Telecommunications masts and wireless transmission sites

This publication is intended for Valuation Officers. It may contain links to internal resources that are not available through this version.

This class encompasses all strands of the telecommunications and broadcast industry. The main areas are:

- mobile network operators

- emergency services

- traffic monitoring sites

- wireless broadband operators

- small Wi-Fi and bluetooth sites in buildings

- smart meter sites

Each site can be considered as a communication station and may, additionally, include premises.

All the above types of sites should be categorised as one of the following:

| Type | Description code |

Description |

Scat |

Suffix |

Mobile phone, emergency services and smart meter sites |

MT1 |

Communication station and premises |

066 |

G |

Traffic monitoring sites |

MT1 |

Traffic monitoring station and premises |

066 |

G |

Wireless broadband (public access) |

MT1 |

Public access wireless broadband site |

066 |

G |

Wireless broadband (subscription access) |

MT1 |

Wireless broadband site |

066 |

G |

Short range WiFi/Bluetooth equipment in buildings |

MTX |

Wifi/Bluetooth site |

066 |

G |

Overall responsibility for the valuation approach lies with the Utilities, Transport and Telecoms Team (UTT) of the National Valuation Unit. The Regional Valuation Units (RVUs) are responsible for individual list entries (compilation, maintenance and Check Challenge appeal settlement) for all of the above types.

The mast class co-ordination team (CCT) and the UTT are responsible for ensuring effective co-ordination takes place. The mast CCT is the first point of contact for guidance on maintenance or settlement work. The CTT and UTT will deliver practice notes describing the valuation basis for revaluation and provide advice as necessary during the life of the rating lists. Caseworkers have a responsibility to:

- follow the advice given at all times

- not to depart from the guidance given on settlement or maintenance work, without approval from the co-ordination team

- seek advice from the co-ordination team before starting any new work

5.1 Identification of the hereditament

A hereditament exists when the four essential elements of rateable occupation are present. The occupation must be actual, exclusive, beneficial and not be transient. A detailed discussion of the principles can be found in the Rating Manual: section 3 part 1 - part C hereditament (Para 3).

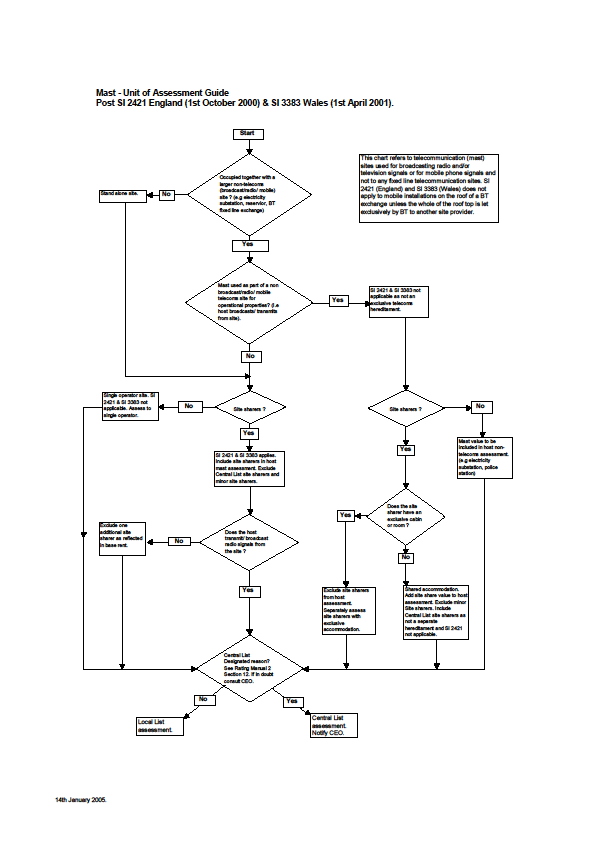

Additionally, the provisions of the non-domestic rating (telecommunications apparatus) (England) Regulations 2000 (SI 2000 No. 2421) must be applied when considering the establishment of a mast hereditament. See section 5.2 below.

5.2 Telecommunication sites which are artificial hereditaments

Telecommunication sites are a class of hereditament which may fall outside the normal rules of unit of assessment. These types of hereditaments are known as prescribed hereditaments. See Rating Manual: section 3 part 1.

The non-domestic rating (Telecommunications Apparatus) (England) Regulations 2000 (SI 2000 No. 2421) came into effect on 1 October 2000. It applies to telecommunications hereditaments occupied exclusively by telecommunications apparatus. The regulation enables the aggregation of all site sharers into a single hereditament on sites which are occupied exclusively by telecommunications apparatus. The principal operator or “host” of the site is held to be the rateable occupier in these circumstances. The host regulations apply only to sites which are occupied by two or more operators which do not form part of the same joint venture company.

The regulations make different provisions when telecommunication apparatus of a designated Central List is on site. See section 5.5 below.

The non-domestic rating (Telecommunications Apparatus) (Wales) Regulations 2000 (SI 2000 No. 3383) came into effect on 1 April 2001 in respect of local rating list in Wales. It is worded differently to the English regulations, but mirrors the effect.

5.3 Exclusive test

The regulations outlined above do not make a landowner or landlord responsible for the rate liability, provided they are not in the telecommunications business and they occupy the land, buildings or structures for a purpose other than telecommunications.

For example, where a hospital lets space to a telecommunications operator, the hospital remains as the principal hereditament, but a separate telecommunications hereditament is created. The telecommunications use creates a separate hereditament as it is a different use to the principal hereditament which is neither occupied exclusively by telecommunications equipment nor primarily used for sending or receiving wireless signals

The regulations achieve this by:

applying specifically to a telecommunication hereditament. The definition of this is a site forming a hereditament occupied exclusively by telecommunications apparatus of either a single operator or more than one operator; and

not enabling aggregation where the telecommunications hereditament is on or forms part of a structure occupied by the host for any purpose other than the provision of or operation of a site for telecommunications apparatus. An exclusive telecommunications hereditament means a broadcast or mobile telecommunications hereditament. It does not apply to fixed line or fibre exchanges.

The exclusivity test disregards the presence of ancillary accommodation used in the normal operation of a telecoms site, which may correctly form part of the principal telecoms hereditament.

The provisions of SI 2000 No. 2421 do not apply in the following circumstances:

- where the principal hereditament becomes redundant for the purpose it was originally designed.

- on a rooftop where each operator has a separate agreement with the building owner and there is no principal telecommunications hereditament.

However, if the building owner lets the entire rooftop to a telecommunications site provider which then sublets the rooftop to individual operators as site sharers, the site provider becomes a host of a principal telecommunications hereditament. All the site sharers must be aggregated into the site provider’s host telecommunications hereditament.

5.3 Single operator sites

A single operator site is a site from which only one operator broadcasts or transmits telecommunication signal. A single operator may still exist when a joint venture company, formed by two separate network operators, broadcasts signals for each of the operators within it. A single operator site exists even when the site is provided by a third party which is not broadcasting from the site.

