Cyber security longitudinal study - wave two

Updated 19 December 2022

© Crown copyright 2022

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/cyber-security-longitudinal-survey-wave-two-results/cyber-security-longitudinal-study-wave-two

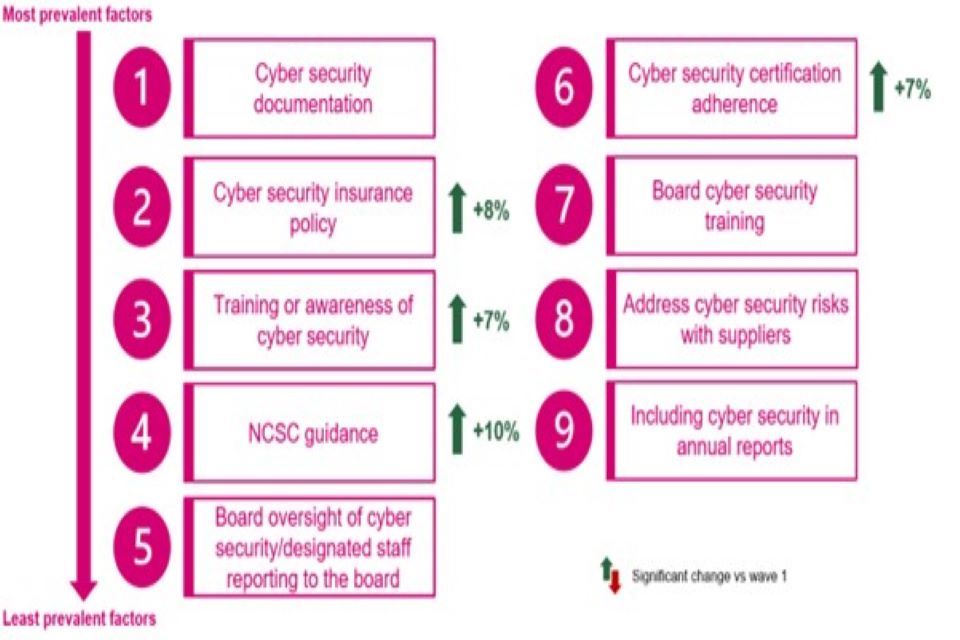

Executive summary – key findings

The Cyber Security Longitudinal Survey (CSLS) aims to better understand cyber security policies and processes within medium and large businesses and high-income charities, and to explore the links over time between these policies and processes and the likelihood and impact of a cyber incident.

This is the second research year (or wave) of a three-year study, and therefore this report includes comparisons with CSLS Wave One in 2021, as well as descriptive findings for all businesses and charities interviewed in Wave Two and summaries specific to organisations interviewed in both waves. Further insight into longitudinal trends in the findings will be available in the Wave Three report, upon completion of the three-year study. The main stage survey for Wave Two took place between 8 April and 28 June 2022. Qualitative interviews took place between June and July 2022.

This report also summarises additional insight from 30 follow-up qualitative interviews with survey respondents, that covered topics such as cyber security resilience, awareness and usage of the Cyber Essentials standard, record keeping, internal and external reporting, responsibility for cyber security, and monitoring of supply chains. These are intertwined with reporting on quantitative findings.

Overall, the cyber resilience profile of organisations continues to vary between businesses and charities as well as by business size and sector. Businesses are more likely than charities to have formal, written cyber security policies and processes in place. Large businesses (250+ staff), and particularly very large businesses (500+ staff), demonstrate greater cyber maturity compared to medium businesses and charities. However, overall, organisations’ approach to cyber is likely to be more reactive than proactive, with many struggling to get senior level buy-in to improve their cyber defences. Below is a more detailed summary of key findings from each chapter of this report.

The survey results are subject to margins of error, which vary with the size of the sample and the percentage figure concerned. For all percentage results, subgroup differences by size, sector and survey answers have been highlighted only where statistically significant[footnote 1] [footnote 2] (at the 95% level of confidence).

Cyber profile of organisations

In the last few years, technology has dramatically changed the way that people work, ranging from remote working through to the use of cloud storage. In response, organisations have had to adapt to these changing needs and consider the ways that cyber security requirements have changed in this new environment. To understand some of the ways that larger organisations have changed, a selection of new technologies were included in this survey.

An organisation’s cyber profile refers to the organisation’s baseline set of minimal cyber security requirements for mitigating described threats and vulnerabilities. As in Wave One (2021), almost all businesses and charities (98% and 97% respectively) use a cloud-based or physical server to store data or use a virtual private network (VPN) that allows staff to connect remotely.

Around eight in ten businesses (82%) and charities (75%) with a VPN require their staff to use it when accessing the organisation’s network or files from outside the workplace. These figures are in line with the Wave One survey. The requirement is most strongly enforced among businesses that have a specific cyber security insurance policy.

Although more businesses use physical than cloud-based servers, the opposite is true among charities, where there remains greater adoption of cloud-based data storage. Eight in ten charities store data or files in the cloud.

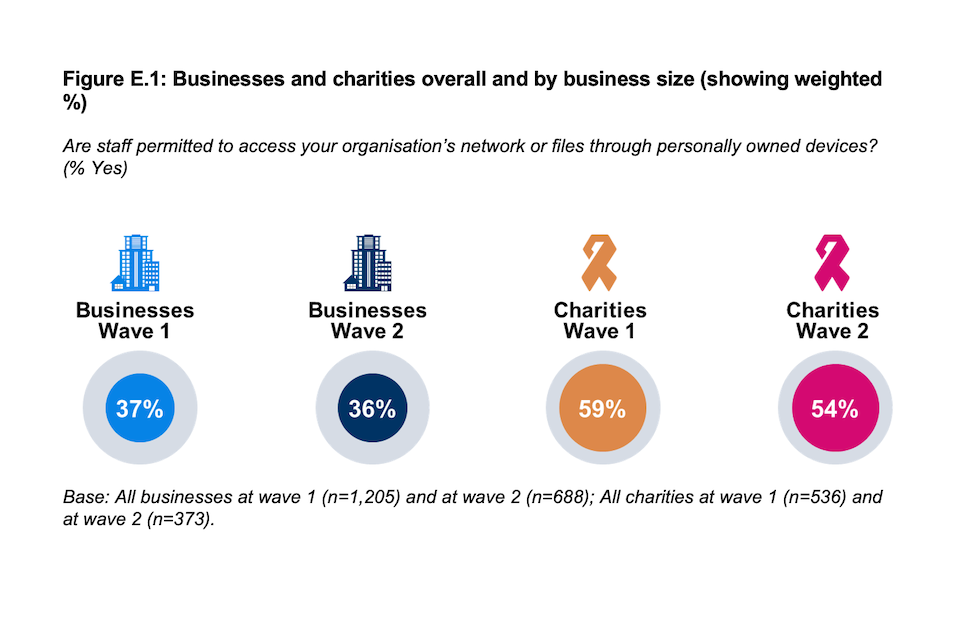

Businesses employ more controls than charities in terms of how staff access their network when working remotely. A majority of charities (54%) allow access via personally owned devices, compared to around one in three businesses (36%). Both figures are similar to the baseline survey (59% and 37% respectively).

Figure E.1: Businesses and charities overall and by business size (showing weighted %)

Are staff permitted to access your organisation’s network or files through personally owned devices? (% Yes)

Are staff permitted to access your organisation’s network or files through personally owned devices? (% Yes.) Businesses wave one: 37%; Businesses wave two: 36%; Charities wave one 59%; Charities wave two 54%.

Base: All businesses at wave 1 (n=1,205) and at wave 2 (n=688); All charities at wave 1 (n=536) and at wave 2 (n=373).

Although correlation does not mean causation, the higher the proportion that allow staff to access their network via personal devices the more likely an organisation is to report a data security incident. This relationship is most evident within charities.

Cyber security policies

This chapter investigates the cyber security policies of businesses and charities. Monitoring changes to these policies over time helps us better understand how organisations are evolving their cyber defences. The chapter also helps explore the impact this may have on organisations’ resilience to incidents.

There has been an increase in the proportion of organisations adopting a more rigorous approach to cyber security. For both businesses and charities there is generally more documentation, greater uptake of specific cyber security insurance and more training of ‘non-specialist’ staff.

Approximately nine in ten organisations (86% of businesses and 91% of charities) have in place at least one of the five documents considered part of an effective cyber security strategy (see Figure 3.1 for more information). While this is almost identical to the Wave One share for charities (92%), it represents an increase among businesses (82% in Wave One).

In the last twelve months approximately six in ten businesses (58%) and charities (62%) have delivered cyber security training or awareness raising sessions specifically for staff and/or volunteers who are not directly involved in cyber security. Both shares represent an increase from the baseline survey (48% and 55% respectively).

Cyber security processes

This chapter provides insight on the uptake of cyber security certifications by organisations. It also explores the cyber security processes that organisations have in place, the technical controls required to attain Cyber Essentials certification, and actions taken over the last twelve months to improve or expand various aspects of organisations’ cyber security.

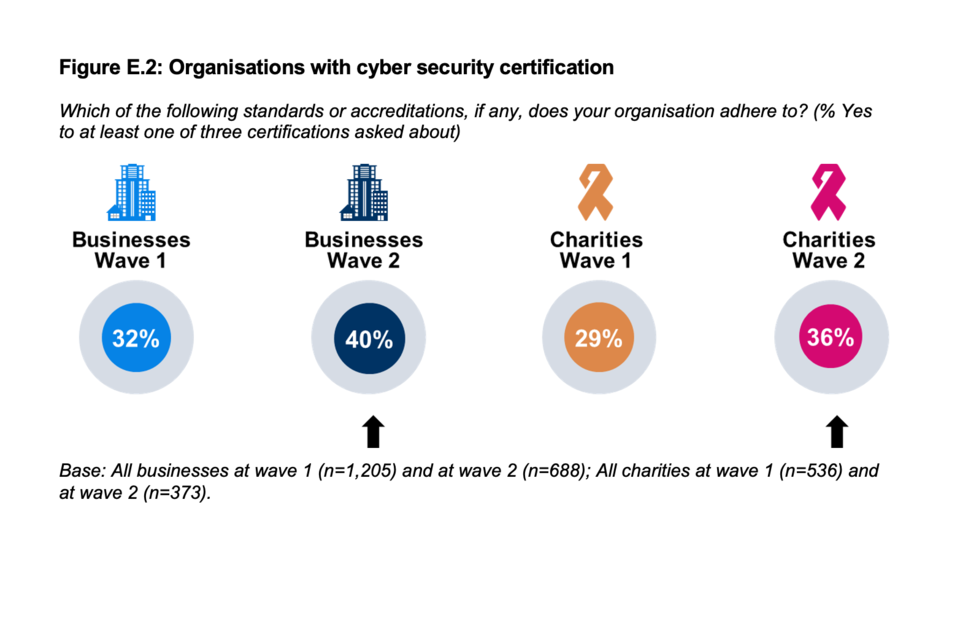

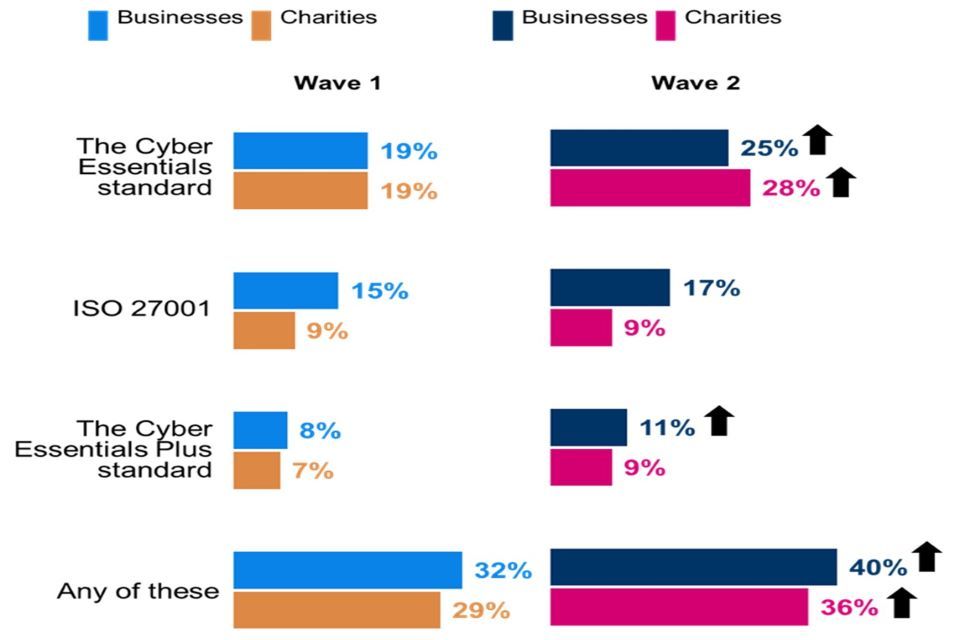

Compared to Wave One, more businesses (40% vs. 32%) and charities (36% vs. 29%) are certified to at least one of three certifications asked about (the Cyber Essentials standard, Cyber Essentials Plus standard and ISO 27001). The Cyber Essentials standard is most often adhered to by businesses (25%) and charities (28%) with both shares higher than in Wave One.

Figure E.2: Organisations with cyber security certification

Which of the following standards or accreditations, if any, does your organisation adhere to? (% Yes to at least one of three certifications asked about)

Organisations with cyber security certification. Businesses wave one: 32%; Businesses wave two: 40%; Charities wave one 29%; Charities wave two 36%.

Base: All businesses at wave 1 (n=1,205) and at wave 2 (n=688); All charities at wave 1 (n=536) and at wave 2 (n=373).

Even if they have not been Cyber Essentials certified, six in ten businesses (61%) and charities (58%) operate all five of the technical controls required to attain the Cyber Essentials standard. These figures are similar to the baseline survey.

Outside of the technical controls required to attain Cyber Essentials certification, most organisations have specific rules for storing and moving files containing people’s personal data (85% of businesses, 86% of charities), backing up data securely via a cloud device (75% vs. 85%), backing up data by other means (70% vs. 63%) and monitoring user activity (66% vs. 64% respectively). These findings were in line with the previous year. Charities are more likely than in Wave One and more inclined than businesses to securely back up data via a cloud service.

While the proportion has increased from Wave One, it remains the case that only around one in five businesses (19%) include cyber security in their annual reports. A similar proportion of charities (18%) do this, which is almost identical to Wave One.

