BLM80550 - sale of lessor companies and similar arrangements: calculating the income amount: adjustments to the basic amount: company becomes a consortium company - example 2 of 2

Section 405 CTA2010

{kind=link}

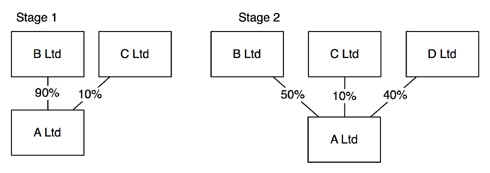

In this example A Ltd is a 75% subsidiary of B Ltd even though B Ltd only owns 90% of the shares in A Ltd. A Ltd is not a consortium company as one company owns more than 75% of the shares in A Ltd.

At stage 2 A Ltd is a consortium company and B Ltd is a member of the consortium. B Ltd has not relinquished the whole of its interest in A Ltd and this must be reflected in an adjustment to the basic amount. There is no change in the interest in A Ltd held by C Ltd.

The amount of the income is restricted to the appropriate percentage of the basic amount.

The appropriate percentage is found by subtracting the ‘ownership percentage’ at the end of the day from 100% even though B Ltd does not own 100% of the shares in A Ltd.

The ownership percentage is the lesser of:

- The percentage of the ordinary share capital of company A owned by company B;

- The percentage to which company B is beneficially entitled of any profits available for distribution to equity holders of Company A;

- The percentage to which company B would be beneficially entitled of any assets of Company A available for distribution to its equity holders on a winding up.

In this case the ownership percentage is 50% and the appropriate percentage is therefore 50%. Note that once this transaction has been completed C Ltd is now able to surrender to and claim losses from A Ltd as it is a member of a consortium. The 50% appropriate percentage therefore accurately reflects the change in access to group relief.