CFM96750 - Interest restriction: joint ventures: treatment when no elections apply: example 2: transparent JV

For visual illustration view Diagram showing X plc investing 50% in a joint venture, with profits and interest expenses shown for X plc and the JV

{kind=link}

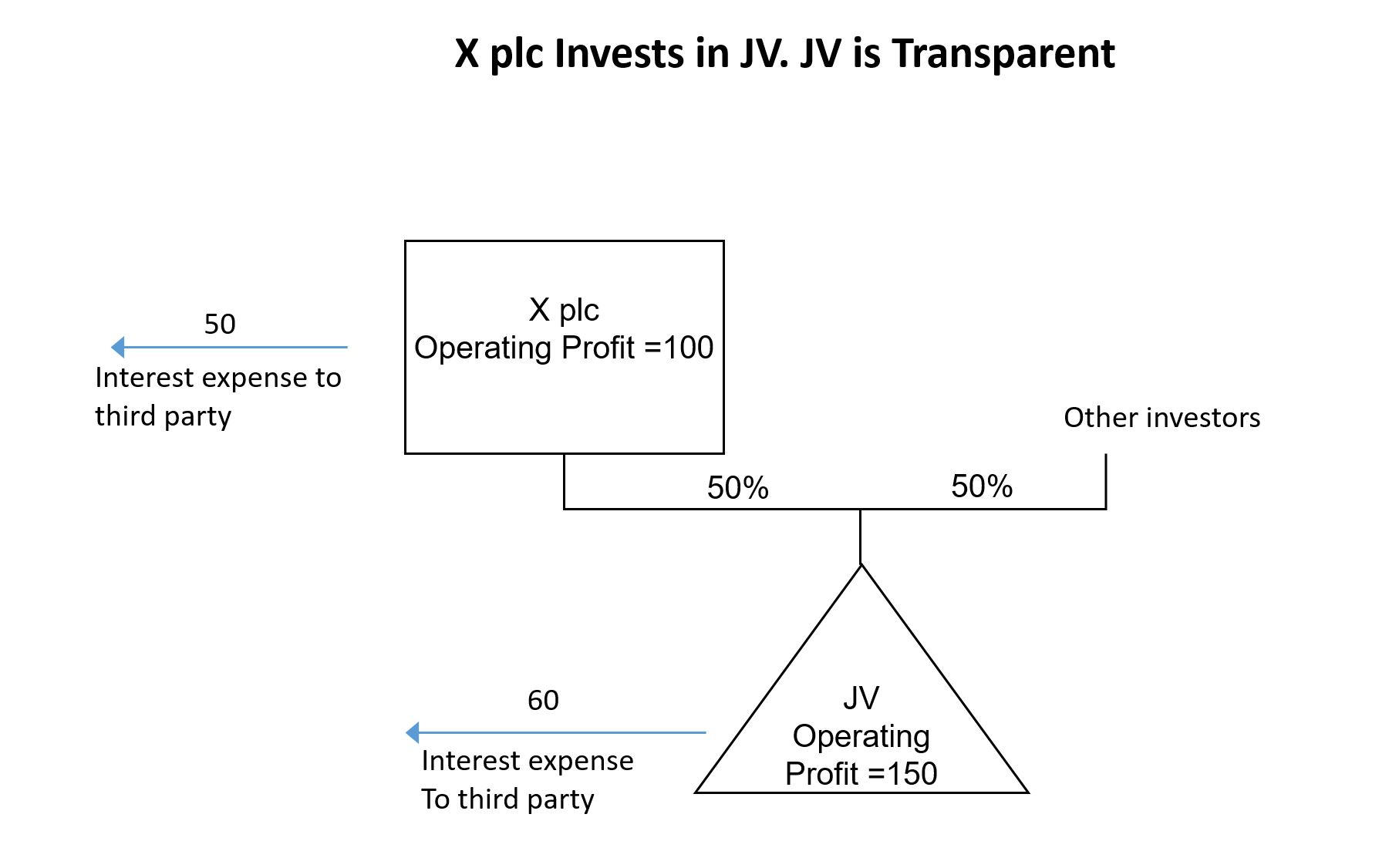

In this example we consider X plc, A worldwide group that has a 50% share of JV. X plc has operating profits of 100 and pays interest to a third party of 50. JV has operating profits of 150 and pays interest to a third party of 60. The JV in this example is transparent.

| Accounts | X plc | JV | X plc Group |

|---|---|---|---|

| Operating profit | 100 | 150 | 100 |

| 3rd party interest expense (QNGIE) | - 50 | - 60 | - 50 |

| Share of profits of JV | 0 | - | 45 |

| Profit Before Tax | 50 | 90 | 95 |

| Calculation of Group Ratio | X plc Group |

|---|---|

| Qualifying net group-interest expense - (A) | 50 |

| PBT | 95 |

| Add back interest expense | 50 |

| Group-EBITDA - (B) | 145 |

| Group Ratio ( A/B) | 34% |

| Interest allowance | X plc |

|---|---|

| Tax-EBITDA | 175 |

| X plc group ratio | 34% |

| Interest allowance | 60 |

| Net tax -interest expense | 80 |

| Less interest allowacnce | - 60 |

| Interest restriction | 20 |

X plc

The accounting is exactly the same as for example so the group ratio remains the same. It is 34%.

However looking at the taxable profits of the X plc group all figures from its share of JV are brought into the X plc's tax computation. This means that X plc recognises 30 of interest from JV and 75 of operating profits. Therefore X plc has net tax interest of 50 + 30. It also included tax EBITDA of 75 from JV meaning that the tax-EBITDA for the group is 175. This means that there is an interest allowance of 60 which creates an interest restriction of 20.

JV

JV is transparent and is not a taxable entity. Therefore the interest allowance and interest restriction do not apply to JV.