Mortgage and landlord possession statistics: October to December 2024

Published 13 February 2025

Applies to England and Wales

© Crown copyright 2025

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/statistics/mortgage-and-landlord-possession-statistics-october-to-december-2024/mortgage-and-landlord-possession-statistics-october-to-december-2024

1. Main Points

This publication presents quarterly mortgage and landlord possession statistics up to October to December 2024. In general, we have compared figures to the same quarter in the previous year. Should users wish to compare against previous years, they can do so using the accompanying statistical tables. For technical detail, please refer to the accompanying supporting document. The documents published alongside this bulletin can be found here: Mortgage and landlord possession statistics - GOV.UK

| Mortgage claims, orders, warrants and repossessions increased | Compared to the same quarter in 2023 there were increases in mortgage possession claims from 4,385 to 6,080 (39%), orders from 2,697 to 4,178 (55%), warrants from 2,240 to 3,305 (48%) and repossessions by county court bailiffs from 595 to 957 (61%). |

| Landlord possession actions have all increased | When compared to the same quarter in 2023 there were increases in landlord possession claims from 23,374 to 24,010 (3%), orders from 17,994 to 18,416 (2%), warrants from 10,170 to 10,877 (7%) and repossessions from 6,664 to 7,020 (5%). |

| Mortgage possession claims have risen across most regions | Increases in landlord possession claims have been driven by an increase in London although this is offset slightly by falls in Wales, the North East, and the South West. Increases in mortgage possession claims have been recorded in all regions. Private landlord and mortgage claims remained concentrated in London. |

| Median timeliness for mortgage repossessions has continued to decrease. | The median average time from claim to mortgage repossession has decreased to 46.0 weeks, down from 50.7 weeks in the same period in 2023. |

| Median timeliness for landlord repossessions has increased. | The median average time from claim to landlord repossession has increased to 25.0 weeks, up from 23.6 weeks in the same period in 2023. |

A data visualisation tool has also been published that provides further breakdowns in a web-based application. The tool can be found here.

For feedback related to the content of this publication and visualisation tool, please contact us at CAJS@justice.gov.uk

2. Statistician’s Comment

Landlord possession actions (claims issued, orders, warrants, and repossessions) have all increased across 2024 compared to the previous calendar year. When compared to the same quarter in 2023, the median time for claims to orders has remained largely stable (increasing by less than a week). Claims to warrants have also remained largely stable with the median time taken decreasing by less than a week whilst the median time taken for claim to repossession has seen an increase of 1.4 weeks.

The number of mortgage possession actions have all risen compared to Q4 2023, whilst the median time taken from claims to orders reflect this trend, also rising slightly. In contrast, timeliness from claim to warrants and repossessions continues to fall this quarter compared with a year ago, as increased case volumes progress through the system.

3. Overview of Mortgage Possession

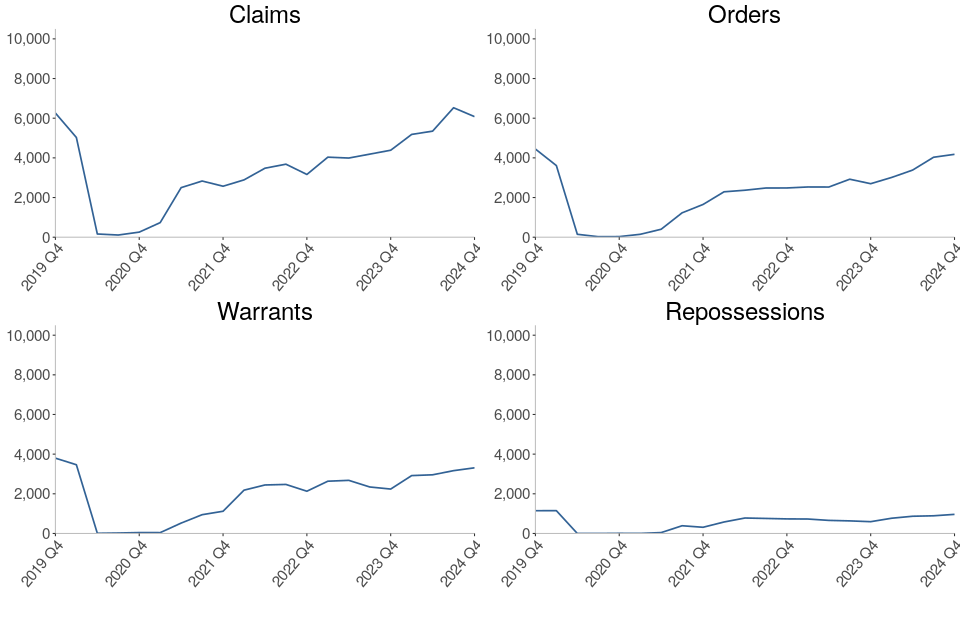

Mortgage possession actions: claims, orders, warrants and repossessions continue recent rises and are all currently above the previous year’s levels.

