Budget 2016

Updated 16 March 2016

© Crown copyright 2016

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/budget-2016-documents/budget-2016

1. Executive summary

This is a Budget that puts the next generation first. In uncertain times and against a deteriorating global economic outlook, this Budget delivers security for working people. It takes the next bold steps in the government’s long-term economic plan. It reduces the deficit, achieves a surplus and makes the reforms needed so Britain is fit for the future.

The UK is forecast to grow faster than any other G7 economy this year, with employment at record highs, but with productivity growth weaker than forecast. So this Budget sets out long-term solutions to long-term problems and invests in the education, builds the infrastructure and supports the savings of the next generation.

In this Budget, the government will take action to:

- make additional savings equivalent to 0.5% of total government spending, to ensure the nation lives within its means

- back business with a major overhaul of corporation tax reliefs, a lower corporation tax rate and a big reduction in small business rates

- boost enterprise with a reduction in Capital Gains Tax and tax for the self-employed

- accelerate education reforms and improve children’s health with a soft drinks industry levy

- support working people with a £11,500 personal allowance and a £45,000 higher rate threshold

- back savers with a new flexible Lifetime ISA for young people and a higher ISA limit for all

1.1 The UK economy and public finances

Britain is forecast by the Organisation for Economic Co-operation and Development (OECD) to be the fastest growing major advanced economy this year. With employment at a record rate of 74.1%. But the challenges the country faces are growing.

Since the Spending Review and Autumn Statement was published in November 2015, the outlook for the global economy has worsened and global growth has slowed, with the International Monetary Fund (IMF) predicting global growth of 3.4% in 2016, 0.2 percentage points lower than its October forecast. In advanced economies, there are growing concerns about productivity growth, high debt levels and deflationary risks. Productivity growth since the financial crisis of 2008 and 2009 has been weaker in all the major advanced economies, including the UK.

In emerging economies risks have also increased, with falling oil prices hitting commodity-exporting economies, Russia and Brazil in recession, and China’s rebalancing leading to lower growth in a number of countries.

Uncertainty about global growth prospects has been reflected in volatility in financial markets, with world stock markets seeing $8 trillion wiped off their value at the start of the year. As one of the most open economies in the world, the UK is not immune to global slowdowns and shocks. All this means the challenge of delivering a sustained rise in living standards following the financial crisis is greater here in Britain than the Office for Budget Responsibility (OBR) had previously forecast.

This is precisely why the UK has been working through its long-term economic plan. Since 2010 the plan has been focussed on reducing the deficit, while delivering the supply side reforms necessary to improve long-term productivity growth. That has allowed an active monetary policy to support the economy while ensuring the fiscal position is sustainable in the long term.

As a result, the deficit at 3.8% is forecast to be down by almost two thirds from its peak, bank capital ratios have doubled and there are over 2 million new jobs since 2010. Had the government not taken action to reduce the structural deficit from its 2009-10 level, cumulative borrowing would have been £930 billion higher in 2019-20.

Eight years ago, the UK was one of the worst prepared to face the financial crisis. Today, in the face of a cocktail of global risks, the UK is one of the best prepared. The UK responds to lower productivity growth and a more difficult global economy by:

- maintaining credible public finances and running a surplus in 2019-20

- cutting taxes for business and enterprise

- investing in infrastructure and devolving power

- improving education and healthcare

- supporting savings

- cutting taxes for working people

This is a Budget which acts now so that the country doesn’t pay later. It is a Budget that steers Britain through uncertain times, providing security now and opportunity for the next generation.

1.2 Economic and fiscal forecast

The OBR forecasts GDP growth of 2.0% in 2016, 2.2% in 2017 and 2.1% to the end of the forecast period. It forecasts employment to be 31.5 million in 2016, rising each year to 32.1 million in 2020. CPI is forecast to be below the 2.0% inflation target in 2016, returning gradually to 2.0% in 2018.

Public sector net borrowing is forecast to fall to 3.8% of GDP in 2015-16 and then to fall each year for the remainder of the forecast period. The OBR forecasts that the public finances will deliver a surplus of £10.4 billion in 2019-20 and £11.0 billion in 2020-21. Public sector net debt is forecast to fall to 74.7% of GDP in 2020-21.

1.3 Sound public finances

The government’s first duty to the next generation is to put the public finances on a sustainable footing. This provides the bedrock of security for working people. This Budget will ensure that the UK will meet its fiscal target of achieving a surplus in 2019-20. In addition to measures announced at the Spending Review and Autumn Statement, the government will:

- conduct a departmental efficiency review, which will help deliver a further £3.5 billion of savings from public spending in 2019-20, while maintaining the protections set out at the Spending Review and Autumn Statement

- ensure that the cost of providing public sector pensions in the future is fairly reflected in the contributions made by employers, by reducing the public service pension scheme discount rate

- continue to spend 0.7% of gross national income on Official Development Assistance (ODA) adjusted in line with the latest economic forecasts

1.4 Support for working people

This Budget provides security for working people and opportunity for the next generation. The government will:

- reduce tax on working people further by increasing the personal allowance to £11,500 and the higher rate threshold to £45,000 in 2017-18

- freeze fuel duty, saving the average driver £75 every year compared to pre-2010 fuel duty escalator plans

- recognise the role pubs play in local communities and support the Scotch whisky industry by freezing duty on beer, spirits and most ciders

- drive forward the radical devolution of power to school leaders, expecting all schools to become academies by 2020, or to have an academy order in place to convert by 2022

- introduce a new soft drinks industry levy to help tackle childhood obesity, by incentivising companies to reduce the sugar in the drinks they sell, to fund a doubling of the primary schools sports premium to £320 million per year from September 2017

- give the next generation choice and flexibility in their savings, by increasing the ISA limit to £20,000 and launching a new flexible Lifetime ISA for under 40s in which people can save up to £4,000 each year and receive an additional 25% bonus from government. Savings, including the government bonus, can be accessed to buy a first home and in retirement

- launch a new Help to Save scheme for people on low incomes, providing a 50% government bonus on up to £50 of monthly savings, benefiting up to 3.5 million people

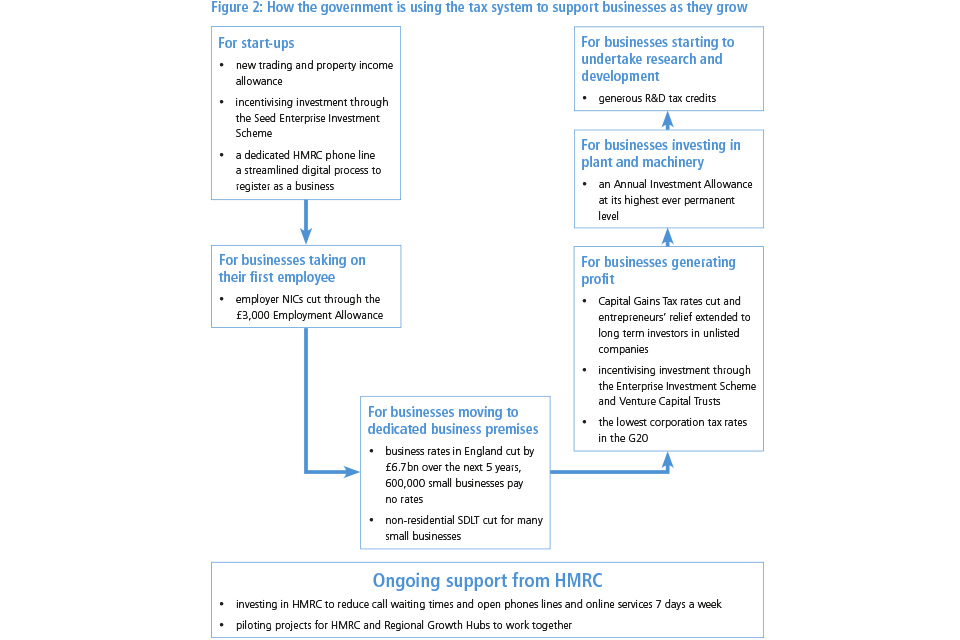

1.5 Backing business and creating opportunity

This Budget backs business and enterprise to drive up productivity growth and create job opportunities. This Budget continues to lower taxes, with new support for small business and entrepreneurs, while also modernising the tax system and taking steps to ensure that taxes are fair and are paid.

The government will:

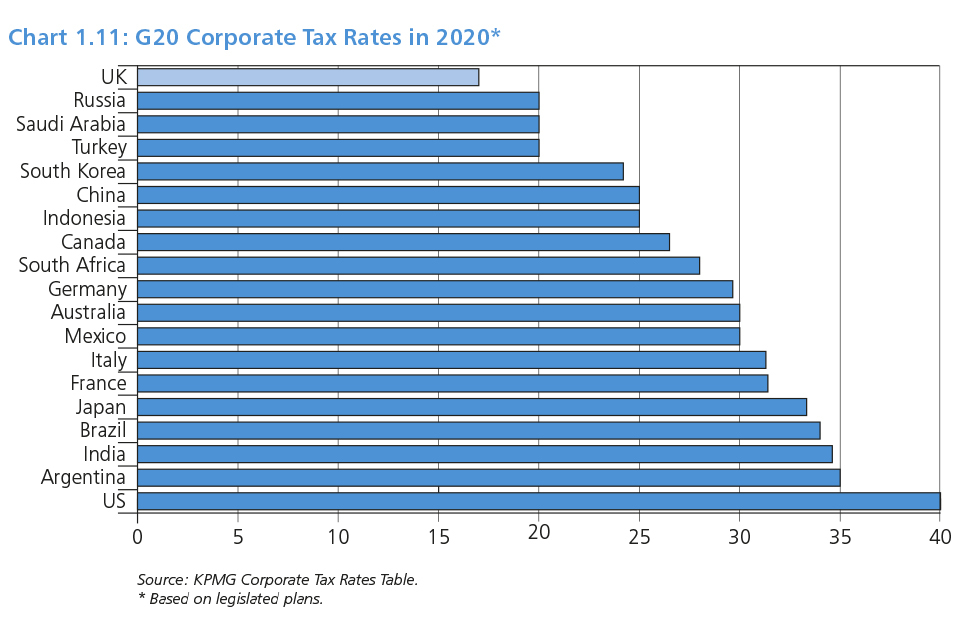

- cut the rate of corporation tax to 17% in 2020, benefiting over one million companies, large and small

- cut business rates for all properties in England, with 600,000 small firms paying no rates so that the business rates burden will fall by £6.7 billion over the next five years

- cut the higher rate of Capital Gains Tax from 28% to 20% and the basic rate from 18% to 10% from April 2016 (except for residential property and carried interest), and extend entrepreneurs’ relief to long term investors in unlisted companies

- cut National Insurance contributions for 3.4 million self-employed people, by abolishing Class 2 National Insurance

- modernise the corporation tax rules on losses, making the system more flexible for businesses while ensuring that companies making large profits pay tax on these, and further restricting banks’ use of their historic losses

- reform Stamp Duty Land Tax on non-residential property transactions, cutting the tax for many small businesses purchasing property, with over 90% of non-residential transactions paying the same or less

- abolish the bureaucratic and burdensome Carbon Reduction Commitment energy efficiency scheme and replace it, in a revenue neutral way, with an increase in the Climate Change Levy from 2019

- support the oil and gas industry by permanently zero-rating Petroleum Revenue Tax, reducing the Supplementary Charge from 20% to 10% and introducing targeted measures to encourage investment in exploration, infrastructure and late-life assets

- give large companies more time to prepare for a new corporation tax payments schedule, with a broadly neutral impact on the public finances

1.6 Opportunity across the UK

To tackle the long term economic challenges in the UK, this Budget announces radical reforms that will drive future prosperity, investing in the infrastructure that will deliver economic growth for the next generation. The Budget drives forward the devolution revolution, giving local areas further control over the decisions that affect their communities.

