The consumer experience at public chargepoints

Updated 30 March 2023

© Crown copyright 2023

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/consultations/the-consumer-experience-at-public-electric-vehicle-chargepoints/the-consumer-experience-at-public-chargepoints

Foreword

The transition to zero-emission vehicles is central to meeting our ambitious climate commitments. We’re already making fantastic progress. In 2020, electric vehicles (EVs) accounted for 1 in 10 new cars sold, up from 1 in 30 in 2019. Overall demand for fully electric vehicles grew by 186%.

As the first major global economy to pass a law that requires us to achieve net-zero emissions by 2050, the UK is on track to end its contribution to climate change. We’re committed to making lasting changes in the way we travel and to building back greener for the benefit of everyone.

In November 2020, we committed to ending the sale of new petrol and diesel cars and vans by 2030, with all vehicles required to have a significant zero-emissions capability (for example, plug-in and full hybrids) from 2030 and to be 100% zero emissions from 2035. We have committed to a world-leading £2.5 billion package to support consumers to make this transition.

Reliable and easily accessible charging infrastructure is key to making the switch to EVs as easy and smooth as possible. This is a fast-moving sector that has already seen tremendous growth of innovative technological solutions for drivers, such as using lampposts as a low-cost charging solution for those without off-street parking. 2020 saw more ultra-rapid chargepoints deployed than any year before. These can deliver up to 145 miles of range in just 15 minutes for a typical EV.

However, it’s essential that EV drivers feel confident using the public chargepoint network. In this consultation, we set out proposals that mean current and future EV drivers will be able to locate available chargepoints simply, pay for a charge more easily and recharge their cars more reliably, regardless of where they are going in the UK. Drivers need to know they can rely on the public charging network for any journey they take. This will reduce range anxiety and position the UK as a world leader in deploying advanced EV charging infrastructure.

These proposals will ensure the growth of EVs can take place at the pace required to hit our bold climate targets. To that end, the measures in this consultation represent significant progress towards our end goal: to ensure that drivers of electric vehicles have a refuelling experience equal to or even better than petrol or diesel vehicle drivers.

Rt Hon Grant Shapps MP

Secretary for State for Transport

Executive summary

In 2019, the government committed the UK to meet net-zero greenhouse gas emissions by 2050, to ensure the UK ends its contribution to climate change. Transport is now the largest sector for UK greenhouse gas emissions. Cars and vans alone represent 19% of all domestic emissions. The transition to zero-emission vehicles is therefore vital to realising our net-zero ambitions.

To achieve this, the government is taking decisive action to end the sale of new petrol and diesel cars and vans, with all vehicles required to have a significant zero-emissions capability (for example, plug-in and full hybrids) from 2030 and to be 100% zero emissions from 2035.

There are now over 300,000 ultra-low emission vehicles registered in the UK and over 20,000 public chargepoints installed for EVs. The government has committed £2.8 billion to support this transition.

EV chargepoint installation and operation is a relatively new and growing market. We want to encourage and leverage private sector investment to build and operate a self-sustaining public chargepoint network that’s affordable, reliable and accessible for all consumers.

As charging technology and infrastructure evolves and expands, new consumer offers will continue to emerge. We want to enable innovative charging approaches while ensuring that all consumers can charge their vehicle in a way that is as straightforward and reliable as refuelling a traditional vehicle. This is essential, not only for existing EV drivers but for giving people who are more reluctant to switch the confidence to do so.

This consultation sets our expectations and ambitions across 4 critical areas.

Making it easy to pay

Consumers should be able to charge their vehicle and pay with ease, as they would for any other service. There should be a minimum standard for payment across all chargepoints, which does not rely on the use of a smartphone. We seek views on the best way to achieve this that meets consumers’ needs and is commercially viable.

Consumers should be able to rely on their chosen payment method, whether they’re making a short or long journey. Implementing roaming across networks means consumers can access all public chargepoints with one membership card or smartphone app. As smartphone technologies advance, we want to see convergence towards fewer apps that can access thousands of chargepoints across the UK.

Opening up chargepoint data

All drivers should be able to locate available chargepoints easily when they need to charge their vehicle.

Opening up chargepoint data will enable the development of consumer-friendly apps and improve consumer experience.

It will also reduce costs by encouraging competition and innovation, and support system planning across the transport and electricity sectors.

Using a single payment metric

Consumers should be able to understand and compare pricing offers across the UK network to select the best available price, as is currently the case for petrol and diesel vehicles.

Standardisation to a pence-per-kilowatt hour (kWh) basis will enable a simpler pricing framework for all users. Providers would still be able to offer a range of bundled services tariffs.

This approach ensures alignment with the energy sector and the price of electricity used across the network, helping consumers compare how much they are paying at home with how much they are paying when they use the public charging network.

Ensuring a reliable charging network

Reliable infrastructure is critical to mass-market roll-out.

It’s essential that the public chargepoint network is maintained and that faults are repaired quickly to ensure a minimum 99% reliability across the charging infrastructure. A 24/7 helpline is required for those who need assistance when struggling to use a chargepoint.

Emerging policy areas

In addition to the 4 areas above, we’re seeking evidence on 3 emerging policy areas:

- accessibility for disabled consumers

- weatherproofing and lighting

- signage

We want to understand the issues facing consumers in these areas and whether there are priority areas to address. This will enable us to get an idea where there may be a need for government intervention in the immediate future and which agency is best placed to intervene.

We’ll be holding workshops to engage with industry and consumer groups to evolve the policy options for each of the 4 areas above to reduce the burden and costs while best meeting consumer needs. Parliamentary time allowing, we expect to bring in the necessary regulation following this consultation in autumn 2021.

How to respond

The consultation period began on 13 February 2021 and will run until 10 April 2021. You can respond using the online form. Please ensure that your response reaches us before the closing date. If you’d like further copies of this consultation document or require alternative formats (Braille, audio CD etc), please contact consumerofferconsult@olev.gov.uk.

When responding, please state whether you’re responding as an individual or representing the views of an organisation. If responding on behalf of a larger organisation, please make it clear who the organisation represents and, where applicable, how the views of members were assembled.

There will be consultation workshops running throughout the consultation period. If you’d be interested in attending these events, please contact consumerofferconsult@olev.gov.uk.

If you have any suggestions about others who may wish to be involved in this process, please contact us.

Freedom of information

Information provided in response to this consultation, including personal information, may be subject to publication or disclosure under the Freedom of Information Act 2000 (FOIA) or the Environmental Information Regulations 2004.

If you want information that you provide to be treated as confidential, please be aware that, under the FOIA, there is a statutory code of practice with which public authorities must comply and which deals, amongst other things, with obligations of confidence.

Given this, it would be helpful if you could explain to us why you regard the information you’ve provided as confidential. If we receive a request for disclosure of the information, we’ll take full account of your explanation, but we cannot give an assurance that confidentiality can be maintained in all circumstances. An automatic confidentiality disclaimer generated by your IT system will not, of itself, be regarded as binding on the Department for Transport (DfT).

The DfT will process your personal data under the Data Protection Act (DPA) and, in most circumstances, this will mean that your personal data will not be disclosed to third parties.

Data protection

The DfT is carrying out this consultation to gather evidence on the consumer experience at public chargepoints. This consultation and the processing of personal data that it entails is necessary for the exercise of our functions as a government department. If your answers contain any information that allows you to be identified, DfT will, under data protection law, be the controller for this information.

As part of this consultation, we’re asking for your name and email address. This is in case we need to ask you follow-up questions about any of your responses. You do not have to give us this personal information. If you do provide it, we’ll use it only to ask follow-up questions. We will not use your name or other personal details that could identify you when we report the results of the consultation.

