Restaurants

This publication is intended for Valuation Officers. It may contain links to internal resources that are not available through this version.

1.1 This guidance applies to restaurants, cafes, snack bars, hot food takeaways, restaurants in former public houses, restaurants with rooms, restaurants in regional shopping centres and some roadside restaurants such as local fish and chip shops and specialised or ethnic food restaurants away from a town centre or retail location. Examples of the types of restaurants covered by this section are attached at Appendix 1.

1.2 This section excludes:

| Drive-to/ drive-thru restaurants | SCAT 091 and 092 ([Rating Manual: section 6 part 3 - section 365](https://www.gov.uk/guidance/rating-manual-section-6-part-3-valuation-of-all-property-classes/section-365-drive-in-and-drive-thru-restaurants)) |

| Motorway service stations | SCAT 194 ([Rating Manual: section 6 part 3 - section 710](https://www.gov.uk/guidance/rating-manual-section-6-part-3-valuation-of-all-property-classes/section-710-motorway-service-areas-major-road-service-areas)) |

| Food courts in regional shopping centres | SCAT 104 ([Rating Manual: section 6 part 3 - section 920](https://www.gov.uk/guidance/rating-manual-section-6-part-3-valuation-of-all-property-classes/section-920-shops-and-shopping-centres)) |

| Public houses | SCAT 226 and 227 |

| Inns | SCAT 062 |

1.3 At the public house/restaurant interface consult the Rating Manual: section 6 part 3 – section 825 public houses, licensed restaurants and wine bars.

1.4 This guidance excludes certain Roadside Restaurants SCAT 238 ([Rating Manual: section 6 part 3 - section 880][(https://www.gov.uk/guidance/rating-manual-section-6-part-3-valuation-of-all-property-classes/section-825-public-houses-licensed-restaurants-and-wine-bars)). These roadside restaurants primarily serve the needs of the motorist and normally stand-alone at the side of main roads and are sometimes sign posted ‘Services’ from the highway.

1.5 Hot Food Takeaways do not fall within the normal definition of a restaurant. However, reference is made within this section to survey and valuation considerations for this type of occupation.

| List descriptions: | Restaurant and premises, cafe and premises, restaurant with rooms |

| Primary description code: | CR (Restaurants) CR1 (Cafes) CS (Hot Food Takeaways) |

| 234 (Restaurants) | |

| 409 (Cafe) | |

| SCAT codes: | 442 (Hot Food Takeaways) |

| 500 (Cafes and restaurants within/ part of a specialist property) | |

| Suffix: | G (Generalist) |

3.1 Generalist valuers are responsible for the survey and valuation of this class.

3.2 It is anticipated that each Regional Valuation Unit (RVU) will have a named individual responsible for the class. More than one named individual is recommended for succession planning.

3.3 It is also recommended that each RVU should allocate a named coordinator, or Lead Valuer, to act as a point of contact within the Unit. This Lead Valuer will be responsible for assisting in the delivery of the Unit’s valuation scheme and also for liaising on value and technical issues with other Lead Valuers across adjoining Units. The Lead Valuer will be responsible for ensuring compliance with this section.

3.4 For establishments that are at the interface with Public Houses refer to paragraph 8.8.3.

4.1 The Restaurant Class Co-ordination Team (CCT) has overall responsibility for the co-ordination of this class. The team are responsible for the approach to and the accuracy and consistency of E/ A3 restaurant valuations.

4.2 The Practice Note describes the valuation basis for revaluation and the CCT will provide advice as necessary during the life of the rating lists.

4.3 Valuers have a responsibility to:

- follow the advice given at all times - practice notes are mandatory

- not depart from the guidance given on appeals or maintenance work, without approval from the co-ordination team.

5.1 A restaurant must comply with certain legislation to trade and compliance is assumed.

5.2 Prior to 2005 The Town and Country Planning use classes order 1987 (as amended) determined permitted use. This Order was amended in England in 2005 dividing the A3 restaurant Class further, into A4 Drinking establishments and A5 Hot food takeaways.

5.3 In England the Town and Country Planning (Use Classes) (Amendment)(England) Regulations 2020 further amended use classes. This created, from 01 September 2020, a new broad “Commercial, business and service” use class (Class E) which includes:

- shops other than F2 (formerly A1)

- financial and professional services (formerly A2)

- café or restaurant (formerly A3)

- office other than a use within Class A2 (formerly B1A)

- non-residential: clinics, health centres, crèches, day nurseries, day centre (formerly D1)

- gymnasiums, indoor recreations not involving motorised vehicles or firearms (formerly D2)

- research and development of products or processes (formerly B1B)

- industrial processes (capable of being carried out in any residential area without causing detriment to the amenity of the area due to noise, vibration, smell, fumes, smoke, soot, ash, dust or grit (formerly B1C)

Pub, wine bar or drinking establishments (formerly A4) and hot food takeaway (some on-site consumption) (formerly A5) are now incorporated in the Sui Generis class

5.4 The amendments to the Order only apply in England and do not apply in Wales which retained the original A3 Use Class under the 1987 Order.

5.5 The sale of alcohol on the premises

Premises serving alcohol are required to hold a Premises Licence issued by the Local Authority under the Licensing Act 2003. It is necessary for both the proprietor and the property to be licensed. The Licensing Act 2003 is the principal Act relating to Licensed Property in England and Wales. Thus,

- any business or other organisation that sells alcohol on a permanent basis needs to have obtained a premises licence.

- anyone who plans to sell or supply alcohol or authorise the sale or supply of alcohol must have obtained a personal licence.

5.6 The details of the licence held will be displayed at the property.

5.7 Hot Food Takeaways supplying hot food after 11pm are also required to hold a Premises Licence

6.1 Inspections should be carried out in accordance with the Valuation Office Agency Code of Measuring Practice.

6.2 Restaurants should be measured to Net Internal Area (NIA) for rating purposes in accordance with the RICS Code of Measuring Practice 6th edition or its replacement.

6.3 NIA is taken as the usable area within a building measured to the face of the internal finish of perimeter or party walls ignoring skirting boards and taking each floor into account.

6.4 NIA will normally exclude toilets and associated lobbies used solely for staff purposes. However toilets in restaurants made available to customers will need to be measured and included in the valuation.

6.5 Separate areas should be provided for the respective uses on each floor level, in particular for the following uses within the hereditament: restaurant, servery, bar, kitchen, stores, offices, cold stores and upper level stores.

