Grants Continuous Improvement Assessment Framework V2

Updated 27 July 2026

© Crown copyright 2026

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/government-functional-standard-govs-015-grants/grants-continuous-improvement-assessment-framework-v11

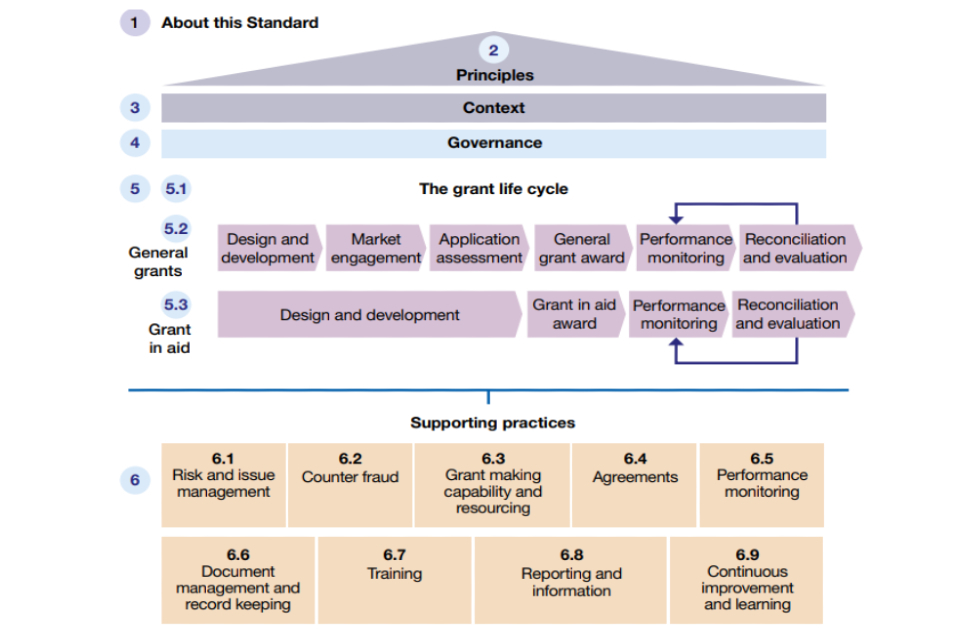

Figure 1: The structure and scope of the functional standard - Government Functional Standard GovS 015: Grants (PDF, 341KB)

1. Purpose, scope and structure of the assessment framework

1.1 Purpose of this continuous improvement assessment framework

This grants continuous improvement assessment framework (“the framework”), is designed to help drive continuous improvement within and across government grant making organisations, by helping them to assess their compliance with, and practical application of, key requirements in the Government Functional Standard GovS 015: Grants (PDF, 341KB).

The framework is consistent with assessment frameworks for other government functions, ensuring that senior leaders can take a consistent and coherent view of compliance with standards, across all functions in their organisation.

The framework should be read in conjunction with the Functional Standard and supporting Minimum Requirements. It is designed for people undertaking an assessment of their organisation’s grant making policies and processes for the design, development and administration of government general grants, together with an assessment of the efficacy of the core functional structure. The assessment is designed to assist people in identifying and implementing organisational improvement actions, as a result of the findings from each completed assessment.

The framework is split into two parts (see section 1.3). The core assessment provides for the assessment of Developing, Good, Better and Best ratings against key criteria, designed to assess compliance within the core function - this is undertaken by departments, via a self-assessment. The second part is a scheme level assessment, undertaken by auditors, providing an assessment of scheme delivery, assessed as Unsatisfactory, Limited, Moderate and Substantial, against key criteria.

For more information on continuous improvement and government functional standards, see the Guide to continuous improvement against functional standards.

1.2 Scope of this Continuous Improvement Assessment Framework

The framework applies to the planning, delivery and management of Exchequer funded government grants activity in all central departments and arm’s length bodies, for general grants. Other public sector organisations that administer government grant funding, such as devolved or local government, might find this document useful and may consider taking account of the guidance within.

The framework will be reviewed regularly by the Cabinet Office and partner organisations across the public sector, to reflect feedback and emerging trends. Any changes made will be communicated to participating organisations.

The structure and scope of the functional standard and the framework is shown in Figure 1.

1.3 The structure of the Grants Continuous Improvement Assessment Framework

The framework is split into 2 parts:

- A Self-Assessment of the overarching core criteria for a Grants Function:

- The core criteria have been collated and written based on the Government Functional Standard GovS015: Grants, the Government Grants Management Function (GGMF) Functional Blueprint, the Minimum Requirements and the Control Framework.

- Validation of the self-assessment will be completed by either GIAA or internal/external auditors.

- A Government Internal Audit Agency (GIAA) assessment of grant scheme criteria:

- The Scheme Criteria have been collated and written based on the Government Functional Standard GovS015: Grants and Minimum Requirements.

This document provides guidance on what is required for the self-assessment of the core criteria and what is required for the GIAA/auditor assessment of the grant scheme criteria, separately.

Note: The scheme level assessment may be undertaken by internal audit teams or external auditors.

2. Using this assessment framework

2.1 How the framework relates to the Functional Standard

The framework supports compliance with the Functional Standard and minimum requirements for general grants, and related products such as the Functional Blueprint. It includes criteria to test different levels of organisational capability against key aspects of those products.

The framework is focused on how the requirements of the Functional Standard can be implemented proportionately, in organisations with different levels of maturity, so that leaders can plan improvement initiatives where needed.

The criteria for the framework are based on statements drawn from the Functional Standard and other core documents. A rating of Good means that all mandatory elements, and most of the important advisory elements, are being met by the core function in an organisation - this is the minimum expectation within the grants function.

2.2 Assessing an organisation

Before starting an assessment, the boundaries of the organisation being assessed need to be defined. A whole department or arm’s length body can be covered, or the assessment can be limited to a defined part, considering the size of grants function and the number of schemes delivered by the ALB, where applicable. Be careful when defining the boundaries in terms of specific business areas, as the perceived remit of the associated management team might be too narrow for the assessment criteria to make sense. On the other hand, dividing a large organisation, where performance across the organisation varies, into its major groups can help pin-point where improvements are needed.

When considering whether a criterion is being met, we would expect organisations to consider whether or not their policies and processes are meeting the criterion, but also whether those same policies and processes are being complied with consistently across the organisation.

For example, for the criterion, “The organisation has embedded due diligence processes across its grants portfolio, ensuring potential risks and issues are identified, evaluated and mitigated as required”, we would expect organisations to consider whether there is both an internal policy to communicate this requirement to grants practitioners, but also whether there is documentary evidence of sufficient quality, for example, through sampling, that this specific policy is being complied with. Links to the evidence tables are provided on page 8.

The assessment should include narrative information, supporting each rating, on how the function meets each of the core and scheme criteria. Departments should guard against optimism bias in arriving at each rating, through ensuring that the assessment is supported by relevant evidence.

An example of the type of documentary evidence required is provided below. When assessing Theme 2: Governance and Management, Criteria 2.6, departments could, for example, provide the following documentation to support an assessment of ‘Good’ performance:

- Copies of communication plans:

- Effective communication plans would detail timelines and methods of expected communications with internal and external stakeholders to ensure they can carry out their role effectively.

- Documentation confirming regular reviews of the plans; this could be minutes of meetings or a documented process for reviews.

The assessor should secure assurance that the above documents are easily accessible and retained for future reference.

Full details of evidence requirements are available below:

Candidness is key: The framework is a tool to support organisational improvement, and the assessment will add no value unless there is honesty in response to the criteria.

Business leaders should set ambitions for their organisation based on business needs, as set out in their strategies and/ or plans. When it comes to the core criteria, for some organisations, Good might be good enough. For other organisations, their area of business might dictate that meeting Best is necessary.

