BLM80330 - Sale of lessor companies and similar arrangements: establishing change of ownership: consortia: consortia and the wider group

CTA2010/S397/S398

S394 looks through the consortium member to the principal company when the consortium member is a 75% subsidiary of another company.

Where the consortium member is a 75% subsidiary of another company there is a relevant change in the relationship between company A the lessor company and its principal company when ever there is either:

- a fall in the ownership proportion: or

- a company which is part of the chain of ownership between Company A, the lessor company and the principal company stops being a 75% subsidiary.

{kind=link}

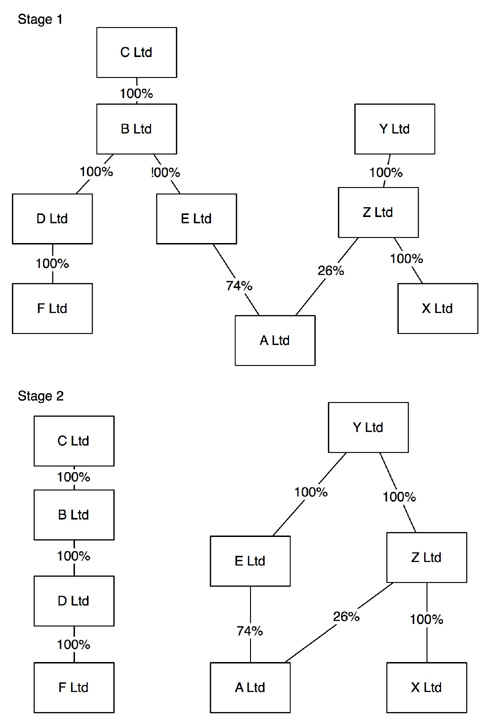

In this example the principal companies of A Ltd are C Ltd and Y Ltd.

The chain of relationships from A Ltd to C Ltd runs through E Ltd and B Ltd.

B Ltd sells all of its holding in E Ltd to Y Ltd.

There is a relevant change in the relationship between A Ltd and C Ltd, its principal company because E Ltd ceases to be a 75% subsidiary of B Ltd.

There is therefore a qualifying change of ownership in relation to A Ltd.