6.6 Inspection

6.7 The Survey Template can be found in the Electronic Document Management System (EDRM). This will need to be completed following inspection. The checklist at Appendix 2 identifies the information that will need to be gathered to properly complete the survey.

6.8 All features likely to have a bearing on value should be recorded in sufficient detail. Their importance will vary, dependent upon the nature of the custom being sought, and the trade potential for the particular style of catering operation. Prominence of position may play an important part in determining the value of a café, snack bar or burger restaurant. The characteristics of the surrounding areas, the presence of parking (or other transport) facilities and the style of a building may have a greater influence for the more exclusive restaurants.

6.9 Accommodation Use, Other Addition and Adjustment Codes

A summary of the main codes for use outside of Central London are shown at Table 1 below. For the main accommodation use codes within Central London see paragraph 7.3 of this section.

7.1 Rating Surveys should be captured on the Rating Support Application (RSA) and plans and surveys stored in the property folder of the EDRM.

7.2 The common Accommodation Use Codes used to record the various areas comprising the restaurant premises are outlined in Survaid for non-zoned restaurants, shops & restaurant users. A summary of the main codes used outside of Central London are shown in Table 1. These relativities are generally used for the overall method of valuation (Scale PROVA3) - not to be used with the zoned method.

7.3 For Central London the common Accommodation Use Codes used to record the various areas comprising the restaurant premises are outlined in Survaid for non-zoned restaurants, shops & restaurant users. These relativities are used for the overall method of valuation (Scale LA3USE) - not to be used with the zoned method.

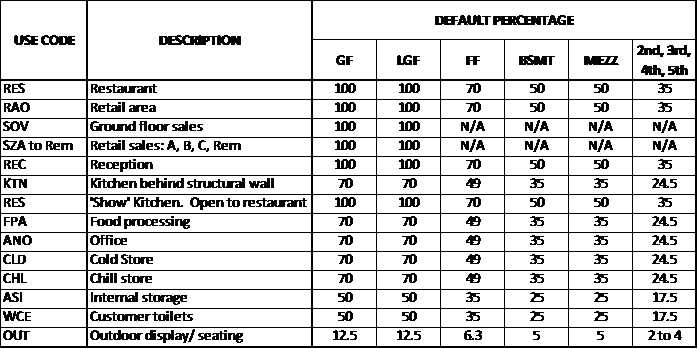

Table 1 referred to at paragraph 7.2 above. Relativities for use in the Overall method of valuation (PROVA3 scale) for use outside of Central London are as follows:

{kind=link}

7.4 As a general rule the use of MEZZ to describe a Mezzanine floor level (which defaults to a value of 50% of the main rate) should be avoided and ‘01’ - First floor (which defaults to 70% of the main rate) should be used for both analysis and valuation. MEZZ must only be used for platforms in situations where for example accommodation is limited by headroom.

7.5 For properties that are predominantly non ground floor, relativities should be based on a factor of 1.00 for the restaurant area and the appropriate scale path adopted. Refer to Survaid for a comprehensive list of accommodation use codes and percentages of the main rate to be used.

7.6 High rise restaurants in Tower blocks should also refer to an appropriate scale. The ‘Tower’ scale path should be used for high rise restaurants in tower blocks.

Methods of valuation

Introduction

8.1 Rents paid in respect of restaurants appear to increasingly support an overall approach when performing analyses, as opposed to the traditional zoned method for shops: the evidence may support a different valuation approach to that of the surrounding shops. In a town/ city centre, in general, one would expect to see the value of restaurants varying, as Zone A pitches do. However, there may not be any direct correlation between the value of a restaurant expressed overall as a £/m², and the zone A value of the shops in the same locality. There will be occasions when a specific feature i.e. tourist hotspot or the existence of a fashionable area or ‘restaurant culture’ may result in premium values for restaurant use, where retail values in the vicinity remain unaffected.

8.2 However in some prime high Zone A pitches the overall price of restaurants may lead to a lower valuation than for a shop. For example in a shopping centre the landlord will want to have a mixed tenant use and may be prepared to accept lower rents from restaurant/café users in order to maximise the value of their development by encouraging shoppers to linger and take lunch as part of their visit. Lower rents for these users in such shopping centres may also reflect the restricted opening hours of the centre.

8.3 There may be occasions where the levels of value evidenced for restaurant units are not distinct from that evidenced for nearby shops. Where this is the case, it may be appropriate to adopt a zoned approach in line with neighbouring shops.

8.4 In all cases local evidence is key to determining the appropriate approach to valuation. All available evidence should be thoroughly collated, adjusted and analysed to provide the best possible indication of the prevailing approach in the locality. The resultant approach should then be adopted when making valuations for rating purposes. Once the evidence has been considered there must be an awareness of the need for consistency in the valuation approach adopted.

8.5 Rental Information and Analysis

8.5.1 Primary valuations are to be derived from rental evidence.

8.5.2 The Notice Requesting Statutory Information (Form of Return) for this class of property is typically VO 6003 - generally used for all bulk classes. This particularly relates to restaurants in areas such as retail or commercial or where there is a mix of leisure and commercial and where a defined rental market exists.

8.5.3 Rental evidence will probably indicate a wide range of values and should be adjusted for factors listed below to enable comparison. It is important to exercise care when considering these factors for the following reasons:

Shell units

8.5.4 It is important to establish whether rents are for an unfitted shell or for a finished unit. With shell units it is helpful to establish the fitting out costs. The majority of restaurants have air-conditioning, quality customer toilets, larger catering kitchens and a level of finish to a standard higher than that found for example in shops. The rent passing therefore needs to be uplifted to reflect the degree of rateable fitting out the tenant is responsible for. See Rating Manual: section 4 part 1 - practice note 1 2023 rental adjustment.

Residential parts

8.5.5 Many restaurants are situated in buildings with residential parts. Exercise caution when analysing a rent that includes living accommodation as this will need to be adjusted prior to analysis. The amount deducted will be that for living accommodation in a composite hereditament rather than the amount the flat would notionally let for on the open market as a residential Assured Shorthold Tenancy.

8.5.6 As the restaurant market is labour intensive there may be a higher proportion of the actual rent placed on the residential upper part than say for a nearby shop which has no need to house staff. Living accommodation enables the proprietor to retain staff, in a climate of anti-social working hours and expensive or non-existent alternative accommodation in the locality.

8.5.7 Alternatively, in the most attractive properties or localities the proprietor may highly value the living accommodation for their own occupation, which could also enhance their rental bid for the property.