Levels are cumulative: An organisation needs to meet all the criteria of each level in order to comply with the next level. For example, when assessing against the core criteria, an organisation cannot be Better if it doesn’t meet all the criteria for Good - even if it meets all criteria at the Better level. When being assessed against the scheme criteria, organisations with Gold schemes, must also meet the criteria for Bronze and Silver schemes.

Functional Standards cross-reference to other functional standards (with cross-references listed in clause 1.3 of each of the standards). This interdependence means that for an organisation to be operating effectively, officials need to consider such dependencies carefully, including their impact on the organisation’s operations. For example, grant delivery in the public sector often relies heavily on recipients undertaking a significant amount of funded activities. Where this is the case, an organisation could not consider itself fully capable in grant delivery without an appropriate level of capability in counter-fraud work, to ensure public funding is protected and used as intended.

Further guidance on assessment frameworks can be found in the Guide to continuous improvement against functional standards.

2.3 Using the output of an assessment

Completed assessments can be used to help identify and share good practice, address perceived weaknesses in the performance of the organisation and to inform continuous improvement activity.

The completed assessment informs internal management policy and processes and is designed to facilitate frank and open discussion on performance. Completed assessments are not intended for publication. Organisations should incorporate areas for improvement identified by the assessment, within their grants continuous improvement action plan, to help manage specific areas for development.

There is a system in place within the GGMF to monitor each organisation’s improvement plan on a periodic basis (currently quarterly), to ensure actions are targeted and progress is being made. A range of engagements, interventions and communications activity takes place to support the sharing of best practice.

- Assessment is a cyclical process: Organisations assess their maturity against the applicable core themes and scheme minimum requirements within the improvement framework. Central government departments then define improvement plans to target specific areas for development and participate in good practice sharing across the network. Improvement activities should have defined owners with a timescale given for completion. Each organisation should have a system in place to monitor the improvement plan to assess progress, understand challenges and identify and implement additional actions, based on activity and evidence.

- The framework is intended to form part of a wider culture of continuous improvement: The assessment data is used (where data has been authorised for sharing with Cabinet Office) to identify leading practices across the network and areas of common challenge across the public sector.

- Gathering evidence: The team conducting the assessment may be reliant on engagement with, or direct provision of, information from the wider business. Early engagement with the business can help to obtain information and evidence may be sourced through proportionate sampling of the relevant organisational processes.

3. Structure and characteristics of the self-assessment on core criteria

3.1 The structure of the core self-assessment framework

The structure of the core self-assessment is designed to give an indicative picture of how well an organisation’s core grant function is performing. The model is organised under the following headings and structure:

- Themes: The themes represent the overall topic being assessed.

- Criteria: Individual statements or requirements which must be met, these aggregate to provide overall ratings under Good, Better and Best.

Theme: A theme is the overall topic being assessed in that section of the framework. The context and more information about the themes addressed can be found in the grants Functional Standard.

Assessment criteria: Criteria help to define what is happening in an organisation (observable in practice, backed up by documentary evidence). The Criteria denote the requirements of Good, Better or Best performance and are taken directly from the requirements of the Government Functional Standard GovS 015: Grants (PDF, 341KB), the Government Grants Management Function (GGMF) Functional Blueprint, the Minimum Requirements and the Control Framework.

For example, the required content of a governance and management framework is described in the Governance section of the Standard.

The assessment is completed via the GCIAF Digital Tool, which provides organisations with the functionality to upload the required documents to evidence how they meet each criterion.

A link to the GCIAF Digital Tool is available on the Grants Centre of Excellence.

Details of the evidence required for completion of the self-assessment is available here: Core Criteria evidence tables

Important note: The use of the comply or explain principle.

The intention for the core criteria, for self-assessment at the good, better and best levels, is that they are achievable by all government grant making organisations, which will mean that an evidenced rating can be provided, by all organisations against all criteria. However, we recognise that there may be exceptional circumstances, specific to an organisation, that we are not aware of, which prevent an organisation from meeting one or more of the criteria within the assessment. Because the self-assessment does not include an option to mark any individual criterion as not applicable, it is necessary to allow the use of the comply or explain principle, to ensure that no organisation is unfairly prevented from achieving any of the three levels under their self-assessment. This may be due to circumstances beyond their control, or that were not evident in the design of the assessment framework, which prevent them from meeting one or more of the criteria. Therefore, if these exceptional circumstances arise, an organisation is permitted to mark an individual criterion as met, where a rationale is provided that clearly explains why the organisation is not able to meet the criterion either partly or in full. For example, there could be a statutory reason which prevents compliance, or some other insurmountable barrier or explanation specific to the organisation. The comply or explain principle cannot be used, for example, where an organisation has chosen not to meet one or more of the criteria, but would otherwise be able to meet the criteria, and wishes to rate the organisation as best.

Organisations planning to use comply or explain, must complete a template with details and submit to the GGMF for agreement. All submissions will be reviewed by the GGMF to ensure that the rationale provided is reasonable in the context of the organisation and the evidence provided. Once reviewed, the GGMF will confirm with the organisation, how the criterion should be scored.

The template is available here: Core Criteria Comply or Explain Template

3.2 Characteristics of developing, good, better and best for Grants - Core Self-Assessment

Developing: By default, an organisation is assessed as developing if it doesn’t meet all of the criteria under the good category. The criteria at the good level represent the minimum expectations of the Functional Standard, linked to the core function. For this reason, the framework does not include criteria for developing. Where an organisation is assessed as developing, that would indicate that there are one or more areas for improvement and a robust improvement plan should be put in place and closely monitored, to address identified challenges.

The tables below set out the expectations and broad descriptions of Good, Better and Best for each core assessment theme. These core criteria rating categories are used to assess the maturity of the core grant function’s policies and processes in government grant making organisations against the requirements of the Functional Standard and associated minimum requirements for general grants.

Note: Good includes the mandatory requirements (‘shall’ statements) from the functional standard and the most important advisory elements - these are also summarised under each minimum requirement guidance document.

| Theme | Score | Description |

|---|---|---|

| Theme 1: Vision and Strategy | Good: Strategy and Continuous Improvement | Focus is on the core function’s key strategies and plans to continuously improve |

| Theme 1: Vision and Strategy | Better: Forward Planning and Networking | Focus is on embedding future strategy whilst monitoring and testing compliance and improvement. The organisation actively networks across government. |

| Theme 1: Vision and Strategy | Best: Cross-Government Development | Focus is on wider, cross government sharing of best practice and expertise to develop grant-making strategy, policy and practices. |

| Theme 2: Governance and Management | Good: Framework, Accountabilities and Communication | Focus is on the accountabilities of those in key grant roles for delivering requirements of the governance and management framework and communication planning. |

| Theme 2: Governance and Management | Better: Pipeline Challenge and Cross Functional Communication | Focus is on organisations interrogating their grants pipeline, ensuring compliance with policy objectives and widening communications for cross-functional collaboration. |

| Theme 2: Governance and Management | Best: Cross-Government Collaboration | Focus is on senior grant-makers using their expertise to provide support across government, enabling the effective development of new schemes. |

| Theme 3: Data, Digital and Reporting | Good: Compliance and Foundational Reporting | Focus is on meeting mandatory requirements for data capture (GGIS fields) and providing standard, typically descriptive, financial and delivery reports. Data is primarily captured and stored. |

| Theme 3: Data, Digital and Reporting | Better: Forward-Looking Data Usage | Shift to using data to inform decisions and improve future outcomes. Data is drawn from historic schemes and evaluations to inform new scheme design. The organisation actively prioritises data quality. |

| Theme 3: Data, Digital and Reporting | Best: Intelligence and Governance | Focus is on achieving full technical integration, predictive capability and data accountability. |

| Theme 4: Risk and Assurance | Good: Risk and Assurance Management | Focus is on embedding clear risk and assurance practices. |

| Theme 4: Risk and Assurance | Better: Assurance Planning and Monitoring | Focus is on the planning of assurance activities and assurance monitoring. |

| Theme 4: Risk and Assurance | Best: Risk and Assurance Testing | Focus is on testing to ensure the effectiveness of the organisation’s assurance and risk practices. |

| Theme 5: Capability and Resourcing | Good: Capability and Resource Planning | Focus is on resource and capability planning, whilst ensuring completion of basic grants training. |

| Theme 5: Capability and Resourcing | Better: Capability Development and Expert Support | Focus is on the widening and developing grants knowledge, resource baselining and engagement with GGMF. |

| Theme 5: Capability and Resourcing | Best: Improving Cross-Government Capability and Capacity | Focus is on further increasing grants knowledge within the organisation, active contribution to develop grants capability across government and seeing resource alternatives. |

3.3 Core Self-Assessment Scoring Methodology

The methodology outlined below is underpinned by the fundamental principle that no organisation can move out of the developing category, without first fulfilling all criteria at the good level: or move from good to better or better to best, without first fulfilling all criteria at the preceding level(s).

