GCA Annual Report and Accounts 2018/2019

Published 24 June 2019

© Crown copyright 2019

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/2018-to-2019-gca-annual-report-and-accounts/gca-annual-report-and-accounts-20182019

SECTION A: PERFORMANCE REPORT

1.Overview

This section of the annual report explains the role and purpose of the Groceries Code Adjudicator (GCA). The Performance Analysis sets out how the GCA has performed during the year against its statutory reporting requirements and strategic objectives, along with other key activities. The main risks to the achievement of the GCA’s objectives and the explanation of the adoption of the going concern basis are set out in the Governance Statement.

1.1 Foreword from the Groceries Code Adjudicator

In May 2018 I received striking evidence that my collaborative approach is reaping significant results. The annual survey demonstrated we had reached a real high point in Code compliance among all the retailers I regulate.

The survey recorded a significant drop in the proportion of suppliers reporting concerns relating to every one of the nine issues on which I have focused my activities since 2013.

Progress against Top Issues as reported in the Groceries Code Adjudicator annual surveys 2014-2018.

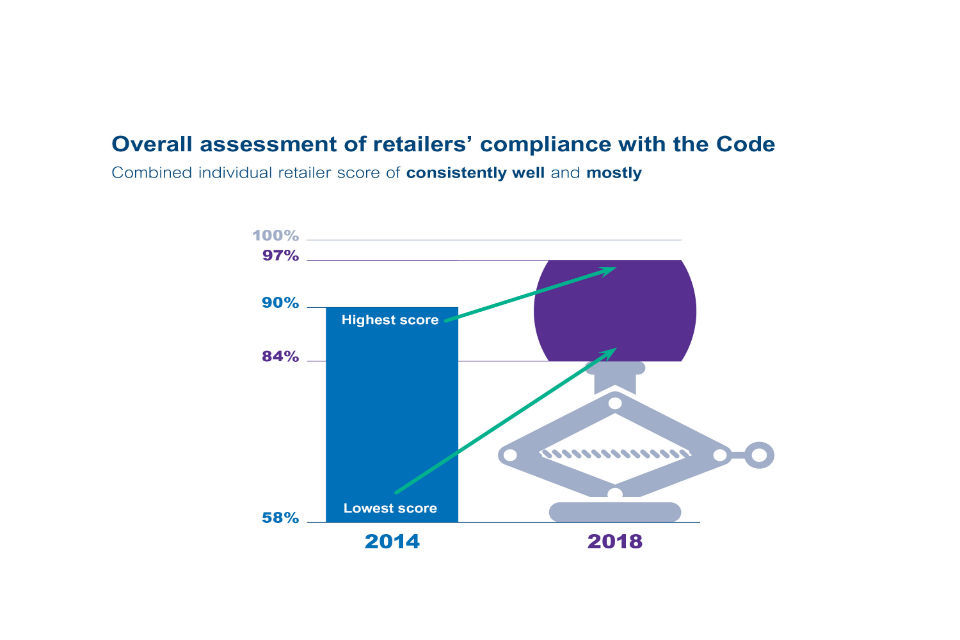

The overall improvement is shown very clearly in my “jack slide”, which represents in graphic form how far we have come in the GCA’s five years of existence. Each year I ask suppliers to rate retailers’ compliance with the Code and in 2018 only two retailers were rated below the level of the very best performing retailer in 2014.

In 2014 the overall assessment of retailer's compliance with the Code was spread between 58% and 90%. In 2018 this had changed to between 84% and 97%.

It was no coincidence that the four most improved retailers had each been subject to increased scrutiny by or enhanced engagement with me through investigations or case studies.

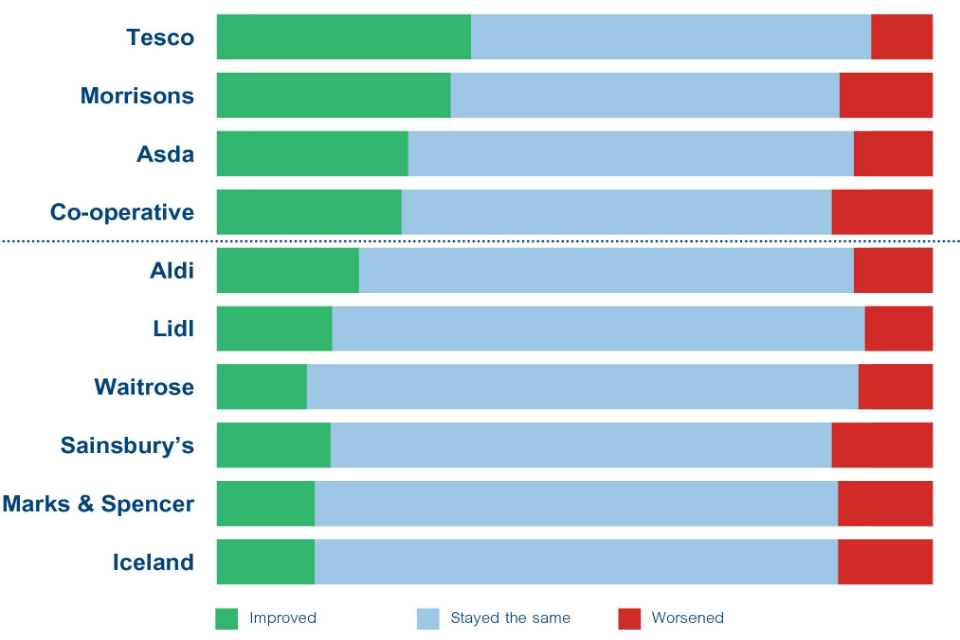

Change in retailer practice over the past 12 months. Tesco, Morrisons, Asda and Co-op take the top 4 slots.

Top Issues

Accordingly, I announced at my conference in June that I no longer had any Top Issue to work on with the retailers and that I would continue to monitor performance of all retailers in relation to delay in payments, forecasting and promotions. The original ten designated retailers have been collating data about these issues and gave me the results in March.

The next step for me is to analyse these results. I am confident that giving the retailers time to consider and make any changes they need to their processes before doing an analysis of their compliance will have led to improvements to help them to do so. I will of course continue to work with any retailers who have struggled to meet my expectations.

I am also committed to keeping on top of issues as they arise. Suppliers need to tell me if there are any potential Code breaches they are concerned about. As additional retailers are designated I will work with them on all previous and monitored Top Issues.

Investigation into Co-operative Group Limited

My main focus throughout this year has been on the Co-op investigation which, like my investigation into Tesco plc, has taken over a year to complete. There has been great dedication from those involved. The process of collecting evidence, interviewing suppliers, following up where information is missing and then clarifying situations with Co-op was extremely time consuming.

The investigation has certainly been thorough. I have learned a lot in the process and am confident that it provides an opportunity to secure a step change in Code compliance across the sector.

I published my report in March and my findings and recommendations are set out later in this report. I want to reflect here on the issues of culture and governance.

For 18 months before the launch of the investigation I engaged intensively with Co-op. I decided to launch an investigation because I realised Co-op was unable to get to the bottom of the issues, to establish root causes and demonstrate to me that remedial action had been taken in all the relevant circumstances.

During that engagement and also during the period under investigation I found that at a senior level within Co-op there was a failure to recognise the need to take steps to ensure that it was compliant with the Code. As a result, the business was not effectively Code-proofed in relation to the requirements I investigated, which were De-listing and Variation of Supply Agreements.

Co-op accepted that at the time the focus of its business was on business recovery and it is clear that the Code was not embedded into its culture as it should have been. Co-op mistakenly assumed that its brand values and desire to work in a certain way meant that it was likely to be acting in accordance with the Code and that, if there were any issues with compliance, suppliers would have made the retailer aware of them. The clear conclusion was that Co-op needed to take a very different approach to Code compliance. I have made robust recommendations for urgent action and I will be helping Co-op to change its approach by monitoring closely how it implements those recommendations. Ultimately, I launched this investigation to help Co-op to get things right for the future.

I cannot over-emphasise the importance of governance in ensuring Code compliance and through this investigation this principle is now firmly embedded in my regulatory requirements.

My interpretation of the relevant paragraphs of the Code applies to all regulated retailers and I have already started talking to them about what this will mean for them.

Case studies

I have published no case studies this year, but there have been a number of occasions when I have raised an issue with a retailer, it has been thoroughly investigated internally and dealt with immediately.

I am also pleased to report that there have been instances when a retailer’s Code Compliance Officer (CCO) contacted me directly to report that they had come across a potential Code breach and were actively putting the situation right. They told me they were keen that I heard it from them before a supplier told me.

During the year I continued to have regular meetings with CCOs and ensured that they all learned from these near-misses.

Investigations and Arbitrations

I am delighted to report that two arbitrations closed during the year and I ended the year with no open arbitrations. I repeat the point I made last year that arbitrations are costly, lengthy legal processes and that I am an arbitrator not a mediator so there is a limit to the extent to which I can assist the parties to achieve a sensible commercial outcome.

Suppliers and retailers should attempt to resolve all issues through commercial discussions or mediation if necessary. I am aware of all issues that are raised with CCOs and I know that retailers work hard to resolve issues whenever they are raised by suppliers and really do try to avoid them leading to arbitration.

Retailers

During the year I held around 40 meetings with CCOs and a further 7 at CEO level. I also met all the chairs (or equivalent) of the audit committees. I can confidently report that all retailers listen to the issues that I raise and work hard to ensure their businesses are Code compliant.

The progress made over the last five years is all theirs and I take great pleasure in reporting that suppliers really notice the difference. Recently, having taken up an issue on a supplier’s behalf, I commented that often the very fact that I have raised an issue makes a difference. The supplier replied: “I am convinced that is the case and thanks for all the work you have done so far to bring the retailers into line, generally making it a more level playing field and making it more pleasurable to do business with them.”

In November the Competition and Markets Authority (CMA) designated Ocado Group plc (Ocado) and B&M European Value Retail SA (B&M) as additional retailers to be regulated under the Code. B&M decided to contest this designation. I have had three meetings with Ocado and am confident that the retailer understands the Code and is working through any implications for its business policies and processes. We are both looking forward to the 2019 survey results to show where work may be needed.

I see the designation of additional retailers to be a positive move towards a more level playing field for large retailers selling groceries. My team and I continue to hear about difficulties suppliers have with other retailers. I cannot take these forward, so I would urge suppliers and trade associations to let the CMA know if there are additional retailers they believe should be covered by the Code.

Suppliers

The GCA Code Confident campaign designed to build awareness of the Code and the GCA has been underway for over a year and is starting to pay dividends. More suppliers are being trained and are increasingly speaking to us about their experiences with retailers, although this comes against a backdrop of a continual decline in Code-related issues arising, as reported in my annual surveys. Of course I would like to hear more, so I continually reinforce with suppliers my statutory duty of confidentiality and my ability to help change things for the future. I am always very tactful about how I raise issues with retailers, partly to protect my sources, but also because I want the retailers to take a proper look at their businesses and to identify all areas where any similar practice may be taking place.

GCA Office

The office has been at full strength all year, although the Co-op investigation has meant that we have had different activities. As a result, there have been many weeks when I have been absent from the office, interviewing suppliers and representatives of Co-op as well as reading a significant amount of material. I am grateful for my team’s support and the assistance they have given to suppliers, including visiting trade shows on my behalf to raise awareness of the Code.

I am also extremely grateful to my in-house lawyer who has always ensured that my enthusiasm to fix all issues as fast as I can is tempered by what is reasonable to expect from retailers and by doing the job properly, as well as supporting me in the Co-op investigation and in my role as arbitrator.