Other Adjustments

8.5.8 To enable comparison, additions should be made for car parking within the curtilage (where it is in excess of that normally found in that locality), air-conditioning (where it is not already reflected in the basic price), and the presence of outside seating areas, which attract trade during fine weather and allow smokers to smoke. Occasionally, some element of quantum may also exist for large units.

8.5.9 Evidence may also reveal a dual set of values, with unlicensed café’s and tearooms having lower values than licensed premises or fast food outlets.

8.6 Valuation Approach

Location

8.6.1 Rental evidence is most commonly available in urban or commercial areas. Restaurants situated in rural or suburban areas are frequently freehold and care should be taken to ensure that comparable evidence is imported from similar locations. Location may be fundamental to business potential and hence value. Proximity to centres of population/ commercial areas, good transport links and tourist areas of natural beauty or historic interest will all enhance the value. Care should be taken in the valuation of restaurants in enclosed shopping malls, where the trading hours and hence income are limited by the opening pattern of the centre. Even with the benefits of good pedestrian footfall a mall offers, they may be disadvantaged over restaurants just outside the mall which benefit from unrestricted evening footfall. Broadly speaking, three different schemes of valuation can be considered.

Overall Method

8.6.2 The floor area of each part of the building is established and the appropriate level of value applied to each part depending on its use and floor level. For example, the main dining and customer seating areas on the ground floor are at 100% of value, and kitchens, stores, customer toilets, etc are expressed as a fraction or percentage of this. This results in an area ‘in terms of main space’ (ITMS) with which to analyse the adjusted rent and ultimately to which the main space value is applied when making the valuation.

8.6.3 There is normally sufficient market evidence to enable rents to be analysed on the overall basis and for schemes of valuation to be derived from such analysis. An advantage of the overall approach is that it can be used for restaurants of all shapes and configurations. Comparison can easily be made between a variety of previous property uses, such as former banks, warehouses, shops, pubs or houses, in locations that share the same attributes.

8.6.4 The e-goad application can assist in determining the occupying uses of a retail locality. It shows the Use Classes and can help determine whether a property is in a mainly core A1 retail parade or in a fringe non A1 or leisure location.

8.6.5 The Restaurant overall scale path that is used generally for ground floor restaurants is PROVA3. This adjusts different use codes in the valuation and areas from basement to fifth floors ‘in terms of main space’ (ITMS). The ancillary areas are taken at 70%-50% in relation to the main restaurant accommodation.

8.6.6 Properties previously valued as retail can transfer to this scale path with little data amendment albeit the capture of kitchens and ancillary space should be reviewed. Zones A to remainder will show on RSA with the same rate applied. This may be confusing if not fully understood that an overall rate has been applied but can be an effective approach to transferring survey data of former retail zoned properties to restaurant overall valuations. It also has the benefit of protecting the data should the restaurant revert to retail use when the zoning data is needed again. See 8.6.7 to 8.6.10 below concerning retail allowances that may apply to A1 use but not to A3 use.

8.6.7 Properties valued for retail purposes with features such as non-standard frontage (for example bank fortress frontages or hard frontages) or with irregular layouts can be considered as being disadvantaged compared to other retail properties with a regular layout. Allowances are sometimes applied to the zoned values.

8.6.8 However, these types of properties have proved to be attractive to restaurant operators, as they often have character without having any negative effect on their business operations. As a result, when valuing restaurants on an overall basis it is not appropriate to apply these allowances and they should be removed. Restaurant rental evidence should be analysed without these allowances.

8.6.9 Examples where allowances are not considered appropriate for restaurant users include irregular shape - including front/depth ratio; masked areas; columns; dividing walls; double units, hard frontage etc.

8.6.10 Allowances for quantum should only be considered where rental evidence supports a reduction and if appropriate it can be reflected in the overall price per metre adopted. Surplus Floor Area

8.6.11 Surplus accommodation of no benefit to the occupier in the open market may need to be considered. This factor is most apparent in congested urban/ historic centres, where buildings are old and converted from a previous use. It occurs when an occupier is anxious to secure a property in a particular area, such as a prime tourist location. The occupier takes a multi-floor property but mainly has use for the lower floors only. Upper floors may be presented as customer dining space or storage but in reality demand is low due to difficulties of access, and they are difficult to serve from the kitchen. It may be necessary to discount the analysis and valuation of this space to reflect its marginal contribution to the business and high costs of operation.

8.6.12 Allowances may sometimes be appropriate. For example converted properties or historic buildings may have areas surplus to normal restaurant requirements.

8.6.13 In rare cases these allowances may take the form of line adjustments. If there is a substantial amount of unused space which at AVD was not required by the market, a nil value for some or all of these unused areas may be appropriate.

8.6.14 For restaurants that are predominantly trading from non-ground floors such as from basements or upper floors an overall or non-zoned scale can be used. This applies the same relativities as the ground floor scale path, namely based on 100% for restaurant space with the ancillary uses in relation.

8.6.15 Where there are a number of these properties in a locality, a separate non ground floor sub-location code may be appropriate with the correct relativities adopted.

8.6.16 Whilst upper floor restaurants may be considered to have lower values in some circumstances the valuer needs to be aware of any value significant aspects. For example where the dining area overlooks an area of interest this may have a higher value than on the ground floor and should be adjusted accordingly.

Restaurants in high rise buildings and mixed commercial use properties

8.6.17 When valuing restaurants on the upper floors of high rise buildings a TOWER scale can be used. This will apply restaurant values to upper floors above the fifth floor at 100% relativity. This type of property is more likely to be found in larger cities and the office values usually compare.

8.6.18 Rental analysis and valuations should be coordinated with valuers responsible for the other commercial uses in the building as the levels of values may relate.

8.6.19 The value of ancillary areas in these cases will generally be 100%.

Outside seating

8.6.20 Outside seating areas have become more important since the smoking ban and can be valued where the area is defined. These areas should be captured as use code OUT, as a line entry, which will give a relativity of one eighth.

8.6.21 Sometimes these are semi-enclosed with heating provided or have terraces with attractive views. For those outside seating areas which are enclosed with a substantial roof covering, i.e. not fabric or similar covering, will need to be captured as a two-line entry. The first line entry as OUT, for the area of outside seating at a scale factor of 0.125, regardless of floor level and a second line entry of CNP with the same area, at a scale factor of 0.10. Any feature, positive or negative which has a bearing on value should be noted and will need to be reflected in the rate adopted.