Attainment is scored on four levels as shown in the table below:

| Attainment Level | Definition | Value of Statement | Outcome |

|---|---|---|---|

| Not Met | The organisation has not taken any action to meet the criterion. | 0 | Not Met |

| In Development | The organisation can evidence it is in the planning stages to meet the criterion, but no tangible work or implementation has begun. | 1 | Not Met |

| Newly Implemented | The organisation can evidence it has fully implemented and established the requirements of the criterion. It is applied consistently, but is still new and requires further establishment and refinement. | 2 | Met |

| Fully Embedded, BAU | The organisation can evidence that the requirements of the criterion are fully implemented, well-established, and consistently practiced and embedded throughout the organisation. | 3 | Met |

Developing: An organisation will always be assessed as being at the developing level, where it is assessed as not having scored a 2 or a 3 against all criteria at the good level, regardless of its status against the better and best criteria.

Good: An organisation which scores a 2 or a 3 against all criteria at the good level, will be assessed as good.

Better: An organisation which scores a 2 or a 3 against all criteria at the good level and the better level, will be assessed as better.

Best: An organisation which scores a 2 or a 3 against all criteria at the good, better and best levels, will be assessed as best.

Detailed analysis will be provided to each organisation, covering scores awarded for each criterion, for example, x% of good criteria met or not-met.

Please Note: For an organisation to sufficiently evidence a score of ‘3 - Fully embedded’ for ‘Better’ and/or ‘Best’, they should provide documentary evidence around how an intervention has been developed, implemented, embedded and improved over time.

4. Core Criteria: Self-Assessment Framework

Theme 1: Vision and Strategy

The organisation’s grants strategy should align with and support the delivery of the commitments in the Government Strategy for Grants Management and clearly state the organisation’s vision and plans for its grants function. It should include a long-term view of the management of the grants portfolio and consider what resources will be needed for effective delivery, in line with the Government Functional Standard GovS 015: Grants and Government Grants Management Function (GGMF) Functional Blueprint. Each organisation’s core function should operate a model capable of delivering within the scope of the Government Functional Standard GovS 015: Grants, to enable the effective delivery of policy objectives, whilst ensuring the sharing of best practice with active participation across stakeholder networks.

| Rating | Number | Criteria | References |

|---|---|---|---|

| Good | 1.1 | The organisation has in place an agreed vision and strategy for its grants function that is aligned with and supports the delivery of the Government Strategy for Grants Management. | GGMF Functional Blueprint, Section 1 - Vision, Strategy, Leadership and Location |

| Good | 1.2 | The organisation has a continuous improvement plan in place that focuses on improving grant-making maturity and supports the delivery of the Government Strategy for Grants Management. The scores are shared with senior governance and audit committee for regular review. |

Government Functional Standard GovS 015: Grants, Section 6.9, page 22 Minimum Requirement Seven: Risk, Controls and Assurance (PDF, 308KB), page 17 ‘Shall’ statement |

| Good | 1.3 | The organisation has an agreed and embedded Counter-Fraud strategy that aligns with Government Functional Standard GovS 013: Counter Fraud, addresses the inherent fraud risks within the grants portfolio, and incorporates assurances from the Government Counter Fraud Strategy. |

Government Functional Standard GovS 015: Grants, Section 6.2, page 19 GGMF Functional Blueprint, Section 1 - Vision Strategy, Leadership and Location |

| Good | 1.4 | The organisation has an operating model and ALB framework documents (where applicable) to ensure compliance with the Government Functional Standard GovS 015: Grants, minimum requirements, and Grants Pipeline Control, enabling the successful delivery of policy, strategy and objectives. |

Government Functional Standard GovS 015: Grants, Section 6.3, page 19 GGMF Functional Blueprint, Section 5 - Cross-Functional Coordination and Communications Government Functional Standard GovS 015: Grants, Section 4.3.1, page 8 |

| Better | 1.5 | Annual reviews are conducted to monitor activity undertaken to successfully achieve the organisation’s vision and strategy, with plans being made accordingly to ensure long-term grant making objectives will be achieved in line with the Government Strategy for Grants Management. | GGMF Functional Blueprint, Section 1 - Vision, Strategy, Leadership and Location |

| Better | 1.6 | The organisation has an individual, or a team, dedicated to monitoring and delivering the continuous improvement plan, ensuring stakeholders are provided with regular communication regarding progress. | Government Functional Standard GovS 015: Grants, Section 6.9, page 22 |

| Better | 1.7 | The organisation arranges for testing of Counter-Fraud compliance by experts that are separate from the grants function. | Government Functional Standard GovS 015: Grants, Section 6.2, page 19 |

| Better | 1.8 | The organisation actively participates in grant stakeholder forums, such as Best Practice networks, to enable the sharing of updates, signal future developments and to enable cross-functional discussion and networking in line with the Government Strategy for Grants Management. |

GGMF Functional Blueprint, Section 5 - Cross-Functional Coordination and Communications Grants Centre of Excellence events page has details of available networks |

| Best | 1.9 | Best practice and lessons learnt from continuous improvement plans are shared across departments and ALBs to support government wide maturity in grant-making and shape cross-government development of grant making strategy. | Government Functional Standard GovS 015: Grants, Section 6.9, page 22 |

| Best | 1.10 | The organisation has someone who takes leadership on cross-government initiatives to direct and improve grant-making policy and practices, ensuring value for money is delivered. | GGMF Functional Blueprint, Section 5 - Cross-Functional Coordination and Communications |

Theme 2: Governance and Management

This theme is concerned with governance and management processes, to ensure they are robust, expert based and provide appropriate assurance. The governance and management framework should clearly define grant-related roles, accountabilities and responsibilities – in line with section 4.4 of the Government Functional Standard GovS 015: Grants. It should be clear where financial authority for grant approval lies within the organisation, including through governance forums, making clear the delegated levels of authority for named individuals. Individuals identified in the organisation’s strategy should actively ensure that the leadership and governance processes support efficient and effective grant-making. The framework should align with the Grants Pipeline Control and provide clear contingency measures for emergencies. The organisation should have a robust communications plan to support government and management practices, enabling information to be shared in relation to developments, opportunities, management information and work plans, to ensure key objectives, tasks and deadlines are clear, monitored and coordinated across the function.

| Rating | Number | Criteria | References |

|---|---|---|---|

| Good | 2.1 | The organisation has a governance and management framework that includes authority limits for making funding decisions, degrees of autonomy, assurance needs, reporting structure and accountabilities, together with the appropriate management practices, processes and associated documentation needed to meet the Government Functional Standard GovS 015: Grants. The framework is referenced within the accounting officer’s system statement (PDF, 477KB). |

Government Functional Standard GovS 015: Grants, Section 4.1.1, pages 6 - 7 ‘Shall’ statements. Minimum Requirement Two: Governance, Approvals & Data Capture (PDF, 421KB), page 9 |

| Good | 2.2 | The organisation has defined accountabilities for the following roles, as a minimum, within the governance and management framework, and ensures they are assigned to people with appropriate seniority, skills and experience: - Departmental Head of Function - Senior Officer Responsible - Grants Champion - Accounting Officer - Grant Manager Roles and responsibilities include, but are not limited to: the activities, outputs or outcomes individuals are responsible for and the person they are accountable to. |