Challenges and forward look

There will be no letting up in the coming year. As well as assessing the response on the monitored Top Issues I will be working closely with Co-op to ensure it fully implements my recommendations and I will be sharing the learnings with retailers and suppliers. During the year the Government will also conduct a second statutory review of the GCA’s performance to cover the period April 2016 to March 2019 and I encourage all those with an interest in the work of the GCA to give their views.

In the Autumn the GCA is due to move office with the CMA to Canary Wharf where we are looking forward to having slightly larger premises and a dedicated meeting room. I will continue to attend an event at least once a month so I can have direct contact with suppliers and my team will attend trade fairs to ensure that even the smallest grocery supplier has heard of the Code and how the GCA can support them.

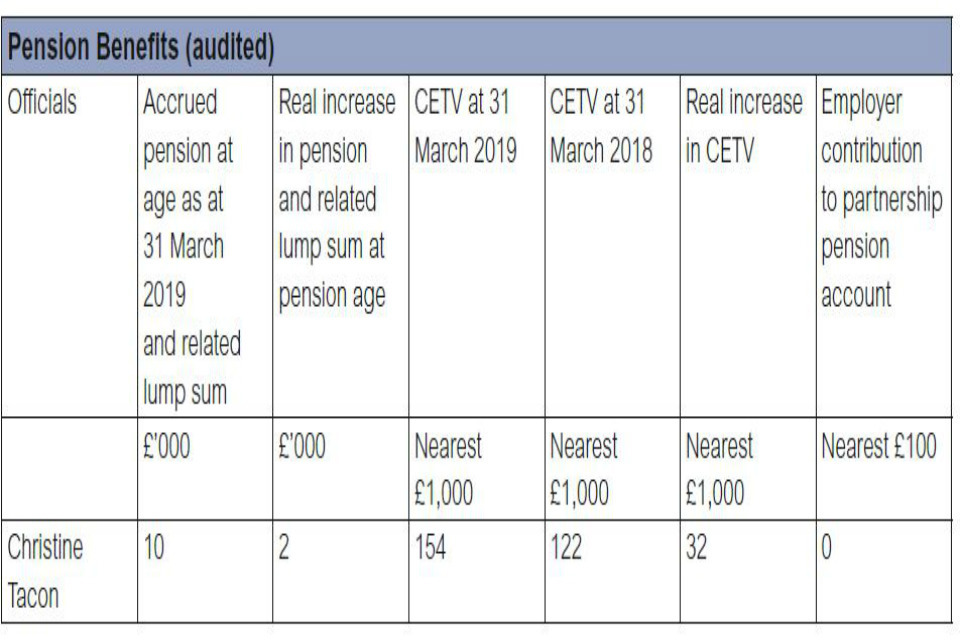

Christine Tacon,

Groceries Code Adjudicator and Accounting Officer

29 May 2019

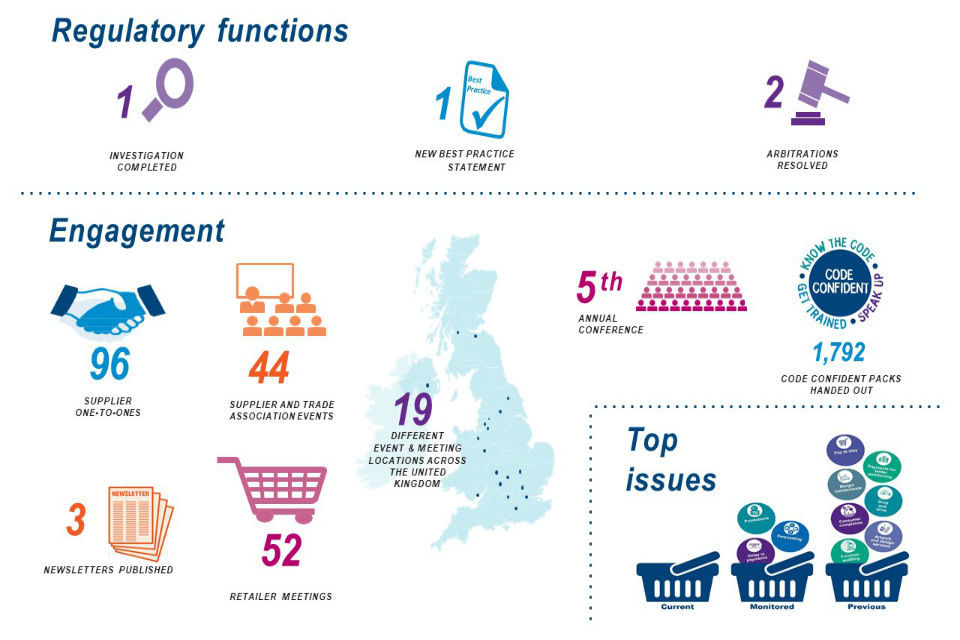

Regulatory functions: 1 investigation completed, 1 new best practice statement and 2 arbitrations resolved. Engagement: 96 supplier meetings, 44 supplier and trade association meetings, 53 retailer meetings in 19 locations.

1.2 Groceries Code Adjudicator: Working for fairness in the groceries supply chain

The Groceries Code Adjudicator (GCA) was formally established on 25 June 2013 by an Act of Parliament. It was set up to ensure supermarkets treat their suppliers lawfully and fairly.

The appointment followed a 2008 Competition Commission Market Investigation into the groceries sector. The Competition Commission found that while the sector was broadly competitive, some large retailers were transferring excessive risk and unexpected costs to their direct suppliers. This could discourage suppliers from investing in quality and innovation; small businesses could fail and ultimately, there could be potential disadvantage to consumers. Following the Commission’s recommendation, the Government introduced the Groceries Supply Code of Practice (the Code) in 2010, designed to regulate the relationship between the 10 retailers at the time with UK annual groceries turnover of more than £1 billion (the regulated retailers) and their direct suppliers. The regulated retailers had some time to set up a voluntary Ombudsman; the GCA was established on a statutory basis when the self-regulatory approach did not progress.

Christine Tacon – the first Adjudicator – is responsible for monitoring and encouraging compliance with and enforcing the Code. The GCA is funded by a levy on the regulated retailers. Suppliers, trade associations and other representative bodies are encouraged to provide the GCA with information and evidence about how the regulated retailers are treating their direct suppliers. All information received is dealt with on a confidential basis and the GCA has a legal duty to preserve anonymity.

In 2016 the Government carried out a statutory review of the GCA’s performance and effectiveness and at the same time called for evidence on the extension of the GCA’s powers. The results of the review published in July 2017 concluded that the GCA is regarded as an ‘exemplary modern regulator with an international reputation’. Following the call for evidence, Ministers decided not to extend the remit however the Competition and Markets Authority (CMA) was asked to assess whether more groceries retailers should be regulated by the GCA. On 1 November 2018 the CMA designated two additional retailers under the Groceries (Supply Chain Practices) Market Investigation Order.

GCA Powers

At a supplier’s request the GCA must arbitrate in disputes and may also do so following a request from a regulated retailer. Arbitration awards are binding and may include compensation.

The GCA can launch investigations. If a breach of the Code is found, the GCA can make recommendations, require regulated retailers to publish details of any breach and in the most serious cases impose a fine. The GCA power to fine a retailer up to 1% of its UK turnover came into force on 6 April 2015. Under the Code the regulated retailers are obliged to deal fairly and lawfully with groceries suppliers across a range of supply chain practices. These include: making payments on time; no variations to supply agreements without notice; compensation payments for forecasting errors; no charges for shrinkage or wastage; restrictions on listing fees, marketing costs and De-listing. This list is not exhaustive and full details are available at www.gov.uk/gca.

The Code does not cover issues such as price setting, the relationship between indirect suppliers and the regulated retailers, food safety or labelling. These issues are outside the GCA’s remit.

The way the GCA works

The GCA encourages suppliers to continue to bring Code issues and evidence to its attention in order to inform decisions and actions. The GCA also gathers information from retailers, trade associations and others. The stronger the evidence base, the greater the justification for action.

As a small regulator the GCA must effectively prioritise its activities. When considering whether to launch an investigation and other activities, the GCA applies the following four prioritisation principles, which are set out in its statutory guidance:

| Impact: | The greater the impact of the practices raised, the more likely it is that the GCA will take action |

| Strategic importance: | Whether the proposed action would further the GCA’s statutory purposes |

| Risks and benefits: | The likelihood of achieving an outcome that stops breaches of the Code |

| Resources: | A decision to take action will be based on whether the GCA is satisfied the proposed action is proportionate |

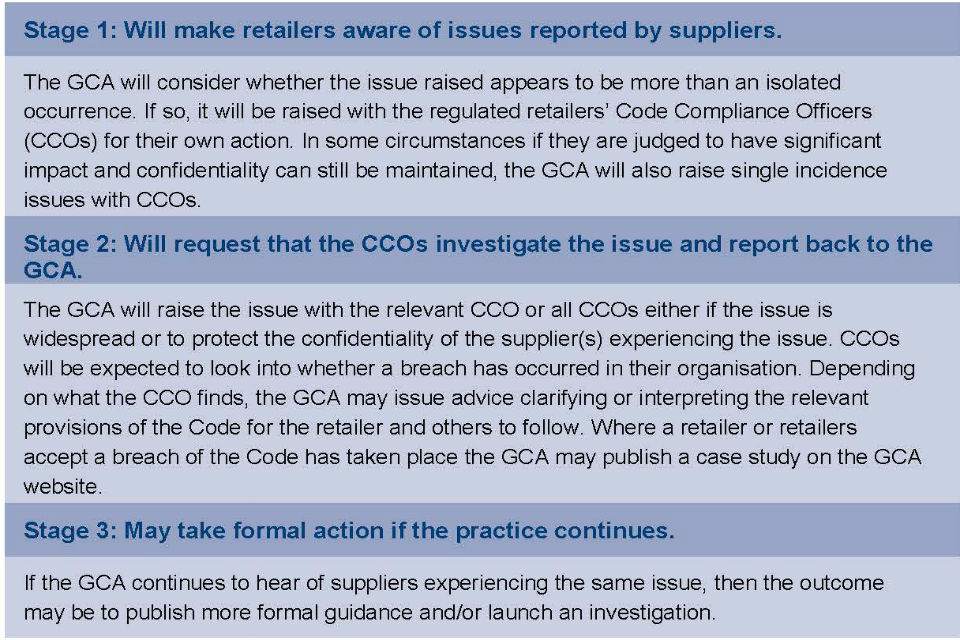

The GCA must carry out its statutory functions set out in the Groceries Code Adjudicator Act 2013. In setting the direction for the GCA, the Adjudicator has developed an approach that fits the resources available and the outcomes the GCA was set up to deliver. It is a modern regulatory approach, with collaboration and business relations at its core and is delivered through a three- stage process. When Code-related issues are raised, the GCA follows the stages set out below.

Stage 1: Will make retailers aware of issues reported by suppliers. Stage 2: Request the CCOs investigate the issue and report back to the GCA. Stage 3: May take formal action if the practice continues.

Through this process the GCA ensures that issues are raised with and promptly considered by the regulated retailers and that any necessary action is agreed and taken as swiftly as possible. This is an efficient way to deal with current groceries sector practices that may not be consistent with the Code. The GCA believes that this collaborative approach has a dual benefit. It significantly reduces the cost of regulating the retailers and it delivers results more quickly.