8.6.22 Seating available on pavements is not generally part of the hereditament. Its presence can enhance the attractiveness of the restaurant and act as an incentive to a restaurant occupier to take the premises. Restaurants with outside seating will most likely be valued on an overall basis.

8.7 The Zoning Method

8.7.1 Many restaurants have taken over pre-existing retail units. Where there is minimal modification to the standard retail unit, and general levels of rental evidence supports it, zoning may still be appropriate. However, it must be borne in mind that levels of value for properties occupied as restaurants, may be significantly different to that of adjacent and similar retail units. Where the rents for these properties, in terms of zone A, devalue at a higher amount than the surrounding shops it may be more appropriate to value the restaurants on an overall basis. This allows for a worthwhile “check” or comparison with restaurants located in the vicinity.

8.7.2 Similarly, it will not be appropriate to zone where there have been significant alterations. For example, kitchen enlargement or extension, installation of quality customer toilets, or improvement to rear parts to make attractive customer seating space, particularly if there is for example, an outlook onto a garden, or a view.

8.7.3 Traditional takeaways in retail units, which do not offer any customer seating, are more likely to be comparable to the surrounding retail units and the zoned approach is likely be more appropriate. However, if the rents on such premises are higher than the comparable shop rents, that should be reflected in the valuation, either by a higher zone A or the application of a survey unit or end adjustment to the prevailing zone A value. In exceptional circumstances this class of property could be valued overall, for example if the Hot Food Takeaway is occupied together with a restaurant or seating area.

8.8 Licensed restaurants or Public Houses

8.8.1 These may share many common features and a trade based valuation may be more appropriate particularly in the absence of any relevant rental evidence.

8.8.2 The VO Approved Guide to the Valuation of Public Houses has been arrived at from the adjustment and analysis of public house open market rents. It will not therefore be appropriate to use the Approved Guide in arriving at the rating assessment for restaurant hereditaments.

8.8.3 However, where a licensed restaurant is in the nature of, and shares many features and characteristics of, a public house/ public house restaurant then a trade based valuation in accordance with the Approved Guide may produce a more accurate assessment than a floor area approach.

8.8.4 In all instances where it is considered that the use of the Approved Guide may be appropriate in valuing a licensed restaurant then it is essential that the Licensed Property Specialist for the Unit be consulted.

8.8.5 If the Approved Guide is inappropriate but there is no direct physical comparable, for example in a remote rural location, then a valuation using the full Receipts and Expenditure method of valuation may be adopted where the restaurant is operated on a fully commercial basis. Guidance on the Receipts and Expenditure method of valuation is contained in Rating Manual Section 4: Part 2. Alternatively, applying a rental percentage to an estimate of the fair maintainable trade at the AVD may produce a more accurate estimate of rental value/ rateable value.

8.8.6 Direct comparison of restaurants with public houses is difficult as methods of valuation are different. Furthermore, the floor areas of public houses are not recorded. However, it is recommended that where these are in the same locality they are reviewed together where possible.

8.9 Hybrid Properties

8.9.1 Properties which are in non-retail locations and which have a mix of commercial uses including a restaurant may also be valued having regard to the other uses. For example, where there is an interface with Public Houses or Hotels. This may also include former public houses now operating as a restaurant (restaurants operating in a former public house shell).

8.9.2 Where the restaurant is of a particularly unusual nature, there will be more emphasis on gaining the full receipts picture together with, or in place of, any rental information (if indeed any rent is payable). In these cases it should be considered in the first instance whether to issue NRSI VO 6010 issued to Public Houses or VO6011 (receipts only).

8.9.3 The CCT should be consulted in the first instance before any forms are issued.

Restaurant with rooms

8.9.4 Some restaurants offer rooms for overnight stays for diners. The value of these rooms will vary, possibly with the DBU valuation approach considered appropriate. In exceptional circumstances a licensed restaurant/ restaurant with rooms (particularly a destination type property) may share physical features and characteristics with small boutique hotels public houses/ pub restaurants with rooms or even a guest house/ B&B establishment. In such cases consultation may be needed with the CCT. It may be more appropriate to arrive at the rateable value by applying a rental percentage to the Fair Maintainable Trade (FMT) at the Antecedent Valuation Date (AVD) using gross receipts excluding VAT. In these cases it may be necessary to issue a NSRI 6030 (gross receipts) or 6036 (gross receipts and information for full Receipts and Expenditure) to provide receipts information.

8.9.5 Before any action of this sort is taken the matter should be referred to the CCT (see 8.9.3).

8.10 Air Conditioning

8.10.1 The valuation approach to air-conditioning will be like that adopted for retail shops. Rating Manual: 5a: Shops and shopping centres - Practice note 1 2026: air conditioning in shops.

8.11 Quality

8.11.1 Adjustments should not be made for quality other than in exceptional circumstances.

8.12 Key rents

8.12.1 All properties where a key rent has been identified should be inspected.

The following sources are available to Property Inspectors and valuers dealing with the valuation and maintenance of restaurants.

- Rating Support Application (RSA)

- Survaid

- Class Coordination Team for Retail 3

- National Valuation Unit (NVU)

Restaurants trade in a wide range of diverse locations, from prime city centre to isolated destinations.

Restaurants provide food for consumption on the premises (this is generally planning use E/ A3), although some offer takeaway food as well. Dining may be formal or casual and either table or self-service. The majority of restaurants are licensed to sell alcohol.

The following are the main types and locality of restaurant:

City centre/ high street

These may be in retail units or in former commercial buildings such as banks or other prestige premises with architectural qualities and will predominantly occupy ground floor accommodation.

Rental evidence in respect of non-standard retail units may have justified allowances in certain circumstances for perceived ‘disabilities’, such as fortress frontages, shape and the like where previously zoned. However, these are more likely to be features that will be seen as a benefit to restaurant occupiers and such end allowances will be inappropriate. Rental evidence for this type of building is unlikely to support any such allowance when analysed overall for this type of frontage and indeed may show a premium when compared to rents passing in respect of other uses.

Upper floor and basement restaurants

Restaurants may occupy space above or below other commercial premises and it is expected that, as a general rule, the value of such restaurants will be less (on a like for like basis) than that of restaurants on the ground floor in the same locality. The visibility of the entrance, width of and ease of access are factors to be considered as value relevant to the unit.

The important exception to this generality will be high level restaurants in prestige or iconic buildings whose restaurants serve food against a backdrop of stunning views over the Capital. Values can be comparable to commercial office rates.

Restaurants retaining retail space at the front

These are retail units where part has been converted to use as a restaurant. Generally, the front portion of the unit has retained its retail use, possibly as a condition of planning permission. The retail use will vary, but is often food related.

