FCDO IATI publishing guidance annex

Updated 19 April 2023

© Crown copyright 2023

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/fcdo-iati-guidelines/fcdo-iati-publishing-guidance-annex

Annex: How to build your publication

An important advantage of IATI is its flexibility. Programmes and underlying projects can be “modelled” in an IATI activity file in multiple ways. FCDO has developed some suggested models to make it easier to combine data from various publishers and create a full picture of how aid is delivered.

These models are not exhaustive, and you may need to combine elements from different models to best represent your activities. Use what is most appropriate for your organisation’s context.

Roles and responsibilities

The roles and responsibilities of different participating organisations need to be clearly defined. IATI recognises different roles for participating organisations: Funding, Accountable, Implementing and Extending.

When publishing to IATI, each organisation:

- only publishes the activities for which it is responsible, and therefore accountable for

- only mentions partner organisations with which it has a direct relationship. For example, if FCDO funds Organisation B who in turn funds Organisation C, Organisation C only refers to Organisation B as a funder, and not ‘up the chain’ to FCDO

Example models

The first step in structuring your data is to determine which model best fits your organisation:

- Project funding: if your organisation manages a project, spending or transferring funds to other organisations.

- Programme funding: if your organisation manages a large programme made up of smaller projects. Funds are generally managed at the “parent” programme level, while transfers or spending usually take place at the “child” project level. This model also works for basket or pooled funds and situations where co-funding is received directly at the child level.

- Partnerships: if your organisation works in a network or strategic alliance. Funding is generally received by a lead organisation and divided amongst partners on a programme level. Each member of the alliance or network then deploys its own activities.

- Core funding: if your organisation receives unearmarked funding, from which you fund one or more activities.

Once you have identified a model or combination of models that best represent your programme, you can begin creating your IATI data.

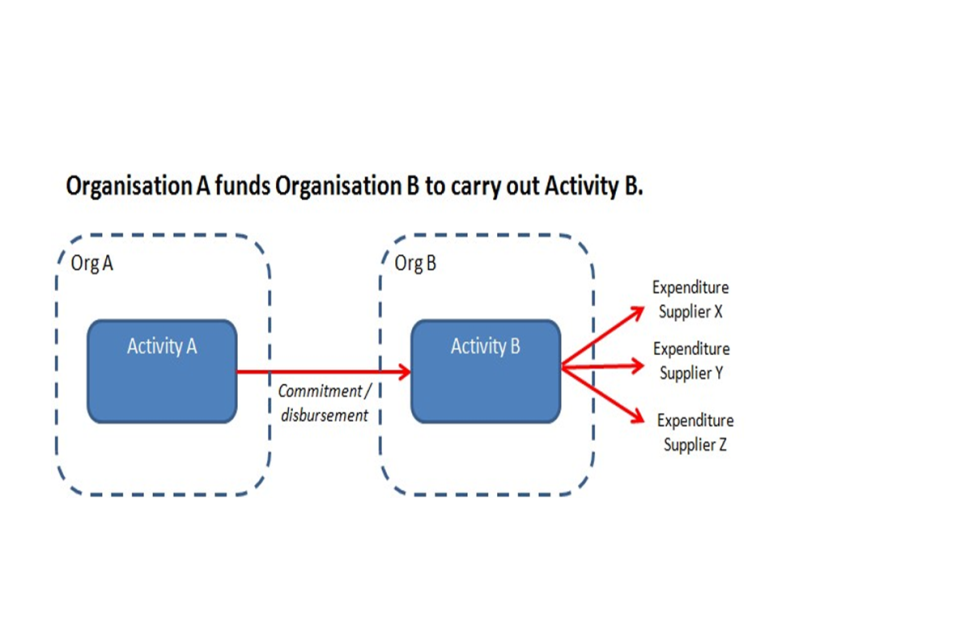

1) Project funding model

This model is for organisations that run an activity as a single project. Your organisation might implement the project yourselves or through organisations you fund.

Your organisation (Organisation B in the diagrams below) will publish a single IATI activity for the project, listing yourselves as accountable for the funding you receive and as an implementing organisation if applicable.

Project funding with a single implementing organisation

| Organisation A publishes: | Organisation B publishes: |

|---|---|

|

Activity A Funding: Organisation A Accountable: Organisation A Implementing: Organisation B Reference to Organisation B: Transactions (outgoing commitments/disbursements) with Receiver-org: Organisation B |

Activity B Funding: Organisation A Accountable: Organisation B Implementing: Organisation B Reference to Organisation A: Incoming commitment/funds transaction with Provider-org: Organisation A Provider-activity-id: id of Activity A |

Narrative: Organisations A and B both publish an IATI activity file.