Headline measures include:

- strengthening city regions within Scotland and Wales by agreeing a City Deal for Cardiff and opening negotiations on deals for Swansea and Edinburgh

- agreeing new mayoral devolution deals with the West of England, East Anglia and Greater Lincolnshire as well as agreeing additional mayoral devolution deals with Greater Manchester and Liverpool City Region

- building the Northern Powerhouse, by giving the go ahead to High Speed 3 between Leeds and Manchester, aiming to bring down journey times from 50 minutes to around 30 minutes, investing an extra £161 million to accelerate the transformation of the M62, and £75 million to improve other road links across the North including the A66 and A69

- securing London’s future infrastructure by giving the green light for Crossrail 2 to proceed. The government will provide £80 million to develop the project with the aim of bringing forward a Hybrid Bill this Parliament

1.7 Budget decisions

A summary of the fiscal impact of Budget policy decisions is set out in Table 1. Chapter 2 provides further information on the fiscal impact of the Budget.

Table 1: Budget 2016 policy decisions (1)

| £ million | |||||

|---|---|---|---|---|---|

| 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | |

| Total tax policy decisions (2) | +645 | -960 | -470 | +330 | -2,760 |

| Corporation Tax: defer bringing forward payment for large groups for two years | 0 | -6,000 | -3,850 | +5,965 | +3,600 |

| Total spending policy decisions | -360 | -590 | -450 | +7,620 | +3,335 |

| TOTAL POLICY DECISIONS | +285 | -7,550 | -4,770 | +13,915 | +4,175 |

| Memo: TOTAL POLICY DECISIONS (2) | +285 | -1,550 | -920 | +7,950 | +575 |

| (1) Costings reflect the OBR’s latest economic and fiscal determinants. |

| (2) This excludes the delay to the timing of corporation tax payments by larger groups. As it represents a cash-flow impact the effect of this measure over the scorecard period is broadly neutral. |

1.8 Government spending and revenue

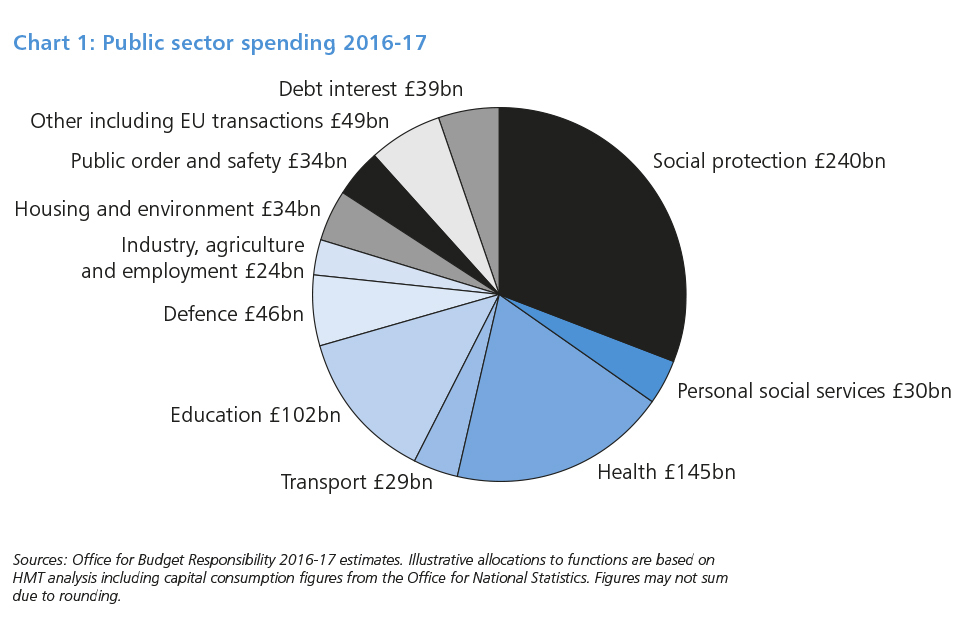

Chart 1 shows public spending by main function. Total Managed Expenditure is expected to be around £772 billion in 2016-17.

Chart 1: Public sector spending 2016-17

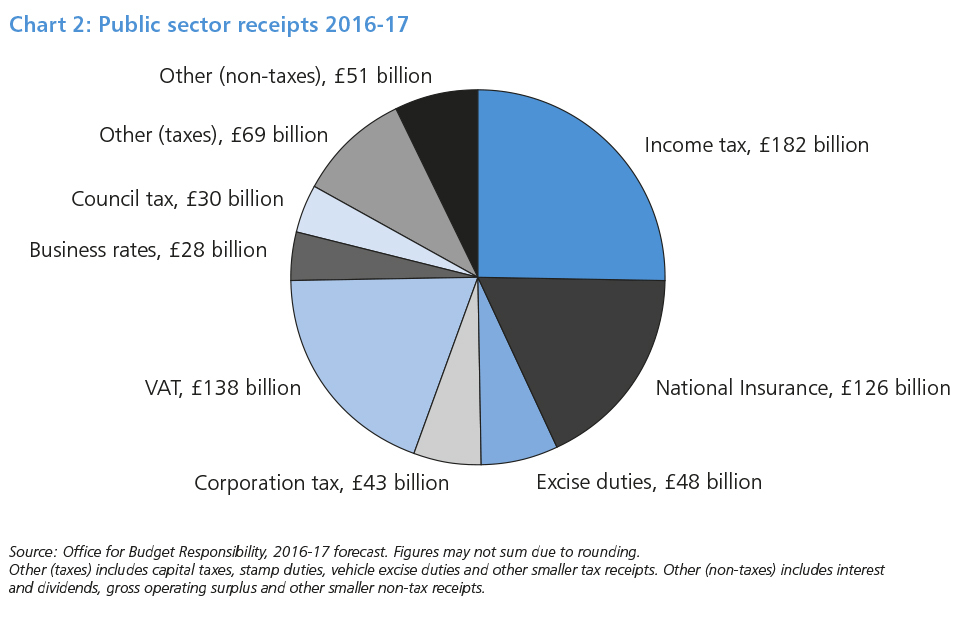

Chart 2 shows the different sources of government revenue. Public sector current receipts are expected to be around £716 billion in 2016-17.

Chart 2: Public sector receipts 2016-17

2. The UK economy and public finances

2.1 Britain and the global economy

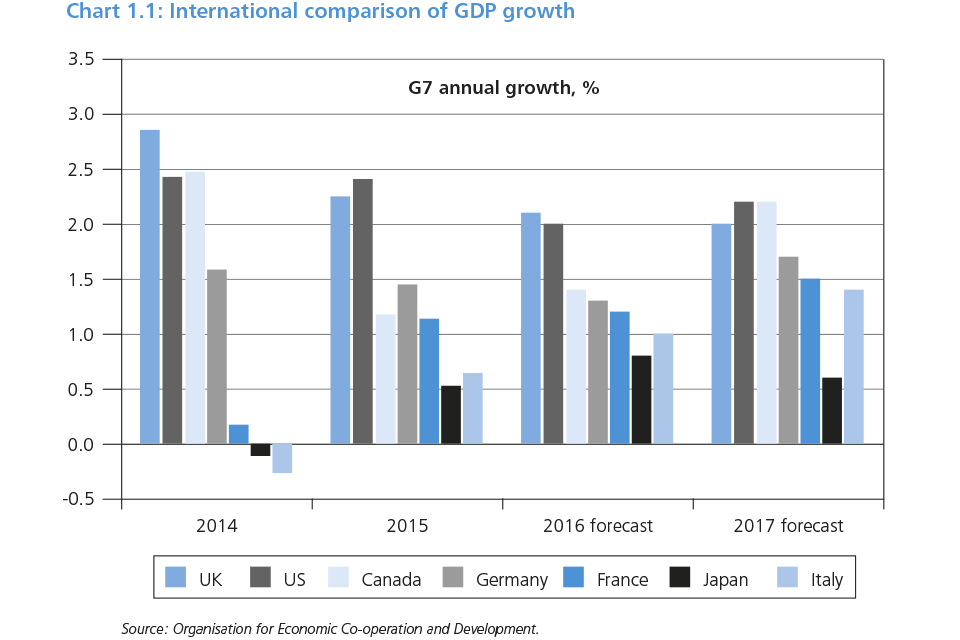

Britain is forecast to grow faster than any other major advanced economy in 2016.[footnote 1] GDP in Q4 2015 was 12.6% higher than it was in Q1 2010.[footnote 2] But the challenges the country faces are growing.

The global economic outlook has deteriorated since the Spending Review and Autumn Statement 2015. Both the International Monetary Fund (IMF) and the Organisation for Economic Cooperation and Development (OECD) have revised down their global forecasts for GDP in 2016. The IMF predicts global growth of 3.4% in 2016, 0.2 percentage points lower than its October forecast while the OECD forecasts growth of 3.0% in 2016, 0.3 percentage points below its November forecast.[footnote 3], [footnote 4]

These downgrades, which reflect a pattern of disappointing post-crisis growth in many countries, are partly driven by concerns over productivity growth. Christine Lagarde, Managing Director of the IMF, recently noted that weaker productivity growth – the rate the economy increases output per hour worked – and echoes of the financial crisis of 2008 and 2009, are still holding back global growth.[footnote 5] Angel Gurria, Secretary-General of the OECD, said “Productivity growth – a central ingredient in the pursuit of well-being – has been decelerating in a vast majority of countries”.[footnote 6]

All G7 economies have seen lower productivity growth since the financial crisis. The UK was hit hard by the financial crisis, and productivity fell 2.2% from its pre-crisis peak.[footnote 7] Since 2012, output per hour has grown each year and increased by 0.8% in 2015 to exceed its pre‑crisis peak.

But as the Office for Budget Responsibility (OBR) says, with a period of weak productivity growth after the financial crisis continuing to lengthen, they have placed more weight on the post-financial crisis period as a guide to future prospects.

Chart 1.1: International comparison of GDP growth

2.2 Global outlook

Prospects for key emerging markets have deteriorated recently. For 2016, the IMF forecasts growth in emerging markets to be 4.3%, compared to 4.7% a year ago.[footnote 8] These economies face a number of risks. As China rebalances towards domestic consumption, the emerging markets whose exports are geared to China’s previous manufacturing and investment-led growth are suffering. And after a decade of cheap debt, emerging markets are facing tighter credit conditions. Over $735 billion in capital flowed out of emerging markets last year.[footnote 9]

These concerns about growth prospects have been reflected in financial market volatility since the turn of the year. Global stock markets had their worst six-week start to the year for more than 45 years, with over $8 trillion wiped off world markets.[footnote 10]

Having fallen by 70% from June 2014 to December 2015, the price of oil fell further to $27 per barrel at the end of January 2016 and has averaged under $33 for the first two months of 2016.[footnote 11] At the time of the Spending Review and Autumn Statement 2015, markets expected the price of oil to rise gradually to $50 per barrel in early 2016. While a sustained fall in the oil price is a net benefit to oil importing economies like the UK, it impacts on particular sectors including the North Sea oil and gas industry. The speed and intensity of the falls in commodity prices in the last 18 months have increased financial stress and worsened the economic outlook for commodity exporters like Brazil, Russia and many countries in the Middle East.

The combination of lower global growth and cheaper oil has meant inflation has fallen across advanced economies, with every major central bank revising down its inflation forecast. As a result, market expectations of the timing of interest-rate rises have been pushed back.

