Implementing the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA)

Updated 28 April 2021

© Crown copyright 2021

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/consultations/implementing-the-carbon-offsetting-and-reduction-scheme-for-international-aviation/implementing-the-carbon-offsetting-and-reduction-scheme-for-international-aviation-corsia

Executive summary

The UK recognises the importance of international action to tackle emissions from international aviation and has been instrumental in agreeing and developing a global offsetting scheme – the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) – aimed at meeting the International Civil Aviation Organization’s (ICAO’s) medium-term climate change goal of Carbon Neutral Growth from 2020 (CNG2020).

As a contracting state of ICAO, the UK is obliged to implement the ICAO International Standards and Recommended Practices, Annex 16, Volume IV(‘CORSIA SARPs’) in its national law. CORSIA implementation can be split into 2 parts, according to the obligations CORSIA imposes on aeroplane operators.

The first part is the monitoring, reporting and verification of CO2 emissions (known as MRV) and the second part is the offsetting of CO2 emissions. We propose to implement CORSIA into UK law as an Air Navigation Order (ANO) under Section 60 of the Civil Aviation Act 1982.

The first section sets out the policy context and outlines our proposed approach.

The second section covers the detail of the CORSIA MRV provisions, including how the scheme will be administered in the UK and how CO2 emissions from both fossil kerosene and CORSIA eligible fuels (CEF) should be monitored, reported and verified. Enforcement provisions for those who do not comply with the scheme are also covered. These MRV provisions constitute the first statutory instrument (SI) (PDF, 966KB) for CORSIA. A copy of the draft SI (PDF, 967KB) is published alongside this consultation.

The second SI, which will be consulted on next year, will cover the second part of CORSIA implementation (the offsetting requirements) and the aim is for this SI to come into force by spring 2022. The design of this part of the policy will need to take into the UK Emissions Trading Scheme (UK ETS) as legislated for through the Greenhouse Gas Emissions Trading Scheme Order 2020 (‘the UK ETS Order’).

The third section of this consultation document therefore includes high-level options for implementing CORSIA alongside a UK ETS and invites initial views. Taking into account the responses to this consultation, there will then be a second consultation in 2021 on the detailed policy design of any interaction between the 2 schemes.

Consultation questions

Section 2

Q1 Do you agree with the overall approach taken to the implementation of CORSIA MRV in the UK, through the draft Air Navigation Order (PDF, 967KB) which is based closely on the CORSIA SARPs, supplemented by provisions from the UK ETS Order where necessary? If not, please explain why.

Q2 Do you agree with the specific provisions contained in the draft Air Navigation Order and summarised here? If not, please explain why.

Q3 Is there anything that should additionally be included in the draft Air Navigation Order? If so, what?

Section 3

Q4 Do you agree that Option 2 (Supply-Adjusted Hybrid) should be preferred over the other options described in this chapter? If not, please explain why.

Q5 Do you have any suggestions for how the preferred option could be implemented, including minimising administrative complexities? If so, please explain.

Q6 Are there any further options that you believe should be considered? If so, please explain.

How to respond

The consultation period began on 18 January 2021 and will run until 28 February 2021. Please ensure that your response reaches us before the closing date. If you’d like further copies of this consultation document, it can be found on GOV.UK or you can contact corsiaconsultation@dft.gov.uk if you need alternative formats (for example, Braille, audio or CD).

Please send consultation responses to: corsiaconsultation@dft.gov.uk

When responding, please state whether you’re responding as an individual or representing the views of an organisation. If responding on behalf of a larger organisation, please make it clear who the organisation represents and, where applicable, how the views of members were assembled.

There will be a consultation event on 28 January 2021. If you’d be interested in attending this event, please contact corsiaconsultation@dft.gov.uk.

If you have any suggestions of others who may wish to be involved in this process please contact us.

Freedom of information

Information provided in response to this consultation, including personal information, may be subject to publication or disclosure under the Freedom of Information Act 2000 (FOIA) or the Environmental Information Regulations 2004.

If you want information that you provide to be treated as confidential, please be aware that, under the FOIA, there is a statutory code of practice with which public authorities must comply and which deals, amongst other things, with obligations of confidence.

Because of this, it would be helpful if you could explain to us why you regard the information you have provided as confidential. If we receive a request for disclosure of the information, we’ll take full account of your explanation, but we cannot give an assurance that confidentiality can be maintained in all circumstances. An automatic confidentiality disclaimer generated by your IT system will not, of itself, be regarded as binding on the department.

The department will process your personal data under the Data Protection Act (DPA) and in the majority of circumstances, this will mean that your personal data will not be disclosed to third parties.

Data Protection

The Department for Transport (DfT) is carrying out this consultation to gather evidence on the UK’s proposed approach to implementing the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). This consultation and the processing of personal data that it entails is necessary for the exercise of our functions as a government department. If your answers contain any information that allows you to be identified, DfT will, under data protection law, be the controller for this information.

As part of this consultation, we’re asking for your name and email address. This is in case we need to ask you follow-up questions about any of your responses. You do not have to give us this personal information. If you do provide it, we’ll use it only to ask follow-up questions.

DfT’s privacy policy has more information about your rights concerning your personal data, how to complain and how to contact the Data Protection Officer. You can view it on GOV.UK

Your information will be kept securely on a secure IT system within DfT and destroyed within 12 months after the consultation has been completed.

Introduction

International aviation emissions

The International Civil Aviation Organization (ICAO) is the United Nations agency established under the Chicago Convention (1944) to manage the administration and governance of international aviation, which includes responsibility for tackling international aviation emissions, which fall outside of states’ nationally determined contributions (NDCs) under the Paris Agreement.

Emissions from this sector are a global problem requiring a global solution, and it’s vital that we find an international answer, rather than simply displacing emissions elsewhere across the world.

The UK plays a key leadership role in ICAO, which has successfully negotiated and secured the first-ever global market-based measure to tackle emissions in a single sector. We’re now negotiating for a long-term emissions reduction goal for international aviation.