5.4 Shared sites

Where more than one operator, not forming part of a joint venture company, or where a third party infrastructure provider broadcasts or transmits themselves then the telecommunications site will be considered as a shared or “hosted site”. The SI 2000 No. 2421, or No. 3383 in Wales, impacts upon the consideration of who is the host and, consequently, the rateable occupier.

When a site is a shared site, consideration must be given to:

- what the principal telecommunication is

- who is the host

- who is in rateable occupation of the whole telecommunications site including the site sharers

The definition of host in the appropriate SI means that the telecommunication site provider or operator who receives the site share payments, or would be entitled to receive the payments, will be the ratepayer for the whole telecommunication hereditament.

Site Sharing is achieved by:

Traditional methods where each of the operators attach their own equipment e.g. cabling etc to the structure and install their own cabin/cabinet.

Random Access Network or RAN sharing is achieved by the installation of additional electronic (non rateable) equipment.

Mobile Operator Random Access Network (MORAN) sharing the installation of additional electronic non rateable equipment which enables the transmission signals of two different mobile network operators from the same set of equipment.

When a site is shared by two operators in the same joint venture company using MORAN technology, no addition is made for this sharing arrangement.

5.5 Central List occupiers and telecommunication sites

Where a telecommunications site contains telecommunication apparatus of a designated Central rating list occupier and that Central Rating List occupier is not the host, their apparatus is deemed to be “excepted apparatus”. It is excluded from the aggregation. No account should be taken of Central List site sharers when considering the valuation of the host site.

This applies whether or not

the Central List telecoms apparatus at the host site is capable of forming a separate hereditament. a designated person shares a site with another designated person who is the host of the principal telecommunications hereditament.

Whilst a Central List occupier’s equipment may be treated as excepted apparatus, its presence will qualify the site as a shared site under SI 2421. This impacts the identification of unit of assessment and appropriate number of operators/sharers The host should be assessed as they are in rateable occupation.

Where a Central List occupier is the host, there are two possible situations.

The mast is a remote stand-alone site. The sharers are merged into the host assessment and included in the central list assessment.

The mast is part of a larger non-telecoms hereditament for example an electricity pylon, water tower or a gas hereditament. The principal hereditament is not used exclusively for telecommunications, so the host provisions of SI 2421 do not apply. A separate assessment is required for each site sharer which has an exclusive room, cabin or compound. Where the site uses non-exclusive accommodation with the Central List host, they will be included in the Central List assessment of the host. There is no separately identifiable hereditament as paramount control of the shared accommodation lies with the “designated occupier”.

Details of Central List Occupiers are set out in the Rating Manual: section 2 part 2.

The Central List host site forms part of the occupier’s central rating list assessment, provided that the site is not an excepted hereditament” as defined in Part III of the Central Rating List (England) Regulations SI 2000 No 535.

Central List assessments are dealt with by the UTT. Queries on the local list/Central List boundary should initially be referred to the team.

5.6 The Electronic Communications code

The electronic communications code (‘the code’) enables electronic communications network providers to construct electronic communications networks. The code enables these providers to construct infrastructure on public land (streets) and to take rights over private land, either with the agreement with the landowner or applying to the County Court or the Sheriff in Scotland. It also conveys certain immunities from the Town and Country Planning legislation in the form of Permitted Development. In addition to providers of electronic communications networks the code is also available to those who wish to construct conduits to be made available to network providers.

There has been an electronic communications code in place since 1984. The current electronic communications code, part of the Digital Economy Act 2017, took effect on 28 December 2017. The new code is designed to further facilitate the installation and maintenance of electronic communications networks of operators with code powers. It changes the assumptions for valuation of land used for the provision of telecommunications infrastructure. Consequently, rents determined under the new code will be significantly different from rents which have been agreed or determined under the previous code.

The valuation assumptions required under the new code do not accord fully with the rating hypothesis. Advice should be sought from the UTT if caseworkers receive arguments that such rents should be used as the basis of a rating valuation.

The type of survey requirements differ depending on the type of site being considered. Surveys for all sites should record information of all site occupiers as this impacts upon the identification of the rateable occupier as well as the valuation.

6.1 Telecommunication mast sites

The majority of communication masts sites are valued using a hybrid approach; rentals approach for site value and contractors’ method of valuation for the rateable plant and machinery.

The survey should identify and record the plant and machinery to enable the cost element of the valuation to be undertaken.

The following details should be recorded when assessing a site.

- relevant site reference, including operator/host

- general description of mast

- mast height

- site dimension where appropriate

- names of all operators present on site

- details of construction, including size and composition of associated cabins/cabinets

All other associated rateable plant and machinery, which may include:

- roadways and car parking

- other surfaced areas

- site fencing, type and height

- gates

- cabling and supporting cable tray

Full guidance on what is included in the costings adopted can be found in the Valuation Office cost guide.

6.2 5G sites

The major network operators began the roll out of 5G infrastructure and equipment from June 2019 onwards. Initially, sites were limited to a few large cities and to small areas within those cities. At time of writing, 5G infrastructure is more widely established covering more towns and cities and larger areas within them. Mobile network operators appear to have focused on upgrading of existing sites, rooftops, greenfield and highways sites. Typically, this will result in taller masts with additional cabins on greenfield site. Rooftops site upgrades may involve replacing stub towers and/or re-siting equipment closer to the edge of the rooftops. They will also include the provision of more cabins on the rooftop. All relevant survey information should be recorded as above.

The deployment of small cells to enable greater network coverage is anticipated but, at time of writing, there is no evidence of such deployment at scale. As 5G networks develop they may utilise large numbers of small cells which may or may not have fibre connectivity. Survey requirements for such sites will be different as there will be implications for the correct unit of assessment. Survey requirements for such sites will be updated as and when such sites come into existence.

6.3 Wireless broadband hereditaments

Wireless Broadband sites are usually installed on or in a building, street furniture or mast and use equipment similar to that of a wireless broadband router in the home.

To establish whether a separate rateable wireless broadband hereditament exists, the host of the assessment must be identified. The following survey data should be recorded:

- is the host property occupied or unoccupied?

- is the wireless broadband site subject to a separate lease or agreement?

- is the WiFi site solely used by the occupier of the host premises in connection with the use of the host premises (see Rating Manual: section 3 part 1 - part C hereditament (Para 3)) and should it be assessed with the host premises?

Is the Wireless Broadband equipment sited on a host mast or communication station covered by Statutory Instrument 2421 and therefore should be assessed as a site sharer on the host mast? Wireless Broadband sites require separate assessment when occupied under a separate lease or agreement to the host property for a period of 12 months or more, other than when it is a site share on a mast (SI2421 in England and SI3343 in Wales), and when the Wireless Broadband service is considered to be part of the Host property occupation, such as a WiFi site in a coffee shop used by the customers of the coffee shop. The installation adds to the customer enjoyment of the “host” property and the value will often be deminimis relative to the value of the whole hereditament.

6.4 WiFi/Bluetooth sites

These sites are mainly found in unoccupied premises. Consideration must be given to whether a site inspection is necessary.

Where it is considered necessary to confirm the details of a Wifi/Bluetooth hereditament through internal inspection of the site, it is recommended that the equipment in use be photographed and recorded on a plan. A checklist is provided at Appendix 3 and must be used to record the details of the site, equipment, the position of equipment and any accompanying display notices.

