CG57400 - Non-resident companies: non-resident group

TCGA92/S14*

A TCGA92/S13* charge could arise on the disposal of an asset by a non-resident company to another company under the control of the same shareholders or participators. TCGA92/S14* prevents this if the transfer is between members of a non-resident group of companies. It does this by applying some of the general Capital Gains Tax rules for groups to non-resident groups for the purposes of calculating the Section 13 charge.

For the purposes of TCGA92/S13* TCGA92/S14 (4)(b) amends the definition of group in TCGA92/S170 by omitting the references to companies resident in the UK and particular types of company. It then defines a non-resident group as being either

- two or more members of the same group, using the amended definition, both of which are non-resident. A UK resident company cannot be a member of the non-resident group. A non-resident company cannot be a member of the UK group. But a UK resident company can group two non-resident companies, see Example 1

or

- the whole of the group if none of the members are resident in the UK.

FA2000/SCH29/PARA1 amended TCGA92/S170 to remove the requirement that members of a group had to be resident on the UK. For the purposes of TCGA92/S14 the definition of a non-resident group remains unchanged by this amendment.

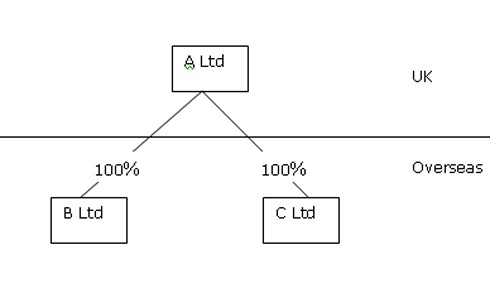

Example 1

{kind=link}

A Ltd is resident in the UK and B Ltd and C Ltd are 100% subsidiaries overseas.

B Ltd and C Ltd form a non-resident group.

A Ltd is not a member of the non resident group but it does have the effect of`grouping’ B Ltd and C Ltd.

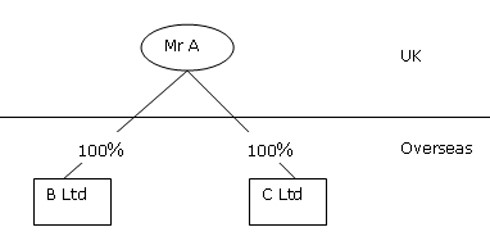

Example 2

{kind=link}

Mr A is resident in the UK and owns 100% of both B Ltd and C Ltd which are resident overseas.

B Ltd and C Ltd do not form a non resident group because they are not members of any group.

Example 3

Mr A is resident in the UK and owns 100% of B Ltd which in turn owns 100% of C Ltd which are both resident overseas.

B Ltd and C Ltd form a non resident group because all of the companies in the group are not resident

* TCGA92/S13 was re-written for disposals from 6th of April 2019 see CG10150.