BLM80360 - Sale of lessor companies and similar arrangements: establishing change of ownership: exceptions to qualifying change of ownership

CTA2010/S395

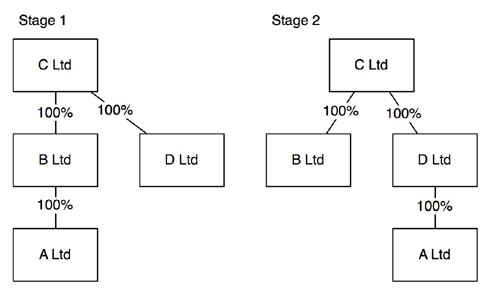

It is possible for a qualifying change in ownership to occur without any true change in the economic ownership of the lessor company - company A.

Use this link to view the example

{kind=link}

The principal company of A Ltd is C Ltd. Shares in A Ltd are sold by B Ltd to D Ltd. A Ltd ceases to be a 75% subsidiary of B Ltd. This is a relevant change in the relationship between A Ltd and C Ltd. However it is clear that A Ltd has not ‘changed hands’: it remains in the group.

CTA2010/S395 offers an exception in the case of intra-group reorganizations so that there is no qualifying change of ownership. The exception applies when every company involved in the chain of ownership running from company A to the principal company remains a qualifying 75% subsidiary of the principal company at the end of the day.

In this example A Ltd B Ltd and D Ltd remain 75% subsidiaries of the principal company. For this exception to apply the relationship tested is that between each company and the principal company. A chain of 75% subsidiaries will not suffice for these purposes.