A copy of the Wifi/Bluetooth operators lease or agreement to occupy is helpful in establishing the facts of occupation.

Survey details should be captured on the appropriate software application - the Communication Masts Application for telecommunication masts and WiFi sites. The Non-Bulk Server (NBS) for larger sites valued using a full contractor’s basis.

Plans, surveys and other information should be stored in appropriate folder within the Electronic Document Records Management (EDRM) system.

The valuation approach for the majority of communication sites is a hybrid approach: the rentals based valuation for the building or land, with additions for rateable plant and machinery based on decapitalised cost at the statutory decapitalisation rate.

The rental evidence has been considered nationally and a scheme of site values has been derived. The site value vary according to site type and geographic location. A summary of the scheme is provided in the Practice Note for Telecommunications Masts.

The valuation of the mast must be carried out within the communication masts application.

Support and guidance can be obtained from the mast class co-ordination team and from the UTT.

Valuations are supported by the Survaid, Communication Masts Application and with reference to the Cost Guide.

Bluetooth

Bluetooth is wireless technology found in most modern mobile phones and computers used to link devices to one another and the internet over short distances (up to 10 metres). Bluetooth networks use unlicensed short-range radio spectrum which only requires a low power supply. They are much slower than WiFi, with limited range and support fewer devices. Bluetooth generally sends data at less than 1 Mbps.

See Rating Manual Section 6: Part 3: 2017 Practice Note Section 860 - 3 WiFi and Bluetooth sites in buildings. The IEEE Standards (see below) for Bluetooth is 802.15.1

Broadband

The term ’broadband’ is widely used to describe a service that provides high speed internet access. Large amounts of data can be sent or received.

Broadband connections - Fixed

Data is sent via fibre and cables. (see cable and fibre below)

Broadband connections – Wireless

Data is sent by wireless radio spectrum from the wireless broadband base station to the device such as a mobile phone, tablet or lap top. The base station will connect to a fixed line network for Internet access through either; wireless relay, fixed fibre connection or through a copper connection such as an unbundled BT local loop.

Broadband speeds

Broadband is delivered in a number of ways and the type of technology used, distances and the number of users online determines the how fast information is sent and received. Information is measured in multiples of megabits.

Broadband speed is measured in megabits per second, stated as Mb or Mbps.

Convergence technology

The telecommunications industry is endeavouring to develop or combine technologies to enable improved communication services. The distinction between fixed and wireless broadband and mobile phone technologies will become increasingly blurred.

Cable and Fibre

Most of the residential and business population in England and Wales are able to access the internet through either:

-

BT (UK) and KCOM (Hull) networks (valued on a full Receipts and Expenditure basis)

-

Cable Networks (Virgin Media and Wightfibre). See: Rating Manual Section 6: Part 3 Section 870.

-

Fibre Optic Networks see Rating Manual Section 6: Part 3 Section 871.

-

Fibre Optic Next Generation Access, see Rating Manual Section 6: Part 3 Section 873.

IEEE Standards for Information Technology

IT standards are set by the Institute of Electrical and Electronics Engineers through its Standards Association. The IEEE sets standards for a number of industries including telecommunications.

The designated standard indentifies the type of technology in use and is useful when trying to decide if the WiFi or WiMax equipment is being used for 3G or 4G.

Mobile technology

Mobile phone technology is used to access the internet through what is known as 4G (4th Generation) and at lower speeds through 3G (3rd Generation) technology. Signals are carried in the licensed spectrum which is managed and regulated by OFCOM. 4G and 3G sites can appear to be very similar to wireless broadband sites, but the suitability of sites to realise the potential of higher level technologies also serves to increase site value.

Any sites using mobile phone technologies to deliver internet access are dealt with in Rating Manual Section 6 part 3 - Section 860 - Radio and TV Transmitting/Receiving Stations and Masts (including Microwave Masts).

Radio Spectrum

This part of electromagnetic spectrum, defined by frequency, is used to send voice, video and data. Frequency is the number of complete cycles of electromagnetic wave in a second and is measured in units of Hertz (Hz).Different types of wireless technology operate at different frequencies through the radio spectrum.

The frequency used often provides an indication of the technology being used.

Next Generation Access

The Valuation Office uses the term Next Generation Access (NGA) to describe a new or upgraded access network that will allow substantial improvements in broadband speeds and quality of service compared to yesterday’s services. Given technological convergence the term is used to describe access networks based on a number of technologies including cable, fibre, fixed wireless and mobile.

Radio Spectrum - Licensed

Certain frequencies are chosen by Government to send signals for specific users, such as the emergency services. Any frequency which has been selected cannot be used without the operator being given a licence. The most commonly known licensed operators are the mobile phone companies especially those who use 3G and 4G technology.

Radio Spectrum - Unlicensed

Parts of the spectrum that are unlicensed can be freely used but they have a short range. Commercial users include, for example, taxi firms but wireless broadband operators now use the unlicensed spectrum. WiMax usage extends into the licensed spectrum depending of the type of coverage needed.

Sites for WiFi in domestic property

Wireless personal area networks in domestic hereditaments are assessed to Council Tax.

Sites for WiFi used in connection with Non-domestic occupations

For example a café which provides WiFi connection for its customers.

Tip in this example the WiFi will fall to be assessed as an ancillary to the host occupation.

Wide Area Networks

Wide area networks link local area networks. The characteristics of WiFi and WiMax are such that they can be used together to create any combination of networks. However as WiFi units are not connected by physical link (contiguous) the site of each WiFi installation will require separate assessment.

WiFi

Wi-Fi is a trademarked term of the IEE however it is generally used to describe; short range wireless technologies that allow an over-the-air connection between a wireless device and a base station, or between two wireless devices. Basic WiFi has a range of over 20 metres indoors, and 300 meters outside. WiFi is often used in homes or small specific areas (Hotspots) such as train stations or restaurants.

These can be identified by being within the IEEE’s 802.11 series.

WiMax

Worldwide Interoperability for Microwave Access. A wireless technology, similar to WiFi, but with a much longer range. WiMax is a high speed wireless alternative for internet access. And has a circa 10 kilometre range. When associated with a base station (mast) it can cover large areas and is the preferred technology when operators are setting up remote “Fixed” wide-area networks.

Some WiMax sites send information on the licensed spectrum and are used by Mobile Phone Operators for either 3G use or 4G. These sites must be valued in line with Rating Manual 5 Section 860 2017 Practice Note Radio and TV Transmitting/Receiving Stations and Masts (including Microwave Masts) These sites will have IEEE standards between of 802.16 e (3G) or IEEE standard of 802.16m (4G).

Wireless broadband

The data is sent through the air using radio waves. Providers use specific frequencies of the radio spectrum to send their signals.

Wireless technology

Wireless sites operate across the unlicensed and licensed spectrum using various wireless technologies including Bluetooth, WiFi, WiMAX, Mobile and broadcast radio/TV. Wireless broadband and mobile technology allows devices to inter-connect and communicate with each other and the internet via broadband. The speeds at which an end user can down load and upload information are measured in Megabits per second (Mbps).