Together, the prospects of weaker growth and inflation have reduced the outlook for GDP measured at current prices, i.e. nominal GDP. Global nominal GDP growth is estimated by the IMF to have been half the rate in 2015 that it was in 2007, making it harder to bring down debt-to-GDP ratios.[footnote 12]

2.3 OBR economic forecast

Table 1.1: Summary of the OBR’s central economic forecast (1)

| Percentage change on a year earlier, unless otherwise stated | |||||||

|---|---|---|---|---|---|---|---|

| Forecast | |||||||

| 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | ||

| GDP growth | 2.2 | 2 | 2.2 | 2.1 | 2.1 | 2.1 | |

| Main components of GDP | |||||||

| -Household consumption (2) | 2.9 | 2.4 | 2.2 | 2.1 | 2 | 1.9 | |

| -General government consumption | 1.7 | 0.2 | 0.6 | 0.5 | 0.2 | 0.7 | |

| -Fixed investment | 4.2 | 2.9 | 4.5 | 4.1 | 4 | 4.3 | |

| –Business | 4.7 | 2.6 | 6.1 | 5.8 | 5.5 | 4.4 | |

| –General government (3) | 2.2 | 0.2 | 1.9 | -0.3 | -0.2 | 6.5 | |

| –Private dwellings (3) | 3.4 | 5.1 | 2.8 | 3 | 3 | 2.9 | |

| -Change in inventories (4) | -0.4 | 0.2 | 0 | 0 | 0 | 0 | |

| -Net trade (4) | -0.5 | -0.4 | -0.1 | -0.1 | -0.1 | -0.1 | |

| CPI inflation | 0 | 0.7 | 1.6 | 2 | 2.1 | 2 | |

| Employment (millions) | 31.2 | 31.6 | 31.7 | 31.9 | 32 | 32.1 | |

| LFS unemployment (% rate) (5) | 5.4 | 5 | 5 | 5.2 | 5.3 | 5.3 |

| (1) All figures in this table are rounded to the nearest decimal place. This is not intended to convey a degree of unwarranted accuracy. Components may not sum to total due to rounding and the statistical discrepancy. |

| (2) Includes households and non-profit institutions serving households. |

| (3) Includes transfer costs of non-produced assets. |

| (4) Contribution to GDP growth, percentage points. |

| (5) Labour Force Survey. |

| Source: Office for Budget Responsibility, Office for National Statistics. |

The UK is one of the most open trading economies in the world and is not immune to the weaker global outlook. And as in other major advanced economies, the UK’s productivity growth has been slower since the financial crisis. Combined, this means that the challenge of delivering a sustained rise in living standards following the financial crisis of 2008 and 2009 is greater here in the UK than the OBR previously forecast, with GDP growth, inflation and nominal GDP growth now forecast to be weaker than at the time of the Spending Review and Autumn Statement 2015.[footnote 13]

The OBR forecasts GDP growth to be 2.0% in 2016, rising to 2.2% in 2017 and 2.1% in 2018.

The main driver of the reduced GDP forecast is a lower forecast for potential productivity growth – the amount of output growth per hour worked the economy is capable of producing sustainably – with the OBR placing more weight on post-crisis weakness in productivity growth. Productivity is expected to grow by 1.0% in 2016 and 1.7% in 2017, before rising to 2.0% for the remainder of the forecast period.

Disappointing productivity growth is evident in many other major advanced economies in recent years, leading other forecasters to revise down their expectations. For example, Table 1.2 from the OBR ‘Economic and fiscal outlook’ March 2016, shows that OBR forecasts for potential productivity growth between 2010 and 2020 have been revised down by 7.5 percentage points. This is similar to the Congressional Budget Office (CBO) in the US which has reduced its forecast for potential productivity growth by 8.9 percentage points. The impact on potential GDP growth has been smaller in the UK, however, largely because the labour market participation rate has held up much more than in the US.

Table 1.2: Contributions to potential output growth between 2010 and 2020

| Potential productivity (1) | Potential average hours | Potential participation rate (2) | Potential unemployment rate (2,3) | Potential population (2) | Potential output growth (4) | |

|---|---|---|---|---|---|---|

| OBR estimates for the UK | ||||||

| Jun 2010 | 21.9 | -2 | -1.8 | 0 | 5.8 | 24.1 |

| Mar 2016 | 14.4 | -1 | 0 | -0.2 | 6.7 | 20.6 |

| Change | -7.5 | 0.9 | 1.8 | -0.2 | 0.9 | -3.5 |

| OBR calculations based on CBO estimates for the US | ||||||

| Aug 2010 | 24.3 | -0.8 | -3 | 0 | 9.5 | 30.8 |

| Jan 2016 | 15.4 | -0.6 | -5.6 | 0.3 | 10.6 | 20 |

| Change | -8.9 | 0.2 | -2.6 | 0.3 | 1.1 | -10.8 |

| (1) Output per hour. |

| (2) Corresponding to those aged 16 and over. |

| (3) Percentage point growth between 2010 and 2020. |

| (4) Changes may not sum due to rounding and interaction effects. |

| Note: Non-farm business employment forecasts are not available for the US, and so we have assumed that non-farm business employment grows at the same rate as whole economy employment. |

| Source: Office for Budget Responsibility. |

The OBR predicts the UK’s strong labour market performance to continue. The OBR revised up its forecast for employment in 2016 from 31.5 million to 31.6 million, and in 2017 employment reaches 31.7 million. The OBR forecast employment to rise by 0.9 million by 2020, meaning that employment will have risen by 3 million since 2010. Wages and salaries are forecast to grow faster than inflation, rising by 3.6% in 2016, and thereafter by an average of 4.0% until 2020. The OBR forecasts CPI inflation to be below the 2.0% target in 2016 before returning to target in 2018.

2.4 Britain in a stronger position to face the challenge ahead

Since 2010, the government’s long-term economic plan has been focussed on ensuring sound public finances, while delivering the supply-side reforms necessary to improve long-term productivity. That has allowed active monetary policy to support the economy while ensuring the fiscal position is sustainable. As a result of the government’s action to date:

- the public finances have improved. In 2010, the IMF forecast the UK to have the largest budget deficit in the G20, at 11.4% of GDP.[footnote 14] As a result of the action that the government has taken, the OBR forecast that the UK’s deficit as a share of GDP will be reduced by almost two-thirds to 3.8% of GDP in 2015-16

- the financial sector is much more resilient. Since 2010, the government has legislated for the ring-fencing of large banks’ retail arms from their investment banking arms, insulating these core functions vital to households and SMEs, and put the Bank of England back in charge of bank prudential regulation. As the Governor of the Bank of England said, “UK banks are now significantly more resilient than before the global financial crisis. Capital requirements for the largest banks have risen ten-fold. Their holdings of liquid assets have increased four-fold. Their trading assets are down by a third, and inter-bank exposures have shrunk by two‑thirds”[footnote 15]

- household finances are more robust. Debt-to-income ratios have fallen from 155% in Q1 2010 to 142% in Q3 2015. The share of households with very high mortgage debt-to-income ratios has been falling and is now back at levels seen in the 1990s.[footnote 16] Interest payments as a proportion of income were 4.8% in Q3 2015, the lowest on record and down from 6.3% in Q1 2010

The long-term economic plan has delivered considerable economic gains since 2010. The UK was the fastest growing major advanced economy in 2014, the second fastest in 2015 and the OECD forecast the UK to be the fastest growing in 2016.

2.5 Employment and earnings

2.6 Employment

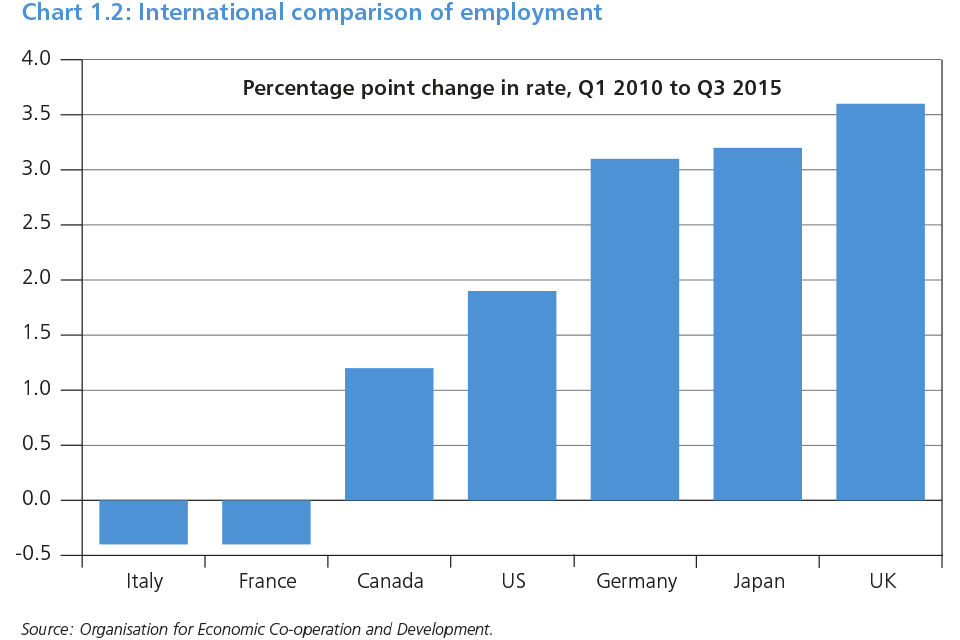

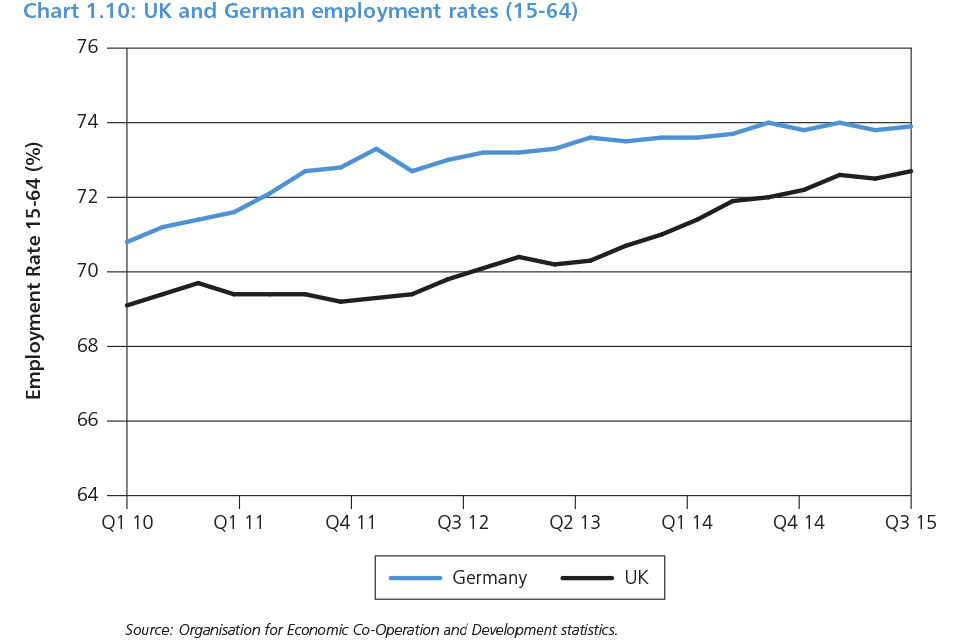

Government action to reward work and reform benefits has delivered a stronger labour market in the UK, with an employment rate that has risen faster in the UK than in any other G7 country since 2010 making progress towards the government’s goal of full employment.[footnote 17] The data for 2015 showed:

- a record employment rate of 74.1% in Q4 2015

- the employment rate of women had risen to 69.1% by the end of 2015, a record high

- 74% of the increase in employment in 2015 was driven by full-time workers

- high and medium skill occupations accounted for 92% of the growth in employment in the year to Q4 2015

- a strong demand for labour with 767,000 vacancies in Q4 2015, a record high

- the claimant count fell to a 40 year low in 2015

- working age inactivity fell by over 600,000 from 2010 to 2015

Chart 1.2: International comparison of employment

2.7 Earnings

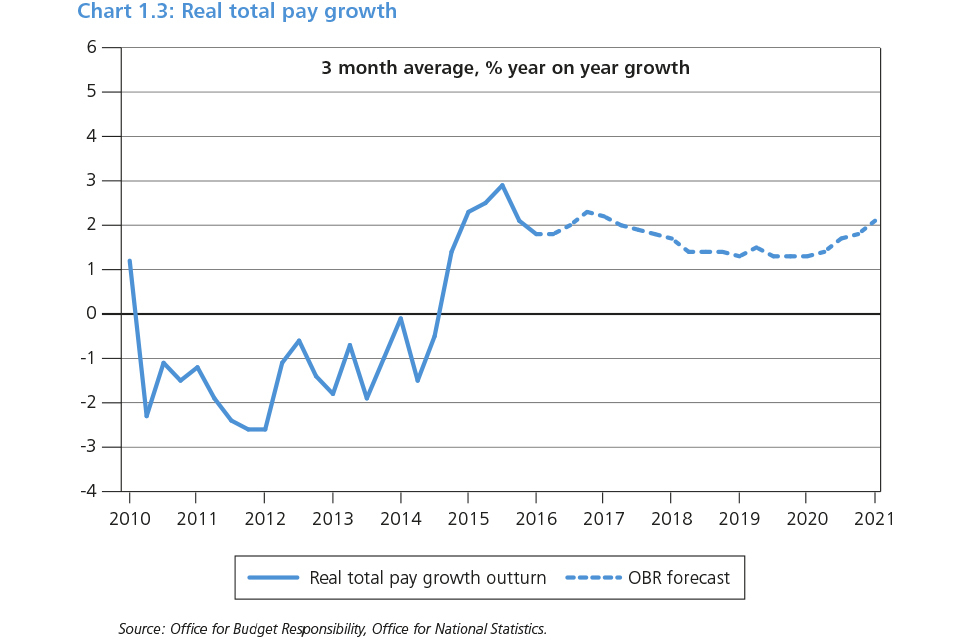

This strong employment performance has been accompanied by rising real wages (see Chart 1.2). Earnings growth picked up in much of 2015, with total annual pay rising 2.5% on the year in nominal terms, and 2.3% in real terms. This represents the highest annual growth in nominal and real earnings since 2008.