The GCA does not act as a complaint handling body, nor can it advise on individual disputes where a supplier seeks a view on whether a regulated retailer has breached the Code. This is because the GCA may later be asked to arbitrate in the same dispute between the supplier and the regulated retailer or may later launch an investigation into the practice raised by the supplier if it becomes apparent that it is a systemic issue experienced by a number of suppliers and of significant impact. Providing a view on individual cases could compromise the GCA’s objectivity. Instead, the GCA encourages suppliers to approach CCOs directly because they can deal with issues quickly and, where needed, discreetly.

The ultimate goal of the GCA is to promote a stronger, more innovative and more efficient groceries market through compliance with the Code and, as a result, to bring better value to consumers. The GCA is working with suppliers and the regulated retailers to respond to issues rapidly and relies on suppliers and others to bring evidence of non-compliance quickly to the GCA to achieve this goal.

2. Performance Analysis

2.1 Statutory Reporting Requirements

The GCA’s key performance indicators are set out in the Groceries Code Adjudicator Act 2013 as statutory reporting requirements. There are four statutory reporting requirements on which performance is measured and the performance against these objectives is set out in the table below.

| Disputes referred to arbitration under the Groceries Supply Order |

| The GCA accepted appointment as arbitrator in no disputes in the reporting period. |

| Investigations carried out by the GCA |

| The GCA concluded the investigation into Co-operative Group Limited on 25 March 2019. This was the GCA’s second investigation. |

| Cases in which the GCA has used enforcement measures |

| The GCA made recommendations to Co-operative Group Limited. |

| Recommendations that the GCA has made to the Competition and Markets Authority for changes to the Code |

| The GCA has made no recommendations to the Competition and Markets Authority for any change to the Code. |

2.2 Strategic Objectives

In addition to the statutory reporting requirements, the GCA also monitors its performance against four strategic objectives:

- Promoting the work of the GCA

- Providing advice and guidance

- Acting on supplier issues and information

- Improving the culture of Code compliance

The GCA considers that these objectives remain fit for purpose.

Objective 1: Promoting the work of the GCA

The GCA built on the success of the Code Confident campaign launched the previous year, which encourages suppliers to ‘Know the Code; Get Trained; and Speak Up’. The Code Confident logo is carried on many GCA publications and on a pack aimed at suppliers containing information about the Code and the role of the Adjudicator. Nearly 2,000 of these packs were distributed this year, helping to raise awareness among suppliers.

The Adjudicator and her team have attended over 40 trade and supplier events across the UK. These included trade shows, conferences and trade association meetings and covered a range of activity including presentations from the GCA, participation in supplier workshops and networking. The GCA exhibited at three trade shows and visited many more to meet suppliers, explain the role of the GCA and hear about Code-related issues. Attending events where there are large numbers of suppliers present and walking around to speak to them has proved an excellent way of getting the GCA’s Code Confident message directly to those that need to hear it. The GCA and her team have held over 90 one-to-one meetings with suppliers, hearing directly from them about their experiences of working with retailers. The GCA also attended an event in Denmark for Nordic groceries suppliers to the UK and elsewhere.

The GCA website, YouTube channel and regular newsletter continue to play an essential role in raising awareness and keeping suppliers up to date. There is a steady stream of people viewing the information and watching relevant GCA videos. The newsletter goes to over 1,550 subscribers.

The fifth annual survey was open during March and April 2018. This was promoted through advertising in The Grocer and work done by retailers and trade associations to encourage their suppliers and members to complete it. The GCA also raised awareness directly at trade shows, including hosting a stand at Food and Drink Expo where suppliers could complete the survey. There was a strong response rate which gave the GCA important information about what retailer practices were still of concern to suppliers. The top three issues suppliers said they had experienced over the past 12 months remained the same: delay in payments; no compensation for forecasting errors or not preparing forecasts with due care; and not meeting duties in relation to De-listing. However, the percentages of suppliers that had experienced these issues had fallen from the previous year.

Over 250 people attended the GCA annual conference held at Church House, Westminster in June 2018. This followed the successful format of a review of the year and forward look from the GCA as well as presentation of the results of the annual survey by YouGov. There was a keynote address by the then Minister of State, Andrew Griffiths MP, and a presentation by Nick Downing from the IGD. After the main conference the GCA and her team met 20 suppliers in one-to-one meetings.

There are over a dozen organisations that provide training on the Code. They play an important role in educating suppliers and raising awareness of the Code. Some of the training providers update the GCA on what Code-related issues they are hearing about from suppliers and report the number of delegates they have trained: two have trained over 250 delegates in 2018. Code Compliance Officers (CCOs) also play an essential role in raising awareness of the Code and the GCA among each retailer’s suppliers.

As a result of these awareness-raising activities there has been a continual flow of supplier feedback directly reported to the GCA. This not only demonstrates the value of the GCA’s initiatives in this area but shows that this work is improving supplier awareness and knowledge. The increase in information reported helps the GCA to understand the issues suppliers are experiencing and priority to raise with retailers, as well as enabling conversations with suppliers to alert them to relevant GCA published material on how they can help to put matters right. The GCA is grateful to all those that provide information about their experience of working with retailers and encourages more suppliers to get trained in the Code and speak up to the CCOs and the GCA office. The number of suppliers raising issues with the GCA either at one-to-one meetings or through calls and e-mails remained at a good level. This continues to show the high degree of confidence suppliers have in reporting issues to the GCA.

Objective 2: Providing advice and guidance

The GCA has continued to produce advice and guidance that responds to concerns raised by suppliers and retailers and to clarify the Code.

Annual Compliance Reports

Advice was provided to retailers about how to improve their annual compliance reports, in particular encouraging them to report more comprehensively in their published annual reports and accounts.

Progressing Top Issues

The GCA published a revised best practice statement on forecasting which included the issue of promotions. In this it was reiterated that retailers should consider what improvements they could make to the transparency of their communications with suppliers about forecasting, to allow suppliers to meet orders and to anticipate and calculate the full costs of supply. While reiterating the ways this may be achieved the GCA also added that retailers should consider explaining to suppliers how to get compensation for inaccurate forecasting, when it might be due and who to talk to; should consider the extent to which retailers might offer compensation for inaccurate forecasting; and understand that the due care test is unlikely to be capable of being met by a retailer that provided no way for a supplier to contribute to the forecasting process, whether collaboratively in reaching agreed volumes to be ordered or by ensuring suppliers can raise questions and queries if a forecast seems to them to be inaccurate or to have resulted in an excessive order.

There were additional points made in relation to promotions including that retailers should ensure that buying-in periods for promotions were reasonable, in particular not exceeding the shelf life of the products, and ensuring that timelines are adhered to and commitments to promotions are delivered in store.

Other activity is recorded in the Top Issues section of this annual report.

Objective 3: Acting on supplier issues and information

Raising Issues with CCOs

The GCA continued to have regular meetings with CCOs throughout the year. These are used to raise issues across all regulated retailers as well as with individual retailers. In some circumstances the GCA will raise issues outside the usual meeting round, for example where there is some urgency for the CCO to look into them or the GCA decides to intensify the collaborative approach with a particular retailer.

Issues raised with the GCA by suppliers either directly or through the annual survey are crucial to identifying the work to be done with retailers. They have helped the GCA to determine where to intensify the collaborative approach with retailers, leading to the publication of case studies or the launch of an investigation, as well as helping to inform the GCA’s decision about which issues to prioritise with all regulated retailers and how supplier concerns can best be addressed by retailer action. Where issues have been escalated with a retailer and have been addressed effectively, suppliers notice a difference and retailers often make systems or process improvements which benefit their businesses and the wider supply base.

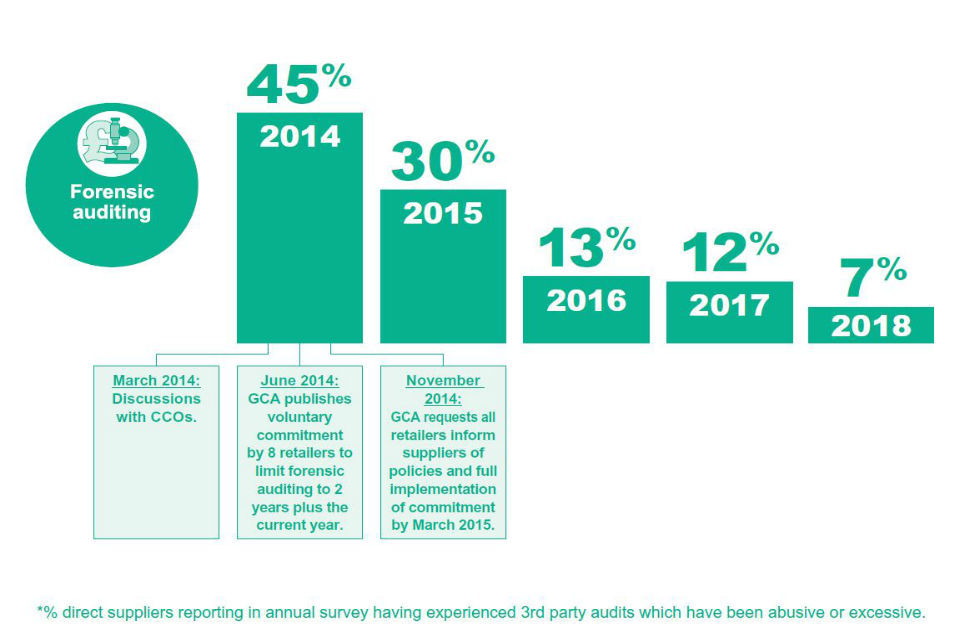

The GCA also published a list of supplier helplines set up to enable suppliers to have finance-to-finance discussions with retailers without the need to involve buyers in resolving payment and invoicing issues and to help retailers identify the root causes of issues suppliers are facing and to put them right. This was a consequence for all retailers of a recommendation made in the report of the investigation into Tesco plc, published in 2016, which established a benchmark for the standard of Code compliance expected of all retailers.

Monitoring progress on supplier issues

Individual reports from suppliers as well as the annual survey contribute significantly to the work of the GCA and together help to identify the areas to focus on. Where an issue has been tackled with retailers the GCA monitors this and continues to publish impact charts from the annual survey which demonstrate the progress made. Where suppliers raise issues and the GCA focuses on tackling them, suppliers really do notice a change in retailer behaviour. These impact charts are set out in the Top Issues section of this annual report.

Objective 4: Improving the culture of Code compliance

The GCA continues to emphasise the need for cultural and behavioural change in retailers and considers that progress in this area had been made. This is regularly raised in conversations with chairs of retailer audit committees as well as on visits to retailer headquarters. Suppliers report that the behaviour of retailers has changed significantly since the GCA was appointed. Improving the culture of Code Compliance has been a feature of two GCA Code clarification case studies as well as the recently published report of the investigation into Co-operative Group Limited. The recommendations, which cover issues such as governance, audit, training, systems and processes will be implemented by Co-op and monitored by the GCA. They also reflect the standard of Code Compliance set by the report which all regulated retailers must meet.

2.3 Annual Survey 2018

In 2018 the GCA maintained its practice of commissioning YouGov to carry out a survey of the groceries sector. This fifth GCA survey was designed to build on the GCA’s understanding of current supplier concerns in the sector and measure progress towards Code compliance. These issues included how far retailer behaviour had improved in the year and more detailed information about supplier views on retailer compliance with the Code. There was also a new question for 2018 which asked whether retailers conducted trading relationships with suppliers fairly, in good faith and without duress, reflecting some suppliers’ perceptions of this as a measure of the quality of their supply relationships overall.

YouGov presented the results to the GCA conference in June 2018.

