Prevent. Resolve. Improve. 2026-2030 Government Debt Management Strategy (HTML)

Updated 20 March 2026

© Crown copyright 2026

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/prevent-resolve-improve-26-30-government-debt-management-strategy/2023-26-government-debt-strategy-html

Foreword

Every year, people and businesses pay what they owe to government – taxes, fees and charges, loan repayments, and the return of benefit overpayments – helping to fund the public services we all rely on, from health and welfare to policing and schools. When payments are missed and debt is owed, it is right that government recovers what is due: to protect our public finances, maintain confidence in the fairness of our systems, and ensure those who pay on time are not disadvantaged.

But we know that debt can also be a source of acute hardship. If it is not managed well, it can deepen financial difficulty for households, contribute to business failure and hamper economic growth which ultimately costs the taxpayer more.

The 2026-2030 Government Debt Strategy: Prevent, Resolve, Improve sets out how we will make the management of debt owed to government more consistent, transparent and fair. Government must be an effective creditor – robust in tackling non-compliance, including fraud and criminality, while acting fairly and proportionately. This means supporting those in vulnerable circumstances, taking account of what is genuinely affordable, and helping to prevent financial difficulties from escalating.

This strategy has been developed with colleagues across central and local government, alongside experts from the debt advice sector and the wider debt management industry. This collaboration is essential to designing approaches that work in practice and reflect the realities people face. Through the strategy we refresh our collective ambition for 2026-2030 around three priorities: preventing avoidable and problem debt; resolving debt to clear standards – pursuing those who avoid repayment and taking robust action where fraud or criminality is involved; and improving capability through stronger data, digital tools and professional leadership for the 8000 public servants working in debt management so that our approach is efficient, modern and fair.

I look forward to working with colleagues and partners to deliver fair debt outcomes and protect public money for the services people depend on.

Lucy Rigby KC MP

Economic Secretary to the Treasury

Background

About the Government Debt Management Function

The Government Debt Management Function (GDMF) comprises around 8,000 public servants who work across 40 ministerial departments and arms-length bodies (ALB). Together we recover over £100 billion every year which is used to pay for vital services that the public rely on, such as health, welfare and education.

Debt is owed to government by both people and businesses for a wide range of reasons including unpaid taxes, benefit overpayments, loans, business supplies, staff overpayments, fees, fines and penalties to debt arising from fraud or criminal activity. While most government debt is money owed directly to government, some – such as child maintenance and certain court-imposed debt – is collected by government on behalf of others.

Each department and ALB has its own policies, approaches and, in many cases, legislation for how they manage debt. This will set out any legal and regulatory requirements that are specific to the debts involved. Underpinning this are common standards, practices and skills that define good debt management, which government aims to demonstrate consistently. The centre for the function, based in HM Treasury, supports this work and provides expertise and strategic leadership to improve the management and resolution of all debt handled by government.

How the function approaches debt management

Ensuring that people or businesses are paying or repaying what is due to government is essential to protecting public finances and supporting confidence in our systems. When debt arises, we seek to deal with it efficiently, effectively and fairly. Collecting money owed to government, or recovered by government on behalf of others, ensures more funding available for public services, reduces pressure to increase borrowing or taxes, and makes sure that no one is better off by failing to pay what they should.

We also recognise that debt can have serious social costs, including poorer health, family breakdown, homelessness and business failure which puts additional pressure on people, businesses, public services and communities and hampers economic growth. As a responsible creditor, government seeks to recover debts in ways that are sustainable - helping people and businesses return to financial stability – while also delivering value for money for taxpayers and ensuring wider public value. Where needed, enforcement action is used. And where debts result from fraud or criminal activity, we pursue them rigorously and to the full extent necessary to protect public money and uphold confidence in the system.

What the function has achieved

Since the launch of the government’s first public Debt Management Strategy in 2023, progress has been made in improving debt resolution practices and reducing silos across departments. The focus has been on achieving fair debt outcomes for all. This means acting in a way that is fair to people and businesses who pay on time, taking a firm approach where debts are not paid or where fraud or criminality are involved, and supporting those who are vulnerable or need additional help. Progress has focused around three broad areas:

Preventing avoidable and problem debt:

- Launched the Debt Fairness Charter setting out a clear, common approach to how people repaying debts to government can expect to be treated.

- Introduced toolkits and training on vulnerability and economic abuse supporting wider government work on child poverty and violence against women and girls.