This globally co-ordinated sector-based (rather than state-based) approach reflects the highly mobile nature of carbon emissions from this sector and the risk that the responsibility for these emissions simply moves to other jurisdictions in response to individual states taking unilateral action.

The government recognises the incredibly challenging times facing the aviation sector as a result of COVID-19. The global health crisis has meant people have had to profoundly change the way they live, work and travel, and it’s clearly sensible that our plans to reduce emissions look to understand and take account of this.

Meanwhile, the government recognises that the fight against anthropogenic climate change is one of the greatest and most pressing challenges facing the modern world. It’s therefore still critical that aviation plays its part in delivering the UK’s net-zero ambitions. We’re planning to consult shortly to update the government’s position on aviation and climate change.

Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA)

In October 2016, ICAO agreed on a global market-based measure to address CO2 emissions from international aviation from 2021, aimed at achieving ICAO’s medium-term climate change goal of Carbon Neutral Growth from 2020 (CNG2020).

This global scheme, known as the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), requires qualifying aeroplane operators to offset their growth in international aviation CO2 emissions covered by the scheme above 2019 levels [footnote 1]. The growth in emissions will be offset by purchasing and cancelling emissions units (with one unit equivalent to one tonne of CO2 equivalent emissions avoided or removed from the atmosphere).

Under the scheme, aeroplane operators will be required to:

- monitor emissions on all international flights (subject to exemption thresholds)

- offset the growth above the baseline in emissions from flights between participating states by purchasing and cancelling eligible emission units generated by projects that reduce emissions in other sectors (for example, renewable energy)

CORSIA is divided into the following 3 phases:

- pilot phase (2021-2023)

- first phase (2024-2026)

- second phase (2027-2035)

States may volunteer for the pilot and first phases, meaning that all qualifying aeroplane operators operating on routes between participating states will be subject to offsetting requirements. The second phase will include all ICAO States subject to exemptions [footnote 2].

As committed to in the European Civil Aviation Conference (ECAC) Bratislava Declaration of September 2016 and reconfirmed in writing to ICAO in June 2020, the UK plans to participate in CORSIA from the start of the pilot phase.

CORSIA will be periodically reviewed, starting in 2022, and the UK strongly believes these reviews should be used to improve the operation of the scheme and increase its environmental integrity.

As a contracting State of ICAO, the UK is obliged to adopt the relevant Standards and Recommended Practices (SARPs) relating to CORSIA into domestic law.

CORSIA implementation can be divided into 2 parts:

-

monitoring, reporting and verification (MRV) of CO2 emissions is contained in Chapter 1 and 2 of the CORSIA SARPs and covered in detail in this consultation document: aeroplane operators have been monitoring, reporting and verifying their international emissions since 2019 to set the baseline emissions level for the scheme

-

the offsetting of CO2 emissions by aeroplane operators is contained in Chapters 3 and 4 of the CORSIA SARPs: high-level policy options for implementing this aspect of CORSIA in the UK are covered in this consultation document. Following the feedback from this consultation, we plan to consult again by summer 2021 on detailed proposals for implementing CORSIA offsetting in the UK (see ‘Legislative process and timeline’ below)

UK Emissions Trading Scheme

Before the end of the transition period, the UK participated in the EU Emissions Trading Scheme (ETS), a measure to limit greenhouse gas (GHG) emissions across key stationary sectors:

- power generation and energy-intensive industries

- oil and gas refining

- manufacturing (stationary sectors)

- aviation (on flights between and within the UK, Gibraltar and the European Economic Area (EEA) or departing any of these regions to Switzerland)

The EU Emissions Trading System (EU ETS) is one of the EU’s key climate change mitigation policies. Both the EU ETS and the proposed UK ETS work on the ‘cap and trade’ principle. A cap is set on the total amount of GHGs that can be emitted by the industrial, power and aviation sectors covered by the scheme.

The cap is divided into allowances, and participants receive or purchase emission allowances which they can trade with one another as needed. This cap is reduced over time, so that total emissions fall. Participants are required to monitor their emissions during a calendar year, surrendering one emissions allowance for every tonne of carbon dioxide equivalent (CO2e) they’ve emitted at the end of each reporting year.

CO2 emissions from aviation were included in the EU ETS from 2012 and will continue to be included as they currently are until the end of 2023, while the EU ETS is being reviewed in light of CORSIA. Only flights within and between aerodromes in the UK, Gibraltar and the EEA or flights departing any of these regions to Switzerland are currently subject to surrendering obligations under the EU ETS.

In July and August 2020, the European Commission consulted on an Inception Impact Assessment (IIA) which included a list of options for its consideration of how CORSIA could be implemented in the EU. In October 2020, the Commission launched a further public consultation on the issue.

On 1 January 2021, the UK introduced its own ETS which covers the UK’s stationary sectors and aviation (flights within the UK, and flights from the UK to the EEA). ‘Policy options for interaction between CORSIA and a UK Emissions Trading Scheme’ describes how these aviation carbon pricing policies overlap and possible options for dealing with this in the UK.

General principles

Our approach to implementing CORSIA in UK law aims to:

- uphold the UK’s international obligations by implementing CORSIA as closely as possible to the globally-agreed ICAO SARPs.

- uphold the UK’s domestic obligations, including our commitment in the 2017 Clean Growth Strategy (PDF, 5.2MB) to ensure our post-Brexit approach to carbon pricing is at least as ambitious as the EU ETS

We’ve also taken into account the extent to which options could lead to:

- operators having to both cancel CORSIA emissions units and surrender UK ETS allowances for the same tonne of CO2 emitted

- competitive distortions between aeroplane operators and increased administrative burden

Legislative process and timeline

It’s envisaged that CORSIA will be implemented in the UK through 2 statutory instruments (SIs). Firstly, through an Air Navigation Order (ANO) under the Civil Aviation Act 1982 (‘the first SI’). Secondly, through an amendment to the above Order (‘the second SI’).

This consultation document is accompanied by a draft ANO (PDF, 966KB) (‘the first SI’) covering CORSIA MRV which we aim to have in force by spring 2021.

The second SI will cover CORSIA offsetting, taking into account the aviation UK ETS. Following the feedback from this consultation, we plan to publish a consultation on the second SI by summer 2021 with the aim that it comes into force by the first UK ETS surrender deadline in April 2022.

