Cyber security longitudinal survey - wave five results

Published 17 February 2026

© Crown copyright 2026

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/cyber-security-longitudinal-survey-wave-five-results/cyber-security-longitudinal-survey-wave-five-results

Cyber security longitudinal survey: wave five

The Cyber Security Longitudinal Survey (CSLS) is a multi-year longitudinal study, which follows the same organisations over time. It aims to better understand cyber security policies and processes within medium and large businesses and high-income charities, and the extent to which these organisations change and improve over time.

It will also explore the links over time between these policies and processes and the likelihood and impact of a cyber incident to quantify specific actions resulting in improved cyber incident outcomes.

This is the fifth research year, and therefore the main objective of this report is to establish any significant changes between the fourth year from cross-sectional data, and investigate longitudinal data across all five years. The quantitative survey was carried out in June – August 2025 and the qualitative element August – September 2025.

Responsible analyst

Emma Johns

Enquiries:

Executive summary

Introduction

The purpose of the Cyber Security Longitudinal Survey (CSLS) is to explore how and why UK organisations are changing their cyber security practices and how they implement and improve their cyber defences. For UK government, policymakers, and businesses, it is important to understand drivers of change, awareness of government guidance, and budgetary constraints. It is also vital to analyse the relationship between the actions organisations adopt to improve their cyber security and the likelihood and impact of cyber incidents, in order to provide insight into how and why organisations are changing their cyber security practices.

This report covers findings from the fifth wave of the multi-year study. The report presents analysis of both cross-sectional and longitudinal quantitative data, as well as qualitative data. Both the cross-sectional and longitudinal analysis includes comparisons to previous waves of the research (Wave One from 2021, Wave Two from 2022, Wave Three from 2023, Wave Four from 2024). Where relevant, differences between businesses and charities, or business size, are reported.

Participants in the study include medium (50-249 employees) and large (250+ employees) UK businesses and high-income charities (annual income of more than £1 million). The Wave Five main stage survey took place between June and August 2025. Qualitative interviews were conducted between September and October 2025.

The cross-sectional analysis demonstrates a snapshot of businesses and charities compared to previous waves. These snapshots explore the extent to which organisations undertook a wide range of cyber security activities within the last 12 months of survey completion and how such activities vary by organisation type and business size.

The longitudinal data explores rates of change across two points in time; an organisation’s first interview as the first point in time, and the second interview as the second point in time. This is examined across key variables, such as the cyber security practices organisations have adopted, levels of adherence to recognised standards, awareness of government guidance, and resource or budgetary constraints. It also compares changes over time between businesses and charities, and business size.

The qualitative analysis triangulates the quantitative data and provides insight into drivers and barriers to behaviour change. These interviews explored cyber incidents, uptake of government products, cyber security policies, cyber security processes, cyber security budgets and understanding cyber security behaviour change.

The cross-sectional, longitudinal and qualitative results have been integrated throughout each chapter to gain a deeper understanding and explanation of cyber practices, policies and behaviour change. Further details on the methodology, interpretation of results, and key findings can be found in the remainder of this report and the accompanying technical report .

Key Findings

While the cyber security landscape appears to be a constantly evolving and complex landscape, businesses and charities demonstrate variability in their cyber security policies, processes and behaviours. Key findings from the report are as follows:

Prevalence and impact of cyber incidents

This survey asks organisations about their experience of cyber security incidents. While the Cyber Security Breaches Survey should considered the main source of data on prevalence of cyber security incidents, this survey shows that cyber security incidents continued to be highly prevalent in Wave Five.

-

Most organisations continued to experience some form of cyber incident in Wave Five (82% businesses, 77% charities)

-

From the longitudinal data, over half of organisations (54%) reported the same experience of incidents, or incidents with impacts and outcomes, at each point of time. For example, 52% of organisations that did not have an incident at the first point of time, also did not have an incident at the second point of time

-

Over a third (34%) of organisations experiencing an incident with impact and/or outcome at time point 1 then experienced an incident without impact and/or outcome at time point 2, which suggests that either the organisation has improved resilience to minimise the impacts of an incident experienced at time point 2, or the incident was not as intrusive as to cause an impact or outcome.

-

Although it might be assumed that a lack of incidents reflects strong cyber resilience, this capacity is not assessed within this approach. As a result, organisations with no reported incidents are treated as having an unknown ability to respond and recover

Organisations’ cyber policies and processes

Businesses and charities generally seem to be inclined towards a proactive cyber security approach than reactive, although variability remained. Supplier management continued to be a pertinent weakness in organisational cyber resilience.

-

The proportion of organisations reporting adherence to Cyber Essentials rose significantly since Wave Four, for both businesses (30% vs 23%) and charities (28% vs 19%)

-

Organisations were also more likely to say they adhere to at least one of the main cyber security standards (Cyber Essentials, Cyber Essentials Plus, ISO27001 at time point 2 (31% gain vs 20% loss)

-

Organisations that experienced an incident with a tangible impact or outcome were more likely to show improved adherence to all five Cyber Essentials controls at time point 2.

-

In contrast, organisations that only experienced minor or no-impact incidents showed no clear change in adherence, and overall adherence at time point 2 was not strongly influenced by whether an organisation had any incident at time point 1.

-

Charities remained more likely to have a risk registry that covered cyber security than businesses (78% vs 64%)

-

The longitudinal data corroborates this trend; charities were much more likely to have propensity for a risk registry over 2-wave data than businesses

-

More businesses and charities reported having specific cyber insurance policies, likely reflecting a significant drop in ‘Don’t know’ responses about the types of cyber security policies in place since Wave Four.

-

Longitudinally, 98% of organisations that had specific cyber insurance at time point 1 had some form of cyber insurance policy (whether cyber specific or within general insurance) at time point 2. This shows that there is minimal fluctuation over time for those organisations already with some form of cyber insurance policy, in contrast to many other cyber security practices which show more fluctuation over time. Supply chain management remained a weakness amongst both charities and businesses.

-

Longitudinally, medium-sized businesses and charities were less likely over time to formally assess cyber security of suppliers. However, this was more likely if an organisation had an incident, or incident with impact and/or outcome.

Understanding cyber security behaviour change

In Wave Five, external influences such as widespread cyber-attack reports[footnote 1] emerged as catalysts to drive behaviour change, whether that was influencing budget, leadership discussions, or internal checks on cyber processes and policies.

Proactive vs reactive approach

-

Cyber incidents that incurred an impact and/or outcome mostly tended to have more influence on an organisation’s cyber security posture than those that experience none, or incidents without impact and outcome.

-

From the longitudinal data, if an organisation experienced no incident at time point 1 there were no statistically significant patterns of increased positive change versus negative change, compared to those organisations who experienced an incident (with or without impact and/or outcome).

-

This demonstrates a generally reactive approach that many organisations take following an incident, rather than a proactive approach. Although organisations cannot predict when a cyber incident may occur, they seemed generally aware of the increasing threat of cyber-attacks. However, the unpredictability of cyber incidents being a catalyst for change is a concern.

External influences and drivers of change

-

Publicised cyber incidents often prompted additional checks or enabled funding, but heightened awareness did not always result in tangible change; some organisations deemed their systems sufficiently secure.

-

External information sources, such as reports on sector-wide incidents, tended to be cited as motivation for improving cyber security posture (51% of businesses vs 41% of charities).

Communication and behaviour change

-

Individuals were frequently cited as weak points within most organisations.

-

Tailored communication emerged as an important approach to influence behaviour change within an organisation.

Training, education, and organisational response

-

Organisations implemented continuous training and regular penetration tests to strengthen cyber security defences and improve staff cyber practices.

-

Staff awareness and readiness were widely recognised as primary defences against future attacks, prompting greater investment in user education.

Cyber security budget and board involvement

Organisations have reported significant increases to incorporate cyber risk over time. However, this did not always translate to effective cyber budgets or board involvement, especially for charities. When an organisation experienced an incident that had a tangible impact or outcome, this often prompted stronger cyber security measures, resulting in more improvements than setbacks over time.