Wages had been rising above inflation for 15 consecutive months by the end of 2015. Living standards, as measured by real household disposable income (RHDI) per capita, are expected to have risen in 2015 at their fastest rate in 14 years, driven by rising earnings and low inflation.

The government has taken unprecedented action to support those on lower pay. From 1 April 2016, low wage workers aged 25 and above will see a pay rise as a result of the introduction of the National Living Wage (NLW). Initially set at £7.20, it will mean a £900 cash increase for a full-time worker on the current National Minimum Wage (NMW) – the largest annual increase in a minimum wage rate across any G7 country since 2009, in cash and real terms.[footnote 18] 2.9 million workers are expected to benefit directly, and the OBR estimated up to 6 million could see a pay rise as a result of a ripple effect causing pay to rise further up the earnings distribution.[footnote 19]

Chart 1.3: Real total pay growth

2.8 Long-term solutions to long-term problems

Given the concerns over slowing growth in advanced economies, policymakers face a choice over how to respond. The OBR forecasts little spare capacity in the economy – as measured by the output gap – for the forecast period. This suggests that there is little benefit to policy increasing overall demand without taking measures to expand supply. Attempting to spend more than the country can afford would not address the challenges Britain faces.

In the UK, debt levels remain high. Short-term, discretionary fiscal stimulus would simply increase public debt without expanding supply.

Furthermore, the Monetary Policy Committee (MPC) forecasts inflation to return to the 2% target in the medium term. As the Governor of the Bank of England has recently said, “the G20 needs to use the time purchased by monetary policy to develop a coherent and urgent approach to supply-side policies”.[footnote 20]

The long-term solution is structural reform. These policies seek to make economies more efficient, competitive and productive. Both the IMF and OECD recognise that structural reform is needed to boost long-term growth.[footnote 21] Their research shows that the most effective structural reforms include lowering the rates of distortive taxes, ensuring that product markets are flexible and competitive, and cutting or simplifying business regulation.[footnote 22] These policies are critical to delivering sustainable growth for the next generation.

Since 2010 the government has acted to reform the supply side of the UK economy including by lowering taxes, cutting regulation, investing in infrastructure, and introducing the National Living Wage and Apprenticeship levy. The government set out comprehensive reforms to support productivity growth in ‘Fixing the Foundations: creating a more prosperous nation’.[footnote 23] In October 2015 the National Infrastructure Commission was established to provide the government with expert independent advice on the country’s infrastructure needs.

This Budget announces further measures to drive productivity growth across the UK:

- reducing distortive taxes by continuing to lower both income tax and business taxes

- improving education by accelerating fairer schools funding and committing to full academisation of schools in England

- promoting enterprise through business rate cuts for small businesses, cutting Capital Gains Tax and extending entrepreneurs’ relief to external investors in unlisted trading companies

- delivering long-term infrastructure improvements, by giving the green light to major projects recommended by the National Infrastructure Commission including Crossrail 2, and High Speed 3 between Leeds and Manchester

- improving economic decision-making by devolving power to cities and regions, including new devolution deals for the East and West of England

2.9 Economic rebalancing

The financial crisis of 2008 and 2009 revealed an unstable and unbalanced model of economic growth in the UK. Since 2010 the government has taken steps to support more balanced growth across sectors and regions and to promote savings and investment.

2.10 Sector rebalancing

The UK is making progress in shifting towards high-value added sectors in both manufacturing and services. The manufacturing, construction and service sectors are now all larger than at the beginning of 2010. By the end of 2015, 62.6% of all employment growth since 2010 has been in high skilled occupations. Within manufacturing, aerospace production has grown by almost 30% and car production has increased by over 60% since the start of 2010. Between 2010 and 2014, 16,000 new jobs in car production have been created and in 2015 car manufacturing exports reached a record high.

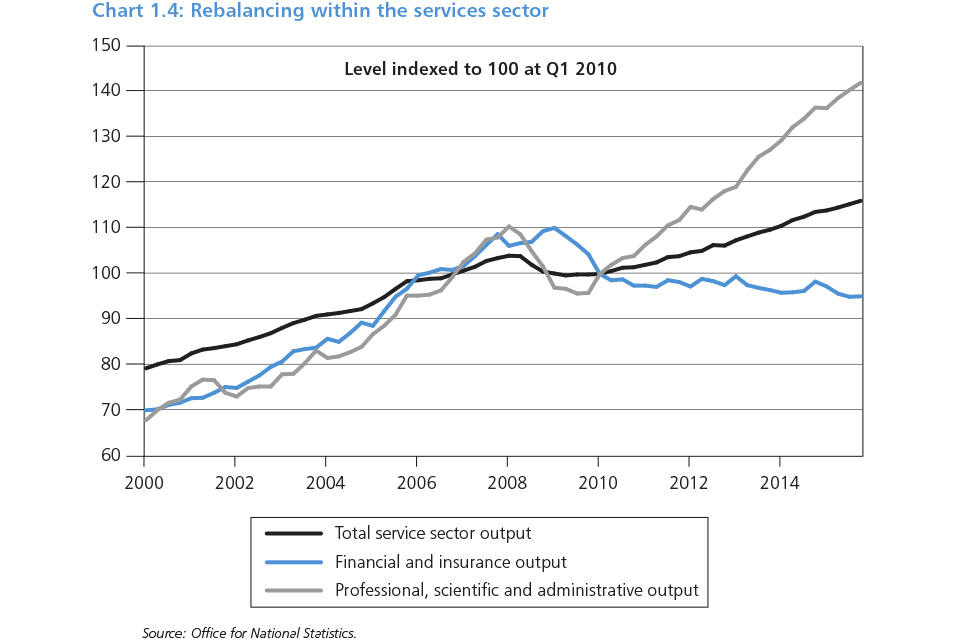

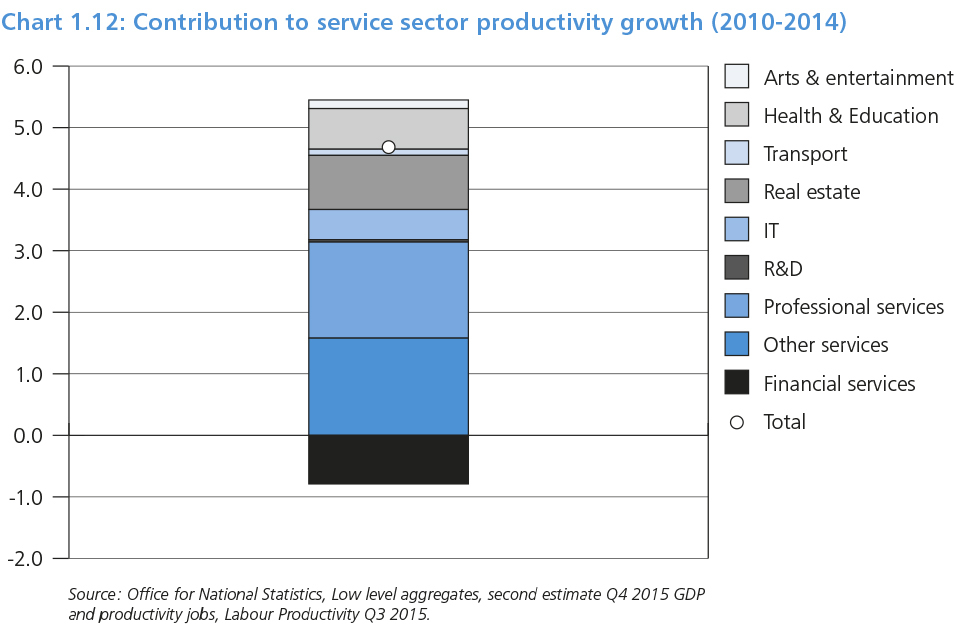

Within services, output has been strong across different high-value added sectors. Scientific research and development has grown by 24.4% and architecture and engineering activities have grown by 42.5% since 2010. Rebalancing within the services sector has been particularly strong.

Chart 1.4: Rebalancing within the services sector

Investment in productive assets, from plant and machinery to software and patents, is vital for a thriving economy. During the financial crisis investment was hit hard in the UK, falling by 24%. Since then it has picked up, and investment grew faster than in any other major advanced economy in 2015 and is forecast by the OECD to continue to increase at the fastest rate in 2016 and 2017.[footnote 24] Business investment has continued to pick up as the economy has recovered, increasing by 25.8% since Q1 2010, more than twice as fast as household consumption. In 2015, business investment increased by 4.7% and it is now 4.2% higher than its pre-crisis peak.

2.11 Regional rebalancing

Regional economic disparities have long been a problem, with London and the South East having higher growth than the UK average for decades. The government is determined to rebalance the economy by building the Northern Powerhouse and the government’s devolution revolution is creating powerful elected mayors, allowing local governments to reduce and retain business rates, and giving local leaders across the country new powers and rewards for driving local growth.

Since 2010, unemployment in the North of England has fallen by a third and the median earnings of full-time employees grew faster in all regions of the North than they did in London.[footnote 25] In 2015, employment grew faster in the North than the South and by the end of 2015, the employment rate in the North was at its highest on record, at 72.2%.

Between 2010 and 2015, labour markets in the regions have performed strongly. Unemployment fell and employment rose in every region, with two-thirds of the increase in employment from outside London and the South East. Labour markets in the regions strengthened in 2015, with every region reaching a record number of people in work.[footnote 26]

In 2015 there were over half a million more businesses outside London and the South East compared to 2010, including nearly 160,000 more businesses in the North and over 95,000 more businesses in the Midlands.[footnote 27],[footnote 28] The South West has had the fastest rate of business growth outside of London.

2.12 External rebalancing

The outlook for world trade continues to be revised down, reflecting both cyclical and structural factors. This weighs on the outlook for UK trade, as the external demand for UK exports is expected to be weaker. In 2015, the sum of UK exports and imports amounted to 57% of GDP, twice the US level. As an open economy, the UK is not immune to developments in the global economy. The OBR have revised down their outlook for UK export markets compared to their November forecast as the inevitable result of lower global growth.

The UK’s current account deficit has narrowed, falling to -3.7% in Q3 2015, but it remains high. This has been driven by a deterioration in the UK’s net investment income. This likely reflects the relatively strong performance of the UK economy compared to its trading partners, which has meant that the income earned on the UK’s overseas assets has been relatively weaker. The current account deficit is forecast to narrow gradually over the forecast period.

2.13 The UK and the EU

On 23 June, the British people will be asked whether they think the UK should remain a member of the EU or leave, in the first referendum on the UK’s membership of the EU since 1975. The government position is to recommend that Britain remains in a reformed EU.