The Greenhouse Gas Emissions Trading Scheme Order 2020 (subsequently referred to as the UK ETS Order 2020) came into force on 12 November 2020.

The second UK ETS order amended the first UK ETS order, to include provisions relating to aviation free allocation, and came into force on 31st December 2020. Subsequent amendments to the UK ETS Order 2020 may be required as a result of the chosen policy option for interaction between CORSIA and a UK ETS. Any such amendments to both the ANO and UK ETS order will be in force no later than the start of UK ETS Phase I(b) in 2024.

CORSIA Monitoring, Reporting and Verification (MRV)

Introduction

This section outlines how the UK proposes to implement the provisions covered by chapters 1, 2 and some elements of Chapter 3 (3.1.3 and 3.3) within Part II of Annex 16, Volume IV of the Chicago Convention. These provisions will be implemented into UK law through an Air Navigation Order (ANO) (Statutory Instrument or SI), a draft (PDF, 966KB) of which is available alongside this consultation document.

Principally, this SI covers the attribution of aeroplane operators to a state, the role of the state in implementing CORSIA and details the monitoring, reporting and verification processes and requirements of CORSIA. The monitoring, reporting and verification of CO2 emissions produced using CORSIA eligible fuels (CEF) is also covered in detail as well as the enforcement action that aeroplane operators will be subject to if they do not comply with their obligations under the scheme.

Attribution of international flights to aeroplane operators, and aeroplane operators to the United Kingdom

Attribution of international flights to aeroplane operators is implemented in article 9 of the draft ANO (PDF, 966KB) in line with CORSIA SARPs paragraph 1.1. This means that the process outlined in paragraph 1.1.3 will be used when assigning a specific international flight to a specific aeroplane operator.

Attribution of aeroplane operators to the United Kingdom will be implemented in articles 8, 16 and 17 of the draft ANO and follow CORSIA SARPs paragraph 1.2. The provisions mean that the ICAO designator, air operator certificate, or the place of juridical registration or residence will be used to determine if an aeroplane operator should be attributed to the UK.

The ICAO document titled ‘CORSIA Aeroplane Operators to State Attributions’ provides an online record of which aeroplane operators are attributed to which state.

Obligations of the UK government

The obligations of the UK government in administering CORSIA in the UK are covered in articles 7, 10, 11, 18, 19 and 20 of the draft ANO and follow paragraph 1.3 of the CORSIA SARPs.

The draft ANO also contains provisions that designate regulators within the UK. The government intends that aeroplane operators who are attributed to the UK for CORSIA and have their place of juridical registration or residence in the UK will be regulated for CORSIA by the same UK regulator as under the UK ETS:

- the Environment Agency (EA) in England

- the Scottish Environmental Protection Agency (SEPA) in Scotland

- Natural Resources Wales (NRW) in Wales

- the Northern Ireland Environment Agency (NIEA) in Northern Ireland

Aeroplane operators who are attributed to the UK for CORSIA but are not participants in the UK ETS are proposed to be regulated by the EA. It’s envisaged that separate secondary legislation will be required to implement CORSIA in the Overseas Territories and Crown Dependencies.

As the UK is a single administering state for the purposes of ICAO, it’s proposed that a single UK CORSIA focal point will report to ICAO on behalf of all the UK regulators. The draft ANO places this obligation on the Secretary of State but the government intends to administratively delegate this function to the EA.

The Department for Transport (DfT) remains the responsible authority in the UK for CORSIA, working in close consultation with the Department for Business, Energy and Industrial Strategy (BEIS) and the devolved administrations.

Recordkeeping, compliance periods, timelines and equivalent procedures

The CORSIA rules for recordkeeping and compliance periods will be implemented in articles 12 and 13 of the draft ANO in line with CORSIA SARPs provisions 1.4.1 to 1.5. The provisions mean that aeroplane operators will be required to keep records that demonstrate compliance with CORSIA for 10 years.

CORSIA compliance periods are implemented in Schedule 1 of the draft ANO and follow the timeline defined in Appendix 1 of the CORSIA SARPs.

Article 14 of the draft ANO implements the provisions at paragraph 1.6 of the CORSIA SARPs by requiring the UK regulator to approve any equivalent procedures that an aeroplane operator may wish to use in place of MRV procedures set out in the CORSIA SARPs.

Applicability of MRV requirements

Provisions covering the applicability of MRV requirements to aeroplane operators are implemented in article 21 of the draft ANO and follow the provisions outlined in paragraph 2.1 of the CORSIA SARPs. The provisions set out which aeroplane operators will be required to undertake CORSIA MRV based on their annual CO2 emissions from the operation of aeroplanes with a maximum certified take-off weight of >5,700kg on international flights. Humanitarian, medical and firefighting flights are excluded from all aspects of CORSIA, as are flights conducted by helicopters.

Monitoring of CO2 emissions

Eligibility to use the CORSIA CO2 Estimation and Reporting Tool

An aeroplane operator’s eligibility to use the CORSIA CO2 Estimation and Reporting Tool (CERT) is subject to certain CO2 emissions thresholds. These provisions are implemented in articles 22, 23 and 24 of the draft ANO and follow CORSIA SARPs provisions 2.2.1.2 for the 2019-2020 period and 2.2.1.3 for the 2021-2035 period.

Emissions monitoring plans

Provisions regarding an aeroplane operator’s emissions monitoring plan are set out in articles 23 to 30 of the draft ANO and follow paragraphs 2.2.1 and 2.2.2 of the CORSIA SARPs. This means that aeroplane operators attributed to the UK, who are within the scope of applicability of CORSIA are required to submit an emissions monitoring plan to their regulator for approval, setting out how they’re to monitor their CO2 emissions.

Reporting of fuel mass and CO2 emissions

Aeroplane operators will be required to submit a verified emissions report for approval by the designated regulator. The relevant provisions are contained in article 31 of the draft ANO (PDF, 966KB) and align with paragraph 2.3.1 of the CORSIA SARPs.