Government Functional Standard GovS 015: Grants: Section 4.4.1, pages 9-11 Role descriptions within Functional Standard: DHoF (SOA for an Organisation’s Grants): 4.4.5 SOR: 4.4.6 Grants Champion (4.4.7) Accounting Officer (4.4.3) Grant Manager (4.4.8) ‘Shall’ statement. Grants Centre of Excellence: Standard Documents |

| Good | 2.3 | The organisation has a process in place that ensures compliance with governance and approval requirements, set out in Minimum Requirement Two: Governance, Approvals and Data Capture (PDF, 421KB). | GGMF Functional Blueprint, Section 2 - Governance & Management Framework and Approvals |

| Good | 2.4 | The organisation has a policy in place to ensure that grants are competed by default, with a defined challenge and approvals process for direct or uncompeted awards. | Minimum Requirement Five: Competition for Funding (PDF, 285KB), page 7 |

| Good | 2.5 | There is a governance model in place to award grant funding in situations that qualify as an emergency under the definition used in the Civil Contingencies Act 2004. The model covers pre and post-award assurance, data requirements, tools and templates, as required by policy guidance on emergency grants, published by the Government Grants Management Function. | GGMF Functional Blueprint, Section 2 - Governance & Management Framework and Approvals |

| Good | 2.6 | The organisation has a communication plan in place, which is reviewed regularly and updated to ensure all those involved in grant making are provided with or have access to the information they need, when it is needed, to carry out their role effectively. | GGMF Functional Blueprint, Section 5 |

| Good | 2.7 | The organisation has input from functional experts for grant approval decisions - such as grants policy, financial, commercial, legal, fraud and national security. Approval decisions are based on accurate, up-to-date information and recorded in the business case (or equivalent document). | Minimum Requirement Four: Business Case Development (PDF, 296KB), page 17 |

| Better | 2.8 | There is a challenge panel (or equivalent model) in place to interrogate the design of new schemes and to inform the review of existing grant schemes, to ensure the delivery model and mechanism remains current, appropriate and fit for purpose. |

Minimum Requirement Two: Governance, Approvals & Data Capture (PDF, 241KB), page 12 Grants Challenge Panel Guidance Note |

| Better | 2.9 | The organisation’s governance and management framework is periodically reviewed and updated to ensure it is still valid in line with policy objectives. | Government Functional Standard GovS 015: Grants, Section 4.1.3, page 7 |

| Better | 2.10 | For smaller grant funded-investments that don’t require formal approval from an investment committee, there’s a clear approvals process. A person with the appropriate level of financial authority approves these cases, following the guidelines in Annex 5.1 (Control) of the Managing Public Money document. | GGMF Functional Blueprint, Section 2 - Governance & Management Framework and Approvals |

| Better | 2.11 | The organisation’s communication plans include arrangements for regular two way communication with the Finance and Commercial Functions for collaboration on scheme development, in particular those that are high-risk, high-value, novel, contentious or repercussive. | GGMF Functional Blueprint, Section 1 - Vision, Strategy, Leadership and Location |

| Best | 2.12 | The organisation has someone at the Senior Civil Servant grade who has membership of or contributes to the working of the Complex Grants Advice Panel (GCAP), providing support and advice for new schemes, either as a panel member or for correspondence cases. This may be managed on a rotational basis, across SCS members. | Minimum Requirement Three: CGAP (PDF, 241KB), page 4 |

| Best | 2.13 | The organisation’s Departmental Head of Function (DHoF) networks across organisational boundaries to provide support, leadership and direction for grant-making activity across government. | Government Functional Standard GovS 015: Grants, Section 4.4.5, page 10 |

Theme 3: Data, Reporting and Digital

This theme is focused on the accuracy and completeness of the data input to the Government Grant Information System (GGIS). Minimum Requirement Two: Governance, Approvals and Data Capture (PDF, 421KB) holds the most up to date information around GGIS requirements. It is important that the data captured is accurate and complete, because it provides important management information and is published on GOV.UK, as part of the Government’s transparency commitment. Data capture and reporting must be compliant with the Grants Pipeline Control and the Government Grants Data Standard – both are available to download from the Grants Centre of Excellence. The Memorandum of Understanding (MoU) agreed with each central department (available from the departmental Grants Champion) should support compliance with the control and data standard, within the organisation’s policy and processes.

| Rating | Number | Criteria | References |

|---|---|---|---|

| Good | 3.1 | The organisation has an information management and retention policy that ensures grant management documentation is retained in line with statutory (PDF, 316KB) and legal requirements. |

Government Functional Standard GovS 015: Grants, Section 6.6 ‘Shall’ statement Minimum Requirement Two: Governance, Approvals and Data Capture (PDF, 421KB), page 7 |

| Good | 3.2 | The organisation has a clear sign-off process in place - overseen by an appropriate person, such as the grants Departmental Head of Function (DHOF), and including ministers as required - to enable the safe publication of grants data on GOV.UK, including taking appropriate steps to ensure data, information, documents and records are accurate, complete and reconcilable to internal reporting. | GGMF Functional Blueprint, Section 2 - Governance & Management Framework and Approvals |

| Good | 3.3 | Timely and accurate management information is available to ministers and senior officials for use internally and externally, to enable effective decision making throughout the grants lifecycle. | GGMF Functional Blueprint, Section 3 - Data, Reporting and Digital |

| Good | 3.4 | The organisation makes use of existing digital tools, alongside investing in digital capability (following Government Functional Standard GovS: 005: Digital), to increase the efficiency and effectiveness of grants administration and to support compliance with the Government Functional Standard GovS 015: Grants. | GGMF Functional Blueprint, Section 3 - Data, Reporting and Digital |

| Good | 3.5 | The organisation reports on the status of grants as part of their annual report and resource accounts, ensuring GovS006: Finance (PDF, 674KB) is followed. |

Government Functional Standard GovS 015: Grants, Section 6.8, page 21 ‘Shall’ statement. |

| Good | 3.6 | The organisation enters details of each grant scheme onto the Government Grant Information System as soon as approval to design and develop the proposal has been given, and updates details as required to ensure data is captured, in line with the agreed Memorandum of Understanding, Grants Pipeline Control and the Data Standards. This includes ensuring compliance with Minimum Requirement Three: CGAP (PDF, 241KB). |

Government Functional Standard GovS 015: Grants, Section 5.2.1, page 14 ‘Shall’ statement. Minimum Requirement Three: CGAP (PDF, 241KB) |

| Better | 3.7 | The organisation promotes the use of and encourages SORs to draw on data from historic grant schemes and awards and evaluation data via the ETF Evaluation Database, or internal sources, to inform the design and development of new grant schemes. | GGMF Functional Blueprint, Section 3 |

| Better | 3.8 | The grants function within the organisation promotes and monitors the use of Grants Scheme Readiness Assessments, for appropriate schemes. |

GGMF Functional Blueprint, Section 3 - Data, Reporting and Digital Grants Centre of Excellence |

| Better | 3.9 | The organisation makes use of the non-mandatory fields on the GGIS, where a requirement for management information is identified, prioritising in particular providing details of both actual and budgeted spend. | Minimum Requirement Two: Governance, Approvals and Data Capture (PDF, 421KB), pages 13-15 |

| Better | 3.10 | The organisation has in place an individual or team that is responsible for assuring the organisation’s grants data quality and accuracy. |

Minimum Requirement Two: Governance, Approvals and Data Capture (PDF, 421KB) GGMF Functional Blueprint, Section 2 - Governance & Management Framework and Approvals |

| Best | 3.11 | Relevant systems are connected to the GGIS via Application Programming Interface (API) automating the data upload process between systems in real-time. | Minimum Requirement Two: Governance, Approvals and Data Capture (PDF, 421KB) |

| Best | 3.12 | The organisation analyses data to provide insight into current and future grants strategy, informing and driving evidence-based improvements in grant-making across government. | GGMF Functional Blueprint, Section 3 - Data, Digital and Reporting |

Theme 4: Risk Management and Assurance

This theme is focused on effective risk management and the need to assess and manage risk at the outset, as part of the business case and throughout the life cycle of the grant scheme. Reducing risk mitigates against fraud and misuse and improves the likelihood of the successful delivery of outcomes and value for money. The focus is on how risks are identified and managed by the organisation, working in partnership with the grant recipient. Organisations should follow best practice, as set out in the Orange Book (PDF, 465KB).