Compared to the same quarter in 2023, mortgage possession claims (6,080) are up 39%. Mortgage orders for possession (4,178) are up 55%, warrants issued (3,305) are up 48% and repossessions (957) are up 61%.

Figure 1: Mortgage possession actions in the county courts of England and Wales, October to December 2019 to October to December 2024 (Source: Table 1)

Mortgage possession claims have generally risen since Q2 2021 and continue to rise in the latest quarter. Claims, orders, warrants and repossession volumes are now 3%,6%, 13% and 17% below the Q4 2019 volume.

Mortgage possession claims fell from a peak of 26,419 in April to June 2009 (in the aftermath of the 2008 financial crash) before stabilising in 2015. In the most recent quarter, Q4 2024, there were 6,080 claims for possession, up 39% from the same quarter in 2023.

Orders and warrants for possession have followed a similar trend to mortgage claims. Compared to the same quarter in 2023, orders are up 55% to 4,178 and warrants are up 48% to 3,305 in Q4 2024.

Before the impact of Covid-19, the historical fall in the number of mortgage possession actions since 2008 has generally coincided with lower interest rates, a proactive approach from lenders in managing consumers in financial difficulties and other interventions, such as the Mortgage Rescue Scheme and the introduction of the Mortgage Pre-Action Protocol. The trend seen in recent years mirrors that seen in the proportion of owner-occupiers.

4. Mortgage Possession Action Timeliness

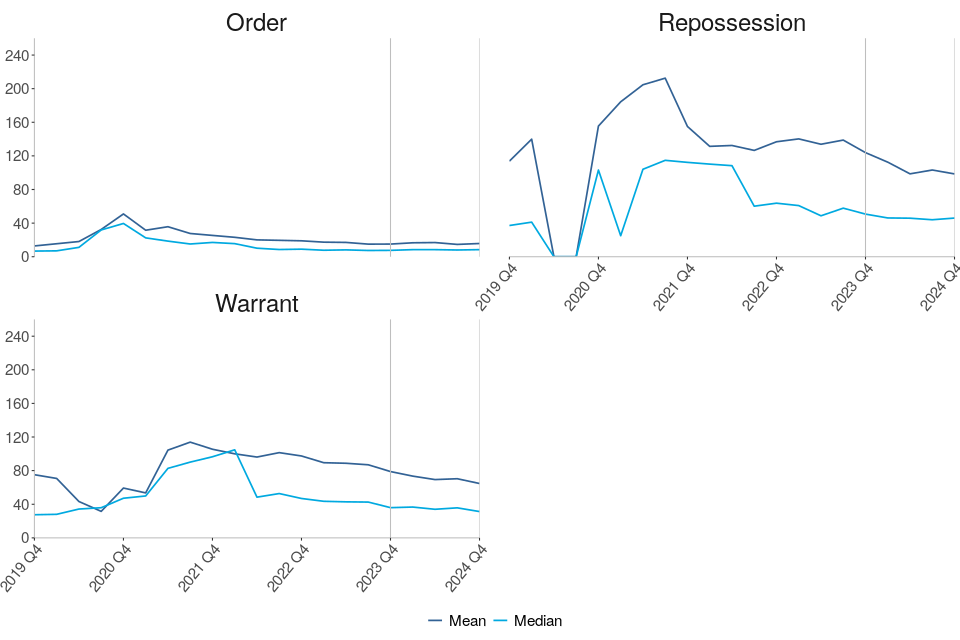

Claim to warrant and claim to repossession median timeliness have decreased compared to the same quarter last year, while median timeliness for claim to order has increased slightly over this period.

The median average time from claim to repossession has decreased to 46.0 weeks, down from 50.7 weeks in the same period in 2023.

