Accounts monitoring review: Do charity annual reports and accounts meet the reader’s needs?

Published 3 September 2018

© Crown copyright 2018

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/accounts-monitoring-charities-annual-reports-and-accounts-meeting-the-readers-needs/accounts-monitoring-review-do-charity-annual-reports-and-accounts-meet-the-readers-needs

Why are we reviewing charities’ accounts?

We are reviewing charities’ sets of accounts because they are the prime means by which the trustees are publicly accountable to donors, beneficiaries and the wider public for the charity’s activities and how they have used the charity’s money. Good reporting is important to public trust and confidence in both the reporting charity and the wider charity sector.

All registered charities with an annual income over £25,000 are required to file the following documents with us within 10 months of their financial year end:

- their trustees’ annual report (annual report)

- their accounts

- the report of an independent scrutiny of their accounts

Approximately 38% (64,000) of the charities on our register have incomes over £25,000 and they account for 99% of the sector’s income.

How do we assess whether accounts meet the needs of readers?

The focus of our assessment was on whether each set of accounts met the basic requirements of the users of those accounts rather than on strict technical compliance with the Charities’ Statement of Recommended Practice (SORP) and other reporting requirements. We based our view of the user’s requirements on the Populus survey of public trust and confidence (June 2016). Since we carried out our review, the results of the 2018 public trust and confidence research have been published (July 2018). In both surveys, Populus found that ‘ensuring that a reasonable proportion of donations make it to the end cause’ and ‘make a positive difference to the cause they work for’ remain the most important factors driving public trust and confidence in charities.

This led us to focus on the following criteria:

- have the trustees filed all of the required documents that make up a set of accounts (the annual report, independent scrutiny report and the accounts) and do they provide a consistent picture of the charity’s activities?

- does the annual report explain what activities the charity had carried out during the year to achieve its purposes?

- have the accounts been prepared on the correct basis depending on the charity’s income and type, either receipts and payments or accruals accounts (also known as SORP accounts)? Also, do the accounts contain both a statement of financial activities (SOFA), which analyses the charity’s expenditure, and a balance sheet that are consistent with each other (or the equivalent if receipts and payments accounts were prepared)?

- have the accounts been subject to the required level of independent scrutiny depending on the charity’s income and gross assets, either an audit or an independent examination? How did we carry out the review?

In April 2017, we selected a random sample of 106 charity annual reports and accounts from the register of charities, covering accounting years ending during the 12 months to 31 December 2015. We did this because we base our published information about charities and accounts on the annual return cycle and AR 2015 was the most recent complete cycle at the time we selected the sample. In previous years, we sampled from accounting years ending on 31 March and so there is an overlap with last year’s review, which covered the 12 months ending 31 March 2015. The sample size means that our findings are statistically representative of the accounts filed with us for this period. However, as with all samples, there is a margin of error.

What did we find?

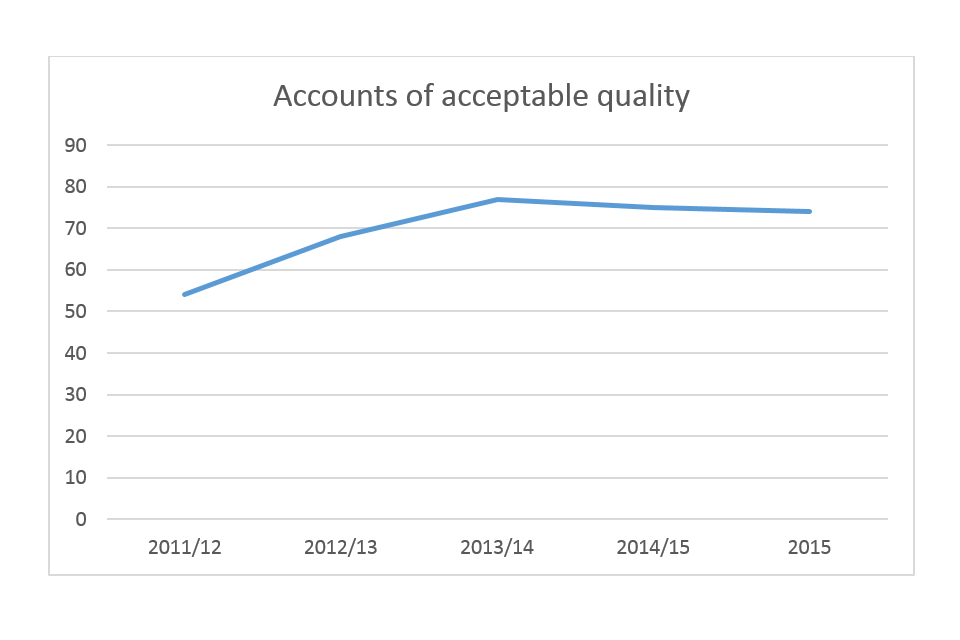

Graph showing the percentage of accounts of acceptable quality: around 54% in 2011-12, 68% in 2012-13, 78% in 2013/14, 75% in 2014-15 and 74% in 2015

74% of the accounts that we reviewed were of acceptable quality, in other words they met the basic standard that we had set. This continues the pattern seen in the last two surveys, which also found that approximately three quarters of submissions were of acceptable quality. The reasons why the other sets of accounts submitted failed to meet the basic standard may be summarised as follows:

- one of the required documents was missing (5% of charities)

- the annual report was inadequate, mainly because it provided little or no information on the charitable activities carried out (11% of charities)

- the independent scrutiny report was inadequate, mainly because the wording of the report demonstrated that the person carrying out the scrutiny was not familiar with the independent examination requirements (5% of charities)

- the accounts were inadequate, mainly because they were incomplete or did not balance (5% of charities) In some instances, the inadequacies may have been the result of an incomplete submission, for example where page numbers were missing from the sequence

In some instances, the inadequacies may have been the result of an incomplete submission, for example where there was a contents page that listed documents or pages that were not present.

What action did we take?

We have reviewed the following year’s accounts for 26 of the 28 charities that did not submit accounts of acceptable quality. Of the other 2 charities, one no longer needs to file because its income is now less than £25,000 and the other is now in default of its filing duties. The action that we have taken as a result is as follows:

- no further action is required (9 charities), usually because the more recent accounts submitted are of acceptable quality

- providing guidance to the trustees (17 charities), where the areas for improvement are such that the guidance should enable the trustees to be able to prepare future sets of accounts to an acceptable standard

- requiring action from the trustees (2 charities), where the most recent accounts contain serious deficiencies and need to be corrected and resubmitted. This includes the charity that is in default

What are the lessons for other charities?

It is a statutory requirement to prepare an annual report and accounts and arrange for them to be subject to independent scrutiny, if required. The annual report and accounts provide an important opportunity for the trustees to take stock of what the charity has achieved over the last year and to demonstrate to the charity’s supporters, potential funders and the public that they have managed its resources effectively and are meeting its objectives.

We have produced guidance to assist trustees on the preparation of their charity’s annual report and accounts. This includes pro-formas of both the annual report and the accounts. These provide a useful structure for preparing documents that meet the reporting requirements. Our guidance can be downloaded from GOV.UK.

We also recommend that the person responsible for submitting the charity’s accounts checks that the final version of all three of the required documents are included and that no pages are missing.

About our accounts monitoring reports

Charities’ accounts are publicly available on GOV.UK. Each year, we develop a programme of reviews, based on issues of regulatory concern. We are publishing a series of reports on our findings, which will help trustees to manage the risks that their charity faces, improve reporting standards and enhance the accountability of charities to their donors, beneficiaries and the public.