CFM96840 - Interest restriction: joint ventures: interest allowance (consolidated partnerships) election: example with interest allowance (consolidated partnerships) election

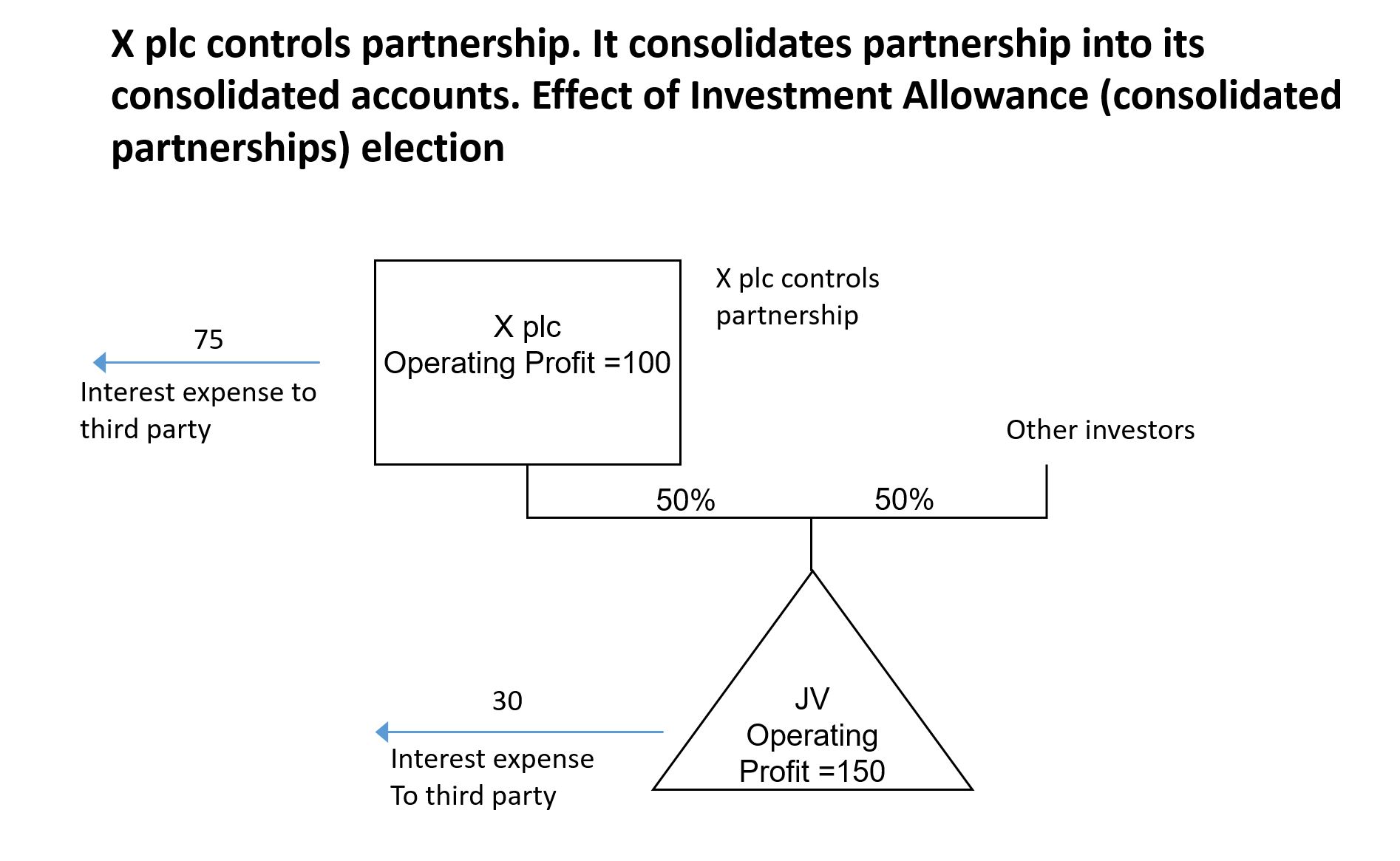

For visual illustration view diagram showing X plc controlling and consolidating a partnership

{kind=link}

The diagram shows X plc controlling a partnership and consolidating it into its accounts following an Investment Allowance (consolidated partnerships) election. X plc has an operating profit of 100 and pays interest of 75 to a third party. X plc and other investors each hold a 50% interest in the partnership. The partnership has an operating profit of 150 and pays interest of 30 to a third party. Because X plc controls the partnership, its results are consolidated.