Organisation A publishes Activity A (the funding activity)

For this activity Organisation A is the funding organisation and accountable organisation. Organisation B is the implementing organisation.

Organisation A refers to Organisation B through its transactions with receiver organisation B.

Organisation B publishes Activity B

For this activity Organisation A is the funding organisation. Organisation B is accountable (towards Organisation A) and implementing.

Organisation B refers to Organisation A through incoming commitment/fund transactions, referencing provider organisation A and Activity A’s IATI identifier as provider-activity-id.

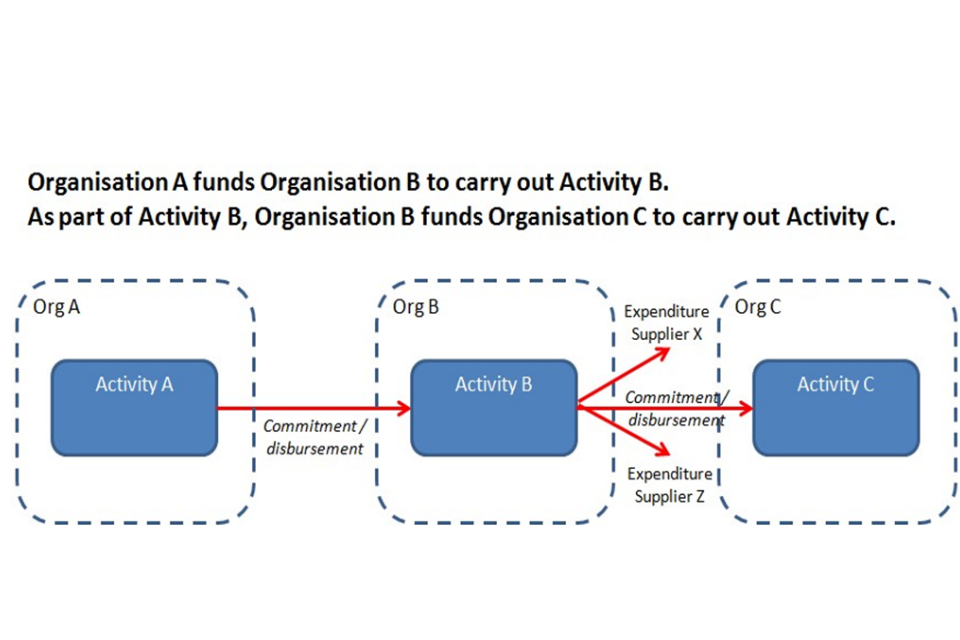

Project funding with multiple implementing organisations

| Organisation A publishes | Organisation B publishes | Organisation C publishes |

|---|---|---|

|

Activity A Funding: Organisation A Accountable: Organisation A Implementing: Organisation B Reference to Organisation B: Transactions (outgoing commitments/disbursements) with Receiver-org: Organisation B |

Activity B Funding: Organisation A Accountable: Organisation B Implementing: Organisation B, Organisation C Reference to Organisation A: Incoming commitment/funds transaction with Provider-org: Organisation A Provider-activity-id: id of Activity A Reference to Organisation C: Transactions (outgoing commitments/disbursements) with Receiver-org: Organisation C |

Activity C Funding: Organisation B Accountable: Organisation C Implementing: Organisation C Reference to Organisation B: Incoming commitment/funds transaction with Provider-org: Organisation B Provider-activity-id: id of Activity B |

Narrative: Organisations A, B and C each publish an IATI activity file.

Organisation A publishes Activity A.

For this activity Organisation A is the funding organisation and accountable organisation, and Organisation B is the implementing organisation.

Organisation A refers to Organisation B through its transactions, with receiver organisation B.

Organisation B publishes Activity B.

For this activity Organisation A is the funding organisation. Organisation B is accountable (towards Organisation A). Organisations B and C are implementing.

Organisation B refers to Organisation A through incoming commitment or incoming funds transactions, with provider organisation A and Activity A’s IATI identifier as provider-activity-id.

Organisation B refers to Organisation C through its transactions, with receiver organisation C.

Organisation C publishes Activity C.

For this activity Organisation B is the funding organisation, Organisation C is accountable (towards Organisation B), and Organisation C is implementing.

Organisation C refers to Organisation B through incoming commitment or incoming funds transactions, with provider organisation B and Activity B’s IATI identifier as provider-activity-id.

