PM163010 - Profits and losses computed at partnership level

S849 Income Tax (Trading and Other Income) Act 2005, S1259 Corporation Tax Act 2009.

Where any of the members of a partnership are chargeable to Income Tax the partnership is required to compute the trade profits of any period of account using the Income Tax rules as they apply to individuals.

The computation is made as if the partnership were an individual resident in the UK. But if the partnership contains a non-resident individual, or a company, or another partnership, then additional computations may be required – see PM163030.

Capital allowances are claimed by the partnership and computed at the partnership level and are given as an expense in computing the amount of the partnership’s profits. Therefore, the profits allocated to each partner are the profits net of capital allowances. See PM163200 for further guidance.

Where a partnership is itself a partner in another partnership the income or loss from that separate partnership must be computed separately from its other sources of income and shown separately in the partnership statement. Other sources of income could include: -

- Trade Income

- Partnership Income from a different partnership

For example, Partnership B is a partner in Partnership A. Partnership A allocates profit to Partnership B. Partnership B allocates its own trade profit to its Partner C, and allocates part of the profit it itself received from Partnership A also to Partner C. Partnership B must provide two separate computations of the profit it allocates to Partner C, and show the separate sources under Partner C’s entries in the partnership statement.

When the reporting partnership receives 5 or more separate income sources from other partnerships the information can instead be submitted on the approved template below as a PDF attachment to the partnership return. This is temporary until such time that HMRC systems and third-party software has progressed digital solutions to facilitate providing this information to HMRC. The template can be found in the Partnerhsip manual at PM163015.

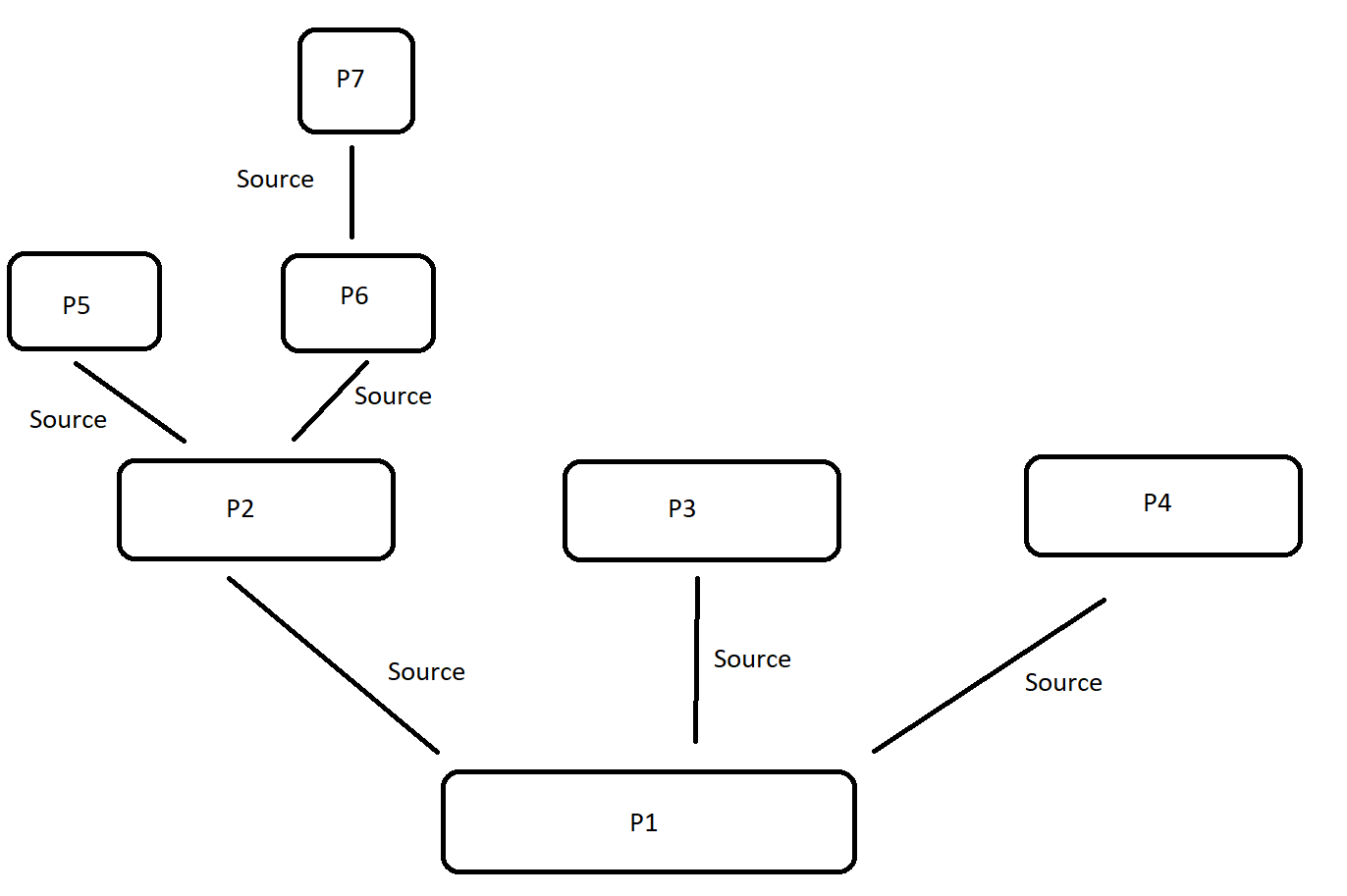

Example

Use this link to view the example

{kind=link}

In the above example, P1 is the reporting partnership. It receives profit share from P2, P3 and P4 which should all be calculated as separate income sources on the relevant bases.

P2 will need to provide calculations to P1 for the 3 separate income sources it receives from P7, P6 and P5 as well as P2’s own income source. P2 will therefore have to submit a partnership return and partnership statements for each separate income source on the relevant bases. P1 will consequently have to report the 6 separate income sources (P7, P6, P5, P2, P3 and P4) and its own, so 7 in total on the relevant bases. As P1 will report 5 or more separate income sources it qualifies to submit all its separate income sources on the template along with its partnership return.

If the reporting partnership has partner(s), indirect or not, that themselves are transparent partnerships for tax purposes, but they do not report in the UK, any income the reporting partnership receives from these non-UK reporting partnerships should also be treated as a separate source and returned as such. If the reporting partnership receives sources of income from partnerships without a UTR, they must provide a foreign Tax Identification Number (TIN) or local tax registration number (guidance can be found at IEIM402040.

If the partnership attempts to return the HMRC approved template and there are less than 5 partnership income sources, or the spreadsheet submitted to HMRC is not in the specified format, the return will be treated as incorrect, and may give rise to penalties and interest.