IEIM403480 - Due Diligence: New Entity Accounts: Passive NFE, Controlling Persons

Due Diligence: New Entity Accounts: Passive NFE, Controlling Persons

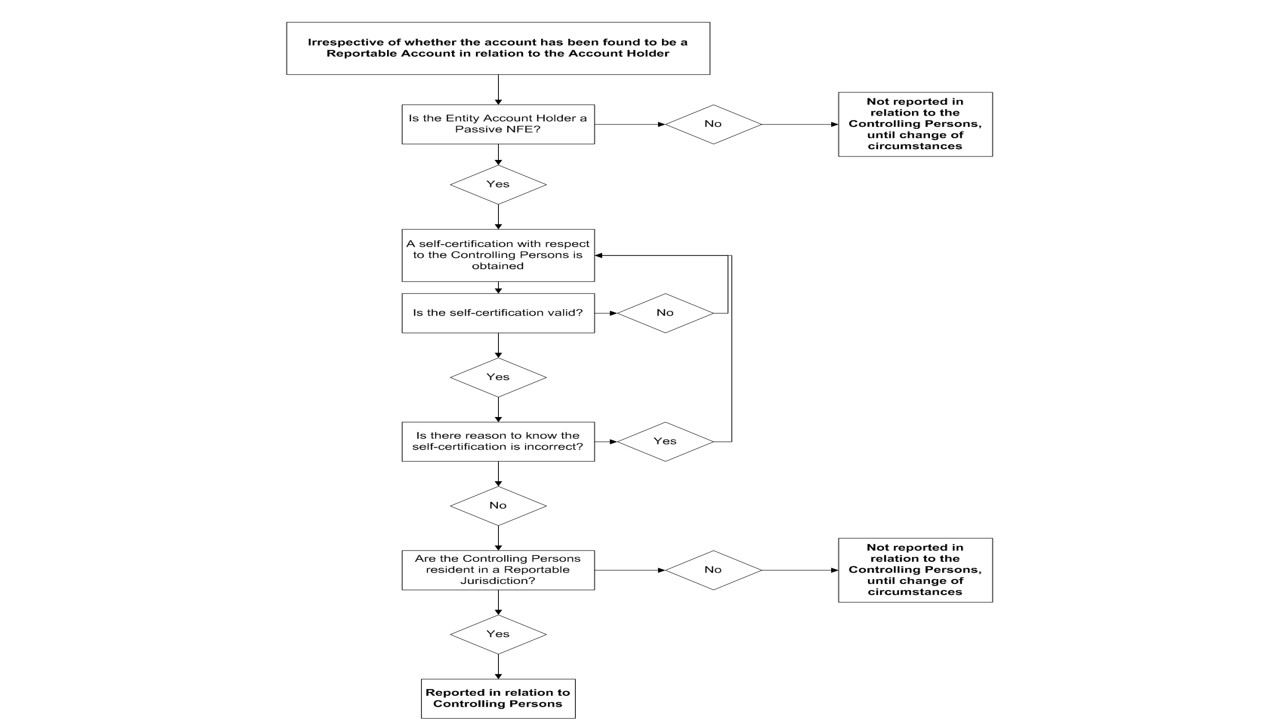

Financial Institutions must determine whether a new entity Account Holder is a Passive NFE with one or more controlling persons who are Reportable Persons. If so, then the account must be treated as a Reportable Account. In making this determination the Financial Institution must follow the guidance below but may do so in the order most appropriate under the circumstances.

Determining whether the Account Holder is a Passive NFE

A Financial Institution may obtain a self-certification from the Account Holder to establish its status, or instead may use:

- information in its possession (such as information collected pursuant to AML/KYC procedures); or

- information that is publicly available (such as information published by an authorised government body or standardised industry coding system) based upon which it can reasonably determine that the Account Holder is an Active NFE or a Financial Institution.

Note though that a professionally managed investment entity resident in a Non-Participating Jurisdiction is always treated as a Passive NFE, notwithstanding that it would be treated as a Financial Institution if it were resident in a Participating Jurisdiction (this ensures that it is not possible for controlling persons to avoid reporting by setting up such entities in Non-Participating Jurisdictions).

Determining Controlling Persons

For the purposes of determining the Controlling Persons of an Account Holder, a Financial Institution may rely on information collected and maintained pursuant to AML/KYC Procedures, provided that such procedures are consistent with Financial Action Task Force (FATF) Recommendations 10 and 25, as adopted in February 2012.

If the Reporting Financial Institution is not legally required to apply AML/KYC Procedures that are consistent with the 2012 FATF Recommendations, it must apply substantially similar procedures for the purpose of determining the Controlling Persons.

Where a publicly listed company exercises control over an Account Holder that is a Passive NFE, there is no requirement to determine the Controlling Persons of the publicly listed company if it is already subject to disclosure requirements ensuring adequate transparency of beneficial ownership information.

Determining whether a Controlling Person is a Reportable Person

For the purposes of determining whether a Controlling Person of a Passive NFE is a Reportable Person, a Financial Institution may only rely on a self-certification from either the entity Account Holder or the Controlling Person.

This can be summarised in the following diagram (© OECD). Use this link to view diagram determining whether a Controlling Person is a Reportable person.

{kind=link}

For guidance on reporting Controlling Persons, see IEIM402183.