{kind=link}

1. Market appraisal

1.1 At the Antecedent Valuation Date (AVD) of 1 April 2024 there remain four primary mobile network operators. There is also an increasing presence of neutral host site providers.

1.1.1 Post AVD, but prior to list compilation date, two of the four mobile network operators (MNOs) have merged.

1.2 The government has a target that gigabit broadband and ’standalone’ 5G will be available nationwide by 2030. The continual development in mobile telecoms technology results in ongoing infrastructure developments, whether upgrading existing equipment, or developing new mobile telecommunications sites.

1.3 The largest MNOs continue to operate joint venture companies to facilitate the sharing of telecommunications infrastructure. However, evidence also shows that MNOs are building unilateral sites for 5G masts in addition to sites they occupy through joint venture companies.

1.4 5G coverage by the four MNOs went live in major UK cities in 2019. Ofcom, the telecoms regulator, estimated that in September 2023, 85% to 93% of UK premises could get 5G coverage outdoors from at least one operator.

5G cells and networks are also being rolled out by neutral host providers.

1.5 At the AVD MNOs were operating site sharing through their existing joint venture company arrangements in some areas.

Some MNOs companies had begun to unwind active sharing agreements, particularly in urban areas.

1.6 In addition to the MNOs there are companies, known as neutral host site providers, which provide infrastructure for the MNOs. They provide traditional infrastructure and new types of infrastructure developed to meet the demands of 5G networks.

1.7 The use of small cell infrastructure continues to increase. Small cells may be stand alone sites or they may form park of a network. The deployment is designed to improve network capacity and coverage, particularly 5G coverage.

1.8 The Shared Rural Network (SRN) is a £1 billion programme, jointly funded by the government and mobile network operators, to tackle 4G mobile not-spots. Masts built or upgraded under the SRN must be available for all four MNOs to use.

2. Changes from the last practice note

2.1 The Electronic Communications Code

2.1.1 The provision and operation of sites for electronic telecommunication networks have been regulated by the Electronic Communications Code since 1984.

A new Electronic Communications Code (part of the Digital Economy Act 2017) took effect on 28 December 2017. The new Electronic Communications Code (ECC) is designed to further facilitate the installation and maintenance of electronic communications networks of operators with Code powers.

2.1.2 The new Code changes the assumptions for the valuation of land to be used for the provision of electronic telecommunications infrastructure. In circumstances where a Code agreement is imposed upon a landowner/occupier or where the court is required to specify terms where the parties are unable to agree, valuation of the compensation will be on a ‘no scheme’ basis based on compulsory purchase principles. The rights are valued on the basis of their value to the landowner rather than on the basis of the value to the operator for use as a telecoms site. Thus, any new agreements for mobile telecommunication sites made after 28 December 2017 under Code powers will be fundamentally different to those agreed before that date.

2.1.3 In December 2022 further changes to the ECC were introduced by the Product Security and Telecommunications Act 2022 including:

- new provisions to actively encourage alternative dispute resolution rather than legal proceedings

- a new procedure to allow operators to gain access to land in circumstances where an occupier is unresponsive

- allow expired agreements to be renewed on terms more closely aligned to the 2017 reforms, including on land valuation

- extend the reformed ECC’s automatic rights to upgrade and share apparatus to apply retrospectively to code agreements entered into before 2017

2.1.4 The Government’s policy position on the ‘no scheme’ valuation regime has not changed, stating there is no intention to revisit the valuation framework contained in the Electronic Communications Code.

2.2 Emergency Services Network (ESN)

2.2.1 Emergency services network provision is in the process of switching from the previous radio-based system to 4G technology. The project has been delayed and the completion date extended.

2.2.2 One of the main four MNOs was successful in the acquiring the contract. It will upgrade its existing network and develop new sites in some areas to accommodate ESN service provision.

2.2.3 Additionally, the government will develop sites in areas with no existing infrastructure and in areas which the MNO contract supplier will not develop sites. It is necessary to ensure the requisite ESN coverage.

2.3 Smart Meter Network

2.3.1 A new national communication infrastructure to support the roll-out of smart meters has been developed. The infrastructure may be on new or existing sites. It may be on highways, greenfield or rooftop locations.

2.3.2 When attached to communications masts already in assessment some of the actual equipment for this infrastructure is not rateable, but it can still impact upon the rateable occupier. The general principle is that if the operator of the new equipment is the rateable occupier of the ‘parent’ mast, the installation will have no effect on who is considered to be the rateable occupier. Alternatively, where the equipment is installed onto a mast from which the operator was not previously transmitting, a review of the assessment will be required to reflect the provisions of SI 2000 2421.

2.3.3 Advice should be sought from CCT lead where changes are being made to a site as a consequence of smart meter technology.

2.4 5G technology

2.4.1 Commercial 5G networks began operating in June 2019. All mobile network operators are continuing their programme of upgrading sites and expanding their 5G network provision.

2.4.2 Upgrading of an existing greenfield or highway site to enable 5G transmission typically involves the replacement of the existing mast with a taller mast and the provision of more cabins and cabinets.

2.4.3 Typically, 5G equipment is heavier and more numerous than the equipment required for 4G transmission. As a result, the upgrade of rooftop sites may require the installation of a taller and more substantial stub tower capable of supporting the 5G equipment. It may result in antenna and supports being upgraded and moved to the edge of the building. It often involves the provision of additional cabins and cabinets on the rooftop.

2.4.4 Small cells are utilised to facilitate 5G coverage. The small cells may be stand alone sites. They may form part of a network of connected cells.

2.4.5 Small cells may be deployed by MNOs. They may be deployed by neutral host providers.

2.4.6 Small cells locations are numerous and varied. Examples include on street furniture, in or on buildings or alongside large infrastructure projects. The list is not exhaustive.

2.4.7 It is anticipated that as the technology develops the areas and nature of the networks will be also change.

3. Ratepayer discussions

3.1 Discussions with agents have not been undertaken for the purposes of Revaluation 2026.

3.2 It is anticipated that discussions with ratepayers’ representatives will take place prior to draft list publication.

4. Valuation scheme

This practice note covers communications stations with a special category code of 066. It includes mobile telecommunication mast sites situated on highways, greenfield sites and rooftops.

4.1 Mobile telecommunication sites

The valuation approach is based on a site rent value with an addition for the rateable plant and machinery on the site.

4.2 Rental Evidence

4.2.1 Rental evidence is available for site rents for greenfield sites, rooftops, micro and pico cells. There is no rental evidence available for communication stations situated on public highways. The site rent values for these sites is derived from greenfield evidence.

4.2.3 Analysis of the available rental evidence has resulted in the designation of two valuation zones:

- Greater London billing authority areas

- Rest of England and Wales

4.2.4 The scheme is split within each of those zones to distinguish between rooftop and non-rooftop sites. The schemes for site values for each zone and each category are set out in this section.

The values below are not yet agreed for the 2026 list. The values will be included within the valuation application. They may be subject to change if agreement is reached through discussions with the operators and their agents prior to list publication.