-

Over one-third of organisations (37% businesses, 36% charities) reported an increase in budgets in Wave Five

-

However, charities were more likely than businesses to report their cyber security budgets as insufficient and potentially leaving them exposed in some areas (10% charities vs 5% businesses)

-

Longitudinally, charities were less likely to report frequent board discussions (more often than 6 months) than businesses over time when comparing positive and negative change rates.

-

Large businesses were twice as likely to see uptake of more frequent board discussion while charities showed a higher propensity for negative change over time (Large business rate of change = 2.1, charity rate of change = 0.8).

-

This highlights that while organisations have attempted to integrate cyber risk into wider business areas, this does not translate into a charity’s budget or board level of involvement.

-

Longitudinally, across all organisations there was a lower propensity for positive change around frequency of board training.

1. Introduction

1.1 Background to the research

The Department for Science, Innovation and Technology (DSIT) commission the Cyber Security Longitudinal Survey (CSLS); a study composed of businesses, which are divided into medium (50-249 employees) and large enterprises (250+ employees), and high-income charities (annual income of more than £1m). In turn, large businesses consist of both large (250-499 employees) and very large businesses (500+ employees).[footnote 2] The findings will evaluate long-term links between the cyber security policies and processes adopted by these organisations, and the likelihood and impact of a cyber incident. It also supports the government to shape future policy in this area and inform future government cyber interventions.

This report is based on cross-sectional findings on Wave 5 (2025) and longitudinal data from 2021 (Wave One), 2022 (Wave Two), 2023 (Wave Three) and 2024 (Wave Four). Due to the longitudinal nature of the study, the aim is to track trends over time and, wherever possible, speak with the same organisations in each wave. The design of this research was influenced by a study the Department for Digital, Culture, Media and Sport (DCMS) previously commissioned to investigate the feasibility of creating a new longitudinal study of large organisations.

The core objectives of this study are to:

-

Explore how and why UK organisations are changing their cyber security profile and how they implement, measure, and improve their cyber defences

-

Provide a more in-depth picture of larger organisations, exploring topics that are covered in less detail in the Cyber Security Breaches Survey (CSBS), such as understanding drivers of change in relation to cyber security, awareness and uptake of government guidance and budgetary constraints in relation to implementing cyber security policies

-

Examine how organisations’ cyber security actions relate to the likelihood and impact of a cyber incident.

1.2 Difference from the Cyber Security Breaches Survey

This study differs from the CSBS in multiple important aspects. Firstly, it uses a longitudinal approach, where the aim is to track changes in cyber resilience over time, whereas the CSBS uses a cross-sectional sample that provides a snapshot of cyber resilience. This five-year longitudinal study (CSLS) collects data from the same organisation (businesses or charities) on more than one occasion (up to five points in time) to analyse the link between large and medium organisations’ behaviours towards cyber security and the extent to which they influence the likelihood and impact of experiencing an incident over time. In comparison, results from CSBS provide a static view of cyber resilience, the cyber threats organisations face and the actions they are taking to stay secure at a given time.

Secondly, the CSLS focuses only on medium and large businesses, and high-income charities whereas the CSBS includes businesses of all sizes, all charities, and educational institutions. CSBS is an official statistic and therefore, for overall statistics on cyber security results from CSBS should be used.

Additionally, different questions are used, so while there are some similarities in the questions and topics covered by the two surveys, results are not comparable. Further detail on overlapping questions can be found in the Cyber Security Longitudinal Survey Wave Four Technical Report. Please visit the gov.uk website to see publications of the Cyber Security Breaches Survey.

1.3 Methodology

There are two strands to the Cyber Security Longitudinal Survey. First, Ipsos undertook a random probability multimode[footnote 3] (telephone and online) survey covering 521 businesses and 273 UK registered charities between June and August 2025.[footnote 4] Of these, 611 interviews (77%) were completed via telephone and 183 interviews (23%) were completed through the online survey option. The data for businesses and charities have been weighted to be statistically representative of these two populations. Subsequently, 24 in-depth interviews were conducted in September and October 2025, to gain qualitative insights from some of the organisations that participated in the Wave 5 quantitative survey.

This longitudinal study tracks changes over time by attempting to follow the same organisations in all five annual waves. In Wave Four, 1,046 organisations (574 businesses and 472 charities) agreed to be recontacted. Data for Wave Five includes 5656 interviews (70%) who were part of the longitudinal sample, comprising 292 interviews with businesses and 264 with charities.

In addition to the organisations that had participated in the study in previous years, the survey was issued to businesses and charities that had not taken part previously. 45% (238 interviews) of the achieved sample in Wave Five came from fresh sample, comprising 229 interviews with businesses and 9 with charities. This allowed the survey to maintain a strong overall achieved sample size and, as such, ensure that robust analysis could be completed from this research and allow more detailed longitudinal analysis in future waves. To avoid possible selection bias, the ‘fresh’ business sample was selected using random probability sampling. The business sample was proportionally stratified by region and disproportionately stratified by size and sector.

The questionnaire for Wave Five of the survey only had one minor change since Wave Four, which was an update to codes for guidance available, to reflect current guidance. This change and more technical details, including methodological notes for the longitudinal analysis and a copy of the questionnaire, are available in the separately published Technical Annex.

1.3.1 Profile of survey respondents

Figure 1.1.1: Businesses and charities overall (weighted %)

Percentage of the sample that were businesses, split by size, and charities

| Businesses | 66% |

| Charities | 34% |

Base: All businesses (n=521); All Charities (n=273)

Figure 1.1.2: Businesses size breakdown – makeup of businesses that responded(weighted %)

| Medium Businesses | 82% |

| Large Businesses | 9% |

| Very Large Businesses | 9% |

Base: Medium businesses (n=427); Large Businesses (n=48); Very Large Businesses (n=46)

Please note: If organisations had been confirmed as eligible and interviewed in an earlier wave but now have fewer than 50 employees (businesses) or a turnover of less than £1 million (charities), they were still considered eligible to be interviewed and treated as medium businesses. This applied to 25 businesses in Wave Five.

Figure 1.2.1: Businesses breakdown by region (weighted %)

The distribution of responding businesses by UK regions

Businesses and charities by nation and region

| North East | 2% |

| Yorks and Humberside | 9% |

| East Midlands | 7% |

| Eastern | 9% |

| London | 10% |

| South East | 15% |

| South West | 11% |

| Wales | 5% |

| West Midlands | 9% |

| North West | 11% |

| Northern Ireland | 4% |

| Scotland | 9% |

Base: 521 UK businesses

Figure 1.2.2: Charities breakdown by nations (weighted %)

The distribution of responding charities by UK nations

| England and Wales | 79% |

| Northern Ireland | 2% |

| Scotland | 19% |

Base: 273 charities

Figure 1.3: Businesses breakdown by sector (weighted %)

Distribution of responding businesses by sector

| Manufacturing | 16% |

| Retail or wholesale (including vehicle sales and repairs) | 14% |

| Administration or Real Estate | 14% |

| Professional, scientific or technical | 11% |

| Health, social care or social work (excluding NHS) | 11% |

| Food or hospitality | 9% |

| Information or communication | 7% |

| Construction | 5% |

| Transport or storage | 4% |

| Finance or insurance | 3% |

| Education (excluding public sector schools, colleges and universities) | 2% |

| Arts or recreation | 2% |

| Utilities or production | 1% |

| Service or membership organisations | 3% |

Base: 521 UK businesses

1.3.2 Profile of qualitative respondents

Twenty-four follow-up interviews were carried out with representatives of organisations covered by the survey. They were selected to provide the following profile:

Table 1.1: Profile of qualitative respondents

| Category | Definition | Achieved | |

|---|---|---|---|

| Category | Businesses | 16 | |

| Charities | 8 | ||

| Size (employees): (Businesses only) | Medium (50-249) | 10 | |

| Large (250+) | 6 | ||

| Sector (Businesses only) | Broad mix of sectors | 16 | |

| Region (Businesses only) | Broad mix of regions | 16 |

1.4 Longitudinal analysis and cross-sectional analysis

The cross-sectional series has been the focus for each previous year of reporting and provides a snapshot of the extent to which organisations undertook a wide range of cyber security activities within the last 12 months of survey completion and how such activities vary by changes over time between businesses and charities, and business size. In principle, the CSLS cross-sectional series could be used to track trends over time. However, for more robust data, both cross-sectional and longitudinal data should be analysed, where viable, to comprehensively grasp changes over time.