The theme also covers extent to which the organisation has in place the three lines of defence, to demonstrate ongoing assurance that its grants design, development and administration is in accordance with the organisation’s assurance strategy, and is compliant with the grants Government Functional Standard GovS 015: Grants, and Minimum Requirement Seven: Risk Controls and Assurance (PDF, 308KB).

| Rating | Number | Criteria | References |

|---|---|---|---|

| Good | 4.1 | The organisation’s risk management practices and procedures are part of their overall assurance and governance, with defined risk registers that include very high and high risks associated with gold and silver schemes (where applicable). The risk registers are maintained and regularly reviewed by the organisation’s senior officers who are accountable for grant activities. |

Minimum Requirement Seven: Risk, Controls and Assurance (PDF, 308KB) ‘Shall’ statement. Government Functional Standard GovS 015: Grants, Section 6.1, page 18 ‘Shall’ statement. Minimum Requirement Four: Business Case Development (PDF, 296KB) |

| Good | 4.2 | The organisation has a defined and agreed grants risk appetite, that provides direction and sets boundaries for risk management. It is reviewed periodically with proportionate and effective, risk based controls in place, with additional controls implemented where residual risk falls outside of the department’s risk tolerance. | Minimum Requirement Seven: Risk, Controls and Assurance (PDF, 308KB), page 7 |

| Good | 4.3 | The organisation has a process in place to ensure assurance reports are shared with senior governance and audit committees for regular review. |

Minimum Requirement Seven: Risk, Controls and Assurance (PDF, 308KB), page 17 ‘Shall’ statement |

| Good | 4.4 | The organisation has a visible, defined and established approach to grants assurance, that has been developed in the context of the three lines of defence, with effective controls and mitigations, that are applied proportionately to the risk, value and complexity of the grant funding activity, and integrated into the organisation’s overall assurance framework. |

GGMF Functional Blueprint, Section 7 Government Functional Standard GovS 015: Grants Section 4.3.1, page 8 |

| Good | 4.5 | The organisation has embedded due diligence processes across its grants portfolio, ensuring potential risks and issues are identified, evaluated and mitigated as required. | Minimum Requirement Seven: Risks, Controls and Assurance (PDF, 308KB), page 14 |

| Better | 4.6 | The organisation has plans in place to ensure there is no duplication of internal and external assurance provider activities, to minimise the disruption to other work, avoid overlaps and meet the needs of stakeholders. | Government Functional Standard GovS 015: Grants, Section 4.3.1, page 8 |

| Better | 4.7 | The organisation undertakes second line of defence activities periodically, to assure that risk management and first line of defence assurance processes are properly designed, in place and operating as intended. | Government Functional Standard GovS 015: Grants, Section 4.3.1, page 8 |

| Best | 4.8 | There is a systematic approach to testing policy and process, to ensure that the third line of defence provides effective assurance against risk. | Government Functional Standard GovS 015: Grants Section 4.3.1, page 8 |

| Best | 4.9 | The organisation establishes a Project Management Office, or has access to an equivalent facility within the organisation, to manage the grants portfolio, providing centralised oversight for consistent assurance and risk mitigation, in line with Government Functional Standard GovS002: Project Delivery. |

Government Functional Standard GovS 015: Grants Sections 4.3 (page 8) and 6.1 (page 18) Government Functional Standard GovS002: Project Delivery |

Theme 5: Capability and Resourcing

This theme is about ensuring that those involved in the design, development and administration of government grant schemes and awards have an appropriate level of capability to enable them to be effective in their role, along with access to further learning and development opportunities, which is essential to ensure efficient and effective management. Minimum Requirement Ten: Training, requires that all those involved in grant making undertake core training (awareness level under the Licence to Practise). It is important that organisations monitor and manage the uptake of training in grant making, to ensure that grants capability across the organisation is well matched to the requirements of its grants portfolio, across the six stages of the life cycle.

It also relates to ensuring that each grant scheme has a proportionate allocation of appropriately qualified people at a range of grades, and ready access as needed to subject matter experts throughout the design, development and administration stages of the scheme and associated awards. This includes the resourcing of any central supporting team, such as a grants portfolio team. Consideration should also be given to engagement with GGMF for expert support, where required. While capacity principally relates to people, the effective use of systems - including digital capability and efficient process - also plays an important part. There should be consideration of the need to be prepared to mobilise quickly, to support emergency grant making when applicable.

| Rating | Number | Criteria | References |

|---|---|---|---|

| Good | 5.1 | The organisation ensures mandatory completion of basic training for all grants practitioners (Grants Awareness Programme - including the eLearning and assessment, or equivalent) to ensure they have the capability to perform their role effectively. |

Government Functional Standard GovS 015: Grants, Section 6.7, page 21 ‘Shall’ statement. The Grants Awareness Programme is available on the Government Commercial College Minimum Requirement Ten: Training (PDF, 268KB), page 6 |

| Good | 5.2 | The organisation’s grant function actively promotes and raises awareness of the Grants Centre of Excellence and encourages its grant practitioners to register for access. | GGMF Functional Blueprint, Section 6 Expert Support |

| Good | 5.3 | The organisation has a resource plan to ensure adequate use of the central grant function’s resources and expertise, in proportion to its grants landscape, and actively monitors and maintains the effectiveness of this plan. | Government Functional Standard GovS 015: Grants, Section 6.3, page 19 |

| Good | 5.4 | The organisation has a capability strategy in place to ensure the appropriate level of training and support is made available to all staff, covering the fundamental principles of grant making. | Minimum Requirement Ten: Training (PDF, 268KB), page 8 |

| Better | 5.5 | The organisation’s resource baseline includes the target cost of the organisation’s grant function, staff grade mix and resourcing plan, which includes administration costs. | Government Functional Standard GovS 015: Grants, Section 6.3, page 19 |

| Better | 5.6 | The organisation promotes the use of the grants competency framework enabling capability and training needs to be reviewed and to identify knowledge gaps. | Minimum Requirement Ten: Training (PDF, 268KB), page 7 |

| Better | 5.7 | The organisation’s capability strategy includes the promotion and budget consideration for the Licence to Practise and strongly encourages grants practitioners to enrol for the Licence to Practise and obtain accreditation. | Minimum Requirement Ten: Training (PDF, 268KB), page 9 |

| Better | 5.8 | The organisation actively engages with GGMF Business Partners, where in place, or via standard GGMF communication channels, to access expert support, particularly following the identification of gold schemes via the Government Grant Functions triage process, where support can have maximum impact. | GGMF Functional Blueprint, Section 6 - Expert Support |

| Best | 5.9 | Grants practitioners collaborate with the GGMF capability team by providing insight and expert input into the development of products and services under the GGMF capability offer. | Minimum Requirement Ten: Training (PDF, 268KB), page 10 |

| Best | 5.10 | The organisation monitors resource capacity and enquires about the use of the Government Grants Managed Service (GGMS) on a comply or explain basis where additional capacity is required for individual schemes. | GGMF Functional Blueprint, Section 1 - Vision, Strategy, Leadership and Location |

5. Structure and characteristics of the assessment on scheme criteria

5.1 The structure of the scheme assessment framework

The structure of the assessment framework for schemes is designed to give an indicative picture of how well an organisation is administering their grant schemes.