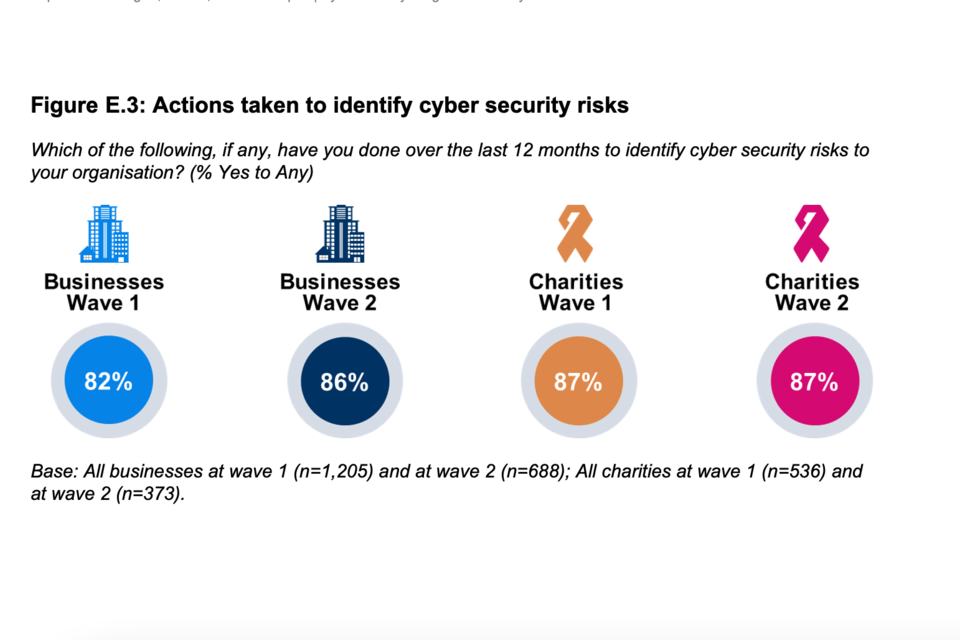

Reflecting the findings of the baseline survey, almost nine in ten organisations (86% of businesses and 87% of charities) continue to take at least one action to identify the cyber security risks their organisation faces. One in five (21% of businesses and 19% of charities) report taking all four measures which is also in line with the Wave One survey. Medium-sized businesses show less willingness to take steps to identify cyber security risks and are half as likely as large businesses to have taken all four steps (18% vs. 37%).

Figure E.3: Actions taken to identify cyber security risks

Which of the following, if any, have you done over the last 12 months to identify cyber security risks to your organisation? (% Yes to Any)

Actions taken to identify cyber security risks. Businesses wave one: 82%; Businesses wave two: 86%; Charities wave one 87%; Charities wave two 87%.

Base: All businesses at wave 1 (n=1,205) and at wave 2 (n=688); All charities at wave 1 (n=536) and at wave 2 (n=373).

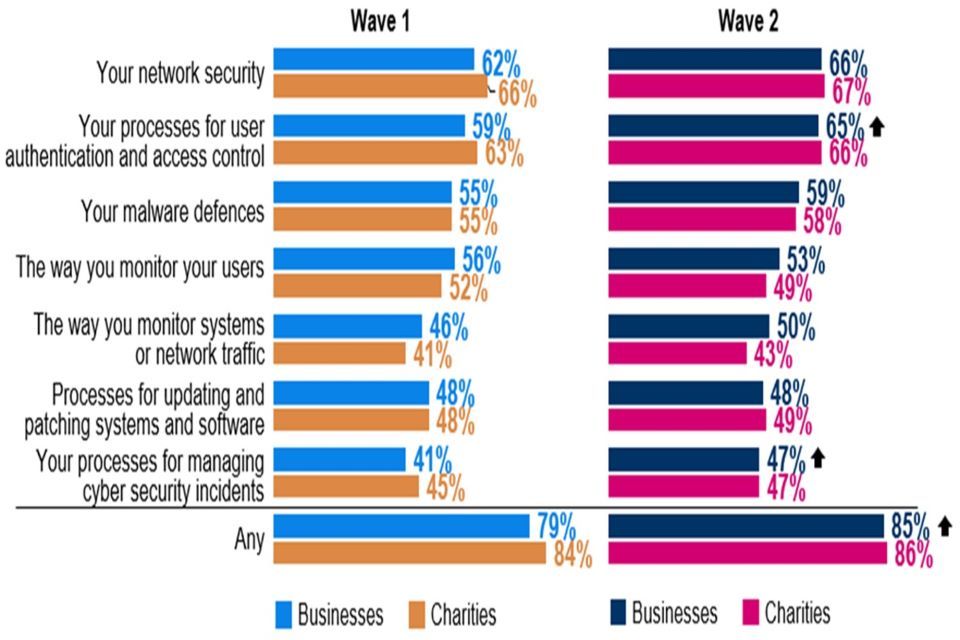

The majority of both businesses and charities took steps to improve their cyber defences and over the past twelve months, almost nine in ten businesses (85%) and charities (86%) have taken at least one action to expand or improve an aspect of their cyber security. For businesses this represents an increase from Wave One (79%). Charities are equally as likely as businesses to have made efforts to expand or improve aspects of their cyber security although they are less likely than businesses to have strengthened the way they monitor systems or network traffic.

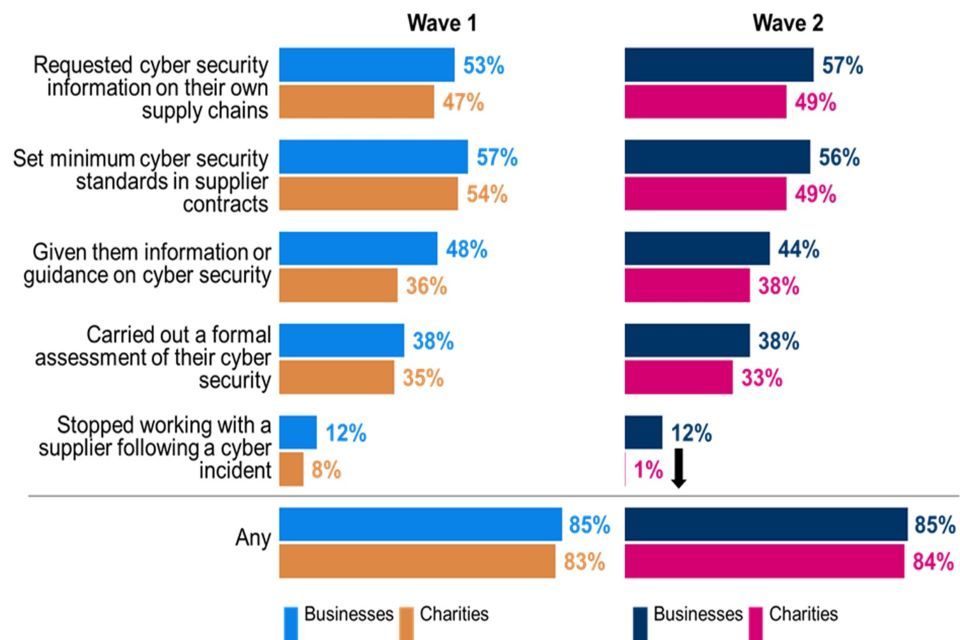

Fewer than three in ten businesses (26%) or charities (28%) have formally addressed the potential cyber security risks associated with their suppliers/ partners. These findings were in line with the baseline survey.

Board involvement

This chapter investigates the level of awareness and engagement with cyber security among board members, including any training received and its frequency.

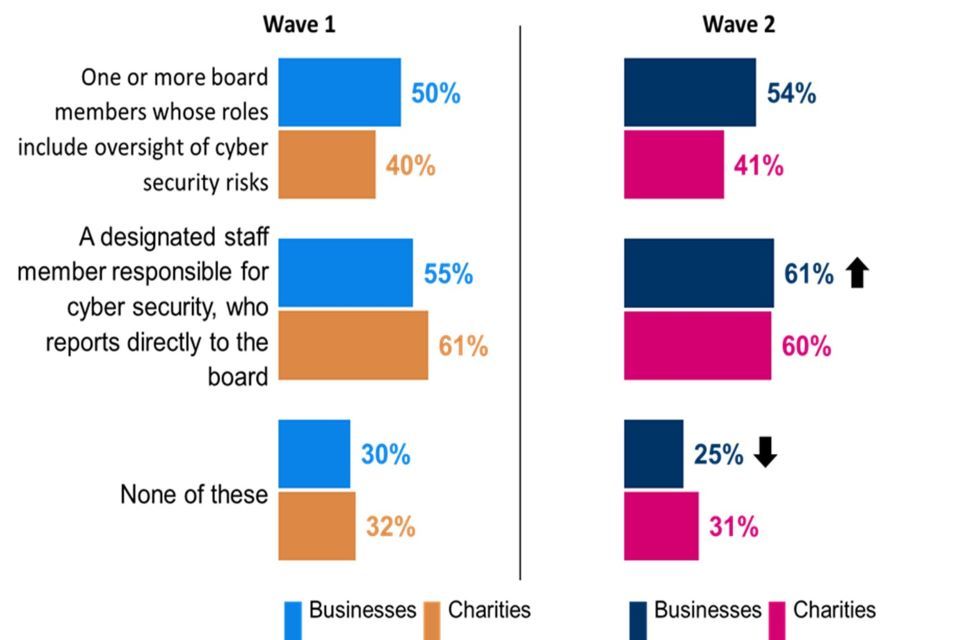

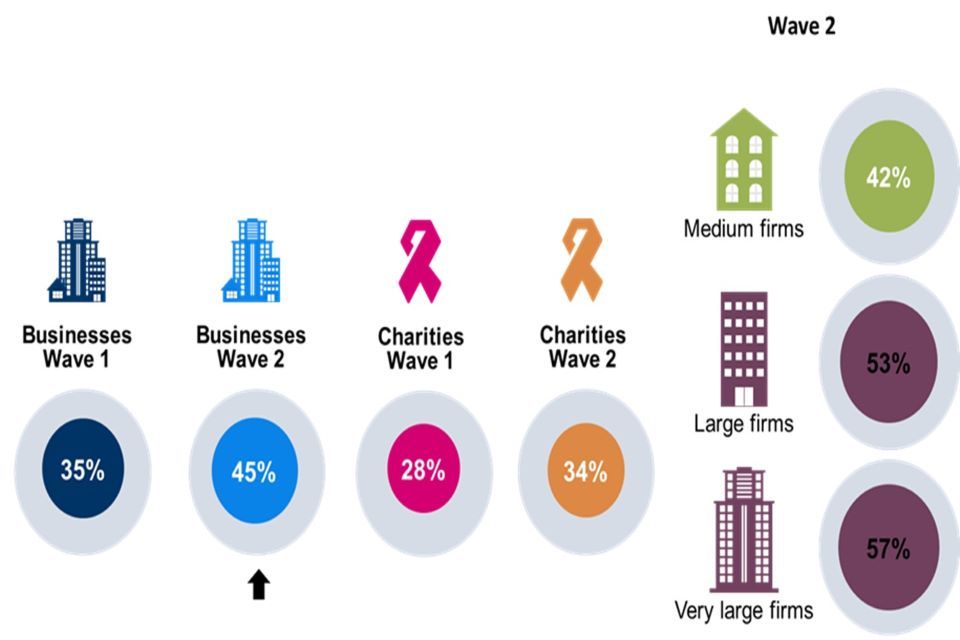

More businesses than charities have board oversight of cyber security risks (54% vs. 41%). In neither type of organisation has there been a change since Wave One in the proportion reporting a board member with specific responsibility for cyber security matters.

Six in ten businesses (61%) and charities (60%) have a designated staff member responsible for cyber security, who reports directly to the board. For businesses this represents an increase (from 55% in Wave One).

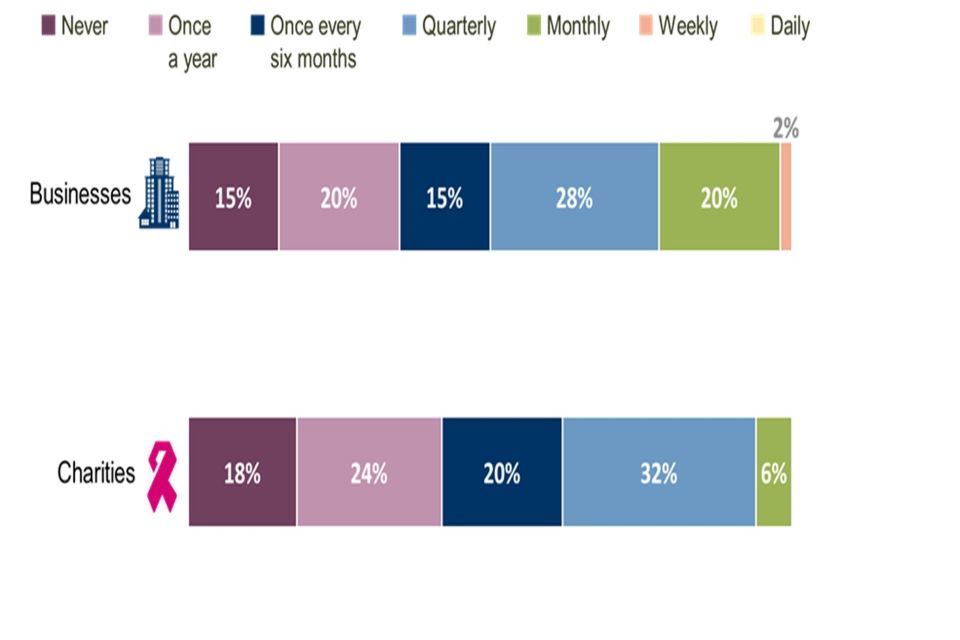

Around half of businesses (49%) say their board discusses cyber security at least quarterly (when don’t know responses are excluded). This is higher than among charities (38%), as was the case in Wave One. These findings were in line with the previous year. Around one in six businesses (15%) and charities (18%) report that their board never discussed or received updates on cyber security over the last twelve months (again excluding don’t know responses), broadly in line with the baseline findings (19% of businesses and 20% of charities.)

It continues to be the case that board members have received cyber security training in fewer than half of organisations (45% of businesses and 34% of charities). However, for businesses this represents an increase from 35% in Wave One. Further, at least one member of the boards of businesses that have received a security certification are more likely to have received some training (65% of businesses adhering to ISO 27001, 66% of businesses that are adhering to Cyber Essentials Plus). This is almost double the proportion of businesses with no training (36%).

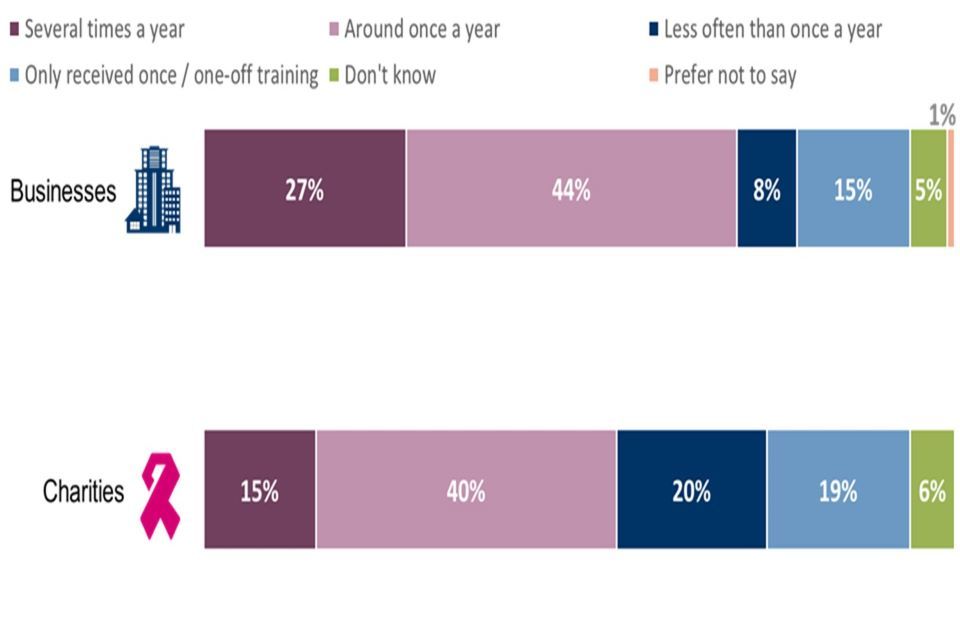

Where board members do receive cyber security training, this tends to happen no more than once a year. Around one quarter of businesses (23%) and almost four in ten charities (39%) report the training as being a one-off or less than once a year. Taken together the data suggest that senior level training is not widespread, nor delivered on a frequent basis.