- Started to align affordability approaches across government with standards used by other major creditors.

Resolving debt to agreed standards:

- Published and embedded updates to the Debt Functional Standard and Continuous Improvement Assessment Framework (CIAF) to drive improvements, with 19 departments now assured, representing 95% of the overdue debt balance.

- Issued guidance on priority areas such as debt communications and staff overpayments to drive more consistent practice.

- Piloted data sharing across government, indicating a 15% increase in debt resolved and better identification of vulnerable cases, laying foundations for wider roll-out.

- Around £350 billion has been recovered by organisations across government over the lifetime of the strategy, with a steady growth in the proportion of debt recovered though repayment plans, from 23% to 27%.

Improving government capability:

- Established Debt Management as a recognised Civil Service Profession and created a cross‑government community, with the Debt Centre of Excellence now supporting around 1,000 members in nearly 40 organisations.

- Developed new tools to improve recruitment, retention and skills including interactive training and the Debt Skills Assessment Tool (with over 900 completions to date).

- Supported 15 organisations, covering 91% of the overdue debt balance, to develop strategic approaches to debt management.

- Automated data collection and analysis to give a clearer view of risks and trends across the system.

These achievements show a cross‑government community that is becoming more professional and joined‑up, with strong foundations in place to meet future challenges.

Where we are now and looking ahead

Our first public strategy provided a common framework for how all government organisations approach debt, with departments mirroring the approach and ambition in their own strategies. Practice has improved, but the current debt picture shows there is more to do together: preventing avoidable and problem debt, resolving debt to clear standards, and improving government’s capability in debt management.

The landscape around us is changing, and our practices must continue to pre-empt, adapt and evolve to respond to this. Public finances are constrained, so every pound lost through non‑payment, fraud or error – or spent on debt recovery – makes it harder to fund the services people rely on.

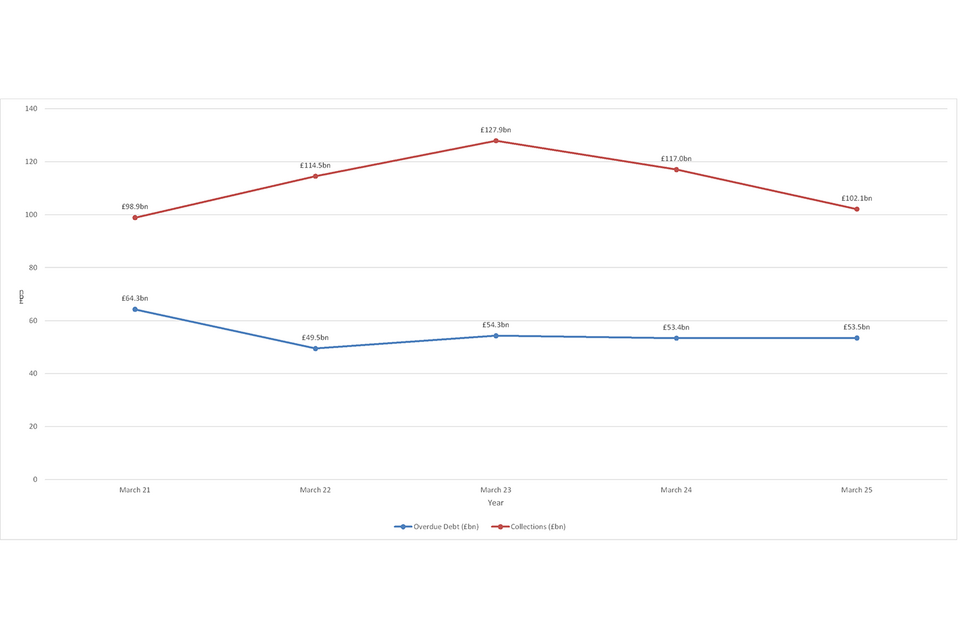

At March 2025, total overdue debt stood at £53.5 billion, with recoveries of £102 billion over 2024/25. This is down from a peak overdue debt balance of £64.3 billion during the pandemic, when government provided essential financial support and paused regular collection activity. This pause led to more aged debt, which is typically harder and more expensive to resolve.

Figure 1. The overdue debt balance owed to government and total collections from March 2021 to March 2025.