Note: if in this example Organisation B only disburses funds to Organisation C and does not work on implementation of the activity itself, Organisation B would mention only Organisation C as the implementing organisation.

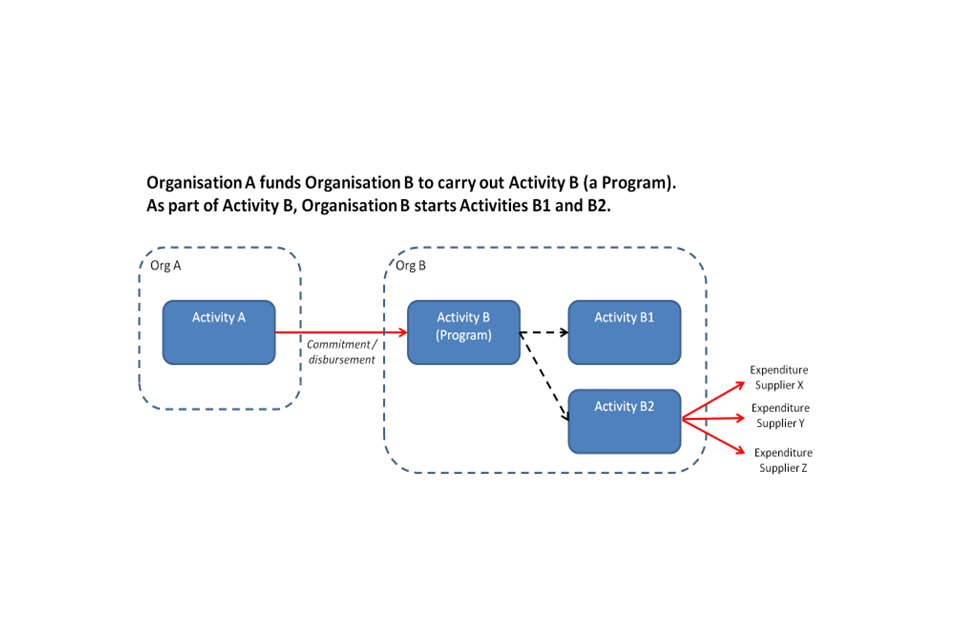

2) Programme funding model

This model is for a larger programme with underlying projects. Your organisation will publish multiple IATI activities in this instance – one for the overall programme and one for each of the projects. Incoming funds will be received for the programme, split between underlying projects, then spent or disbursed on to other organisations.

Programme funding with a single implementing organisation

| Organisation A publishes: | Organisation B publishes: |

|---|---|

|

Activity A Funding: Organisation A Accountable: Organisation A Implementing: Organisation B Reference to Organisation B: Transactions (outgoing commitments/disbursements) with Receiver-org: Organisation B |

Activity B (Hierarchy 1 = parent) Funding: Organisation A Accountable: Organisation B Implementing: Organisation B Reference to Organisation A: Incoming commitment/funds transaction with Provider-org: Organisation A Provider-activity-id: id of Activity A Activities B1 and B2 (Hierarchy 2 = child) Funding: Organisation B Accountable: Organisation B Implementing: Organisation B Reference to Activity B: Related activity: id of Activity B Type: 1 (Parent) Incoming commitment transaction Provider-org: Organisation B Provider-activity-id: id of Activity B |

Narrative: Organisations A and B both publish an IATI activity file.

Organisation A publishes Activity A (the funding activity).

For this activity Organisation A is the funding organisation and accountable organisation, and Organisation B is the implementing organisation.

Organisation A refers to Organisation B through its transactions, with receiver organisation B.

Organisation B publishes Activity B.

For this activity Organisation A is the funding organisation, Organisation B is accountable (towards Organisation A) and implementing.

Organisation B refers to Organisation A through incoming commitment or incoming fund transactions, with provider organisation A and Activity A’s IATI identifier as provider-activity-id.

Organisation B also publishes Activities B1 and B2.

For these activities Organisation B is the funding organisation (Organisation B is responsible for planning the activities). Organisation B is also accountable and implementing.

The relation between Activities B1 and B2 and Activity B is reported using the related-activity field. Activities B1 and B2 both have a related-activity Activity B, of the ‘Parent’ type[footnote 1].

The financial relation between Activity B and Activities B1 and B2 is represented through an incoming commitment transaction, with provider organisation B and Activity B’s IATI identifier.