Careful consideration of the valuation approach will be required to determine whether an overall, zoned or hybrid approach is appropriate. Regard should be given to local market evidence where available.

Restaurants with rooms

Some restaurants offer rooms for overnight stays for diners. The value of these rooms will vary. A Double Bed Unit (DBU) valuation approach should be considered where appropriate. In exceptional circumstances a licensed restaurant/ restaurant with rooms (particularly a destination type property) may share physical features and characteristics with small boutique hotels, public houses/pub restaurants with rooms or even a guest house/ B&B establishment. In such cases consultation may be needed with the CCT. It may be more appropriate to arrive at the rateable value by applying a rental percentage to the Fair Maintainable Trade (FMT) at the AVD (gross receipts exclude VAT). In these cases it may be necessary to issue a NSRI 6030 (gross receipts) or 6036 (gross receipts and info for full R&E) to provide receipts information. Before any action of this sort is taken the matter should be referred to the CCT.

Restaurants in tertiary or rural locations

These will include restaurants in ‘non-restaurant’ locations or away from hubs of leisure/ hospitality activity as well as rural premises.

For valuation and maintenance purposes restaurants may need to be put into groups having regard to local evidence. An overall scheme of valuation can often be established based on rental evidence for differing locations. Such schemes may be helpful in valuing freehold properties that have been converted to restaurants from other uses, including public houses.

Factors that may affect the overall price adopted are: * tertiary urban location * proximity to main arterial route * car parking * converted units in such locations often have no shop front so the overall approach is appropriate

The overall price may vary between rural locations. More affluent commuter villages with good transport links and large catchments may show a premium for restaurant values over other rural locations.

There may be destination restaurants to which people are prepared to travel as they have a good reputation, or are in scenic locations even though they are isolated. A rural tone will help in the assessment of such properties in the absence of rental evidence.

Unlicensed restaurants

This includes operations that are much the same as conventional restaurants but where, for various reasons, a Premises Licence (Licensing Act 2003) has not been applied for or granted. In this case, customers may bring their own alcohol and the restaurant may then charge a ‘corkage’ fee.

There may be restrictions on business hours.

Hot food takeaways combined with restaurants

Some restaurants may also provide a takeaway service. This service may be run from the same counter as the main restaurant area, or from a completely separate entrance or counter. Decide on the principle use (restaurant or takeaway) and value accordingly.

Coffee shops and sandwich bars

Many sandwich outlets and coffee shops where hot food is not generally cooked on the premises are now incorporated into use class E.

1. Market appraisal

1.1 The restaurant sector undoubtedly suffered during the COVID-19 pandemic and in subsequent years it has continued to struggle with several large chain restaurants consolidating their portfolio.

1.2 During the pandemic the restaurant sector had to adapt to the ever-changing circumstances and bring their business model in line by offering delivery service (increase in collaborations with external delivery operators). The year-on-year growth of delivery from restaurants has continued with customers enjoying the ease, convenience of consuming restaurant quality food at home. Whilst sales at eat-in restaurants are recovering since the COVID-19 pandemic and in consequence delivery and takeaways are a smaller share of restaurants combined trade than they were during COVID-19, delivery and takeaway remains a significant element of restaurants operations. It is important that restaurants optimise delivery logistics and partnerships to serve consumers who prefer ordering by delivery and take-away, while continuing to provide compelling reasons for other customers to eat at the restaurant.

1.3 Operational challenges faced by restaurant sector businesses include securing sufficient staff, including skills such as chefs, whilst also manging the pressure on margins caused by rises in prices of raw materials and overheads. In addition, economic factors affect some customers financial ability to eat out.

1.4 The impact of no-shows and last-minute cancellations can be challenging for the restaurant sector. It is reported that there has been a 40% increase in no-shows since 2022, raising to 57% for restaurants located in London, which are having with a significant impact on food waste, staff morale and revenue.

1.5 The Restaurant sector also has emerging opportunities There appears to be demand for restaurant experiences including socialisation, celebration and culinary exploration. Restaurants are no longer seen as just a place to eat — people want an experience, something ‘a little different from the norm’. Adapting to changing dining trends and customer demands include healthier options and increased awareness of food allergies, providing all-inclusive menus, creating more convenient and quicker menu choices.

1.6 There has been a rise in popularity of the quick service restaurants (QSR) as they are fitting better with some people’s lifestyles, as some customers do not always want to have to spend an hour or two in a restaurant for a meal. The menus are kept simple and with an increased use of digital platforms, table ordering with QR codes and online ordering. This sector has also sought collaborations with Supermarkets and other partnerships to expand their brand and to reach new customers.

1.7 Larger, fine dining and more bespoke restaurants can still thrive. These are largely centred around central locations in London and bigger cities.

1.8 Business expansion in the restaurant sector is generally on a lesser scale than has been evident at the last revaluation. Any expansion is mindful, choosing locations carefully and being creative with any new openings. Larger chains now consider the better sites to be in shopping centres, retail parks, tourist destinations and travel hubs.

1.9 Restaurants and cafes are continuing to capitalise on the changing shape of the High Street by acquiring buildings with character and history in addition to the re-purposing of buildings in the more traditional and central retail locations.

2. Changes from the last practice note

2.1 There are no significant changes from the 2023 Practice Note.

2.2 The scope of this Practice Note is to deal solely with Restaurants, Cafés and Snack Bars which excludes Roadside restaurants (SCat 238) (See RM: Section 5a: Roadside restaurants). In addition, this Practice Note does not cover Drive-to (SCat 091) and Drive-thru restaurants (SCat 092) (RM: Section 5a: Drive-to and drive-thru restaurants).

3. Ratepayer discussions

3.1 These have taken place and are ongoing. In general discussions suggest that the market remains relatively flat. Although rents are starting to recover in some areas, they remain below levels achieved prior to the pandemic. It is noted that recovery tends to be stronger in the more traditional and prime restaurant areas, with secondary areas seeing a more modest recovery. Whilst tourist locations appear to have held up better than other locations since the last Antecedent Valuation Date (AVD) of 1 April 2021.

3.12 In general the demand for larger units is limited with any potential new occupiers remaining cautious about entering the market. The market expectation is that incentives may be needed to secure deals for these larger units over the line which may include longer rent-free periods, typically of 12 to 18 months and in some cases capital contributions.

3.13 There is generally more interest in smaller units, with independent operators willing to ‘have a go’ in the market, these are generally related to smaller restaurants and cafes in standard retail locations.