- Minimum Requirement: Is the overall topic being addressed.

- Criteria: The statements to be met.

Minimum Requirement: A minimum requirement is the overall topic being addressed in that section of the assessment framework, which are based on the ten minimum requirements for grants. The context and more information about the minimum requirements addressed can be found in the minimum requirement documents available on gov.uk.

Assessment criteria: Criteria help to define what is happening in an organisation (observable in practice, supported by documentary evidence). The Criteria denote the requirements for schemes based on how they have been categorised as part of the Gold, Silver, Bronze framework and have been written and based on the Government Functional Standard GovS 015: Grants (PDF, 341KB) and the Minimum Requirements.

For example, the required content of a ‘Senior Officer Responsible for a grant’ is described in Minimum Requirement One (PDF, 240KB).

The assessment is completed by the (Government Internal Audit Agency (GIAA) or internal audit, or an external auditor of the organisations choosing, who is required to upload scores to the GCIAF Digital Tool, which provides organisations with the functionality to upload the required documents to evidence how they meet each criterion.

A link to the GCIAF Digital Tool is available on the Grants Centre of Excellence.

Details of the evidence required for completion of the scheme assessment is available here: Scheme Criteria evidence tables

Important Note: Use of the comply or explain principle.

Comply or explain is available to grant makers, in the design, development and administration of general grant schemes. Guidance on the use of comply or explain is contained under paragraphs 5 to 8 in the Guidance for General Grants (PDF, 577KB). Where comply or explain has been used in the administration of a grant scheme being assessed as part of the GCIAF scheme level assessment, organisations should provide the supporting rationale for each use, along with approval information, to their auditor as part of their evidence for their sampled scheme.

5.2 Scoring Methodology - Scheme assessment

The scheme level validation approach has been designed to align with the ten minimum requirements that underpin the Government Functional Standard GovS 015: Grants (PDF, 341KB). All schemes selected will be evaluated against the Bronze criteria. Additionally, schemes that fall into the category of Silver and Gold must comply with the additional metrics defined in the scheme level criteria.

Individual metrics will not be scored in isolation. Instead, the auditor will assess the scheme as a whole, applying professional judgment to assess scheme compliance with the Functional Standard. Audit evaluation will be based on a review of the evidence provided by the organisation to determine the level of assurance provided.

The level of assurance will also consider the results of the transaction testing and verification, where appropriate, of any performance measures to confirm the achievement of scheme policy objectives.

Transaction testing will be conducted to assess whether the organisation has effectively applied/implemented the grant making systems and processes. Based on the findings of our compliance work and the outcomes from the transaction testing and performance assessment, the auditor will provide one of the four opinions below for each scheme.

| Substantial | The scheme governance, risk management and control are adequate and effective. |

| Moderate | Some improvements are required to enhance the adequacy and effectiveness of the scheme governance, risk management and control. |

| Limited | There are significant weaknesses in the scheme governance, risk management and control such that it was inadequate and ineffective. |

| Unsatisfactory | There are fundamental weaknesses in the scheme governance, risk management and control such that it was inadequate and ineffective. |

The auditor will select a sample of transactions using a statistically valid sampling approach (wherever possible) to ensure error rates are as reliable and representative and to ensure consistency in the selection process across all schemes.

The selected transactions will then be tested by reviewing all available evidence to confirm the eligibility of the expenditures and identify potential errors. Errors may include inaccuracies in the amounts claimed, ineligible expenditure, incorrect classifications, missing on incomplete documentation, potential fraudulent transactions, grant claims outside of the scheme timelines, system or process failures, etc.

After completing the testing of all transactions within the sample, the total value of the errors identified will be calculated. The calculated error rate will be reported for each scheme.

Where possible the auditor will review the performance of the scheme to assess whether it has achieved its policy objectives i.e. progress towards meeting its indicative KPIs, milestones or other metrics designed to measure outcomes and success. Where applicable this will be considered in the audit opinion.

Thereafter, the auditor will compile the scores assigned to each scheme and determine an overall error rate and opinion for the organisation. This evaluation will be based on the opinions outlined above i.e. Substantial, Moderate, Limited, Unsatisfactory.

5.3 Sampling Methodology and Financial Testing - Scheme assessment

For the 2026/27 assessment, the population will be defined using GGIS commitment and spend data for the financial years 2024/25 and 2025/26. The auditor will analyse and, if necessary, cleanse/identify any anomalies to determine a population of grant schemes for each organisation. Practicalities when sampling will be taken into account, and the organisations will be consulted throughout the whole process.

To avoid any unnecessary duplication, the auditor will coordinate with bodies such as the NAO, as well as with the assurance functions within the organisations. Any assurances previously provided will be considered, and if it is determined that the assurance work can be relied upon, the scheme will be excluded from the sampling population.

The Auditor will use judgmental[footnote 1] sampling techniques to draw a sample of schemes following the below parameters:

- Where the population allows, at a minimum, 1 Bronze, 1 Silver and 1 Gold scheme will be selected for testing.

- For additional selections the auditors will, again, use judgmental sampling to select based on a risk and materiality perspective.

- A default position of 4 schemes reviewed for each organisation - however, this could be changed depending on the number of ALBs incorporated into their parent departments’ assessment.

The auditor will select a representative sample of transactions to test. For each scheme selected the auditor will determine the transactional level population through discussion with the project team and/or the organisation Finance team.

The auditor will then select a sample of transactions to test using, where possible, a statistical[footnote 2] sampling methodology to ensure a representative sample is drawn. We anticipate no more than 30 items/transactions would be selected for testing per scheme.

The sample will then be tested to substantiate the eligibility of the grant expenditure. This will involve reviewing base level documentation i.e. claims and monitoring reports, invoices or documents of equal probative value, evidence of defrayal, etc.

6. Scheme Criteria: Assessment Framework

Minimum Requirement One – Senior Officer Responsible

All government grants shall have a named Senior Officer Responsible (SOR) for a grant with clearly defined responsibilities throughout the lifetime of the grant.

Organisations should ensure that an SOR for a grant is an individual with the necessary authority, capability and capacity, and a full understanding of their role and associated obligations, is assigned to each grant scheme. The SOR shall take responsibility for delivering value for money and for managing risk within acceptable tolerances, as defined by their organisation’s policies, governance and approvals processes.

Minimum Requirement One: SOR for a Grant (PDF, 240KB)

| Category | Number | Criteria |

|---|---|---|

| Bronze | 1.1 | The appointed SOR was formally appointed in writing by a senior official prior to the scheme’s development. |

| Bronze | 1.2 | The SOR ensured that the scheme’s Gold, Silver or Bronze category accurately reflected the scheme’s specific value, complexity, and risk profile. |

| Bronze | 1.3 | The SOR’s details were maintained on the Government Grants Information System (GGIS), with records updated promptly to reflect any changes in the SOR’s appointment throughout the grant’s lifecycle. |

| Silver | 1.4 | The appointed Senior Officer Responsible (SOR) possesses a level of seniority and experience commensurate with the scheme’s value, complexity, and risk profile. |

| Gold | 1.5 | The scheme SOR is a SCS 1 (minimum) with prior experience of delivering high profile novel and contentious and/or ‘Gold’ schemes. |

Minimum Requirement Two: Governance, Approvals and Data Capture

Departments shall ensure they have a robust grants approval process to approve spend over £100,000, and that details of all current grant schemes and awards are available on the Government Grants Information System (GGIS).

Governance, Approvals and Data Capture is designed to ensure that government grant making organisations have a robust and proportionate governance and approvals process in place to scrutinise and approve their general grant schemes, in line with the grants functional standard and Managing Public Money.