Sources of information

This chapter discusses the use of information or guidance from the National Cyber Security Centre (NCSC) by businesses and charities[footnote 16]. It goes on to discuss the extent to which various stakeholders influence organisations’ policies and processes related to cyber security.

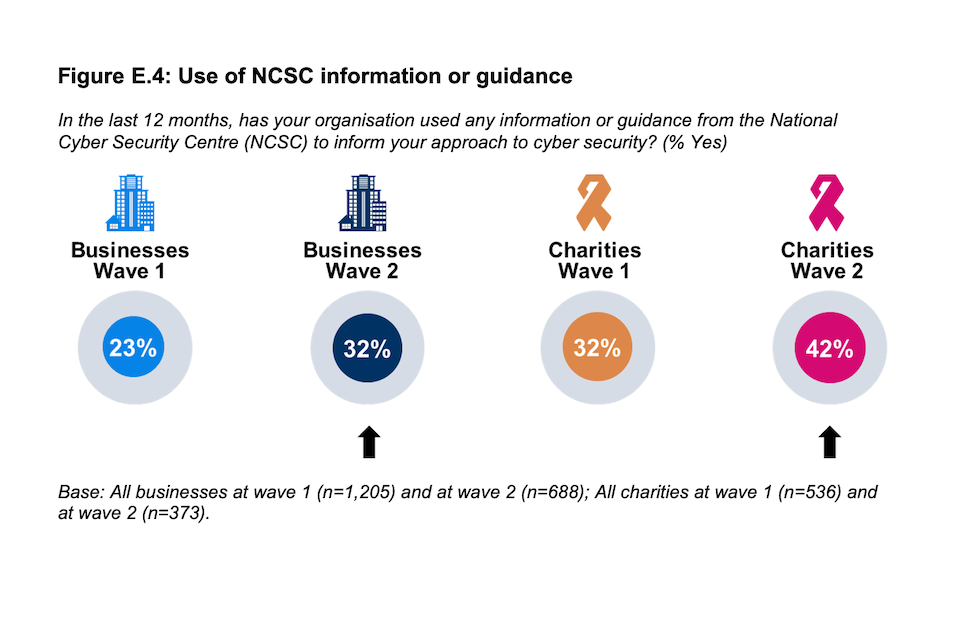

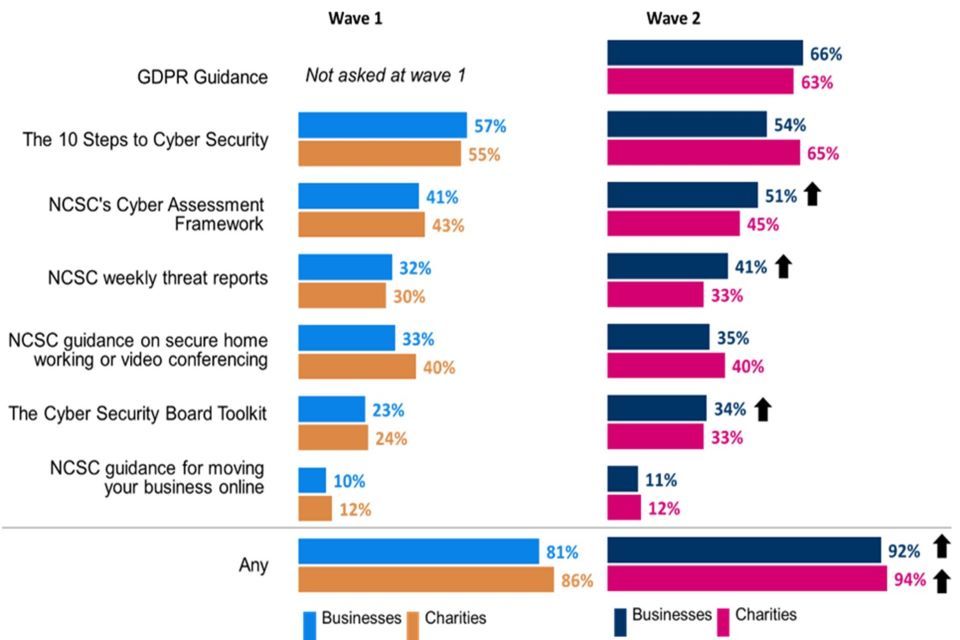

Around one in three businesses (32%) have used information or guidance from the NCSC in the last year, up from 23%) in Wave One. A similar increase is reported by charities (from 32% to 42%). Usage of the NCSC guidance is higher among those that have experienced a cyber security incident (38% usage among those that have experienced a cyber security incident vs 20%).

Figure E.4: Use of NCSC information or guidance

In the last 12 months, has your organisation used any information or guidance from the National Cyber Security Centre (NCSC) to inform your approach to cyber security? (% Yes)

Use of NCSC information or guidance. Businesses wave one: 23%; Businesses wave two: 32%; Charities wave one 32%; Charities wave two 42%.

Base: All businesses at wave 1 (n=1,205) and at wave 2 (n=688); All charities at wave 1 (n=536) and at wave 2 (n=373).

Among organisations that have used NCSC guidance, GDPR guidance is the most common type of information used by both businesses (66%) and charities (63%). Businesses are more likely to have used the Cyber Assessment Framework, weekly threat reports and Cyber Security Board Toolkit than they were in Wave One.

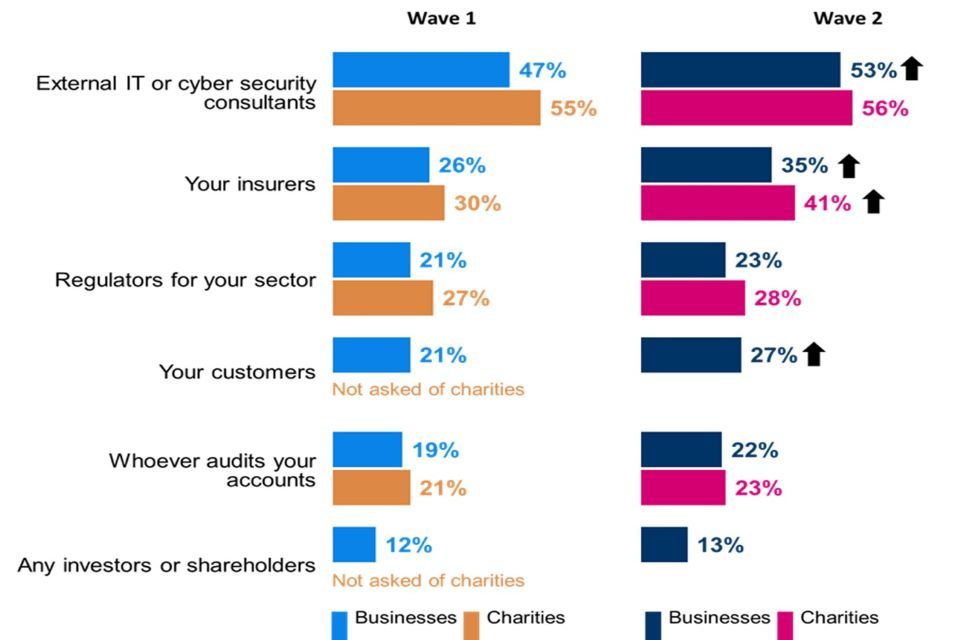

External IT or cyber security consultants are the greatest external influence on the cyber security actions of both businesses (53%, up from 47% in Wave One) and charities (56%, consistent with Wave One). Insurers are the next largest influence on both types of organisations (35% of businesses; 41% of charities) and to a greater degree (up from 26% of businesses and 30% of charities in Wave One).

Businesses are more likely to have reviewed or changed their cyber security processes or policies as a result of another organisation in their sector experiencing a cyber security incident (16%) than as a result of another organisation implementing a similar measure (10%). The same applies to charities (20% vs. 14%). These findings are all consistent with Wave One.

Cyber incident management

This chapter captures the proportion of organisations that have written processes for cyber security incident management and what these may cover.

While the majority of organisations (businesses and charities) document processes for managing cyber security incidents, almost four in ten do not. Documentation of incident management is particularly prevalent among very large businesses with 500+ employees (71%). This is in line with findings from Wave One.

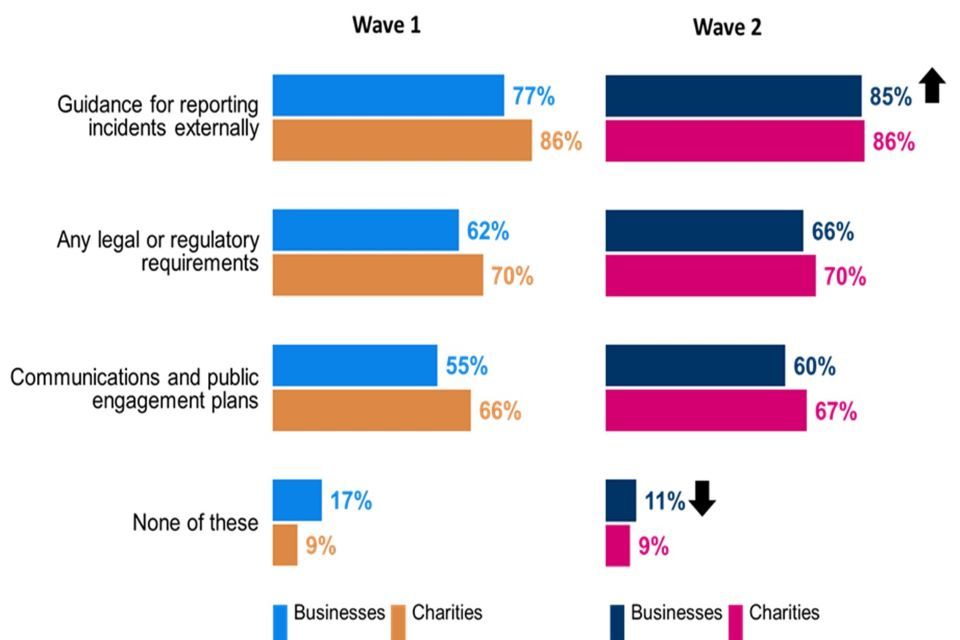

Among those businesses with written incident management processes, almost nine in ten (85%) include guidance for reporting incidents externally, for instance to regulators or insurers. This represents an increase from Wave One (77%).

The content of charities’ written incident management processes is very similar to that of businesses. For example, almost nine in ten charities with written processes (86%) include guidance for reporting incidents externally. The elements of charities’ incident management processes are almost identical to those reported in Wave One.

The overall incidence of such processes has not increased substantially since the baseline survey, and where processes are in place they tend to be treated as passive rather than dynamic tools. Relatively few organisations that have them in place (43% of businesses and 33% of charities) carry out exercises to test their efficacy.

Prevalence and impact of cyber security incidents

This chapter looks at the different kinds of cyber incidents experienced by organisations and their impact and outcome.

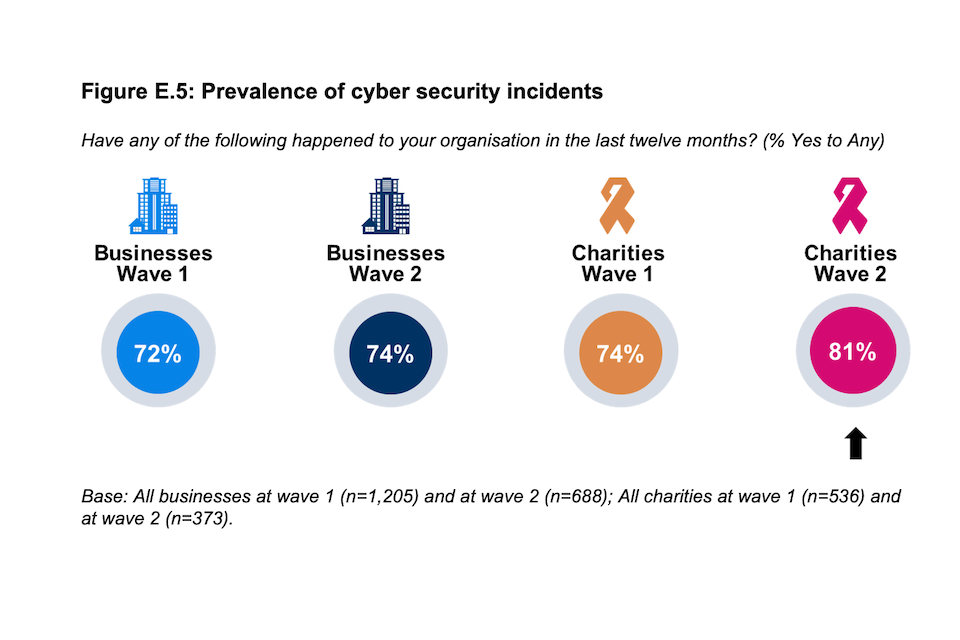

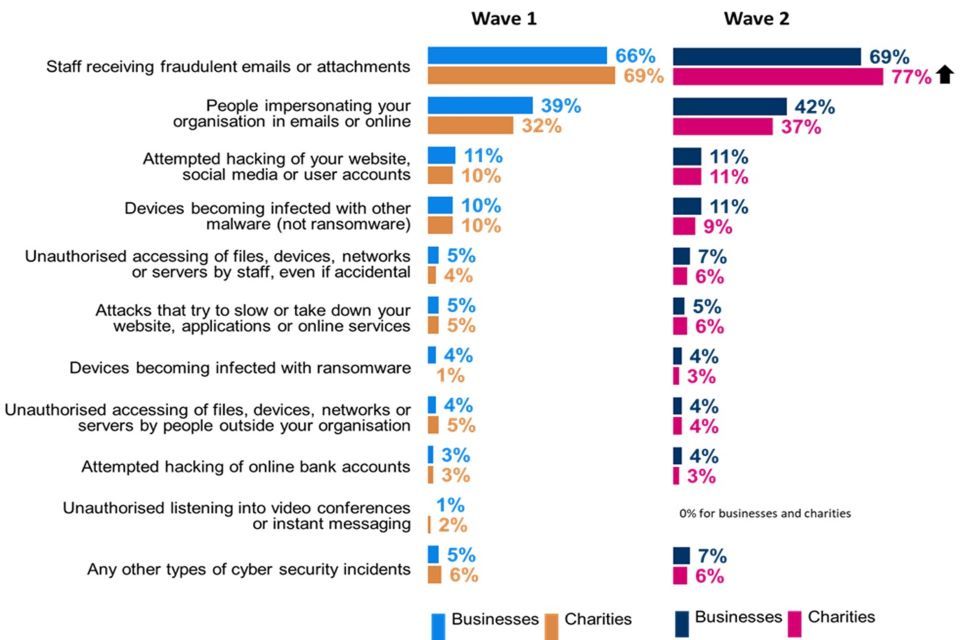

More charities report cyber security incidents in general (81%, up from 74% in Wave One) and phishing attacks (77%, up from 69% in Wave One). There are no notable changes among businesses.

Figure E.5: Prevalence of cyber security incidents

Have any of the following happened to your organisation in the last twelve months? (% Yes to Any)

Prevalence of cyber security incidents. Businesses wave one: 72%; Businesses wave two: 74%; Charities wave one 74%; Charities wave two 81%.

Base: All businesses at wave 1 (n=1,205) and at wave 2 (n=688); All charities at wave 1 (n=536) and at wave 2 (n=373).

The frequency of cyber security incidents reported is consistent with Wave One – i.e., incidents are occurring with the same degree of frequency as reported in the baseline survey.