Participants

The retailers again supported the GCA survey by sending links to their direct suppliers, including those based overseas. Participation remained high, albeit with responses slightly down on the record number received in 2017. A total of 1,045 responses were received, including 911 from direct suppliers, 133 from indirect suppliers and 28 trade associations.

The number of suppliers stating that they had experienced issues that could be breaches of the Code again fell in 2018 with 43% reporting issues, down from 56% in 2017.

All retailers were reported as having improved over the last year with Tesco plc the most improved (Table 1) for the third survey running. Wm Morrison Supermarkets plc, Asda Stores Ltd and Co-operative Group Limited also showed good progress. Each of these retailers had clearly learned from the enhanced engagement with the GCA as a result of investigations or activity leading to case studies.

Shows Tesco plc as the most improved retailer for the 3rd year running. Morrisons, Asda and Co-op have also improved by more than 10% in the past 12 months.

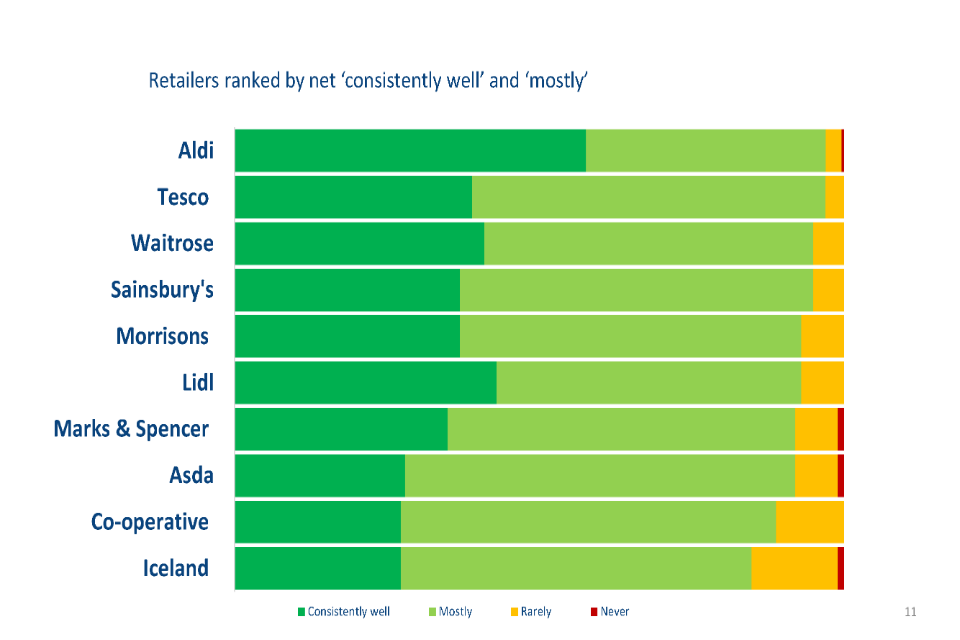

Views by suppliers on the overall assessment of compliance with the Code

Aldi Stores Ltd was again considered by direct suppliers to be the retailer that complied most with the Code, placing the retailer for the fifth consecutive year top of the 2018 survey (Table 2).

From the survey results, Iceland Foods Limited (Iceland) was assessed by its suppliers as overall being the retailer least likely to comply with the Code. This was the same as 2017 but in both years suppliers reported low levels of specific Code issues. The GCA worked with Iceland to understand why suppliers felt at risk when negotiating with the retailer.

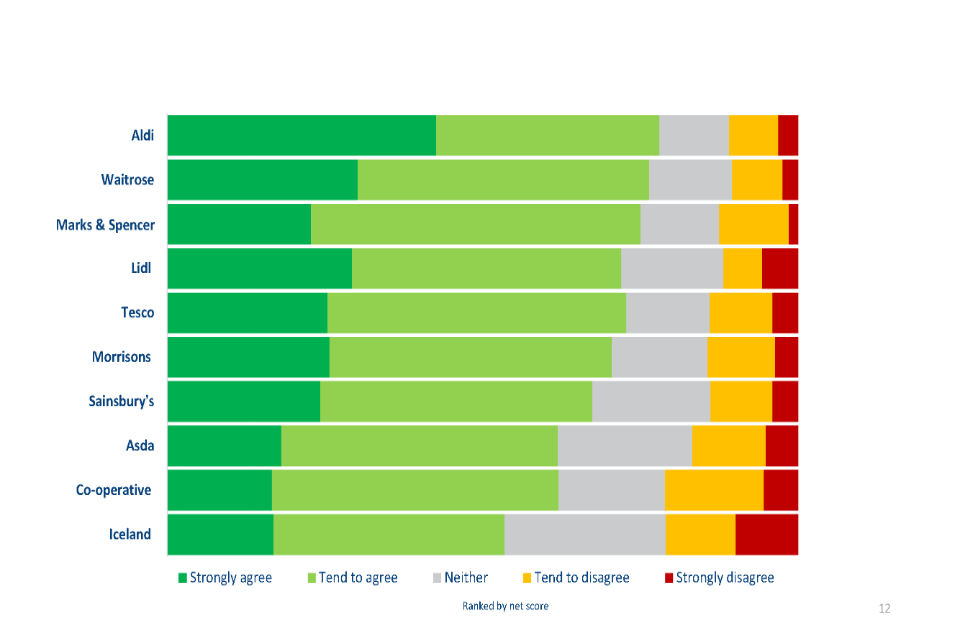

Aldi tops the table for assessment of whether retailers conduct trading relationships with suppliers fairly, in good faith and without duress.

In 2018, partly as a result of this work with Iceland, a new question was introduced to the survey. This question asked whether suppliers believed each of the retailers conducted its trading relationships fairly, in good faith and without duress. The results are set out in Table 3.

Decorative

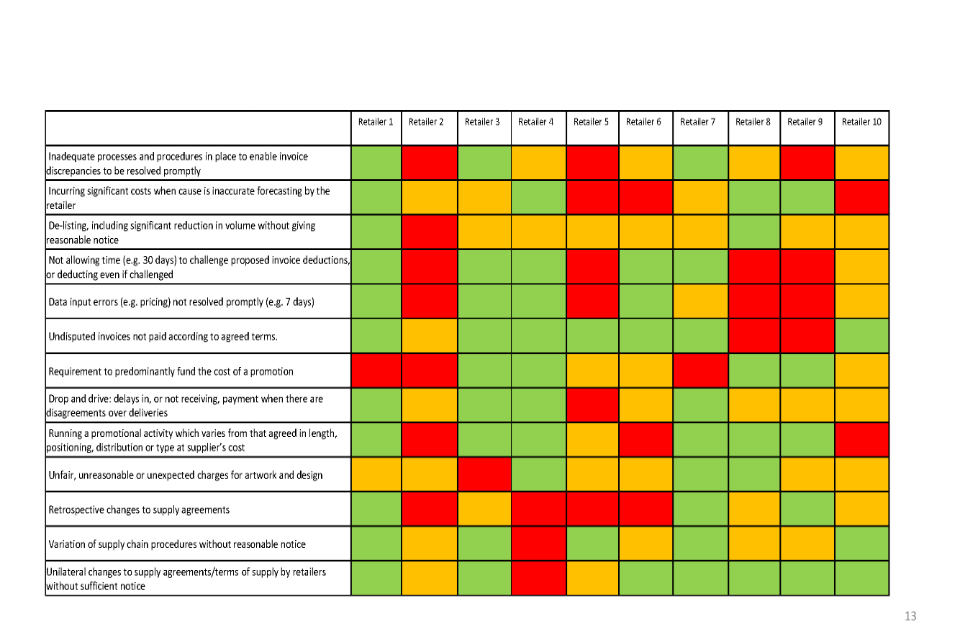

Using data to drive better behaviour

As well as measuring overall performance the YouGov survey focused on specific Code-related areas for each retailer. Table 4 shows some of the results. The retailers are anonymised and presented in no particular order. The survey used a traffic light system to show where retailers were performing better than average (green) and below average (red).

It offered the GCA a valuable tool to encourage retailers to improve performance in particular areas, even if their overall rating was good. It also provided valuable insight for the CCOs.

Decorative

It offered the GCA a valuable tool to encourage retailers to improve performance in particular areas, even if their overall rating was good. It also provided valuable insight for the CCOs.

Code Issues

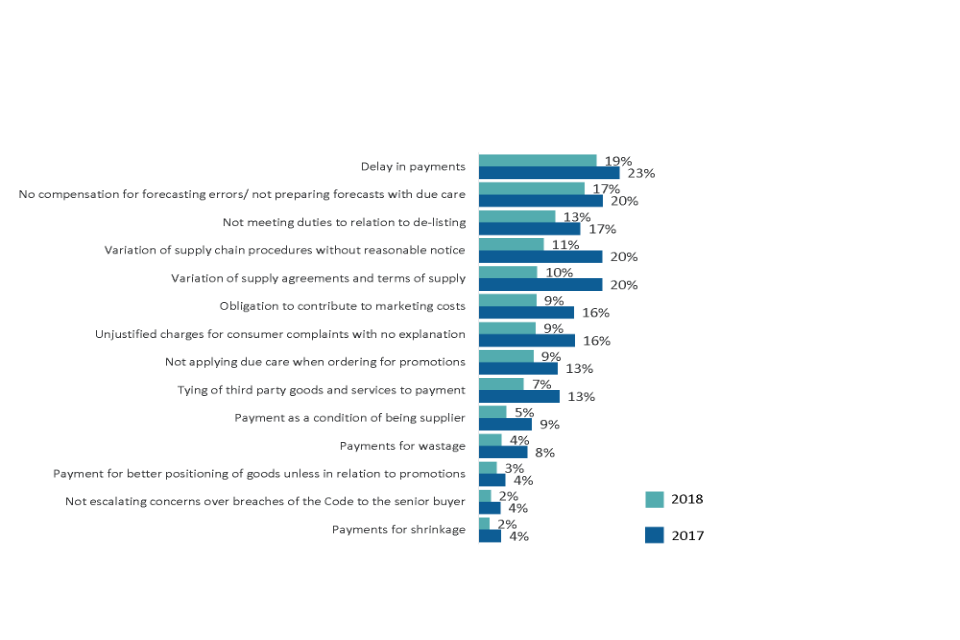

The annual survey identified that the most common issues reported by suppliers were delay in payments (19%), no compensation for forecasting errors or not preparing forecasts with due care (17%), and not meeting duties in relation to De-listing (13%), as shown in Table 5. This information helped to inform the GCA’s activities with retailers throughout 2018/19.

Decorative

Training

As a key element of the Code Confident Campaign, the Adjudicator continued to prioritise promoting to suppliers the importance of training so they could use the Code effectively in negotiations with retailers. This was reflected in the 2018 survey which showed a rise in the number of direct suppliers who had undertaken training, from 39% in 2017 to 49% in 2018.