Minimum Requirement Two: Governance Approvals and Data Capture (PDF, 421KB)

| Category | Number | Criteria |

|---|---|---|

| Bronze | 2.1 | Details of the grant scheme have been fully and accurately recorded on the Government Grants Information System (GGIS), ensuring the scheme details are entered on to the system at the design and development stage and in accordance with the agreed Memorandum of Understanding, Grants Pipeline Control and the Data Standards. |

| Bronze | 2.2 | The scheme was subject to appropriate approvals in line with the delegated authority spending framework for the organisation and HMT Green Book (PDF, 951KB) guidance and GovS 006 Finance (PDF, 674KB) has been complied with. |

| Silver | 2.3 | Non-mandatory fields on the GGIS are populated and kept up to date, including actual and budgeted spend. |

| Gold | 2.4 | The scheme has been triaged and provided with a bespoke support offer. |

Minimum Requirement Three: Complex Grants Advice Panel

New government grants, including those that are high-risk, novel, contentious or repercussive, as well as those undergoing a step-change in scope or funding, should be considered for submission to the Complex Grants Advice Panel (CGAP) for scrutiny and advice from subject experts.

The CGAP ensures that there is proportionate, expert scrutiny and challenge applied to the development of all grant schemes, in particular, during the design and development stage.

Minimum Requirement Three: CGAP (PDF, 241KB)

| Category | Number | Criteria |

|---|---|---|

| Bronze Silver Gold |

3.1 | The scheme complied with all Complex Grants Advice Panel (CGAP) submission requirements. |

| Bronze Silver Gold |

3.2 | CGAP recommendations were implemented, or a clearly documented, evidence-based rationale for non-implementation was provided and formally approved at an appropriate level within the organisation. |

Minimum Requirement Four: Business Case Development

A robust business case, proportionate to the level of expenditure and risk, shall be developed for all government grants. This should be scrutinised and approved in stages, as part of the grants’ approval process, in line with managing public money.

Business case development aims to ensure that government grant schemes are developed in line with domestic standards and the principles contained in Managing Public Money, to ensure that funding is used as intended, outcomes are optimised, and performance, expenditure and risk are managed effectively to maximise value for money.

Minimum Requirement Four: Business Case Development (PDF, 296KB)

| Category | Number | Criteria |

|---|---|---|

| Bronze | 4.1 | A basic business case was developed and approved by the organisation’s Financial Business Unit (or equivalent) in line with HMT’s proportionality requirements/guidelines. |

| Bronze | 4.2 | A range of experts were consulted during the business case development process for the scheme. Depending on the nature of the scheme, this could, for example, include experts from legal, finance, commercial, audit, subsidy control, and counter fraud. |

| Bronze | 4.3 | The business case was reviewed and updated throughout the grant lifecycle to reflect material changes in value, delivery period, or design, ensuring formal re-approval was obtained whenever such changes occurred. |

| Bronze | 4.4 | Grant risks were addressed in the grant scheme’s business case, along with mitigating actions and proportionate controls, and where appropriate, arrangements were in place to adjust/revisit the business case, to reflect changes in the risk profile and/or complexity of the scheme. |

| Silver | 4.5 | The Readiness Assessment Tool has been used to assess the readiness of the scheme. |

| Silver | 4.6 | A medium complexity business case, in line with HMT Green Book (PDF, 951KB) guidance was developed and approved by senior finance business partner (or equivalent) and the organisation’s investment committee (or equivalent) and approved by HMT if appropriate. |

| Gold | 4.7 | In line with HMT’s Green Book (PDF< 951KB) guidance a five-case model business case was developed and approved by a senior finance business partner, or equivalent, via the organisation’s investment committee (or equivalent) with mandatory input from CGAP and further approval HMT if appropriate. |

Minimum Requirement Five: Competition for Funding

Government grants should be competed by default; exceptions may be approved where competition would not be appropriate. Detailed supporting evidence for any direct award decision should be provided in the approved business case.

Competition for funding aims to ensure that value for money is optimised through effective competition of all general grants and that any decision taken not to compete a general grant opportunity is fully justified and made with the necessary approval.

Minimum Requirement Five: Competition for Funding (PDF, 285KB)

| Category | Number | Criteria |

|---|---|---|

| Bronze Silver Gold |

5.1 | The scheme was competed. If it was not competed, there was justification for a direct award, the decision was approved by an official or approvals body with appropriate authority, and an audit trail has been retained in support of the decision. |

| Bronze Silver Gold |

5.2 | The grant scheme, if general grants which are competed or criteria-based, was advertised on Find a Grant, in line with the mandatory requirement for government general grant schemes. |

| Bronze Silver Gold |

5.3 | Where competition occurred, an open and transparent process was undertaken using an appropriate assessment and scoring methodology, taking risk, complexity, and materiality into account for high value, novel or contentious or repercussive schemes. |

Minimum Requirement Six: Grant Agreements

All government general grants shall be awarded through robust grant agreements, proportionate to the value of the grant, which reflect the Grants Functional Standard for government grants and are in line with Managing Public Money. All government grant agreements shall include terms of eligible expenditure.

Grant agreements are provided to help ensure that all government general grants schemes have appropriate agreements in place, which set out amongst other provisions: the purpose and objectives of the award; standard terms and conditions for the receipt of funding; performance monitoring; financial assurance; and a payment schedule. This should assist in minimising risk around accidental or deliberate misuse, provide necessary controls to manage delivery and ensure adherence to the appropriate parts of the minimum requirements for general grants.

Minimum Requirement Six: Grant Agreements (PDF, 285KB

| Category | Number | Criteria |

|---|---|---|

| Bronze | 6.1 | A Grant Funding Agreement (GFA), or equivalent, is in place for the scheme which includes all the provisions of the Model Grant Funding Agreement. |

| Bronze | 6.2 | The scheme Grant Funding Agreement, or equivalent, has been reviewed and quality assured to ensure it is robust, tailored and proportionate. Experts e.g., legal, finance, etc. were consulted to ensure any scheme specific requirements were correctly reflected in the GFA and, if appropriate, advise on any deviations from the funding agreement. |

| Silver | 6.3 | The Short-form or Long-form Model Grant Funding Agreement (or an equivalent bespoke agreement) was used as a template for general grants at a minimum with terms and conditions proportionate to the value and complexity of the scheme. |

| Gold | 6.4 | The Long-form Model Grant Funding Agreement was used as a template for general grants at a minimum with terms and conditions proportionate to the value and complexity of the scheme. |

Minimum Requirement Seven: Risk, Controls and Assurance

All government grants shall be subject to timely and proportionate due diligence, assurance and fraud risk assessment.

Risks, controls and assurance provides detail on the creation and maintenance of a risk, controls and assurance management framework, including the management of national security and economic crime threats. An effective risk, controls and assurance framework is designed to reduce the risk of grant schemes failing to achieve their objectives and will support efficiency and the achievement of value for money, helping to minimise the misuse of public money.

Minimum Requirement Seven: Risk, Controls and Assurance (PDF, 308KB)

| Category | Number | Criteria |

|---|---|---|

| Bronze | 7.1 | A Fraud Risk Assessment, proportionate to the scheme’s size and complexity and aligned with GovS013 Counter Fraud Standards (PDF, 266KB), was completed and signed off by the SOR before funding approval. For schemes exceeding £100,000, a dedicated fraud risk register was established, setting out specific mitigating actions and proportionate controls. |

| Bronze | 7.2 | Proportionate due diligence was conducted prior to any funding decisions, involving expert consultation where necessary. All potential red flags were investigated. |

| Bronze | 7.3 | The scheme risk register is reviewed periodically, and the effectiveness of mitigating actions are tested through the life of the scheme. |

| Bronze | 7.4 | Probative testing was performed to verify that all expenditure was eligible, grant conditions were fully met, and the scheme delivered overall value for money. Any errors were considered for clawback and suspected misuse prompted immediate investigation. |

| Silver | 7.5 | Proportionate due diligence was conducted and documented at all relevant tiers of the contracting chain. |

| Silver | 7.6 | The Fraud Risk Assessment has been reviewed periodically to test the effectiveness of prevention and detective controls and updated throughout the life of the scheme. |

| Gold | 7.7 | The scheme adopted a proportionate approach to testing scheme expenditure to confirm eligibility of expenditure claimed, grant conditions have been complied with and value for money has been achieved. This could include tests by grant teams i.e., 1st line or as part of 2nd line assurance checks. |

| Gold | 7.8 | The Fraud Risk Assessment has been reviewed, within an appropriate governance structure, working with experts from the Public Sector Fraud Authority (PSFA) and/or fraud experts within the organisation, and if necessary, updated to account for emerging fraud risks throughout the scheme lifecycle. |

| Gold | 7.9 | The scheme adopted a proportional approach to testing scheme expenditure to confirm the eligibility of expenditure claimed, grant conditions have been complied with and value for money has been achieved. This could include tests by grant teams i.e., 1st line, 2nd line assurance checks and 3rd line i.e., internal audit. Evidence is available to demonstrate corrective action has been taken where errors have been found i.e., clawback and/or action taken to improve scheme controls. |

Minimum Requirement Eight: Performance and Monitoring

All government grants should have performance measures agreed and longer-term outcomes defined, wherever possible, to enable active performance management, including regular reviews and adjustments where deemed necessary.