Wave Four and Wave Five of the CSLS study has enabled the size of the available longitudinal sample to grow such that it can produce robust results to help inform the trends seen in the cross-sectional series. Previous uses of the longitudinal component of the study have largely been exploratory and indicative in nature. This year’s report is the first time it has been possible to provide an integrated report providing insights based both on the aggregate net change seen in the cross-sectional analysis and the individual change seen at the level of the organisation.

For the purposes of analysis, businesses are divided into medium (50-249 employees) and large enterprises (250+ employees).[footnote 5] Large businesses consist of both large (250-499 employees) and very large businesses (500+ employees). All charities included in the survey have a reported annual income of at least £1 million according to national charity regulator sample data.[footnote 6] The nature and size of cyber threats and incidents faced differs by size of organisations and charities, as shown in previous reports. Hence, it is anticipated that longitudinal patterns of response will differ between these organisational types.

Previous analysis of the longitudinal component has illustrated that growth apparent in the cross-sectional series cannot always be interpreted as a year-on-year incremental gain based on organisations attaining a positive status on a cyber security activity in one year and necessarily retaining a positive response in all future years. Rather, underlying growth trends are based both on gains and losses of positive behaviours accompanied by positive stability for some organisations previously carrying out that activity.

In this report, the focus of the longitudinal analysis is on assessing the extent of behavioural flux in cyber security activities and how this varies by two classifications, as explained below. Further work is required to understand why some activities show more flux than others and reasons for both positive and negative changes of cyber activities.

A second classification, used in the longitudinal analysis, is the experience of cyber incidents reported at the first interview. It is anticipated that experience of an incident, particularly one with adverse consequences, may influence organisations to increase positive activity among organisations not undertaking the activity at their first interview. Similarly, it may decrease positive activities among those already undertaking them. Using any experience of the incidents listed in the questionnaire (excluding phishing), organisations were first classified as experiencing an incident or not. Among those who experienced an incident (excluding phishing), any impact or outcome resulting from that incident was used to classify incidents as less adverse (incident with no impact or outcome) and more adverse (incident with an impact and/or outcome). Thus, three levels of experience were created: no incident; incident only and incident with adverse consequences (impact and/or outcome). Changes in positive and negative activities were compared between these three groups with more adverse consequence expected to have greater impacts on gains and losses.

1.5 Interpretation of cross-sectional quantitative findings

The cross-sectional analysis reports on the aggregate trends in cyber experiences and protective behaviours. This report analyses significant[footnote 7] changes (at the 95% confidence level) since Wave Four and Wave Five, and between organisation type and size within Wave Five. As stated above, the quantitative cross-sectional results should be interpreted in conjunction with the longitudinal and qualitative analysis to understand the wider state of cyber security over time.

The survey results are subject to margins of error, which vary with the size of the sample and the percentage figure concerned. For all percentage results, subgroup differences by size, sector and other survey answers have only been mentioned in the text of the report where they are statistically significant. There is a guide to statistical reliability in the technical report.

For the purposes of analysis, businesses are divided into medium (50-249 employees) and large enterprises (250+ employees).[footnote 8] In turn large businesses consist of both large (250-499 employees) and very large businesses (500+ employees). All charities included in the survey have a reported annual income of at least £1 million according to national charity regulator sample data.[footnote 9]

Where base sizes are noted as smaller than 50, they should be treated with caution.

1.6 Interpretation of longitudinal quantitative findings

The longitudinal data enable exploration of rates of positive and negative activities underlying the aggregate trends shown by the cross-sectional series. The longitudinal results are framed between time point 1, when a respondent was first interviewed, and time point 2, when they were interviewed a second time. Thus, the data can be analysed across two time points to assess rates of change.

The rates of change are considered through creating a ratio of positive to negative activity changes. A ratio of more than ‘1’ shows that the positive activity exceeds the negative activity rate from time point 1 to time point 2. A ratio of less than ‘1’ therefore shows that the negative activity rate exceeds the positive rate. For example, large businesses with a ratio of 1.2 adherence to Cyber Essentials shows that more large businesses are gaining adherence to Cyber Essentials, a positive activity, between two points in time than losing, a negative activity, at a rate of 1.2.

As described in the accompanying Technical Report, it has been necessary to pool together organisations that started at Waves One, Two, Three and Four into a single analytic dataset to create a substantial sample size. The longitudinal analysis thus focuses on these organisations’ status at their first interview and explores how this status has remained stable, or changed, at the second interview. For example, the analysis reveals how many of those undertaking a cyber security vulnerability audit at the time of their first interview also carried one out at the time of their second interview. This da ta depicts experience levels of incidents only at time point 1, in order to measure the impact on other variables over time, namely the time point 2 data.

1.7 Interpretation of qualitative findings

The qualitative findings in this report are intended to provide insight into the behaviours, views, and experiences of a range of businesses and charities. As part of the changes in Wave Four, which remained in Wave Five, Ipsos continued the Capability, Opportunity, Motivation - Behaviour model (COM-B) behavioural science approach to help understand behaviour changes. The qualitative research did not set out to determine the prevalence of these behaviours, views, and experiences.

Where the report indicates that ‘few’, ‘some’, or ‘many’ businesses and charities experienced or felt something, this is in relation to the research participants only. Findings cannot be considered representative of the entire UK business and charity population and should not be interpreted as generalisable to the entire business population.

Qualitative findings follow a cross-sectional nature and should not be interpreted as longitudinal findings.

1.8 Acknowledgements

Ipsos and DSIT would like to thank all the organisations and individuals that participated in the survey. We would also like to thank the organisations that endorsed the fieldwork and encouraged businesses and charities to participate, including:

- Tech UK

- Association of British Insurers

- Institute of Chartered Accountants in England and Wales (ICAEW)

2. Prevalence and impact of cyber incidents

This chapter examines the prevalence, type and frequency of cyber incidents that organisations have experienced in Wave Five of the Cyber Security Longitudinal Survey. This is important baseline information to understand the cyber security landscape among businesses and charities. The primary use of prevalence data is to allow for longitudinal comparisons, rather than analyse cross-sectional changes wave on wave. Therefore, this chapter presents Wave Five cross-sectional findings only, with separate longitudinal analysis presented in section 2.5. These longitudinal findings explore the prevalence and frequency of incidents, and incidents with impacts and outcomes, over time.

It is important to note that the official government statistics of cyber incidents should be taken from the Cyber Security Breaches Survey. The CSLS Wave Five results presented here focus only on medium-sized businesses, large businesses, and high-income charities. CSBS has further statistical data about the wider business population in the UK.

In Wave Five, most businesses and charities continued to experience some type of cyber incident (82% businesses, 77% charities). While phishing remained the most common type of attack, businesses reported a higher likelihood of experiencing different types of attacks than charities, such as email impersonation scams (56% businesses vs 46% charities ) or takeovers or attempts to take over website, social media accounts or email accounts (11% businesses vs 6% charities). These impersonation scams were not only limited to emails and included WhatsApp or other channels.

Following an incident, businesses were more likely to report a negative outcome than charities (22% businesses vs 15% charities). Common responses to incidents with outcomes included re-training of staff on specific threats, or technical solutions such as multi-factor authentication.

Organisations also reported wider impacts from cyber incidents. For example, 29% of large businesses reported additional staff time to deal with an incident, or to inform customers/beneficiaries or stakeholders. In addition to financial impacts, reputational damage and disruptions to day-to-day running of the organisation emerged as problematic impacts.