Raising an issue with the GCA

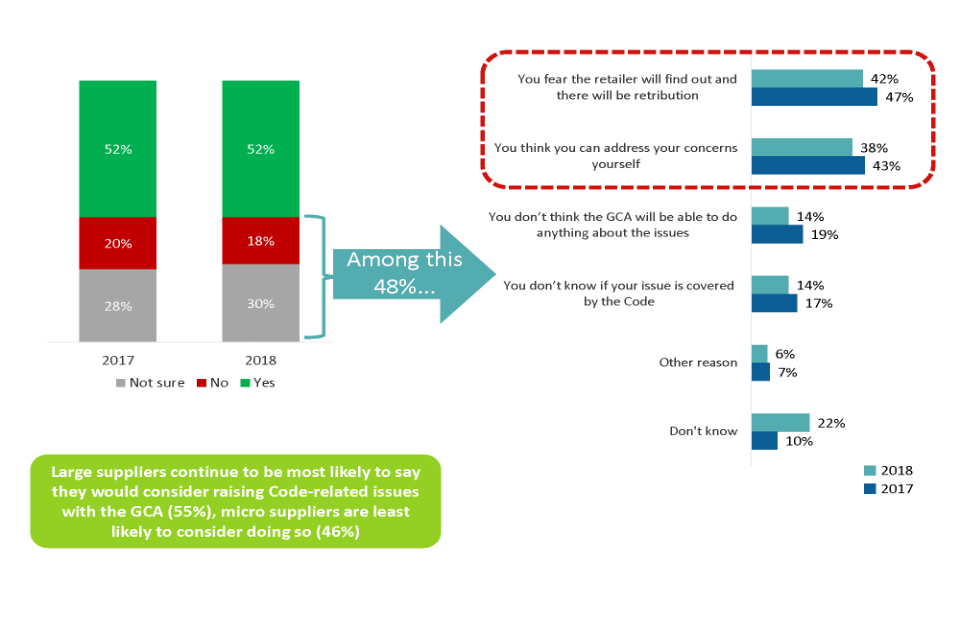

The number of direct suppliers who felt they had a good or fair understanding of the Code rose slightly from 78% in 2017 to 79% in 2018, with 75% saying they had a good or fair awareness of the GCA’s role and responsibilities.

The proportion of suppliers who said they would not raise an issue with the GCA or were unsure whether they would do so stayed the same, at 52%. The 48% who said they would not raise an issue with the GCA or were not sure if they would indicated the reasons for this were a fear the retailer would find out and there might be adverse consequences or that they could simply address the issues themselves (Table 6).

Decorative

The Adjudicator has continued to work hard to assure suppliers that they can bring issues to the GCA, confident that their identities will be protected. There was a significant increase in the number of issues brought forward over 2017 and in the period leading up to the 2018 survey. At all public engagements the Adjudicator offers suppliers the opportunity to have one-to-one meetings, during which the duty to maintain supplier confidentiality is reiterated to each of them.

2.4 Significant Activities

The following section reproduces the core content of any GCA publications concluding significant activities in the year.

1. Report of the investigation into Co-operative Group Ltd

On 25 March 2019 the GCA published the report of the investigation into Co-operative Group Ltd. The Executive Summary is reproduced here. The full report is available at www.gov.uk/gca.

Executive Summary

This summary sets out in brief my findings and decisions.

Findings on De-listing without reasonable notice

Paragraph 16 of the Groceries Supply Code of Practice (the Code) states: “Prior to De-listing a Supplier, a Retailer must… provide Reasonable Notice to the Supplier of the Retailer’s decision to De-list.” The De-listing Guidance and Supplementary De-listing Guidance that I published to help Retailers to interpret paragraph 16 of the Code set out a number of factors for a Retailer to consider when deciding “significance” of a reduction in the volume of purchases being made from a Supplier and what amounts to “reasonable notice”, confirming that both would vary from case to case.

I find that Co-op applied the Code wrongly in relation to the reasonable notice requirement of paragraph 16. I find that Co-op De-listed Suppliers with no, or short, fixed notice periods that were not reasonable in the circumstances. These were applied unilaterally without due consideration of the De-listing Guidance. These De-listing decisions included but were not limited to decisions issued between summer 2016 and summer 2017 as part of the Co-op Right Range Right Store programme. Further, when making volume changes, I found that Co-op did not always correctly consider significance to determine whether the De-listing requirements of the Code were engaged. This conduct was not compliant with the Code. I find that Co-op broke paragraph 16 of the Code.

Co-op applied standard notice periods on numerous occasions without any consideration as to the particular circumstances of the product or Supplier in question. This was contrary to the Code, my De-listing Guidance and my Supplementary De-listing Guidance, all of which specify that notice of De-listing should be considered on a case-by-case basis.

Co-op failed to identify what decisions might result in significant reductions in the volume of groceries bought from Suppliers and at times to deal with them in a Code-compliant way by giving reasonable notice in accordance with paragraph 16.

Scale and impact on Suppliers of De-listing without reasonable notice

The evidence I have received indicates that a significant number of Suppliers have been affected by De-listing without reasonable notice. This includes Suppliers of various sizes and across different categories of the Co-op groceries business.

For a large number of the Suppliers that I received evidence from, there was no or very little financial impact from the short notice given to them of De-listing. However for a number of Suppliers the lack of notice of a significant reduction in orders or removal of a product resulted in them incurring significant costs which might have been avoided had they received reasonable notice. In addition, for several Suppliers, the short notice given of distribution reductions or product removals resulted in wastage of packaging and products. Other consequences of De-listing without reasonable notice included adverse effects on the efficiency of Suppliers’ businesses, the resources used by Suppliers trying to obtain information from Co-op and uncertainty about the stock Suppliers would be required to provide to Co-op at any given time.

Root causes of De-listing without reasonable notice

Compliance risk management, proactively undertaken at all levels in the business

There was inadequate governance to oversee and manage compliance with the De-listing requirements of the Code. Co-op did not take adequate steps to reassure itself that it was acting in compliance with paragraph 16 of the Code. This meant that Co-op did not recognise when there were problems with Code compliance, such as buyers failing to give reasonable notice of De-listing. It also failed properly to identify and oversee De-listing decisions that were effectively being taken outside the commercial team. There was not enough focus within the organisation on compliance with the Code and it mistakenly relied on a wrongly held belief that because of its brand values, Suppliers would highlight to Co-op any concerns that they had. Where problems were identified Co-op did not appreciate the level of change required to rectify the problem or lacked the systems to implement the changes that were necessary.

Legal, compliance and audit functions working to support Code compliance

There was insufficient legal, compliance and audit support to deliver compliance with paragraph 16 of the Code and prevent De-listing without reasonable notice. This meant that the failure to give reasonable notice of De-listing and the root causes of these failures continued over a sustained period of time without effective internal challenge.

Internal systems and processes working to support Code compliance

Co-op IT systems contributed to its failure to comply with paragraph 16 of the Code. One of the main issues was the absence of a central IT system that could be accessed by all relevant Co-op employees who were dealing with Suppliers. Another particular problem was that the IT systems restricted the notice that could be given to Suppliers of distribution changes arising from the range review process. These systems did not allow consideration of what might be reasonable notice of any De-listing for a Supplier and effectively prevented Co-op from delivering on the notice periods set out in its own internal policy.

Training on paragraph 16 of the Code

The training which Co-op provided was inadequate to equip buyers to identify decisions that might result in a significant reduction in the volume of a product or products ordered from a Supplier or properly to consider on a case-by-case basis what might amount to reasonable notice of De-listing for any particular Supplier.

Individuals from both within and outside the Co-op buying team were inadequately trained to recognise and raise concerns about Code compliance. The failures in training were compounded by the weaknesses in the Co-op policies and process documents, which did not adequately equip buyers properly to perform their roles and to assess significance and reasonable notice in compliance with the Code.

Communication between the Retailer and Suppliers facilitating Code compliance

At times there was a lack of communication by Co-op with Suppliers about decisions that might amount to De-listing. Many Suppliers were not given the opportunity to explain or discuss the impact of De-listing decisions before they were made and notice periods fixed. This meant that Co-op did not always have the information it needed to determine significance and reasonable notice on a case-by-case basis. Moreover, because at Co-op other parts of the business outside the commercial team could make decisions that affected ranging, it was not possible for Co-op to be assured that all information relevant to the assessment of significance was properly taken into account.

Findings on variation of Supply Agreements without reasonable notice

Paragraph 3 of the Code states: “If a Retailer has the right to vary a Supply Agreement unilaterally, it must give Reasonable Notice of any such variation to the Supplier.” I have published three case studies on paragraph 3 of the Code which make quite clear the point of interpretation about reasonable notice. I find that Co-op unilaterally and without reasonable notice varied its Supply Agreements with Suppliers by its application of depot quality control charges and benchmarking charges. This conduct was not compliant with the Code. I find that Co-op broke paragraph 3 of the Code. This caused particular difficulties for Suppliers with fixed cost contracts, which would not have been able to amend their cost prices accordingly.

In some cases Co-op did not provide sufficiently clear or detailed information to Suppliers about depot quality control charges and benchmarking charges to enable them to form reasonable estimates of the amount and frequency of the charges. Co-op buyers were not aware of the likely amount and frequency of these charges and were accordingly unable to give notice of them. Co-op did not appear to consider what constituted reasonable notice of the application of either of the charges for Suppliers on fixed cost contracts because of a failure to understand the Code.

Scale and impact on Suppliers of variation of Supply Agreements without reasonable notice

The failure to give reasonable notice of depot quality control charges affected Suppliers of fresh produce and Suppliers of meat. The failure to give reasonable notice of benchmarking charges affected only Suppliers of own-label products.

Following my raising of the issue with Co-op and an intense period of escalation, some Suppliers received large sums as refunds for depot quality control charges and benchmarking charges which Co-op determined had been applied without reasonable notice. Suppliers from which I received evidence gave mixed views as to the significance of the amounts they had been charged by Co-op without reasonable notice; many considered the charges to be a cost of doing business or that they were not significant enough to warrant being challenged. There were other consequences of variation of Supply Agreements without reasonable notice for some Suppliers including the administrative burden of checking what they had been charged and trying to challenge charges and operating in an uncertain environment in which they would be expected to absorb unforeseen costs.

Root causes of variation of Supply Agreements without reasonable notice

Compliance risk management, proactively undertaken at all levels in the business

Co-op failed to identify the risk to Code compliance associated with depot quality control and benchmarking charges being applied not by buyers but by other parts of the Co-op business or in the case of depot quality control charges, the independent co-operative societies. Co-op failed to demonstrate to me its oversight of the proposed charges, when they would be applied and with what notice. There was a lack of recognition across the Co-op business that it had proactively and consistently to manage its Code compliance risk in relation to paragraph 3 of the Code.

Legal, compliance and audit functions working to support Code compliance

Co-op legal, compliance and audit functions did not appear adequately to have worked together to develop or to oversee any policy or rationale governing the circumstances in which charges would be applied.

There was not sufficient co-ordinated oversight of Co-op systems by Co-op legal, compliance and audit functions to ensure Code compliance. The co-ordinated engagement of these functions with the systems and policies relating to charges happened too late to ensure or to compensate for lack of Code compliance. Internal systems and processes working to support Code compliance.

One of the root causes of the failure to give Suppliers reasonable notice of the application of depot quality control and benchmarking charges was that Co-op unreasonably relied on its portal as the principal or only way of communicating with Suppliers about variation to Supply Agreements. Co-op informed me that the primary method it used to communicate with Suppliers about changes to its terms and conditions was updating documents contained on the portal. Co-op was not however entitled to assume that Suppliers who continued to use its portal were on notice of any change to charges.

Co-op systems also failed to support Code compliance in relation to Suppliers’ challenges to charges.

Training on paragraph 3 of the Code

Co-op failed to recognise the importance of ensuring that all employees who have the ability to apply charges or otherwise to affect a Supplier’s commercial arrangements with Co-op are trained on the Code. Co-op training material did not adequately deal with the issue of variation of Supply Agreements or explore on a case-by-case basis what constitutes reasonable notice under paragraph 3 of the Code.