DfT’s privacy policy has more information about your rights concerning your personal data, how to complain and how to contact the Data Protection Officer.

Your information will be kept securely on a secure IT system within DfT and destroyed within 12 months of the consultation end date.

Introduction

Aims and scope of the consultation

In 2019, the UK made history by becoming the first major global economy to pass legislation to end our contribution to climate change. Delivering net-zero emissions will require a drastic reduction in greenhouse gas emissions across all sectors of the economy including transport.

Cars and vans represent 19% of all domestic emissions. We’ll only achieve our net-zero commitment if we can transition this fleet to zero-emission vehicles.

In November 2020, the Prime Minister announced the commitment to end the sale of new petrol and diesel cars and vans, with all new cars and vans required to have a significant zero-emissions capability (for example, plug-in and full hybrids) from 2030 and be 100% zero emissions from 2035.

To support the transition to EVs, the government has committed £2.8 billion, with grants available for plug-in cars, vans, lorries, buses, taxis and motorcycles, as well as funding to support chargepoint infrastructure at homes and workplaces, on residential streets, and across the wider roads network.

We’re increasing the provision of chargepoints along the strategic road network through the Rapid Charging Fund.

We know high consumer confidence in charging infrastructure is crucial to securing the market transition at pace and ensuring a modern, innovative market that attracts investment. We’re building on the positive steps from industry to encourage the uptake of EVs through a better consumer experience at the public network.

This consultation reflects our ambitions for the EV sector to:

- build confidence in the market

- build up the demand for EVs

- open opportunities for innovation and market investment

This is an important stage of EV roll-out across the country. The EV driver of today is not the EV driver of tomorrow, with the EV market still in the early adopter phase. As we transition to mass-market roll-out, consumer needs and priorities will need to change to reflect the wider changing driver make-up.

We need to ensure this emerging market can continue to innovate and grow while providing an excellent consumer experience. Therefore, any new regulation must be proportionate and appropriate. This consultation sets out our baseline expectations to improve consumer experience when using the charging network. We’re proposing interventions in 4 areas:

- quick payment process

- network reliability

- pricing transparency

- open data

We’re also seeking evidence in areas where we think there may be a case for the government to intervene, but further evidence is required, such as accessibility.

The Competition and Markets Authority (CMA) is conducting a forward-looking market study to help develop competition as the sector grows. This study is also looking at consumer interaction, including building consumer trust, pricing and access to a reliable charging infrastructure. We’ll be working alongside the CMA to ensure alignment in considering these and related issues.

This consultation covers all publicly available chargepoints in the UK, including those in the devolved nations. We’re considering these proposals alongside the potential requirements for smart charging[footnote 1].

The charging experience and our vision

The EV chargepoint market has grown rapidly over the past 10 years. In this short time, we’ve seen considerable market development and growing breadth of consumer offers such as payment apps covering multiple chargepoint networks and private bodies providing availability data; however, consumers too often report frustrations over unnecessary complexity when using public charging infrastructure. This is detrimental not just to the charging experience but to encouraging faster take-up of EVs by other consumers.

We’re consulting on measures to improve various stages of the consumer experience at public chargepoints, including:

Locating chargepoints

Consumers should be able to access a range of software solutions providing them with comprehensive and accurate chargepoint data that enables them to locate and access chargepoints with ease. Currently, chargepoint operators (CPOs) only display static information such as location and power rating related to their network on their apps.

More comprehensive private-sector led solutions are emerging such as Zap-Map’s platform and its provision of location and ‘live’ availability chargepoint data; however, this data is not openly available, and lack of mandated data provision standards means that chargepoint data can be incomprehensive and inaccurate, leading to a poor consumer experience.

Comparing costs of charging

We want consumers to be able to easily compare the cost of charging between different networks, helping drive competition and bring down prices. Evidence suggests that consumers are confused by a lack of comparability of pricing information at either public chargepoints or through other means (for example, smartphone apps).

The cost of electricity drawn from public chargepoints is priced using a range of different metrics. A lack of a standard pricing metric prevents consumers from easily comparing prices.

Charging the vehicle

Public chargepoint reliability is improving. Analysis[footnote 2] shows that in August 2019 around 8% of public chargepoints were out of service, a decrease from 15% in 2017; however, further improvements are required to drive consumer confidence.

Chargepoints being out of order undermines consumer confidence in the public chargepoint network and can put people’s safety at risk if they are left stranded and unable to charge their vehicle.

Paying for the charge

Paying for charge should be a smooth, hassle-free process for the consumer, regardless of who operates the individual chargepoint. Simple payment solutions have emerged.

But there remains no common method of access across chargepoint networks and consumers can sometimes need a different smartphone app or membership card for each network. This results in a more complicated experience than that enjoyed by petrol or diesel vehicle drivers and those on the continent, where roaming solutions exist.

Legislative framework

The Automated and Electric Vehicles Act 2018 (AEVA) enables the government to introduce regulations to improve the consumer charging experience and increase the provision of public chargepoints. This includes being able to:

- require a common payment method at all public chargepoints

- introduce requirements on CPOs to make available static and dynamic information on public chargepoints, and prescribe when, how, to whom and in what format the information is made available

- introduce availability and performance standards for public chargepoints

- introduce connector standards to ensure physical interoperability between EVs and public chargepoints

The government also has powers under the Pricing Act 1974 to introduce a common pricing metric for the supply and sale of electricity to consumers.

Timings and implementation

The consultation period began on 13 February 2021 and will run until 10 April 2021, and we welcome feedback through the consultation period. We’ll then review the responses before responding formally.

We’ll work with stakeholders alongside this consultation to test and refine our proposals. We’ll also produce an impact assessment informed by the consultation responses before introducing any regulations. Any regulations will be introduced as soon as the parliamentary timetable allows.

Policy proposals

Payment methods

Consumers should be able to pay instantly for using public chargepoints in a smooth and hassle-free manner.

At present, consumers need to have multiple membership cards or smartphone apps to access the public charging network. Currently, only 41% of rapid and higher-powered chargepoints (50 kW+) have contactless debit or credit card payment as an option.

Consumers should have a comparably simple payment experience at all chargepoints. Consumers should be able to have a payment option that enables them to pay without the use of a smartphone. We seek views on the best way to achieve this that meets consumer needs and is commercially viable.

Fleet drivers need a simple payment solution that operates across the chargepoint network and allows them to manage their business effectively. We ask how best to deliver a roaming solution to achieve this.

We prpose the requirements would apply from the point of regulations coming into force for new chargepoints. There would be a 12-month period to retrofit existing chargepoints.

Current state of the market and the problem to be addressed

Historically, there have been numerous methods of payment for using public chargepoints for EVs including membership cards, SMS text and online web platforms. The most common method is by membership card (known as a radio-frequency identification or RFID card). If customers want to use different chargepoint networks then they require multiple cards.

Many CPOs established subscription-based membership models where an RFID card is issued once a consumer has signed up to be a member of their network. Memberships create a sustainable income stream for CPOs that enable them to attract private investment.

The Alternative Fuels Infrastructure Regulations 2017 (AFIR) helped to improve ease of payment by requiring chargepoint operators to provide impromptu access [footnote 3] at all public chargepoints by November 2018.

Under AFIR, chargepoint operators can prescribe their own method for accessing its services and set different pricing for members and non-members. Most chargepoint operators provide impromptu access through a smartphone app, contactless card payment, or a QR code provided at the chargepoint, which then directs consumers to a payment platform.