If phishing attacks are excluded from the analysis, the proportion of businesses experiencing cyber security incidents at least monthly has increased (from 53% to 60%).

The proportion of organisations that have been negatively impacted by cyber security incidents has remained constant (22% of businesses and 26% of charities experiencing at least one such incident in the last twelve months).

Among both businesses and charities, the wider organisational impact of cyber security incidents is almost identical to that recorded in Wave One.

Businesses (47%) are now more likely to have an established rule or policy not to make ransomware payments, both when compared to Wave One (an increase from 41%) and charities (39% in Wave Two, unchanged from 40% in Wave One).

Importantly, organisations that adhere to one or more cyber security certifications are more likely to report having experienced a cyber security incident. Four in five businesses (81%) adhering to the Cyber Essentials Plus standard experienced a phishing incident in the last year compared to 68% of businesses not adhering to any certifications. Additionally, nearly six in ten (57%) businesses adhering to the Cyber Essentials Plus standard say people impersonated their organisation in emails or online, compared to 41% of businesses not adhering to any certifications.

This would suggest that the organisations could be responding to threats to their cyber security by seeking to bolster their resilience through the certification. However, it is important to be cautious with this finding. It is also possible that the organisations that have achieved the Cyber Essentials certification have improved their monitoring protocols ensuring that they are to detect these attacks more effectively. Further, it is also a possible that organisations that are more likely to be exposed to a threat are also more likely to be aware of cyber security and these organisations therefore more likely to have acquired a Cyber Essentials certificate. As a result of this, pulling apart the correlations is difficult.

Glossary

| Term | Definition |

|---|---|

| Baseline survey | Also see the Wave One survey. The first research year of the survey that took place. |

| Cloud computing | Cloud computing uses a network of external servers accessed over the internet, rather than a local server or a personal computer, to store or transfer data. This could be used, for example, to host a website or corporate email accounts, or for storing or transferring data files. |

| Cyber security | Cyber security includes any processes, practices or technologies that organisations have in place to secure their networks, computers, programs or the data they hold from damage, attack or unauthorised access. |

| Cyber attack | A cyber attack is a malicious and deliberate attempt by an individual or organisation to breach the information system of another individual or organisation. |

| Cyber profile | A cyber profile is a baseline set of minimal cyber security requirements for mitigating described threats and vulnerabilities, as well as supporting compliance requirements for a defined scope and type of a particular use case (e.g., industry, information system(s)), using a combination of existing cyber security guidance, standards and/or specifications baseline documents or catalogues. |

| Impact | A negative impact on organisations did not have to involve a material loss. This could be issues relating to staff disruption or implementing new measures in the organisation. |

| Large business | Businesses with 250 employees or over |

| Longitudinal Survey | A longitudinal survey is a research design that involves repeated observations of the same variables (e.g., people or businesses) over short or long periods of time |

| Malware | Malware (short for “malicious software”) is a type of computer program designed to infiltrate and damage computers without the user’s consent (e.g., viruses, worms, Trojan horses etc). |

| Managed Service Provider (MSP) | A supplier that delivers a portfolio of IT services to business customers via ongoing support and active administration, all of which are typically underpinned by a Service Level Agreement. A Managed Service Provider may provide their own Managed Services or offer their own services in conjunction with other IT providers’ services. |

| Medium business | Businesses with 50 to 249 employees |

| Outcome | A negative outcome of an attack involved a material loss from an organisation, such as a loss of money or data. |

| Patch management | Having a policy to apply software security updates within 14 days of them being released |

| Penetration testing | Penetration testing is where staff or contractors try to breach the cyber security of an organisation on purpose, in order to show where there might be weaknesses in cyber security. |

| Personally-owned devices | Personally-owned devices are things such as smartphones, tablets, home laptops, desktop computers or USB sticks that do not belong to the company, but might be used to carry out business-related activities. |

| Phishing | Fraudulent attempts to extract important information, such as passwords, from staff with infiltration through a link or attachment sent via email. |

| Ransomware | A type of malicious software designed to block access to a computer system until a sum of money is paid. |

| Removable devices | Removable devices are portable things that can store data, such as USB sticks, CDs, DVDs etc. |

| Restricting IT admin and access rights | Restricting IT admin and access rights is where only certain users are able to make changes to the organisation’s network or computers, for example to download or install software. |

| Security breach | A security breach is any incident that results in unauthorised access of data, applications, services, networks and/or devices by bypassing their underlying security mechanisms. |

| Smart devices | Network connected devices, like personal assistants, locks, alarms, or thermostats. |

| Social engineering | Fraudulent attempts to extract important information, such as passwords, from staff with infiltration through an impersonation attempt of the organisation. |

| Threat intelligence | Threat intelligence is where an organisation may employ a staff member or contractor or purchase a product to collate information and advice around all the cyber security risks the organisation faces. |

| Two-Factor Authentication | Two-Factor, or Multi-Factor, Authentication is an electronic authentication method in which a user is granted access to a network or application only after successfully presenting two or more pieces of evidence to an authentication mechanism (e.g., a password and a one-time passcode). |

| Wave One Survey | Also see Baseline survey. The first research year of the survey that took place. |

Chapter 1- Introduction

1.1 Background to the research

Publication date: 2022

Geographic coverage: United Kingdom

The Department for Digital, Culture, Media and Sport (DCMS) commissioned the Cyber Security Longitudinal Survey of medium and large UK businesses (50+ employees) and high-income charities (annual income of more than £1m) as part of the National Cyber Security Programme. The findings will evaluate long-term links between the cyber security policies and processes adopted by these organisations, and the likelihood and impact of a cyber incident. It also supports the Government to shape future policy in this area, in line with the National Cyber Strategy 2022, and will inform future government cyber interventions and support future strategies with quality evidence.

There will be three annual waves of this study overall. Due to the longitudinal nature of the study, the aim is to track trends over time and speak largely with the same organisations in each wave. This report is based on Wave Two (2022) data that begins to provide longitudinal analysis when compared to the Wave One (2021) baseline data. The design of this research was influenced by a study DCMS previously commissioned to investigate the feasibility of creating a new longitudinal study of large organisations.

The core objectives of this study are to:

- Explore how and why UK organisations are changing their cyber security profile and how they implement, measure, and improve their cyber defences

- Provide a more in-depth picture of larger organisations, covering topics that are lightly covered in the Cyber Security Breaches Survey (CSBS), such as corporate governance, supply chain risk management, internal and external reporting, cyber strategy and cyber insurance

- Explore the effects of actions adopted by organisations to improve their cyber security on the likelihood and impact of a cyber incident

1.2 Difference from the Cyber Security Breaches Survey

This study differs from the CSBS in multiple important respects. Firstly, it uses a longitudinal approach, where the aim is to track changes in cyber resilience over time, whereas the CSBS uses a cross-sectional sample that provides a snapshot of cyber resilience. This three-year longitudinal study collects data from the same unit (businesses or charities) on more than one occasion, to analyse the link between large and medium organisations’ cyber security behaviours and the extent to which they influence the impact and likelihood of experiencing an incident over time. In comparison, results from CSBS track changes over time, and provides a static view of cyber resilience at a given time.

Secondly, this survey focuses only on medium, large and very large businesses, and high-income charities whereas the CSBS includes all businesses (micro, small, medium, and large), all charities, and educational institutions. Additionally, different questions are used, so while there are some similarities in the questions and topics covered by the two surveys, results are not comparable. Finally, as previously discussed, the two studies have different objectives.

The CSBS is an official government statistic, and representative of all UK businesses, charities, and educational institutions. Therefore, for overall statistics on cyber security, results from CSBS should be used. Further detail on overlapping questions can be found in the Cyber Security Longitudinal Survey Technical Report.

Please visit the gov.uk website to see publications of the Cyber Security Breaches Survey.

1.3 Methodology

There are two strands to the Cyber Security Longitudinal Survey:

- Ipsos undertook a random probability multimode[footnote 3] (telephone and online) survey covering 688 businesses and 373 UK registered charities between April and June 2022[footnote 4]. Of these, 883 interviews (83.2%) were completed via telephone and 178 interviews (16.8%) were completed through the online option. The data for businesses and charities have been weighted to be statistically representative of these two populations.

- Subsequently, 30 in-depth interviews were conducted in July and August 2022, to gain further qualitative insights from some of the organisations that participated in the quantitative survey.

This longitudinal study aims to track changes over time, so follows the same organisations in all three annual waves. In Wave One, 1,404 organisations (955 businesses and 450 charities) agreed to be recontacted in Wave Two. Around half (674 completed interviews with repeat organisations) of these were retained for Wave Two (2022). This constitutes the majority of completed interviews; 70% of businesses interviewed in Wave Two were also interviewed in Wave One, and the same applies to 64% of charities. To supplement the longitudinal panel sample, 387 interviews were completed from a fresh (or top-up) cross-sectional sample.

The Wave Two sample included eleven interviews with businesses that were eligible (had 50 or more employees) in Wave One but had dropped below this figure in Wave Two.

To avoid possible selection bias, the ‘fresh’ business sample was selected using random probability sampling. The business sample was proportionally stratified by region, and disproportionately stratified by size and sector. More technical details and a copy of the questionnaire are available in the separately published Technical Annex.

Profile of survey respondents

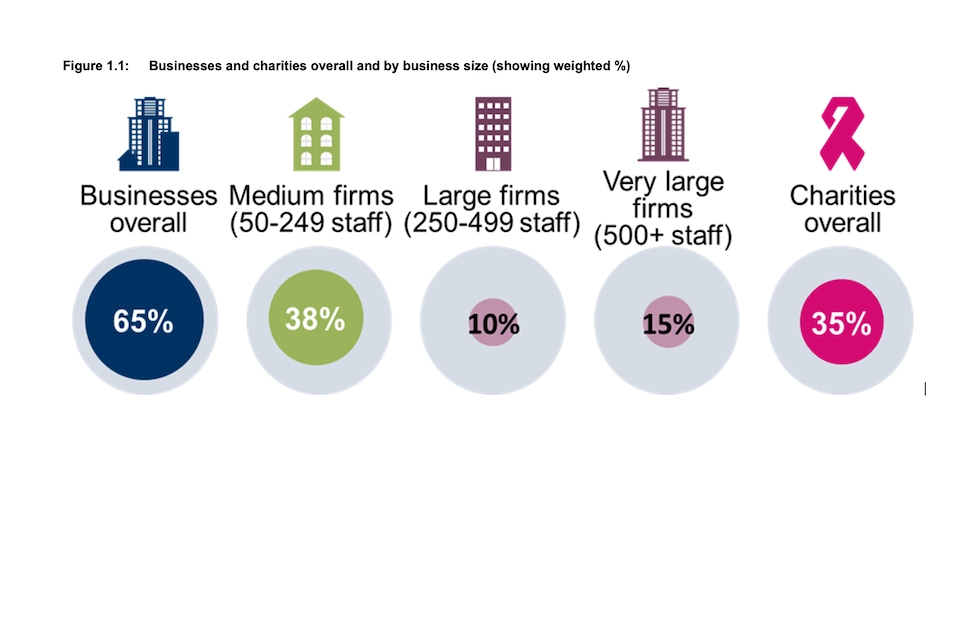

Figure 1.1 Businesses and charities overall and by business size (showing weighted %)

Figure 1.1 Businesses and charities overall and by business size

Base: All businesses (n=688); Medium firms (n=408); Large firms (n=108); Very large firms (n=160), includes 11 panel businesses confirmed as eligible in Wave One but now with fewer than 50 employees and one panel business that could not confirm their current number of employees; All charities (n=373).

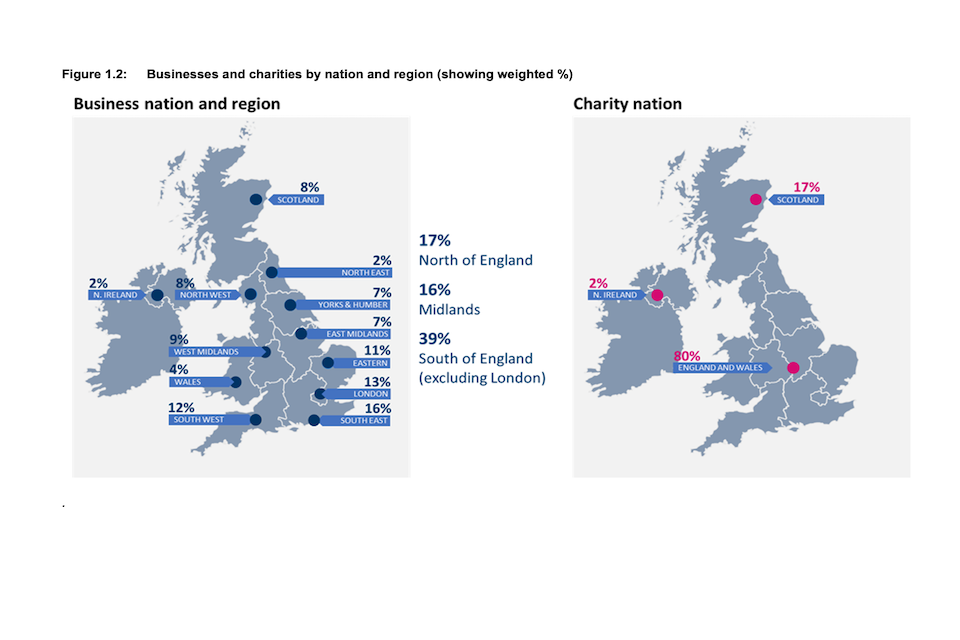

Figure 1.2 Businesses and charities by nation and region (showing weighted %)

Figure 1.2: Businesses and charities by nation and region

Base: All businesses (n=688); All charities (n=373). Businesses in East Midlands (n=50); Eastern England (n=73); London (n=92); North East (n=12); North West (n=58); Northern Ireland (n=13); Scotland (n=54); South East (n=113); South West (n=85); Wales (n=27); West Midlands (n=63); Yorkshire and Humber (n=48); Charities in England and Wales (n=300); Northern Ireland (n=8); Scotland (n=65).

Figure 1.3 Businesses by sector (showing weighted %)

| Utilities and production | 18% |

| Administration and real estate | 15% |

| Retail and wholesale | 15% |

| Health, social care and social work | 9% |

| Professional, scientific and technical | 9% |

| Food and hospitality | 8% |

| Construction | 7% |

| Information and communications | 6% |

| Transport and storage | 5% |

| Finance and insurance | 4% |

| Education | 3% |

| Entertainment, service and membership organisations | 2% |

Base: All businesses (n=688); Administration and real estate (n=100); Construction (n=43); Education (n=17); Entertainment, service and membership organisations (n=19); Finance and insurance (n=28); Food and hospitality (n=63); Health, social care and social work (n=61); Information and communications (n=53); Professional, scientific and technical (n=45); Retail and wholesale (n=101); Transport and storage (n=35); Utilities and production (n=123)

Profile of qualitative respondents

Thirty follow-up interviews were carried out with representatives of organisations covered by the survey. They were selected in order to provide the following profile:

Table 1.1 Profile of qualitative respondents

| Category | Definition | Achieved |

|---|---|---|

| Type | Businesses | 20 |

| Charities | 10 | |

| Size (employees): Businesses only | Medium (50-249) | 8 |

| Large (250-499) | 6 | |

| Very large (500+) | 6 | |

| Sector: Businesses only | Broad mix of sectors | 20 |

| Region: Businesses only | Broad mix of regions | 20 |

Cyber roles and responsibilities

Where possible both the survey and follow-up qualitative interviews were addressed to the person at each organisation with greatest responsibility for cyber security. However, in many organisations there is nobody with specific responsibility for cyber security so, in these cases, interviews were completed with representatives that took responsibility for various aspects of IT and data security. This was particularly the case within organisations that do not have an in-house IT department.

