IEIM400120 - Background: How it works

How it works

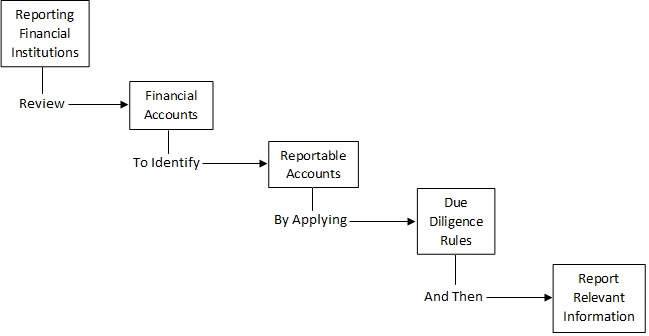

The International Tax Compliance Regulations 2015 bring into effect the obligations that financial institutions have to report details of accounts to HMRC for exchange with other jurisdictions.

Whether the obligations are for the purposes of FATCA or the CRS the basic process is the same:

Use this link to view diagram showing process for reporting details of accounts to HMRC

{kind=link}

Each of these steps is described in the following guidance and the differences in approach under each of the regimes identified.