Drivers need to be able to pay quickly and easily for charging when making longer journeys. Consumers have reported frustrations with the number of apps and cards needed. They’re less likely to be aware in advance of which charging apps may be needed for their journey than on short-distance journeys or when charging near their work/home.

To remedy this, in July 2019, the Secretary of State for Transport announced that government wanted to see all newly installed rapid and higher-powered chargepoints provide debit or credit card payment by spring 2020[footnote 4].

Several CPOs have responded, and 41% of existing 3,500 rapid devices now have contactless card payment compared with 28% in 2019[footnote 5]. We’d expect to have seen more progress on new rapid devices, but this has not been the case.

Access to public chargepoints should also be achieved by a payment roaming solution, meaning that drivers can access any public chargepoint using one membership card or smartphone app. A roaming approach requires CPOs to cooperate and third parties to enable members of other networks to access their network.

In July 2019, the Secretary of State for Transport[footnote 6] signalled that government expects industry to develop a payment roaming solution across the charging network. The lack of payment interoperability is a regular theme raised by consumer bodies and fleet operators.

The EV Energy Taskforce, which brought together over 300 stakeholders, has recommended that a roaming solution should be in place by the end of 2021 and adopted by all CPOs at all chargepoints. Some progress has been made in the past 12 months, with peer-to-peer roaming agreements established between some CPOs and third-party aggregators.

Emerging technologies

This is a rapidly evolving market, with new technologies and business models emerging. We need to ensure that any solutions address the needs of current consumers, but we recognise maintaining flexibility is important to encourage innovation.

For example, plug and charge[footnote 7] technology would allow consumers to simply plug their car into a chargepoint and charge without the need for a membership card, smartphone app, or debit or credit card.

Instead, the car and the chargepoint would communicate to identify the consumer and their charging contract. Some original equipment manufacturers (OEMs) are testing this experimental technology, which could see charging speeds, times and cost limit preferences set from within the vehicle.

This would enable service bundles in which charging fees and ongoing vehicle loan finance are grouped into one payment plan.

Minimum payment requirements for the consumer

We’re encouraged by the innovation in the application of payment methods in the chargepoint sector, but further improvements are needed.

The Alternative Fuels Infrastructure Regulations 2017 (AFIR) requires chargepoint operators to provide impromptu access at all public chargepoints, avoiding the need for membership.

Chargepoint operators can choose their preferred option for meeting this requirement and set differential pricing structures between members and non-members. Most chargepoint operators provide impromptu access through a smartphone app, contactless card payment, or a QR code provided at the chargepoint that then directs consumers to a payment platform.

In practice, impromptu payment often requires access to a smartphone or an online platform. We want to see more progress for supporting payments without reliance on a smartphone.

Minimum payment outcomes we want to see

Consumers arriving at a chargepoint should be able to start it and begin charging quickly. The payment process and the cost-per-charge should be easy to understand and to access with clear instructions given at the chargepoint.

Consumers should be able to easily understand and compare payment methods. All acceptable payment types should be displayed equally prominently on the chargepoint.

The minimum payment method should not require a mobile or fixed internet connection and should work at the location of the individual chargepoint – including where this is underground or where there’s no mobile signal.

If a chargepoint operator chooses to offer an impromptu solution requiring the consumer to connect to the internet via their phone, the chargepoint operator must also offer an alternative improvised option.

This could be in the form of contactless payment, for example, or a call or text-based solution. The minimum payment methods will exclude payment methods that require the use of a downloadable app, proprietary software or proprietary card before or after the transaction takes place. Options may include a form of contactless payment, for example, or, potentially, a call or text-based solution.

The impromptu solution should be available to all consumers, regardless of how long they are charging for, or how frequently they use a particular chargepoint or network. The definition of charge includes any amount of charge, with no time limit.

Q1: Are you in agreement that the payments specified should be allowed as an acceptable payment options? If you don’t agree, please set out why.

Q2: If implemented, do you think these requirements should apply to all chargepoints? If not, which chargepoints should be covered and why?

Q3: What alternative solutions to contactless would provide consumers with a comparable quick and simple payment mechanism (provide evidence on costs)?

Payment approaches for fleets

Companies with fleets need access to a simple payment method that allows the company to monitor and manage payments centrally rather than relying solely on the individual driver. Typically, this has been managed through fuel cards. These enable fleet drivers to refuel their vehicle using any fuel station contracted with the refuelling card.

Leading fuel card suppliers issue RFID cards to individual drivers or cars, which they use to pay for the fuel they consume, and then aggregate, payment and utilisation data for the respective fleet. Fuel card companies are looking to replicate the service they provide for EV fleets, and some have launched a recharging card; however, to date, only a small number of CPOs are participating in charging cards for fleets.

The emergence of electric fleets is also key to growing the second-hand EV market.

Case study – Mitie

Mitie operates a large commercial vehicle (van) and job-car fleet of approximately 5,500 vehicles. It transitioned this fleet to fully electric with 790 pure EVs already on the road (as of October 2020). With diesel vehicles, all drivers are provided with fuel cards to purchase fuel for their vehicles for business use, with the cost of the fuel paid directly by Mitie. On-street and communal parking charging infrastructure is critical to support the 45% of employees who do not have off-street parking.

To support the roll-out of EVs across fleets and to enable the fleets to effectively charge using the public network, there needs to be a mechanism for Mitie to pay for the electricity used to charge the vehicle directly.

A reclaim system would have a significant cash-flow impact on employees – potentially over £200 a month – acting as a barrier to electrification. Given multiple CPOs with their own systems, and typically no commercial account capability, direct agreements are not considered to be a commercially viable approach.

Corporate cards (such as through Visa and Mastercard) require RFID butm even then, will create significant financial control challenges. Mitie’s preferred mechanism is either a recharge card (in the style of a fuel card) allowing the use of all public chargepoints, or a roaming solution through an app or software platform to achieve the same outcome of a fleet operator being able to pay for and reconcile all electricity used through public chargepoints.

Roaming

A roaming solution would provide a common method of access to all public chargepoints, including lower-powered chargepoints, through one membership card or smartphone app. It could also provide a payment solution to meet the needs of fleet vehicle drivers.

Several pan-European roaming solutions have been well received by consumers [footnote 8]. These have been supported by public and private sector investment, and can be implemented in two ways:

- E-mobility service providers (peer-to-peer model) – E-mobility service providers (eMSPs) are third-party charging aggregators that do not own and operate chargepoints but contract with individual CPOs and provide a single card or app so that drivers can access all the chargepoints of the CPOs with which the third party is contracted.

- Roaming hubs – Platforms that connect eMSPs and CPOs, linking up their respective back offices. Drivers only need to register with one operator or eMSP to have access to all the chargepoints operating on the platform with one contract and invoice[footnote 9]. eMSPs also use the platforms to agree electricity prices with CPOs, acting as a clearing house. Most, but not all, eMSPs use roaming hubs to provide their services. Their use is widespread on the continent, with Gireve and Hubject leading the markets in France and Germany respectively. The Gireve platform was established by various companies, including Renault and EDF. It provides access to over 75,000 chargepoints in 20 EU countries.