Communication between the Retailer and Suppliers facilitating Code compliance

Buyers’ lack of awareness of the charges and consequential inability to discuss them with Suppliers caused particular problems in circumstances where the portal, which Co-op used as the primary means of communicating with Suppliers, was not fit for purpose.

I note nonetheless that I did not identify any concerns with the nature and tone of communication by Co-op, either internally or with its Suppliers. Correspondence was broadly courteous and reflected the commercial nature of Supplier relationships.

Enforcement measures

The enforcement measures available to me as a result of finding that Co-op broke the Code were to make recommendations, to require information to be published and to impose financial penalties.

I consider Co-op’s breach of the Code to be serious because I have found that both paragraphs 16 and 3 of the Code were broken and a significant number of Suppliers were affected by its conduct. I have decided that recommendations are a proportionate and effective measure to reduce the likelihood of repetition of non-compliance with paragraphs 16 and 3 by Co-op. I also believe that the implementation of those recommendations will provide greater certainty to Suppliers that in future, any De-listing or variation of Supply Agreements will be carried out in accordance with the Code.

My recommendations are as follows:

1. Co-op must have adequate governance to oversee and manage its compliance with the Code.

2. Co-op legal, compliance and audit functions must have sufficient co-ordinated oversight of Co-op systems to ensure Code compliance.

3. Co-op IT systems must support Code compliance.

4. Co-op must adequately train on the Code all employees who make decisions which affect a Supplier’s commercial arrangements with Co-op.

5. Co-op must in any potential De-listing situation communicate with affected Suppliers to enable Co-op to decide what is a significant reduction in volume and reasonable notice.

I will engage with Co-op to ensure that the recommendations are implemented efficiently and effectively. I require Co-op to provide a detailed implementation plan within four weeks of the publication of this report setting out how it will comply with my recommendations. Co-op will then be required to respond to the recommendations on a quarterly basis and I will set reporting metrics for this purpose.

I do not consider the nature and seriousness of the breaches by Co-op to merit a financial penalty.

2.5 Top Issues

The GCA has a range of issues referred to it from direct and indirect suppliers, trade associations, other bodies and the media. These issues give the GCA vital information to inform current and future action.

In order to ensure the GCA meets the duty to preserve the confidentiality of those who provide information, the GCA will not publish statistical information on issues raised. A table of issues raised is included as an Appendix to this report.

Taking into account the information received about retailer practices, applying the GCA’s published prioritisation principles and in keeping with the collaborative approach, the GCA identifies on an iterative basis up to five key areas to focus on where suppliers believe that the regulated retailers’ practices may breach the Code. The GCA puts these Top Issues into three categories (current, monitored and previous) and keeps them under regular review, responding to changing supplier concerns and retailer activity. These issues are raised with CCOs and discussed on an ongoing basis with them at their individual meetings.

The current issues are the main focus of the GCA’s attention at any one time, whether because the GCA needs to understand more about them or because they reflect significant ongoing work. Retailers report progress against these issues at meetings with the GCA.

The monitored issues are those on which the GCA has made its position clear or retailers have committed to carrying out some form of action, and the GCA wants to continue to monitor supplier feedback on the issue and what steps retailers have taken. These are reviewed a year after being categorised as monitored and thereafter they are either moved back into current issues, remain as monitored or moved into previous, depending on whether or not they remain of concern.

If an issue is classified as previous, this means it has been closed as an issue in its own right because the GCA’s position or interpretation of the Code has been made clear and the Adjudicator no longer considers that ongoing monitoring or active work on the issue is merited.

Supplier feedback on all issues, remains welcome and the GCA will take it into account when considering from time to time whether there are grounds to change the status of any particular issue.

This year, delay in payments, forecasting and promotions were moved to the monitored category. Pay to stay and payments for better positioning were moved to the previous category following a review of retailer progress on those issues and because the annual survey results indicated they were no longer of concern to suppliers. There were no new current issues. The GCA continues to review supplier feedback on the issues they are experiencing.

The GCA is working with the additional designated retailers on all the Top Issues regardless of whether they are classified as monitored or previous.

The status of the Top Issues at the end of the reporting year was as follows:

3 shopping baskets with roundels in 2 of them. Each circle represents a different Top Issue, there are no current top issues.

Monitored Top Issues

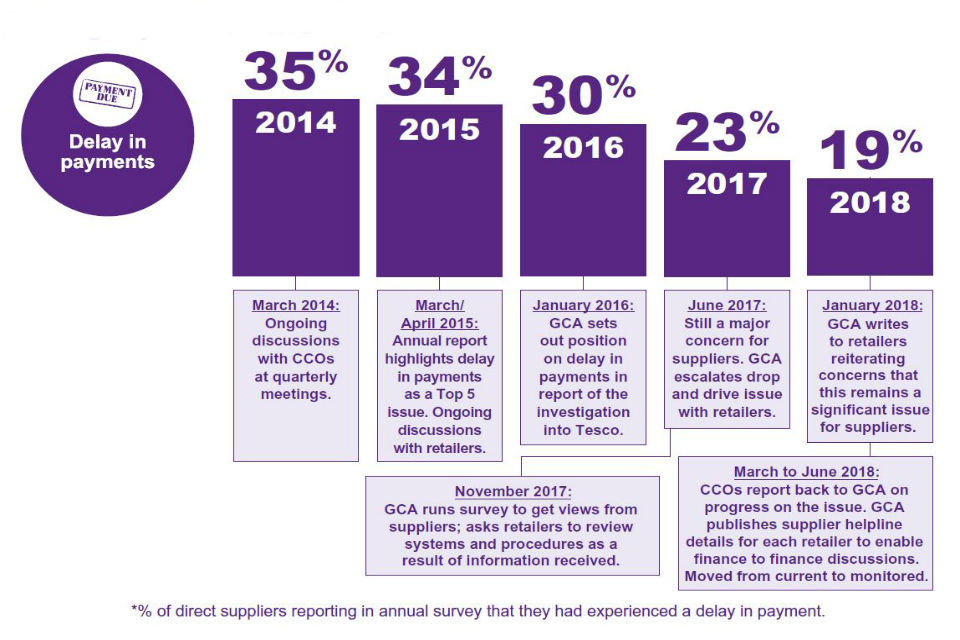

Delay in payments

Description

The report of the investigation into Tesco plc stated clearly for the benefit of all in the sector how the GCA interpreted the practices found to have taken place in relation to delay in payments. Some of the practices that might lead to delay in payments are unilateral deductions relating to drop and drive disputes, duplicate invoices, alleged short deliveries, unknown or unagreed items; current and historic promotion fees. Further practices that might lead to delay in payments include delays in paying entire invoices where only part of an invoice is disputed, not paying in the period set out in the supply agreement, the length of time taken by the retailer to resolve an issue, and depot and retailer haulier practices.

Potential Code breach

The GCA considers the effect of unilateral deductions and not paying to terms falls under part 4 (paragraph 5) of the Code: No delay in Payments, read with part 2 (paragraph 2) of the Code: Principle of fair dealing.

GCA progress

The interpretation of the Code set out in the report of the investigation into Tesco plc is a clear statement of the GCA’s view as to what is and is not Code-compliant behaviour and as such, is the regulatory standard required to be met by all regulated retailers. This makes clear that suppliers should be given at least 30 days to challenge any proposed deduction and where this is challenged, a retailer is not entitled to deduct the disputed sum from the supplier’s trading account until the query is resolved. Data input errors should be resolved promptly and in particular, pricing errors should be resolved within seven days of notification by the supplier.

Delay in payments remained the number one concern highlighted by suppliers in the 2018 survey, as it was in 2017, and continued to be an issue reported directly to the GCA by suppliers. In particular, the GCA continued to hear that not all retailers had adequate systems and processes in place fully to demonstrate compliance with the GCA’s interpretation of the Code on delay in payments as set out in the report of the investigation into Tesco plc. Recurring themes involving delay in payments included the persistence of unilateral deductions and the practice of holding back entire invoices while one element is queried, as well as too much time taken to resolve disputes.

As a result of the Tesco investigation, the GCA recommended the retailer set up a single point of contact for suppliers to resolve queries and went on to suggest that an effective way to do this would be to set up a supplier helpline to handle payment disputes without involving its buying teams. To facilitate finance-to-finance conversations between retailers and suppliers the GCA asked all retailers to explain what arrangements they have in place for a supplier helpline or other means to enable disputes and queries to be handled without the involvement of commercial teams publicised these arrangements on its website.

The GCA continued to monitor retailer compliance on this issue and provided retailers with examples of practices reported by suppliers where delays in being paid could arise. In particular, the GCA: escalated the issue of drop and drive (see separate issue under Previous Top Issues) and all retailers who engage in it explained the actions they are taking to minimise the risk of breaches of the Code arising as a result of that practice; and gathered more detailed feedback from suppliers about delay in payments in a mini survey.

Following continuing progress on this issue as reported by suppliers in the 2018 annual survey and taking into account the GCA’s engagement and clarity with retailers on the issue, it was decided to move delay in payments to the monitored category.

In July 2018, the GCA wrote to the ten original designated retailers setting out how progress on this issue would be monitored and asked for retailer responses to be provided in March 2019. The GCA will use this information together with the results of the annual survey 2019 to track the impact of retailer initiatives before deciding the next steps on this issue. The GCA is working with the additional designated retailers on this issue.

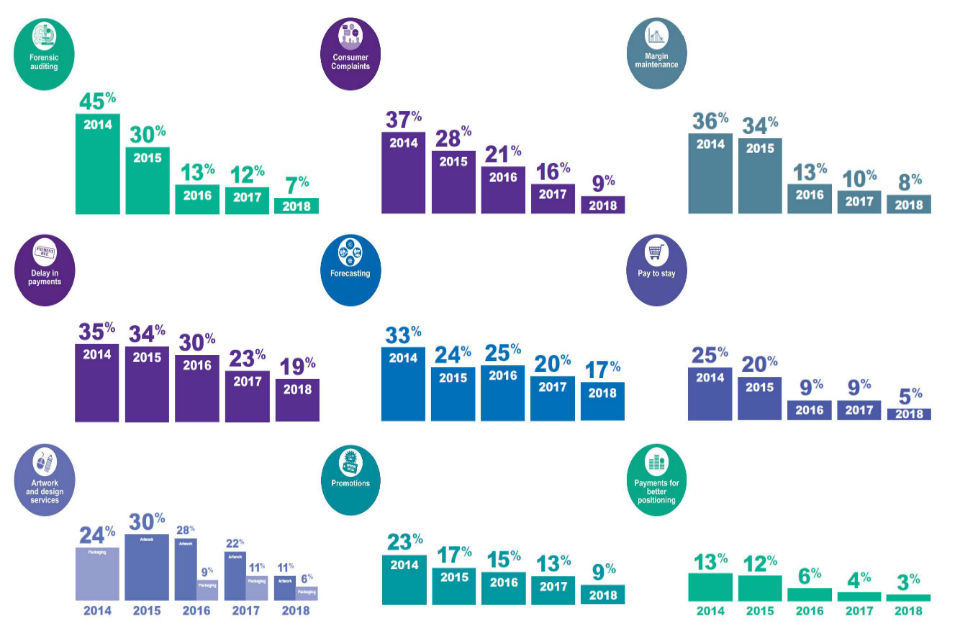

Delay in payments has dropped from 35% of suppliers reporting an issue in 2014 to 19% in 2018.