The longitudinal data in section 2.5 show that over half of organisations experienced the same levels of incidents, or incidents with impacts and/or outcomes, from time point 1 to time point 2. Slight improvements in incident recovery capabilities seemed apparent, likely because the organisation has improved capacity to minimise the impacts of an incident experienced at time point 2, or the incident was not as intrusive to as to cause an impact or outcome.

2.1 Prevalence of cyber incidents

In Wave Five, most organisations experienced a cyber incident. In fact, around eight in ten businesses (82%) and charities (77%) reported they had experienced some form of cyber security incident over the last twelve months. Businesses were more likely than charities to experience some form of cyber incident (63% businesses vs 53% charities). Excluding phishing attacks, very large businesses were significantly more likely to experience a cyber incident than medium-sized businesses (74% very large vs 62% medium-sized businesses). From the qualitative findings, cyber security incidents occurred frequently, with incidents reported within the last month, two months previously, and even on the current day of the interview. The constant threat levels were generally seen as tiresome.

“We get literally hundreds of phishing emails daily.”

Business, Medium, Transportation and Storage, England

2.2 Types of cyber incidents

Phishing and email impersonation scams were the most prevalent cyber security incidents experienced by organisations. Around three-quarters of organisations (76% businesses, 73% charities) reported phishing incidents. Around half (56% of businesses, 46% of charities) reported email impersonation scams, with businesses significantly more likely to experience impersonations than charities.

In Wave Five, businesses were also more likely than charities to experience:

-

Email or online impersonation of staff, volunteers, or the organisation (56% of businesses vs 46% of charities)

-

Takeovers or attempted takeovers of a website, social media, or email account (11% of businesses vs 6% of charities)

-

Denial of service attacks (8% of businesses vs 3% of charities)

Among businesses, larger organisations were more likely than medium-sized ones to experience:

-

Phishing attacks (83% of large businesses vs 74% of medium-sized businesses)

-

Unauthorised access to files or networks by staff (14% of large businesses vs 5% of medium-sized businesses)

This highlights that businesses, and in particular large businesses were more likely to have experienced incidents and attacks, but also more varied incidents and attacks.

Qualitatively, organisations described a similar pattern of cyber incident prevalent and type. Phishing attacks emerged as the main incident type across organisations, which included phishing links from suppliers and general phishing emails.

Impersonation attempts represented another significant threat, with communications impersonating CEOs and senior managers occurring through WhatsApp, email, and other channels. Account compromises also occurred, including incidents where email accounts were hijacked resulting in thousands of ransom payment emails, alongside regular attempts to hack into user accounts.

Email was the main way cyber-attacks occurred. Attackers used email to steal login credentials and deliver ransomware. Attack methods exploited multiple communication channels beyond email, with WhatsApp scams commonly noted. This highlighted a concerning trend in multi-channel phishing attempts.

Cloud storage systems presented additional vulnerabilities, demonstrated by an incident where a malicious file downloaded via Edge browser spread to an organisation’s OneDrive through syncing.

The effectiveness of training programmes was limited, with staff clicking on phishing links and providing credentials despite having undergone training. Communications showed increasing sophistication, potentially due to the use of artificial intelligence, which made fraudulent messages challenging for staff to identify.

2.3 Outcomes of cyber incidents

In Wave Five, businesses were more likely to report any type of outcome from cyber incidents than charities (22% businesses vs 15% charities). Outcomes were asked only of businesses and charities who experienced an incident, so this result is not attributable to the higher likelihood of a business receiving an attack. The most common outcomes mentioned were:

-

the organisation’s website, applications or online services were taken down or made slower (6% of businesses, 4% of charities, not significantly different)

-

temporary loss of access to files or network (5% of businesses, 4% of charities, not significantly different)

Large businesses were more likely to experience outcomes from a cyber security incident than medium-sized businesses (30% large businesses vs 20% medium-sized businesses), specifically to experience:

-

Compromised accounts or systems used for illicit purposes (11% large businesses vs 3% medium-sized businesses)

-

Physical devices or equipment being corrupted or damaged (7% large businesses vs 3% medium-sized businesses)

These negative outcomes from attacks could be linked to more sophisticated attacks, or potentially increased awareness of the outcomes among larger businesses.

From the qualitative findings, incident analysis involved various investigative activities. These included exporting sign-in logs, conducting antivirus scans, and investigating device activity using tools such as Microsoft Defender for Endpoint. Device isolation represented another immediate response measure, with potentially impacted devices isolated from networks and restricted access implemented.

Account management also emerged as a priority in immediate cyber security incident response. Organisations disabled accounts involved in incidents, including those where users had not clicked malicious links, with restrictions lifted only after accounts were confirmed secure.

After incidents occurred, organisations improved their staff cyber security training and awareness programmes. Key messages about recognising and avoiding phishing attempts were repeated to staff, with instructions to check email addresses and wording for inconsistencies. Organisations shared findings from incident analyses with all teams to help them understand threats and how to respond effectively.

Technical responses to cyber security incidents included implementing multi-factor authentication where it had not been used before. This helped prevent unauthorised access to sensitive information. Organisations also improved their encryption measures as part of their response. Security audits were conducted to examine login patterns, checking where and when employees logged in to ensure these matched their normal behaviour.

Organisations kept detailed records of all response actions using service desk systems to maintain audit trails. They brought in external IT experts to help deal with attacks and understand how they happened. Vendors supported organisations by providing updated security patches and advice. Increased monitoring was put in place, which included putting affected users on priority monitoring lists for extended periods.

In some instances, incidents validated existing measures rather than prompting changes. Where successful recovery occurred, this reinforced confidence in existing approaches rather than prompting overhaul of security measures.

2.4 Impact of cyber incidents on organisations

Incidents that did not directly have a negative outcome were still shown to have wider impact on organisations. The wider impacts measured included additional staff time to deal with an incident, prevention of carrying out day-to-day work, new measure to prevent future incidents, among other measures outlined in the technical report.

Around one-third of businesses and charities reported experiencing some kind of impact from cyber incidents (37% businesses vs 35% charities). Again, large businesses were more likely to report an impact from an incident than medium-sized businesses (47% large businesses vs 36% medium-sized businesses).

Large businesses were also more likely to report impacts compared to medium-sized businesses (excluding phishing, 53% large businesses vs 45% medium-sized businesses). This was particularly higher for large businesses for the following impacts:

- Additional staff time to deal with the incident, or to inform customers/beneficiaries or stakeholders (35% vs 24%)

-

Stopped staff from carrying out their day-to-day work (15% vs 10%)

-

New measures needed to prevent or protect against future incidents (42% vs 32%)

This places a high burden on large businesses to be vigilant in their cyber security posture, as they were more likely to report impacts from attacks.

2.5 Longitudinal analysis of cyber incidents

A longitudinal measure of experience of incidents was created through the combination of three variables: no incident, an incident without an impact and/or outcome, and an incident with an impact and/or outcome. This longitudinal data allows for analysis of the level of impact and/or outcomes organisation’s experience over time. Further, it is used as a key variable to understand how positive and negative cyber activity changes relate to levels of incidence, impact and/or outcome.