4. Valuation scheme

4.1 The valuation scale generally adopted for restaurants valued on an overall method is V1SPROVA31 with the relativities in paragraph 7.2 of the Rating Manual (Table 1). For Central London the scale V1SLA3USE1 should generally be used.

4.2 Where properties have a restaurant area main space that is predominately non-ground floor it is necessary to be aware of the relativities in valuation scale V1SPROVA31. In these predominantly non-ground floor hereditaments, it may be more appropriate to use the scale V1SNONZONED1 or V1SGPOVERAL1 (for restaurants on levels up to floor 5).

4.3 A TOWER scale path is available for premises on upper floors in high rise buildings (generally above floor 5). The Central London scale V1SLA3TOWER can also be used in the Provinces.

4.4 Method of valuation

The Rating Manual gives further guidance on valuation approaches.

4.4.1 In a town or shopping centre it is important to carefully consider the method of valuation to adopt, whether it be an overall method or on a zoned basis and change if necessary.

4.4.2 The tenant mix of the locality and footfall needs to be considered together with the rental evidence available.

4.4.3 Restaurants valued as overall should have a separate sub-location code and not be included within zoned sub-locations, to facilitate proper comparison.

4.5 Overall method of valuation

4.5.1 Generally rents paid for restaurants away from core retail locations support the overall method of valuation. The relativities used for rental analysis must relate to the valuation approach adopted.

4.5.2 It is important to have regard to the tenant mix in fringe areas away from a prime central retail pitch and consider the relative footfall, whether that is daytime or evening footfall. An overall approach is appropriate where there is a predominance of non-core uses and/ or mainly evening or leisure trade.

4.5.3 Where large kitchens have been created, other significant alterations have been made or where there is a large rear dining area the overall valuation approach is more appropriate than a zoned method.

4.5.4 The main dining area is valued at 100%. Where kitchens, food preparation and servery areas are separated from the main dining area by non-structural walls/stud partitioning these areas should also be valued at 100%. Where the kitchen, food preparation and servery areas and most other ancillary areas including cold stores and offices are separated from the main dining area by structural walls then the ground floor relativities are taken at 70%. Ground Floor stores and customer toilets are taken at 50%. Non ground floors are taken at a relative percentage of this (for restaurants outside Central London, see Table 1 referred to in paragraph 7.2 of the Rating Manual).

4.5.5 Where a property has been adapted or converted from another use such as a shop, any disabilities will no longer be relevant and should be removed. This will include allowances for quantum, layout, split or double units, width-to-depth, non-standard frontage, pillars, shape or masking etc.

4.6 Zoning method of valuation

4.6.1 It may be more appropriate to adopt the zoning method in predominately core retail locations such as in the peak Zone A area of the high street and prime areas within shopping centres as that will be the market within which the restaurant is competing.

4.6.2 However, where evidence of restaurant rents are at a higher value relative to the prime retail values nearby, an overall approach is to be preferred.

4.6.3 Restaurant premises within shopping or town centres where the primary footfall is mainly daytime may show evidence of rents at a lower relative value by comparison to the prime retail values nearby and their rateable values will need adjusting accordingly.

4.6.4 Primary valuations are to be derived from local and national rental evidence. For comparison purposes, rents should be analysed in terms of the appropriate floor area relativities and valued in the same way — as you devalue so must you value.

4.6.5 Particularly high or low specification of accommodation is not considered valuation sensitive for restaurants.

4.7 Outside seating

4.7.1 All outside seating should be recorded on the survey.

4.7.2 Outside seating areas have become more important since both the smoking ban and the pandemic and can be valued where the area is defined. These areas should be captured as use code OUT, as a line entry, which will give a relativity of one eighth.

4.7.3 Sometimes outside seating areas are semi-enclosed with heating provided and some may have a retractable roof or have terraces with attractive views. For those outside seating areas which are enclosed with a substantial roof covering, i.e., not fabric or similar covering, will need to be captured as a two-line entry. The first line entry as OUT, for the area of outside seating and a second line entry of CNP with the same area. Any feature, positive or negative which has a bearing on value should be noted and will need to be reflected in the rate adopted.

4.7.4 Consideration should be given as to whether the forecourt is reflected in the rent or whether it is a highway for which the occupier might pay an additional rent to the Local Authority. Seating available on pavements is not generally part of the hereditament. Restaurants with outside seating will most likely be valued on an overall basis.

4.7.5 In some locations and largely since the pandemic it has been noted that properties with large forecourt areas used for outside seating and that were previously covered by simple canopies have now been substantially improved and more permanent structures created. These areas now provide additional seating area for the restaurants which are enclosed and covered which can be used all year round. Depending on the valuation approach and quality of these areas they will need to be recorded in the survey either as OUT, part of the restaurant area if valued on an overall approach or included within the relevant zone, if the zoning method is to be adopted.

4.8 Kitchens

4.8.1 ‘Traditional’ kitchens located behind a structural wall are valued at a lower relativity.

4.8.2 ‘Show’ kitchens i.e. the kitchen is open plan on the ground floor and maybe considered as part of the dining experience, should be valued at factor 1 as the rental value is no different to the restaurant area. These areas should be captured as RES but overwritten as ‘open kitchen’ or ‘show cooking area’.

4.8.3 Additionally, where kitchens, food preparation and servery areas are separated from the main dining area by non-structural walls/stud partitioning these areas should also be valued at factor 1.

4.8.3 When analysing rents, ‘as you devalue so must you value’ - Marks and Spencer v Collier (VO) [1966] RA 107.

1. Market appraisal

1.1 In the lead up to April 2021 (AVD) it has been widely reported that the restaurant sector has been subject to a range of adverse market conditions including oversaturation, over-rented property, increasing costs and the Covid -19 pandemic.

1.2 This is reflected in the share price performance of listed restaurant chains and by a number of chains entering administration or entering Company Voluntary Arrangements (CVAs).

1.3 Although the industry is in the mature stage of its life cycle, restaurant culture remains an integral part of society and there are growth opportunities for industry operators that monitor and quickly respond to changing consumer tastes and preferences.

1.4 On the demand side the sector has been affected by a reduction in discretionary spending and a decline in High Street footfall.

1.5 The sector is subject to increased competition from hot food delivery services and special offers at major food retailers.

1.6 Many customers are increasingly health conscious and looking for new offerings and restaurants that attract such a clientele will need to keep abreast of this and the increasing demand for vegetarian, vegan, gluten free and sustainable food sourcing.