Figure 2: Average timeliness of mortgage possession actions, October to December 2019 to October to December 2024 (Source: Table 3)

Number of weeks taken from initial mortgage claim to…

Median times taken to complete mortgage actions has increased slightly for claims to orders compared to the same quarter in 2023, whereas a larger decrease has been recorded for claims to warrants and claims to repossession over the same period. This is following a push from courts to reduce backlogs and ensure swift access to justice. This quarter;

-

Claims to order median timeliness is currently 8.4 weeks, up from 7.6 weeks in the same period in 2023.

-

Claims to warrant median timeliness has decreased to 31.3 weeks, down from 35.9 weeks in the same period in 2023.

-

Claims to repossession median timeliness has decreased to 46.0 weeks, down from 50.7 weeks in the same period in 2023.

The trend for mortgage possession timeliness is driven by outright orders, which make up around two thirds of all cases. In the most recent quarter, the median time taken from claim to repossession was 40.5 weeks for outright orders, and 182.9 weeks for suspended orders.

The above charts distinguish between the timeliness of possession claims at different stages of a case. Average time taken from claim to warrant or claim to repossession can fluctuate and is affected by various factors. For example, the final two charts take account of the amount of time between the court order being issued and the claimant, such as the mortgage lender, applying for a warrant of possession.

Median figures are generally considerably lower than mean figures, demonstrating that progression from claim to successive stages can be positively skewed by outlying cases.

5. Overview of Landlord Possession

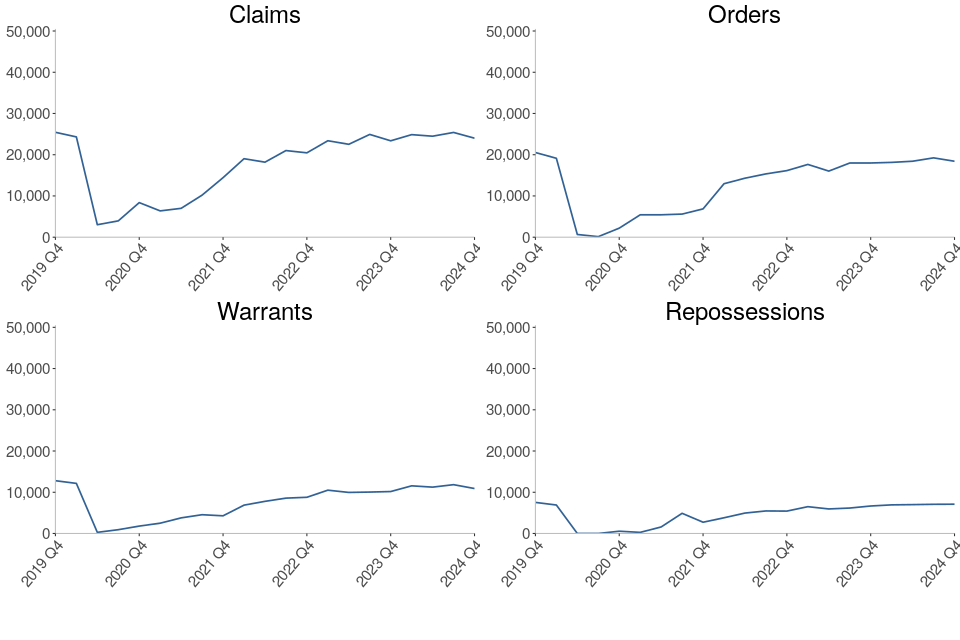

The numbers of landlord possession actions for all court stages have increased compared to the same quarter of last year.

Claims (24,010), orders for possession (18,416), warrants (10,877) and repossessions (7,020) have increased by 3%, 2%, 7% and 5% respectively compared to the same quarter in 2023.

Figure 3: Landlord possession actions in the county courts of England and Wales, October to December 2019 to October to December 2024 (Source: Table 4)

Landlord possession actions have shown a general increase since Q2 2021. Within the landlord possession actions, accelerated claims are up 3%, private landlord claims are down 2% and social landlord claims are up 7% compared to the same quarter in 2023.

In Q4 2024, 38% (9,085) of all landlord possession claims were social landlord claims, compared to 30% (7,084) private landlord claims and 33% (7,841) accelerated claims. This contrasts with pre-covid proportions when a majority of claims (around 60%) were social landlord claims.

The rise in claim and orders volumes is observed across most geographical regions. As in previous quarters, a concentration was seen in London, with 8,366 landlord claims and 5,870 landlord orders at London courts in Q4 2024, accounting for 35% and 32% of the respective totals. In London, there was an increase of 10% (from 7,632 in Q4 2023) for landlord claims and an increase of 7% for landlord orders (from 5,479 in Q4 2023).