4.3 Site values rest of England and Wales (excluding Greater London billing authority areas)

4.3.1 Greenfield sites

| Type/definition | Height | Base site value | Cap |

|---|---|---|---|

| Highway sites: non-demised sites up to 15m in height located on a highway where no rent is paid | up to 15m | £4,600 | Not applicable |

| All Monopoles and towers not located on a highway | Up to 25m | £5,750 | Not applicable |

| All Monopoles and towers | between 25.01 and 45m | £6,600 | Not applicable |

| Towers | Between 45.01 and 60m | £13,000 | Not applicable |

| Towers | Between 60.01m and 150m | £13,500 | Not applicable |

| Guyed masts | Between 30.01 and 150.9m | £7,500 | Not applicable |

| Towers and or guyed masts | Over 151 m | £27,000 | Not applicable |

| Single guyed radiators | All heights | £7,500 | Not applicable |

| Paired guyed radiators | All heights | £11,250 | Not applicable |

| Traffic monitoring sites | All Sites | £140 | Not applicable |

| Site share addition/(Greenfield payaway) | Not applicable | £2,500 | Not applicable |

| Pico or Micro Cells where wall mounted on or in buildings /kiosks | Not applicable | £4,000 | Not applicable |

| Pico or micro cells within airports, stadia, shopping centres and similar. | Not applicable | To valued individually | Not applicable |

| TV stations. A greenfield site used as a TV and radio broadcast ‘repeater’. Generally located in rural locations where there is generally little/no demand by the MNOs. These sites will be single operator and could be up to a height of 45 m | Not applicable | £2,750 | Not applicable |

4.3.2 Rooftop sites England and Wales (excluding Greater London billing authority areas)

Rooftop sites are divided into three broad categories.

Category 1: non-typical rooftop sites offering greater than normal coverage. These are often, but not exclusively, to be found in central or prime locations or in areas of high mobile traffic volumes. Regard is had to the individual rents and facts of each case.

Category 2: these sites make up the majority of rooftop assessments. They will be in a variety of locations; secondary commercial areas, suburban and industrial areas.

Category 3: sites not within those above. These sites may be in very rural locations or may be on rooftops which offer only limited coverage due the height and being overshadowed by surrounding buildings.

4.3.3 Site values (Rooftop sites in England and Wales (excluding Greater London Billing Authority areas)

| Category 1 | Category 2 | Category 3 | |

|---|---|---|---|

| Outside Greater London BAs (rest of England and Wales) | To be valued individually. Non-typical and where the passing rent, adjusted to AVD, falls outside category 2 or 3. Non-typical sites may be regarded as rooftops offering greater than normal coverage, those in central or prime locations or in areas of high mobile traffic volumes. | £12,500 | £6,000 Poorer locations, for example rural areas with limited population density. Regard may be had to individual rents. Any rent must be suitably adjusted to reflect lease terms and dates so that the rent is suitably adjusted for rating purposes. |

4.4 Site values Greater London Billing Authority areas

4.4.1 Greenfield sites

| Type/definition | Height | Base site value | Cap |

|---|---|---|---|

| Highway sites: non-demised sites up to 15m in height located on a highway where no rent is paid | up to 15m | £6,200 | Not applicable |

| All Monopoles and towers not located on a highway | Up to 25m | £7,750 | Not applicable |

| All Monopoles and towers | between 25.01 and 45m | £13,500 | Not applicable |

| Towers | Between 45.01 and 60m | £18,500 | Not applicable |

| Towers | Between 60.01m and 150m | £22,000 | Not applicable |

| Guyed masts | Between 30.01 and 150.9m | £17,000 | Not applicable |

| Towers and or guyed masts | Over 151 m | All valued individually | Not applicable |

| Single guyed radiators | All heights | £17,000 | Not applicable |

| Paired guyed radiators | All heights | £25,000 | Not applicable |

| Traffic monitoring sites | All Sites | £140 | Not applicable |

| Site share addition/(Greenfield payaway) | Not applicable | £2,500 | Not applicable |

4.4.2 Available rental evidence for pico and micro cells within the M25 shows differing values for high volume traffic areas such as railway stations or shopping centres and similar, as well as in postcode areas within Westminster, City of London and some other business districts. The 3 categories are set out below.

Pico and micro cells

| Category | Location | Site value |

|---|---|---|

| Category 1 | High demand sites – on the facts of each case | To be valued individually |

| Category 2 | City of London (5030), Westminster (5990) and additional districts if identified as Category 1 | To be valued individually |

| Category 3 | Sites outside of Category 1 and Category 2 areas | £4,000 |

4.4.3 The above table is not intended to cover small cells, such as those situated on street furniture, and DAS systems. These types of small cells are to be valued on the facts in each case and are not valued by the scale above.

4.4.4 Additionally, it will be necessary to determine the correct unit of assessment for these types of small cells prior to the valuation stage.

4.5 Rooftop sites (Greater London billing authority areas)

4.5.1 Rooftop sites are divided into two broad categories.

Category 1: typical rooftop sites located on buildings with good coverage. These are usually to be found in central or busier locations or in areas of high mobile traffic volumes. Regard is had to the individual rents on such sites.

Category 2: these sites make rooftop assessments that do not have the characteristics of Category 1 rooftop sites. They will be in a variety of locations including, but not limited to, secondary commercial areas, suburban and industrial areas.

Rooftop Site Values

| Category 1 | Category 2 | |

|---|---|---|

| City of London (5030), Westminster (5990) | Valued individually where the rent passing, adjusted to AVD, is greater than the Category 2 site value. | £28,000 |

| Camden (5210), Hammersmith & Fulham (5390), Kensington & Chelsea (5600), | Valued individually where the rent passing, adjusted to AVD, is greater than the Category 2 site value. | £20,000 |

| Hackney (5360), Islington (5570), Tower Hamlets (5900), | Valued individually where the rent passing, adjusted to AVD, is greater than the Category 2 site value. | £18,500 |

| Haringey (5420), Lambeth (5660), Lewisham (5690), Newham (5750), Southwark (5840), Wandsworth (5960), Barking & Dagenham (5060), Barnet (5090), Bexley (5120), Brent (5150), Bromley (5180), Croydon (5240), Ealing (5270), Enfield (5300), Greenwich (5330), Harrow (5450), Havering (5480), Hillingdon (5510), Hounslow (5540), Kingston upon Thames (5630), Lewisham (5690), Merton (5720), Redbridge (5780), Richmond upon Thames (5810), Sutton (5870), Waltham Forest (5930) | Valued individually where the rent passing, adjusted to AVD, is greater than the Category 2 site value. | £17,000 |

4.6 Site Sharing and Payaway

Mobile network operators continue to share sites through joint venture companies and the use of Mobile Operator Random Access Network (MORAN) sharing. This practice is not universal. MNOs have begun to unwind this type of sharing arrangement in certain areas. MNOs may deploy separate operational equipment on existing sites or locate on new unilateral sites are site provided by third party hosts.

The new Electronic Communications Code prevents this type of payment being taken into consideration when agreeing Code site rents. Rent reviews in older agreements will be on terms which do not reflect the new Code provisions. Such rents may still include provision for site sharing and payaway.