X plc gets a 50% profit share from the partnership but it controls the partnership. This means that the partnership is consolidated into X plc’s financial statements. X plc has an operating profit of 100 with third party interest expense of 75. The partnership has operating profits of 150 and 30 of third party interest expense.

The position without the election

Firstly assume that an election is not made.

| Accounts | X plc | Partnership | X plc group |

|---|---|---|---|

| Operating profit | 100 | 150 | 250 |

| 3rd party interest expense (QNGIE) | - 75 | - 30 | - 105 |

| Profit before tax | 25 | 120 | 145 |

| Calculation of group ratio | X plc Group |

|---|---|

| Qualifying net group-interest expense (A) | 105 |

| PBT | 145 |

| Add back interest expense | 105 |

| Group EBITDA (B) | 250 |

| Group Ratio (A/B) | 42% |

| Interest allowance | X plc |

|---|---|

| Tax-EBITDA | 175 |

| X plc group ratio | 42% |

| Interest allowance | 74 |

| Net tax-interest expense | 90 |

| Less interest allowance | - 74 |

| Restriction | 16 |

For the purpose of calculating the group ratio X plc picks up a small amount of interest but a large amount of group-EBITDA from the partnership. The group ratio is calculated on a group-EBITDA of 250. However when calculating the interest allowance the group ratio is applied to a tax-EBITDA of 175. This disparity between group-EBITDA and tax-EBITDA causes an interest restriction of 16.

With the consolidated partnership election

Applying the same figures and making an interest allowance (consolidated partnerships) election. Under this election the financial statements for the group are assumed to include a share of the partnership's profits instead of being fully consolidated.

| Accounts | X plc | Partnership | X plc group |

|---|---|---|---|

| Operating profit | 100 | 150 | 100 |

| 3rd party interest expense (QNGIE) | - 75 | - 30 | -75 |

| Share of profits of partnership | - | - | 60 |

| Profit before tax | 25 | 120 | 85 |

| Calculation of group ratio | X plc Group |

|---|---|

| Qualifying net group-interest expense (A) | 75 |

| PBT | 85 |

| Add back interest expense | 75 |

| Group-EBITDA (B) | 160 |

| Group ratio (A/B) | 47% |

| Interest allowance | X plc |

|---|---|

| Tax-EBITDA | 175 |

| X plc group ratio | 47% |

| Interest allowance | 82 |

| Net tax interest expense | 90 |

| Less interest allowance | - 82 |

| Restriction | 8 |

The election is applied by treating the partnership as a joint venture. The election increases the group ratio to 47% and reduces the interest restriction to 8.

However, the worldwide group also has the option to elect into the Investment Allowance (non-consolidated investment) election.

With the consolidated partnership and non-consolidated investment elections

Applying the same figures and making an interest allowance (consolidated partnerships) election and an interest allowance (non-consolidated investment) election.

| Accounts | X plc | Partnership | X plc group |

|---|---|---|---|

| Operating profit | 100 | 150 | 100 |

| 3rd party interest expense(QNGIE) | - 75 | -30 | -75 |

| Share of profits of partnership | - | - | 60 |

| Profit before tax | 25 | 120 | 85 |

- X plc group share of profits from JV - 50%

| Calculation of QNGIE | X plc Group |

|---|---|

| QNGIE in X plc | 75 |

| Share of JV QNGIE | 15 |

| Total QNGIE | 90 |

| Calculation of group-EBITDA | X plc Group |

|---|---|

| Group-EBITDA of X plc group | 160 |

| Reduction in group-EBITDA from JV profits | - 60 |

| Share of JV's Group-EBITDA | 75 |

| Group-EBITDA | 175 |

| Group ratio | 51% |

| Interest allowance | X plc |

|---|---|

| Tax-EBITDA | 175 |

| X plc group ratio | 51% |

| Interest allowance | 90 |

| Net tax-interest expense | 90 |

| Less interest allowance | - 90 |

| Restriction | - |

Here the effect of the non-consolidated investment election with the consolidated partnership election increases the group ratio to 51%. X plc’s net tax-interest expense is not restricted.