1.7 Chains that have been able to respond effectively to these challenges are succeeding and expanding. Niche operators are becoming more prominent in the sector, with Jamaican, Brazilian and Argentinian restaurants all reporting increased sales.

1.8 As shifting dynamics change the shape of British High Streets, many restaurants and cafes are capitalising on opportunities for acquisition with many traditional town centres now underpinned by these occupiers.

2. Changes from the last practice note

2.1 The scope of this Practice Note is to deal solely with Restaurants, Cafés and Snack Bars which now excludes Roadside restaurants (SCat 238) (See RM: Section 6: Part 3 – Section 880.

3. Ratepayer discussions

3.1 Central discussions are ongoing with representative agents for the class.

4. Valuation scheme

4.1 The valuation scale generally adopted for restaurants valued on an overall method is V1SPROVA31 with the relativities in paragraph 7.2 of the Rating Manual (Table 1). For Central London the scale V1SLA3USE1 should generally be used.

4.2 Where properties have a restaurant area main space that is predominately non-ground floor it is necessary to be aware of the relativities in valuation scale V1SPROVA31. In these predominantly non-ground floor hereditaments it may be more appropriate to use the scale V1SNONZONED1 or V1SGPOVERAL1 (for restaurants on levels up to floor 5).

4.3 A TOWER scale path is available for premises on upper floors in high rise buildings (generally above floor 5). The Central London scale V1SLA3TOWER can also be used in the Provinces.

4.4 Method of Valuation

The Rating Manual gives further guidance on valuation approaches.

4.4.1 In a town or shopping centre it is important to carefully consider the method of valuation to adopt, whether it be an overall method or on a zoned basis and change if necessary.

4.4.2 The tenant mix of the locality and footfall needs to be considered together with the rental evidence available.

4.4.3 Restaurants valued as overall should have a separate sub-location code and not be included within zoned sub-locations, to facilitate proper comparison.

4.5 Overall method of valuation

4.5.1 Generally rents paid for restaurants away from core retail locations support the overall method of valuation. The relativities used for rental analysis must relate to the valuation approach adopted.

4.5.2 It is important to have regard to the tenant mix in fringe areas away from a prime central retail pitch and consider the relative footfall, whether that is daytime or evening footfall. An overall approach is appropriate where there is a predominance of non-core uses and/ or mainly evening or leisure trade.

4.5.3 Where large kitchens have been created, other significant alterations have been made or where there is a large rear dining area the overall valuation approach is more appropriate than a zoned method.

4.5.4 The main dining area is valued at 100%. Generally, the ground floor relativities for the kitchen, food preparation and servery areas and most other ancillary areas including cold stores and offices are taken at 70%. Ground Floor stores and customer toilets are taken at 50%. Non ground floors are taken at a relative percentage of this (for restaurants outside Central London, see Table 1 referred to in paragraph 7.2 of the Rating Manual).

4.5.5 Where a property has been adapted or converted from another use such as a shop, any disabilities will no longer be relevant and should be removed. This will include allowances for quantum, layout, split/ double units, width-to-depth, non-standard frontage, pillars, shape or masking etc.

4.6 Zoning method of valuation

4.6.1 It may be more appropriate to adopt the zoning method in predominately core retail locations such as in the peak Zone A area of the high street and prime areas within shopping centres as that will be the market within which the restaurant is competing.

4.6.2 However, where evidence of restaurant rents are at a higher relative value to the prime retail values nearby, an overall approach is to be preferred.

4.6.3 Restaurant premises within shopping or town centres where the primary footfall is mainly daytime may show evidence of rents at a lower relative value by comparison to the prime retail values nearby and their rateable values will need adjusting accordingly.

4.6.4 Primary valuations are to be derived from local and national rental evidence. For comparison purposes, rents should be analysed in terms of the appropriate floor area relativities and valued in the same way – that is to say as you devalue so must you value.

4.6.5 Particularly high or low specification of accommodation is not considered valuation sensitive for E/A3 restaurants.

4.7 Outside Seating

4.7.1 All outside seating should be recorded on the survey.

4.7.2 Outside seating areas have become more important since the smoking ban and can be valued where the area is defined. These areas should be captured as use code OUT which will give a relativity of one eighth.

4.7.3 Sometimes outside seating areas are semi-enclosed with heating provided and some may have a retractable roof or have terraces with attractive views. Any feature, positive or negative which has a bearing on value should be noted and will need to be reflected in the rate adopted.

4.7.4 Consideration should be given as to whether the forecourt is reflected in the rent or whether it is a highway for which the occupier might pay an additional rent to the Local Authority. Seating available on pavements is not generally part of the hereditament. Restaurants with outside seating will most likely be valued on an overall basis.

4.8 Kitchens

4.8.1 ‘Traditional’ kitchens located behind a structural wall are valued at a lower relativity.

4.8.2 ‘Show’ kitchens i.e. the kitchen is open plan on the ground floor and maybe considered as part of the dining experience, should be valued at factor 1 as the rental value is no different to the restaurant area. These areas should be captured as RES, but overwritten as ‘open kitchen’ or ‘show cooking area’.

4.8.3 When analysing rents, ‘as you devalue so must you value’ - Marks and Spencer v Collier (VO) [1966] RA 107

1. Market appraisal

1.1 The total eating out market was approximately £83bn in 2014 (an increase on the year before of about 3%). Of this, the UK restaurant market was around £48bn. This too is rising and expected to reach £52bn by 2017.

1.2 However, different sectors of the market may not enjoy equal growth, and independent restaurants are likely to struggle as consumers switch to branded casual dining where good quality food is delivered to the table quickly.

1.3 Casual restaurants (for example Nandos; Wagamama; Yo Sushi; Zizzi; Giraffe etc) have increased their market share at the expense of full service restaurants. The reason for this is a focus on families, price; convenience and a quick service coupled with the atmosphere of a restaurant. Casual dining attracts the younger consumer as well. Branded restaurants are predicted to outperform independent establishments.

1.4 In response to the current national trend for people to eat out more frequently, and the strong predicted growth for 2015, many operators are planning to expand in the near future. They are targeting shopping centres; retail parks; transport hubs; town centres and high streets although the cost and availability of suitable property is a big challenge for them.

1.5 Other sectors that are forecast to do well in the short to medium term are fast food; gourmet burgers; Mexican and street food.

1.6 Street food is more expensive than a sandwich but less expensive than eating in which gives the impression of good value. Ethnic dishes are most popular with variety of choice, freshness and authentic tastes and flavours. Consumers can also enjoy the social aspect and a sense of community. There is room for growth in the informal (or casual) food market.