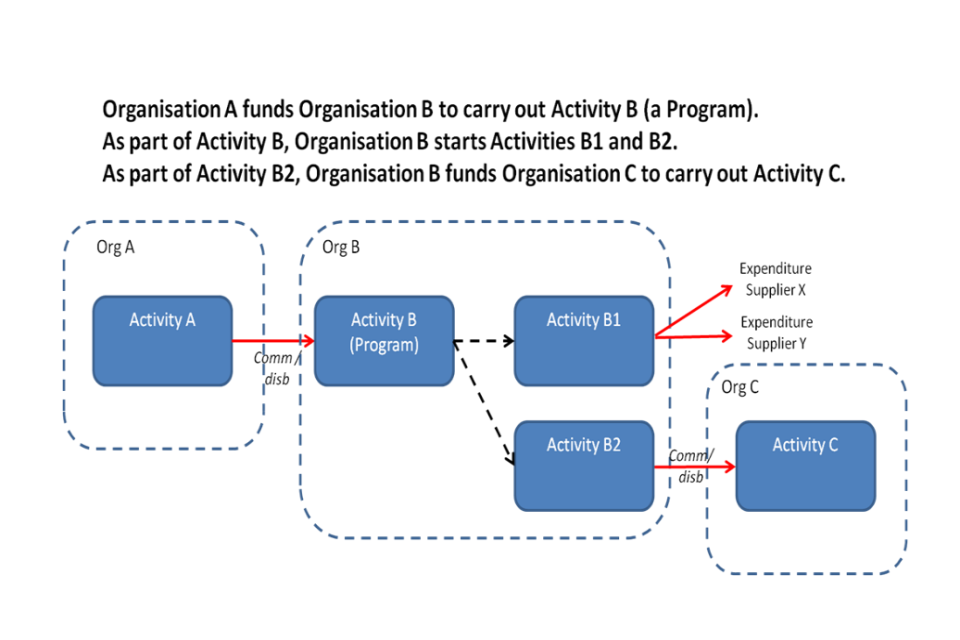

Programme funding with multiple implementing organisations

| Organisation A publishes: | Organisation B publishes: | Organisation C publishes: |

|---|---|---|

|

Activity A Funding: Organisation A Accountable: Organisation A Implementing: Organisation B Reference to Organisation B: Transactions (outgoing commitments/disbursements) with Receiver-org: Organisation B |

Activity B (Hierarchy 1 = parent) Funding: Organisation A Accountable: Organisation B Implementing: Organisation B Reference to Organisation A: Incoming commitment/funds transaction with Provider-org: Organisation A Provider-activity-id: id of Activity A Activity B1 (Hierarchy 2 = child) Funding: Organisation B Accountable: Organisation B Implementing: Organisation B Reference to Activity B: Related activity: id of Activity B Type: 1 (Parent) Incoming commitment transaction Provider-org: Organisation B Provider-activity-id: id of Activity B Activity B2 (Hierarchy 2 = child) Funding: Organisation B Accountable: Organisation B Implementing: Organisation C Reference to Activity B: Related activity: id of Activity B Type: 1 (Parent) Incoming commitment transaction Provider-org: Organisation B Provider-activity-id: id of Activity B Reference to Organisation C: Transactions (outgoing commitments/disbursements) with Receiver-org: Organisation C |

Activity C Funding: Organisation B Accountable: Organisation C Implementing: Organisation C Reference to Organisation B: Incoming commitment/funds transaction with Provider-org: Organisation B Provider-activity-id: id of Activity B2 |

Narrative: Organisations A, B and C each publish an IATI activity file.

Organisation A publishes Activity A (the funding activity)

For this activity Organisation A is the funding and accountable organisation, and Organisation B is implementing.

Organisation A refers to Organisation B through its transactions, with receiver organisation B.

Organisation B publishes Activity B.

For this activity Organisation A is the funding organisation, Organisation B is accountable (towards Organisation A) and implementing.

Organisation B refers to Organisation A through an incoming commitment or incoming fund transaction, with provider organisation A and Activity A’s IATI identifier as provider-activity-id.

Organisation B also publishes Activities B1 and B2.

For these activities Organisation B is the funding organisation (Organisation B is responsible for planning the activities). Organisation B is also accountable and implementing. For Activity B2, Organisations B and C are both implementing.

The relation between Activities B1 and B2 and Activity B is reported using the related-activity field. Activities B1 and B2 both have a related-activity Activity B, of the ‘Parent’ type[footnote 2]. The financial relation between Activity B and Activities B1 and B2 is represented through an incoming commitment transaction, with provider organisation B and Activity B’s IATI identifier.