Forecasting

Description

Suppliers experiencing issues with forecasting reported difficulties communicating with buying teams, retailers not taking enough responsibility for forecasts after they have been set and often making last-minute changes, little or no engagement when sales are not meeting forecasts, and inadequate retailer systems which do not take into account known or past issues. Suppliers reported that the accuracy of regulated retailers’ forecasts was poor and that significant variations occurred between forecasts made and orders placed, sometimes at very short notice. In some cases, suppliers had been charged for non-delivery against orders when they had only been given an annual target and were then penalised for not meeting a 99% service level on each order, regardless of its variation from average. Suppliers also reported being left with significant amounts of stock through no fault of their own and that it was unclear how to seek compensation for inaccurate forecasting.

Potential Code breach

The GCA considers that the effect of this practice falls under part 4 (paragraph 10) of the Code: Compensation for forecasting errors, read with part 2 (paragraph 2) of the Code: Principle of fair dealing.

GCA progress

In 2015 the GCA reviewed the forecasting approach of the regulated retailers to assess their compliance with the Code. In March 2016 the GCA published a statement of best practice which the retailers should work towards, intended to promote better working practices by the retailers.

One year on, the GCA asked the retailers to provide information on their progress towards the best practice set out in the statement. Following monitoring, the GCA was unconvinced that sufficient improvements had been made. Forecasting was the second highest issue of concern to direct suppliers reported in the annual survey 2017. For these reasons the issue was moved back to the current category.

The GCA continued to receive feedback from suppliers about this issue in workshops and from training courses held by third parties. The GCA wrote to retailers in October 2017 to give feedback on their progress and launched a mini survey to learn more about supplier experiences. In December 2017 the GCA reported to retailers at a high level the outcome of the mini survey and noted some recurring themes raised by suppliers.

In January 2018 the GCA wrote to retailers again and expressed its view that there would almost always be some circumstances in which compensation was appropriate as a result of a forecasting error, so a blanket exclusion in a supply agreement would be unlikely to be Code compliant. Because suppliers might be unlikely to ask for compensation, the GCA asked retailers to consider the extent to which they might offer it. The GCA also expressed its view that the due care test, as set out in paragraph 10(1)(a) of the Code, was unlikely to be met by a retailer that provided no way for a supplier to contribute to the forecasting process, whether collaboratively in reaching agreed volumes to be ordered or by ensuring suppliers could raise questions and queries if a forecast seemed to them to be inaccurate or to have resulted in an excessive order.

Taking into account these points, the GCA published a revised statement of best practice in June 2018, which also addressed the issue of promotions (see separate Top Issue). The GCA noted that retailers are looking at their systems, processes and staff training to ensure they are consistent with the best practice statement.

In July 2018, the GCA wrote to the original ten designated retailers setting out how progress on this issue would be monitored and asked for retailer responses to be provided in March 2019. The GCA will use this information together with the results of the annual survey 2019 to track the impact of retailer initiatives before deciding the next steps on this issue. The GCA is working with the additional designated retailers on this issue.

In 2014 33% of suppliers said they had an issue with forecasting. By 2019 this had dropped to 17%.

Promotions

Description

Suppliers reported forecasting in relation to promotions in particular was poor and that it led to overbuying at promotional prices or had the impact of suppliers predominantly funding the cost of a promotion. Suppliers were also concerned about a number of poor practices such as buying-in periods for promotions exceeding the promotional period and the shelf life of products, not adhering to timelines agreed for promotional activity, buyers not activating promotions in stores and failure to deliver on agreed promotional activity.

Potential Code breach

The GCA considers that the effect of this practice falls under part 4 (paragraph 10) of the Code: Compensation for forecasting errors, part 5 (paragraph 13) of the Code: Promotions and part 5 (paragraph 14) of the Code: Due care to be taken when ordering for Promotions, all read with part 2 (paragraph 2) of the Code: Principle of fair dealing.

GCA progress

In 2017 the GCA put this issue in the current category to understand it more fully. Issues around promotions were closely related to forecasting, but also included concerns that buying-in periods exceeded the promotional period and the shelf life of products, and failure to deliver on commitments in store for promotions.

The GCA wrote to retailers asking for more information about their practices in relation to running promotions and sought comments from suppliers in a mini survey. Taking this into account the GCA informed retailers that there appeared to be limited evidence of deliberate over-buying for promotions and the way that most retailers ran their promotional activity helped to minimise the risk of Code breaches. However, because suppliers had raised some important issues which appeared to engage the Code, the GCA asked all retailers to report on what changes they were making to the way they managed promotional activity to ensure each was compliant with the Code and that any deductions made were consistent with the GCA’s interpretation of paragraph 5 of the Code.

In June 2018 the GCA published a revised statement of best practice on forecasting, which also addressed the issue of promotions. The points made in relation to the issue of promotions largely reflected where retailers could improve their processes and were based on the practical experiences that suppliers had shared.

In July 2018, the GCA wrote to the original ten designated retailers setting out how progress on this issue would be monitored and asked for retailer responses to be provided in March 2019. The GCA will use this information together with the results of the annual survey 2019 to track the impact of retailer initiatives before deciding the next steps on this issue. The GCA is working with the additional designated retailers on this issue.

23% of suppliers in 2014 reported they had an issue with Promotions. This had dropped to 9% by 2018.

Previous Top Issues

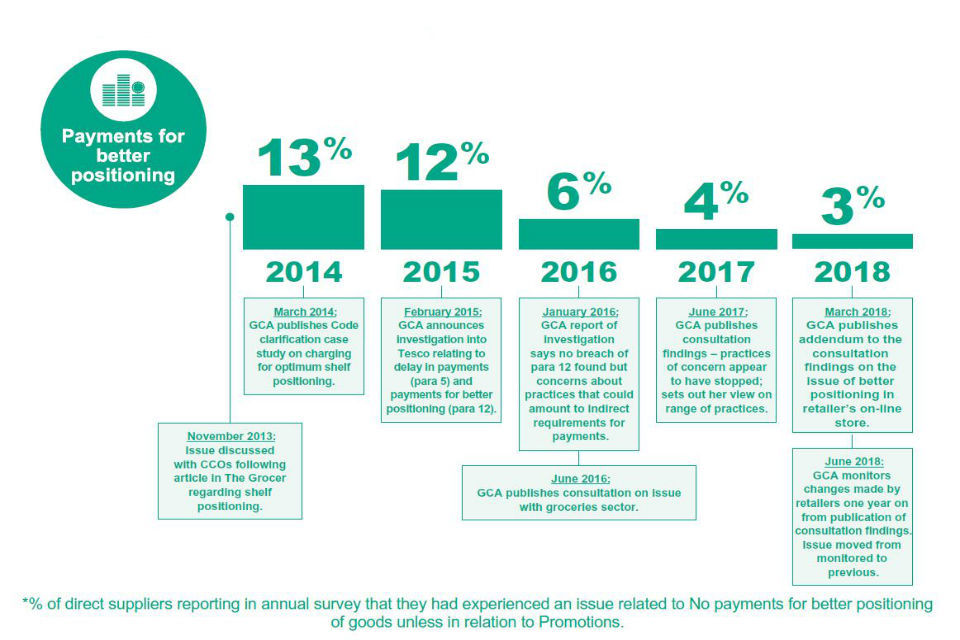

Payments for better positioning

Description

During the investigation into Tesco plc, the GCA was concerned to find evidence of practices that could amount to an indirect requirement for payments to be made by suppliers to secure better positioning or an increased allocation of shelf space. These practices included large suppliers negotiating better positioning and increased shelf space in response to requests for investment from the retailer, as well as paying for category captaincy and to participate in range reviews. No breach was found but the GCA determined to look into the issue across all regulated retailers.

Potential Code breach

Practices in this area may fall under part 5 (paragraph 12) of the Code: No Payments for better positioning of goods unless in relation to Promotions, read with part 2 (paragraph 2) of the Code: Principle of fair dealing.

GCA progress

The GCA consulted with the groceries sector on the proper scope of indirect requirements for payment to secure better positioning of goods or increased shelf space within a store. The GCA published its response in February 2017, noting that the practices that had caused concern appeared to have stopped and making clear what it considered to be Code compliant behaviour for the future.

Formal monitoring was carried out in February 2018 to evaluate the most recent supplier information and to identify whether retailers had decided to make any changes as a result of the GCA’s published consultation response. At the same time, the GCA also considered the issue of better positioning of goods in relation to retailers’ virtual sales, asking all retailers to provide information about their practices. In March 2018 the GCA issued an addendum to the conclusions published following the consultation on paragraph 12 of the Code. This made clear that the GCA will consider physical and virtual positioning of groceries in the same way when interpreting the Code and that retailers should consider whether their activities in relation to groceries for resale online are compliant with the Code. Retailers are expected to make clear on their websites where goods not on promotion appear more visible to customers as a result of advertising paid for by a supplier or any payment received from a supplier to secure more space or better positioning.

Following the GCA’s annual survey 2018 and feedback by suppliers that this was not a major issue of concern, the GCA moved it to the previous category.

Payments for better positioning now only reported by 3% of suppliers in 2018, down from 13% in 2014.

Pay to stay

Description

Suppliers raised concerns about potential pay to stay arrangements. The terminology has been used informally in the context of lump sum payments being requested or required and the supplier feeling they would experience detriment if they refused. A GCA Code clarification case study on requests for lump sum payments made by one retailer highlighted instances where payments were requested for the first half of the financial year and suppliers felt they would suffer a detriment if these payments were not made. The GCA was also informed about other payments that suppliers might make to retailers which those suppliers saw as contributions they had to make in order to do business with the retailer, such as to participate in social events or marketing initiatives, payments made immediately prior to or at the time of a tender not as part of the tender or bidding process and payments to secure exclusivity.

Potential Code breach

The GCA considers that the effect of this practice falls under part 3 (paragraph 3) of the Code: Variation of Supply Agreements and terms of supply, and part 4 (paragraph 9) of the Code: Limited circumstances for Payments as a condition of being a supplier, read with part 2 (paragraph 2) of the Code: Principle of fair dealing.

GCA progress

The GCA sought views from retailers on their practices in a range of circumstances and also from direct suppliers in one-to-one meetings and workshops arranged specifically to discuss pay to stay. Examples were raised in each context that retailers clearly saw as normal commercial negotiations but suppliers saw differently.

The GCA clarified the meaning of pay to stay and what behaviours are not considered to be Code compliant. The GCA emphasised that retailers needed carefully to consider when making any request for lump sum payment, not only what the payment was for and the basis for it in the supply agreement, but also how it would appear to the supplier and how payment was documented to provide clarity about the arrangement.

Following the GCA’s annual survey 2017 and what was reported to the GCA by suppliers and retailers on the issue of pay to stay, the GCA moved it to the monitored category as it was not a major issue reported in the survey.

The GCA continued to monitor feedback from suppliers on this issue and in December 2017 informed all retailers that although the issue of pay to stay appeared to be of less concern to suppliers now, some suppliers still reported they felt pressured, for example, to agree to a promotion in order to keep their business with a retailer. The GCA effectively saw this as a pay to stay arrangement. The GCA advised retailers that accordingly, in seeking to manage their compliance risk, retailers should avoid these differences in understanding wherever possible, whether by avoiding lump sum payments altogether or by clear communication between the retailer and supplier about what any money paid is for. The GCA also urged retailers to ensure that their training was properly updated. Following further monitoring of progress on this issue again in summer 2018 the GCA moved it to the previous category.

Only 5% of suppliers reported an issue related to limited circumstances for payments as a condition of being a supplier in 2018. Down from 25% in 2014.