There are variations by sector but in general large businesses (especially ‘very large’ enterprises) are the most likely to have employees with dedicated IT roles and they tend to have larger IT teams. This can be the case for many medium-sized businesses and charities, but often these smaller organisations fully outsource the management of IT and cyber security. This is in line with research from the 2022 Cyber Security Labour Market survey, which also found that medium and large businesses are the most likely to employ staff in dedicated cyber security related roles, rather than in general IT roles in which cyber security may not be their only or top priority.

Respondents with a general, or less technically specific role, tended to have lower awareness of cyber security issues. Meanwhile people at organisations where the cyber security role is combined with other responsibilities are often stretched. As a result, they may not be able to give cyber security matters as much attention as they would like.

1.4 Interpretation of findings

The survey results are subject to margins of error, which vary with the size of the sample and the percentage figure concerned. For all percentage results, subgroup differences by size, sector and other survey answers have only been highlighted where they are statistically significant[footnote 5] (at the 95% level of confidence).

There is a guide to statistical reliability at the end of this report.

Subgroup definitions and conventions

For the purposes of analysis, businesses are divided into medium (50-249 employees) and large enterprises (250+ employees).[footnote 6] In turn large businesses consist of both large (250-499 employees) and very large businesses (500+ employees). All charities included in the survey have a reported annual income of at least £1 million according to national charity regulator sample data.[footnote 7]

Where figures are marked with an asterisk (*) these refer to base sizes smaller than 50 and should be treated with caution.

1.5 Acknowledgements

Ipsos and DCMS would like to thank all the organisations and individuals that participated in the survey. We would also like to thank the organisations that endorsed the fieldwork and encouraged businesses and charities to participate, including:

- The National Cyber Security Centre (NCSC)

- The Home Office

- The Scottish Government

- The Charity Commission

- The Confederation of British Industry (CBI)

- The Institute of Chartered Accountants in England and Wales (ICAEW)

Chapter 2- Cyber profile of organisations

In the last few years, technology has dramatically changed the way that people work, ranging from remote working through to the use of cloud storage. In response, organisations have had to adapt to these changing needs and consider the ways that cyber security requirements have changed in this new environment. To understand some of the ways that larger organisations have changed, a selection of new technologies were included in this survey.

This chapter summarises the extent to which organisations use various types of data storage and the ways in which employees are able to access data. It also outlines the extent to which businesses and charities deploy cyber security tools that use Artificial Intelligence (AI) or machine learning. The final section of the chapter provides insight from the qualitative interviews and covers organisations’ use of external IT suppliers or cyber security consultants.

The ways in which organisations currently store and allow access to data show minimal changes from those reported in Wave One:

- As in the baseline survey, almost every business and charity (98% and 97% respectively in this wave) has a cloud or physical server to store data or uses a virtual private network (VPN) that allows staff to connect remotely.

- While more prevalent among charities (54% vs. 36% of businesses), the proportion of organisations that allow staff to access their network or files through personally owned devices is in line with Wave One (59% of charities and 37% of businesses).

- The proportion of businesses (82%) and charities (75%) that require staff to use their VPN when remotely accessing data is similar to that recorded in the baseline survey (79% and 72% respectively).

- For both businesses (25%) and charities (17%), the proportion employing AI or machine learning within their cyber security tools is in line with the baseline survey (20% of businesses and 15% of charities).

2.1 Data storage and access

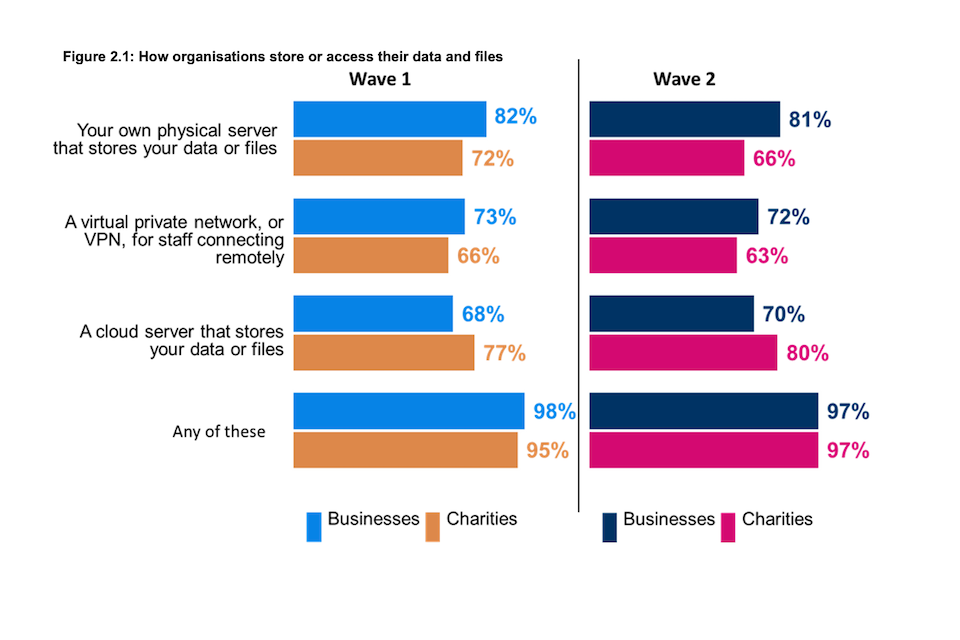

In response to their workforces’ changing needs businesses and charities have had to reconsider the ways in which their data is stored and accessed. The ways in which organisations store and access their data files are very similar to those observed in the baseline survey. As in Wave One, almost all businesses (98%) and charities (97%) have one or more of a cloud or physical server to store data or use a virtual private network (VPN) that allows staff to connect remotely.

Businesses remain more likely than charities to use physical servers (81% vs.66%). In contrast, charities are more likely than businesses to store data or files in the cloud (80% vs. 70%).

To help build cyber resilience given the rise of remote working and concerns around access of sensitive data, Virtual Private Networks (VPN) have become a critical part of organisations’ cyber security. The proportion of organisations, either businesses or charities, with a VPN that allows staff to connect remotely is almost the same as that recorded in the baseline survey. As in Wave One, around seven in ten (72%) businesses have a VPN, as compared to around six in ten charities (63%).

Figure 2.1: How organisations store or access their data and files

Does your organisation use or provide any of the following?

Figure 2.1: How organisations store or access their data and files

Base: All businesses at Wave 1 (n=1,205) and at Wave 2 (n=688); All charities at Wave 1 (n=536) and at Wave 2 (n=373). Don’t know not shown. Statistically significant changes between Wave 1 data and Wave 2 data are represented by an arrow.

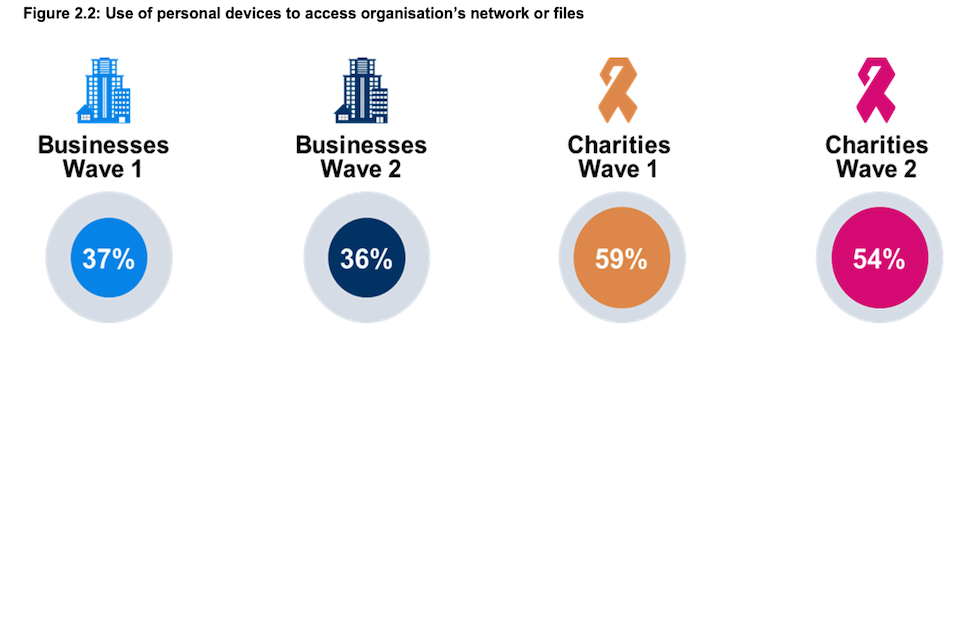

2.2 Use of personal devices to access organisation’s network or files

The pandemic led many organisations to review their remote working capabilities and ensuring that employees can access sensitive data securely has become an important organisational need.

As in the baseline survey, charities are more likely than businesses to allow staff to access their organisation’s network or files through personally owned devices. A majority of charities (54%) allow this compared to around one in three businesses (36%). Neither figure is significantly different from Wave One.

This pattern also applies when looking specifically at the longitudinal sample within this study (organisations taking part in both Wave One and Wave Two). The share of businesses within this group that permit their staff to access their business’s network or files through personally owned devices is 37% (vs. 41% in Wave One), and for charities it is 54% (vs. 61% in Wave One).

Although correlation does not mean causation, those organisations that allow staff to access their network via personal devices appear more likely to have experienced a data security incident in the past twelve months. Of those businesses that have experienced an incident (other than ‘phishing’) in the past twelve months, 42% allow network access via personal devices. Where no incidents are reported the corresponding share is 28%. Among charities the difference is even greater with six in ten (60%) of those experiencing an incident allowing personal device access. For those charities experiencing no incidents the figure is lower (37%).

Figure 2.2: Use of personal devices to access organisation’s network or files

Are staff permitted to access your organisation’s network or files through personally owned devices? (% Yes)

Figure 2.2: Use of personal devices to access organisation’s network or files

Base: All businesses at Wave 1 (n=1,205) and at Wave 2 (n=688); All charities at Wave 1 (n=536) and at Wave 2 (n=373). Statistically significant changes between Wave 1 data and Wave 2 data are represented by an arrow.

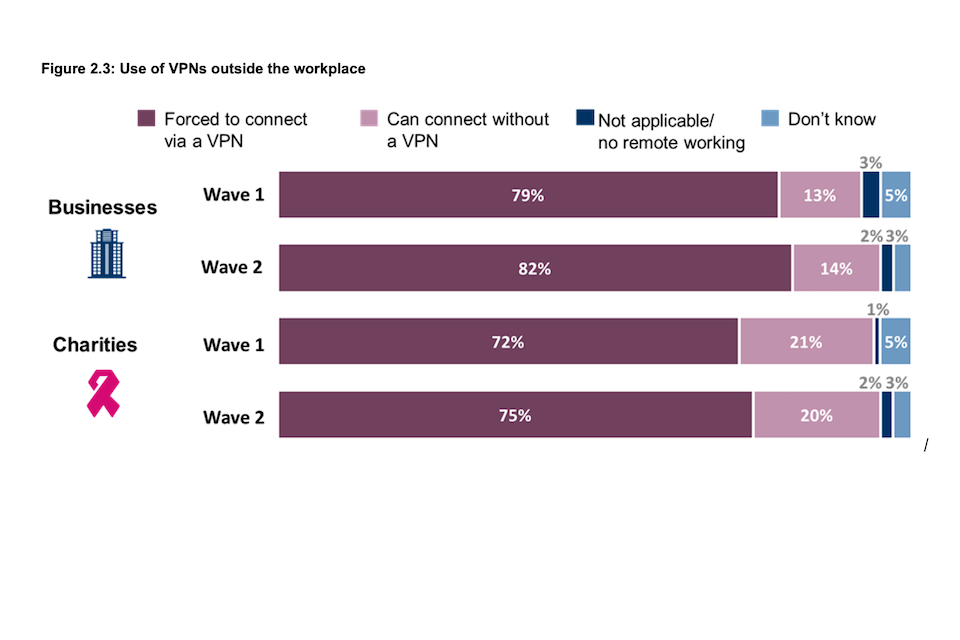

Among businesses with a VPN, four in five (82%) require their staff to use it when accessing the organisation’s network or files from outside the workplace. Although the figure is lower, three-quarters (75%) of charities with a VPN also require staff to use this when working remotely. Both figures are in line with the baseline survey (79% and 72% respectively for businesses and charities).

Perhaps reflecting the terms of the agreement, almost nine in ten (88%) businesses with a specific cyber security insurance policy require staff who are working remotely to connect via their VPN. However, this is not the case among charities. Charities with a specific cyber security insurance policy are no more likely than the average charity to require staff working outside the workplace to use their VPN for access (71% and 75% respectively).

The longitudinal sample behaves no differently to the overall sample in terms of the share of organisations that force staff to connect remotely using a VPN (83% of businesses in the longitudinal sample vs. 82% of all businesses, and 74% of charities in the longitudinal sample vs. 75% of all charities).

Figure 2.3: Use of VPNs outside the workplace

Are staff permitted to access your organisation’s network or files through personally owned devices (e.g., a personal smartphone or home computer)?

Figure 2.3: Use of VPNs outside the workplace

Base: All businesses with a VPN at Wave 1 (n=909) and at Wave 2 (n=525); All charities with a VPN at Wave 1 (n=354) and at Wave 2 (n=235). Statistically significant changes between Wave 1 data and Wave 2 data are represented by an arrow.

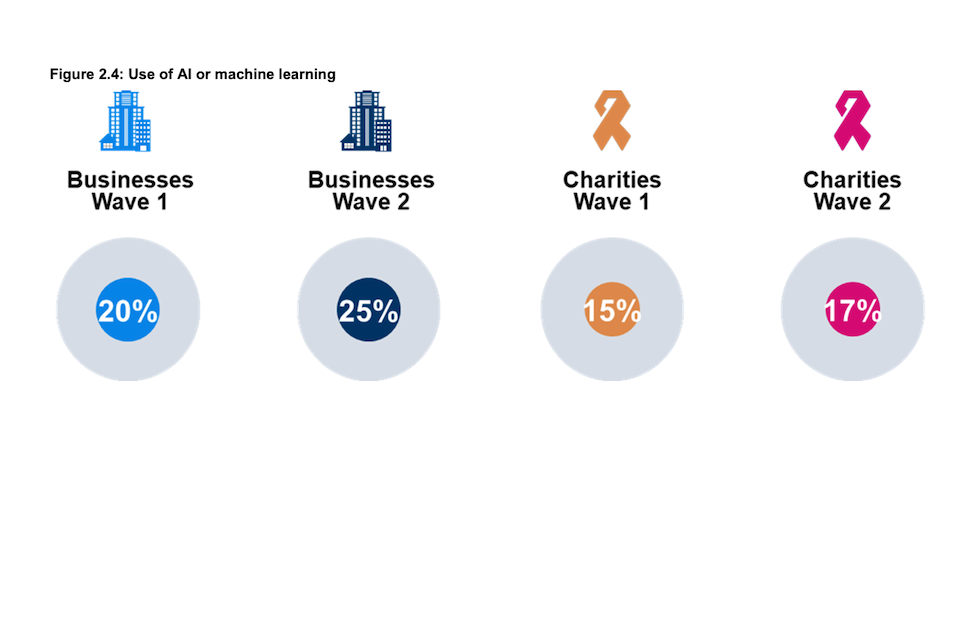

2.3 Use of artificial intelligence (AI) and machine learning

As pattern recognition algorithms can be applied to network data flows to automate threat detection, AI is an important element of cyber security. Meanwhile, machine learning is a subset of AI that can be used to support security measures by ensuring systems ‘remember’ and take account of any new patterns identified from recent incidents.