The 7% increase in landlord warrants compared to Q4 2023, was driven by an increase in London. Meanwhile, the South East, North West, and Wales all saw decreases in the number of warrants over this period. The largest regional number (4,218) was again found in London, making up 39% of all landlord warrants. There was an increase of 22% for landlord warrants in London (from 3,447 in Q4 2023 to 4,218 in Q4 2024).

The Housing Loss Prevention Advice Service (HLPAS) provides advice to tenants and homeowners as soon as they are served with a written notice asking them to leave their home. Individuals who require the service do not need to meet legal aid financial eligibility rules as the service is not means tested but they are required to show evidence that they are at risk of losing their home. More information can be found here.

6. Landlord Possession Timeliness

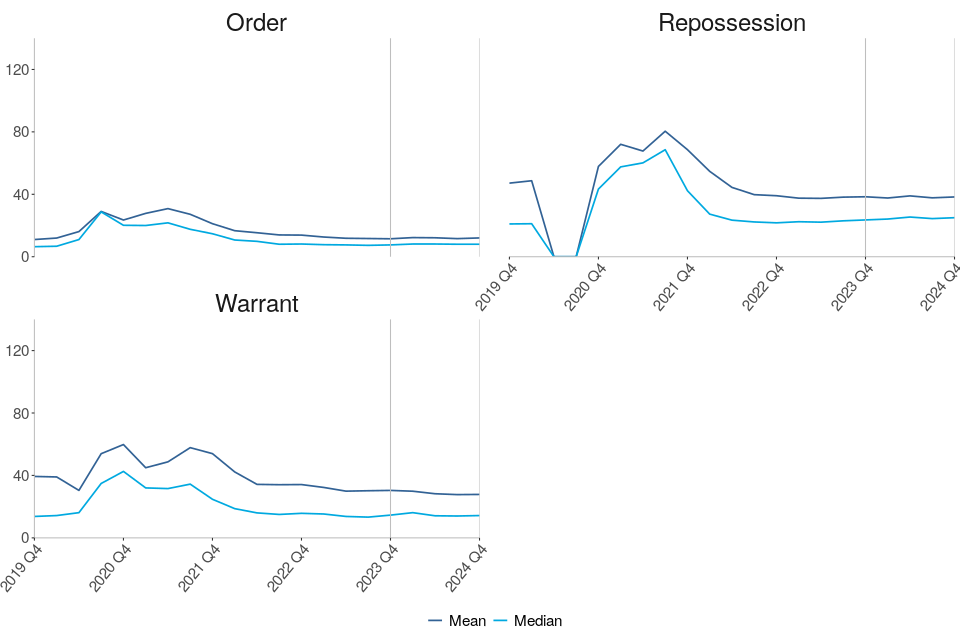

Median timeliness figures have increased for landlord orders and repossessions this quarter, with timeliness figures for warrants falling slightly.

The median average time from claim to repossession has increased to 25.0 weeks, up from 23.6 weeks in the same period of 2023.

Figure 4: Average timeliness of landlord possession actions, October to December 2019 to October to December 2024 (Source: Table 6)

Number of weeks taken from initial landlord claim to…

The median time taken to complete landlord actions increased for orders and repossessions this quarter.

-

Claims to order median timeliness is currently 8.0 weeks, up less than a week from the same period in 2023.

-

Claims to warrant median timeliness is currently 14.3 weeks, down from 14.6 weeks in the same period in 2023.

-

Claims to repossessions median timeliness has increased to 25.0 weeks, up from 23.6 weeks in the same period in 2023.

As shown in Figure 4, median figures are generally considerably lower than mean figures, demonstrating that progression from claim to successive stages can be positively skewed by outlying cases.

7. Regional Possession Claims

Since Q4 2022, the methodology used for calculating the rates of possession claims and repossessions had been modified to take into account the variation in proportions of tenure types in each local authority (LA) as measured by the 2021 census. The previous methodology (in place prior to Q4 2022) used total household figures as the denominator for all claims and repossessions rates. Since Q4 2022, this has now been modified to use household volumes by tenure[footnote 1]; mortgage, social and private landlord volumes for each local authority. For example, the rate of mortgage claims is now calculated as the number of mortgage claims divided by the number of households owned by a mortgage or loan in each LA. Similarly, rates for private and social landlord claims and repossessions have now been calculated separately[footnote 2] as a rate of households in each LA owned by a private or social landlord respectively. More information on this change is provided in the accompanying guide to this publication here.