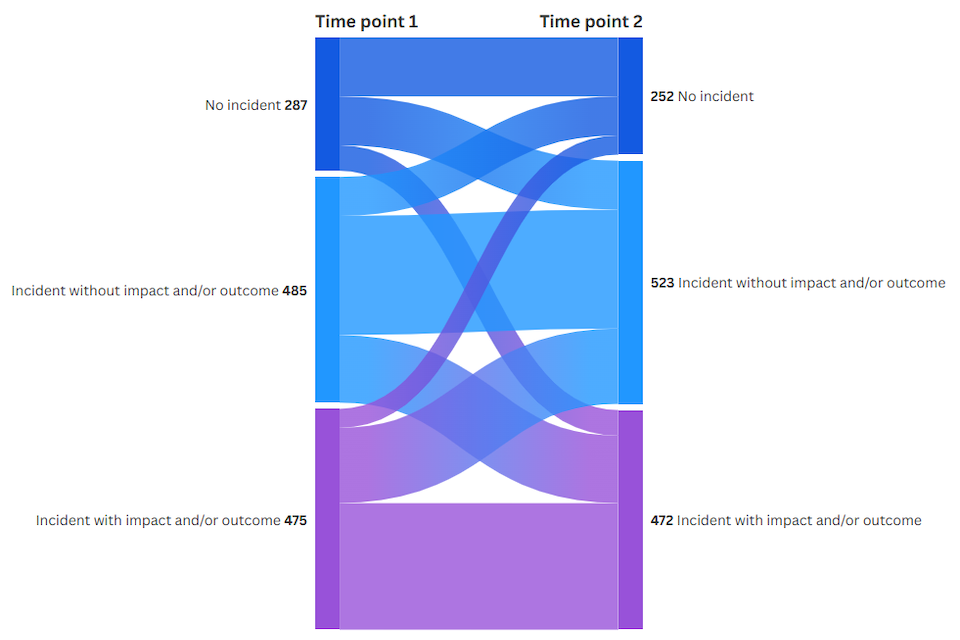

The longitudinal data, as illustrated in Chart 2.1 below, shows that of those organisations that did not experience any incidents at time point 1:

-

52% did not experience any incident at time point 2

-

32% of organisations experienced an incident without an impact or outcome at time point 2

-

16% experienced an incident with an impact and/or outcome at time point 2

Of those organisations that experienced an incident without an impact and/or outcome at time point 1:

-

17% did not experience an incident at time point 2

-

53% experienced an incident without an impact or outcome at time point 2

-

30% experience an incident with an impact or outcome at time point 2

Of those organisations that experienced an incident with an impact or outcome at time point 1:

-

9% experienced no incident at time point 2

-

34% experienced an incident without an impact or outcome at time point 2

-

57% experience an incident with an impact or outcome at time point 2

Figure 2.1: Longitudinal Cyber Security Incident Experience

| Type of incident | Time point 1 | Time point 2 | |

|---|---|---|---|

| No incident | 287 | 252 | |

| Incident without impact and/or outcome | 485 | 523 | |

| Incident with impact and/or outcome | 475 | 472 |

This data suggests that organisations’ experience of cyber incidents can vary from year to year. However, across two time points, over half of organisations (54%) reported the same experience of incidents, or incidents with impacts and/or outcomes.

Over a third (34%) of organisations experiencing an incident with impact and/or outcome at time point 1 then experienced an incident without impact and/or outcome at time point 2, which suggests that either the organisation has improved resilience to minimise the impacts of an incident experienced at time point 2, or the incident was not as intrusive as to cause an impact or outcome. This is compared to less than a third (30%) of organisations who had an impact and outcome at time point 2, after experiencing no impact and outcome at time point 1.

Although it might be assumed that a lack of incidents reflects strong cyber resilience, this capacity is not assessed within this approach. As a result, organisations with no reported incidents are treated as having an unknown ability to respond and recover.

Experience of an incident with an impact and/or outcome at the first interview tended to be associated with a similar experience at the second interview. This was especially apparent for large businesses with two-thirds (66%) of those experiencing an incident with an impact and/or outcome at time point 1 also experiencing one at time point 2.

However, 57% of charities and 55% of medium-sized businesses also reported experiencing an incident with an impact and/or outcome at both time points. Large businesses were also slightly more likely than others to see an incident at time point 1 convert to an incident with an impact and/or outcome at time point 2 (37% large businesses, 31% medium-sized businesses, 27% charities). Charities were not exempt from an increased exposure to cyber incidents. Of those experiencing no incident at time point 1, 57% experienced an incident (with or without an impact and/or outcome) at time point 2, compared to 54% of large businesses and 41% of medium-sized businesses following the same pattern of experience over time.

3. Cyber security policies and processes

This chapter explores the reported cyber security policies and processes of businesses and charities. Effective cyber security policies and processes are important building blocks for an organisation’s cyber security posture. This chapter explores cross-sectional, longitudinal and qualitative data.

Adherence to Cyber Essentials showed a significant increase among both businesses and charities compared with Wave Four (30% of Wave Five businesses vs 23% of Wave Four; 28% of Wave Five charities vs 19% of Wave Four). Over time, the longitudinal data demonstrated that organisations were more likely claim adherence with at least one of the three standards at time point 2 (Cyber Essentials, Cyber Essentials Plus, ISO 27001).

Further from the longitudinal data, adherence to any one of the accreditations showed 31% gains vs 20% losses. Additionally, adherence to all five Cyber Essentials controls[footnote 10] were more likely increase over time, after an organisation experienced an incident with an impact and outcome. Therefore, although adherence to accreditation standards was lost among some organisations, a much greater percentage reported a gain rather than a loss.

Overall, adherence did not seem significantly impacted by whether a business or charity experienced some kind of incident, or incident with impacts and outcomes. This suggests that regardless of levels of incidence, adherence may be influenced by other factors. Charities and smaller businesses were 1.5 times more likely to experience a gain than a loss of adherence to an accreditation standard, as were medium-sized businesses. For large businesses the gain to loss ratio was slightly higher at 1.65.

Businesses were more likely to report investing in threat intelligence in Wave Five (44% Wave Five vs 36% Wave Four). However, the longitudinal data highlights that this threat intelligence can fluctuate over time. More investigation would be needed in potential next waves to understand the increase.

Charities remained more likely to have a risk registry that covered cyber security than businesses (78% vs 64%). The longitudinal data corroborates this trend; charities were much more likely to have propensity for a risk registry over two points in time than businesses.

Both businesses and charities were more likely to report having a specific cyber insurance policy compared to Wave Four. Businesses increased from 29% to 35% , and charities increased from 30% to 40% . The number of businesses and charities that reportedly did not know about insurance significantly dropped wave on wave (from Wave Four to Wave Five, Don’t know reduced from 20% to 13% for businesses , and 12% to 7% for charities). This suggests that awareness and uptake of a specific insurance policy, or broader knowledge of insurance policies, may be the reason for an apparent increase in cyber insurance policies over time.

Supply chain management remained a weakness amongst both charities and businesses. Less than a third of organisations stated they carried out formal assessment of suppliers in the past 12 months (28% of businesses and 26% of charities in Wave Five ). Qualitatively, organisations generally lacked awareness about cyber security incidents in their supply chains, acknowledging they likely happen without their knowledge. Longitudinally, medium-sized businesses and charities were less likely over time to formally assess cyber security of suppliers. However, this was more likely if an organisation had an incident, or incident with impact and/or outcome (See Figure 3.9.3 below).

3.1 Uptake and usage of standards, certifications and government guidance

Organisations were asked if they adhered to each of three standards for cyber security: Cyber Essentials, Cyber Essentials Plus and/or ISO 27001, rather than whether they were formally accredited to them. Cyber Essentials has seen a significant increase amongst both businesses and charities, compared to Wave Four. Amongst businesses at Wave Five, 30% reported that they adhered to Cyber Essentials, compared to 23% in Wave Four. There was no significant difference among business sizes for Cyber Essentials, although adherence to the ISO 27001 standard remained higher for larger businesses than medium-sized businesses (24% large businesses vs 16% medium-sized businesses). Businesses also remain more likely to adhere to ISO 27001 compared to charities (17% vs 10% ). Amongst charities, 28% reported adherence to Cyber Essentials compared to 19% in Wave Four. Despite this increase wave on wave, a large proportion of businesses (37%) and charities (41%) did not comply with either ISO 27001, Cyber Essentials, nor Cyber Essentials Plus.

Figure 3.1: Businesses’ standards and accreditations

Which of the following standards or accreditations, if any, does your organisation adhere to?

| Wave | % ISO 27001 | % Cyber Essentials | % Cyber Essentials Plus | % None of these | % Don’t know |

|---|---|---|---|---|---|

| Wave 1 | 15 | 14 | 8 | 42 | 26 |

| Wave 2 | 17 | 19[s1] | 11[s1] | 39 | 20 |

| Wave 3 | 19 | 18 | 9 | 41 | 21 |

| Wave 4 | 15 [s2] | 23 | 15[s1] | 35 | 20 |

| Wave 5 | 17 | 30 | 15 | 37 | 11 |

[s1] Significant change from previous year at 95% significance level

[s2] Significant difference between businesses and charities at 95% significance level

Base: All businesses at Wave One (n=1205), Wave Two (n=688), Wave Three (n=542), Wave Four (n=674) and at Wave Five (n=521).

