IEIM400835 - Investment Entity: Reporting on a Collective Investment Scheme

Reporting on a Collective Investment Scheme

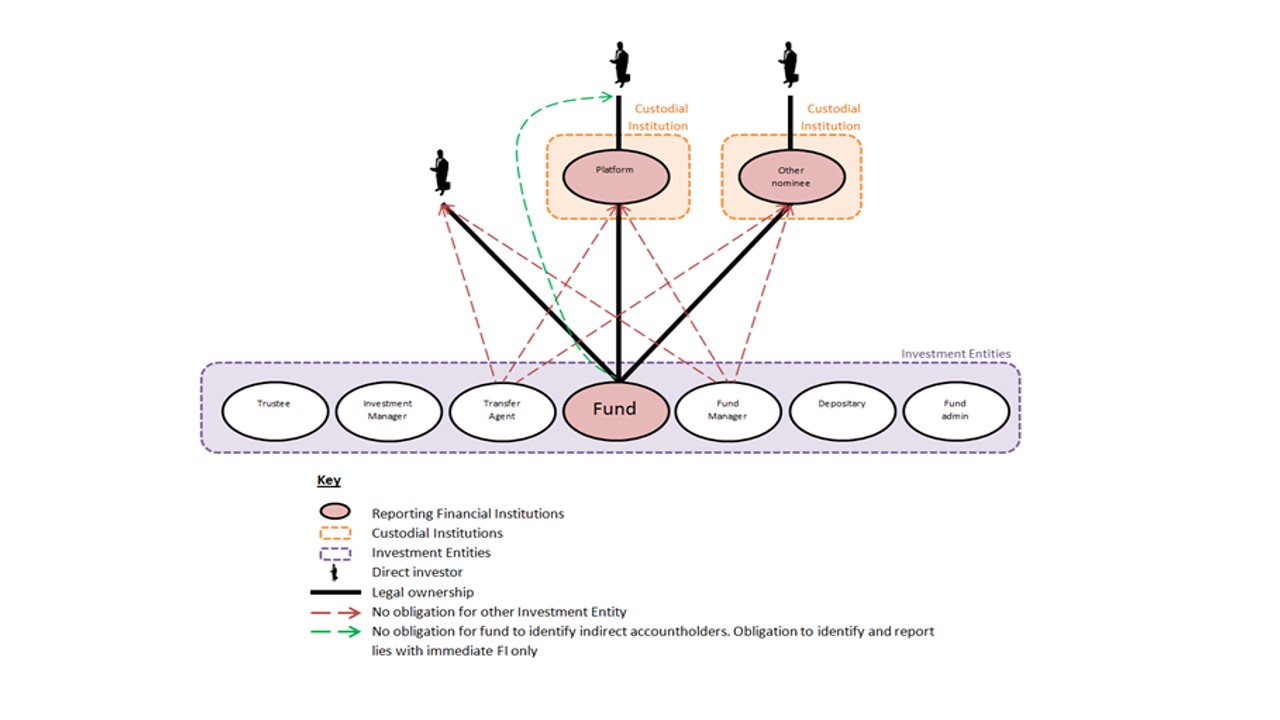

The diagram below illustrates how the account identification and reporting obligations under the Regulations could work for Collective Investment Schemes.

Use this link to view CIS reporting diagram

{kind=link}

Depending on how the fund is structured, various entities may fall within the definition of Investment Entity. The fund itself will need to determine which entity carries out the obligations to identify, verify and report on account holders that are reportable under the various regimes, by reference to its own governance structure and contractual arrangements.

Example

Authorised funds in the UK (which are Authorised Unit Trusts, Open-Ended Investment Companies, and Tax-Transparent Funds) are required to have a fund manager that acts as operator of the fund and is normally assigned responsibility for fulfilling the regulatory obligations of the fund.

Therefore, the fund manager will normally have responsibility for compliance with the obligations in relation to the financial accounts of the fund. In turn, fund operators typically use third party service providers to provide fund administration, including maintaining records of investors, account balances and transaction services provided by the transfer agent. In these cases the fund manager might appoint the third party service provider to fulfil account identification and reporting requirements as they will have the necessary records.

The fund’s account identification and reporting obligations apply only to its immediate account holders. It is required to identify all direct individual Account Holders pursuant to the due diligence obligations outlined in this guidance. Any indirect individual account will be held through a Financial Institution (for example a platform or other nominee), and the fund’s obligation is to identify the direct Account Holder (such as the Financial Institution) only. In turn the intermediary Financial Institution will have its own obligation to identify and report on its Account Holders.

In the diagram the fund would only need to identify any direct individual Account Holders (shown on left hand side), and the Financial Institutions on the share register. It would be required to report information on any of these that are Reportable Persons under the regimes.

In turn Custodial Institutions that act as distributors (and not the fund) would be required to identify and report on their direct Account Holders. The fund has no obligation to identify and report on accounts held indirectly through other Financial Institutions.