Calculation of CO2 emissions

The calculation of CO2 emissions for CORSIA is provided for in articles 28 to 33 of the draft ANO and includes provisions for the fuel conversion factors specified in CORSIA (which differ from the fuel conversion factors in the EU ETS and the UK ETS) [footnote 3].

Under these provisions, aeroplane operators will input their fuel consumption data into an electronic form which will automatically calculate their CO2 emissions using the correct fuel conversion factor.

This electronic form will form part of an aeroplane operators Emissions Report which must be verified before being submitted to the appropriate regulator.

The obligations of the UK CORSIA focal point in reporting CO2 emissions to ICAO are contained in article 33 of the draft ANO and align with paragraph 2.3.2 of the CORSIA SARPs.

Verification of CO2 emissions

Provisions for the annual verification of an aeroplane operator’s CO2 emissions are set out in articles 34 to 36 of the draft ANO and align with the provisions of paragraph 2.4 of the CORSIA SARPs. This means aeroplane operators will be required to engage a verification body from the list on the ICAO CORSIA website to verify their annual emissions report. It also means verification will be conducted according to ISO 14064-3:2006 and the requirements in Appendix 6 to the CORSIA SARPs.

CORSIA eligible fuels

Monitoring

Provisions for monitoring CORSIA eligible fuels (CEF) are covered under articles 29 and 30 of the draft ANO and follow paragraph 2.2.4 of the CORSIA SARPs. This means CEF must meet the standards set out in the ICAO document entitled ‘CORSIA Sustainability Criteria for CORSIA Eligible Fuels’ (PDF, 320KB) and be certified by an approved sustainability certification scheme, a list of which can be found in the ICAO document ‘CORSIA Approved Sustainability Certification Schemes’.

Reporting

Provisions for reporting the use of CEF are covered under article 32 of the draft ANO and follow paragraph 2.3.3 of the CORSIA SARPs. This means that aeroplane operators must report any emissions reductions they wish to claim for the use of CEF through their emissions report, after having subtracted any CEF traded or sold. It also means that fuels used to reduce CORSIA obligations cannot be used to claim emissions reductions under any other greenhouse gas (GHG) scheme in which the aeroplane operator participates.

Verification

Provisions for the verification of CEF are contained in article 36 of the draft ANO and align with paragraph 2.4.3 of the CORSIA SARPs. These detail the documentary proof required to verify emissions reductions claimed from the use of CEF. The provisions also state that aeroplane operators must have audit rights to the production records for any CEF it purchases.

Data management, data gaps, and error corrections to emissions reports

Provisions for data management and control are contained in articles 37 to 41 of the draft ANO and follow Article 24 and Schedule 4 of the UK ETS Order 2020 which amend provisions within Commission Implementing Regulation (EU) 2018/2066.

The provisions mean that the aeroplane operator must establish, implement, document and maintain a control system and procedures for data flow activities.

The issue of data gaps and error corrections is implemented in articles 37 and 38 of the draft ANO and aligns with sections 2.5 and 2.6 of the CORSIA SARPs. On the treatment of data gaps, provisions are based upon Article 66 of Commission Implementing Regulation (EU) 2018/2066 which are adopted in Article 24 of the draft UK ETS Order 2020. These provisions mean that aeroplane operators will be required to engage with their regulator to ensure the correct action can be taken to mitigate any data gaps or errors.

Charging

Provisions for charging an applicant, aeroplane operator or any other person in relation to CORSIA MRV are covered in articles 42 to 44 of the draft ANO. These provisions follow Articles 35 to 37 of the UK ETS Order 2020 and mean that the regulator can charge any of the above persons to recover costs that the regulator incurs when performing activities related to CORSIA.

It also means that the regulator must publish a document that sets out the charges payable and, before publishing this document, must notify the persons likely to be affected and specify opportunities for those affected to object to the charges.

Any charging document must be approved as follows:

- for the EA, by the Secretary of State

- for SEPA, by Scottish Ministers

- for NRW, by Welsh Ministers

- for the Chief Inspector Northern Ireland, by the Department of Agriculture Environment and Rural Affairs [DAERA]

Compliance monitoring

The provisions in articles 52 to 63 of the draft ANO cover the enforcement and penalties for non-compliance. These follow Part 7 of the UK ETS Order 2020 and mean that the regulator can issue an enforcement notice when it believes an aspect of CORSIA implementation has been or is likely to be implemented incorrectly. The enforcement notice will set out the steps required to correct the contravention.

Penalties and enforcement

The provisions in articles 55 to 66 of the draft ANO cover the enforcement and penalties for non-compliance. These follow Part 7 of the UK ETS Order 2020 and mean that the regulator can issue an enforcement notice when it believes an aspect of CORSIA implementation has been or is likely to be implemented incorrectly. The enforcement notice will set out the steps required to correct the contravention.

The provision also denotes the civil penalties that the regulator may impose. The following penalties mirror those within the UK ETS Order 2020:

- for failure to apply for or make a revised application for an emissions monitoring plan, failure to monitor emissions, or failure to report emissions – £20,000 plus a daily rate of £500 up to a maximum of £45,000

- for failure to keep records – £50,000

- for failure to comply with an enforcement notice given by the regulator – £20,000 plus a daily rate of £1,000 up to a maximum of £45,000

- for failure to comply with an information notice – £5,000 plus a daily rate of £500 up to a maximum of £45,000

- for providing false or misleading information – £50,000

- for refusing to allow the regulator or authorised person access to inspect premises – £50,000

Articles 64 to 69 of the draft ANO outlines provisions related to the right of appeal. These provisions follow Part 8 of the UK ETS Order 2020. They mean that where an appeal is made against SEPA, the appeal body will be the Scottish Land Court. Where an appeal is made against the chief inspector of Northern Ireland, the appeal body is the Planning Appeals Commission. For all other appeals, the appeal body will be the First-tier Tribunal.

Questions

Q1 Do you agree with the overall approach taken to the implementation of CORSIA MRV in the UK, through the draft Air Navigation Order (PDF, 966KB) which is based closely on the CORSIA SARPs, supplemented by provisions from the UK ETS Order where necessary? If not, please explain why.