1. Market Appraisal

Consolidation and mergers of mobile network operating companies were not a feature of the telecommunications market at the Antecedent Valuation Date (AVD) of 1 April 2021.

Mobile network operators began to install new infrastructure and equipment to enable the rollout of their 5G networks from June 2019 onwards, limited initially to a small number of cities. By the AVD mobile operators had developed 5G capability in many towns and cities.

The largest mobile network operators (MNOs) continue to operate joint venture companies to facilitate the sharing of telecommunications infrastructure. However, evidence is emerging that MNOs are building unilateral sites for 5G masts in addition to sites they occupy through joint venture companies.

The impact of site sharing through joint venture companies together with the introduction of a new Electronic Communications Code has resulted in a decline in the number of payaway fees. Whilst such fees are less common in the market, they have not disappeared completely. Where a site is shared by operators not subject to the same joint venture agreement then a payaway fee may be payable.

In addition to the MNOs there are companies, known as third party providers, which provide infrastructure for the MNOs and the provision of sites for the broadcast of TV and radio signals and the smart meter network.

2. Changes from the Last Practice Note

2.1 The Electronic Communications Code

The provision and operation of sites for electronic telecommunication networks have been regulated by the Electronic Communications Code since 1984.

A new Electronic Communications Code (part of the Digital Economy Act 2017) took effect on 28 December 2017. The new Code is designed to further facilitate the installation and maintenance of electronic communications networks of operators with Code powers.

The new Code changes the assumptions for the valuation of land to be used for the provision of electronic telecommunications infrastructure. In circumstances where a Code agreement is imposed upon a landowner/occupier or where the court is required to specify terms where the parties are unable to agree, valuation of the compensation will be on a “no scheme” basis based on compulsory purchase principles – rights valued on the basis of their value to the landowner rather than on the basis of the value to the operator for use as a telecoms site. Thus, any new agreements for mobile telecommunication sites made after 28 December 2017 under Code powers will be fundamentally different to those agreed before that date.

2.2 Emergency Services Network (ESN)

Emergency services network provision is in the process of switching from the previous radio-based system to 4G technology. This requires the construction of new sites to ensure the coverage necessary for the emergency services. The existing system remains as there have been delays in the development of a sufficient number of sites to enable the anticipated 4G network to become fully operational.

2.3 Smart Meter Network

A new national communication infrastructure to support the roll-out of smart meters has been developed. The infrastructure may be on new or existing sites. It may be on highways, greenfield or rooftop locations.

When attached to communications masts already in assessment some of the actual equipment for this infrastructure is not rateable, but it can still impact upon the rateable occupier. The general principle is that if the operator of the new equipment is the rateable occupier of the “parent” mast, the installation will have no effect on who is considered to be the rateable occupier. Alternatively, where the equipment is installed onto a mast from which the operator was not previously transmitting, a review of the assessment will be required to reflect the provisions of SI 2421. However, advice should be sought from NVU where changes are being made to a site as a consequence of smart meter technology.

2.4 5G technology

Commercial 5G networks began operating in June 2019. Initial roll-out was limited to a small number of cities. All mobile network operators are continuing their programme of upgrading sites and expanding their 5G network provision.

Upgrading of an existing greenfield or highway site to enable 5G transmission typically involves the replacement of the existing mast with a taller mast and the provision of more cabins and cabinets.

Typically, 5G equipment is heavier and more numerous than the equipment required for 4G transmission. As a result, the upgrade of rooftop sites may require the installation of a taller and more substantial stub tower capable of supporting the 5G equipment. It may result in antenna and supports being upgraded and moved to the edge of the building. It often involves the provision of additional cabins and cabinets on the rooftop.

The wider deployment of small cells as part of 5G networks is anticipated, but, as yet, evidence is very limited.

3.0 Ratepayer Discussions

Discussions with agents for the purposes of Revaluation 2023 had not taken place at the time of writing. It is anticipated that discussions with ratepayers’ representatives will take place prior to draft list publication.

4.0. Valuation Scheme

This practice note covers communications stations with a special category code of 066. It includes mobile telecommunication mast sites situated on highways, greenfield sites and rooftops.

4.1 Mobile telecommunication sites

The valuation approach is based on a site rent value with an addition for the rateable plant and machinery on the site.

4.2 Rental Evidence

Rental evidence is available for site rents for greenfield sites, rooftops, micro and pico cells. There is no rental evidence available for communication stations situated on public highways. The site rent values for these sites is derived from greenfield evidence.

Analysis of the available rental evidence has resulted in the designation of two valuation zones:

- Outside M25

- Inside M25

The scheme is split within each of those zones to distinguish between rooftop and non-rooftop sites. The schemes for site values for each zone and each category are set out below.

The values below are not yet agreed for the R2023 list. The values will be included within the valuation application. They may be subject to change if agreement is reached through central discussion with the operators and their agents prior to list publication.

4.3 Site values outside M25

4.3.1 Greenfield sites

| Greenfield sites | |||

|---|---|---|---|

| Type/definition | Height | Base site value | Cap |

| Highway sites: non-demised sites up to 15m in height located on a highway where no rent is paid | up to 15m | £4,600 | N/A |

| All Monopoles and towers not located on a highway | Up to 25m | £5,750 | To be confirmed |

| All Monopoles and towers | between 25.01 and 45m | £6,600 | To be confirmed |

| Towers | Between 45.01 and 60m | £13,000 | To be confirmed |

| Towers | Between 60.01m and 150m | £13,500 | To be confirmed |

| Guyed masts | Between 30.01 and 150.9m | £7,500 | To be confirmed |

| Towers and or guyed masts | Over 151 m | £27,000 | |

| Single guyed radiators | All heights | £7,500 | N/A |

| Paired guyed radiators | All heights | £11,250 | |

| Single and paired guyed radiator with monopole or tower | All heights | value as a pair Guyed radiator +25% of appropriate value attached to monopole/tower If single +50% of appropriate value attached to monopole/tower | N/A |

| Traffic monitoring sites | All Sites | £140 | £XXX |

| Site share addition/(Greenfield payaway) | To be confirmed | ||

| Minor Sharers | A company paying a rent less than or equal to £5,000 will be considered a minor sharer and therefore no valuation addition made for them being present on a site. | ||

| Pico or Micro Cells where wall mounted on or in buildings /kiosks | £2,500 | N/A | |

| Pico or micro cells within airports, stadia | To be confirmed | N/A | |

| TV stations. A greenfield site used as a TV and radio broadcast “repeater”. Generally located in rural locations where there is generally little/no demand by the MNOs. These sites will be single operator and could be up to a height of 45 m | £2,750 | N/A |

4.3.2 Rooftop sites

Rooftop sites are divided into three broad categories.

Category 1: non-typical rooftop sites offering greater than normal coverage. These are often, but not exclusively, to be found in central or prime locations or in areas of high mobile traffic volumes. Regard is had to the individual rents on such sites.

Category 2: these sites make up the majority of rooftop assessments. They will be in a variety of locations; secondary commercial areas, suburban and industrial areas.