Figure 5: Mortgage possession Claims per 100,000 households owned by a mortgage or loan, October to December 2024 (Source: map.csv; see supporting guide)

| Local Authority | Rate (per 100,000 households owned by a mortgage or loan) | Actual number |

|---|---|---|

| City of London | 588 | <10 |

| Westminster | 279 | 30 |

| Kensington and Chelsea | 279 | 22 |

London boroughs accounted for 7 of the 10 local authorities with the highest rate of mortgage claims. City of London, in the London region, had the highest rate of mortgage possession claims at 588 per 100,000 households owned by mortgage or loan, followed by Westminster (London region) and Kensington and Chelsea (London region); both with 279 claims per 100,000. The Isles of Scilly and the City of London have very small populations (ranked 309th and 308th out of 309 respectively for population size) therefore rates may be less robust.

2 local authorities had no mortgage possession claims during this period. Excluding this Fareham had the lowest rate of mortgage claims (17.6 per 100,000 households owned by a mortgage or loan)..

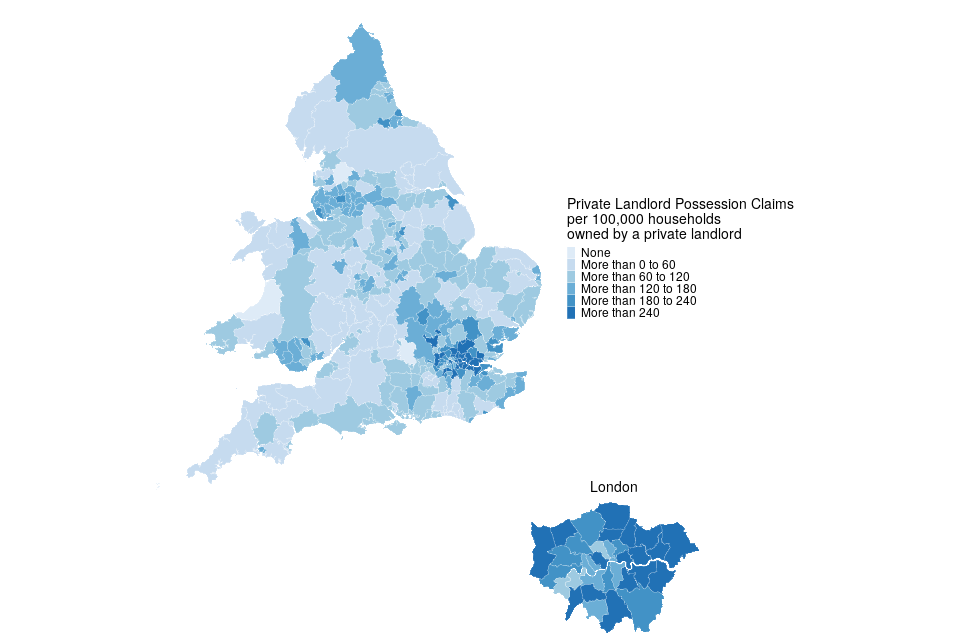

Figure 6: Private landlord possession Claims per 100,000 households owned by a private landlord, October to December 2024 (Source: map.csv; see supporting guide)

| Local Authority | Rate (per 100,000 households owned by a private landlord) | Actual number |

|---|---|---|

| Waltham Forest | 762 | 218 |

| Newham | 537 | 239 |

| Barking and Dagenham | 475 | 85 |

London boroughs accounted for 7 of the 10 local authorities with the highest rate of private landlord claims. Waltham Forest (London region) had the highest rate for private landlord claims (762 per 100,000 households owned by a private landlord), followed by Newham (London region) and Barking and Dagenham (London region) with 537 and 475 claims per 100,000 households owned by a private landlord respectively.

4 local authorities had no private landlord claims during this period. Excluding these, North Devon had the lowest rate of private landlord claims (11.3 per 100,000 households owned by a private landlord).