Q2 Do you agree with the specific provisions contained in the draft Air Navigation Order and summarised here? If not, please explain why.

Q3 Is there anything that should additionally be included in the draft Air Navigation Order? If so, what?

Policy options for interaction between CORSIA and a UK Emissions Trading Scheme

Introduction and general principles

As outlined in the introduction, the UK has long supported strong, concerted international action to tackle the contribution of international aviation to climate change. As outlined in the Aviation 2050 consultation (PDF, 7.7MB), the UK continues to advocate for robust, environmentally-effective measures that minimise market distortions and address the sector’s emissions in the most cost-effective way. For these reasons, the UK is committed to participating fully in CORSIA and, alongside 87 other states (PDF, 550KB), has confirmed its intention to do so from the start of the scheme in 2021.

At the same time, the UK recognises that further action is required to ensure that international aviation contributes to the global temperature goals of the Paris Agreement. The UK is therefore negotiating in ICAO for a long-term goal for international aviation emissions that, like our national targets under the Climate Change Act, is consistent with the Paris Agreement. The UK is also acutely aware of its responsibility as COP26 President to push for great ambition in tackling climate change across all sectors. The UK will use the platform of COP26 to push for progress in decarbonising all sectors including aviation.

In addition, as set out in the government’s response (PDF, 797KB) to the future of UK carbon pricing consultation, the UK government and the devolved administrations have higher climate change ambitions than those currently set by ICAO. That is why flights departing the UK to aerodromes in the European Economic Area were included under the UK ETS from 1 January 2021.

We have therefore considered how these 2 carbon pricing policies for the UK’s international flights should interact from 2021. In doing so we have sought to ensure that the UK upholds its:

- international commitments to implement and participate fully in the CORSIA

- domestic commitments, including to ensure that the UK’s post-Brexit approach to carbon pricing is at least as ambitious as the current scheme

We’ve also considered the extent to which aeroplane operators would be required both to cancel CORSIA emissions units and surrender UK ETS Allowances for the same tonne of CO2 emissions. [footnote 4]

We’ve also sought to minimise competitive and administrative burdens where possible, whilst recognising that, in many cases, an increase in complexity compared to the current situation cannot be avoided.

While we acknowledge that aviation has significant climate impacts in addition to CO2, these are not yet well enough understood to be able to form policy with any certainty that aviation’s total climate change impact would be reduced. Neither CORSIA nor UK ETS therefore require aircraft operators to monitor, report or address these effects and they are therefore out of scope of this consultation. It’s possible that either or both schemes may seek to incorporate non-CO2 effects in the future.

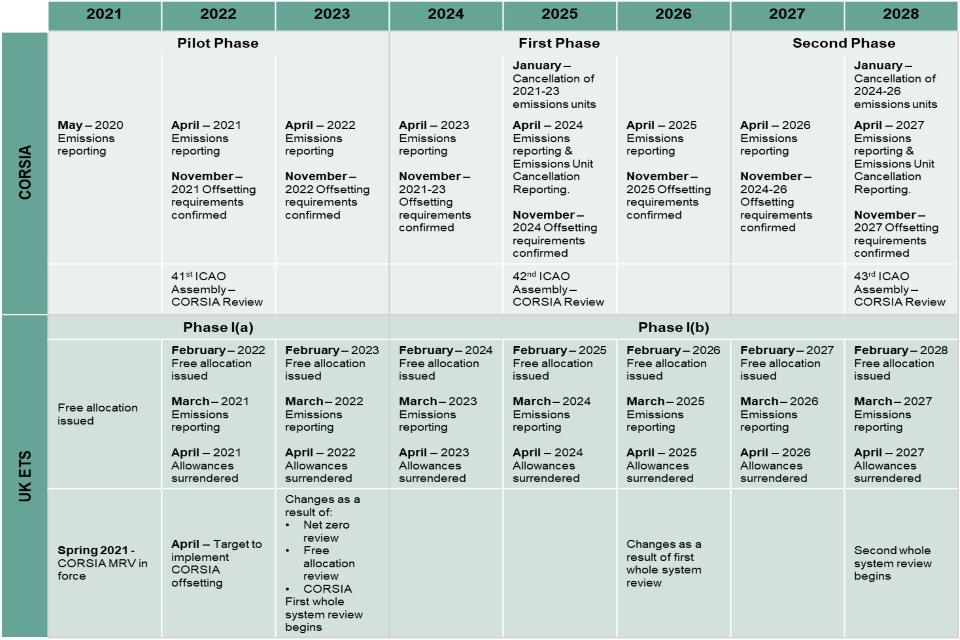

CORSIA and UK ETS timelines

Timeline setting out the key dates for each scheme

CORSIA is subject to triennial reviews by ICAO, starting from 2022, which may necessitate amendments to the CORSIA Air Navigation Order or UK ETS Order. The UK ETS whole system reviews are also opportunities to review how CORSIA and UK ETS interact.

Policy options for implementing CORSIA in the UK

Without policy action, CO2 emissions above the CORSIA baseline from international flights departing from the UK to the European Economic Area would incur obligations from both the UK ETS and CORSIA, leading to aeroplane operators being charged twice for these emissions.

We’ve therefore considered options for CORSIA and UK ETS interaction on international flights covered by the UK ETS [footnote 5]. In any scenario (except Option 5 ‘Domestic offsetting scheme’) we assume that:

- UK domestic flights (that depart from and arrive at aerodromes in the UK) will only be included in the UK ETS

- international flights to or from the UK that are not covered by the UK ETS would only be included in CORSIA (where the other state is also a participant in the scheme)

- flights from EEA States to the UK would be covered by the EU ETS

The following sections detail the CORSIA-UK ETS interaction options that we have considered for UK to EEA flights, including the government’s proposed preference.

We acknowledge that these represent high-level options for interaction between CORSIA and the UK ETS. Responses to this initial consultation will be used to work up a preferred CORSIA-UK ETS interaction policy in more detail ahead of a second consultation on detailed policy design that we plan to publish by summer 2021.