With one in four businesses (25%) using AI or machine learning, they are more likely than charities (17%) to be using cyber security tools that include this technology. Neither of these shares has changed significantly since the baseline survey (20% of businesses and 15% of charities).

The use of AI and machine learning is more prevalent in larger businesses with those employing 250+ employees (38%) twice as likely as medium-sized enterprises (21%) to say it is a feature of their cyber security tools. Possibly a function of the size of the organisation, use of AI and machine learning is also more common among businesses that have some form of accreditation or a specific cyber security insurance policy.

More than one-third (35%) of charities certified to the Cyber Essentials Plus standard report having cyber security tools that include AI and machine learning technology.

Figure 2.4: Use of AI or machine learning

Does your organisation deploy any cyber security tools that use AI or machine learning? (% yes)

Figure 2.4: Use of AI or machine learning

Base: All businesses at Wave 1 (n=1,205) and at Wave 2 (n=688); All charities at Wave 1 (n=536) and at Wave 2 (n=373). Statistically significant changes between Wave 1 data and Wave 2 data are represented by an arrow.

2.4 Use of external IT providers

Many businesses and charities do not have the resources available to them to adequately adjust their cyber security infrastructure. To help them with this adjustment, they can outsource their technology requirements to external IT providers.

Within the qualitative interviews, businesses and charities were asked whether they use external IT suppliers or cyber security consultants. The majority did and for a variety of reasons. In some cases, organisations contracted external suppliers for specific, short-term tasks, such as penetration tests, or for site installations, while others received a more extensive IT management service.

Where external advice was used most extensively this tended to reflect a lack of in-house resources or knowledge. In some instances, especially for smaller organisations or organisations in less technical industries, this was considered more cost-effective than developing or maintaining in-house expertise.

We use external consultants to test security systems. We previously used NCC Group to do penetration tests then switched to a more local company for tests.

–Business, Medium, Information and Communication

Yes, we use several consulting companies. It saves us money as we started as a small family business so third-party companies remove the need for more hires. Consulting companies fulfil a fully managed cyber security service. Long-standing relationships that we trust.

–Business, Large, Administration

Yes, consultants are used. Data is hosted in a data centre – the platform is a service, so we get support for that. We also have other consultants from time to time, including one helping on ISO formalisation and some helping with pen tests. We go external because of a lack of skill in house, lack of knowledge, experience. It is often less expensive to have a consultant for a short period of time.

–Business, Medium, Information and Communication

They just cover my leave and are available for me to ask questions and seek advice. [They] do projects for us on request.

–Charity

Most relationships with external IT providers go back several years, such that some participants “inherited” the relationship on taking the role and therefore were not involved when the consultants were first engaged. In other cases, the relationship came out of their insurance arrangements or via other ‘channels.’ Only rarely were formal procurement procedures undertaken.

–Business, Large, Health, social care or social work

[We use] four different companies for penetration tests. [We are] provided with various cyber security specialists as part of our cyber insurance.

–Business, Large, Health, social care or social work

Yes, we use consultants, especially for pen tests. They are chosen through a strict procurement process. Costs are important here as well; it may sometimes prioritise the quality of consultancy. There has to be a level of trust when considering data and data security.

–Business, Medium, Information and Communication

Choosing external contractors will be decided by the manager who goes through a procurement process following approval and finance team review.

–Charity

Whichever approach was taken to choosing consultants, the trust involved in these relationships was highlighted as important to their continued success. Typically, these longer-term relationships with external consultants were characterised by a high level of trust in their expertise and security procedures.

Chapter 3- Cyber security policies

This chapter covers cyber security policies, including the documentation, cyber insurance policies and staff training organisations have in place that are crucial to building cyber resilience. Through the improvement of governance documentation and insurance policies, as well as ensuring that staff have the necessary skills, businesses and charities will be better placed to improve their cyber security.

In Wave Two, organisations do seem to be putting more cyber security policies in place, with businesses in particular having shown increased prevalence of many types of cyber security policy. Compared to Wave One, the findings of greatest note are:

- Approximately nine in ten organisations (86% of businesses and 91% of charities) have in place at least one of the five documents considered part of an effective cyber security strategy. While this is almost identical to the Wave One share for charities (92%), this represents an increase among businesses (82% in Wave One).

- The maintenance of a risk register that covers cyber security remains more common among charities (74%) than in businesses (50%).

- The proportions of businesses and charities with all five types of documentation in place are in line with Wave One, as are the shares for each of the individual documents.

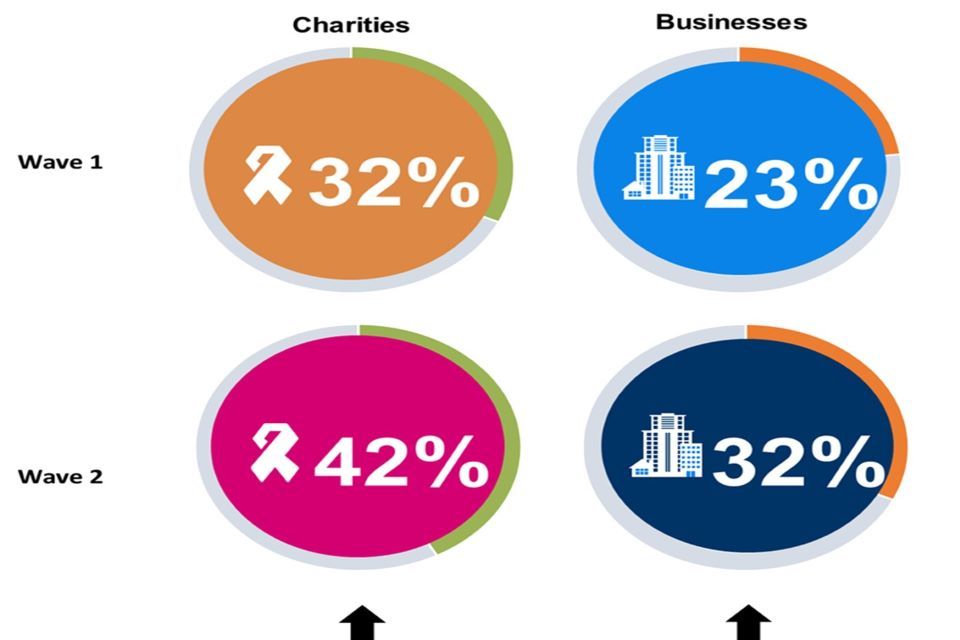

- Both businesses (up from 53% to 61%) and charities (up from 66% to 74%) are more likely than in Wave One to possess some form of cyber security insurance, even if this is covered within a more general policy. The proportion of organisations with a specific cyber security policy is also higher than in Wave One (businesses up from 18% to 25%, charities from 24% to 32%).

- Both businesses and charities are more likely than in Wave One to have delivered cyber security training or awareness raising sessions specifically for individuals not directly involved in cyber security (businesses up from 48% to 58%, charities from 55% to 62%).

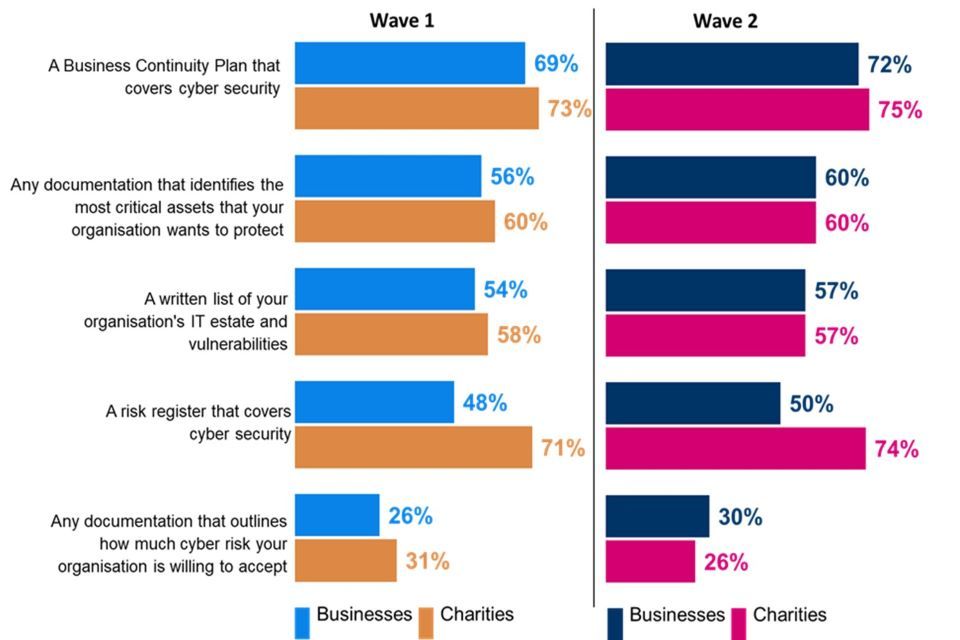

3.1 Governance and planning

As in Wave One, the survey asked about five types of documentation that organisations may have in place as part of an effective cyber security strategy. As detailed in Figure 3.1, these are: a Business Continuity Plan covering cyber security; documentation identifying critical assets; documentation of the organisation’s IT estate and vulnerabilities; a risk register that covers cyber security; and documentation of what is considered an acceptable level of cyber risk (‘risk appetite’).

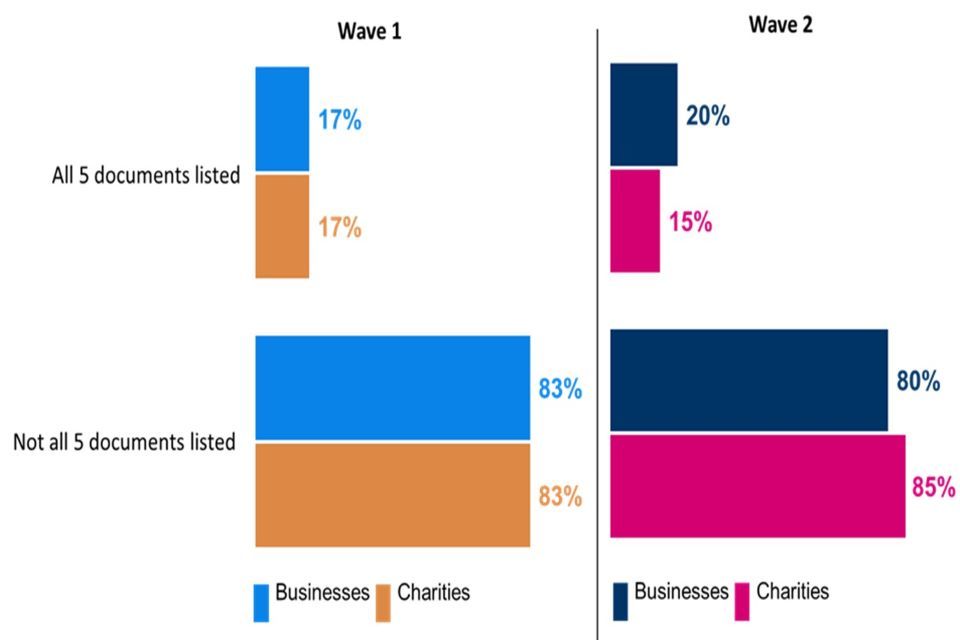

The vast majority of organisations (86% of businesses and 91% of charities) have at least one of these documents in place. While the share of charities is almost identical to Wave One (92%), the share of businesses represents an increase (from 82%) since the baseline survey. One in five businesses (20%) and a slightly lower share of charities (15%) have all five types of documentation in place. There is little change from Wave One when a share of 17% was recorded for both business and charities.

As illustrated in Figure 3.1, a majority of businesses currently have each type of documentation in place, with the exception of ‘risk appetite’ documentation (30%). Most prevalent among businesses is a Business Continuity Plan (72%). However, as with all other types of documentation, usage is in line with Wave One.

Around one-quarter (26%) of very large businesses (500+ staff) have all five types of documentation in place, which is above the average figure. A ‘complete’ set of documentation is also more likely to be held where a business has some form of accreditation or board oversight of cyber security risk. For example, 48% of businesses certified to the ISO 27001 standard have all five types of documentation, as do 29% of businesses with a designated staff member responsible for cyber security who reports directly to the board.

The level of cyber security documentation within charities is similar to that of businesses. The only exception relates to the maintenance of a risk register that covers cyber security, which is more common in charities (74%) than in businesses (50%). Three-quarters of charities (75%) have a business continuity plan in place, but relatively few have established documentation that outlines the level of cyber security risk they are willing to take (26%). As with businesses, the shares for individual documents are in line with Wave One.

Figure 3.1: Documentation in place to help organisations manage their cyber security risks

Does your organisation have any of the following documentation in place to help manage cyber security risks?

Clustered bar charts for Wave 1 and Wave 2 showing the proportion of organisations who have documentation in place to help manage their cyber security risks. Responses are split between businesses and charities.

Base: All businesses at Wave 1 (n=1,205) and at Wave 2 (n=688); All charities at Wave 1 (n=536) and at Wave 2 (n=373). Statistically significant changes between Wave 1 data and Wave 2 data are represented by an arrow.

Figure 3.1.1: Documentation in place to help organisations manage their cyber security risks (NETS)

Does your organisation have any of the following documentation in place to help manage cyber security risks?

Clustered bar charts for Wave 1 and Wave 2 showing the proportion of organisations who have all 5 documents in place to help manage their cyber security risks, and the proportion who do not have all 5. Responses are split between businesses and charities.

Base: All businesses at Wave 1 (n=1,205) and at Wave 2 (n=688); All charities at Wave 1 (n=536) and at Wave 2 (n=373). Statistically significant changes between Wave 1 data and Wave 2 data are represented by an arrow.