Figure 3.1 above shows businesses’ standards and accreditations. Figure 3.2 below shows charities’ standards and accreditations.

Figure 3.2: Charities standards and accreditations

Which of the following standards or accreditations, if any, does your organisation adhere to?

| Wave | % ISO 27001 | % Cyber Essentials | % Cyber Essentials Plus | % None of these | % Don’t know |

|---|---|---|---|---|---|

| Wave 1 | 9 | 16 | 7 | 46 | 25 |

| Wave 2 | 9 | 23[s1] | 9 | 40 | 24 |

| Wave 3 | 7 | 23 | 8 | 45 | 19 |

| Wave 4 | 9 | 19 | 12 | 47[s2] | 18 |

| Wave 5 | 10 | 28 | 11 | 41 | 15 |

[s1] Significant change from previous year at 95% significance level

[s2] Significant difference between businesses and charities at 95% significance level

Base: All charities at Wave One (n=536), Wave Two (n=373), Wave Three (n=310), Wave Four (n=548) and at Wave Five (n=273).

Longitudinally, a higher percentage of organisations claimed adherence to at least one of the accreditations at time point 2 compared to time point 1. 31% of organisations showed a gain of any accreditation adherence, compared to 20% loss of any accreditation adherence (shown in Figure 3.3 below). There were no statistically significant differences in adherence gains and losses by organisation type, or whether an organisation experienced no incident, an incident without an impact and/or outcome, or an incident with an impact and/or outcome.

Figure 3.3: Longitudinal Cyber Essentials rules or controls

| Standard or Accreditation | Positive change | Negative change | Rate of change |

|---|---|---|---|

| Any | 31% | 20% | 1.55 |

| Standard or Accreditation by impact type | None | Incident without impact and/or outcome | Incident with impact and/or outcome | |

|---|---|---|---|---|

| Any | 1.5 | 1.5 | 1.6 |

| Standard or Accreditation by organisation type | Medium-sized businesses | Large businesses | Charities | |

|---|---|---|---|---|

| Any | 1.45 | 2.23 | 1.48 |

Base: 3,361

Note: “Any” includes accreditation to at least one of: Cyber Essentials, Cyber Essentials Plus, ISO 27001

Standard or accreditation

The cross-sectional and longitudinal data demonstrate that organisations are becoming more resilient by adhering to at least one accreditation. Specific periods show increased adherence, such as the increase in Cyber Essentials uptake from Wave Four to Wave Five . A longitudinal comparison of adherence to each individal accreditation standard is complex and has the potential for misdirection. There is much flux in the gain and loss of adherence to each accreditation standard. However, adherence losses in this case do not necessarily imply losing a positive behaviour because they also include moves to a different type of accreditation among these three standards . Consequently, references to losses here should be treated with caution because they refer to flux more generally rather than a simple loss of positive activity.

The cross-sectional and longitudinal data demonstrate that organisations are becoming more resilient by adhering to at least one accreditation, and specific periods show increased adherence, such as the increase in Cyber Essentials uptake from Wave Four to Wave Five. However, individual accreditation shows fluctuation across two-time points, for example the longitudinal data showed more adherence loss than gain at time point 2 for Cyber Essentials overall (13% gain vs 39% loss across two time points).

To attain Cyber Essentials accreditation, organisations are required to have technical controls in place in five key areas:

-

A policy to apply software security updates within 14 days

-

Up-to-date malware protection across all your devices

-

Firewalls that cover your entire IT network, as well as individual devices

-

Restricting IT admin and access rights to specific users

-

Security controls on your organisation’s own devices (e.g. laptops)

In addition to the question about adherence to Cyber Essentials, organisations were asked whether they have controls in place in each of these five technical areas (regardless of whether or not they had accreditation). Despite varied claimed adherence to Cyber Essentials as a whole, more organisations showed an uptake in controls needed for Cyber Essentials across two points in time (42% gain vs 23% loss across two time points, shown in Figure 3.4 below). The longitudinal data also shows that organisations were more likely to have all five Cyber Essentials controls in place if they experienced an incident, and even more so if they experienced an incident with an impact or outcome at time point 2, as shown in Figure 3.4 below.

Figure 3.4: Longitudinal Cyber Essentials rules or controls

| Rule or Control | Positive change | Negative change | Rate of change |

|---|---|---|---|

| All five Cyber Essentials | 42% | 23% | 1.82 |

| Rule or Control | None | Incident without impact and/or outcome | Incident with impact and/or outcome |

|---|---|---|---|

| All five Cyber Essentials | 1.1 | 1.8 | 2.5 |

| Rule or Control | Medium-sized businesses | Large businesses | Charities |

|---|---|---|---|

| All five Cyber Essentials | 1.96 | 2.04 | 1.48 |

Base: 3361

Regardless of accreditation compliance, most businesses and charities reported to have at least one rule or control in place against cyber threats. Since Wave Four, more businesses reported that they backup data securely via a cloud service (92% Wave Five vs 86% Wave Four). Large businesses were more likely to report any monitoring of user activity (82% vs 66% medium), backup data securely via other means (79% vs 67% ), or use a VPN (91% vs 78% medium). Charities saw increased numbers reporting a policy to apply software security updates within 14 days (74% vs 64% at Wave Four). Compared to charities, businesses were more likely to:

-

Use a VPN (80% businesses vs 58% charities)

-

Implement firewalls that cover your entire IT network, as well as individual devices (97% businesses vs 90% charities)

-

Backing up data securely via other means (69% businesses vs 55% charities)

-

Monitor user activity (68% businesses vs 57% charities)

Advice and guidance

Businesses and charities displayed similar levels of awareness of NCSC or DSIT guidance, except for the Software Security Code of Practice which businesses were more likely to be aware of (50% businesses vs 41% charities). Just under half of organisations (44% of businesses and 47% of charities) reported use of any information or guidance from the NCSC to inform their cyber security approach. This was more likely within large businesses than medium-sized businesses (59% large businesses vs 41% medium-sized businesses).

Figure 3.5: Guidance awareness of businesses and charities

Which of the following NCSC and DSIT information or guidance, if any, are you aware of or have you used? Summary of aware

| Wave | Businesses | Charities |

|---|---|---|

| 10 steps to Cyber Security | 54% | 51% |

| Cyber Security Toolkit for Boards | 33% | 36% |

| Cyber Aware, including top tips for staying online | 57% | 56% |

| Check your Cyber Security guidance | 47% | 42% |

| Cyber Governance Code of Practice | 46% | 39% |

| Software Security Code of Practice | 50%[s2] | 41% |

| None of these | 25% | 25% |

[s2] Significant difference between businesses and charities at 95% significance level

Bases: 521 UK businesses; 273 charities

From the qualitative findings, businesses commonly cited regulatory compliance as a strong driver of cyber security practices. Several organisations adhered to Financial Conduct Authority (FCA) guidelines and related industry regulations, while aligning with ISO 27001, NIST frameworks, and NCSC recommendations. Cyber Essentials and Cyber Essentials Plus formed a baseline, supplemented with internal policies on password management, Single Sign-On (SSO), and general cyber security monitoring

Frameworks such as CISSP and SOC 2 were also referenced, alongside the NHS Data Security and Protection Toolkit for healthcare operations. Businesses emphasised a zero-trust approach, rigorous internal monitoring, red team audits, employee activity tracking, and controlled access. Policies were often linked to employee contracts to ensure accountability. AI tools and vendor newsletters were used to support gap analysis and drive proactive improvements.

“We are registered with NCSC…There’s lots of certification we have…BSI…IEC…Crest…CIIs…So we, we usually follow the procedures anyway.”