In assessing these options, we’ve considered factors such as:

- consistency with the UK’s domestic and international legal obligations

- impact on global CO2 emissions

- costs to operators

- competitive impacts

- impact on levels of compliance with both schemes

- consistency with existing UK policy, including our climate ambitions

- reputational impact on the UK and its international relations

Policy options

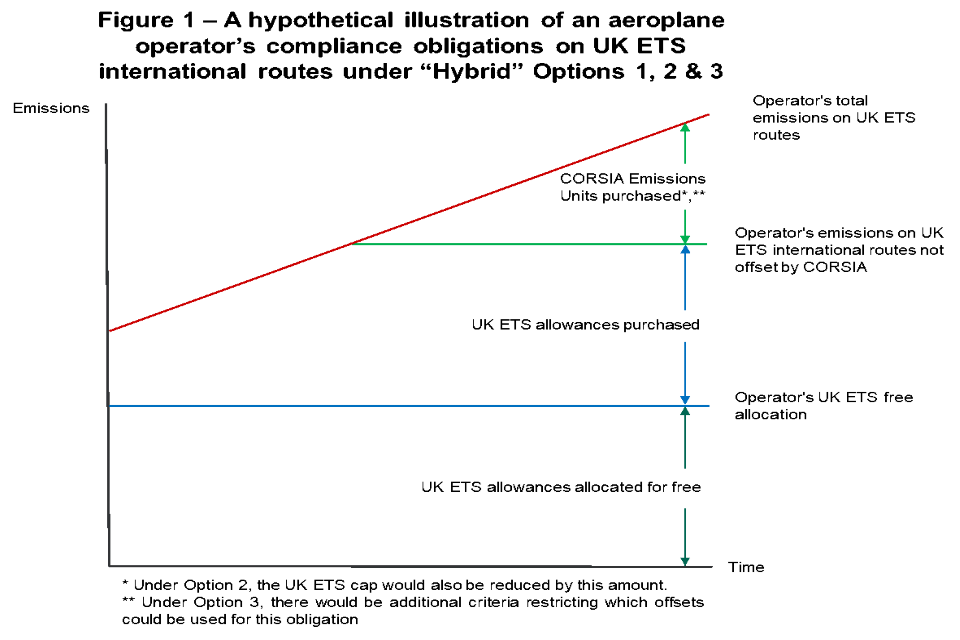

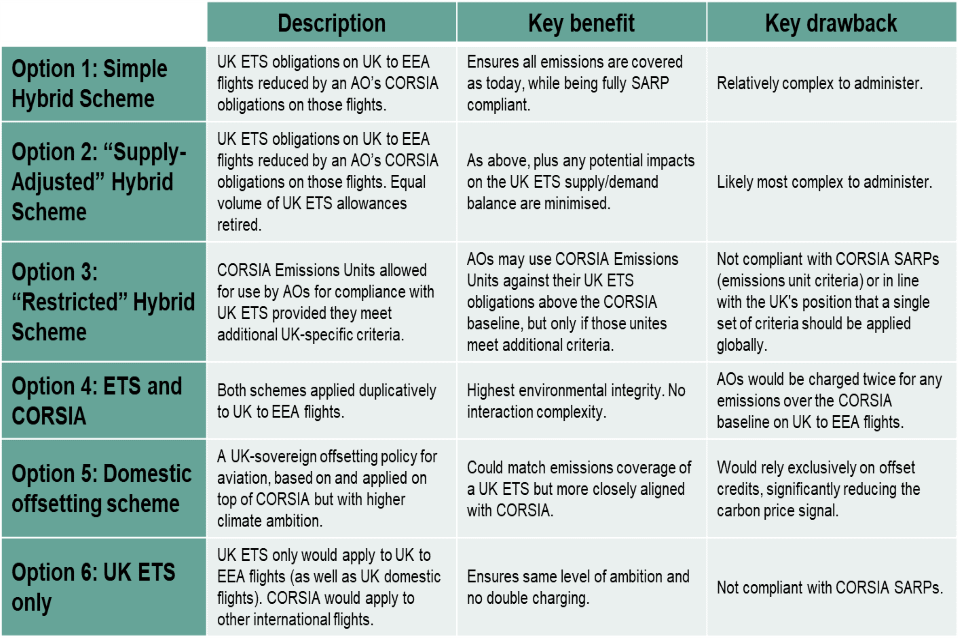

Option 1: Simple hybrid scheme

Design

Under this option, an aeroplane operator’s UK ETS obligations would be reduced by an amount equivalent to their CORSIA obligations on flights from the UK to EEA states.

This means that an operator’s UK ETS obligations would be reduced by the amount of CO2 they’re required to offset under CORSIA for UK ETS international flights.

In effect, this means that the UK ETS would apply to emissions on these flights unless they are covered by CORSIA. A method of calculating or estimating the split between an operator’s obligations on these routes, that also considers the implications of different surrendering deadlines, would need to be devised if this option is taken.

This option does not allow an aeroplane operator to directly use CORSIA emissions units against their UK ETS surrendering obligations.

This option is broadly similar to the ‘ETS-CORSIA “mix”’ option in the EU’s inception impact assessment.

Figure 1 provides a visual representation of what this option might look like in practice

Considerations

We assess that this option offers the simplest method of interaction between the UK ETS and CORSIA. It means the UK is fully compliant with the CORSIA SARPs whilst ensuring aeroplane operators face obligations either under CORSIA or the UK ETS on all UK to EEA emissions. However, this option would see the demand for allowances reduced without an equivalent adjustment to the supply, which could contribute to a build-up of surplus UK ETS allowances.

This option could add a level of complexity for aeroplane operators on UK to EEA flights, however, we would aim to mitigate these additional complexities through combined operational procedures and clear guidance from the UK’s designated regulators.

Option 2: ‘Supply-adjusted’ hybrid scheme

Design

This option is based on the simple hybrid option above. Aeroplane operators would be entitled to claim a reduction in their UK ETS obligations equivalent to their CORSIA obligations on flights from the UK to EEA States.