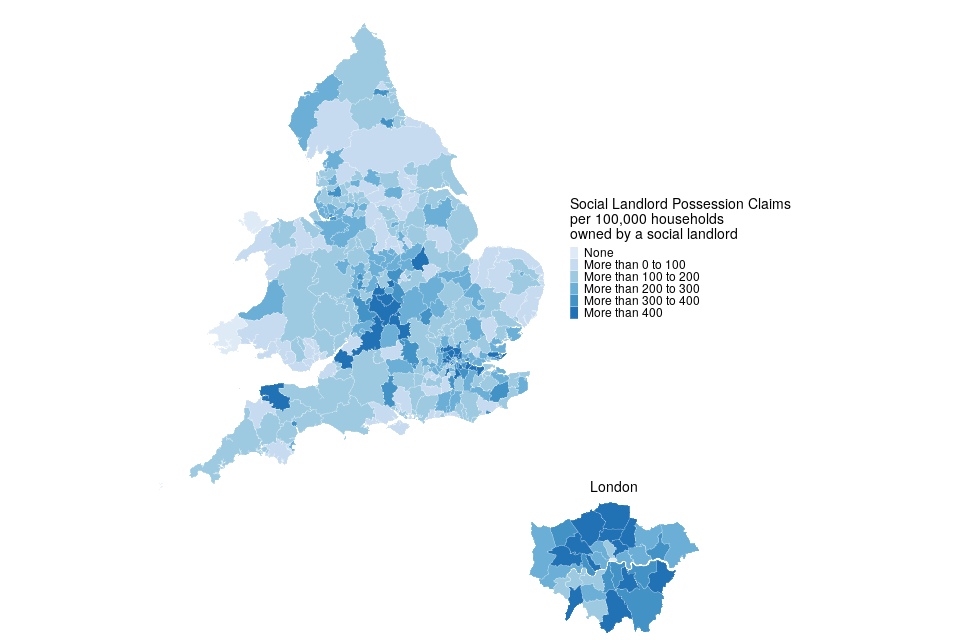

Figure 7: Social landlord possession Claims per 100,000 households owned by a social landlord, October to December 2024 (Source: map.csv; see supporting guide)

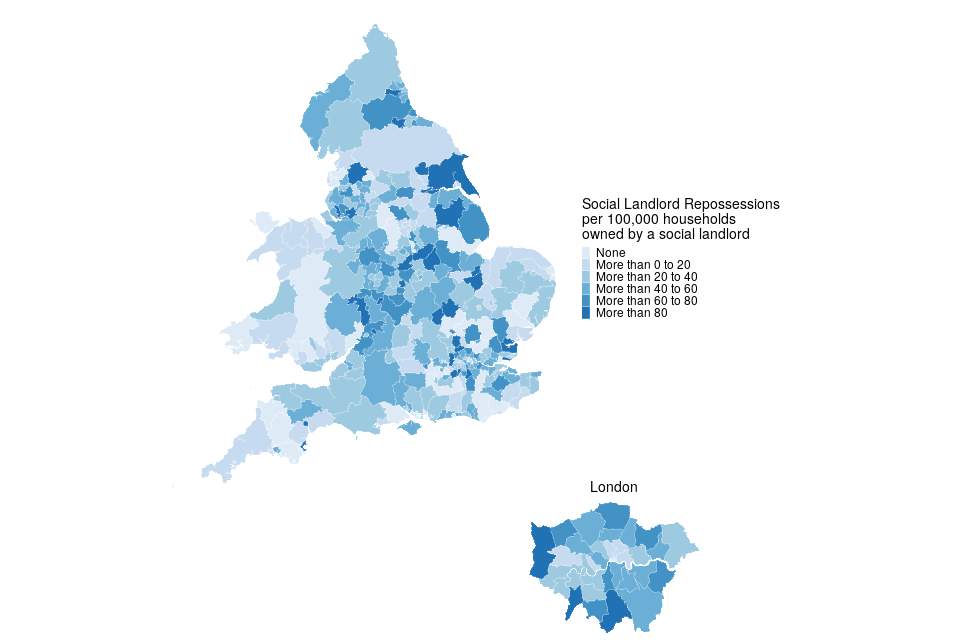

| Local Authority | Rate (per 100,000 households owned by a social landlord) | Actual number |

|---|---|---|

| Stratford-on-Avon | 759 | 60 |

| Kensington and Chelsea | 624 | 115 |

| Dartford | 618 | 39 |

London boroughs accounted for 4 of the 10 local authorities with the highest rate of social landlord claims. Stratford-on-Avon (West Midlands region) had the highest social landlord possession claim rate with 759 per 100,000 households owned by a social landlord. This was followed by Kensington and Chelsea (London region) and Dartford (South East region) with 624 and 618 per 100,000 households owned by a social landlord respectively.

4 local authorities had no social landlord claims during this period. Excluding these, Bridgend had the lowest rate of social landlord claims (11.5 per 100,000 households owned by a social landlord).