2.14 Economic opportunities and risks linked to the UK’s membership of the European Union

Membership of the EU has increased the UK’s openness to trade and investment, reinforcing the dynamism of the economy. The Treasury has highlighted openness as a key driver of productivity, wages and living standards.[footnote 29] The UK’s full access to the single market, through its EU membership, clearly increases the openness of the British economy, creating jobs and supporting livelihoods.

At the February 2016 European Council, the Prime Minister secured a new settlement for the UK in a reformed EU. The agreement covered four key areas: economic governance; competitiveness; sovereignty; and welfare and free movement. Together, the new settlement and the UK’s existing opt-outs from the single currency and common border-free area give the UK a special status in the EU.[footnote 30]

Voting to leave the EU would create a profound economic shock and years of economic uncertainty.[footnote 31] Such a vote would be the start of a series of lengthy, interlocking negotiations with the EU and with other international partners. The associated uncertainty would have a material effect on jobs, the economy and the public finances. Some of the concerns related to such an outcome are already becoming apparent in financial markets. In their discussion of external analysis of the impact of an exit from the EU the OBR conclude that “Leaving aside the debate over the long-term impact of ‘Brexit’, there appears to be a greater consensus that a vote to leave would result in a period of potentially disruptive uncertainty while the precise details of the UK’s new relationship with the EU were negotiated”.[footnote 32]

The UK’s current full access to the single market cannot be matched by any existing alternative. UK firms and consumers enjoy tariff-free trade and reductions in non-tariff barriers across the EU. The UK is also inside the customs union, eliminating the need for customs compliance for trade between EU member states. None of the alternative arrangements with the EU would provide the same level of access, particularly for services, which accounts for 79% of the UK economy. A new relationship which gives the UK the access to the single market that it needs would involve contributing financially to the EU, accepting the free movement of people and adopting EU rules without having any say over them.

In their discussion of current risks and uncertainties the OBR highlight that “whatever the long-term pros and cons of the UK’s membership of the European Union, a vote to leave in the forthcoming referendum could usher in an extended period of uncertainty regarding the precise terms of the UK’s future relationship with the EU. This could have negative implications for activity via business and consumer confidence and might result in greater volatility in financial and other asset markets”.[footnote 33] The OBR note that, reflecting their statutory remit to prepare forecasts based on current government policy, it is not for them to judge at this stage what the impact of leaving the EU might be on the economy and public finances.

Remaining in a reformed EU will make the UK stronger, safer and better off. It will allow a reformed EU to continue supporting UK productivity. And it will offer certainty for UK businesses and consumers and those foreign firms investing in the UK. As Christine Lagarde, the Managing Director of the IMF has made clear, a vote to leave the EU would create uncertainty in the UK: “no economic player likes uncertainty. They don’t invest, they don’t hire, they don’t make decisions in times of uncertainty.”[footnote 34]

The Treasury will set out a comprehensive assessment of the costs and benefits of membership of a reformed EU in the coming months.

2.15 Monetary policy and credit easing

The steps taken by the government to fix the public finances and put banks and household finances on a surer footing have allowed monetary policy to play an active role in supporting the recovery.

The MPC has full operational independence to set policy to meet the inflation target. Budget 2016 reaffirms the inflation target of 2.0% for the 12-month increase in the CPI, which applies at all times. This target is symmetric, meaning deviations below the target are treated the same way as deviations above the target. Symmetric targets help to ensure that inflation expectations remain anchored and that monetary policy can play its role fully. The government also confirms the Asset Purchase Facility (APF) will remain in place for the financial year 2016-17.

Inflation was 0.3% in January, well below the 2.0% target. In February, as required by the MPC remit, the Governor of the Bank of England wrote to the Chancellor a fifth open letter setting out that the current low level of inflation predominantly reflects the effect of external inflationary pressure, citing falling food, energy and other goods prices as explaining ‘the vast majority of the deviation of inflation from the target’.[footnote 35]

Some measures of banks’ funding costs, in particular the price that banks pay in wholesale markets to fund lending to the wider economy, have increased in recent months. However, they remain much lower than at the time of the launch of the Funding for Lending Scheme (FLS) in 2012. The FLS will continue to support lending to small and medium-sized enterprises (SMEs) until 2018. Annual growth in the stock of lending to SMEs continues to improve, and reached 1.4% in January. This is up from a low of -4.5% in August 2012.[footnote 36] Net lending to SMEs by participants in the FLS extension was also positive for the fourth quarter in a row, at £0.6bn in Q4 2015.[footnote 37]

The government fundamentally restructured the UK’s system of financial regulation in 2013. As part of this, the government created the Financial Policy Committee (FPC) as the UK’s macroprudential authority, within the independent Bank of England. This macroprudential role did not feature in the regulatory architecture before the government took action. The FPC is responsible for identifying, monitoring and addressing risks to the system as a whole. In 2014 and 2015, the FPC undertook stress tests of the UK banking system. The FPC concluded that the UK’s banking system has become more resilient and has the capacity to maintain its core functions, including lending capacity, in these stress scenarios.[footnote 38]

2.16 The government’s fiscal plan

Significant progress has been made since 2010 in fixing the public finances. In 2009-10, the government borrowed around £1 in every £4 it spent. In 2015-16 the government is forecast to borrow around £1 in every £10 it spends and this is expected to reduce to around £1 in every £14 in 2016-17.[footnote 39]

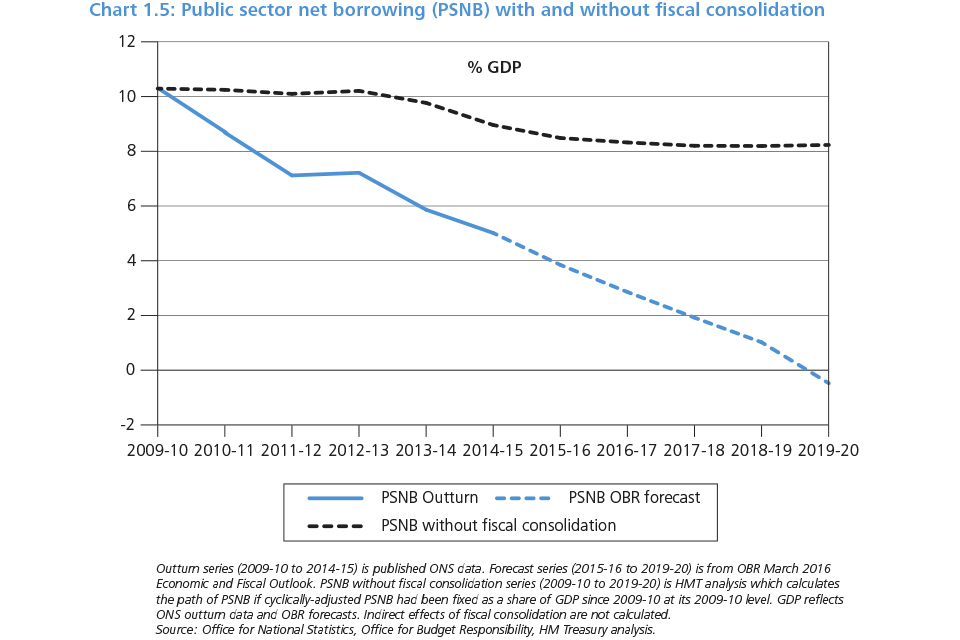

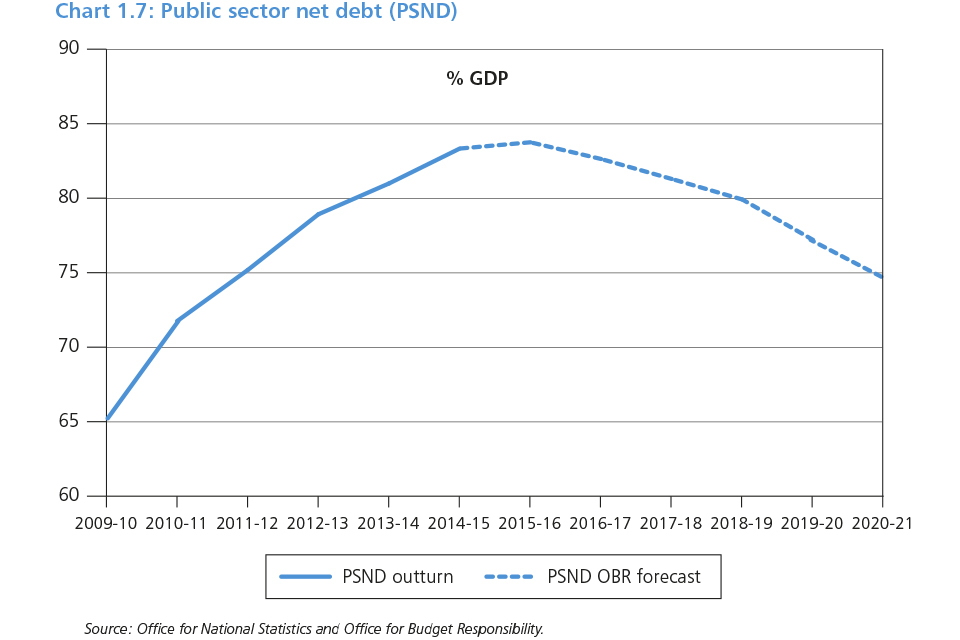

The deficit as a share of GDP is forecast to be cut by almost two thirds from its 2009-10 post-war peak and will reach 3.8% of GDP in 2015-16.[footnote 40] The government has addressed the rapid rise in public sector net debt (PSND) which more than doubled as a share of GDP between 2007-08 and 2011-12. Net debt as a share of GDP is forecast to fall over this Parliament, reaching 77.2% of GDP by the end of 2019-20.[footnote 41]

The public finances would be in a much worse position had the government not undertaken the fiscal consolidation that has occurred since 2010. Analysis in Chart 1.5 shows that the government would have borrowed an additional £930 billion over the period 2010-11 to 2019-20 compared to the outturn and the OBR forecast.[footnote 42] This is calculated as the path of public sector net borrowing if cyclically adjusted public sector net borrowing (the structural deficit) had been fixed as a share of GDP since 2009-10 at its 2009-10 level. The chart shows the cyclical improvement in the economy since 2009-10 which would have reduced public sector net borrowing from its post war peak of 10.3% of GDP. However, the persistence of the structural deficit means that borrowing would have been higher in every year from 2010-11.

Chart 1.5: Public sector net borrowing (PSND) with and without fiscal consolidation

However more work needs to be done – the deficit and debt levels are still too high. The government remains committed to continuing the job of returning the public finances to surplus by 2019-20 and running a surplus thereafter in normal times so Britain bears down on its debt and is better placed to withstand future economic shocks. In a low inflationary environment, with the risk of economic shocks, the only reliable way to bring debt down as a share of GDP is to run a surplus.

This Budget sets out the action the government is taking to meet the fiscal mandate, achieving an overall surplus of £10.4 billion on the headline measure of public sector net borrowing in 2019-20 and a surplus of £11.0 billion in 2020-21.

Table 1.3 sets out the OBR forecast of the key fiscal aggregates at March Budget 2016.