1.7 At the other end of the spectrum, the fine dining market where consumers are getting excellent quality food has held its own as ‘customers are prepared to pay for an experience which is real, immersive, artisanal and engaging’. Source (paras 1.1 to 1.7): BigHospitality

1.8 In support of the above, research from the NPD Group suggests that between 2008 and 2014 the numbers of customers eating out at independent restaurants fell from 53% to 43%, whilst visits to chain restaurants rose by 15.5%. Indications are that over this period (incorporating recession) those who chose a venue due to price rose from 9% to 25%. Consumers are more price conscious in periods of economic uncertainty. The larger, casual, high street dining chains appear better able to meet expectations on price and quality. The competition in the high street retail scene is mirrored in the food industry which is better able to keep pace with modern trends and this has fuelled demand for retail units vacated by other retailers between the 2010 and 2017 Revaluations.

1.9 At the very top end however, the number of Michelin Starred restaurants increased over the same period, suggesting that restaurant food as a social occasion is still a strong draw.

1.10 Interviews with industry executives revealed to market research firm Allegra Foodservice, that 2015 will be the year that many believe economic recovery from recession will be consolidated. Furthermore, studies show that growth in the eating out sector is at its strongest since the recession began in 2009.

1.11 As at April 2015, CBRE reports that the number of restaurants and food outlets has risen by 258% since 1998, with a total of 17,450 chain branches across the country. This represents 17 years of unbroken growth of chain operators. Since the 2010 Revaluation traditional offerings such as steaks and Italian food for example, have given way to a wide range of more ‘global’ offerings as customer taste has become more adventurous and exotic.

1.12 For example Mexican chain brands have grown by 57% since 2009. Mixed world cuisine outlets have grown by 40% over the last 5 years and openings by natural health food operators have grown by 15%.

1.13 In conclusion it seems that the market at April 2015 is dominated by those seeking out quality with a sense of occasion or ‘event’, where prices per meal are high, and those in greater number attracted by chains where the offer is less formal, more predictable and good value.

1.14 This should manifest itself in higher property values in the high street, where chain competition is prevalent and related to footfall/ leisure – and standalone premises that suit the high end offer, including public houses of character. The independent operators in the middle of these two ranges are likely to be the restaurants that suffer, as they seek to retain a market share in secondary locations surrounded by new and vibrant outlets seeking to cash in on the next food trend.

2. Ratepayer discussions

2.1 Central discussions are scheduled with representative agents for this restaurant class.

3. Changes from the last practice note

3.1 The scope of this Practice Note is to deal solely with Restaurants, Cafés and Snack Bars which now excludes Roadside Restaurants SCAT 238 (See Rating Manual: section 6 part 3 - section 880). In addition, it is important to make it clear that this Practice Note does not cover Drive-to and Drive-Thru Restaurants (Rating Manual: section 6 part 3 - section 365).

3.2 Since the 2010 Practice Note there has been a growth in the number of High Floor Level Restaurants in iconic buildings particularly in London. The TOWER scale should be used.

3.3 The state of the market has progressed with growth in this sector and the presence of more national chain operators and franchises in addition to established local operators.

4. Valuation scheme

4.1 The valuation scale generally adopted for restaurants valued on an overall method is VVSPROVA31 with relativities tabled in paragraph 7.2 of the Rating Manual. For Central London the scale VVSLA3USE1 should be generally be used.

4.2 Where properties have a restaurant area main space that is predominately non-ground floor it is necessary to be aware of the relativities the VVSPROVA31 scale adopts. In these predominantly non-ground properties it may be more appropriate to use the scale VVSNONZONED1 or VVSGPOVERAL1 (for restaurants on levels up to floor 5).

4.3 A TOWER scale path is available for premises on upper floors in high rise buildings (generally above floor 5). The Central London scale VVSLA3TOWER can also be used in the Provinces.

4.4 Method of valuation

The Rating Manual gives further guidance on valuation approaches.

4.4.1 In a town or shopping centre it is important to carefully consider the method of valuation to adopt, whether it be an overall method or on a zoned basis and change if necessary.

4.4.2 The tenant mix of the locality and footfall needs to be considered together with the rental evidence available.

4.4.3 Restaurants valued as overall should have a separate sub-location code and not be included within zoned sub-locs in order to facilitate proper comparison.

4.5 Overall method of valuation

4.5.1 Generally rents paid for restaurants away from core retail A1 locations support the overall method of valuation. The relativities used for rental analysis must relate to the valuation approach adopted.

4.5.2 It is important to have regard to the tenant mix in fringe areas away from a prime central retail pitch and consider the relative footfall, whether it be daytime footfall or evening. An overall approach is appropriate where there is a predominance of non core A1 uses and/ or mainly evening or leisure trade.

4.5.3 Where large kitchens have been created or other significant alterations have been made or where there is a large rear dining area the overall valuation approach is more appropriate than a zoned method.

4.5.4 The main dining area is valued at 100%. Generally, the ground floor relativities for the kitchen, food preparation and servery areas and most other ancillary areas including cold stores and offices are taken at 70%. Ground Floor stores and customer toilets are taken at 50%. Non ground floors are taken at a relative percentage of this (for restaurants outside Central London, see Table 1 referred to at paragraph 7.2 of the Rating Manual).

4.5.5 Where a property has been adapted or converted from another use such as a shop, any disabilities will no longer be relevant and should be removed. This will include allowances for quantum, layout, split/ double units, width-to-depth, non standard frontage, pillars, shape or masking etc.

4.6 Zoning method of valuation

4.6.1 Where rental evidence can be found that supports a zoned approach it may be more appropriate to adopt this method in predominately core retail (A1) locations, such as in the peak zone A area of the high street and prime areas within shopping centres as that will be the market within which the restaurant is competing.

4.6.2 However, where restaurant rents are found to be excessive in relation to the nearby retail occupiers, an overall approach can be adopted.

4.6.3 Restaurant premises within shopping or town centres where the primary footfall is mainly daytime may show rents payable at a lower relative value to the prime retail values nearby and their values will need adjusting accordingly.

4.6.4 Primary valuations are to be derived from local and national rental evidence. For comparison purposes, rents should be analysed in terms of the appropriate floor area relativities and valued in the same way, that is to say as you devalue so must you value.

4.6.5 Particularly high or low specification of accommodation is not considered valuation sensitive for A3 restaurants.