Business, Medium, Information or Communication

Businesses highlighted the need to balance operational feasibility with stringent security measures. Certification efforts frequently required adaptations to accommodate legacy systems or minimise operational disruption, while still demonstrating a commitment to formalising and improving processes.

Among charities, adherence to recognised frameworks was similarly central. Cyber Essentials and Cyber Essentials Plus were widely implemented, alongside ISO 27001 where feasible.

“We follow quite a lot of best practice because we’re ISO 27001 certified and Cyber Essential certified. So we follow best practice in regards to things like malware, having antivirus installed and updated, keeping our platforms updated within 14 days for urgent updates.”

Charity, England

Charities also referenced NHS or local government guidelines, including the DSP Toolkit when handling NHS data, and accessed specialist advice through insurers. Cyber Essentials Plus accreditation was often jointly managed with IT services, with ongoing staff training. Collaborative learning was emphasised, with lessons shared across dioceses and government bodies. Internally, charities prioritised proactive monitoring using Avast antivirus and Microsoft Admin Portal alerts, alongside user education and restricted external access, particularly for suppliers.

“We can access some specialist advice and support through the insurance company as well, because they like to know that we’re, you know, we’re not just open to anybody, you know, our systems are fairly well locked down.”

Charity, England

3.2 Current cyber security policies

Businesses and charities were asked to report whether they identified cyber security risks such as vulnerability audits, risk assessments, threat intelligence investments or use specific tools such as Intrusion Detection Systems. Compared to Wave Four, both businesses and charities significantly increased their levels of threat intelligence at Wave Five. Overall, businesses reported using more identification methods outlined above than Wave Four (90% vs 85% in Wave Four) . This was largely driven by threat intelligence which significantly increased from 36% in Wave Four to 44% in Wave Five. Large businesses were more likely to use one of these identifying tools than medium-sized businesses. Businesses in general were more likely to use one of these tools than charities (90% vs 85%). One-third (33%) of charities said they invested in threat intelligence compared to 25% in Wave Four. Risk assessments remained the most commonly used form of risk identification for charities at 70% in Wave Five.

Figure 3.6: Identifying cyber security risks

Which of the following, if any, have you done over the last 12 months to identify cyber security risks to your organisation?

| Wave | Businesses | Charities |

|---|---|---|

| A cyber security vulnerability audit | 60% | 49% |

| A risk assessment covering cyber security risks | 71% | 70% |

| Invested in threat intelligence | 44% [s1] | 33% |

| Used specific tools designed for security monitoring, such as Intrusion Detection Systems | 67% [s1] | 56% |

| None of these | 10% | 15% |

[s1] Significant change from previous year at 95% significance level

Bases: 521 UK businesses; 273 charities

Similarly to Wave Four, businesses were more likely than charities to have:

-

Performed a cyber security vulnerability audit (60% businesses vs 49% charities)

-

Invested in threat intelligence (44% businesses vs 33% charities)

-

Used specific tools designed for security monitoring (67% businesses vs 56% charities)

Longitudinally, organisations demonstrated an uptake in identifying some cyber security risks. Cyber security vulnerability audits showed higher gains of reported audits in organisations across two time points (positive change 34%, negative 27%, shown in figure 3.7). Organisations experiencing an incident, or an incident with an impact or outcome were more likely to show a positive change around auditing (shown in Figure 3.7).

Figure 3.7: Longitudinal cyber identification processes

| Cyber identification processes | Positive change | Negative change | Rate of change | |

|---|---|---|---|---|

| A cyber security vulnerability audit | 34% | 27% | 1.26 | |

| A risk assessment covering cyber security risks | 44% | 17% | 2.59 | |

| Invested in threat intelligence | 21% | 37% | 0.57 | |

| Used specific tools designed for security monitoring | 40% | 19% | 2.1 |

| Cyber identification processes | None | Incident without impact and/or outcome | Incident with impact and/or outcome |

|---|---|---|---|

| A cyber security vulnerability audit | 1 | 1.3 | 1.44 |

| A risk assessment covering cyber security risks | 2 | 2.3 | 3.2 |

| Invested in threat intelligence | 0.3 | 0.5 | 0.9 |

| Used specific tools designed for security monitoring | 1.2 | 2.2 | 2.9 |

| Cyber identification processes | Medium-sized businesses | Large businesses | Charities | |

|---|---|---|---|---|

| A cyber security vulnerability audit | 1.14 | 2.81 | 1.21 | |

| A risk assessment covering cyber security risks | 2 | 4.36 | 3.3 | |

| Invested in threat intelligence | 0.51 | 1.13 | 0.53 | |

| Used specific tools designed for security monitoring | 2.17 | 5.2 | 1.6 |

In the longitudinal panel, organisations that completed a risk assessment covering cyber security risks showed a particularly high pattern of positive change from time point 1 to time point 2 (positive change 44%, negative change 17%, shown in Figure 3.7).

Investment in threat intelligence, while shown increase wave on wave from the cross-sectional data (36% businesses in Wave Four vs 44% in Wave Five; 25% charities in Wave Four vs 33% in Wave Five), has shown fluctuation longitudinally. Counterintuitively, despite the recent increase in cross-sectional prevalence, organisations overall showed more negative change than positive change (positive change 21%, negative change 37%, shown in Figure 3.7). This pattern of results arises because until Wave Five, the cross-sectional prevalence levels were relatively flat.

Given that the longitudinal panel comprises only two interviews from each cohort of entrants to the study averaged across the first four waves of data entrants, the spike in Wave Five take-up is not apparent for most of the longitudinal cases. Nevertheless, businesses that were medium-sized were more likely to invest in threat intelligence than charities, and even more so for large businesses who showed more positive change between two time points. Organisations also showed a higher propensity for positive change around threat intelligence if they had an incident, or incident with impact and/or outcome at time point 2.

When asked to identify if they used specific tools designed for security monitoring, almost two-thirds (63%) of organisations in Wave Five reported that they do, in line with Wave Four. However, the longitudinal data showed an increased propensity over time for positive change (positive change 40%, negative change 19%, shown in figure 3.7) to use security monitoring tools. Again, incidents and incidents with impacts and outcomes were more likely to influence security monitoring tool uptake, and larger businesses were much more likely to do this than medium-sized businesses or charities (rates of change shown in Figure 3.7).

Charities remained more likely to have a risk registry that covered cyber security than businesses (78% charities vs 64% businesses), whereas businesses were more likely to have documentation that:

- identified most critical assets their organisation wanted to protect than charities (64% vs 55%)

- outlines how much cyber risk their organisation is willing to accept (34% vs 26%)

Longitudinal data corroborates this increase, as charities were much more likely to have propensity for positive changes related to a risk registry at time point 2 than businesses (Charity rate of positive change was 3.5 times, compared to 1.5 for medium-sized businesses and 1.6 for large businesses).

Businesses with documentation that outlines how much cyber risk their organisation is willing to accept increased compared to Wave Four (34% Wave Five vs 28% Wave Four). This was seemingly driven by large businesses (44% large businesses vs 33% medium-sized businesses).

Both businesses and charities were more likely to report having a specific cyber insurance policy compared to Wave Four. Businesses increased from 29% to 35%, and charities increased from 30% to 40%. Further, businesses and charities were more aware whether they had a specific, general, or no insurance. Don’t know reduced from 20% to 13% for businesses, and 12% to 7% for charities. This suggests that awareness may be the reason for the apparent uptake of a specific insurance policy, or broader knowledge of insurance policies. Large businesses were more likely to have specific cyber insurance policies (43% large businesses vs 34% of medium-sized businesses), while medium-sized businesses are more likely to have cyber security cover as part of a broader insurance policy (29% large vs 38% medium).

Longitudinally, 98% of organisations that had specific cyber insurance at time point 1 had some form of cyber insurance policy (whether cyber specific or within general insurance) at time point 2. 90% of organisations that had some form of cyber insurance policy (whether cyber specific or within general insurance) at time point 1 had some form of cyber insurance policy (whether cyber specific or within general insurance) at time point 2. This shows that there is minimal fluctuation over time for those organisations already with some form of cyber insurance policy.