Organisation B refers to Organisation C through its transactions under Activity B2, with receiver organisation C.

Organisation C publishes Activity C.

For this activity Organisation B is the funding organisation, Organisation C is accountable (towards Organisation B), and Organisation C is implementing.

Organisation C refers to Organisation B through an incoming commitment or incoming funds transaction, with provider organisation B and Activity B2’s IATI identifier as provider-activity-id.

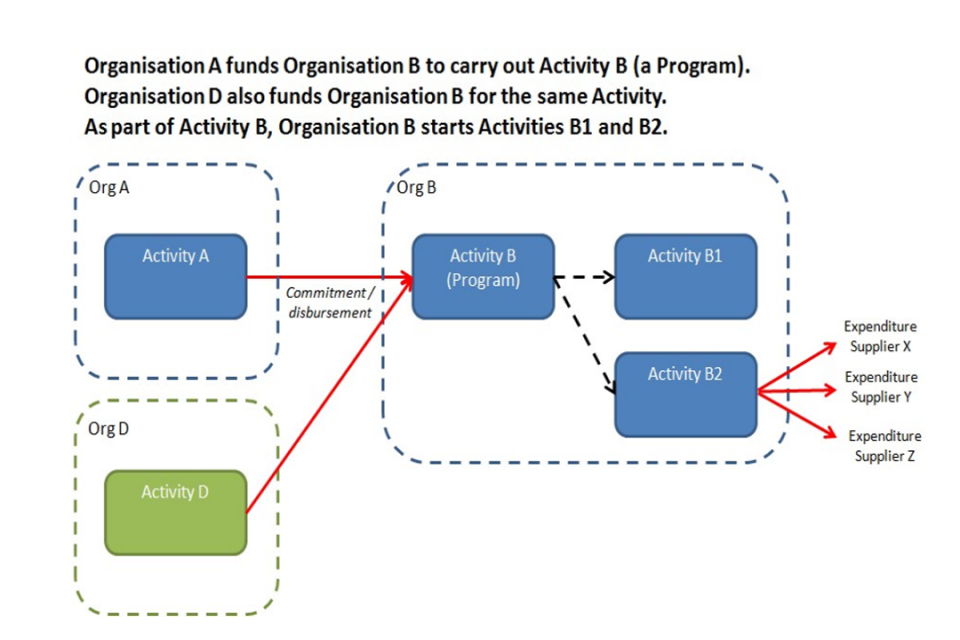

Programme funding with multiple donors

| Organisation A publishes: | Organisation B publishes: | Organisation D publishes: |

|---|---|---|

|

Activity A Funding: Organisation A Accountable: Organisation A Implementing: Organisation B Reference to Organisation B: Transactions (outgoing commitments/disbursements) with Receiver-org: Organisation B |

Activity B (Hierarchy 1 = parent) Funding: Organisation A, Organisation D Accountable: Organisation B Implementing: Organisation B Reference to Organisation A: Incoming commitment/funds transaction with Provider-org: Organisation A Provider-activity-id: id of Activity A Reference to Organisation D: Incoming commitment/funds transaction with Provider-org: Organisation D Provider-activity-id: id of Activity D Activities B1 and B2 (Hierarchy 2 = parent) Funding: Organisation B Accountable: Organisation B Implementing: Organisation B Reference to Activity B: Related activity: id of Activity B Type: 1 (Parent) Incoming commitment transaction Provider-org Organisation B Provider-activity-id: id of Activity B |

Activity D Funding: Organisation D Accountable: Organisation D Implementing: Organisation B Reference to Organisation B: Transactions (outgoing commitments/disbursements) with Receiver-org: Organisation B |

Narrative: Organisations A, D and B each publish an IATI activity file.

Organisation A publishes Activity A.

For this activity Organisation A is the funding organisation and accountable organisation, and Organisation B is the implementing organisation.

Organisation A refers to Organisation B through its transactions, with receiver organisation B.

In this case the second funder, Organisation D, publishes Activity D.

For this activity Organisation D is the funding organisation and the accountable organisation, and Organisation B is the implementing organisation.

Organisation D refers to Organisation B through its transactions, with receiver organisation B.

Organisation B publishes Activity B.

For this activity both Organisation A and Organisation D are the funding organisations. Organisation B is accountable (towards Organisations A and D) and implementing.

Organisation B refers to Organisation A through an incoming commitment or incoming funds transaction, with provider organisation A and Activity A’s IATI identifier as provider-activity-id.