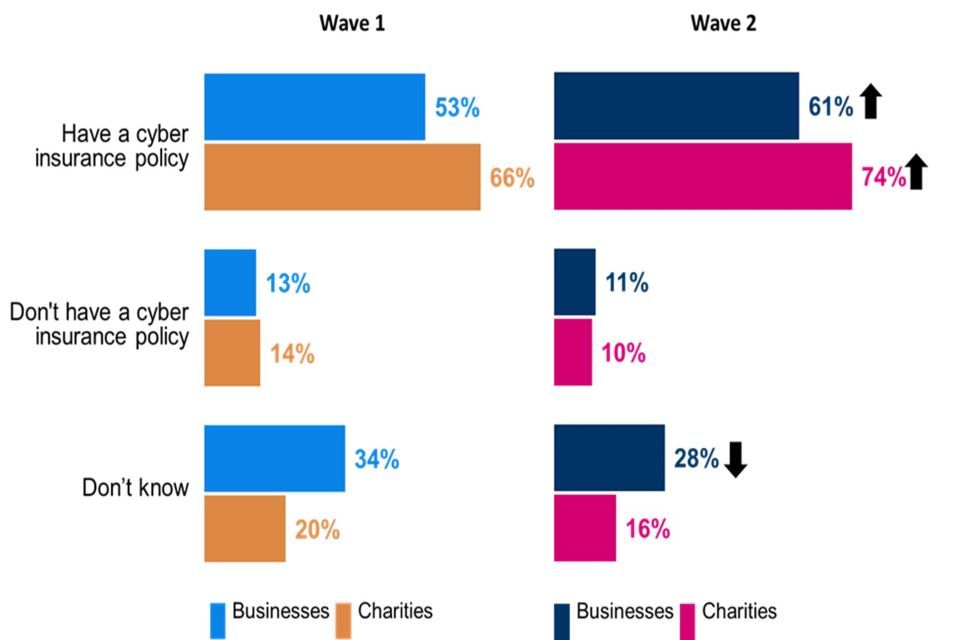

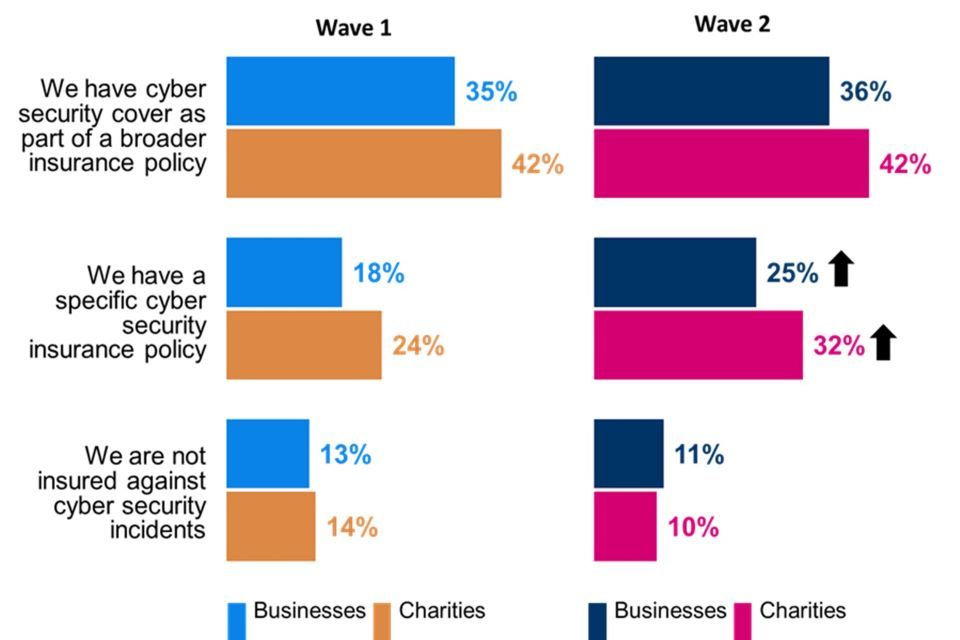

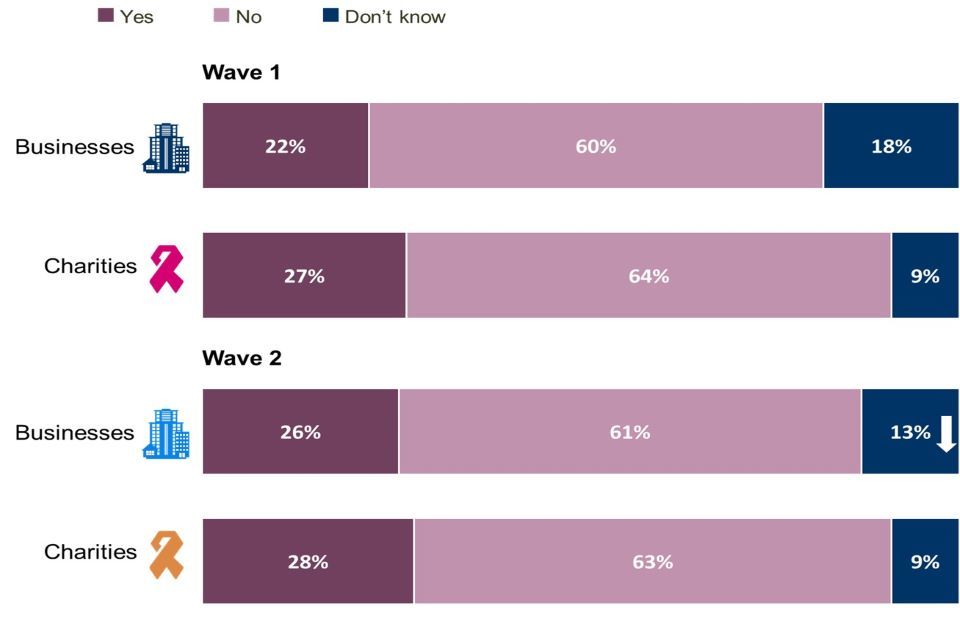

3.2 Cyber insurance policies

Businesses and charities are both more likely than in Wave One to have some form of cyber insurance cover in place. Six in ten businesses have some form of cover (61%), compared with just over half (53%) in the baseline survey. The respective shares for charities are 74% and 66%.

The increase is driven by a general uplift in the proportion of organisations that have a specific cyber security policy, rather than this being covered as part of a broader insurance policy. One-quarter of businesses (25%) and one-third of charities (32%) have specific cyber security policies with both shares higher than in Wave One.

The Wave Two data shows that one in ten organisations (11% of businesses, 10% of charities) have no form of cyber security insurance in place. Many others remain unaware of what may be in place, and among businesses almost three in ten (28%) do not know what insurance cover they have against cyber incidents.

Insurance cover is more frequently in place where businesses have also made wider investment in cyber security protection. For example, businesses with all five types of documentation mentioned above are twice as likely to have specific insurance cover (41%) than those without all five (21%). In addition, 44% of businesses that are certified to the Cyber Essentials standard have specific cover, as do 36% of businesses with Cyber Essentials Plus certification and 30% with ISO 27001. The share among those businesses holding none of these three certifications is 21% and these businesses are equally as likely to have no insurance at all against cyber security incidents (18%).

Figure 3.2: Organisations with cyber insurance

Which of the following best describes your situation?

Clustered bar charts for Wave 1 and Wave 2 showing the proportion of organisations who have cyber insurance. Responses are split between businesses and charities.

Base: All businesses at Wave 1 (n=1,205) and at Wave 2 (n=688); All charities at Wave 1 (n=536) and at Wave 2 (n=373). Statistically significant changes between Wave 1 data and Wave 2 data are represented by an arrow.

The increase in the share of businesses with a specific cyber security insurance policy is reflected in the longitudinal sample interviewed in both Wave One and Wave Two (from 21% to 28%, which is higher than the 18% of the fresh business sample with a specific cyber insurance policy). In contrast, there is no difference in the shares of longitudinal and fresh charity sample with a specific cyber insurance policy (31% and 32% respectively).

Figure 3.3: Type of cyber insurance policy organisations have

Which of the following best describes your situation?

Clustered bar chart showing the proportion of organisations that different types of cyber security insurance. Responses are split between Wave 1 businesses, Wave 2 businesses, Wave 1 charities and Wave 2 charities.

Base: All businesses at Wave 1 (n=1,205) and at Wave 2 (n=688); All charities at Wave 1 (n=536) and at Wave 2 (n=373). Don’t know not shown. Statistically significant changes between Wave 1 data and Wave 2 data are represented by an arrow.

The qualitative interviews suggested that cyber security insurance can come at a considerable cost to the organisation, but where implemented it is regarded as being highly important. One business viewed it in the same way as buildings, contents, and public liability insurance. A charity representative said that although cyber insurance was a big cost it was “essential to protect themselves”.

In addition to the financial benefit and mitigation of potential losses, cyber security insurance can provide wider organisational benefits. Part of the process of obtaining this insurance is to review and document procedures, which can prove helpful.

We are learning and picking up from the questions we are being asked for cyber insurance forms.

–Business, Medium, Transport or Storage

Another business outlined how the feedback from seeking insurance cover was forcing the business to improve its systems and approach.

An assessment in March gave us a score of 2/4. In some areas we were down on that. We need to get to 2.5 to get meaningful cover in all the areas identified. That helps us make a judgement on what [we] need to do – we need additional investment.

–Business, Large, Information and communication

3.3 Staff training

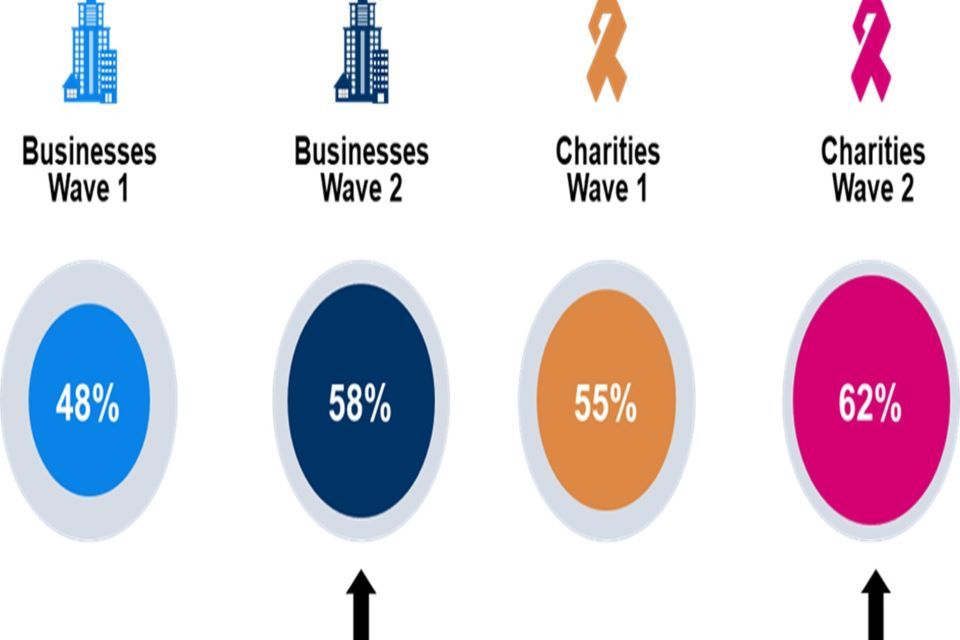

In the past twelve months, approximately six in ten businesses (58%) and charities (62%) have delivered cyber security training or awareness raising sessions specifically for staff and/or volunteers who are not directly involved in cyber security. Both shares represent an increase from the baseline survey (48% and 55% respectively).

Large businesses with 250+ employees (68%) are more likely to have delivered such training than medium sized businesses (56%). Other types of business more likely to have delivered this training are those with documentation for all five of the technical controls required to attain Cyber Essentials, with one or more certifications, board oversight or specific cyber insurance policies. As such, training appears to be part of a generally more holistic approach to cyber security threats. Around one-quarter of those businesses ‘lacking’ all five of the technical controls required to attain Cyber Essentials (24%) have delivered relevant training to their general workforce in the past twelve months. Almost half of businesses not certified to any of the three standards (49%), and businesses with no cyber security insurance (42%) had delivered such training.

This trend was reflected among businesses interviewed in both Wave One and Wave Two (61% carried out general staff training sessions in the last twelve months, compared to 49% in Wave One, in line with the increase for all businesses). However, there was little change among charities interviewed in both waves (62% carried out training sessions in the last year, compared to 60% in Wave One).

Figure 3.4: Cyber security training or awareness raising delivered by organisations in the last 12 months

In the last 12 months, have you carried out any cyber security training or awareness raising sessions specifically for any staff or volunteers who are not directly involved in cyber security?

Chart showing the proportion of organisations who had cyber security training or awareness raising delivered by their organisation in the last 12 months. Responses are split between Wave 1 businesses, Wave 2 businesses, Wave 1 charities and Wave 2 charities.

Base: All businesses at Wave 1 (n=1,205) and at Wave 2 (n=688); All charities at Wave 1 (n=536) and at Wave 2 (n=373). Statistically significant changes between Wave 1 data and Wave 2 data are represented by an arrow.

The qualitative interviews suggested that for those involved in designing or managing these activities, the key is raising staff awareness of their responsibilities. This encompassed formal training, for example in ISO 27001 and GDPR compliance, as well as targeted activities such as sending an email reminder with a relevant screenshot if the system indicates that rules have been broken by individual staff members (such as unauthorised devices being connected).

The key thing is staff awareness. If you can crack that, you don’t have to worry about the tooling quite so much. Make people aware of the vulnerabilities. If you can get that embedded in people’s way of work life, everything else becomes non-essential. The problems always start with people, everything else is peripheral.

–Business, Medium, Information and Communication

Participants in these interviews were also asked if their organisation had conducted a cyber skills assessment of their workforce. Many had not done so, but for those that had, it typically involved a phishing test or a simulation that checked whether staff responded appropriately. Some organisations carried out broader exercises.

Yes - we recently did a general quiz with staff to gauge knowledge of the business which helped highlight the skilled staff and good general knowledge.

–Business, Medium, Media

Every new starter has to go through security training, about two hours, (there is also) an annual programme, also phishing. Phishing is more beneficial than annual training. The person broadcasts the fact they’ve received it to the rest of the company - doing [the respondent’s] job for me. People won’t listen to me, but they’ll listen to their colleagues.

–Business, Medium, Information and communication

Chapter 4- Cyber security processes

In addition to the policies, documentation and training that are being put in place, it is also vital that specific processes are outlined to help develop cyber resilience. This chapter discusses the cyber security processes and documentation organisations have in place, including any standards and certifications they hold. It goes on to describe the extent to which organisations monitor and evaluate their policies and where relevant whether any improvements have been made over the last twelve months. Understanding these changes will help to illustrate the actions that organisations are undertaking to help improve their cyber security.

Organisations are increasingly adhering to at least one cyber security certification (although it remains less than a majority) and have taken steps to develop an aspect of their cyber security. Compared to Wave One, the findings of greatest note are:

- A higher share of businesses (40%) and charities (36%) now adhere to at least one of the three cyber security related certifications asked about (Cyber Essentials, Cyber Essentials Plus, and ISO 27001).

- Businesses (up from 19% to 25%) and charities (from 19% to 28%) are more likely to adhere to the Cyber Essentials standard. The share of businesses adhering to the Cyber Essentials Plus standard (11%) is also higher than in Wave One (8%).

- Although still low, the proportion of businesses that include something about cyber security in their annual report has increased (from 14% to 19%). There is no equivalent change among charities (18% in both waves).

- Although it has not changed since the baseline survey, almost nine in ten organisations (86% of businesses and 87% of charities) continue to take at least one action to identify the cyber security risks their organisation faces.

- Businesses have increased their use of security monitoring tools and vulnerability audits compared to Wave One.

- There has been an increase in the proportion of businesses that have taken at least one step over the past twelve months to expand or improve some aspect of their cyber security (from 79% to 85%). This is primarily the result of greater use of authentication and access control (up from 59% to 65%), and processes for managing cyber security (up from 41% to 47%).

- Fewer than three in ten businesses (26%) and charities (28%) have formally addressed the potential cyber security risks associated with their suppliers or partner organisations. This is in line with Wave One.

4.1 Standards and certifications

To help instil good practice, organisations can apply to receive one of several cyber security certifications. Often based on standards taken from government guidance, achieving one of these certifications puts an organisation in a more resilient position. This survey focuses on three specific standards: Cyber Essentials, ISO 27001 and Cyber Essentials Plus.

Compared to the baseline study, higher proportions of businesses and charities now adhere to at least one of three cyber security certifications shown in Figure 4.1 (businesses increased from 32% to 40%, and charities from 29% to 36%). Cyber Essentials[footnote 8] is the standard most often adhered to by businesses (25%) and charities (28%), with both proportions higher than in Wave One (19% for both).

Almost two in ten businesses (17%) adhere to the ISO 27001[footnote 9] standard, while around one in ten are certified to the Cyber Essentials Plus[footnote 10] standard (11%). The proportion adhering to the Cyber Essentials Plus standard is higher than in the baseline survey (8%).

