scheme.

Public sector engagers

We are not aware of any public sector organisations actively promoting the use of DR tax avoidance schemes to their employees or contractors.

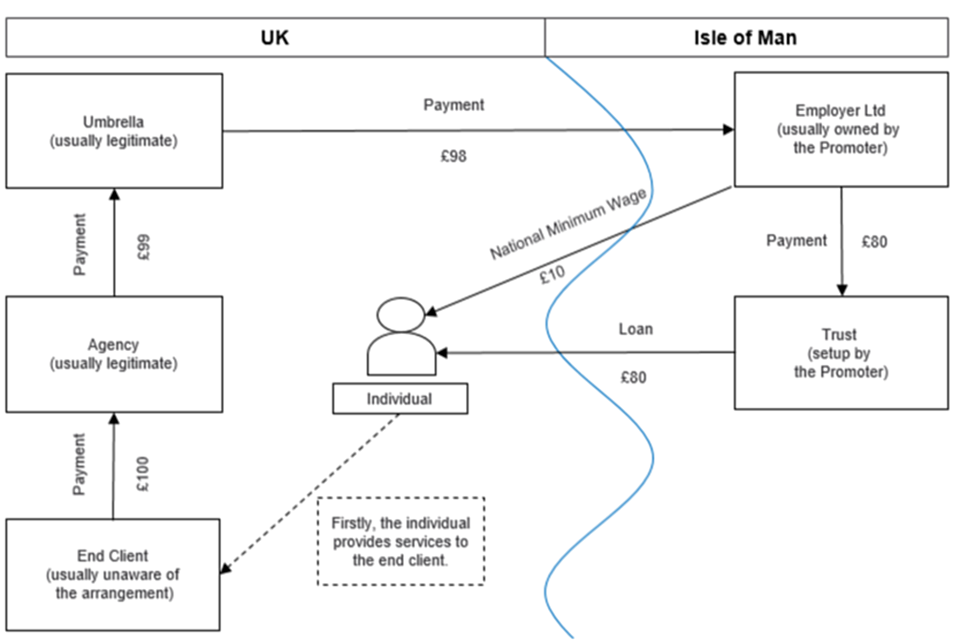

A common DR scheme used by individuals before 2011 looked like below:

Image showing a common DR scheme.

The end client will require a service and will approach a recruitment agency, which range from high street names to boutique firms specialising in particular industries. The agency will know an individual who can provide that particular services or will identify them.

The agency will not employ individuals so will ask them to find an umbrella company. The individual then has a choice about the umbrella company, some of which offered DR schemes.

The individual provides their services to the end client via their offshore employer and one or more intermediaries on shore. Each party, beginning with the offshore employer, invoices the next party for the services provided by the individual. The end client will pay the recruitment agency, and each party takes their small fee until the offshore employer operates the DR scheme.

Some schemes required strict confidentiality clauses which stipulated that the individual must not tell their end client that monies would ultimately be routed offshore. Therefore, it is common for the end client to be unaware of what is happening further down the supply chain as they are contracting with a reputable firm. This applies equally to private and public sectors.

The iCA database does not contain information about end clients. However, in one particular scheme we undertook an exercise to look at the end clients. We identified several public sector bodies who, along with the recruitment agency, were unaware that there was an avoidance scheme or an offshore employer.

Any individuals providing their services to the public sector identified in the course of our compliance work would be investigated in the same way as someone working for a private sector client.

HMRC has worked with some public sector organisations and other professional bodies to increase awareness of DR schemes. This includes engagement with NHS, the General Medical Council and the General Dental Council, and others. We have also placed articles in various publication, including in the Nursing Times, about DR schemes and the loan charge.

Go to section 4: Policy costing.