Organisation B refers to Organisation D through an incoming commitment or incoming funds transaction, with provider organisation D and Activity D’s IATI identifier as provider-activity-id.

Organisation B also publishes Activities B1 and B2.

For these activities Organisation B is the funding organisation (Organisation B is responsible for planning the activities). Organisation B is also accountable and implementing.

The relation between Activities B1 and B2 and Activity B is reported using the related-activity field. Activities B1 and B2 both have a related-activity Activity B, of the ‘Parent’ type.

The financial relation between Activity B and Activities B1 and B2 is represented through an incoming commitment transaction, with provider organisation B and Activity B’s IATI identifier.

Programme funding with co-funding for a specific project

| Organisation A publishes: | Organisation B publishes: |

|---|---|

|

Activity A Funding: Organisation A Accountable: Organisation A Implementing: Organisation B Reference to Organisation B: Transactions (outgoing commitments/disbursements) with Receiver-org: Organisation B |

Activity B (Hierarchy 1 = parent) Funding: Organisation A Accountable: Organisation B Implementing: Organisation B Reference to Organisation A: Incoming commitment/funds transaction with Provider-org: Organisation A Provider-activity-id: id of Activity A Activity B1 (Hierarchy 2 = child) Funding: Organisation B, Organisation D Accountable: Organisation B Implementing: Organisation B Reference to Activity B: Related activity: id of Activity B Type: 1 (Parent) Incoming commitment transaction |

|

Organisation D publishes: Activity D Funding: Organisation D Accountable: Organisation D Implementing: Organisation B Reference to Organisation B: Transactions (outgoing commitments/disbursements) with Receiver-org: Organisation B |

Provider-org: Organisation B Provider-activity-id: id of Activity B Incoming commitment/funds transaction Provider-org: Organisation D Provider-activity-id: id of Activity D Activity B2 (Hierarchy 2 = child) Funding: Organisation B Accountable: Organisation B Implementing: Organisation B Reference to Activity B: Related activity: id of Activity B Type: 1 (Parent) Incoming commitment transaction Provider-org: Organisation B Provider-activity-id: id of Activity B |

Narrative: Organisations A, D and B each publish an IATI activity file.

Organisation A publishes Activity A.

For this activity Organisation A is the funding organisation and accountable organisation, and Organisation B is the implementing organisation.

Organisation A refers to Organisation B through its transactions, with receiver organisation B.

Organisation D publishes Activity D.

For this activity Organisation D is the funding organisation and accountable organisation, and Organisation B is the implementing organisation.

Organisation D refers to Organisation B through its transactions, with receiver organisation B.

Organisation B publishes Activity B.

For this activity Organisation A is the funding organisation. Organisation B is accountable (towards Organisation A) and implementing.

Organisation B refers to Organisation A through an incoming commitment or incoming funds transaction, with provider organisation A and Activity A’s IATI identifier as provider-activity-id.

Organisation B publishes Activity B1.

For this activity Organisation B and Organisation D are the funding organisations (Organisation B is responsible for planning the activities, Organisation D co-funds the activity). Organisation B is also accountable and implementing.

Organisation B refers to Organisation D through an incoming commitment or incoming funds transaction, with provider organisation D and Activity D’s IATI identifier as provider-activity-id.

Organisation B also publishes Activity B2.

For this activity Organisation B is the funding organisation (Organisation B is responsible for planning the activity). Organisation B is also accountable and implementing.

The relation between Activities B1 and B2 and Activity B is reported using the related-activity field. Activities B1 and B2 both have a related-activity Activity B, of the ‘Parent’ type.

The financial relation between Activity B and Activities B1 and B2, is represented through an incoming commitment transaction, with provider organisation B and Activity B’s IATI identifier.