The wider environment is also challenging. Higher living costs mean some people and businesses are finding it harder to keep up with regular bills and repay what they owe. At the same time, improvements in data sharing and analytics mean more fraud, error and non-compliance are being identified, which increases the volume of debt needing recovery and requires more intensive action, including the use of new powers such as those in the Public Authorities Fraud, Error and Recovery (PAFER) Act and HMRC’s Direct Recovery of Debt. Policy changes to make repayment more sustainable are also lengthening repayment periods, affecting the pace of recoveries in some areas. And new forms of debt are arising – sometimes intentional as is the case with loans – that bring new considerations.

Continued investment in debt management has helped increase recoveries and bring more debt into repayment plans, a trend that is expected to continue. Digital and data innovation – including self‑service technologies, automation, data analytics and generative AI – is already transforming how we work. These tools offer better insight, reduce administrative effort and improve user experience, enabling earlier engagement, more tailored approaches and greater use of self‑service.

Across government there is a growing focus on preventing avoidable and problem debt from arising, where debt is not an intentional and necessary product of policy. Problem debt imposes unnecessary costs on the public sector, strain on households and businesses and wider social costs. Better policy design, clearer payment approaches, earlier intervention and sustainable repayment plans – especially for those in vulnerable circumstances – all have a role to play. At the same time, government remains committed to resolving outstanding debt in the most efficient and cost‑effective way, including exploring new approaches to collect harder‑to‑recover debt and debt owed by those who do not engage.

The centre of the function continues to support this change as the debt management community evolves. Departments increasingly seek proactive advice, cross‑government insight and strategic challenge, including on new or emerging types of debt, professionalisation and assurance against standards. With debt management established as a formal civil service profession since June 2025, and greater investment in this area, the complex and unique skills involve in debt resolution are now fully recognised. The next challenge is to work with departments to grow and deepen this expertise, agree clear professional standards, and build capability through targeted learning and development and improved use of technology.

Our Vision

We are collectively looking to build on the progress that has been made across the GDMF through our 2026-30 strategy. The strategy renews the focus on achieving our vision of fair debt outcomes by:

-

Preventing avoidable debt upstream and reducing the number who fall into problem debt;

-

Resolving debt to clear standards, pursuing those who avoid repaying and enforcing recovery where appropriate; and

-

Improving government’s capability to resolve debt efficiently, effectively and fairly.

We will support this work by strengthening the centre’s activity in four key areas:

- Focusing more intensely on building a professional, skilled and thriving debt management community across government and the wider public sector;

- Putting data-led approaches at the heart of what we do, including on cost-efficiency metrics and fairness, to better understand risks across the system;

- Better distinguishing how we manage and support different types of debt, and departments with smaller debt books;

- Maximising the links with operational delivery and finance functions and professions across government.

Objectives

1. Prevent

Prevent avoidable debt upstream and reduce the number who fall into problem debt.

Debt creates costs for government, taxpayers, businesses and individuals. In some cases debt is an intentional and necessary consequence of policy, such as loans that support investment in skills, infrastructure or business growth and raise long‑term incomes. But debt can also arise through poor policy design or error. And where people are vulnerable or face affordability challenges, poor debt management can worsen their financial hardship. Debt should be collected at the lowest cost to the taxpayer, but it is far more efficient, and fairer, to prevent unintended debt arising in the first place. Better policy design, clearer payment approaches and early engagement, both before debt arises and at the first signs of difficulty, can stop people and businesses falling into problem debt and reduce the amount of aged debt government must manage.

Our aim for this strategy is to design out debt where possible, improve early engagement and support people who are vulnerable from falling into problem debt. This supports the Government’s efforts through the Financial Inclusion Strategy to tackle problem debt.

We will:

1. Seek to design out avoidable debt by:

- Embedding debt risk identification and prevention into new policy design in order to prevent avoidable debt from occurring at the earliest opportunity.

- Supporting the development of policy approaches and payment systems that encourage people to pay on time and provide flexibility.

2. Improve early engagement by:

-

Promoting the use of predictive technology to enable government to support people and businesses early and prevent them falling into problem debt.

-

Growing opportunities for contact through design, communications and different channels at earlier stages in payment and debt resolution.

3. Support people who are vulnerable by:

- Developing clearer channels between government and specialist support organisations.

- Exploring opportunities to support people to budget and maximise their income as part of the debt resolution process.

2. Resolve

Resolve debt to clear standards, pursuing those who avoid repaying and enforcing resolution where appropriate.