Performance and monitoring are designed to ensure that there is active performance and financial management of the grant, after it has been awarded. Active management of the grant is essential to minimise the risk of financial loss and to ensure risks to delivery are effectively managed, in order to support full achievement of the objectives and outcomes, to maximise the value for money obtained from the expenditure.

Minimum Requirement Eight: Performance and Monitoring (PDF, 193KB)

| Category | Number | Criteria |

|---|---|---|

| Bronze | 8.1 | Monitoring processes were implemented using performance indicators and milestones to track the scheme’s progress. |

| Bronze | 8.2 | For grants paid in arrears, all financial and performance monitoring returns were received and verified before payments were released. |

| Bronze | 8.3 | Performance improvement plans were triggered if monitoring returns were missing or incomplete, errors were identified during validation, performance fell below agreed tolerances, or if fraud and misuse were suspected. |

| Bronze | 8.4 | A formal impact evaluation was undertaken based on appropriate research and evaluation methods– in line with the evaluation strategy and model, approved in the business case. |

| Bronze | 8.5 | The scheme’s evaluation findings are published on the Evaluation Registry to ensure lessons are shared, standards are raised, and government grant-making is continuously improved. |

| Silver | 8.6 | A proportionate approach was taken to monitoring i.e., more frequent and more detailed reports submitted and reviewed by the SOR and/or a grants delivery board or equivalent. |

| Gold | 8.7 | A proportionate approach was taken to monitoring i.e., more frequent and more detailed reports submitted and reviewed by the SOR and any wider organisation delivery boards, including escalation routes to the Audit and Risk Committee, with evidence of independent review. |

Minimum Requirement Nine: Annual Review and Reconciliation

All government grants shall be reviewed annually at a minimum with a focus on financial reconciliation, taking into account delivery across the period, resulting in a decision to continue, discontinue or amend funding.

Annual review and reconciliation aims to ensure that there is an efficient and effective review and reconciliation of the grant scheme at the end of each financial year, for multi-year schemes, and also the end of the grant delivery period for all schemes. The review shall include both financial and delivery considerations, providing scrutiny and contributing to the identification of lessons learnt through the wider, formal evaluation, to apply to future policy making. The purpose of the reconciliation and evaluation step is to establish whether value for money has been achieved, to confirm that the delivery objectives have been achieved, that the funding has been used for the intended purpose and managed appropriately, and to assess the impact of the intervention and capture and share learning. Longer term outcomes are further assessed via the impact evaluation.

Minimum Requirement Nine: Annual Review and Reconciliation (PDF, 269KB)

| Category | Number | Criteria |

|---|---|---|

| Bronze | 9.1 | An annual review and financial reconciliation was completed and payments were compared against declared expenditure in accordance with the requirements of Managing Public Money. |

| Bronze | 9.2 | The organisation correctly accounted for the grant scheme and costs have been allocated under the appropriate expenditure and budget category in line with grants policy and standards. |

| Silver | 9.3 | Reconciliations were conducted more frequently (e.g., quarterly), allowing for earlier corrective action. The performance of the reconciliation exercises was confirmed by a 2nd line control function, such as Finance, an internal assurance team, etc. |

| Gold | 9.4 | Reconciliations were carried out on a more frequent basis, i.e., monthly, demonstrating additional financial control and enabling the scheme to take corrective action at an earlier stage in line with the principles of risk and proportionality. |

Minimum Requirement Ten: Training

All those involved in the development and administration of grant awards should undertake core training in grant management best practice.

Training is aimed at ensuring that anyone involved in the design, development and administration of government general grants is competent and properly equipped to undertake their role effectively. The appropriate level of training and support should be made available to all staff, covering the fundamental principles of grant making, including optimising value for money and identifying and managing risk, including fraud risk.

Minimum Requirement Ten: Training (PDF, 268KB)

| Category | Number | Criteria |

|---|---|---|

| Bronze Silver Gold |

10.1 | All staff working on scheme grants administration completed the Grants Awareness Programme – including the eLearning and assessment or equivalent. |

| Bronze Silver Gold |

10.2 | Grant practitioners working on the scheme undertook fraud, bribery and corruption awareness training as defined and required by their organisation and PSFA guidance. |

| Bronze Silver Gold |

10.3 | The SOR is or has considered undertaking the SOR training in place of the Grants Awareness Programme. |

| Bronze Silver Gold |

10.4 | The SOR and lead officials for the scheme are or have considered working towards the Grants Licence to Practise. |

Glossary

| Term | Definition |

| Accounting officer system statement (AOSS) | The accounting officer system statement is to provide to Parliament a single statement setting out all of the accountability relationships and processes within a department, making clear who is accountable for what, from the principal accounting officer down. |

| Assessment criteria | Each theme is supported by a number of criteria. Criteria help to define what is happening in an organisation (observable in practice, backed up by documentary evidence). The Criteria denote the requirements of good, better or best performance |

| Assurance | A general term for the confidence that can be derived from objective information over the successful conduct of activities, the efficient and effective design and operation of internal control, compliance with internal and external requirements, and the production of insightful and credible information to support decision making. Confidence diminishes when there are uncertainties around the integrity of information or of underlying processes. |

| Blueprint | The GGMF Blueprint provides advice and guidance for the functional standard to grant funders. The Blueprint provides transparency regarding the key features and expectations for a grant funder and an articulation of the flexibilities and choices available to the funder in seeking to comply with the requirements of individual elements of the Functional Blueprint. |

| Business case | A management tool that records the current state of evidence and thinking concerning the development approval and implementation of a proposal. It supports the processes of scoping, analysis, appraisal, planning, monitoring, evaluating, approval and implementation of a proposal and is the repository for the evidence base |

| Continuous improvement plans | Improvement plans agreed between the organisation and GGMF, designed to target specific areas for development as informed by the results of the continuous improvement assessment. These improvement plans are to be monitored on a periodic basis - recommended quarterly - alongside GGMF to ensure progress to being made in targeted areas. |

| Functional standard | Functional standards are government standards designed to provide a coherent, effective and mutually understood way of doing business across organisational boundaries, and a stable basis for assurance, risk management and capability improvement. |

| Governance and management framework | A governance and management framework sets out the authority limits, decision making roles and rules, degrees of autonomy, assurance needs, reporting structure, accountabilities and roles, together with the appropriate management practices and associated documentation needed to meet this standard. |

| Government Grant Information System (GGIS) | Holds data on schemes, awards and grants in aid across government. It aims to do this by providing a consistent view of grants data fields, ensuring data can be compared and aggregated across departments. departments and arms length bodies are responsible for the input of data. |

| Grant in Aid (GiA) | Grant-in-aid provides general support, usually for an Arms length Body, with fewer specific, but more general controls on the body, which may mean less oversight by the funder; for example, to fund running costs |