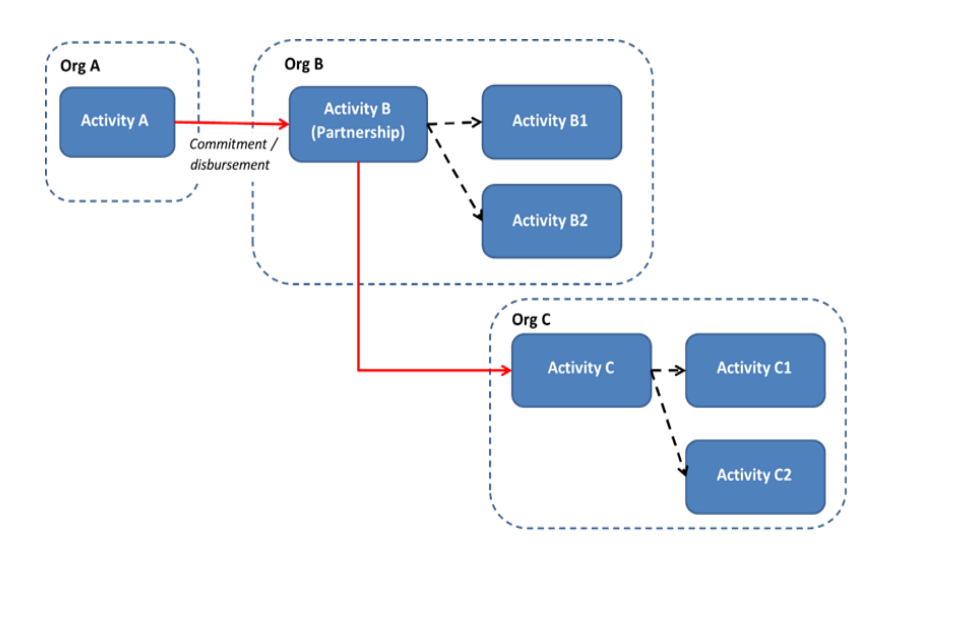

3) Partnerships

Organisation A funds Organisation B as lead organisation of a Partnership with Organisation C.

As part of Activity B, Organisation B starts Activities B1 and B2. Organisation B also transfers funds to Organisation C for its role in the Partnership

| Organisation A publishes: | Organisation B publishes: | Organisation C publishes: |

|---|---|---|

|

Activity A Funding: Organisation A Accountable: Organisation A Implementing: Organisation B and Organisation C Reference to Organisation B: Transactions (commitments/ disbursements) with Receiver-org: Organisation B |

Activity B (Hierarchy 1 = parent)Funding: Organisation A Accountable: Organisation B Implementing: Organisation B, Organisation C Reference to Organisation A: Incoming commitment/funds transaction with Provider-org: Organisation A Provider-activity-id: id of Activity A Reference to Organisation C: Transactions (commitments/ disbursements) with Receiver-org: Organisation C Activities B1 and B2 (Hierarchy 2 = child) Funding: Organisation B Accountable: Organisation B Implementing: Organisation B Reference to Activity B: Related activity: id of Activity B Type: 1 (Parent) Incoming commitment transaction Provider-org: Organisation B Provider-activity-id: id of Activity B |

Activity C (Hierarchy 1 = parent) Funding: Organisation B Accountable: Organisation C Implementing: Organisation C Reference to Organisation B: Incoming commitment/funds transaction with Provider-org: Organisation B Provider-activity-id: id of Activity B Activities C1 and C2 (Hierarchy 2 = child) Funding: Organisation C Accountable: Organisation C Implementing: Organisation C Reference to Activity C: Related activity: id of Activity C Type: 1 (Parent) Incoming commitment transaction Provider-org: Organisation C Provider-activity-id: id of Activity C |

Narrative:

Organisations A, B and C each publish an IATI activity file.

Organisation A publishes Activity A (the funding activity).

For this activity Organisation A is the funding organisation and accountable organisation. Organisation B and C are implementing organisations. Organisation A funds a partnership with Organisations B and C, where Organisation B is the lead organisation.

Organisation A refers to Organisation B through its transactions, with receiver organisation B.

Organisation B publishes Activity B.

For this activity Organisation A is the funding organisation. Organisation B is accountable (towards Organisation A) and implementing. Organisation C is also an implementing organisation and receives the funds for its activities as part of the partnership directly from the ‘Partnership’ activity.

Organisation B refers to Organisation A through an incoming commitment or incoming funds transaction, with provider organisation A and Activity A’s IATI identifier as provider-activity-id.

Organisation B refers to Organisation C through its transactions, with receiver organisation B.

Organisation B also publishes Activities B1 and B2.

For these activities Organisation B is the funding organisation (Organisation B is responsible for planning the activities). Organisation B is also accountable and implementing.

The relation between Activities B1 and B2 and Activity B is reported using the related-activity field. Activities B1 and B2 both have a related-activity Activity B, of the ‘Parent’ type.

The financial relation between Activity B and Activities B1 and B2, is represented through an incoming commitment transaction, with provider organisation B and Activity B’s IATI identifier.

Organisation C publishes Activity C.

For this activity Organisation B is the funding organisation. Organisation C is accountable (towards Organisation B) and implementing.