Roaming requires the interoperability of operating protocols amongst CPOs and eMSPs. While Gireve and Hubject operate their own proprietary protocols, many eMSPs use the independently developed protocol, Open Chargepoint Protocol (OCPI). This has been collaboratively developed by industry and represents a more decentralised system. This facilitates billing services (meaning: charge detail records) and provides data to the driver including:

- static data on station specifications: connector types, power, location, operator name

- dynamic data on chargepoint availability

- session data after charging session completed

Case study – RFID in the Netherlands

Nearly all public chargepoints in the Netherlands are accessible with a single RFID card. Following direction from the Dutch government, a trade association, eViolin, was launched by CPOs and freight services in 2012. This ensures payment interoperability through uniform standards across all networks (developed by industry under direction from the government).

eViolin also maintains a Central Interoperability Register, which assigns CPOs a unique identification code for chargepoints to be used in payment-related communications between CPOs, eMSPs and other actors. The Dutch government, in conjunction with distribution network operators (DNOs), contributes funding and has board representation at the Netherlands Knowledge Platform for Public Charging Infrastructure EV (NKL), which coordinates development of the OCPI protocol.,

Implementing roaming

Any roaming solution must balance the potential benefits of improved customer experience and confidence in EVs against the potential impact of implementation costs on a largely new market. We have identified 4 options for consultation.

1) Market-led approach – the government continues to work with industry to establish an industry-led roaming solution, but does not regulate at this stage.

Intervention at this early stage could stifle the market and negatively impact the business case for installing and operating chargepoints. Charging cards for fleets and roaming solutions are emerging, and are expected to continue to develop over time as market grows and utilisation increases. However, in the short to medium term, it’s possible that no common method of access across all chargepoints, or effective payment solution for fleets, will emerge. This would undermine work to ensure a faster transition to mass-market for EVs.

2) Require all public chargepoints to be accessible via a QR code provided on, or close to, the chargepoint that then directs consumers to a payment platform.

This would provide EV drivers with a relatively straightforward payment method accessible across the entire network. CPOs would still be able to offer membership benefits; however, it would not deliver the payment and billing services required by fleet operators, and is reliant on drivers having access to a smartphone.

We recognise that upgrading the network to provide this facility will mean additional cost for CPOs and would be in addition to the contactless requirements we’re proposing for rapid and higher-powered chargepoints. We could limit the mandatory provision of the QR code to 3 to 22 kW chargepoints, leaving CPOs the choice to provide this facility at rapid and higher-powered chargepoints if they wish.

3) Government establishes an interoperable roaming platform.

We could establish a UK interoperable roaming platform like those operating on the continent. This would enable drivers to access any charger with one membership card or smartphone app. However, it would be highly complex and costly. The full establishment and operation of a platform would require close collaboration with industry participants and require a longer timeframe to introduce.

4) Require CPOs to open their networks to any third-party eMSP or each other without any discrimination.

This would allow multiple roaming business models to emerge (for example, peer-to-peer or roaming hubs) without regulatory mandating of a preferred model. While this approach offers flexibility and advantages to consumers, it relies on CPOs sharing commercial information with eMSPs outside of the CPO’s control.

This exposes the CPO to increased operational and reputational risk unless protections are established. There are also significant development and legal costs associated with connecting with other organisations to deliver charging services. In this scenario, we would propose the following supporting measures:

- all CPOs in the UK would be required to publish and maintain a roaming tariff: this would reflect both the minimum price a CPO would accept for a third-party eMSP to pay per kWh to access their chargepoints and the maximum ad-hoc price they charge – CPOs would also publish terms of payment for transparency and to encourage roaming agreements to materialise (such as expected payment timeframe)

- CPOs would allow access to a charging station from an eMSP that is willing to pay the roaming tariff, agrees to the published terms and meets a minimum level of baseline criteria

- the government would nominate an organisation to maintain a public list of roaming tariffs

- the market would be monitored by an independent body to ensure compliance

eMSPs who wish to gain access to CPOs through this regulation must meet the following minimum criteria. Any eMSPs that do not satisfy these could still operate in the market, but CPOs would not be required to work with them.

-

minimum baseline criteria will be published and updated annually by the government or another organisation, and relate to the level of technical development, size and business processes

-

only Financial Conduct Authority (FCA)-regulated eMSPs would be able to secure access to all UK CPOs under this regulation: industry and government would work with the FCA to deliver a regulatory regime that ensures minimum cybersecurity levels and payment processes by eMSPs

Q4: Do you agree we should intervene now to implement roaming? If not why?

Q5: Which option do you think is the most suitable approach for delivering roaming in the UK? Please rank the options in order of preference.

Q6: Please provide reasons for your answers, including supporting evidence or analysis, and suggest any alternative approaches to achieving roaming. Please state any challenges you foresee and what you would need to address them.

Q7: Do you agree with our suggested criteria when requiring chargepoint operators to allow access to their network?

Provision of data on public electric vehicle chargepoints

Consumers should be able to locate and access chargepoints with ease.

The lack of mandated data provision adhering to a standard means chargepoint data can be incomprehensive and inaccurate.

More comprehensive, private sector-led solutions are emerging; however, this data is not openly available, meaning there’s a lack of competition in the EV services market.

We propose that government will set a data standard that CPOs need to meet when making public-chargepoint-data openly available and will mandate that ‘must-have’ data types including location, power-rating and pricing data must be made available.

We propose the data standard should be the internationally recognised OCPI as this provides the data types we think are likely to be most important to EV drivers.

We’ll continue to work with CPOs and wider industry to determine if live ‘availability’ data can be provided without impacting commercial interests.

Current state of the market and problems to be addressed

Open, accessible and reliable chargepoint data is essential for innovation, providing information to consumers, strategic network oversight and meeting our net-zero targets. We share the EV Energy Taskforce’s wish for a greater breadth of data types to be openly available and accessible on a consistent and accurate basis[footnote 10].

We want to enable software developers and automotive manufacturers to develop the tools needed to help consumers easily locate and access public chargepoints. This will also support network companies in their investment decisions for reinforcing the electricity grid and procuring flexible solutions.

The government established the National Chargepoint Registry (NCR) in 2011 to provide a public database of publicly funded chargepoints across the UK. It was intended to encourage CPOs to publish a freely available static dataset of chargepoints (for example, location, power rating and connectors) to promote the uptake of EVs. But the data is incomplete and contains inaccuracies due to an absence of agreed data sharing standards or incentives on parties to update and maintain their data submissions.

Central and local government and other parties with an interest in network oversight, planning or data sharing, including distribution network operators (DNOs), rely on oft-incomplete, unstandardised and inconsistent data. This impacts their ability to support network and new services development and optimisation.

Zap-Map, a user-friendly private-sector solution, is currently the most comprehensive data source available. We want to encourage greater competition and innovation in the EV services space. Most CPOs provide data to its platform, including dynamic availability data for 70% of the network.

Open data proposals

We developed and tested options for making chargepoint data openly available. This involved comprehensive market research and over 60 interviews with key stakeholders across different sectors including:

- local authorities

- central government

- CPOs

- DNOs

- planners

- OEMs

- software developers

- fleets

- power and utilities (P&U) companies

Data types

The table below presents a consolidated stakeholder view of ‘must-have’, ‘should have’ and ‘could have’ data types, and our preferred approach for making these data types available. We know that some stakeholders, particularly CPOs, have concerns about the sharing of live availability data. This is due largely to the commercial sensitivity around the utilisation of chargepoints.

But drivers must have access to the information they need to easily locate and access chargepoints. We invite evidence on options for making live availability data available to consumers.

Q8: Are there any ‘must-have’ data types that should not be made available? If not, state which data sets and why, providing evidence.

Q9: Do you think that the ‘should have’ and ‘could have’ data types should not be mandated to be available now?

Q10: What, in your view, should be included in the disabled access information?

| Data classification | Research outcome: data types needed | Preferred approach to making these data types available |

|---|---|---|

| Must have: | Static: – chargepoint ID – owner/operator – location (* address and coordinates) – operating hours – power (kW) – connector type (type 2, CHAdeMO, CCS) – payment method (RFID card, contactless, smartphone app, QR code) – cost of obtaining access – parking enforcement arrangements (and physical access restrictions) – disabled access information[footnote 11] dynamic: – availability (in-use, available, booked) – state of repair – pricing (p/kWh) |

Mandated provision of these ‘must have’ data types for the public chargepoint network in the UK through an application programming interface (API). This will specify: – semantics (meaning) – syntax (format) – quality – acess rights and permissions – transportation of data (how it’s shared) – governance of use of the data – where the data will be stored – how compliance will be enforced – what counts as ‘timely’ (meaning: refresh periods) *GPS coordinates are essential for accurate location data |

| Should have: |

– booking information [footnote 12] – ancillary services on site |

Not to mandate provision of these ‘should have’ data types at this stage. The data standard, OCPI, which government intends to adopt (see ]Introduction of the open-data solution](#open-data)) is structured to accommodate both booking information and ancillary services onsite should CPOs wish to provide this information[footnote 13]. |

| Could have: | dynamic: – who is charging [footnote 14] – queue length[footnote 15] – new chargepoints coming online soon – historic (aggregated) – utilisation – periodic aggregated view of UK public CP network [footnote 16] |

Not to mandate this data being made openly available, instead allowing the market to determine demand for these data types and how best to satisfy this. This data will however be captured and aggregated to form historic data sets available to nominated stakeholders (such as DNOs). |

Introduction of the open-data solution

Data standard(s) for CPOs are required to support the introduction of any open-data solution. Standards would specify the data types and the format they should be provided in, in addition to requirements for maintaining the data. They would also set out how provisions for access, storage and transportation of the data.

We propose that government set the standards for open public chargepoint data provision and delegate enforcement powers to an appropriate body. Feedback from stakeholder engagement indicates that most industry stakeholders believe that government is best suited to this role.

We propose to adopt a standard that meets the ‘must have’ data types, reflecting the public chargepoint network’s current and anticipated near-future needs. Adopting a single standard will help ensure consistency of data across the network.

Our preliminary research has indicated that developing a new standard specifically for the UK would be costly, delaying implementation of the recommended data sharing solution. We therefore propose to use the global and freely available OCPI standard. We propose that the OCPI latest standard is implemented throughout the CPO system. This would need to be reviewed regularly as the OCPI standard is updated.

While alternative industry standards exist, OCPI is the most utilised standard not only in the UK but also other international EV markets. The standard already enables widespread sharing of chargepoint data in Europe and is already familiar to or in use by some UK CPOs.

Flexibility to adapt to new standards in the future may be needed as standards or technologies emerge and/or evolve. We’ll keep under review the relevance of new and evolving standards, engaging with industry and consumers before adopting any new standards.

Q11: Do you think that Open Charge Point Interface should be adopted as the standard for the provision of public chargepoint data across the chargepoint operator’s systems?

Q12: Do you think that adoption of a standard will present challenges? If so, what challenges?

Data architecture

We’ve considered options for an industry-wide digital architecture to making public chargepoint data open and accessible. These have focused on 3 principal architectures:

- a distributed architecture, where CPOs individually publish data and consumers connect with CPOs on a bilateral basis

- a federated architecture, where data is ‘sent’ from multiple CPOs through one or more platforms.

- a centralised architecture, where CPOs ‘push’ their data to a centralised platform

Preferred approach for the industry data architecture

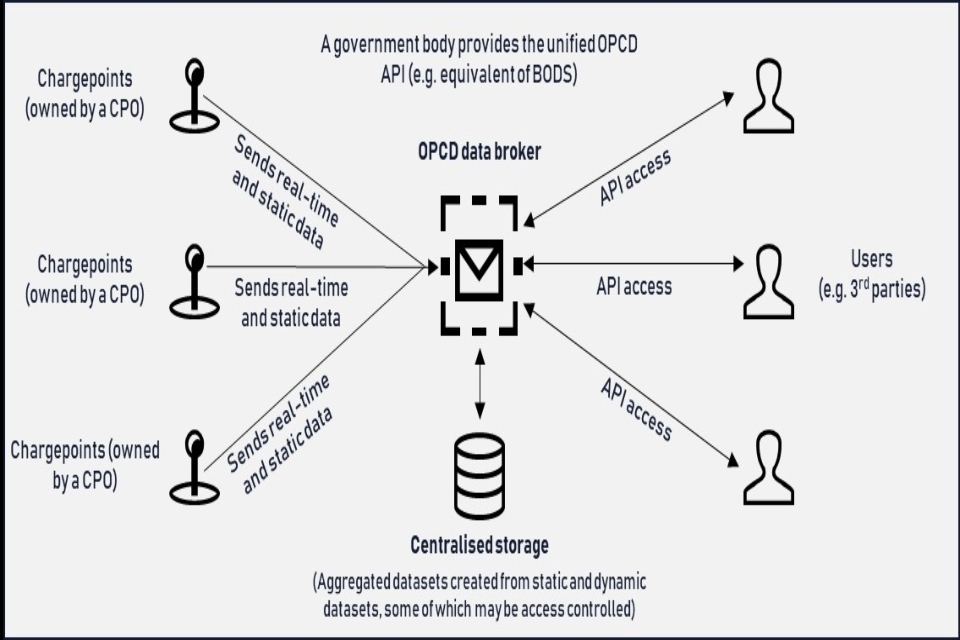

The research found a hybrid (federated – centralised) data architecture to be the most appropriate solution for the UK. Under this model, CPOs would manage their own data, sharing it with a centrally administered data broker through a push mechanism.

This approach provides a single unified interface (an API) for consumers to access chargepoint data from one location (meaning: a third-party app). Each CPO retains ownership and management of their source data. It avoids creating a disproportionate cost of compliance for those needing to share or access the data. EV data consumers will only need to access one interface, rather than multiple CPOs.

This simplifies the process and reduces costs. CPOs would ensure the management and provision of data access complies with the standards and policies set out by the government.

To enable this hybrid architecture, we propose a central API for use by consumers, and a centralised broker solution (with associated storage) to allow CPOs or data providers to share static and dynamic data. Chargepoint data will be openly available for consumption in line with established data-sharing attributes[footnote 17], enabling data to be understood consistently by all stakeholders. This will be flexible to grow with the rate of growth of the sector.

Figure 1: Overview of the Hybrid Digital Architecture Model

The model includes central storage of aggregated historic and static datasets, which eliminates the dependency and burden on CPOs to provide reports to support regulatory oversight and enforcement. It enables the creation of longitudinal datasets to inform ongoing government policy development.

Access to specific data sets may be limited to certain user types and this will be determined on a use case-by-use case basis. We’ll conduct a technical discovery, alpha and beta phase with input from industry in line with the Government Digital Service (GDS) code of practice[footnote 19].

Q13: Do you think that the preferred hybrid data architecture achieves the overall policy aim to make data available to support electric vehicle drivers?

Q14: What opportunities or challenges will this present for your organisation?

Q15: Are there any future technology, policy, or regulatory changes you are aware of that might impact the preferred data architecture?

Q16: What does government need to do to further minimise costs for industry?

Please provide reasons for your answers, including supporting evidence or analysis, and suggest any alternative approaches.

Alignment with Modernising Energy Data

Modernising Energy Data Access (MEDA)[footnote 20] is aiming to develop architecture to allow efficient data sharing, and enable interlinking of existing and new datasets, across different sectors. It offers an alternative approach to the hybrid architecture model as it may, for example, offer a solution that enables innovators to auto-pull open data from CPOs as needed.

The Energy Data Taskforce (EDTF) [footnote 21], commissioned by the Department for Business, Energy and Industrial Strategy (BEIS), Ofgem and Innovate UK, published a series of recommendations in June 2019. These advocated a shift towards a ‘presumed open’ data triaging model, centred around making data more visible and accessible through better data management and cataloguing. More efficient exchange of data will allow the energy system to optimise the use of low-carbon energy solutions – including EV chargepoints.

While the EDTF has now ended, the Modernising Energy Data (MED)[footnote 22] grou,p made up of BEIS, Ofgem and Innovate UK, has undertaken the implementation of the taskforce vision, alongside the delivery of MEDA. If viable, this would enable data-sharing between energy sector bodies, such as the DNOs and energy suppliers, and reduce costs across the value chain.

Close collaboration with MEDA also enables the possibility of reusing emerging data and digital infrastructure from other relevant initiatives. This is an opportunity to develop a coordinated, whole-system approach to data sharing, and to ultimately meet our net-zero targets.

Q17: Do you think the government should use the data architecture that emerges from the Modern Energy Data Access competition as a vehicle for open electric vehicle data?

Q18: Are there any related data platforms which the Open Public Chargepoint Data should be linked to? If so, please specify.

Pricing transparency

EV drivers should be able to easily compare the cost of charging between different networks.

Electricity drawn from public chargepoints by EVs is currently priced using a range of different metrics. This creates confusion for EV drivers and a lack of comparability of pricing information between different chargepoint networks.

We propose to mandate CPOs to adopt a p/kWh metric for a unit of electricity sold under both subscription and pay-as-you-go (PAYG) models.

CPOs will have the flexibility on how they display pricing, consumption and cost information to the customer in a clear and easily accessible manner.

The current state of the market and the problem we’re trying to solve

In today’s market, CPOs deploy a variety of different formats for pricing the cost of charging an EV. These include:

- a charge for the electricity drawn (p/kWh)

- a charge for the time spent charging (for example, p/minute or £ per 30 min/hour)

- a flat charge per charging session

- an annual or monthly membership fee, which can result in chargepoints that are free to use or charged at a lower rate per kWh or unit of time

- connection fees (a fee charged to connect to the chargepoint, approximately £1)

- overstay charges for customers staying when the EV has finished charging

Most CPOs charge for the electricity drawn in p/kWh. But analysis undertaken in August 2019[footnote 23] shows that 8 CPOs were charging on a time or per session basis, and 12 were charging connection fees.

In 2016, we consulted on potential pricing formats ahead of the introduction of the Automated and Electric Vehicles Act. An overwhelming majority of respondents favoured a pricing format of p/kWh.

The Alternative Fuels Infrastructure Regulation 2017 (AFIR) mandates that all public chargepoints must incorporate an intelligent metering system. Information on performance and how this is being converted for billing purposes must be available to customers at the point when they are recharging their vehicles[footnote 24]. CPOs can choose how they provide this information – for example:

- web app

- SMS

- at the chargepoint itself

Despite these requirements, they do not force CPOs to charge for electricity drawn in p/kWh.

Our proposed approach

We propose to mandate CPOs to adopt a p/kWh metric for a unit of electricity sold under both subscription and PAYG models. This would enable consumers to easily compare prices across the UK network and find the best available price. Any regulations brought forward would still permit:

- CPOs to provide free charging under their membership models (the kWhs drawn must be made available to the consumer after the charging event as required by AFIR)

- parking and charging bundled offers, where both are provided in a one-off fee (the kWhs drawn must be made available to the consumer after the charge as required by AFIR)

- CPOs applying overstay charges to prevent drivers from blocking a parking space after their charging session has ended

- giving CPOs the flexibility on how they display the proposed p/kWh cost of charging to the customer, and then how they display the kWh consumed and the total cost of the charging event, so long as it is clear and easily accessible for all customers

- consumers being paid to provide energy from their EV to the grid via vehicle to grid (V2G) technology

In the medium term, it’s intended that live pricing data will become available via our chosen open chargepoint data solution. This would then be available to consumers through third-party apps, further improving pricing transparency.

We propose that compliance with the pricing metric should apply as soon as the regulations come into force and that the unit price for electricity could change between the consumer first identifying a price for charging and then physically arriving at a chargepoint. The price the consumer pays must not change once they have initiated the charging event.

As the cost to the driver will be based on the quantity of electricity supplied, as determined by a meter, we consider that these meters are used for trade. They would therefore constitute a regulated active electrical energy meter which should comply with the Measuring Instrument Regulations 2016 (MIR).

The use of MIR-compliant meters will help ensure that consumers are not short-sold electricity because of an inaccurate meter. We understand that it will be costly for CPOs to have to retrofit their charging fleet with MIR-compliant meters. Therefore, we propose that this requirement will only apply to newly installed or renewed chargepoints.

Q19: Do you think the government should mandate a p/kWh metric? If not, why?

Q20: Do you think the government should allow chargepoint operators to have the flexibility to determine how the cost of charging, the energy consumed, and the total cost of a charging event is made available to a consumer?

Q21: Do you think the government should allow the exemptions to the p/kWh proposal and are there others we should consider?

Q22: Do you think that Measuring Instruments Regulations-compliant meters should be mandated for newly installed and renewed chargepoints to ensure the energy provided to a vehicle is accurately recorded?

Q23: Do you think that all chargepoints should have a Measuring Instruments Regulations compliant meters?

Reliability

Consumers should have access to a consistently reliable public charging network.

Public chargepoint reliability is improving. Analysis commissioned by the Office for Zero Emission Vehicles shows that in August 2019 around 8% of public chargepoints were out of service, a decrease from 15% in 2017. However, further improvements are required to drive consumer confidence in the public network.

We propose that CPOs must meet a minimum 99% availability standard as an average across its entire fleet of chargepoints. We expect industry to work with us to identify an effective approach to monitor reliability.

We propose that CPOs must provide a 24/7 call helpline for consumers so that help can be provided to consumers who are struggling to access or use a chargepoint.

We propose to allow CPOs a one-year lead time from the point the regulations come into force to comply with the standard. This is to enable supply chains and manufactures to respond to improve the reliability of products readily available.

Current state of the market and the problem we are trying to solve

Public chargepoints require regular maintenance when used in the public domain. We’re aware of a significant number of chargepoints that are out of action at any one time or have a fault that damages the consumer experience using public chargepoints. This is largely a consequence of CPOs or host sites having less of an incentive to repair them when utilisation rates are low.

There are different types of chargepoint failure. These include but are not limited to:

- malicious damage – physical or cyber abuse of the chargepoint

- software malfunction (within the chargepoint or via the smartphone app)

- hardware malfunction – wear and tear (for example, chargepoint socket gets worn meaning drivers struggle to connect properly)

Analysis undertaken by Zap-Map in July 2017 showed that 14.8% of public chargepoints or around 1 in 8 were out of service (including 4.1% partially operational)[footnote 25]. By August 2019, 8% were out of service. This compares with the 99% availability expected by chargepoint operators in the Netherlands.

It’s important to note that the 2019 analysis is based on 60% of public chargepoints providing availability data to Zap-Map and many CPOs cite much higher availability percentages.

Having a significant number of public chargepoints out of order creates inconvenience and frustration for consumers. It risks drivers running out of charge trying to find the next available chargepoint, posing a safety risk if they are left stranded.

Representations from industry highlight that many of the maintenance issues cited by consumers are derived from older charging equipment, some of which installed in the early days of the charging sector by local authorities who did not put in place adequate maintenance contracts.

We understand these views. But reliance on reputational impact alone will not deliver the improvements needed in sufficient time to ensure 99% availability across the network or consumer confidence in the public charging network.

Our proposed approach

We propose introducing regulations mandating that CPOs must meet a 99% availability standard as an average across its entire fleet of chargepoints.

Where a chargepoint has an assumed starting availability of 24 hours a day, 365 days a year, the operator would be allowed up to 4 days’ of downtime per chargepoint for repairs and maintenance a year.

For chargepoints with restricted hours, the 99% standard would apply to those restricted hours. By giving CPOs the flexibility to meet the target as an average across its entire fleet, it provides them with longer lead times for more troublesome repairs such as tethered connector replacements.

We’re also proposing to mandate that CPOs provide a 24/7 call helpline for consumers so that assistance can be provided to consumers who are struggling to access a chargepoint, for example, if a CPO’s app isn’t working correctly on their phone. The provision of this service is already commonplace among most CPOs. Consumers must be able to contact an operator for support, and to resolve any issues as quickly and as easily as possible.

We’ve considered applying that 99% standard to all chargepoints on a chargepoint network. But we do not consider this appropriate at this stage. It places a significant burden on CPOs, giving them very little flexibility in meeting the target at a time when the business case for installing and operating public chargepoints is challenging. A tighter standard may also skew the market towards larger CPOs with greater financial backing and the ability to quickly improve their supply chains.

Implementation of reliability standards

We recognise that monitoring and reporting of the reliability standard presents challenges due to variation in chargepoint technologies, configurations and communication systems across different chargepoint networks. We want to work with industry to identify a solution to define ‘available’ and establish the best approach to collecting relevant data, where currently this is not openly and readily available. Options could include data collection, self-reporting requirements on CPOs, or the introduction of a gold-standard certification process.

CPOs will need time to improve their supply chains and for manufacturers to improve the reliability of their products, which is an ongoing process. Therefore, we propose to give CPOs a one-year lead time from the point the regulations come into force and having to be compliant with the standard.

The 99% fleet average target makes clear the downtime that is allowed across a chargepoint network. Therefore, we do not consider we need to specify repair times in regulations. We’ve considered whether any types of failure warrant exemption from the target in regulations. A failure that is out of the CPO’s control is a power outage causing the supply of electricity from the network connection to cease. Therefore, we would look to exempt this type of failure from the availability standard. DNOs are responsible for correcting such an outage[footnote 26].

Q24: Do you think that a reliability standard should be set?

Q25: Do you think that the 99% availability standard should be set on a fleet average basis?

Q26: Do you have any other suggestions to achieve a more reliable network?

Q27: Do you agree a one-year lead time for operators to achieve reliability compliance after the regulations come into force is sufficient to implement the reliability proposals?

Q28: If the reliability metric across fleets was enforced, we propose that there should be exemptions from the availability target that are out of the operator’s control. What types of failures should be exempt?

Q29: Do you think the government should mandate that chargepoint operators provide 24/7 call centres? Should we mandate this be low-cost or free-to-call?

Impact assessment

A detailed impact assessment will be carried out drawing on the evidence gathered from this consultation. We expect the proposals in this consultation to result in hardware, software and operating costs to:

- retrofit and install necessary equipment to all existing and new chargepoints to meet the minimum payment requirements (minimum payment requirements)

- upgrade the chargepoint network to provide a QR code facility (roaming option 2)

- establish an interoperable roaming platform (roaming option 3)

- open chargepoint networks to any accredited third party eMSP (roaming option 4)

- gather and present ‘must have’ data (open data)

- adopt a p/kWh metric for a unit of electricity (pricing transparency)

- meet a 99% availability standard and provide a 24/7 helpline (reliability)

We expect these costs to be offset by improvements in the consumer experience due to reduced search time, payment time and time planning journeys, and increased comparability of prices, enabling consumers to select the lowest price.

Q30: Provide any cost and consumer data you may have to support a detailed assessment of these impacts (provide separate data for minimum payment methods, roaming, open data, price transparency and reliability).

Q31: Do you think there are other impacts that have not been identified? If yes, what other impacts are there that you think have not been included (provide supporting evidence)?

Q32: Are there any groups you expect would be uniquely impacted by these proposals, for example small businesses or people from protected categories? If yes, which groups do you expect would be uniquely impacted by each of these proposals? Provide supporting evidence.

Enforcement and penalties

We’ll work with CPOs and the wider industry to provide the support and guidance necessary to ensure the smooth introduction of the regulations, and to assist in compliance with the regulatory requirements.

We propose appointing an appropriate body to enforce the regulations. We’ll assess options ahead of the introduction of the regulations. We propose to introduce a similar approach to enforcement as that adopted under the AFIR. The enforcement body will require powers to inspect, test and remove hard and software situated on both public and private land.

We anticipate that, where they consider there to have been a breach of the requirements, they may serve a notice on the person in breach describing the steps required to remedy it and by when. Where a person does not comply with the compliance notice, the enforcement body may require them to pay a civil penalty.

The civil penalty regime will need to be fair and proportionate, and ensure that CPOs are not penalised for aspects over which they have no control. Any civil penalties will be at the discretion of the enforcement body. This will take various factors into consideration, for example, the:

- nature and perceived intent of the non-compliance

- number of consumers impacted

- frequency of non-compliance

- materiality of a penalty to company finances

Emerging policy areas

Consumers need EV charging to be as easy, if not easier, than current refuelling of petrol and diesel vehicles. Consumer protection is an area of growing importance that cuts across private and public spheres. This section outlines emerging policy areas, including accessibility, weatherproofing, lighting and signage.

We’ve explored these areas through existing user research and we’re seeking feedback on our proposed objectives. We’ll use this to inform our views on the extent to which any further intervention is required at this stage.

Q33: Do you have concerns about consumer protection related to the use of public chargepoints that haven’t been discussed in this consultation? Please provide reasons, analysis or evidence on what other consumer protection issues should be considered by government in the future.

Accessibility

Anyone, regardless of their mobility, should be able to access EV chargepoints. Currently, there’s little in the way of regulation that specifically directs CPOs and local authorities to make chargepoints accessible to those who experience disabilities[footnote 27].

Under the Equality Act 2010, goods and services, including petrol filling stations, have a duty to make reasonable adjustments so that everyone can access their facilities. Provisions for adjustments are not prescriptive – leading to a different experience for disabled users depending on the station used.

The switch to mass-market EVs creates a significant opportunity to ensure that the UK has one of the most accessible and user-friendly chargepoint networks, and improves upon internal combustion engine (ICE) vehicle refuelling infrastructure accessibility. Retrofitting chargepoints is likely to increase costs overall.

An example of the most accessible public chargepoint in the UK is in Salford, which was co-designed with People’s Parking[footnote 28]. The bay is a dual blue badge and electric charging bay. In the recent survey by the Research Institute for Disabled Consumers[footnote 29], of the respondents who had seen public charging for EVs, 73% perceived them as neither accessible nor easy to use. 26% categorised ‘finding accessible chargepoints’ as a key concern about owning an EV.

Case study – Motability, the disability and transport charity

With the end of the sale of petrol, diesel and hybrid vehicles rapidly approaching, a large and important group of consumers risk being left behind as we transition to a greener future. 21% of people reported a disability in 2018 to 2019 and that proportion is rising.

