LAM17040 - Exemption for certain BLAGAB or eligible PHI business: FA12/S153

A friendly society is not chargeable to corporation tax (whether on income or chargeable gains) on its profits arising from “exempt BLAGAB or eligible PHI business” (FA12/S153(1)), but it must make a claim for this exemption to apply (FA12/S153(2)).

Claims for exemption can be made by submitting a corporation tax return exempting “exempt BLAGAB or eligible PHI business” from corporation tax, or by notifying an officer of HMRC.

“BLAGAB or eligible PHI business” is defined at FA12/S154 – see LAM17050, and “exempt BLAGAB or eligible PHI business” is defined at FA12/S155 – see LAM17060.

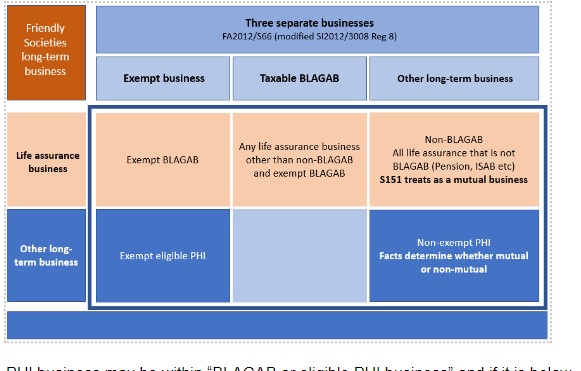

The general rule for life insurance companies at FA12/S66 is that “BLAGAB” and other “long-term business” are treated as separate businesses – see LAM02040. Regulation 8 of the Friendly Societies (Modifications of the Tax Acts) Regulations 2012 (SI2012/3008) expands this for friendly societies to three separate businesses:

(a) basic life assurance and general annuity business,

(b) tax exempt business,

(c) other long-term business.

The diagram here illustrates the separate business categories which may apply to a friendly society.

{kind=link}

PHI business may be within “BLAGAB or eligible PHI business” and if it is below the FA/S155 premium limits, then it is exempt under FA12/S153. Where PHI business falls within the definition of “BLAGAB or eligible PHI” but is above the FA12/S155 premium limits, then it might remain exempt if written on a mutual basis under FA12/S71(3). If PHI business falls outside the scope of “BLAGAB or eligible PHI business”, then it may also be exempt if written on a mutual basis under FA12/S71(3) or if the society meets the conditions under FA12/S164-165 for a qualifying society.

Where the friendly society long-term business is substantially all non-BLAGAB (LAM02040), SI2012/3008/REG9 modifies the separate business rules in FA12/S67. The society is treated as carrying on two businesses, one consisting of the tax exempt business and the other consisting of the (insubstantial) BLAGAB and other long-term business. The BLAGAB and other long-term business will be taxed as “non-BLAGAB long-term business”.

Where an insurance company has tax exempt business, in determining the credits arising and the expenses incurred which are to be regarded as referable to the company’s BLAGAB, no account is to be taken of credits, other income, debits, other losses and expenses incurred which relate to the tax exempt business (SI 2012/3008/REG11 modifying FA12/S98).

The tax treatment of transfers of business for friendly societies is summarised at LAM17080, and LAM17160 to LAM17200.