Charities are less likely than businesses to adhere to the ISO 27001 standard (9%) than businesses. Charities are just as likely to adhere to ISO 27001 as they are to the Cyber Essentials Plus standard (also 9%).

Around four in ten businesses (39%) and charities (40%) confirmed adhering to none of the three certifications asked about in the survey.

Large businesses (250+ staff) are more likely than medium sized enterprises (50-249) to be certified to each of the three standards. Half (50%) of large businesses adhere to at least one standard or accreditation, compared to four in ten medium sized companies (38%). Large businesses are particularly more likely than medium sized businesses to be certified to the Cyber Essentials (34% vs. 23%) and Cyber Essentials Plus (17% vs. 10%) standards.

The 28% share of charities adhering to the Cyber Essentials standard is reflected across both the longitudinal and fresh charity samples (27% and 28% respectively). Specifically looking at the longitudinal sample, this represents an eight-point[footnote 11] increase from the 19% recorded in Wave One.

Figure 4.1: Standards and accreditations held by organisations

Which of the following standards or accreditations, if any, does your organisation adhere to?

Clustered bar charts for Wave 1 and Wave 2 showing the standards and accreditations held by organisations. Responses are split between businesses and charities.

Base: All businesses at Wave 1 (n=1,205) and at Wave 2 (n=688); All charities at Wave 1 (n=536) and at Wave 2 (n=373). Don’t know not shown. Statistically significant changes between Wave 1 data and Wave 2 data are represented by an arrow.

Probably reflecting greater levels of monitoring and awareness, and as in Wave One, businesses that experienced a cyber incident in the last twelve months are more, not less, likely to adhere to a relevant standard or accreditation. It may show that their systems are effectively picking up incidents. It is of note that three in ten businesses that experienced a cyber security incident were certified to the Cyber Essentials standard (30%), compared to one in ten (11%) with no cyber security incident in the last year. Among charities, levels of certification were similar for charities that had and had not experienced a cyber incident in this time.

The qualitative research revealed mixed views on the usefulness, or otherwise, of Cyber Essentials. Some regarded it as a ‘tick box’ exercise that was only adopted because some clients required it. For others, it provides a beneficial framework that helps them adhere to high industry standards:

Gaining certification was a tick box exercise, we already had all the policies in place. Cyber Essentials wasn’t much of a leap.

–Business, Medium, Information and Communication

It’s a bit heavy duty for us but it seemed to fit in with clients’ requirements. It’s the industry standard without being too onerous or expensive like ISO.

–Business, Medium, Information and Communication

It aligns you with the best practice for security.

–Business, Large, Construction

From an internal IT point of view, we have a framework to follow and adhere to.

–Charity

4.2 Cyber Essentials processes

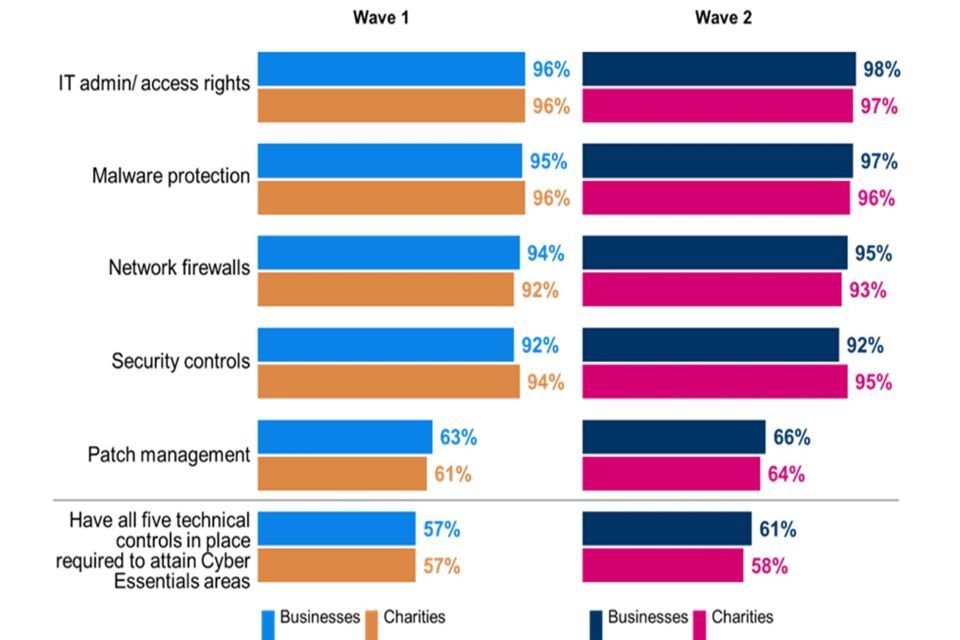

To attain Cyber Essentials accreditation, organisations are required to have five technical rules or controls in place. As illustrated by Figure 4.2, approximately six in ten businesses (61%) and charities (58%) do operate all five of these rules or controls. These figures are in line with the 57% recorded for both businesses and charities in Wave One.

Regardless of whether certified against Cyber Essentials, 9 in 10 businesses and charities had the follow technical controls in place, which comprise 4 of the 5 technical controls required under the Cyber Essentials standard:

- Restriction of IT admin and access rights to specific users

- Up to date malware protection across all devices

- Firewalls that cover the entire IT network, as well as individual devices

- Security controls on the organisation’s own devices e.g., laptops

Only around two-thirds of organisations say they have a policy to apply software security updates within 14 days. i.e., patch management (66% of businesses and 64% of charities). However, for each of the five technical controls required to attain Cyber Essentials, the proportions are in line with Wave One, for both businesses and charities.

Figure 4.2: Technical controls in place in the areas required to attain Cyber Essentials

And which of the following rules or controls, if any, do you have in place?

Clustered bar charts for Wave 1 and Wave 2 showing the technical controls in place that are required in order for organisations to attain Cyber Essentials. Responses are split between businesses and charities.

Base: All businesses at Wave 1 (n=1,205) and at Wave 2 (n=688); All charities at Wave 1 (n=536) and at Wave 2 (n=373). Don’t know not shown. Statistically significant changes between Wave 1 data and Wave 2 data are represented by an arrow.

Large businesses (68%) are more likely than medium-sized enterprises (60%) to have in place all five technical controls required to attain Cyber Essentials certification. Among very large businesses (with 500+ staff) the share is 72%. This difference is ‘driven’ by variations in the extent to which businesses are applying patch management. Compared to medium-sized companies (64%), large businesses (75%) are implementing patch management to a much higher degree.

Businesses that have experienced a non-phishing incident (66%) are more likely than those who have not (54%) to have all technical controls required to attain Cyber Essentials in place. This potentially highlights how the greater use of controls helps identify and manage, rather than eradicate, cyber security incidents. This is also the case where there is board oversight of cyber security (75%), and where specific cyber security insurance has been taken out (75%). The same relationships are observed within charities.

Four other rules and controls were covered by this question, and in each case at least six in ten organisations say they have these controls in place:

- Specific rules for storing and moving files containing people’s personal data (85% of businesses and 86% of charities)

- Backing up data securely via cloud device (more likely among charities than businesses, 85% vs. 75%)

- Backing up data by other means (more likely among businesses than charities, 70% vs. 63%)

- Monitor user activity (66% of businesses and 64% of charities)

The 85% of charities securely backing up data via a cloud service, also represents an increase compared with Wave One (77%). However, there is little difference between the longitudinal and fresh charity samples on this measure (84% and 88% securely back up data via a cloud service respectively).

4.3 Reporting and identifying risks

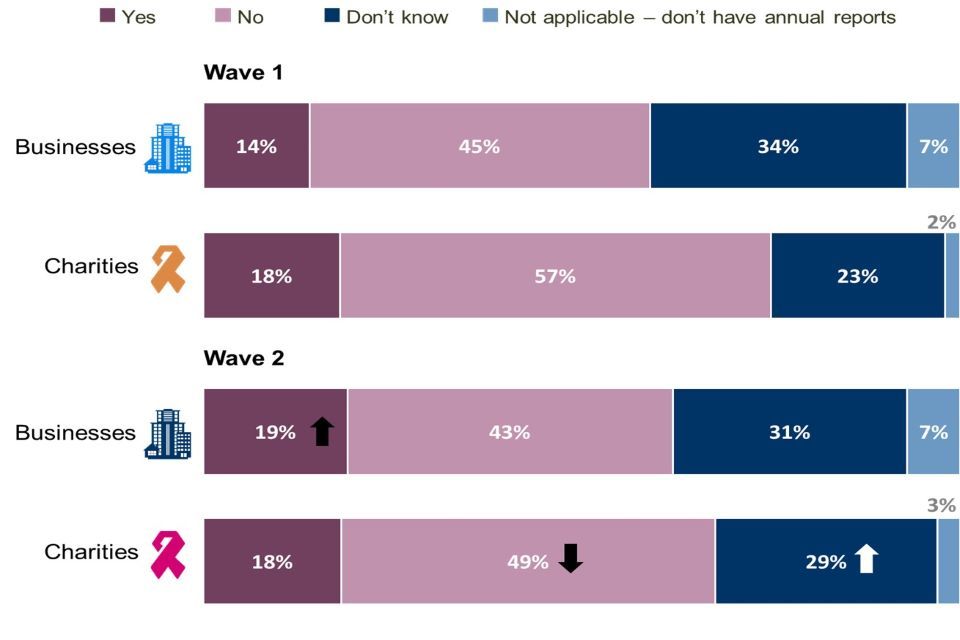

Annual reports

As illustrated by Figure 4.3, while the proportion has increased from Wave One (from 14% to 19%), fewer than one in five businesses include something about cyber security in their annual reports. Similarly, around one in five charities (18%) say cyber security is ‘covered’ in their annual report, which is identical to Wave One.

Figure 4.3: Reporting on Cyber Security

Did you include anything about cyber security in your organisation’s most recent annual report?

Stacked bar chart showing the proportion of organisations who included cyber security in their organisation’s most recent annual report. Responses are split between Wave 1 businesses, Wave 2 businesses, Wave 1 charities and Wave 2 charities.

Base: All businesses at Wave 1 (n=1,205) and at Wave 2 (n=688); All charities at Wave 1 (n=536) and at Wave 2 (n=373). Statistically significant changes between Wave 1 data and Wave 2 data are represented by an arrow.

Three in ten very large businesses with 500+ employees (31%) include cyber security in their annual report. This is also more prevalent among businesses certified to the ISO 27001 (30%) and Cyber Essentials Plus (39%) standards. These are the highest figures seen among business sub-groups. Coverage of cyber security in their most recent annual report is also more common among charities with recognised cyber security standards (e.g., ISO 27001 (31%), Cyber Essentials Plus (50%)).

Organisations in the longitudinal sample are as likely to confirm inclusion of cyber security in their annual report (18% of businesses and 19% of charities) as those interviewed for the first time in Wave Two (21% of businesses and 18% of charities).

The relatively low proportion of organisations including cyber security in their annual reports was reflected on in the qualitative research. Some respondents felt that this may change, but opinion was divided on usefulness:

I expect with how things are changing with ISO that that will change.

–Business, Medium, Information and Communication

My stance is it [cyber security] should be visible to our customers in our annual report because we’re quite strong and we should be quite proud of it - we put a lot of effort in to maintain it, so should be keen to broadcast.

–Business, Medium, Information and Communication

I’m not sure I see the value of having it added - who would be reading it?

–Business, Medium, Information and Communication

Identification of cyber security risks

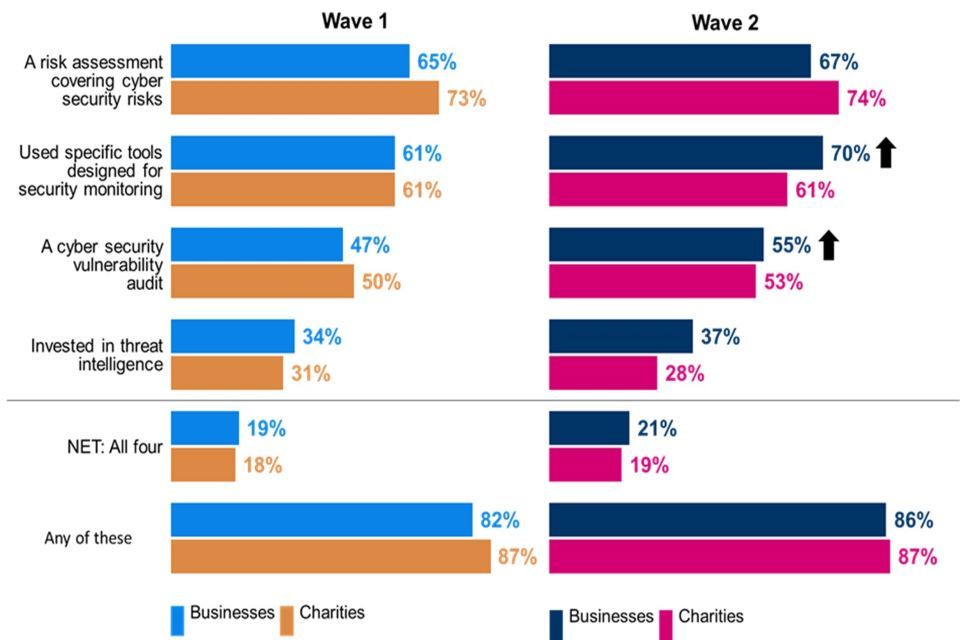

In order to ensure that organisations are able to plan and build processes that will protect them adequately it is vital that businesses and charities are able to identify their cyber security risks. Reflecting the findings of the baseline survey, almost nine in ten organisations (86% of businesses and 87% of charities) say they have taken one of the four actions detailed in Figure 4.4 in the last year to identify cyber security risks facing their organisation. One in five organisations (21% of businesses and 19% of charities) report taking all four measures, which is also in line with the Wave One survey.

A minimum of six in ten organisations (both businesses and charities) have conducted a cyber security risk assessment in the past twelve months or have used specific tools (such as Intrusion Detection Systems) designed to monitor such risks. Organisations that experienced a cyber security incident in the last twelve months are more likely to have conducted a risk assessment covering cyber security risks (72% compared to 61% who had not had an incident), or a cyber security vulnerability audit (58% compared to 43% who had not had an incident).

A majority of organisations have also completed a cyber security vulnerability audit. While the level of deployment by charities is unchanged from Wave One, a higher share of businesses have used specific security monitoring tools (70%, up from 61% in Wave One) and vulnerability audits (55%, up from 47% in Wave One).

Investment in threat intelligence remains relatively rare but has been undertaken by a higher proportion of businesses than charities (37% vs. 28%). Charities remain more likely than businesses to have undertaken a risk assessment covering cyber security risks (74% vs. 67%), but businesses are now more likely than charities to use specific tools designed for security monitoring (70% vs. 61%).

Figure 4.4: Steps taken to identify cyber security risks

Which of the following, if any, have you done in the last twelve months to identify cyber security risks to your organisation?

Clustered bar charts for Wave 1 and Wave 2 showing the steps organisations have taken to identify cyber risks. Responses are split between businesses and charities.

Base: All businesses at Wave 1 (n=1,205) and at Wave 2 (n=688); All charities at Wave 1 (n=536) and at Wave 2 (n=373). Don’t know not shown. Statistically significant changes between Wave 1 data and Wave 2 data are represented by an black arrow.

Compared to large businesses, medium-sized businesses are only half as likely to have taken all four steps to identify cyber security risks facing their organisation (18% vs. 37%). More than twice as many medium (17%) as large businesses (7%) say they have taken none of these steps. The respective proportions for each individual action are as follows: