Looking to the future: greater member security and rebalancing risk

Published 22 November 2023

Applies to England, Scotland and Wales

© Crown copyright 2023

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/calls-for-evidence/looking-to-the-future-greater-member-security-and-rebalancing-risk/looking-to-the-future-greater-member-security-and-rebalancing-risk

This document is the government’s:

-

Part 1 – response to the public consultation on the proposal to resolve the small pots issue

-

Part 2 – call for evidence on the long-term direction of workplace pension saving

Ministerial Foreword

The issue, and continued growth, of deferred small pots puts huge pressure on individuals and the pensions industry; adding increased costs and inefficiency into the UK workplace pensions market. Estimates show they result in annual industry-wide losses of up to £225m, reducing the value for money schemes can provide. This is an issue that continues to worsen, and despite significant industry work over the last few years, no clear consensus has been found.

In July, the department launched a consultation proposing to take forward the multiple default consolidator approach to tackle this issue; to ensure that a better functioning and more efficient pension market, while supporting member engagement where possible. This consultation response reaffirms my intention to proceed definitively with this approach, which we estimate will benefit the average saver by £700 at retirement[footnote 1], we must now move towards delivery.

I understand that not all of industry will agree with this direction, however, in the long term, we expect commercial interests to be aligned with this ambition. Through the industry delivery group, we will work together, continuing to put members interests first.

The small pots solution is just a starting point. I want to understand how we can go further to set out a long-term vision for workplace pension saving. Savers will still be left with multiple pots to manage. This, makes it harder to maximise their savings, understand what they have, and manage their retirement funds. Australia have successfully implemented a ‘stapling’ model, based on the idea of a pot for life. I want to understand what the benefits and considerations of this approach are.

I also want to see the CDC market expand, so that more savers can take advantage of the benefits it has to offer. This offers the opportunity of higher overall returns on investments and a solution for accessing their pots without the need to engage.

There may also be mutual benefits between the two, including how lifetime provider could help grow the CDC market. There will be questions for this including the right time to look at this and how we would go about phasing any future implementation.

These options build on the current package of reforms, including the multiemployer CDC schemes, the small pots solution, the Value for Money Framework, and the development of decumulation products. Both these measures could improve the opportunity for investment in productive finance assets, given the potential for longer investment horizons, supporting better member outcomes.

Nothing here is intended to change the current and medium-term development of the CDC and the decumulation products markets. We want these innovations to facilitate the delivery of potential long-term changes. We need to balance the needs of those approaching retirement today, and those still a long way off retirement. This is all part of the wider plan for pensions, which has pension savers at its heart.

Paul Maynard MP, Minister for Pensions

Introduction

The first part of this document sets out the feedback the Department for Work and Pensions (DWP) received to the consultation which ran from 11 July 2023 to 5 September 2023. The consultation concentrated on the government’s proposals to implement a multiple default consolidator approach to end the proliferation of deferred small pots, with several questions around the proposed framework. The document then goes on to set out the government response in respect of the proposed framework and next steps, considering the feedback received.

The second part of this document looks to set a long-term vision for workplace pension saving in the UK. It explores the potential development of a lifetime provider model and the relationship between Automatic Enrolment (AE) and the development, and wider use, of Collective Defined Contribution (CDC) schemes.

Part 1: Government response to the consultation – ‘Ending the proliferation of deferred small pots’ and next steps.

November 2023

Chapter 1: Summary of responses to the consultation

About the government response

1. This document forms the government’s response to the public consultation[footnote 2] that was launched on the 11 July 2023 and closed on 5 September 2023. The public consultation sought views on the department’s proposals to implement a multiple default consolidator approach to solve the proliferation of deferred small pots, with several questions for stakeholders to offer views on proposals.

2. The consultation set out the department’s ambition to introduce a multiple default consolidator system, whereby members with deferred small pots will be automatically consolidated into a small number of schemes that are authorised, by the relevant regulator, to act as a consolidator. As part of this, the consultation proposed the following:

- that a central clearing house would be created to act as a central point informing schemes where to transfer a members’ eligible deferred pot

- that a pot would be eligible for automatic consolidation 12 months after the last contribution was made into the pot

- that the maximum pot size limit for automatic consolidation would be initially set at £1,000, with a statutory requirement on the Secretary of State to review this limit at regular intervals

- that there would be no minimum pot value for a pot to be eligible for automatic consolidation

- that we would not mandate schemes to undertake same scheme consolidation, however, we would encourage schemes to undertake this where possible

- that we encourage the member exchange group to continue with their work to test the feasibility of the solution, given the learning opportunities and insight it will provide to support the delivery of the proposed multiple consolidator approach

- that we will form an industry group in late 2023 working with interested parties to explore the design and implementation of the default consolidator framework

Responses to the consultation

3. We received 55 responses to the consultation, this included responses from the following sectors:

- 20 Pensions schemes providers

- 20 Pensions industry professionals/trade representatives

- 4 Law firms specialising in pension(s) law

- 7 Financial service providers

- 2 Employer/employee representatives

- 2 Consumer groups

4. Chapter 1 of this document highlights the main feedback raised in response to consultation questions but is not an exhaustive commentary on every response received.

A Clearing House or a Central Registry?

Question 1: Do you agree with this proposal or do you believe a central registry would be a more effective approach to support the consolidation of deferred small pots, if so how would you design a central registry?

Summary of responses

5. The consultation set out the importance of having a central point or system to manage and match data, to enable ceding schemes to identify where a member’s deferred pot should be transferred. The consultation proposed two options for this:

- a central clearing house (which would be responsible for matching deferred pots and lead on communication with members and schemes), or

- a central registry (which would act as a database which schemes could access to identify where a member’s chosen consolidator was)

6. Throughout the responses there was broad support, across a range of sectors, including pension providers, for the adoption of a clearing house. These responses agreed with the benefits set out in the consultation and outlined some additional benefits for a clearing house the consultation did not raise.

7. Respondents suggested that the creation of a clearing house could make the automated process simpler for providers, given they would set up systems to interact with a single organisation, which they considered would be preferable than dealing with multiple potential competitors. Further to this, respondents believed that a clearing house would be less complex for members and could result in improved understanding/engagement, as they would engage with one organisation and remove the risk of multiple providers contacting members regarding their various pots.

8. It was also suggested by some respondents that the clearing house provides a more effective model for capturing and consolidating historical pots than a central registry, given it is less reliant on individual schemes and can take a holistic view across the whole market. Other benefits of the clearing house approach raised by respondents included, that, dependent on the design, there may not be a need for a regulator to directly monitor the clearing house if it were a public body, reducing cost and burden, whilst also ensuring that clearing house is fit for purpose.

Which?:

We agree with the arguments set out in the consultation in favour of a central clearing house and we believe this is likely to produce a simpler and more consistent experience for members. The specific design of the clearing house and the proposed consolidation process will need careful development and will likely benefit from testing with members.

9. In addition, some responses to the consultation suggested that the clearing house could support the government further if they wished to explore a longer-term aim of moving towards a lifetime provider/stapling approach.

Hargreaves Lansdown:

The clearing house should be designed so that it could also be used for pension contributions as part of a future lifetime pension. The additional functionality would be to allow payroll contributions to be paid from a participating employer to the employee’s chosen pension scheme.

10. However, some respondents raised concerns about the clearing house approach, with a key concern being around how the clearing house will be funded. To set up the clearing house there will be initial costs to create and develop systems, with the necessary automated processes, as well as ongoing costs in terms of data storage, system maintenance and administrative costs. Some schemes suggested they would not be supportive of existing levies being increased or new levies being applied to schemes to cover these costs, while other schemes suggested that this would be the most appropriate funding model.

Smart Pension:

As stated in the consultation this will require additional investment. We would be keen to understand how this would be funded. In particular we would not be supportive of levies being increased or applied in order to bear these costs.

Scottish Widows:

We should also consider how a clearing house would be funded. In our view, given that ending small pot proliferation will benefit the whole industry, the whole industry should contribute to the solution. This may be achieved through the General Levy or a similar mechanism.

11. Some responses outlined that there would need to be significant thought given to messaging around the clearing house; to ensure that members are aware of the role of the clearing house, to avoid the presumption that it could be a scam, some respondents suggested that this could be mitigated through clarity that the communication is coming from a government/ government backed organisation. Several respondents raised concerns around the clearing house and potential security risks. An additional risk outlined with this approach is that it is reliant on the clearing house having the correct contact details for members. This may result in members having their pots consolidated without being given the opportunity to opt-out as communications never reached them.

Capita:

It is essential that the clearing house is a trusted, government-endorsed organisation, as individuals will otherwise see any approach about a pension transfer from an unknown entity as a potential scam.

Sackers:

Whether a clearing house or central registry is used, thought will need to be given to ensuring appropriate data protection and cyber security measures are in place to reduce the risk of breaches and scams, and to promote confidence in the system.

12. While most respondents, supported the clearing house approach, some felt that a central registry approach would be more suitable. This was generally because of the belief that this approach would be quicker to implement and could potentially rely more heavily on the work already undertaken as part of pensions dashboard[footnote 3].

13. In addition to this, respondents considered that the creation of a central registry would have lower implementation costs in comparison to a clearing house. Given a clearing house will require the development of a new digital infrastructure whereas the central registry relies on communication between providers. A small number of respondents also considered that a central registry approach could be more efficient in practice as providers would be able to access the database themselves and send their own communications. Alongside this, respondents also suggested that if the communication was coming from a provider the member already has a pot with (as it would with the central registry approach), this could reduce the risk of members not engaging with communication regarding consolidation of deferred pots.

14. However, there were significant concerns raised in response to the central registry being a security/data risk and ultimately a target for cyber-attacks.

Society of Pension Professionals (SPP):

We acknowledge that the most effective and cost-effective approach could (as is suggested) be to use the pensions dashboards framework as a central registry point in the long-term. However, we are not convinced the current initial framework and infrastructure would be sufficient in terms of holding the relevant data to do this effectively, thus, further developments would be required to use the dashboards framework for this purpose.

15. Another option raised in response to our consultation was that rather than creating a single centralised organisation to allocate small pots to consolidators, we could look to adopt a model like seen in Australia. Under this approach, it was suggested that DWP or HMRC or another part of government could act as a central point focussing on developing the enabling services and rules that will govern the network, which will enable third party clearing houses to connect and act as a clearing house providing services to schemes directly; in a cost-effective, timely manner.

What happens when a member fails to choose a consolidator?

Question 2: Which, of the options we have set out, do you think is the best approach to allocate a member a default consolidator in cases where a member does not make an active decision? Are there alternatives?

Summary of responses

16. The consultation set out two options as potential approaches to allocate members to a default consolidation in situations where a member did not make an active choice, these options were:

- Option A – allocate all small pots between the providers who meet the criteria to be a consolidator at a level proportionate to their market share

- Option B – given the likelihood that a member will have a deferred pot already with a consolidator scheme, this scheme would be allocated as the members consolidator scheme. In cases where a member has pots with multiple schemes that are authorised consolidators their deferred pots could be allocated to the consolidator scheme that holds their largest deferred pot

17. There was broad agreement from respondents that Option A was a less favourable approach than Option B. With Option A being criticised for a range of reasons, the key concern being the risk of creating an uncompetitive default consolidator market, bedding in existing market share, and restricting the ability of new entrants to the market, whilst removing incentives for smaller providers to grow their share of consolidated pots.

18. Alongside this, respondents felt the suggestion that this approach would reduce the risk of creating an oligopoly was not relevant, given the policy aim to introduce a small number of default consolidators in the first place. Respondents considered there to also be a risk that this approach could unfairly benefit some schemes and not comply with competition law, whilst also require regular monitoring, which could be challenging to implement effectively.

The Investment and Life Assurance Group Limited (ILAG):

Under Option A, we question if allocating pots based on a consolidator’s market share might create perverse incentives to manipulate size. In any case, market share can change significantly if, for example, one provider loses a very large employer to a competitor, and this would need to be monitored and updated on a regular basis.

19. In addition, responses outlined Option A reduces the chances of a member being allocated to a consolidator where they already have a deferred (or active) pot, resulting in a higher number of transfers than potentially required and resulting in more members being allocated to a consolidator where there is no previous relationship – increasing the risk of members being disengaged and/or confused. With a common view across respondents that it would be more favourable to design the approach in a way that pots are consolidated with or into existing pots where possible – given it would reduce unnecessary administration costs and would build on an existing relationship between the members and provider.

20. Further to the engagement argument, respondents also made the point it would be simpler for members to understand why their pot had been consolidated into an existing pot rather than a new pot being created with an alternate scheme, crucial to meeting one of our key objectives – faith in the system on the part of members.

21. In response to Option B, respondents highlighted that they thought the key benefit of allocation pots based on greatest value was that it would support consolidators to develop economies of scale, noting that very small pots are costly to run and are unprofitable – so this could be an important balance to ensure that consolidators are financially viable.

22. Alongside this, respondents suggested that Option B could reduce the overall number of transfers as pots will stay with authorised consolidators in the first instance (as opposed to Option A where there is no link between where a member’s pot is and where they will be allocated as a consolidator).

Society of Pension Professionals (SPP):

We are supportive of Option B as a default for members who have a small pot with an existing consolidator. This will simplify the journey and likely provide a better outcome and experience for members. It will also minimise administration for ceding schemes and better support economies of scale for the consolidators.

23. However, some respondents presented areas where they thought Option B would need to be amended to work in practice, one example of this is for a member who does not have an active pot with an authorised consolidator. Alongside this, respondents suggested that this approach is only effective if the schemes that hold many deferred pots apply to become a consolidator.

24. In addition to the two options presented in the consultation, some respondents proposed alternative approaches, with some suggesting that a combination of the different options would work best. Some respondents felt that Option B could work well if this approach was combined with additional criteria/factors. For example, in the first instance, where a member does not make an active choice regarding their consolidator, they would be allocated a consolidator based on where their largest pot was (with an authorised consolidator). However, in cases where they do not hold a pot with a consolidator, they would then be allocated a consolidator based on a carousel approach – where each consolidator gains an equal proportion of deferred pots for members which fall into this category. This approach will allow a member to keep an existing relationship with a previous consolidator if they have one.

M&G:

We believe that a simple carousel system whereby small pots are divided evenly between all registered consolidators unless the member makes an active decision would be a better option – allowing for new market entrants and fair competition.

25. A further alternative, which some respondents suggested, was that in the first instance a member should be consolidated into a consolidator scheme where they have an active pot. With respondents arguing that this is likely to increase the chances of engagement, due to the link to their current pension pot with their current employer.

Authorisation to act as a Consolidator

Question 3: Do you agree that there is a need for an authorisation regime for a scheme to act as a consolidator? If so, what essential conditions do you think should form part of the authorisation criteria?

Summary of responses

26. The consultation set out the importance of ensuring that schemes acting as default consolidators must demonstrate that they deliver good levels of value for money for their members. As such the consultation proposed the idea of an authorisation regime, operated by the relevant regulators, which would set out certain conditions that a scheme must meet to become a consolidator.

27. Overall, there was strong support for an authorisation regime for a scheme to act as a consolidator, with the majority of respondents agreeing that this should be a key part of the multiple default consolidator framework. With respondents providing a wide range of essential conditions for a provider to become a consolidator. The most common of these was ensuring that the consolidators provide strong value for money (VFM) outcomes for members ensuring that a small pot would not be transferred from a well performing scheme to a poor performing consolidator.

28. A consistent argument put forward in responses was making sure a member’s pot was protected from schemes with poor investments returns to minimise the risk of a pot reducing in value following consolidation. Responses tied this argument closely with the VFM a scheme was able to provide for a member’s small pot. Similarly, some respondents made it clear that the consolidators should be monitored by a regulator, to ensure that they continue to provide the levels of value they had to demonstrate in order receive authorisation to act as a consolidator.

29. Another common view presented by respondents was that schemes should be able to demonstrate an ability to process transfers efficiently at a low cost; given it will be essential to keep costs of transfer as low as possible to make the economics of an automated solution work.

30. Respondents raised questions around what charging structure consolidator should be allowed to use, with some suggesting that they should not be able to charge a flat fee on consolidated pots; with the argument that there would be little benefit to the member of consolidation if their pot was exposed to higher charges.

Hymans Robertson LLP:

We agree that there should be an authorisation regime. Without an authorisation regime there is a risk of having consolidators that don’t offer value for money. This will ensure there is a positive investment strategy for members. There should be some sort of regulation around charges for small pots members, possibly not allowing the charges in the consolidator to be higher than the charges in the scheme they are coming from.

31. Some responses presented the view that they expect a consolidator to demonstrate more regular contact with members than is required under current regulations; with a particular focus on member communications with a drive to increase member engagement. Respondents argued that member communications and engagement should be measured, to ensure they are keeping to a set standard. Additionally, a large number of respondents agreed with our consultation that schemes must actively undertake same scheme consolidation as part of the authorisation process.

32. However, some respondents argued that same scheme consolidation should not be mandated or required as part of authorisation to act as a consolidator because multiple benefit tiers should be transferred on a like-for-like basis (for example, protected Normal Minimum Pension Age (NMPA) 55), and this may be difficult under a same scheme consolidator approach.

33. While most respondents considered that an authorisation regime to act as a consolidator was necessary, some respondents considered that the current Master Trust Authorisation and Monitoring regime was sufficient for trust-based schemes, and to avoid additional burden/complexity on pension schemes we should proceed under this approach.

Mercer:

We do not believe that there is a need for an extensive regulatory regime specific to consolidators as long as they are authorised master trusts. The master trust supervisory regime, combined with the new holistic VFM requirements, will, in our view suffice.

Pot size

Question 4: Do you agree with setting the initial maximum limit for consolidation at £1,000, with a regular statutory review?

Summary of Responses

34. The consultation discussed the importance of setting the correct eligibility scope for automatic consolidation, with the risk of going too low being that you reduce the level of consolidation resulting in a situation where the cost of implementation is higher than the potential savings/benefits. Whereas if you go too high there is a greater risk of detriment to members and scheme, if the individual was consolidated into a scheme that had lower investment returns. Therefore, the consultation suggested an initial maximum limit for consolidation of £1,000, with a regular review to ensure the limit remained appropriate.

35. Responses to this question were mixed, with broadly half the responses agreeing that £1,000 struck the right balance, with the other half disagreeing – either considering the limit should be higher or lower.

36. Respondents who supported the £1,000 limit outlined that they considered this to be a good starting point to achieve significant levels of consolidation without having an overly destabilising effect on the market. With respondents agreeing that with the overall average pot size being approximately £350[footnote 4], this limit would allow for the consolidation of a significant number of pots and benefit many members.

Which?:

The data presented in the consultation document suggests that £1,000 will be sufficiently high to capture enough pots with a sufficiently large total asset value to make the introduction of an automatic consolidation process worthwhile.

37. Throughout several responses to this question, it was argued that, from the perspective of a member, £1,000 is very small in terms of the impact it can have on their retirement income. By having a higher maximum value for consolidation, it allows a member’s pot within a consolidator to increase in value at a greater rate, as a result of more pots being eligible for consolidation, and is more favourable for investment. Whilst also supporting consolidator schemes to increase their scale, enabling them to provider greater economies to their members.

38. Respondents suggested that when considering the implementation of the solution, the Government should give thought to a phased approach to the pot limit, gradually increasing the limit over time to reach £1,000. Allowing for a more gradual roll out will enable schemes to test the initial process with lower value pots, while also reducing the financial burden of transferring a significant number of assets out of their scheme.

The Investing and Saving Alliance (TISA):

The data shows the average value of a deferred pot of under £1,000 is £350. It would seem prudent to set the initial deferred small pot limit at £500 to ensure the regime, once implemented, is functioning as intended without consumer detriment. Once the framework has been proven in an operational environment over a period of time, we believe it would then be appropriate to increase the limit to £1,000 without the need for a full statutory review.

39. Some respondents agreed with the initial figure of £1,000 as a starting limit, however, went further and argued that this figure should be regularly reviewed with the aim of increasing it overtime. One reason behind this viewpoint was as the value of the limit gets higher it captures more pots and therefore benefits more members. Further as schemes become more in tune with the policy of consolidation the market will be more susceptible for slow gradual increases, therefore will have less of an effect.

40. However, some responses argued that the limit should be set higher, given how quickly a member is likely to reach the £1,000 limit, considering this would be too low for the solution to have any real impact on the overall number of deferred small pots. With increasing wages and inflation, the figure could quickly become obsolete. Additional to this, some respondents went further and argued the Government should aim to put the maximum pot size value at or just under the breakeven point, as this will remove schemes unprofitable pots.

Mercer:

We believe that the maximum limit for small pots should be set above the proposed amount of £1,000 and propose that it should be set at a higher level, closer to £5,000. A worker earning £19,000 p.a. would likely amass £1,000 in just a year, assuming statutory minimum pension contributions at 8% of Qualifying Earnings. Setting the maximum limit at £1,000 therefore does too little to stem the proliferation of small pots.

41. In contrast to this, there was a proportion of respondents who argued the maximum limit of £1,000 was too high. Given the average size of a small pot referred to in the consultation was £350, responses suggested a phased introduction, starting at a level of no more than £500 would be more appropriate. This is because a value of £500 will still sweep up the majority of small pots and would have a smaller impact on the market initially; some respondents considered that starting at £1,000 may have a detrimental impact on some providers which would challenge their financial sustainability.

Society of Pension Professionals (SPP):

Of the options initially presented, we believe the lowest option is the best one, and as per our initial consultation response, a cohort of our members believes that £1,000 is too high (noting the DWP has stated that the average value of a pot smaller than £1,000 is approximately £350), and therefore we would better support a value of c£500 as a starting point, with this being statutory reviewed periodically. It may allow the industry to embed the new model effectively before it increases the threshold and volume of members impacted.

42. Whilst responses to this question did not completely agree that £1,000 was the correct starting point, there was a strong proportion of responses who acknowledged the value selected strikes the right balance for both schemes and importantly members.

Further, respondents raised two questions the consultation did not address:

- where the value is below the limit at the time of point when it is assessed as eligible, but is above at the time of transfer due to investment gains during the period between identification and transfer, will it still be eligible for consolidation

- what happens if a member has two eligible pots for consolidation with one provider and they do not adopt same scheme consolidation

Same scheme consolidation

Question 5: Do you agree with this proposal not to mandate schemes to undertake same scheme consolidation at this current time?

Summary of Responses

43. The consultation proposed not to mandate schemes to undertake same scheme consolidation, however, encouraged schemes to undertake this where possible, but proposed it would be an expectation that schemes who wished to act as a default consolidator would already undertake same scheme consolidation.

44. A large majority of responses agreed with the proposal not to mandate same-scheme consolidation at this current time, noting legislative and operational barriers. With respondents setting out how, they believed, that in some cases members have multiple pots with the same provider for good reason, including different features, guarantees or charges. Some respondents outlined the problem with mandating same scheme consolidation because schemes provide varying benefits and protections to different pots and therefore are unable to transfer them across without the member losing some benefits.

Phoenix Group:

Yes we agree with this approach. Same scheme consolidation can be complicated particularly in contract-based pensions and providers that provide different terms based on the employer providing the pension. Pilots and initiatives should be allowed to progress without mandation.

45. However, many respondents highlighted the benefits of mandating same scheme consolidation, given that it could reduce cost, risk, and increase customer service. This in turn could improve value for money, enable better guidance, and member centricity.

46. Others welcome the idea of allowing same-scheme consolidation without consent, however, acknowledge for this to be a whole market solution changes in legislation will need to occur. It was supported that same scheme consolidation reaps great benefits and should be mandated further down the line if there is no voluntary uptake across pension schemes.

47. As set out earlier, in response to the question regarding authorisation to act as a default consolidator, there was a significant number of responses who agreed that a scheme must already be offering same scheme consolidation to be able to act as a consolidator.

Nest:

We agree that there should be an expectation that any scheme applying for authorisation to act as a default consolidator would already undertake same scheme consolidation. We also agree that schemes should not be mandated to undertake same-scheme consolidation at this time.

Default Consolidator Framework

Question 6: As a whole, do you agree with the framework set out above for a default consolidator approach? Are there any areas that you think have not been considered, that need to form part of this framework?

48. The consultation outlined the proposed approach to address the small pots challenge, as part of this we set out a range of proposals to provide direction on key elements of the framework. As part of this, we were keen to understand from respondents whether there was overall support for this approach, or whether there were areas that would benefit from further exploration.

49. Overall, the framework set out in the consultation received broad support from respondents with the majority of respondents agreeing to the framework; although there were some elements that may benefit from further exploration as part of the industry delivery group.

Nest:

We believe this consultation sets the right direction of travel to resolve the issue of the proliferation of small pots in UK workplace DC schemes – an issue that requires resolution. We believe the idea of appointing a small number of schemes as default consolidators is in tune with the direction that the market should be taking, in the interests of members. Providing deferred pots are moved to ‘link up with’ an existing pot – active or deferred – within a consolidator, it should improve member experience, and we believe it will be welcomed by members.

50. One area that respondents raised was the 12-month period for a pot to be classified as deferred, with some considering that this period should be longer given the risk that members may go on long-term sick / parental leave and return to find their pot has been consolidated.

Pensions and Lifetime Savings Association (PLSA):

However, it is not uncommon for employers into cease pension contributions whilst a member of staff is on parental leave. Further, according to UK Government data, 6% of women take 53 weeks, or more, in maternity leave[footnote 5]. Under the proposed 12-month rule, an employee could return to work from such a period of leave to find that their pot has been consolidated.

51. While broadly respondents were supportive of the default consolidator approach, a small number of respondents continued to believe that the Government should reconsider their approach and opt with a pot follows member approach instead. Key arguments against the consolidator approach included that some considered the solution should focus on working closer to the pensions dashboards.

Association of British Insurers (ABI):

We do not agree with the framework set out for a default consolidator approach. The impact on competition, on savers and on the employer relationship requires further exploration, and needs to form part of this framework.

52. As set out above, some respondents, while agreeing with the framework broadly, considered there were some areas that would benefit from further consideration as the policy is developed further through the industry delivery group. Key areas that respondents considered should be explored further included:

- whether members can change their default consolidator after their pots have been consolidated

- are members able to move their pots to another scheme outside the consolidators once their small pot have been joined together

- how will the Government approach achieving a material reduction in the cost of transfers, to support the delivery of this approach

- what are the timeframes involved for schemes to transfer eligible pots out, and will this be done on a rolling basis or periodically

- how best to improve member communication to ensure that it is consistent across schemes, creating trust and encouraging active engagement

Equality impacts of the proposal

Question 7: Do you have any comments on the positive or negative impacts of a default consolidator approach on any protected groups, and how any negative effects could be mitigated?

Summary of responses

53. Under the Equality Act 2010, public bodies have a duty to give due regard to the needs of people with ‘protected characteristics. The Public Sector Equality Duty covers the protected characteristics of age; disability; gender reassignment; pregnancy and maternity; race; religion or belief; sex; sexual orientation; and marriage and civil partnership – in respect of eliminating unlawful discrimination only. In line with this we sought input from respondents around the impact of the default consolidator approach on protected groups.

54. Respondents recognised that deferred small pots are held by a higher proportion of low earners and multiple job holders, women, ethnic minorities and other under pensioned groups who are making minimal pension contributions and who change jobs more frequently due to insecurity of part-time work.

UNISON:

We think that the default consolidator approach will have particular benefit for those most likely to be in insecure or lower paying work, which particularly includes women, those with certain disabilities, and members of some ethnic groups.

55. Many respondents felt a default consolidator would provide a more substantive outcomes for members with deferred small pots, and result in a positive impact on many protected groups. Although some respondents felt the 12-month deferral period could negatively impact those employees who take paternity, maternity, or sick leave, as discussed in the response to question 6.

56. Respondents felt that consideration should be given to other protected groups including older members and those with disabilities, with particular attention to be paid to how industry would communicate changes to their pots to these groups. Some respondents felt the communication should be clearly demonstrated from the government to increase trust and confidence.

57. There was a strong consensus to identify best practice for communications, with multiple mentions of referring to the Financial Conduct Authority’s (FCA’s) Guidance for firms on the fair treatment of vulnerable customers[footnote 6] and the FCA’s Consumer Duty. Communications should be of appropriate format, clear and easily understandable to help members make decisions, especially to those protected groups who are less likely to be engaged due to lack of understanding of the process.

58. Concerns were also raised in relation to societal views or religious beliefs being considered when a pot is consolidated, including ensuring that members such as those within Sharia funds were not disadvantaged or excluded from any automated consolidation solution. Many responses highlighted the protection of members holding schemes with specific benefits, such as a protected pension age, a guaranteed annuity rate, or tax-free cash obligations.

Chapter 2: The Multiple Default Consolidator Framework and next steps

Introduction

59.Our consultation in July 2023, Ending the proliferation of deferred small pots[footnote 7], outlined the proposed approach to address the small pots challenge. In this consultation, we put forward a multiple default consolidator approach, from the responses we have received to this consultation, we have concluded that this is the most appropriate approach and will work to introduce it. While some respondents outlined that this was not their preferred approach, many of them agreed that if implemented correctly, it could effectively address the small pots challenge. As set out in the July consultation, we will establish an industry delivery group, working together with government, to work through the complex and challenges design and delivery questions that need to be addressed to ensure the successful implementation of this approach – that members can understand and trust.

60. This chapter sets out the government response to the consultation, to give further clarity on the outline of the multiple default consolidator framework, while also outlining areas which will be the key focus of the industry delivery group. The creation of the industry delivery group will provide government with time to further develop the policy and address some of the complex challenges that need to be overcome ahead of implementation. It is our ambition to legislate for this approach when Parliamentary time allows, building time for the required collaboration to ensure that the overall solution can support members achieving greater outcomes from their workplace pensions.

Central clearing house

61. Our consultation set out that a key obstacle of the multiple default consolidator approach would be the need for a central point to inform schemes of where to transfer a member’s deferred pot to. The consultation set out two options to overcome this barrier:

-

a central clearing house, which would be responsible for matching deferred pots and lead on communication with members and schemes

-

a central registry, which would act as a database which schemes could access to identify where a member’s chosen consolidator was

62. From the responses we received, it is clear that both approaches have their merits. However, there was agreement across the responses that a clearing house approach was more favourable.

63. The Government recognises there were potential benefits of opting for the central registry approach, with supporters of this approach considering that it could align more closely to the pensions dashboard, which could have made the implementation of this approach simpler and lower cost. Further, a central registry approach could remove the need for third party involvement as providers could access the information directly.

64. However, significant concerns were raised around the potential data and security risks of creating a central registry, alongside the potential competition risks that could occur because of giving schemes access to their competitor’s data.

65. Some respondents suggested that that we should look to rely on the pensions dashboard infrastructure, including the pensions finding service, instead of creating a new central infrastructure to support small pot consolidation. However, dashboard infrastructure, being member initiated, is significantly different to what would be required from a clearing house – where action is taken without requiring member involvement. The small pots delivery group will be tasked with considering the interactions between the pensions dashboard and the delivery of small pots solutions, we will look to involve individuals with extensive knowledge of the dashboards work to ensure greater collaboration.

66. On this basis, we have concluded that the clearing house approach is our preferred approach to support the delivery of the multiple default consolidator approach. It will enable for a central point, to support schemes and members through the consolidation process and can act independently in allocating members to a consolidator scheme in cases where a member does not make an active choice. It will reduce the burden on schemes who will be able to interact with a single organisation, and it could, dependent on role and remit, support greater communication and engagement with members.

67. Further to this, we have considered how the clearing house could better support an evolving pensions landscape. In part two of this document, we seek evidence on whether a move towards a lifetime provider model would be more beneficial for members. To do this, it is likely that there will need to be a significant change in how pension contributions are currently paid by the employer to the scheme. One option for this, as seen in Australia, would be to introduce a clearing house. This would give a wider, longer-term benefit of adopting a centralised clearing house approach for the consolidation of deferred small pots.

68. There are questions outstanding regarding the role, remit and design and funding of the central clearing house, this will be one of the key areas for the industry delivery group to focus on, where we will look to leverage industry expertise and take advantage of international evidence to design a central clearing house that will support the drive towards achieving a low-cost administration and transfer system which will be fundamental to the overall delivery of net benefits to members.

69. Further work with stakeholders will also be important to develop a better understanding of the potential transition costs to an automated solution. Whilst it is believed the costs of establishing an automated solution should be relatively small in comparison to the long-term benefits from automatically transferring pots (in terms of reduced administrative burden), at this stage the Government is unable to present a precise estimate of the transitional costs associated with developing a solution that facilitates this (including its design and implementation, and any transitional changes providers will need to make to their processes and infrastructure), as well as the ongoing costs of maintaining and updating it.

70. For comparison, Australia’s SuperStream reforms (which included a clearing house and gateway platform) took about 4 years to fully develop and had investment costs of an estimated A$1.5bn[footnote 8] (£930m)[footnote 9] over the 2012 to 2018 financial years. However, this was based on estimated A$900m (£560m) costs to providers and A$600m (£370m) costs to employers. These costs were borne by providers through levies. Due to differences in the pension systems, we do not anticipate there being significant costs to employers in the UK.

71. However, initially, Australia projected the costs of implementing the SuperStream reforms to be A$467m (£280m) over 7 years[footnote 10]. Of this, about 2/3s of the costs were expected to be IT-based, the majority of which were expected to be data and e-commerce standardisation. Any solution implemented in the UK is likely to build upon the data requirements in the regulations for the Pensions Dashboard – a similar large-scale reform which estimated an upfront cost to industry of £324m[footnote 11]. As some data standardisation will already be necessary for the Dashboard, we would expect £324m to represent the top-end of an estimate for the transition costs to industry of an automated transfer system as some of these costs will already have been incurred. If data standardisation is assumed to account for up to 2/3s of the costs, as in Australia, that would represent significant savings. We intend to assess these assumptions with the industry delivery group as we further develop the policy design/approach.

Conclusion – a clearing house

In conclusion, the government has decided to proceed with a clearing house approach to underpin and support the multiple default consolidator. The industry delivery group will be tasked to carefully considered the role, remit, and design of the clearing house as a priority area.

Allocating a member to a consolidator who hasn’t made an active decision

72. A key feature of the multiple default consolidator approach is that it enables a member, where they wish to, the opportunity to make an active choice about which default consolidator they would like to use. However, we anticipate there will be a number of cases where a member does not make an active choice. The consultation proposed two approaches to deal with this:

- Option A: allocate all small pots between the providers who meet the criteria to be a consolidator at a level proportionate to their market share

- Option B: given the likelihood that a member will have a deferred pot already with a consolidator scheme, this scheme would be allocated as the members consolidator scheme. In cases where a member has pots with multiple schemes that are authorised consolidators their deferred pots pot could be allocated to the consolidator scheme that holds their largest deferred pot

73. The consultation acknowledged that both of these approaches had their limitations but sought views from respondents on which of these was most suitable or whether there was an alternative that was worth consideration.

74. As discussed in Chapter 1, option A received very limited support as an appropriate method to allocate members to a consolidator in the absence of member choice. With a key concern being that that it could create an uncompetitive default consolidator market.

75. While option B received greater levels of support, there were concerns raised about how this approach would work for members who didn’t have a pot with a consolidator previously. Despite this, option B still has some merit as an approach for allocating a member to a consolidator, this is due to members being more likely to make a connection to the scheme if they are consolidated into a scheme where they already have a pot, which could result in improved engagement. Alongside this, it should also reduce the number of transfers required (and therefore cost), as schemes authorised to act as a consolidator would have a greater probability of retaining their members with deferred pots.

76. Some respondents suggested approaches where either members would be allocated purely on a carousel approach, or where schemes would partner up with authorised consolidators and transfer eligible pots to the partnered consolidator when eligible. Both of these approaches would not enable a member to be consolidated into a previous pot, creating unnecessary pots and also not taking advantages of a pre-existing relationship where possible.

77. We agree with respondents that a key aim when allocating members to a consolidator should be to consolidate them into an existing pot, where possible, to continue the relationship between member and scheme and reducing cost. However, we accept that there needs to be an alternative approach for those that do not have a pot with an authorised consolidator, therefore, it would seem sensible that in those instances, a member should be allocated a scheme based on a carousel approach.

Conclusion – allocation of members to a default consolidator

We will proceed with an amended option B approach, this will in the first instance look to consolidate members into a scheme where they already have a pot. If they have multiple pots with different consolidators, they will be allocated to the scheme which holds their largest pot.

In cases where a member does not have a pot with an authorised consolidator, we will look to allocate members to an authorised consolidator based on a carousel approach. The carousel approach will divide pots at an equal proportion, between the authorised consolidators.

Authorisation to act as a consolidator

78. Our July consultation, set out that in order to deliver an effective multiple default consolidator approach we would need a proportionate default consolidator regime which will enable the relevant regulators to authorise a small number of schemes to undertake this role – consistent with our objectives to move towards a more consolidated workplace pensions market.

79. As part of this, we set out that schemes, would be required to apply for authorisation, and alongside this we would consider with the FCA a similar authorisation framework to ensure appropriate parity for contract-based schemes that wished to act in the space. To clarify, no schemes will be required to apply for authorisation to act as a default consolidator, only those schemes that wish to act as a consolidator would need to seek authorisation. This proposal received broad support from respondents, with the majority agreeing that authorisation to act as a consolidator would be vital in ensuring that members were consolidated into schemes that offered the greatest levels of value for money.

80. Alongside this, the suggestion that to be a consolidator you must already offer same scheme consolidation received broad support from respondents, with many agreeing that this is a vital component of what a consolidator scheme must be able to deliver. We are aware of the difficulties faced by contract-based providers and we are carefully exploring legislative changes necessary to enable providers to transfer pension savers without consent, internally or to another provider, with appropriate protections built into the process.

81. We sought views on which essential conditions should form part of any authorisation criteria. There were a wide range of views provided in response to this, discussed in Chapter 1, but most supported the view was that it would be important to link authorisation of a consolidator to the Value for Money framework, ensuring that schemes must demonstrate value for their members to become a consolidator.

82. As such, we continue to believe that it will be necessary to develop an authorisation regime for schemes to be able to act as consolidators, but it will be important that we are able to create this in a proportionate way that encourages schemes to enter this market. There are some questions that require further consideration, with the benefit of insight from the industry delivery group, around what the overall authorisation process should look like, and how consolidators are supervised to ensure they continue to deliver good value for money for their members.

Conclusion – authorisation to act as a default consolidator

We will develop an authorisation and supervisory regime for trust-based schemes to act as consolidators and investigate options for a similar framework for contract-based schemes, working with the FCA, with the aim of ensuring parity of requirements and member experience.

We have considered the areas that respondents suggested as suitable condition to form part of the authorisation criteria, and we believe that a scheme will need to demonstrate the following:

- they must be an AE scheme and/or a qualifying scheme for AE

- must already undertake same scheme consolidation (acknowledging the need for legislative change for contract-based schemes to undertake this)

- would have to demonstrate good levels of VFM, which would be reviewed periodically

- they must themselves offer decumulation services, including a default decumulation offer to members

- high quality communication to affected members focused on driving improved engagement

- protection for members against flat fee charges, above the level of the current de minimis

- the scheme would have to have sufficient scale and/or hold a certain number of small pots, to be able to deliver value for consolidated members

Eligible pot criteria

83. In the July consultation, we set out the importance of striking the right balance for the eligibility of automatic consolidation solutions, between achieving high levels of consolidation, while also ensuring that member outcomes are improved. Our consultation set out that the starting point for eligible pots were that they must be within the automatic enrolment workplace pensions market within charge-capped default funds (including sharia compliant funds) but did not include pots with guarantees.

84. From the responses to our consultation, it was broadly agreed that this scope is correct as a starting point and would keep the solution sufficiently broad to benefit individuals. However, there was a question raised in relation to how to best deal with hybrid schemes, and schemes designed to tailor for specific beliefs, whose members are unlikely to want to be consolidated into a default consolidator. These are important areas to consider further, and we will look to explore these with the industry delivery group to ensure a suitable position is found.

85. Alongside this, the consultation set out two further proposed criteria for a pot to be eligible for automatic consolidation.

Pot limit

86. The first of these criteria was that the pot must be valued below £1,000. As seen in Chapter 1 of this document, respondents broadly agreed that £1,000 was a sensible limit for automatic consolidation. However, some respondents still considered that setting the limit at a lower level would be more appropriate, arguing that the average pot size referenced in our consultation was £350. While we understand this argument, it is important to consider the impact more widely on members if we reduced the maximum value for consolidation. For example, based on previous DWP data gathering exercises, we estimate that if the limit was set at £500, this would likely reduce the number of eligible pots for consolidation by almost a third, from 12m to approximately 8.5m.

87. Furthermore, it would take approximately only 5 months (22 weeks) for a full-time employee on National Living Wage making minimum contributions to reach this limit[footnote 12]. According to DWP analysis of HMRC data[footnote 13], just under half (48%) of the 4.3m instances of people stopping contributing to their pension in 21/22 had been after contribution spells of less than a year. Of which, the majority (68%) were after contribution spells of less than six months.

88. We strongly believe that reducing the maximum pot limit would have significant impacts on the overall benefits the multiple default consolidator approach would have on individuals and would run the risk of implementing a solution that creates higher costs than the benefits that members would receive. While we understand the arguments regarding the financial impact a £1,000 limit may have on schemes, it is also important to remember that these pots are unprofitable for schemes to administer, which in turn will have a negative impact on members within the scheme with larger pots, who are effectively cross subsidising these unprofitable pots.

89. On the other hand, as set out in Chapter 1, some respondents felt that the government should set a higher limit than £1,000; with concerns that the scheme economics of becoming a consolidator may not add up without a higher limit. Furthermore, there were suggestions that increasing the limit would also encourage greater member engagement, and support greater outcomes. While we appreciate these views, we must balance this against the potential impact starting with a higher pot limit may have on current pension schemes; alongside the increasing risk of member detriment as the pot value limit for automatic consolidation grows.

90. When considering this figure, we tried to strike the balance between not setting the limit too low and restricting consolidation or setting the limit too high and increasing the risk of detriment to members. From the responses received, we continue to believe that £1,000 currently does strike the correct balance. Therefore, we have concluded that the £1,000 pot limit suggested within our consultation remains a sensible starting point, when legislating for this, we also propose to include a regular statutory review requirement on government to ensure that this limit does not become obsolete.

91. Across the responses received to the consultation some queried at what point the value of pot was considered, whether this was at the 12-month period or at the point of transfer (considering potential for investment gains). Our initial view on this is that it would seem sensible to take the value at the 12-month point, and if the pot does increase in value (over £1,000) during the period of member communications / allocation of a consolidator, it should not become ineligible for automatic consolidation. On the contrary, pots that are above £1,000 at the 12-month point, but then fall below £1,000 subsequently, should not become eligible for automatic consolidation (unless, of course, it remains below £1,000 at the next 12-month point).

When does a pot become deferred

92. The second further criterion for a pot to be eligible for automatic consolidation was that it must not have received any contributions for a period of at least 12 months. The aim for this was that it would act as a sensible middle ground to target eligible pots, while trying to avoid including individuals who may, for a range of reasons, have temporarily stopped paying pension contributions, but remain with their existing employer and are likely to return to pension saving.

93. While we did not ask a specific question on this in our consultation, we received limited disagreement on this criterion. Although there were a few respondents who raised the interaction with the 12-month period and individuals taking parental leave / career breaks, suggesting that it would be sensible to increase this limit further to reduce the risk of including these individuals.

94. One of the key reasons driving the need to consolidate deferred small pots is the financial burden they put on schemes, who have to administers these pots at a loss, therefore, it is important that deferred pots are eligible to be transferred out as soon as possible. In relation to maternity leave, pension contributions continue during a period of maternity leave – except in the circumstance where an individual is not eligible for statutory maternity pay, as such, cases where contributions have ceased for an individual for more than 12 months, as a result on going on parental leave, are likely to be very limited. As part of the consolidation process, we intend that all members will be given the opportunity to opt-out of consolidation, so for those who know that they will return to their employer’s pension scheme, this will also act as a safety net.

95. Therefore, we have concluded that the 12-month period set out in our consultation remains an appropriate period for a pot to be classified as deferred.

Conclusion – eligible pot criteria

In conclusion, the Government has decided that the broad scope of the solution set out in the July consultation remains appropriate. Therefore, the criteria for pots to be eligible for automatic consolidation that Government intends to take forward will be:

- pots that were created since the introduction of AE (including contractual enrolment) and

- within automatic enrolment workplace pensions market within charge-capped default funds (including sharia compliant funds), excluding pots with guarantees

- pots must have had no active contributions made for a period of at least 12 months

- pots must be valued at equal to or less than £1,000. This threshold will be kept under review as we monitor impacts

Equality impacts

We have considered all responses on equality considerations and recognise small pots are disproportionately held by low earners and multiple job holders, women, ethnic minorities and other under pensioned groups. Therefore, we will continue to keep these sections of society in mind when developing policy and consider the impact of any potential solution on all those with protected characteristics in accordance with the public sector equality duty.

Industry delivery group

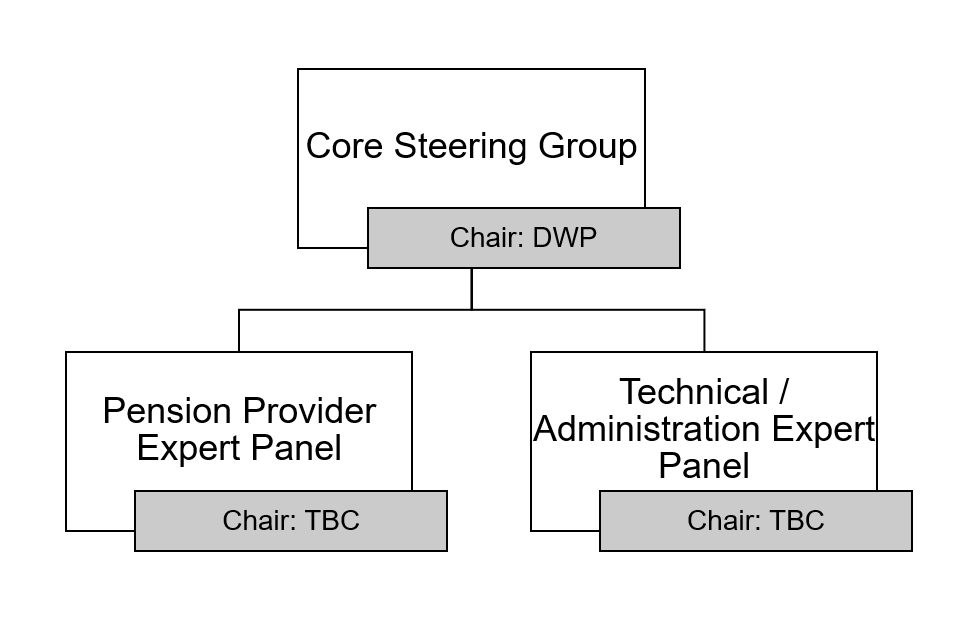

96. As set out in the July consultation, we will create an industry delivery group to support the Government to work through the complex issues that implementing a solution to the deferred small pots challenge presents. It will be key that industry is able to work closely with government to provide input and expertise to collaboratively develop and implement this solution in the most effective way. The group will need to remain focussed on ensuring the overall process minimises burdens on pensions schemes whilst balancing the need for simplicity, member security and speed.

97. The cross-sector delivery group will be tasked to examine specific elements of the framework, to support the development of a viable, efficient, and cost-effective automated consolidation process for ceding and receiving schemes. For this group to deliver on this complex task it will be important that the role and remit of this group is carefully defined, and the key question that need to be examined are agreed from the outset.

98. From the responses to the consultation the key areas that we consider will be vital for the delivery group to explore further are:

- the role and function of the proposed clearing house

- the design of a low-cost and efficient transfer system

- the authorisation and monitoring of default consolidator schemes

- the appropriate communication to members and member journeys

- the interactions and cross-over with the pensions dashboard programme

- the implementation approach for the default consolidator approach

99. We will aim to launch this group in early 2024, with the expectation that the group will provide an interim update to Ministers by Spring/Summer 2024, with proposals in late 2024 – for Ministers consideration and decisions.

100. We have provided a draft terms of reference for the industry delivery group at Annex B of this document, which sets out in more detail the role and remit of the group, the areas of focus and the proposed structure.

Part 2: Looking to the future: Great member security and rebalancing risk

About this call for evidence

Who this call for evidence is aimed at

The government welcomes input from:

- pension scheme providers

- trustees

- scheme managers

- members of workplace pension schemes

- employee representatives

- trades unions

- consumer groups

- employers and employee representative groups

- pension industry professionals

- members of the advisory community and any other interested stakeholders.

Purpose of the call for evidence

The purpose of this call for evidence is to seek evidence and views on a long-term vision for workplace pension saving in the UK. We want to explore whether a lifetime provider model would improve outcomes for savers, how we can grow the CDC market, and whether there are synergies between the two.

We also welcome views on possible alternative long-term visions we could set out, and what the evidence shows in regard to this.

Scope of call for evidence

This call for evidence applies to Great Britain. Occupational pensions are a devolved matter for Northern Ireland. We will be working closely with counterparts in Northern Ireland at the Department for Communities in relation to the matters set out in this call for evidence.

Duration of the call for evidence

Part 2 – the call for evidence, will run for 9 weeks, starting on 22 November 2023, and close on 24 January 2024. Please ensure your response reaches us by that date as any responses received after that date may not be taken into account.

How to respond to this call for evidence

Please send your call for evidence responses to:

Email: caxtonhouse.lifetimeprovidercallforevidence@dwp.gov.uk

Government response

We will publish the government response to this call for evidence on the GOV.UK website.

Feedback on the call for evidence process

We value your feedback on how well we seek evidence. If you have any comments on the process of this call for evidence (as opposed to comments about the issues which are the subject of the call for evidence), please address them to the DWP Consultation Co-ordinator: caxtonhouse.legislation@dwp.gov.uk

Freedom of information

The information you send us may need to be passed to colleagues within the DWP, published in a summary of responses received and referred to in the published government response.

All information contained in your response, including personal information, may be subject to publication or disclosure if requested under the Freedom of Information Act 2000. By providing personal information for the purposes of the public consultation exercise, it is understood that you consent to its disclosure and publication. If this is not the case, you should limit any personal information provided, or remove it completely. If you want the information in your response to the consultation to be kept 5 confidential, you should explain why as part of your response, although we cannot guarantee to do this.

To find out more about the general principles of Freedom of Information and how it is applied within DWP, please contact the Central Freedom of Information team: freedom-of-information-request@dwp.gov.uk

The Central Freedom of Information team cannot advise on a specific call for evidence exercise, only on Freedom of Information issues. Read more information about Freedom of Information Act.

Introduction

101. In part two of this document, we set out a long-term vision for pension saving in the UK. This model attempts to balance security for members who choose not to, or are unable to, engage, while facilitating choice for those who can and do. We want to ensure there is a greater balance of risk across the system and that savers do not individually bear unreasonable levels of risk for managing a retirement pot they may not fully understand.

102. We believe automatic consolidation of deferred small pots is the right starting point for a conversation on whether a lifetime provider model could bring wider benefits to savers and to the market. We are also making good progress developing CDC schemes, with a broader ambition to grow the CDC market so more savers can benefit, and we want to understand how these two approaches could work together.

The consultation response set out in part one of this document outlines our intended direction towards a defined contribution (DC) market with a small number of schemes, a subset of which act as authorised default consolidators of eligible deferred small pots. This approach will reduce the financial burden on pension providers by removing their most unprofitable pots, enabling them to provide greater value for money to their members.

The generation of multiple pension pots, of any size, under the existing AE framework leaves individuals with multiple risks to manage. Firstly, the risk of managing multiple pots in and of itself. Secondly, timing their investment risk appetite to avoid volatility approaching retirement. Finally, the risk that the arrangement offered by their scheme does not meet their needs, given it is chosen by their employer with little to no input from them. This is combined with the difficulties individuals have managing longevity risk, navigating, and providing for themselves across their whole retirement.

We want to build on the reforms already announced, including the multiple default consolidator solution for small pots, the Value for Money Framework, the development of Collective Defined Contribution Schemes, and Pensions Dashboards to deliver security for members in later life while continuing to use defaults to harness power of inertia that has already ensured millions more people are saving for retirement.

The case for a lifetime provider model

103. The original concept of a workplace pension was based on a model where an individual had a job for life. In return for staying with that employer, they were compensated with a generous defined benefit pension at retirement that would be paid for the remainder of the person’s life.

104. Greater rights for workers, the expansion of the workforce, and the emergence of non-pecuniary benefits has meant this model no longer functions in the same way. Employees are moving jobs more often, sometimes working in multiple jobs at the same time, and the paternalistic relationship many employers have with their employees is changing.

105. The current automatic enrolment system creates multiple pots for savers due to this job mobility, averaging at 10 pots across an individual’s working life[footnote 14]. Already, over 12 million deferred pots under £1,000 have been created[footnote 15]. Given all of this, we think there is a case for changing the relationship between the employer and employee, ensuring that employers are still required to contribute to a pension for their employee, but redesigning the system so that employees have more agency and control over their own pension.

106. A key element of the success of the AE framework is the use of defaults, which reduces the need for, and likelihood of, engagement. It harnesses the power of inertia. Despite this, there are key points where individuals do need to engage. There are several initiatives seeking to drive engagement, but it remains low. The recent Financial Lives Survey showed[footnote 16]:

- only 25% of people contributing to a DC pension were highly engaged with their pension

- nearly half (47%) of people contributing to a DC pension have not reviewed how much its worth in the last 12 months.

107. Building up multiple pots makes it difficult for individuals to understand the totality of their pensions savings and increases barriers to engagement, such as multiple online logins and passwords, and benefit statements. It also increases the likelihood that savers will lose valuable savings by forgetting or losing track of previous pots they have accrued (the PPI estimate[footnote 17] £26.6bn may be currently lost).

108. It can also increase the risk of cashing out perceived small amounts of pension savings; over 80% of pension pots worth less than £10,000 were cashed out when accessed compared to around 10% of pots worth £50,000[footnote 18] or more.

109. Multiple pots also make eventual decumulation decisions more complex and difficult to action with the need to speak to multiple providers and interpret their different sets of scheme rules and administration processes[footnote 19]. This could cost savers money as their accumulation product may not offer a full range of products to access their funds, and they could be charged to transfer out.

110. The existence of multiple pots also creates inefficiencies in the system, and we want to understand how we can support schemes to invest in productive finance assets that have the ability to deliver higher returns for savers. Multiple pots impact on a scheme’s ability to maximise the investment possibilities of an individual’s savings as individuals may be more likely to request to transfer their pots with the aim of consolidating at any point. Although switching rates are currently very low, where people do switch workplace pensions, this is predominantly (72%) to have their pensions all in one place[footnote 20]. We want to explore whether a lifetime provider model could support wider investment in high growth assets.

111. Pensions dashboards will be a significant step forward in enabling individuals to tackle the challenge of multiple pots. Dashboards will help people track lost pots and see all their different pensions, including the state pension, in one place online.

112. The proposed default consolidator model for small pots will support consolidation of the stock of pots, initially below £1000 in value. As set out in part one of this document. this threshold will be regularly reviewed and potentially increased to cover pots of a larger value. This will get us closer to a solution by creating a subset of providers that will be capable of consolidating pots from other schemes, solving a significant proportion of the inefficiency of high relative pot maintenance costs. Nevertheless, we need to consider whether a system that relies on the creation and subsequent consolidation of pensions savings is the most efficient and effective for the savers it is set up for.