Motability estimates that there will be 2.7 million drivers living with disabilities in 2035, with up to 1.35 million partially or wholly reliant on public charging infrastructure. Yet, many components of this infrastructure – such as heavy charging cables, connectors that require force to attach and parking bays without dropped kerbs – are being designed without their needs in mind.

People living with disabilities are also less likely than non-disabled people to own or rent homes where effective home charging solutions can be implemented. Motability argues that if we’re to create a truly inclusive energy transition, accessibility must be a key focus of the EV consumer experience.

Having a reliable mode of transport is particularly important to those who have a disability. It’s paramount to a person’s independence and autonomy that they can reliably use their vehicle. There are concerns around the current provisions for disabled users at chargepoints. These range from high raised kerbs and insufficient space around bays to charging cables as tripping hazards.

It’s important for any new and emerging technology to be user-friendly, both to support individual drivers and to encourage the widespread take-up of EVs. This is a complex area with responsibilities falling across several parties. We want to continue working with consumer representatives, CPOs, local authorities and other interested parties to understand priority issues and whether there is a need for central government intervention.

Q34: Do you agree with the accessibility issues raised?

Q35: Are there any accessibility issues we should regulate on?

Q36: Should there be standards that are enforced/brought in across chargepoints (such as payment height and instructions)? If so, what standards?

Q37: Do chargepoint operators need to provide supervised stations to help assist those with accessibility needs?

Weatherproofing and lighting

Chargepoints are installed in a diverse range of locations, often in more isolated locations than is the case for fuel stations for diesel or petrol vehicles.

One type of charging location where consumers can feel safe and covered is in a charging hub. Government, Innovate UK and industry have invested in hubs across the UK. The first installation of a hub was in Dundee within walking distance of the city centre with capacity to charge 18 EVs at once, while providing users with a sheltered and well-lit charging location.

Hubs have now been or are being set up in cities across the UK. Many are installed with roofing and lighting, solving issues surrounding weatherproofing, lighting and signage. The Mayor of London has specified the desire to have at least one hub in every sub-region of London.

However, much of the charging on the public network will not be in these types of larger charging hubs. We’re interested in views as to the extent to which requirements are needed to provide specific lighting and/or weatherproofing arrangements in other settings. We need to balance providing a safe experience for EV consumers with the risk of additional cost and negative impact on local areas’ work to reduce street furniture, which could lead to residential opposition to new installation of public chargepoints[footnote 30].

Q38: Does the lack of weatherproofing and lighting at most chargepoints require improvement? If so, what would this look like in your view?

Q39: Should any improvement apply to all chargepoints or those in specific locations? If specific locations, can you identify which?

Signage

Drivers need to be able to locate chargepoints quickly and easily while driving. One option to support this would be to introduce signage requirements. We want to balance EV signage requirements with local approaches to reducing street clutter. There are several existing policies to support locating individual charging points. We do not think additional mandatory requirements are required at this stage; however, we welcome views on this.

EV charging is usually delivered in the form of a dedicated EV charging or parking bay that is signed at the location to ensure use by EVs; in common with other parking bays (for example, disabled badge holder bays), direction signs are not erected to them.

There is a dedicated standard on-street parking signage for EV chargepoints for use next to an EV parking space with a chargepoint. Signage is enabled by the Traffic Signs Regulations and General Directions with placement determined by local authorities. Whether EV charging spaces require permits and other specific parking requirements is at the discretion of local authorities.

These signs indicate EV chargepoint locations in a standardised way without causing too much street clutter. We’ll continue to work with local authorities in providing advice and are currently developing guidance relating to the deployment of chargepoints to reinforce the need for proper signage for EV parking bays without undermining local authorities’ work to de-clutter their streets.

Currently, chargepoints are not indicated on motorway service area (MSA) signage on the motorway. Current regulations require signing indicating up to 6 facilities. These are represented by pictogram symbols for facilities or brand logos and can be a mix of both. MSAs must pay for the cost of the signage (£30 to £40,000) and it’s therefore commonplace for the signage to include 6 of the main brand logos in exchange for a financial contribution from commercial operators.

The current government ambition is to have at least 6 high-powered, open-access chargepoints in every MSA in England by 2023. We’ll work with MSAs and CPOs to ensure appropriate signage are provided as part of any funding provided under Project Rapid. Over the next 5 to 10 years, as EV charging becomes more profitable, we expect that CPOs will become one of the major commercial operators in MSAs and will be able to finance the location of their service, including on the MSA approach signage.

Consumers can also find the general location of chargepoints through apps such as Zap-Map, Google Maps and EV navigation systems. However, the location on such services is not always precise. Implementation of our proposals to open data to third parties will enable other similar services to emerge. More precise latitude and longitude data from public chargepoints will be accessible by vehicle navigation systems and third-party applications pinpointing the exact location of the chargepoint.

Q40: Is signage to chargepoints an area that requires improvement? If so, what would this action look like in your view?

What will happen next

A summary of responses, including the next steps, will be published within 3 months of the consultation closing. Paper copies will be available on request.

Annex A: consultation principles

The consultation is being conducted in line with the government’s key consultation principles.

If you have any comments about the consultation process, please email consultation@dft.gsi.gov.uk

Annex B: definitions lists

- AFIR – Alternative Fuel Infrastructure Regulations 2017

- CPO – A chargepoint operator operates one or more charging stations on its own account and is responsible for the installation, operation and service thereof

- DNO – distribution network operator

- dynamic data – describes data types that are subject to change on a regular basis such as whether the chargepoint is in use or available

- eMSP – an eMobility Service Provider is a provider of charging services to customers. Such services typically include providing access to charging stations for vehicle users via charging cards or apps, processing requests to charge, and taking payments for charging sessions. A CPO may also perform the role of an eMSP

- EV – electric vehicle

- p/kWh – pence per kilowatt hour, a measurement of the price per kilowatt hour

- MIR – Measurement Instrument Regulations 2016[footnote 30]

- MSA – notorway service area

- OCPI – The Open Charge Point Interface protocol is an international standard that enables chargepoint operators to standardise their data collection and storage

- OEM – original equipment manufacturer

- PAYG – pay as you go. In this context, for consumers who drive to the chargepoint, charge and pay at the chargepoint either through contactless, an app or through another payment method after each charging session

- public chargepoints – a chargepoint intended for use by members of the general public as defined in the AFIR regulations[footnote 31]

- roaming – CPOs and eMSPs enter into agreements with each other or an intermediary body that enable customers to use one membership account to access and pay at the stations of multiple CPOs

- RFID card – radio-frequency identification chargepoint travel card, which enables users to charge without using an app

- static data – data that describes the reference data of the chargepoint such as location, number of charging points and who operates and owns the chargepoint

- V2G – vehicle to grid technology enables batteries to store and discharge energy back to the grid

-

Electric Vehicle Smart Charging (PDF, 916KB) ↩

-

AFIR defines ad-hoc access as ‘the ability for any person to recharge an electric vehicle without entering into a pre-existing contract with an electricity supplier to, or infrastructure operator of, that recharging point’. ↩

-

“All new rapid chargepoints should offer card payment by 2020”. ↩

-

“All new rapid chargepoints should offer card payment by 2020”. ↩

-

A parallel to this are the food apps, such as Just Eat and Uber Eats. Consumers can order from multiple restaurants using one smartphone app. ↩

-

As part of our accessibility emerging policy area, we’ll work with accessibility groups to identify the key accessibility data types. ↩

-

Booking information pertains to data associated with the booking of fixed charging timeslots. ↩

-

OCPI documentation, version 2.2. ↩

-