However, in addition, to maintain the supply-demand balance (and therefore the UK ETS auction price), the UK ETS cap would also be adjusted to account for those emissions covered by CORSIA. For every tonne of CO2 that is removed from the UK ETS obligations of an aeroplane operator due to CORSIA, a tonne of CO2 in UK ETS allowances would also be retired from the system. Allowances could be taken from the overall UK ETS cap or from the allowances allocated to the aviation sector.

As with option 1, a method of calculating or estimating the split between an aeroplane operator’s obligations on UK ETS international routes would need to be devised if this option is taken forward in the next consultation. This option does not allow an aeroplane operator to directly use CORSIA emissions units against their UK ETS surrendering obligations.

Considerations

This option would be more environmentally stringent than the Simple Hybrid as it would go further towards maintaining the integrity of the UK ETS cap. It would also be fully compliant with the CORSIA SARPs. This option would also help reduce any potential impacts on the UK ETS price as it would help to maintain the supply/demand balance of the UK ETS.

This is therefore the government’s initial preferred option. This option is likely to be the most complicated to administer, although any additional complexity compared to option 1 is likely to fall on the administering authority and regulators, rather than the aeroplane operator.

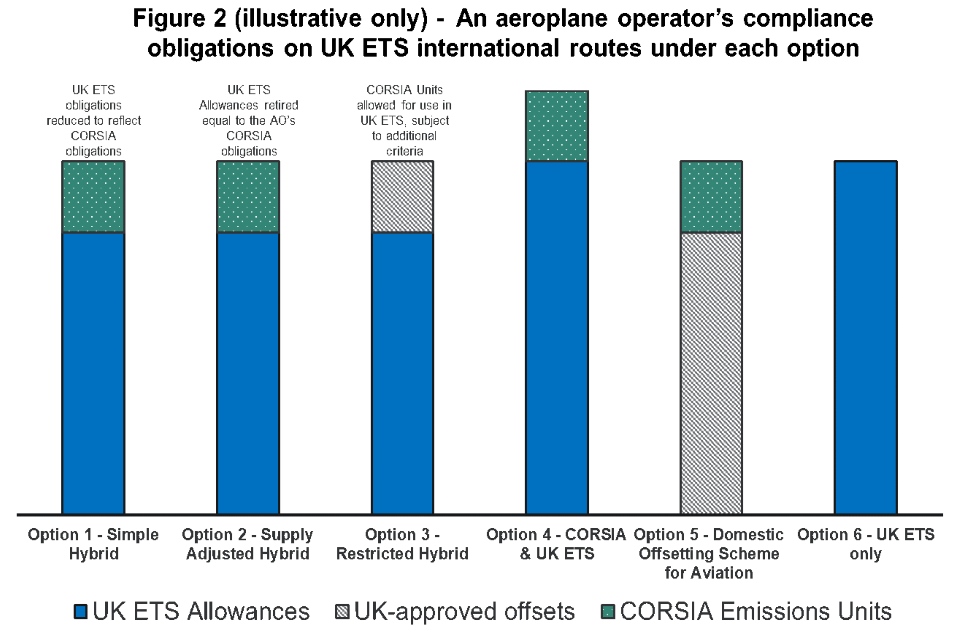

Option 3: ‘Restricted’ hybrid scheme

Design

Under this option, aeroplane operators would be allowed to use CORSIA emissions units against their UK ETS obligations, but only if those units meet additional criteria to further minimise any risk that the CORSIA emissions units used did not represent additional verifiable emissions reductions or that they have been double-counted.

In this option, CORSIA emissions units would be eligible for use against UK ETS obligations, although this could be capped at a level equal to the CORSIA obligations on UK ETS international routes. If this safeguard were to be introduced, a method of calculating or estimating an aeroplane operator’s CORSIA obligations on UK ETS international routes would need to be devised, as for options 1 and 2.

Without this safeguard, this option could lead to cheaper CORSIA emissions units being used in place of UK ETS allowances, leading to oversupply and a significantly reduced price. The safeguard is therefore assumed to be included in this option as depicted in figure 2 above.

Considerations

This option would mean the UK developing its own emissions unit criteria, in addition to those in the CORSIA implementation elements. However, this would contradict our long-held position that the criteria for CORSIA emissions units should not vary between states to avoid competitive distortions.

This option would see the demand for allowances reduced without an equivalent adjustment to the supply, which could contribute to a build-up of surplus UK ETS allowances.

Option 4: ETS and CORSIA

Design

This option would implement both the UK ETS and CORSIA independently. Aeroplane operators with international flights in the UK ETS would be required to comply with both schemes for emissions above the CORSIA baseline and therefore have overlapping obligations on these flights.

Considerations

This would be the most environmentally ambitious option.

This option would mean aeroplane operators were required to pay twice for the same tonne of CO2 but it’s expected that this would be less administratively complex than a ‘hybrid’ scheme as the 2 schemes would run largely separately.

Option 5: Domestic offsetting scheme

Design

In this case, CORSIA would still be applied to international flights, as per the ICAO SARPs. However, instead of aviation being covered by the UK ETS, an offsetting scheme based on the design of CORSIA would be applied to the flights that would have been in scope of the UK ETS. This means it could use CORSIA MRV, thresholds, exemptions and compliance periods.

However, as a UK policy, this scheme could also:

- have a more stringent baseline than CORSIA for international flights, potentially achieving the same emissions reductions as would be achieved through including these flights in the UK ETS

- include UK domestic flights

- apply its own emissions unit criteria for emissions not covered by CORSIA, including limiting the provenance to certain jurisdictions or to negative emissions. [footnote 6]

This option would use offset credits, rather than allowances, for all emissions. This option would aim to ensure aeroplane operators were required to purchase enough offsets through both CORSIA and the UK scheme to achieve the same level of emissions reductions as would be achieved through an emissions trading system.

A method would need to be devised to split an operator’s obligations on UK ETS international routes between CORSIA and the UK scheme, as for options 1, 2 and 3

Because this option would replace the UK ETS it would require some time to deliver. It may not be possible to bring this into effect from 2021, but we expect it could be introduced by the start of the CORSIA First Phase.

Considerations

This option would be fully compliant with the CORSIA SARPs as it would apply separately in addition to CORSIA.