Table 1.3: Comparison of key fiscal aggregates between Budget 2016 and Autumn Statement 2015

| Outturn | Forecast | ||||||

|---|---|---|---|---|---|---|---|

| 2014-15 | 2015-16 | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | |

| Public sector net borrowing (£ billion) | |||||||

| -Budget 2016 | 91.9 | 72.2 | 55.5 | 38.8 | 21.4 | -10.4 | -11.0 |

| -Autumn Statement 2015(1) | 94.7 | 73.5 | 49.9 | 24.8 | 4.6 | -10.1 | -14.7 |

| -Change compared to Autumn Statement 2015 | -2.8 | -1.3 | 5.5 | 14.0 | 16.8 | -0.3 | 3.7 |

| Public sector net borrowing (% GDP) | |||||||

| -Budget 2016 | 5.0 | 3.8 | 2.9 | 1.9 | 1.0 | -0.5 | -0.5 |

| -Autumn Statement 2015(1) | 5.2 | 3.9 | 2.5 | 1.2 | 0.2 | -0.5 | -0.6 |

| -Change compared to Autumn Statement 2015 | -0.2 | 0.0 | 0.3 | 0.7 | 0.8 | 0.0 | 0.1 |

| Public sector net debt (% GDP)(2) | |||||||

| -Budget 2016 | 83.3 | 83.7 | 82.6 | 81.3 | 79.9 | 77.2 | 74.7 |

| -Autumn Statement 2015(1) | 83.1 | 82.5 | 81.7 | 79.9 | 77.3 | 74.3 | 71.3 |

| -Change compared to Autumn Statement 2015 | 0.2 | 1.3 | 0.9 | 1.4 | 2.6 | 2.9 | 3.4 |

| (1) Outturn figures for Autumn Statement are given as estimated at Autumn Statement. |

| (2) Debt at end March. GDP centred on end March.Source: Office for Budget Responsibility and Office for National Statistics. |

| Source: Office for Budget Responsibility and Office for National Statistics. |

At the Summer Budget 2015 and Spending Review and Autumn Statement 2015, the government set out detailed measures to secure a surplus in 2019-20. As a result of the revision in the OBR’s fiscal forecast, the government is taking action to ensure a surplus is still achieved in 2019-20. Table 2.1 shows £14 billion of new measures by 2019-20.

The government is maintaining a balanced pace of deficit reduction, with public sector net borrowing forecast to fall as a share of GDP at the same average annual rate over 2015-16 to 2019-20 as was achieved over 2010-11 to 2014-15.[footnote 43]

2.17 Fixing the public finances and achieving a surplus

2.18 Public spending

The government will build on the measures set out at Spending Review 2015 to deliver a surplus and ensure the sustainability of the public finances. Over the last five years government expenditure was reduced from the unsustainable level of 45% of GDP in 2010-11.[footnote 44] Spending Review 2015 set out savings of £21.5 billion, of which £9.5 billion was reinvested in the government’s priorities. This Budget sets out that the government is adjusting those plans and will find a further £3.5 billion of savings from public spending in 2019-20, in line with continuing action to ensure maximum efficiency from every pound of public spending. This is equivalent to less than 0.5% of total spending, in 2019-20.

Total Managed Expenditure (TME) as a share of GDP will be 37.0% in 2019-20 and 36.9% in 2020-21.[footnote 45] After the public finances move into surplus in 2019-20, total departmental resource spending will grow in line with inflation from 2019-20 to 2020-21. Departmental spending will fall in real terms by an average of 0.9% per annum from 2015-16 to 2019-20, compared to 1.7% from 2010-11 to 2015-16.[footnote 46]

The government has already shown that savings can be delivered from spending while protecting core services and that a well-run state can do more for less – crime has fallen by more than a quarter since 2010, there are more young people going to study full time at university than ever before and record numbers of children are now taught in good or outstanding schools.[footnote 47]

2.19 Delivering further efficiency savings

The Chief Secretary to the Treasury, with the support of the Paymaster General, will lead an efficiency review, which will report in 2018. This will review the efficiency of all departmental spending to inform future expenditure decisions.

The government’s spending priorities remain unchanged. As set out in Spending Review 2015, the defence and overseas aid commitments, the real-terms protections for the NHS in England, schools funding in England, the police and science will be maintained. The NHS has an ambitious programme of work underway to deliver £22 billion of efficiency savings and this is unchanged.

2.20 Sound financial management

The government’s policy is to review the discount rate used to set employer contributions to the unfunded public service pension schemes every 5 years. The discount rate is based on the OBR’s long term projections of GDP growth. Budget 2016 sets out that the recent assessment has resulted in a reduction in the discount rate which will increase the contributions employers pay to the schemes from 2019-20 onward. This will ensure that the costs of providing pension benefits in the future are fairly reflected in the contributions paid by employers, and that the pension promises made today are on a sustainable basis to ensure fairness to future tax payers.

As set out in the Spending Review, the government will continue to meet the commitment to spend 0.7% of Gross National Income (GNI) on Official Development Assistance (ODA) in every year of the Parliament. In line with the commitment, the ODA budget will be adjusted to reflect the latest economic forecasts, taking existing plans into account. The ODA budget will therefore be reduced by £650 million in 2019-20.

At Spending Round 2013, the government announced a control total to limit payments under PFI and PF2 contracts in nominal terms in each future Parliament. The control total is set at £70 billion and the Treasury is on track to meet this target, with forecast cumulative spending from 2015-16 to 2019-20 for payments on all PFI and PF2 contracts funded by central government standing at £51.7 billion.[footnote 48]

2.21 Capital investment

The Spending Review prioritised long term investment over day-to-day spending. This Budget accelerates its commitment to invest £100 billion in infrastructure by 2020-21. The government is now accelerating its investment plans in priority areas to deliver around £1.5 billion investment in areas such as housing, schools and transport over the next three years that would otherwise have taken place at the end of the decade. This will include bringing forward funding for the Highways Maintenance Challenge Fund and the Pothole Action Fund, and enabling the delivery of thirteen thousand shared ownership homes two years early. As set out in Spending Review 2015, capital budgets will be £12 billion higher than planned at Summer Budget 2015.

2.22 Overview of the OBR central fiscal forecast

As a result of the measures the government is taking, the OBR forecast a surplus of £10.4 billion will be achieved in 2019-20. Table 1.4 sets out the OBR forecasts for key fiscal aggregates.

Table 1.4: Overview of the OBR’s central fiscal forecast

| % GDP, unless otherwise stated | ||||||||

|---|---|---|---|---|---|---|---|---|

| Outturn | Forecast | |||||||

| 2014-15 | 2015-16 | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | ||

| Deficit | ||||||||

| -Public sector net borrowing | 5.0 | 3.8 | 2.9 | 1.9 | 1.0 | -0.5 | -0.5 | |

| -Public sector net borrowing (£ billion) | 91.9 | 72.2 | 55.5 | 38.8 | 21.4 | -10.4 | -11.0 | |

| -Cyclically-adjusted net borrowing | 4.3 | 3.6 | 2.7 | 1.9 | 1.0 | -0.5 | -0.5 | |

| -Primary balance | -3.4 | -2.2 | -1.1 | -0.1 | 0.9 | 2.2 | 2.1 | |

| -Treaty deficit(1) | 5.0 | 3.9 | 2.9 | 2.0 | 1.1 | -0.3 | -0.4 | |

| Debt | ||||||||

| -Public sector net debt(2) | 83.3 | 83.7 | 82.6 | 81.3 | 79.9 | 77.2 | 74.7 | |

| -Treaty debt(3) | 87.4 | 88.9 | 88.3 | 87.1 | 85.6 | 83.0 | 80.3 | |

| Memo: Output gap | -0.7 | -0.3 | -0.1 | 0.1 | 0.0 | 0.0 | 0.0 | |

| Memo: Total policy decisions(4) | - | - | 0.0 | -0.4 | -0.2 | 0.6 | 0.2 |

| (1) General government net borrowing on a Maastricht basis. |

| (2) Debt at end March; GDP centred on end March. |

| (3) General government gross debt on a Maastricht basis. |

| (4) Equivalent to the ‘Total policy decisions’ line in Table 2.1. |

| Source: Office for National Statistics, Office for Budget Responsibility and HM Treasury calculations. |

2.23 Performance against the government’s fiscal targets

The Charter for Budget Responsibility was approved by the House of Commons on 14 October 2015.[footnote 49] It defines the government’s fiscal mandate as a surplus on the headline measure of Public Sector Net Borrowing (PSNB) by 2019-20, maintaining a surplus in normal times thereafter. This is supplemented by a target for debt as a share of GDP to be falling in each year until 2019-20. The simplicity and clarity of the metrics ensure that governments will be held to account for their fiscal policy when the economy is performing well.

Under the updated Charter, the surplus rule will be suspended if the economy is hit by a significant negative shock (defined as 4 quarter-on-4 quarter GDP growth below 1%). This provides flexibility to allow the automatic stabilisers to operate freely when needed. Following a shock, the government of the day will be required to set a plan to return to surplus, including appropriate fiscal targets. The framework does not prescribe what the targets should be, allowing the government of the day to respond to the circumstances. However, the targets will be voted on by the House of Commons and assessed by the OBR.

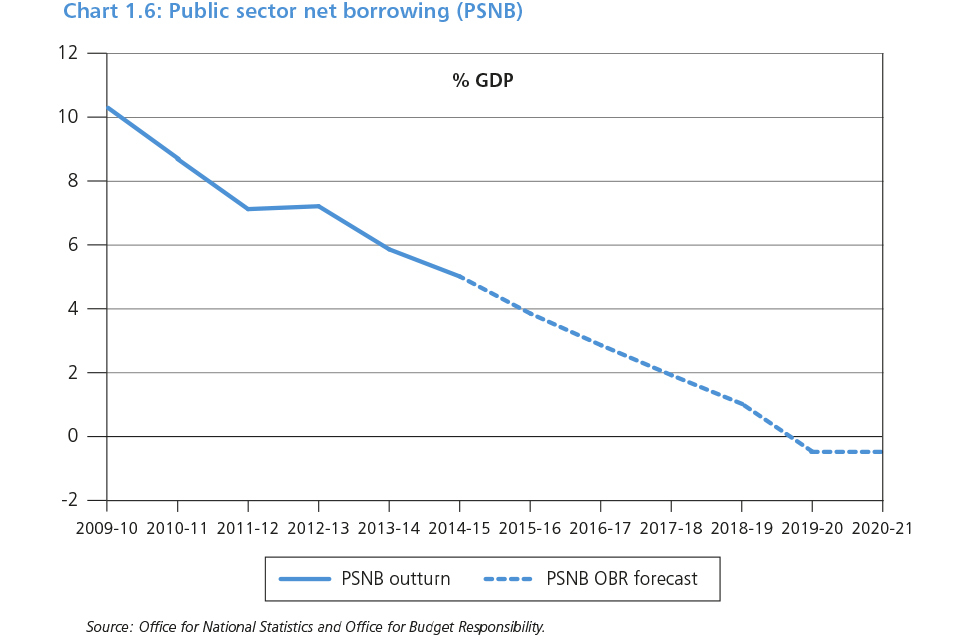

The OBR’s March 2016 ‘Economic and fiscal outlook’ provides an assessment of the government’s performance against its fiscal targets. It confirms the government is on track to meet its fiscal mandate, achieving a surplus of £10.4 billion on the measure of public sector net borrowing in the target year of 2019-20 and to maintain a surplus in the following year, 2020-21.[footnote 50] The OBR’s judgement is that the government’s policies are more likely than not to achieve the mandate in 2019-20.[footnote 51]

Chart 1.6: Public sector net borrowing (PSND)

The fiscal mandate is supplemented by a target for public sector net debt to be falling as a share of GDP in each year to 2019-20. Chart 1.7 shows PSND as a percentage of GDP. Public sector net debt is forecast to fall from 2016-17 to the end of the Parliament, reaching 77.2% of GDP by the end of 2019-20.[footnote 52] The OBR forecasts that the level of cash debt at the end of 2015-16 will be £1591 billion, down from £1599 billion in its November forecast. Debt as a share of GDP is forecast to rise to 83.7% of GDP at the end of 2015-16 because the economy is smaller in nominal terms in 2015-16 than forecast in November, largely due to lower inflation. The government has also delayed the sale of the remaining shares in Lloyds Banking Group as a result of market conditions.[footnote 53]

Chart 1.7: Public sector net debt (PSND)

The government remains committed to bringing the UK’s Treaty deficit in line with the 3% target set out in the Stability and Growth Pact. The OBR’s forecast indicates that this target will be met in 2016-17.

2.24 Welfare Cap

The government introduced the Welfare Cap at Budget 2014 to strengthen control of welfare spending, support fiscal consolidation and improve Parliamentary accountability for the level of welfare spending. The cap applies to welfare spending in Annually Managed Expenditure (AME) with the exception of the state pension and the automatic stabilisers. It is assessed at Autumn Statements.