Organisation C refers to Organisation B through an incoming commitment or incoming funds transaction, with provider organisation B and Activity B’s IATI identifier as provider-activity-id.

Organisation C also publishes Activities C1 and C2.

For these activities Organisation C is the funding organisation (Organisation C is responsible for planning the activities). Organisation C is also accountable and implementing.

The relation between Activities C1 and C2 and Activity C is reported using the related-activity field. Activities C1 and C2 both have a related-activity Activity C, of the ‘Parent’ type.

The financial relation between Activity C and Activities C1 and C2, is represented through an incoming commitment transaction, with provider organisation C and Activity C’s IATI identifier.

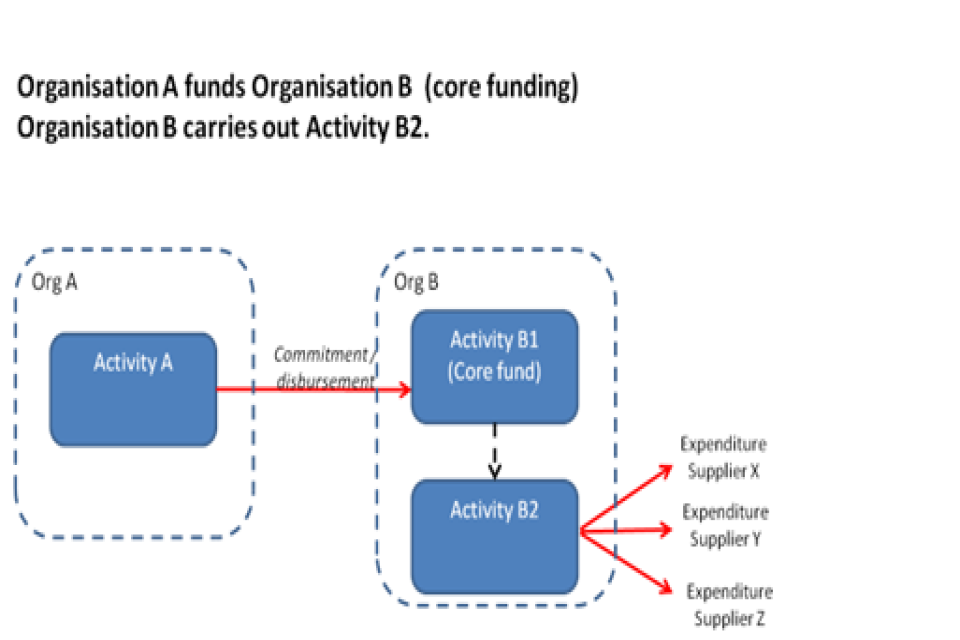

4) Core funding

| Organisation A publishes: | Organisation B publishes: |

|---|---|

|

Activity A Funding: Organisation A Accountable: Organisation A Implementing: Organisation B Reference to Organisation B: Transactions (outgoing commitments/disbursements) with Receiver-org: Organisation B |

Activity B1 Funding: Organisation A Accountable: Organisation B Reference to Organisation A: Incoming commitment/funds transaction with Provider-org: Organisation A Provider-activity-id: id of Activity A Activity B2 Funding: Organisation B Accountable: Organisation B Implementing: Organisation B Reference to own funds: Incoming commitment transaction Provider-activity-id: id of Activity B1 |

Narrative:

Organisations A and B both publish an IATI activity file.

Organisation A publishes Activity A (the funding activity)

For this activity Organisation A is the funding organisation and accountable organisation. Organisation B is the implementing organisation.

Organisation A refers to Organisation B through its transactions, with receiver organisation B.

Organisation B publishes its Core Fund as Activity B1.

For this activity Organisation A is (one of) the funding organisations. Organisation B is accountable (towards Organisation A).

Organisation B refers to Organisation A through an incoming commitment or incoming funds transaction, with provider organisation A and Activity A’s IATI identifier as provider-activity-id.

Organisation B also publishes Activity B2.

For this activity Organisation B is the funding organisation: Organisation B is responsible for planning the activity and funds it from its core fund. Organisation B is also accountable and implementing.

The financial relation between Activity B1 and Activity B2 is represented through an incoming commitment transaction, with provider organisation B and Activity B1’s IATI identifier.

-

While several types of related activities are possible within IATI, for reasons of clarity and simplicity this reporting structure only uses the ‘Parent’ type ↩

-

While many different types of related activities are possible within IATI, for reasons of clarity and simplicity this reporting structure only uses the ‘Parent’ type. ↩