As this option uses offset credits rather than ETS allowances, it would provide the highest demand for domestic and potentially international emissions reduction programmes, consistent with the government’s carbon finance ambitions.

However, the price of offsets is likely to be below the price of allowances for some years. Because all emissions obligations would be met through offsetting, rather than the surrender of allowances, there could therefore be a significantly reduced incentive to reduce in-sector aviation emissions.

Option 6: UK ETS only

Design

Under this option, only the UK ETS would apply on UK to EEA flights, whilst CORSIA would apply to all other international flights in scope of the scheme. In this case, UK to EEA flights would not be subject to CORSIA obligations and the UK would need to file a difference against the definition of international flights in the CORSIA SARPs.

This option is broadly similar to the ‘ETS-CORSIA ‘clean-cut’ option in the EU’s Inception Impact Assessment.

Considerations

This option would ensure the same level of ambition as today on UK to EEA flights, without double charging for the same emissions.

However, this option does not fully comply with CORSIA SARPs since UK to EEA flights, despite being international flights, would not be covered by COR

Options we have not assessed

We’ve not assessed in any detail options which:

- apply the UK ETS beyond the scope described above: we have never proposed to include these routes in the UK ETS

- do not implement CORSIA: as recalled in this consultation, the UK has long been a strong supporter of a coordinated international approach to tackling international aviation emissions and is committed to participating in CORSIA from the start

- do not apply the UK ETS to any international flights: this would represent a significant reduction in climate ambition compared to the status quo

- discriminate between operators based on nationality: this would risk creating competitive distortions between operators on the same route – something we have strenuously sought to avoid in the design of both the UK ETS and CORSIA

- aim at price parity between UK ETS allowances and CORSIA emissions units, for example, using exchange mechanisms: we acknowledge there is likely to be a price difference between the two schemes, given the differences in abatement costs between different parts of the global economy, and have therefore not focused on the price of these units but rather environmental integrity in the round

Summary of options

Questions

4 Do you agree that Option 2 (Supply-Adjusted Hybrid) should be preferred over the other options described in this chapter? If not, please explain why.

5 Do you have any suggestions for how the preferred option could be implemented, including minimising administrative complexities? If so, please explain.

6Are there any further options that you believe should be considered? If so, please explain.

What will happen next

Following this consultation and analysis of all responses, a short government response will be issued summarising the responses received and responding to any issues raised.

It’s then proposed that the draft Air Navigation Order (ANO) (PDF, 966KB), including any amendments that may be considered necessary as a result of this consultation or internal review, will be made and enter force by spring 2021.

Responses to this consultation will also be used to select and work up a preferred CORSIA-UK ETS interaction policy in more detail. A second consultation will be published by summer 2021 on the details of this policy design.

Following this second consultation, and the analysis of all responses received, a government response will be published in the second half of 2021 and any secondary legislation required to amend either the CORSIA ANO (a draft of which is provided with this consultation) or the UK ETS Order will be made.

We aim to have any changes in force by the first UK ETS compliance deadline in April 2022, and no later than the start of Phase 1(b) of the UK ETS in 2024.

A summary of responses, including the next steps, will be published within 3 months of the consultation closing on GOV.UK.

Paper copies of all these documents will be available on request. If you have questions about his consultation, please contact corsiaconsultation@dft.gov.uk

Annex A Full list of consultation questions

Question 1

Do you agree with the overall operational approach taken to the implementation of CORSIA MRV in the UK, through the draft Air Navigation Order which is based closely on the CORSIA SARPs, supplemented by provisions from the UK ETS Order where necessary? If not, please explain why.

Question 2

Do you agree with the specific provisions contained in the draft Air Navigation Order and summarised here? If not, please explain why.

Question 3

Is there anything that should additionally be included in the draft Air Navigation Order? If so, what?

Question 4

Do you agree that Option 2 (Supply-Adjusted Hybrid) should be preferred over the other options described in this chapter? If not, please explain why.

Question 5

Do you have any suggestions for how the preferred option could be implemented, including minimising administrative complexities? If so, please explain.

Question 6

Are there any further options that you believe should be considered? If so, please explain.

Annex B: consultation principles

The consultation is being conducted in line with the government’s key consultation principles which are listed below.

If you have any comments about the consultation process please contact:

Consultation Co-ordinator

Department for Transport

Zone 1/29 Great Minster House

London SW1P 4DR

-

The baseline is currently defined as an average of 2019 and 2020 emissions, however due to the COVID-19 pandemic, the ICAO Council agreed in June 2020 to change this to 2019 emissions only for the Pilot Phase. The CORSIA periodic review in 2022 will consider whether to extend the baseline change to the subsequent phases. ↩

-

Least Developed Countries (LDCs), Small Island Developing States (SIDS) and Landlocked Developing Countries (LLDCs) are exempt from all phases of CORSIA but may volunteer to participate in any or all stages. In addition, states with a very small share of international aviation activity in 2018 are exempt from taking part in any phase of CORSIA but may volunteer to participate in any or all phases. ↩

-

The CORSIA SARPs give a fuel conversion factor for Jet-A fuel of 3.16 (in kg CO2/kg fuel) whereas the EU ETS and UK ETS will use a value of 3.15 (in kg CO2/kg fuel). ↩

-

‘The Future of UK Carbon Pricing: A Joint Consultation’ (PDF, 1.5MB), page 84 (viewed on 19 August 2020). ICAO Assembly Resolution A40-18 states that market-based measures for international aviation “should not be duplicative and international aviation CO2 emissions should be accounted for only once”. Aeroplane operators, as polluters, are, of course, free to voluntarily mitigate their emissions multiple times. ↩

-

These options would also apply to flights to Switzerland, if an agreement is reached with Switzerland to include flights from the UK to Switzerland in the UK ETS. The UK Crown Dependencies and Overseas Territories, except Gibraltar, are not proposed for inclusion in the UK ETS, and all are considered part of the UK for the purposes of CORSIA. ↩

-

This could, for example, contribute to demand for UK-based offsets and negative emissions, assisting these nascent domestic markets. ↩