Summer Budget 2015 and Autumn Statement 2015 announced reforms to ensure that the welfare system is both fair and sustainable. The Welfare Reform and Work Bill legislates for the majority of these reforms. As announced by the Secretary of State for Work and Pensions, the Department for Work and Pensions (DWP) will continue to deliver Personal Independence Payments (PIP) in line with their original intention of supporting claimants with the greatest need in helping them meet the extra costs of their disability or long-term health condition. Spending in 2015-16 on PIP and its predecessor, the Disability Living Allowance, is expected to be over £3 billion higher in real terms than in 2009-10.[footnote 54] Spending on these benefits is forecast to be higher in real terms in 2019-20 than in 2009-10.

The government’s intention is for the cap to be met by the end of the Parliament when the OBR conducts its next assessment at Autumn Statement 2016.

The Charter for Budget Responsibility requires the Treasury to set out the level of the welfare cap in the Budget Report. This is in Table 1.5. OBR forecasts of the level of welfare spending are set out in the ‘Economic and fiscal outlook’, March 2016.

Table 1.5: The welfare cap

| £ billion | |||||

|---|---|---|---|---|---|

| 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | |

| Welfare cap set at Summer Budget 2015 | 115.2 | 114.6 | 114.0 | 113.5 | 114.9 |

| Forecast Margin (2%) | 2.3 | 2.3 | 2.3 | 2.3 | 2.3 |

| Source: HM Treasury |

2.25 Financial sector and other state-owned asset sales

The government is committed to returning the financial sector assets acquired in 2008-09 to the private sector. As there is no longer a policy need for the government to hold these assets, it will seek to dispose of them, reducing PSND while maximising value for taxpayers.

Since 2010, the government has recovered over £75 billion, including further progress in 2015-16 in getting taxpayers’ money back.[footnote 55] This included:

- £2.1 billion from an initial sale of Royal Bank of Scotland (RBS) shares in August 2015[footnote 56]

- approximately £7.5 billion through the continuation of the Lloyds Banking Group trading plan[footnote 57]

- receipt of the final payment of £740 million from the Landsbanki estate in Iceland[footnote 58] and

- a further £5.1 billion in payments received from our holdings in UK Asset Resolution (UKAR).[footnote 59]

Decisions on disposals will be made taking into account market conditions and value for money.

The government is committed to launching a retail sale of Lloyds Banking Group shares and to fully returning its stake to the private sector in 2016-17. UK taxpayers’ money was used to bail out the banks, so it is right to give the public the opportunity to invest in Lloyds Banking Group. The government will shortly receive the final payment from RBS of £1.2 billion for the retirement of the Dividend Access Share (DAS), and it continues to seek further opportunities to dispose of its holding in RBS.[footnote 60] From both the DAS and share disposals, the government expects to raise up to £25 billion from RBS by the end of 2019-20.

Following the recent successful sale of £13 billion of former Northern Rock mortgages, the Treasury, UK Financial Investments (UKFI) and UKAR have been exploring further sales of UKAR mortgages: in particular, a programme of sales designed to raise sufficient proceeds for Bradford & Bingley (B&B) to repay the £15.65 billion debt to the Financial Services Compensation Scheme (FSCS) and, in turn, the corresponding loan from the Treasury.[footnote 61] It is expected that this programme of sales will have concluded in full before the end of 2017-18.

The government is making progress towards achieving a further £5 billion of corporate and financial asset sales by March 2020. The process to transfer the Green Investment Bank to private ownership has begun and the government will shortly consult on options to move the operations of the Land Registry to the private sector. In addition, the government is continuing to pursue the sale of the pre-2012 income contingent repayment student loan book, with a first sale in 2016-17.

2.26 Debt and reserves management

The Official Reserves, which include the government’s foreign currency assets, were $134 billion in February 2016, almost 90% larger than in June 2010.[footnote 62] This reflects a total of £42 billion of additional financing provided for the reserves since 2010 and changes in the market prices of the assets held. The government will provide £6 billion of sterling financing for the Official Reserves in 2016-17.

The government’s financing plans for 2016-17 are summarised in Annex A. They are set out in full in the ‘Debt management report 2016-17’, published alongside the Budget.

3. Support for working people

The Budget puts the next generation first, providing security and opportunity from childhood to working age and through to retirement. This means building an economy based on lower taxes, so that people can take home more of what they earn. It also means investing in education to equip the next generation for the future, tackling childhood obesity and investing in school sports. It means building the housing Britain needs and it means providing the next generation with better incentives to save, and more choice and flexibility as they do so. It means delivering on the government’s aim to reach full employment, increasing wages so that more people are in work and earning more.

The Budget continues to reform public services in a way that is fair. The policies of this government mean that the richest are paying an increasing share of taxes, with those lower down the income distribution continuing to pay less. Distributional analysis published today confirms that half of public spending continues to go to the poorest 40% of households, and that the richest 20% will pay over half of taxes in 2019-20.[footnote 63] In addition, the richest 1% paid over 28% of all income tax revenue in 2013-14 – a higher proportion than in any year of the last two decades.[footnote 64]

3.1 Lower tax society: cutting tax for working people

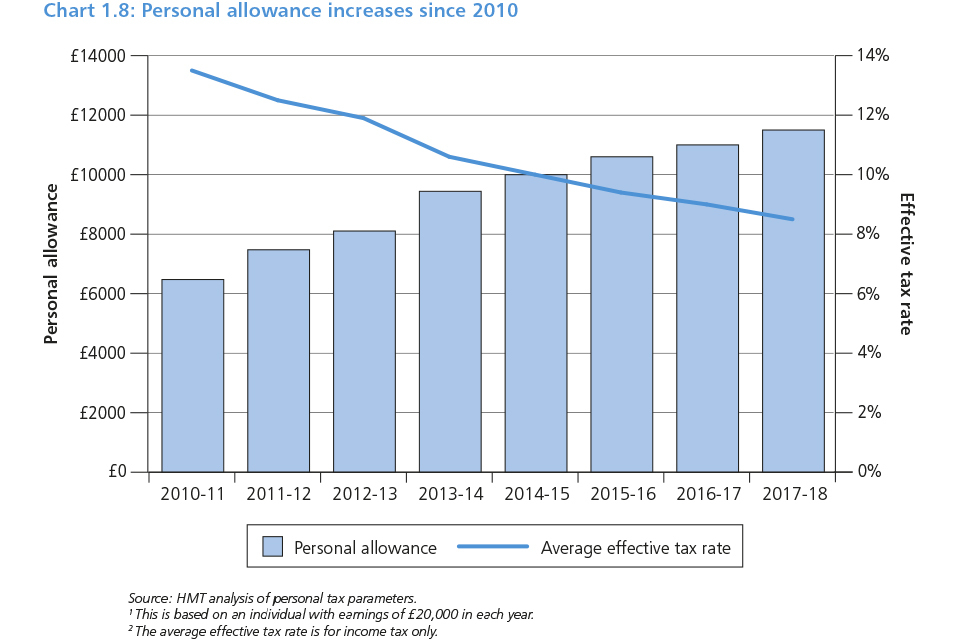

The government is determined to support those in work by continuing to cut taxes and has committed to raise the personal allowance to £12,500, and the higher rate threshold to £50,000 by the end of this parliament.

The personal allowance will be 70% higher in April of this year than in 2010-11.[footnote 65] At Budget 2016, the government takes another significant step towards this commitment, by increasing the personal allowance from £11,000 in 2016-17 to £11,500 in 2017-18. This continues to ensure that no-one working 30 hours per week on the National Minimum Wage (NMW) will pay income tax in 2017-18, and will bring the total number of taxpayers taken out of income tax since the start of this parliament to 1.3 million.[footnote 66] As a result, a typical basic rate taxpayer will pay over £1,000 less income tax in 2017-18 than in 2010-11.[footnote 67]

The government also wants to ensure that the tax system encourages individuals to progress. At Summer Budget 2015 the government announced that the higher rate threshold would rise from £42,385 in 2015-16, to £43,000 in April this year.

This Budget goes further. The government will increase the higher rate threshold by £2,000 to £45,000 in 2017-18. This will be the biggest above inflation cash increase to this threshold since it was introduced by Lord Lawson in 1989.[footnote 68] This delivers the government’s ambition to reverse the trend whereby an increasing number of individuals are faced with paying the higher rate. In 2017-18, there will be 585,000 fewer higher rate taxpayers than at the start of the parliament.[footnote 69]

Chart 1.8: Personal allowance increases since 2010

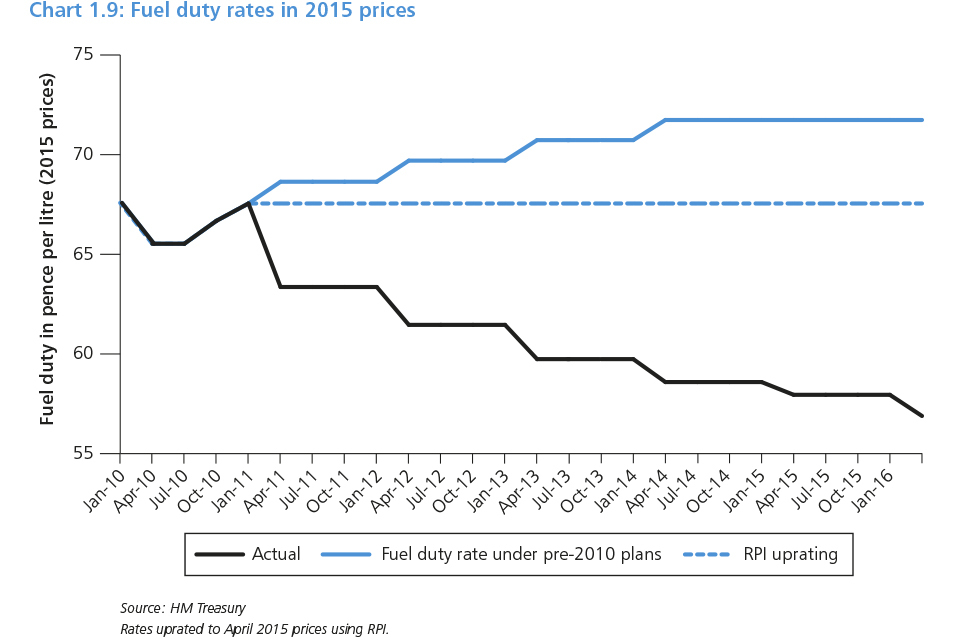

3.2 Freezing fuel duty

Budget 2016 announces that, for the 6th successive year, the government will freeze the main rate of fuel duty at 57.95 pence per litre for 2016-17. This marks the longest fuel duty freeze in over 40 years.[footnote 70] Since Budget 2011, fuel duty has been kept at this level, delivering year-on-year real cuts for motorists. The average driver will save around £75 every year in duty compared to pre-2010 fuel duty escalator plans.[footnote 71] Pump prices are now 18 pence per litre lower than they would have been if the government had maintained pre-2010 fuel duty escalator plans,[footnote 72] and the typical motorist now spends £450 a year less on motor fuel than they did in 2011 when the freeze began.[footnote 73]

Chart 1.9: Fuel duty rates in 2015 prices

3.3 Freezing alcohol duties

Pubs play an important role in their local communities. The British Beer and Pub Association report that beer duty rate changes since Budget 2013 have helped support both pubs and over 19,000 jobs.[footnote 74] To continue this support, the duty rates on beer will be frozen in cash terms this year.

The Scotch whisky industry is a great British success story. Exports are worth around £4 billion a year making up around a fifth of UK food and drink exports.[footnote 75] To continue to support the Scotch whisky industry, the duty rate on spirits will be frozen this year. The duty rates on most ciders will also be frozen this year in recognition of the important role cider makers play in rural communities. Other alcohol duty rates will rise by inflation. Beer and wine duties will continue to be broadly similar.