Figure 3.8: Businesses that have cyber insurance policies or cover

There are general insurance policies that provide cover for cyber security incidents, among other things. There are also specific insurance policies that are solely for this purpose. Which of the following best describes your situation?

| Wave | % We have a specific cyber security insurance policy | % We have cyber security cover as part of a broader insurance policy | % We are not insured against cyber security incidents | % Don’t know |

|---|---|---|---|---|

| Wave 1 | 18 | 35 | 13 | 34 |

| Wave 2 | 25[s1] | 36 | 11 | 28 |

| Wave 3 | 26 | 43[s1] | 13 | 17 |

| Wave 4 | 29 | 40 | 11 | 20[s2] |

| Wave 5 | 35 [s1] | 36 | 16 [s1] | 13 [s1] |

[s1] Significant change from previous year at 95% significance level

[s2] Significant difference between businesses and charities at 95% significance level

Base: All businesses at Wave One (n=1205), Wave Two (n=688), Wave Three (n=542), Wave Four (n=674) and at Wave Five (n=521).

Figure 3.8 above shows businesses that have cyber insurance policies or cover. Figure 3.9 below shows charities that have cyber insurance policies or cover.

Figure 3.9: Charities that have cyber insurance policies or cover

There are general insurance policies that provide cover for cyber security incidents, among other things. There are also specific insurance policies that are solely for this purpose. Which of the following best describes your situation?

| Wave | % We have a specific cyber security insurance policy | % We have cyber security cover as part of a broader insurance policy | % We are not insured against cyber security incidents | % Don’t know |

|---|---|---|---|---|

| Wave 1 | 24 | 42 | 14 | 20 |

| Wave 2 | 32[s1] | 42 | 10 | 16 |

| Wave 3 | 32 | 46 | 10 | 11 |

| Wave 4 | 30 | 41 | 16[s1][s2] | 12 |

| Wave 5 | 40 [s1] | 42 | 11 | 7 [s1] |

[s1] Significant change from previous year at 95% significance level

[s2] Significant difference between businesses and charities at 95% significance level

Base: All charities at Wave One (n=536), Wave Two (n=373), Wave Three (n=310), Wave Four (n=548) and at Wave Five (n=273).

From the qualitative findings, businesses highlighted continuous efforts in vulnerability management and Security Operations Centre (SOC) activities as central to improving cyber security. These measures were reported to reduce system vulnerabilities and enable faster incident response, contributing to fewer incidents and improved reaction times. Key effective actions included implementing multi-factor authentication (MFA), onboarding cyber security monitoring and detection software for threat visibility, deploying endpoint security, and enhancing staff education on password security.

Other impactful measures included deploying email security from malicious emails (phishing, ransomware, spam, and malware), company firewalls, incident response planning, and strict deadlines for mandatory training. Staff awareness and proactive reporting were consistently emphasised as crucial to maintaining a secure environment. Conversely, over-reliance on antivirus software, previous approaches focused solely on technology purchases and attempts to lock down network ports were reported as less effective, often creating a false sense of security or encountering user resistance.

Technical and procedural measures were viewed as integral to maintaining resilience. Organisations reported using comprehensive firewalls, conditional access controls, and micro-segmentation to limit the spread of potential breaches. Cyber security certifications, including Cyber Essentials and ISO 27001, alongside regular staff awareness activities, reinforced these controls. One business described strict adherence to internal policies and external audits as a major strength that ensured ongoing improvement. Overall, technical controls and formal governance frameworks appeared mutually reinforcing, combining technology and process to reduce vulnerability.

Partnerships with Managed Security Service Providers (MSSPs) provided additional assurance through 24/7 monitoring, incident response, and staff training. Participants described a strong security culture, where employees actively questioned suspicious communications. Organisations that had experienced attacks cited effective recovery processes and lessons learned as evidence of maturity, indicating that prior incidents reinforced organisational readiness.

“We’re not just talking, we’re walking the walk.”

Business, Medium, Transport and Storage

Large businesses remained more likely to have a physical server than medium-sized businesses (81% businesses vs 71% charities). Overall, businesses also remained much more likely to have a physical server than charities (74% businesses vs 47% charities), although this remained relatively stable wave on wave for both businesses and charities.

Figure 3.10: Businesses’ use of physical server or cloud server

Does your organisation use or provide any of the following?

| Wave | % A cloud server that stores your data or files | % Your own physical server that stores your data or files | % None of these |

|---|---|---|---|

| Wave 1 | 68 | 82 | 3 |

| Wave 2 | 70 | 81 | 2 |

| Wave 3 | 72 | 76 | 4 |

| Wave 4 | 79[s1] | 76[s2] | 3 |

| Wave 5 | 83 | 74[s1] [s2] | 3 |

[s1] Significant change from previous year at 95% significance level

[s2] Significant difference between businesses and charities at 95% significance level

Base: All businesses at Wave One (n=1205), Wave Two (n=688), Wave Three (n=542), Wave Four (n=674) and at Wave Five (n=521).

Figure 3.10 above shows businesses’ use of physical server or cloud server. Figure 3.11 below shows charities’ use of physical server or cloud server.

Figure 3.11: Charities’ use of physical server or cloud server

Does your organisation use or provide any of the following?

| Wave | % A cloud server that stores your data or files | % Your own physical server that stores your data or files | % None of these |

|---|---|---|---|

| Wave 1 | 77 | 72 | 5 |

| Wave 2 | 80 | 66 | 3 |

| Wave 3 | 86 | 60 | 2 |

| Wave 4 | 88[s2] | 54 | 5 |

| Wave 5 | 88 [s1] | 47 | 4 |

[s1] Significant change from previous year at 95% significance level

[s2] Significant difference between businesses and charities at 95% significance level

Base: All charities at Wave One (n=536), Wave Two (n=373), Wave Three (n=310), Wave Four (n=548) and at Wave Five (n=273).

3.3 Cyber processes

Supplier cyber security management remains a low priority for most organisations. Similar to Wave Four, less than a third of organisations at Wave Five stated they formally assessed the potential cyber security risks presented by their suppliers in the past 12 months (28% businesses, 26% of charities in Wave Five). At Wave Five, this was more common in large businesses compared to medium-sized businesses (40% large businesses vs 25% medium-sized businesses). This is a potentially concerning challenge since suppliers can be a risk factor in cyber incidents.

Of those who reported they reviewed immediate supplier risks, businesses were more likely than charities to carry out a formal assessment of their cyber security (44% businesses vs 28% charities) and give suppliers information or guidance on their cyber security (55% businesses vs 35% charities).

The longitudinal data shows that more organisations had a propensity to show negative change than positive change around any supplier cyber engagement. On a formal level, organisations were less likely to carry out any assessment or management of cyber risks by suppliers or partners over time (negative change 37%, positive change 16%, shown in Figure 3.12). However, if the organisation experienced an incident (with or without impacts and outcomes), the organisation was less likely to lose supplier cyber security assessment/management (shown in Figure 3.12). Large businesses were the only subset of organisations to show the same level of change over time for supplier management, that is the rate of change across two points were equal (rate of change=1).

Figure 3.12: Longitudinal supplier activity

| Supplier Activity | Positive change | Negative change | Rate of change |

|---|---|---|---|

| Any supplier activity | 12% | 42% | 0.29 |

| Formally assess/manage potential cyber security risks | 16% | 37% | 0.43 |

| Supplier Activity by impact type | None | Incident without impact and/or outcome | Incident with impact and/or outcome |

|---|---|---|---|

| Any supplier activity | 0.17 | 0.26 | 0.4 |

| Formally assess/manage potential cyber security risks | 0.2 | 0.4 | 0.63 |

| Supplier Activity by organisation type | Medium-sized businesses | Large businesses | Charities |

|---|---|---|---|

| Any supplier activity | 0.22 | 0.79 | 0.29 |

| Formally assess/manage potential cyber security risks | 0.33 | 1.00 | 0.45 |