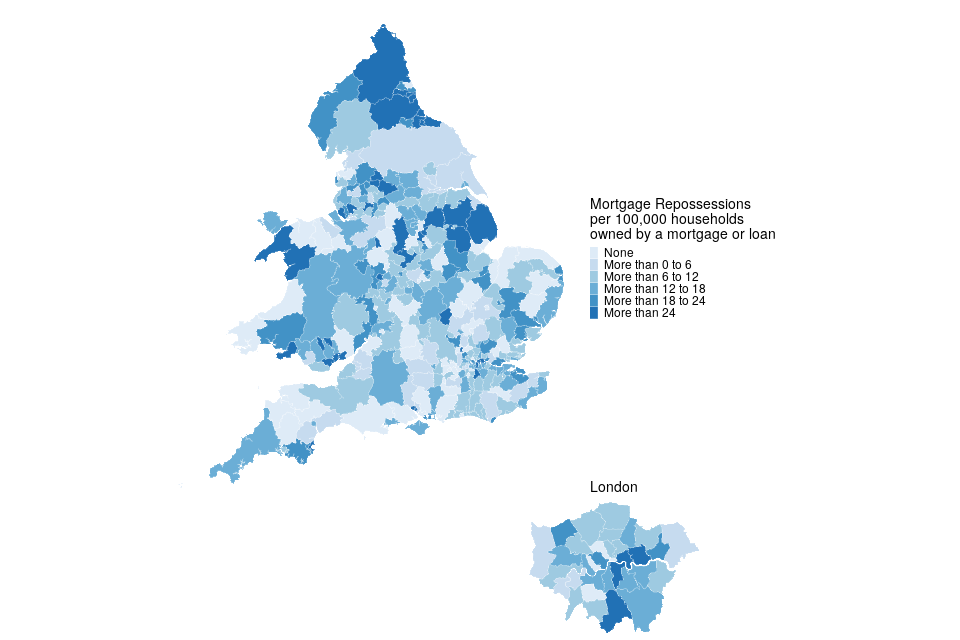

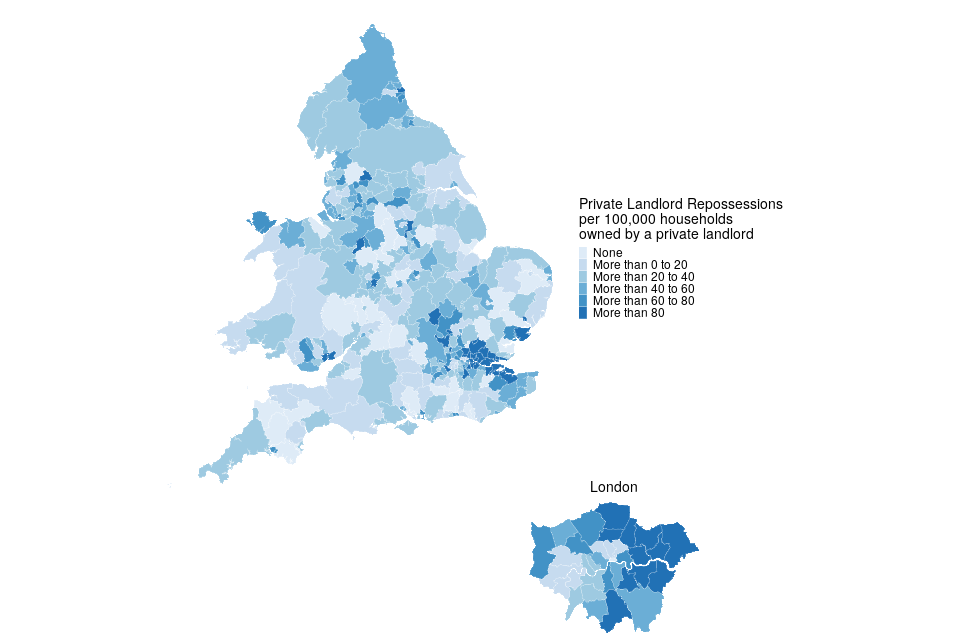

8. Regional Repossessions (by County Court Bailiffs)

Burnley had the highest overall rate of mortgage repossessions at 65 per 100,000 households owned by a mortgage or loan.

Private landlord repossessions were highest in Redbridge with 241 per 100,000 households owned by a private landlord.

Social landlord repossessions were highest in Croydon with 241 per 100,000 households owned by a social landlord.