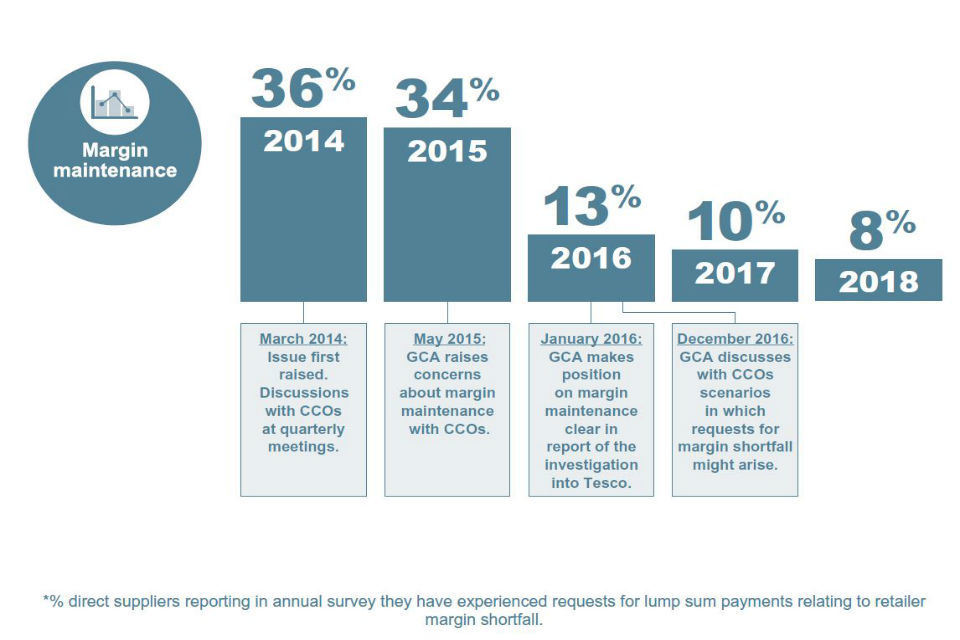

Margin maintenance

Description

The report of the investigation into Tesco plc identified a number of practices occurring as a result of a focus on hitting budgeted or aspirational margin targets. Suppliers provided information to the GCA that other regulated retailers occasionally engaged in this practice.

Potential Code breach

The GCA considers that the effect of this practice falls under part 3 (paragraph 3) of the Code: Variation of Supply Agreements and terms of supply, read with part 2 (paragraph 2) of the Code: Principle of fair dealing.

GCA progress

The GCA made clear in the report of the investigation into Tesco plc how the Code will be interpreted and that unilateral deductions made in order to satisfy an unachieved aspirational margin target are unreasonable. The GCA set out that requests for margin maintenance must be unambiguously supported by the supply agreement.

Since the GCA issued the report of the investigation into Tesco plc, it has been listening to suppliers on this issue. The GCA wrote to all retailers in November 2016 requesting information about practices that related to margin made on a particular product and the impact of those practices on suppliers. The responses from retailers showed that their practices were generally compliant with the Code and feedback from suppliers indicated that margin maintenance was less of an issue for them.

In 2017 the GCA decided to move this issue to the previous category. It was nonetheless made clear to retailers that as the issue had been explored and the GCA had promulgated a clear interpretation of the Code in this area, if the GCA found evidence of the practice reoccurring it may indicate the collaborative approach had been effectively exhausted, making further regulatory action likely. The annual survey 2018 continued to show that suppliers were not reporting this as an area of concern.

36% of suppliers in 2014 reported a request for lump sum payments relating to retailer margin shortfall. By 2018 this has dropped to 8%.

Drop and drive

Description

Suppliers reported that they experienced problems where there was a disparity between what suppliers said they had delivered and invoiced, and what the relevant regulated retailer said had been received. In some cases retailers appeared to make automatic deductions from invoices for alleged shortages. These deductions were difficult to challenge, depending on the haulage method and particularly where no proof of delivery had been issued.

Suppliers informed the GCA that this was a major issue for them. There appeared to be different patterns of deductions among retailers in respect of the same suppliers; and varying error rates being recorded despite suppliers using the same processes with each retailer.

Drop and drive continues to be considered as an example of a practice which can lead to delay in payments.

Potential Code breach

The GCA considers that the effect of this practice falls under part 4 (paragraph 5) of the Code: No delay in payments, read with part 2 (paragraph 2) of the Code: Principle of fair dealing.

GCA progress

The GCA received more information on this issue from retailers and suppliers. While some progress had been made on this issue, it was clear that some retailers’ progress in responding to supplier concerns had been too slow and the GCA accordingly escalated its concerns on drop and drive.

The GCA intensified its collaborative engagement and in May 2017 wrote to all regulated retailers setting out its view on their progress in actively managing the risk of breaches of the Code occurring under paragraph 5 (No delay in payments) arising from the practice of drop and drive.

The GCA received detailed responses from those retailers whose progress on tackling delay in payments arising from drop and drive was causing most concern. The GCA was satisfied that based on the information provided by retailers and the updated evidence received from suppliers, that all retailers that carry out drop and drive appeared to have adequate systems and processes in place to minimise the risk of delay in payments arising. For example, some retailers chose to implement good faith receiving for suppliers as a commercial solution to drop and drive issues.

Retailers have continued to make progress on the issue and many have implemented new operational and supply chain practices as a result. Supplier feedback has been that these systems are delivering benefits in terms of greater certainty about payments and better supply chain management. The GCA expects all retailers to continue to focus on this issue and continues to monitor what suppliers say about drop and drive. The 2018 annual survey continued to show that suppliers were reporting this as less of an issue, thereby indicating that they were benefiting from retailer initiatives to secure Code compliance. The Drop and drive issue is now being monitored under Delay in Payments.

First asked in 2015 when 28% of suppliers reported an issue with Drop and Drive. Down to 12% in 2018.

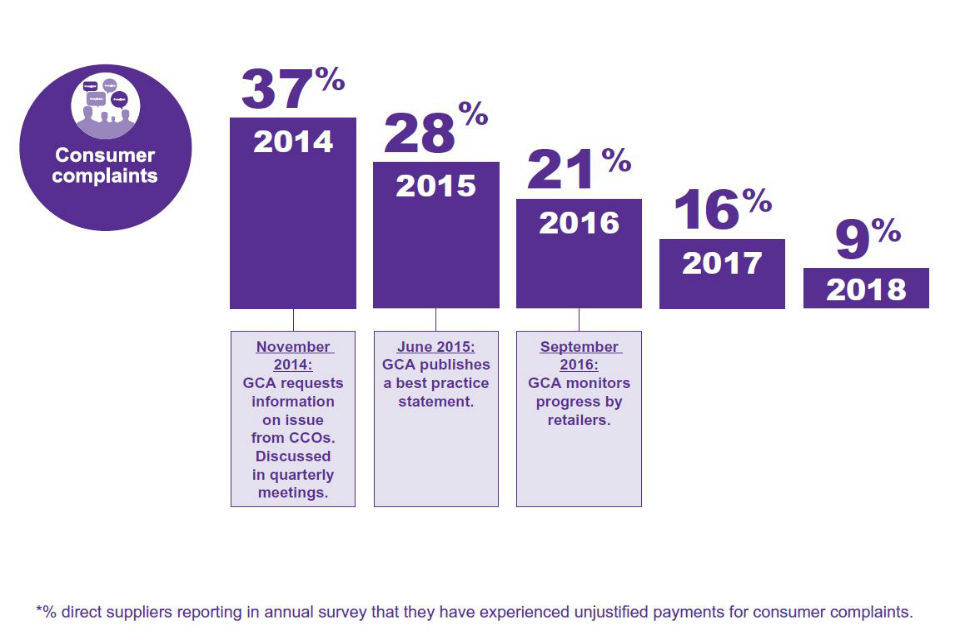

Consumer complaints

Description

Suppliers reported that regulated retailers dealt with consumer complaints in different ways. Practices included applying fixed rates, applying variable rates depending on the seriousness of the complaint, while some made no charge. Suppliers were concerned that retailers may be overcharging for dealing with consumer complaints and deriving profit from them.

Potential Code breach

Consumer complaints fall under part 6 (paragraph 15) of the Code: No unjustified payment for consumer complaints, read with part 2 (paragraph 2) of the Code: Principle of fair dealing.

GCA progress

The GCA announced a best practice statement on consumer complaints at the 2015 conference. Since then the Adjudicator has been closely monitoring this issue and CCOs were asked to report back in September 2016 on what improvements they had made. Following this monitoring, the Adjudicator has confirmed that retailers’ practices are broadly in line with the best practice statement and the issue is now categorised as previous.

9% of suppliers reported in 2018 that they had a experienced unjustified payments for consumer complaints. Down from 37% in 2014.

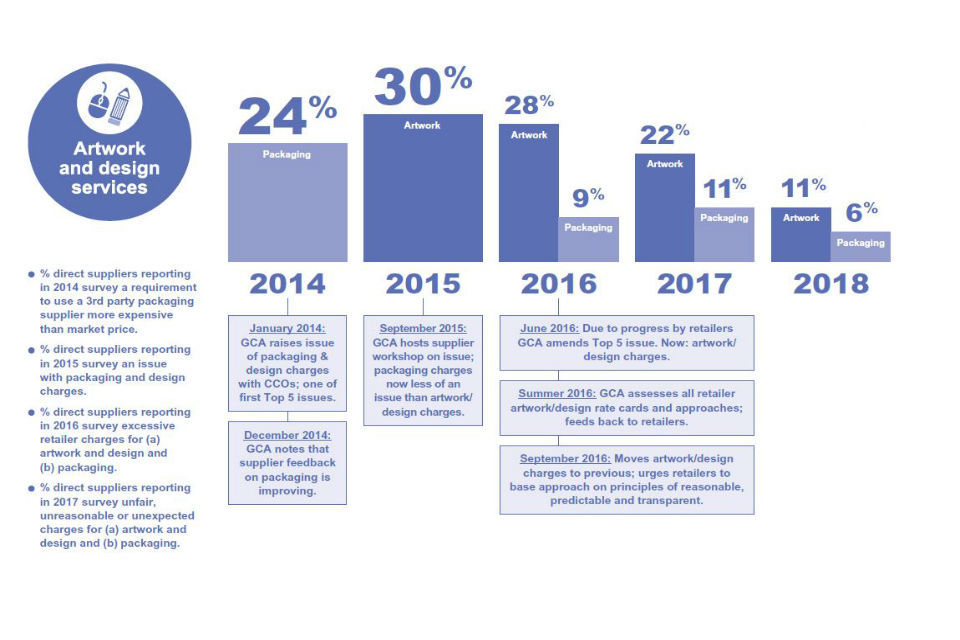

Artwork and design services

Description

The GCA heard concerns from suppliers about the arrangements, costs and services in relation to packaging, artwork and design services. A workshop with suppliers in September 2015 on the issue delivered positive news that the position on packaging for suppliers had improved. As a result, this Top Issue was refined to focus on artwork and design services. Suppliers remained concerned that the charges made by artwork and design companies approved or required to be used by some retailers were considerably higher than those available on the open market.

Potential Code breach

The GCA considers that the effect of this practice falls under part 4 (paragraph 6) of the Code: No obligation to contribute to marketing costs; and part 4 (paragraph 11) of the Code: No tying of third-party goods and services for Payment, read with part 2 (paragraph 2) of the Code: Principle of fair dealing.

GCA progress

Following a review of the issue, the Adjudicator noted that all retailers were taking steps to bring their practices and charges closer to the principles of being reasonable, predictable and transparent for suppliers. The GCA’s review did not identify any breach of the Code and the issue was moved to the previous category, although the GCA continues to monitor what suppliers say.