**Category 3: **sites not within those above. These sites may be in very rural locations or may be on rooftops which offer only limited coverage due the height and being overshadowed by surrounding buildings.

| Rooftop Site Values | |||

|---|---|---|---|

| Category 1 | Category 2 | Category 3 | |

| Outside M25 (England and Wales) | To be valued individually. Non-typical and where the passing rent, adjusted to AVD, falls outside category 2 or 3. Non-typical sites may be regarded as rooftops offering greater than normal coverage, those in central or prime locations or in areas of high mobile traffic volumes. | £12,500 | £6,000 Poorer locations, for example rural areas with limited population density. Regard may be had to individual rents which, when suitably adjusted to AVD, produce a value below £5,000. |

4.4 Site values inside M25

4.4.1 Greenfield sites

| Greenfield Sites | |||

|---|---|---|---|

| Type/definition | Height | Base site value | Cap |

| Highway sites: non-demised sites up to 15m in height located on a highway where no rent is paid | up to 15m | £6,200 | N/A |

| All Monopoles and towers not located on a highway | Up to 25m | £7,750 | To be confirmed |

| All Monopoles and towers | between 25.01 and 45m | £13,500 | To be confirmed |

| Towers | Between 45.01 and 60m | £18,500 | To be confirmed (6 Major sharers) |

| Towers | Between 60.01m and 150m | £22,000 | To be confirmed (7 Major sharers) |

| Guyed masts | Between 30.01 and 150.9m | £17,000 | To be confirmed |

| Towers and or guyed masts | Over 151 m | All value individually | |

| Single guyed radiators | All heights | £17,000 | N/A |

| Paired guyed radiators | All heights | £25,000 | |

| Single and paired guyed radiator with monopole or tower | All heights | value as a pair guyed radiator +25% of appropriate value attached to monopole/tower If single +50% of appropriate value attached to monopole/tower | N/A (Not agreed under working party) |

| Traffic monitoring sites | All Sites | £140 | To be confirmed |

| Site share addition/(Greenfield payaway) | To be confirmed | ||

| Minor sharers | A company paying a rent less than or equal to £5,000 will be considered a minor sharer and therefore no valuation addition made for them being present on a site. |

Available rental evidence for pico and micro cells within the M25 shows differing values for high volume traffic areas such as railway stations or shopping centres and postcode areas within Westminster, City of London and some other business districts. The 5 categories are set out below.

| Pico and micro cells, wall mounted on or in buildings/kiosks (including flag pole types on sides of buildings and forecourts) | ||

|---|---|---|

| Category | Location | Site value |

| Category 1 | Main line stations termini and shopping centres | To be confirmed |

| Category 2 | Postal districts W1, WC2, EC1, EC2, EC3, EC4, E14 | To be confirmed |

| Category 3 | Postal districts N1,N6, N7, NW1, NW3, NW5, NW6, NW8, SW1, SW3, SW5, SW7, SW10, W2, W8, W9, W10, W11, W14, WC1, E1, E2, N1, N14 | To be confirmed |

| Category 4 | Postal districts NW10, SW6, W6, W12, E3, E5, E8, E9, N5, N7, N16, N19 | To be confirmed |

| Category 5 | All other postal districts and locations not included above. | To be confirmed |

4.4.2 Rooftop sites

Rooftop sites are divided into three broad categories.

Category 1: non-typical rooftop sites offering greater than normal coverage. These are often, but not exclusively, to be found in central or prime locations or in areas of high mobile traffic volumes. Regard is had to the individual rents on such sites.

Category 2: these sites make up the majority of rooftop assessments. They will be in a variety of locations; secondary commercial areas, suburban and industrial areas.

**Category 3: **sites not within those above. These sites may be in very rural locations or may be on rooftops which offer only limited coverage due the height and being overshadowed by surrounding buildings.

| Rooftop Site Values | |||

|---|---|---|---|

| Category 1 | Category 2 | Category 3 | |

| Inside M25 (Excluding Central London postcode areas: EC, E13 – E16; NW1, NW3; SW1; W1; WC) | Valued individually where the rent passing, adjusted to AVD, is tbc% greater than the Category 2 site value. | £18,000 | Valued individually where the rent passing, adjusted to AVD, is tbc% lower than the Category 2 site value. |

| Central London Postcode Areas | Valued individually where the rent passing, adjusted to AVD, is tbc% greater than the Category 2 site value. | £28,000 | Where the rent passing, adjusted to AVD, is tbc% lower than the Category 2 site value; site value £20,000. |

4.5 Site Sharing and Payaway

Mobile network operators continue to share sites through joint venture companies and the use of Mobile Operator Random Access Network (MORAN) sharing.

The new Electronic Communications Code prevents this type of payment being taken into consideration when agreeing Code site rents. Rent reviews in older agreements will be on terms which do not reflect the new Code provisions. Such rents may still include provision for site sharing and payaway.

The valuation scheme makes no addition for site sharing and payaway.

1. Market Appraisal

1.1 Consolidation

The Telecoms market at the AVD and before has been undergoing change with companies entering into collaborations leading to a general convergence of the Telecom companies and the products that they are able to offer.

In 2008 T Mobile and Hutchison Whampoa (otherwise known as 3 (Hutchison 3G)) created a 50:50 joint venture called Mobile Broadband Network Limited. MBNL was set up to allow the sharing of infrastructure that would provide savings in both Capital Expenditure (CAPEX) as well as Operational Expenditure (OPEX). Their aim was to be achieve these costs by sharing sites through RAN sharing methodology. In contrast to the traditional method of sharing, where each company installs it own equipment (cabling cabins etc) RAN or radio access network sharing is achieved through electronic means - see glossary.

In locations where T Mobile and 3 both previously existed, the direct consequence of this joint venture was for Hutchison or “3” sites to be decommissioned, with the transmission being moved to the nearby T Mobile site.

In late 2009 initial discussions between Telefonica UK Ltd and Vodafone commenced which led to the establishment of Cornerstone.

Cornerstone’s model was fundamentally different to MBNL. Unlike MBNL who share sites and operate through one set of infrastructure, it is understood that CTIL initially provided an estate management function for the two Mobile Network Operators (MNOs) before developing a longer term operational network plan/structure.

Subsequently the relationship was strengthened with the creation and incorporation of the company now known as Cornerstone Telecommunication Infrastructure Limited in 2012. CTIL commenced the delivery of a revised network of masts in 2014/2015 with the country now split geographically. Vodafone will now be the primary operator in the west of England and Wales; Telefonica UK Ltd known as O2 will be the primary operator on the eastern side of the country. Each will also occupy as sharers where they are not the primary operator.

In April 2010 France Telecom (Orange) and Deutsche Telekom (T Mobile) announced a formal merger of their UK operations and Everything Everywhere (EE) was born.

The reality is that this was a re-branding of T Mobile, their company number simply was transferred to the new company, with the assets of Orange being acquired.

All of the above events have occurred since the 2010 list AVD but importantly have done so well before the AVD for the 2017 list. It has been agreed that the rental evidence used to establish the proposed scheme of value for 2017 reflects the circumstances outlined above.

The market in Telecoms is forever changing; further mergers have been announced or known:

-

In November 2014 BT announced proposals to acquire either O2 or EE. Following discussions BT made an offer of £12.5 billion for EE, with the deal being announced in February 2015

-

In early March 2015 3 (Hutchison Whampoa) agreed to purchase O2 for £10.25 billion.