Figure 8: Mortgage repossessions per 100,000 households owned by a mortgage or loan, October to December 2024 (Source: map.csv; see supporting guide)

| Local Authority | Rate (per 100,000 households owned by a mortgage or loan) | Actual number |

|---|---|---|

| Burnley | 65 | <10 |

| Bassetlaw | 57 | <10 |

| Watford | 49 | <10 |

North East local authorities account for 4 of the 10 boroughs with the highest rate of mortgage repossessions.

No repossessions by county court bailiffs were recorded during this period in 62 local authorities out of a total of 318.

Figure 9: Private landlord repossessions per 100,000 households owned by a private landlord, October to December 2024 (Source: map.csv; see supporting guide)

| Local Authority | Rate (per 100,000 households owned by a private landlord) | Actual number |

|---|---|---|

| Redbridge | 241 | 76 |

| Barking and Dagenham | 224 | 40 |

| Thurrock | 223 | 27 |

London local authorities account for 6 of the 10 boroughs with the highest rate of private landlord repossessions.

42 local authorities had no private landlord repossessions by county court bailiffs in Q4 2024.

Figure 10: Social landlord repossessions per 100,000 households owned by a social landlord, October to December 2024 (Source: map.csv; see supporting guide)

| Local Authority | Rate (per 100,000 households owned by a social landlord) | Actual number |

|---|---|---|

| Croydon | 241 | 66 |

| Fenland | 179 | 10 |

| Southend-on-Sea | 166 | 15 |

East Midlands, West Midlands, and East of England local authorities account for 2 each of the 10 boroughs with the highest rate of social landlord repossessions.

46 local authorities had no social landlord repossessions by county court bailiffs in Q4 2024.

As with claims, it should be noted that for some of these areas the rates are based on a small number of possessions.

9. Further information

The statistics in the latest quarter are provisional and revisions may be made when the next edition of this bulletin is published. If revisions are needed in subsequent quarters, these will be annotated in the tables.

9.1 Accompanying files

As well as this bulletin, the following products are published as part of this release:

-

A supporting guide providing further information on how the data is collected and processed, including a guide to the csv files, as well as legislation relevant to mortgage possessions and background information.

-

A set of overview tables (also available in accessible format), covering key sections of this bulletin.

-

CSV files of the map data and the possession action volumes by local authority and county court.

-

A data visualisation tool which provides a detailed view of the Mortgage and Landlord statistics. We welcome feedback on this tool to help improve it in later editions and to ensure it meets user needs.

These can be found in the relevant quarterly publication here.

9.2 National Statistics status

National Statistics are accredited official statistics (https://osr.statisticsauthority.gov.uk/accredited-official-statistics/) that meet the highest standards of trustworthiness, quality and public value.

Accredited official statistics are called National Statistics in the Statistics and Registration Service Act 2007. These accredited official statistics were independently reviewed by the Office for Statistics Regulation in September 2021. They comply with the standards of trustworthiness, quality and value in the Code of Practice for Statistics and should be labelled ‘accredited official statistics’.

It is the Ministry of Justice’s responsibility to maintain compliance with the standards expected for National Statistics. If we become concerned about whether these statistics are still meeting the appropriate standards, we will discuss any concerns with the Authority promptly. National Statistics status can be removed at any point when the highest standards are not maintained, and reinstated when the standards are restored. These statistics have been audited and re-accredited as National Statistics. The most recent compliance check completed by the Office of Statistics Regulation can be found here.

9.3 Future publications

Our statisticians regularly review the content of publications. Development of new and improved statistical outputs is usually dependent on reallocating existing resources. As part of our continual review and prioritisation, we welcome user feedback on existing outputs including content, breadth, frequency and methodology. Please send any comments you have on this publication including suggestions for further developments or reductions in content.

9.4 Contact

Press enquiries should be directed to the Ministry of Housing, Communities and Local Government press office:

email: newsdesk@communities.gov.uk

Other enquiries and feedback on these statistics should be directed to the Courts and People unit of the Ministry of Justice:

Rita Kumi-Ampofo - email: CAJS@justice.gov.uk

Next update: 15 May 2025

© Crown Copyright

Produced by the Ministry of Justice

-

Tenure - Office for National Statistics ons.gov.uk. ↩

-

Please note rates for private and social landlord possession claims and repossessions do not include accelerated claims. This is because accelerated claims are recorded onto the case management system at point of entry so do not specify the tenure type. ↩