CFM96740 - Interest restriction: joint ventures: treatment when no elections apply: example 1: opaque JV

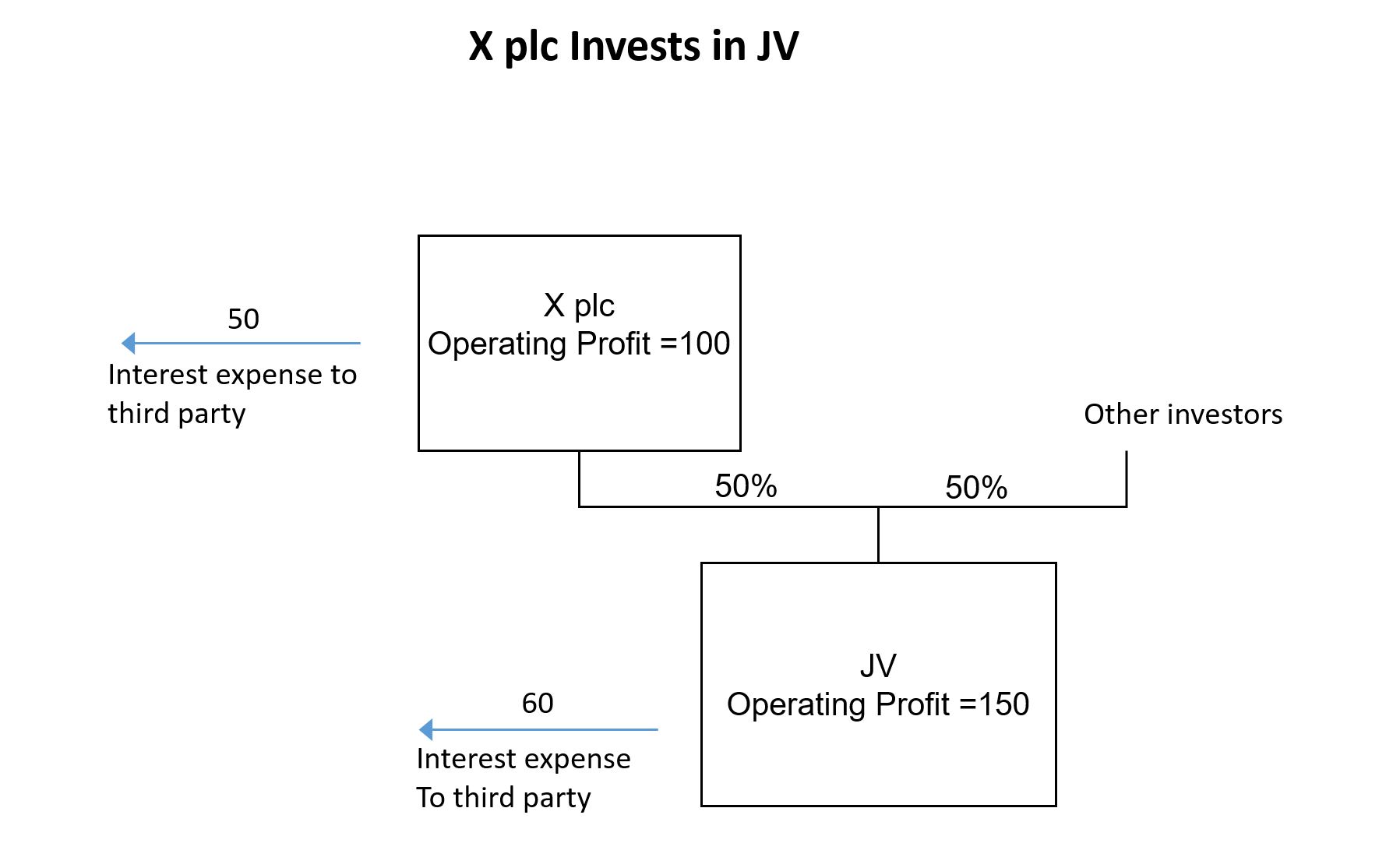

For visual illustration view diagram showing X plc investing in a joint venture alongside other investors

{kind=link}

The diagram shows X plc investing in a joint venture (JV). X plc has an operating profit of 100 and pays interest of 50 to a third party. X plc and other investors each hold a 50% interest in the JV. The JV has an operating profit of 150 and pays interest 60 to a third party.

In this example we consider X plc, A worldwide group that has a 50% share of JV.

X plc has operating profits of 100 and pays interest to a third party of 50. JV has operating profits of 150 and pays interest to a third party of 60.

The calculations for the X plc group (the results of X plc with the share of the profits from the JV) and the JV are as follows.

| Accounts | X plc | JV | X plc Group |

|---|---|---|---|

| Operating profit | 100 | 150 | 100 |

| Third party interst expenses (QNGIE) | - 50 | - 60 | - 50 |

| Shares of profits of JV | - | - | 45 |

| Profits Before Tax | 50 | 90 | 95 |

| Calculation of group ratio | X plc Group | JV |

|---|---|---|

| Qualifying net group-interest expenses - (A) | 50 | 60 |

| PBT | 95 | 90 |

| Add back interes expense | 50 | 60 |

| Group - EBITDA - ( B) | 145 | 150 |

| Group ratio - ( A/B) | 34% | 40% |

| Calculation of corporate interest restriction | X plc | JV |

|---|---|---|

| Tax - EBITDA | 100 | 150 |

| Group ratio | 34% | 40% |

| Interest allowance | 34 | 60 |

| Net tax interest expense | 50 | 60 |

| Less interest allowance | - 34 | - 60 |

| Interest restriction | 16 | 0 |

X plc

The X plc group has a qualifying net group-interest expense of 50. Its group-EBITDA is the group-EBITDA of X plc which is 100 and add to this the share of the profits of the JV which will feature in the consolidated accounts of X plc. This is 45 making the total Group EBITDA of 145. From this the group ratio of 34% is calculated.

Calculating the interest allowance this group ratio is applied to the tax-EBITDA of the X plc group. Tax-EBITDA is 100 because the 45 of profits from the JV is not taxed in X plc and the JV is not part of the group. This gives interest allowance of 34. The net tax-interest expense is assumed to be the same as the group-interest figure of 50 meaning that there is an interest restriction of 16.

JV

JV has qualifying net group interest expense of 60. Its group-EBITDA is 150. This creates a group ratio of 40%.

Calculating the interest capacity allows this 40% to be calculated against the tax-EBITDA. In this case the tax-EBITDA is assumed to be the same as the group-EBITDA and the net tax-interest expense is assumed to be the same as the qualifying net group interest expense of 60. This means that the interest allowance is 60 and, therefore, no interest restriction is applied to the JV. This is because the group ratio in the JV follows the interest profile of the JV.