Successful debt resolution is increasingly underpinned by timely data, enhanced analytics and tailored approaches. While parts of government are forging ahead and more debt is now going into repayment plans, there is further to go. The stock of aged debt also highlights that some debt remains hard to resolve, requiring more bespoke changes to repayment terms, rescheduling, enforcement activity or fair remission processes. This may also be the case where debt is complex or novel. And where there is non-engagement or debt arises from fraud or criminal activity with no intent to repay, there is an imperative to take a firm and robust approach to recovery, and ensure government has the right tools to address this.

Over the strategy period, we will promote more tailored approaches to recovery, support the resolution of harder-to-collect debt and improve systems for multiple and complex debts.

We will:

1. Promote tailored approaches by:

- Creating a stronger culture of gathering, maintaining, validating and using data, including from third parties, to inform communications and collections strategies.

- Maximising data-sharing between government organisations, enabling better identification and targeting of activities.

2. Support the resolution of hard-to-collect debt by:

- Enabling consistent decision-making to support effective enforcement and, where necessary, fair write-off and remission practices.

- Ensuring debt resolution powers and legislation are relevant, fit for purpose and fair.

3. Improve systems for multiple and complex debts by:

- Understanding where businesses, people and public sector or charitable bodies owe complex or multiple debts to government, including intra-governmental debt;

- Ensuring that the sequence in which debts are recovered is fair and proportionate.

- Establishing greater consistency in understanding ability to pay.

3. Improve

Improve government’s capability to resolve debt more efficiently, effectively and fairly.

Improving government’s overall capability in managing debt is a key pillar of our strategy. Our vision is to improve skills and expertise among Government Debt Management professionals. We want to recruit, develop and retain debt specialists, demonstrating leading practice in ensuring the delivery of high-quality debt services while ensuring existing Government Debt Management staff – whether in finance, customer-facing, assurance, specialist or management roles – are supported in their work. Digital and data capability are also key to effective, efficient and fair debt management, providing Government Debt Management professionals with the tools to deliver.

Over the course of the strategy, we will accelerate work on strengthening the profession and community, support innovation and continue to drive up standards in line with other creditors.

We will:

-

Strengthen debt capability and expertise by developing a joined-up consistent Government Debt Management profession induction, comprehensive career framework, training offer, mentoring and recognition programmes.

-

Build a motivated and skilled debt management community within government and the wider public sector through networks, training and sharing good practice and standards.

-

Improve innovation in government debt management by promoting and expanding access to digital tools, including the use of AI and analytics, while closing maturity gaps across government.

-

Raise standards and consistency in debt practices, debt forecasting and use of metrics that drive efficiency and fairness.

-

Build stronger partnerships with the private sector and the Government Commercial Agency to support innovative debt resolution approaches, share good practice, deliver social value and ensure consistent standards.

-

Develop debt-specific approaches to support the requirements of different types of debt such as commercial, personal, overpayments, tax, fees and charges and intra-government debt.

Delivering the strategy

This strategy will be implemented over a 4-year period by the GDMF functional centre, working together with debt-holding government organisations and with input from stakeholders from the wider debt sector, beyond government.

The functional centre will deliver key activities which underpin the strategy including:

- Maintaining the cross-government governance and management framework;

- Reviewing and updating the cross-government debt strategy;

- Co-ordinating the debt management profession, training and capability activity;

- Assuring and further developing the debt functional standard;

- Gathering, analysing and reporting key cross-government debt metrics;

- Communicating good practice across government using networks and channels;

- Providing expert advice and support to organisations;

- Maintaining stakeholder relationships with the debt and wider public sector through the Fairness Group, with a view to keeping standards high in debt management.

We will support this by strengthening the centre’s focus in four key areas:

- Focusing more intensely on building a professional, skilled and thriving debt management community across government and the wider public sector;

- Putting data-led approaches at the heart of what we do, including on cost-efficiency metrics and fairness, to better understand risks across the system;

- Better distinguishing how we manage and support different types of debt, and departments with smaller debt books;

- Maximising the links with operational delivery and finance functions and professions across government.

We will work with our senior decision-making board, the Debt Management Leadership Group (DMLG), to provide oversight for the work; developing actions, establishing relevant metrics and monitoring progress. This will be reviewed annually to ensure it is on track, with any changes endorsed by DMLG.

For more information, please contact the Government Debt Management Function: gdmfcentre@hmtreasury.gov.uk.