3.4 Investing in the next generation

3.5 Education

This Budget accelerates the government’s schools reforms and takes steps to create a gold standard education throughout England. The government will:

- drive forward the radical devolution of power to school leaders, expecting all schools to become academies by 2020, or to have an academy order in place to convert by 2022. The academies programme is transforming education for thousands of pupils, helping to turn around struggling schools while offering our best schools the freedom to excel even further

- accelerate the move to fairer funding for schools. The arbitrary and unfair system for allocating school funding will be replaced by the first National Funding Formula for schools from 2017-18. Subject to consultation, the government’s aim is for 90% of schools who gain additional funding to receive the full amount they are due by 2020. To enable this the government will provide around £500 million of additional core funding to schools over the course of this Spending Review, on top of the commitment to maintain per pupil funding in cash terms. The government will retain a minimum funding guarantee

- ask Professor Sir Adrian Smith to review the case for how to improve the study of maths from 16 to 18, to ensure the future workforce is skilled and competitive, including looking at the case and feasibility for more or all students continuing to study maths to 18, in the longer-term. The review will report during 2016

- invest £20 million a year of new funding in a Northern Powerhouse Schools Strategy. This new funding will ensure rapid action is taken to tackle the unacceptable divides that have seen educational progress in some parts of the North lag behind the rest of the country. In support of this, Sir Nick Weller will lead a report into transforming education across the Northern Powerhouse

3.6 Soft drinks industry levy to pay for school sport

Childhood obesity is a national problem. The UK currently has one of the highest overall obesity rates amongst developed countries.[footnote 76] In England 1 in 10 children are obese when they start primary school, and this rises to 2 in 10 by the time they leave.[footnote 77]

The evidence shows that 80% of children who are obese between the ages of 10 and 14 will go on to become obese adults,[footnote 78] and this has widespread costs to society, including through lost productivity and the direct costs of treating obesity-related illness. The estimated cost to the UK economy today from obesity is approximately £27 billion,[footnote 79] with the NHS currently spending over £5 billion on obesity-related costs.[footnote 80]

Sugar consumption is a major factor in childhood obesity, and sugar-sweetened soft drinks are now the single biggest source of dietary sugar for children and teenagers.[footnote 81] A single 330ml can of cola can contain more than a child’s daily recommended intake of added sugar.[footnote 82] Public health experts have identified sugar-sweetened soft drinks of this kind as a major factor in the prevalence of childhood obesity.[footnote 83]

Budget 2016 announces a new soft drinks industry levy targeted at producers and importers of soft drinks that contain added sugar. The levy will be designed to encourage companies to reformulate by reducing the amount of added sugar in the drinks they sell, moving consumers towards lower sugar alternatives, and reducing portion sizes.

Under this levy, if producers change their behaviour, they will pay less tax. The levy is expected to raise £520 million in the first year. The OBR expect that this number will fall over time as the total consumption of soft drinks in scope of the levy drops, in part as a result of producers changing their behaviour and helping consumers to make healthier choices.[footnote 84]

In England, revenue from the soft drinks industry levy over the scorecard period will be used to:

- double the primary school PE and sport premium from £160 million per year to £320 million per year from September 2017 to help schools support healthier, more active lifestyles. This funding will enable primary schools to make further improvements to the quality and breadth of PE and sport they offer, such as by introducing new activities and after school clubs and making greater use of coaches

- provide up to £285 million a year to give 25% of secondary schools increased opportunity to extend their school day to offer a wider range of activities for pupils, including more sport

- provide £10 million funding a year to expand breakfast clubs in up to 1,600 schools starting from September 2017, to ensure more children have a nutritious breakfast as a healthy start to their school day

The Barnett formula will be applied to spending on these new initiatives in the normal way.

3.7 Improving health

The government is committed to investing in the next generation’s health, and will:

- invest £1.5 million in child prosthetics, giving hundreds of children with limb deficiency access to sports prosthetics, and creating a fund to incentivise the development of new breakthrough innovative prosthetic products for the NHS

- tackle the health impacts of smoking, by continuing the tobacco duty escalator, ensuring tobacco duties rise by more than inflation each year in this Parliament. Hand-rolling tobacco is currently taxed at a lower rate than cigarettes. The government will therefore increase the duty on hand-rolling tobacco by an additional 3% above the escalator from 6pm on Budget day

3.8 Apprenticeships

The government is committed to increasing the quality and quantity of apprenticeships, and will deliver 3 million apprenticeship starts by 2020. As announced at the Autumn Statement 2015, an apprenticeship levy will be introduced in April 2017, and employers that are committed to training will be able to get out more than they put in.

From April 2017, employers will receive a 10% top-up to their monthly levy contributions in England and this will be available for them to spend on apprenticeship training through their digital account. The government will set out further details on the operating model in April and draft funding rates will be published in June.

3.9 Lifetime learning, from basic skills to PhDs

The digital revolution is transforming the world of work. As working lives lengthen and jobs change, adults will need more opportunities to retrain and up-skill. This Budget announces that, for the first time, direct government support will be available to adults wishing to study at any qualification level, from basic skills right the way up to PhD. During this parliament, loans will be introduced for level 3 to level 6 training in further education, part-time second degrees in STEM, and postgraduate taught master’s courses.

From 2018-19, loans of up to £25,000 will be available to any English student without a Research Council living allowance who can win a place for doctoral study at a UK university. They will be added to any outstanding master’s loan and repaid on the same terms, but with the intention of setting a repayment rate of 9% for doctoral loans and a combined 9% repayment rate if people take out a doctoral and master’s loan. The government will launch a technical consultation on the detail. Those who take out only a master’s loan will still repay at 6%, as announced at Autumn Statement 2015. The government will also extend the eligibility of master’s loans to include three-year part-time courses with no full-time equivalent.

To promote retraining and prepare people for the future labour market, the government will review the gaps in support for lifetime learning, including for flexible and part-time study. The government will bring together information about the wages of graduates of different courses and the financial support available across further and higher education to ensure that people can make informed decisions about the right courses for them.

The government will continue to free up student number controls for alternative providers predominantly offering degree level courses for the 2017-18 academic year. The best providers can also grow their student places further through the performance pool.

3.10 Supporting people to save for the long term and buy their own home

The government has taken significant steps to support savers. It has nearly tripled the amount of cash that people can save in ISAs and made them more flexible, abolished tax on savings for 17 million people through the introduction of the Personal Savings Allowance,[footnote 85] and given people the freedom to take their pension savings in a way that best suits their needs without being bound by the straitjacket of having to buy an annuity. To further help savers at a time of unprecedentedly low interest rates, the ISA allowance will rise from £15,240 to £20,000 in April 2017.

Since their launch, the Help to Buy: equity loan and mortgage guarantee schemes have helped over 150,000 people to buy a home.[footnote 86] More than 350,000 first time buyers have opened a Help to Buy: ISA with someone signing up every 30 seconds.[footnote 87] Over 45,000 people have bought their home under Right to Buy since the scheme was reinvigorated in 2012.[footnote 88]

The government consultation ‘Strengthening the incentive to save’ looked at the way pensions are taxed.[footnote 89] The consultation found that while the current system gives everyone an incentive to save into a pension, and people like the 25% tax free lump sum, it is also inflexible and poorly understood. Young people in particular are not saving enough, often because they feel they have to choose between saving for their first home and saving for retirement.[footnote 90] Budget 2016 therefore addresses both of these concerns, continuing to prioritise transparency, choice and flexibility for savers.

3.11 A brand new flexible saving opportunity for the next generation

Building on the success of the Help to Buy: ISA, Budget 2016 gives the next generation a brand new opportunity to save in one place for a home and for retirement, and introduces new support for those who find it hardest to save.

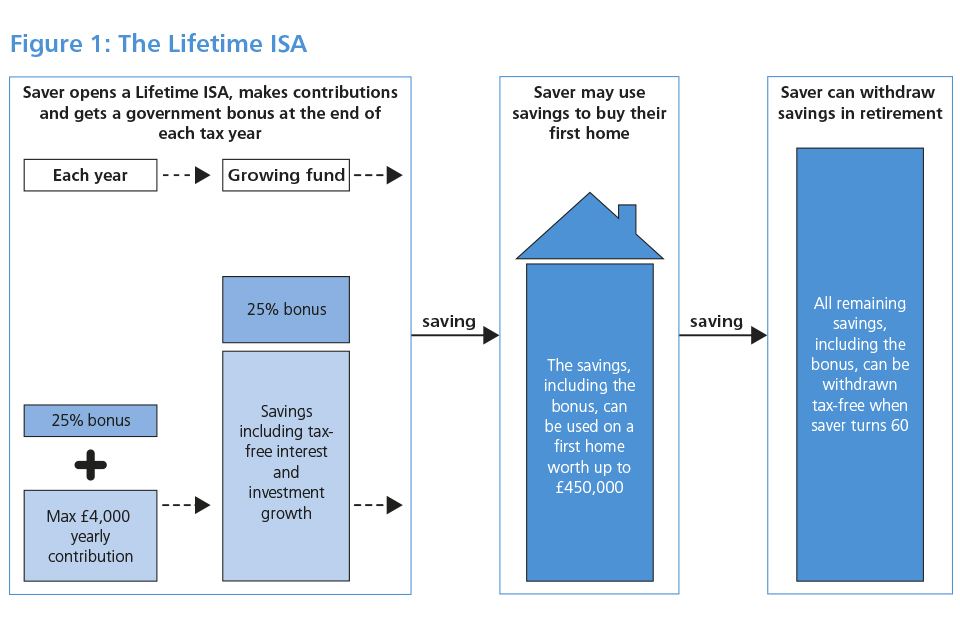

3.12 The Lifetime ISA

The government wants to help young people save flexibly for the long term and ensure they do not have to choose between saving for retirement and saving for their first home. The Budget announces that from 6 April 2017 any adult under 40 will be able to open a new Lifetime ISA. They can save up to £4,000 each year and will receive a 25% bonus from the government on every pound they put in.

Contributions can continue to be made with the bonus paid up to the age of 50. Funds can be used to buy a first home with the government bonus at any time from 12 months after opening the account, and can be withdrawn from the Lifetime ISA with the government bonus from age 60 for use in retirement.

The government will set the limit for property purchased using Lifetime ISA funds at £450,000. This limit will apply nationally. People can continue to open a Help to Buy: ISA until November 2019, as planned. They can also choose to open a Lifetime ISA, but will only be able to use the government bonus from one of their accounts to buy their first home. During the 2017-18 tax year, those who already have a Help to Buy: ISA will be able to transfer the savings they have built up into the Lifetime ISA and still save an additional £4,000.

Whilst this is a product aimed at encouraging saving for the long term, the government understands that circumstances change so wants to ensure that people can access their own money if they need it whilst also keeping an incentive to leave funds invested for the long term. The government will consider whether Lifetime ISA funds plus the government bonus can be withdrawn in full for other specific life events in addition to buying a first home.

The government proposes that savers can make withdrawals at any time for other purposes, but with the bonus element of the fund plus any interest or growth on it returned to the government, and a small 5% charge applied. The government will also explore with the industry whether there should be the flexibility to borrow funds against the Lifetime ISA without incurring a charge if the borrowed funds are fully repaid. In the US some retirement plans allow 50% to be borrowed up to a maximum of $50,000. Further details on the Lifetime ISA are set out in the document published alongside Budget.

Figure: The Lifetime ISA

3.13 Help to Save

To help the people who find it hardest to save, the government will introduce a new Help to Save scheme for those on low incomes who wish to regularly set aside some of their income. The scheme will be open to 3.5 million adults in receipt of Universal Credit with minimum weekly household earnings equivalent to 16 hours at the National Living Wage, or those in receipt of Working Tax Credit.[footnote 91] It will work by providing a 50% government bonus on up to £50 of monthly savings into a Help to Save account. The bonus will be paid after two years with an option to save for a further two years, meaning that people can save up to £2,400 and benefit from government bonuses worth up to £1,200. People will be able to use the funds in any way they wish.

3.14 Understanding pension savings

As people work longer and change jobs more often, pension savings can become confusing. The average person will move employers 11 times over their working life, meaning they could end up with 11 or more private pensions by the time they retire.[footnote 92] Research shows that over a third of people approaching retirement find it difficult to keep track of their pension pots.[footnote 93] To help the next generation to clearly view their pensions savings, the government will ensure the industry designs, funds and launches a pensions dashboard by 2019. This will mean an individual can view all their retirement savings in one place.

3.15 Financial advice