Although not yet completed it could reasonably be argued that they would be in the mind of the hypothetical landlord and tenant in reaching an agreement at the AVD. It certainly can be suggested that any actual evidence of market rents since this time would have been agreed in the knowledge of potential future changes.

Consolidation within the telecommunication market is leading to an increase in the sharing of sites and decommissioning of sites where two former competitors had sites neighbouring each other. However there is still demand for sites in areas where operators do not have a presence.

1.2 Changes to the Electronic Communication Code

Under pressure from the industry to reduce costs (site rents) and to provide easier access to enable them to fulfil the licence requirements, the government is preparing proposals to update the Electronic Communication code (The Code) and make some minor amendments to the planning regime.

At the time of publication it is still unknown what is being proposed.

However, with consultations commencing 2014 it could be reasonably argued that the hypothetical landlord and tenant would have been aware that changes to The Code were being proposed and would be in their minds in reaching an agreement on value at AVD.

2. Changes From The Last Practice Note

The changes are a consequence of company mergers and joint ventures, as outlined above. The main operators are currently:

a) Everything Everywhere previously T Mobile and Orange;

b) Hutchison 3G;

c) Vodafone; and

d) O2 (Telefonica UK Ltd)

Other mast providers include:

e) Airwave Solutions - provide mission critical closed network for the emergency services;

f) Arqiva - Provide sites for the broadcast of TV and Radio as well as infrastructure provision to the mobile companies;

g) Wireless Infrastructure Group (WIG)

Whilst the mobile phone companies operate independently their network of mast sites are managed by:

Firstly - MBNL for EE and 3; and

Secondly - CTIL for Telefonica (O2) and Vodafone

Please note that although these “managing” companies acquire and project manage the site development they are not in rateable occupation.

2.1 Site Sharing

This is the term used where operators agree to co-locate on a single site/Mast. Traditionally this has resulted in the sharer adding their own equipment to an existing structure.

Technological advances means that sharing can be achieved by installation of additional electronic non rateable equipment. The term for this type of sharing is radio Access Network (RAN) sharing.

2.1.1 Greenfield Sites

Due to changes in the market highlighted in para 1.1 above the site rental now reflects the occupation of a site to be used by the “head tenant” to operate their “family of providers” through the site.

To reiterate changes brought about by network consolidation have been noted in the passing base site rents.

It is recognised that at both the Antecedent Valuation Date (AVD) and potentially Compilation Date (CLD) not all greenfield sites will have been consolidated. However, in discussion with the operators representatives they were very clear that the rents paid in the period post Jan 2013 reflected the right of MBNL to operate any one of their joint venture companies network. This situation is now being replicated by CTIL for Vodafone and Telefonica UK Ltd (O2) under their MORAN (Multiple Operator RAN) project.

2.1.2 Payaway

The term Payaway is used by the telecoms industry to reflect the additional amount a landlord would expect in addition to the base rent. This has tended to be a percentage of the fees received by the head tenant from other users on the site. The percentage on Greenfield sites has declined as the telecoms market has matured.

The evidence suggests that where any of the head tenant’s extended family occupy part of the site there should be no Payaway, but may be sought where there are users unconnected to the head lessee.

There is evidence still to suggest an addition to the base rent (Payaway) is demanded and paid in respect of users unconnected to the head lessee.

Analysis of the evidence suggests that this should be £2,500 for sharers on a Greenfield sites both inside and outside the M25.

The qualification for an addition to be made the assessment is, where in addition to the HOST operator, the sharer: a.has their own rateable plant and machinery; and b.is not part of the host company

Where both these criteria are satisfied then a separate sharing addition should be added.

2.1.3 Site Rent - The Cap

This is the maximum site rental value that should be applied to the Hybrid valuation in calculating the overall rateable.

It is acknowledged that the market the landlord would not expect or receive infinite additional payments (Payaways). Therefore the CAP replicates the market in establishing a maximum that we apply for a given site. The CAP is based on the base rent plus an amount of Payaway assumed from the maximum number of site sharers that would likely to be present.

On the highest structures the CAP will be greater as the anticipated number of site sharers will be greater.

2.1.4 Sharers - Major and Minor

As outlined above the base site rent reflects the occupation of a head tenant. In those instances where they themselves do not transmit or broadcast then they are substituted by the immediate first operator (sub tenant).

If there are any further occupiers it is then necessary to consider if they are

(i) minor sharer

defined as any other occupier/operator who whilst occupying pays a rent of less than or equal to £5,000.

No site share addition will be made in these instances to reflect their presence on the site.

(ii) Major Sharers

All the major mobile phone companies are considered major sharers together with anyone who pays a rent above the £5,000 limit.

The addition of £2,500 is applicable and applied where appropriate given the rules set out above.

2.1.5 Sharing - Rooftop Sites

The basis for rooftops is completely different and so is the calculation to arrive at the addition made where sharing takes place.

Once the evidence has been considered a further paragraph may be added re the approach to caseworkers should take where rental evidence exists/doesn’t exist.

2.2 Impact of Changes Post 2010

Potential changes to “the code” being proposed at the AVD as well as the joint ventures outlined in 2.0 above provided doubts that there would be sufficient information to retain the site share addition especially on sites up to 30 metres in height.

However, following discussions with the various parties it was confirmed that site share fees are still paid where a CTIL company shares with an MBNL company and vice versa.

In the circumstances it was agreed to retain the addition £2500 for site sharing (see below) on Greenfield sites. In a change from previous lists where the addition for within the M25 was greater than the remainder of the country the addition is now considered a national addition and applicable in all areas to Greenfield sites.

3. Ratepayer Discussions

Members of the CCT met with industry representatives in a series of meetings between 18 and 20 August 2015.

A number of matters were discussed, including:

-

Clarification on rental payments and the number of permitted operators;

-

Highways/Streetwork sites; and

-

Whether height was a real determining factor on value.

The results of these exchanges is shown in paragraph 4 below.

4. Valuation Scheme

4.1 National Scheme

There are two valuation zones: i.Outside M25; and ii.Inside M25

4.2 Greenfield Basis

4.2.1 Highway / Streetwork Sites

The definition was not agreed or finalised in the discussions with industry, however, the Valuation Office view is:

“a non demised site of up to 15 metres in height located on the highway, where no rent is paid”

4.2.2 Size Height Bands

It was agreed to simplify the valuation approach and to reduce the “size” bands. The table below reflects outcome of the discussions, which the operators’ representatives intend to recommend to their clients for sites up to 30 metres in height.

All operators are working towards all sites being consolidated before 1 April 2017. There will still be instances where sites are occupied by a single operator. It is also becoming less common for sites to be “traditionally” shared, with the exception being on sites hosted by an infrastructure provider e.g Arqiva.

4.2.3 Single Operator Sites

From the discussions with the operators it is understood that at the compilation date there will be instances where sites will be occupied by a sole operator.

The basic site rent will apply with no allowance applicable.

4.2.4 Consolidated Sites

In a change from previous rating lists the base site rents, tabulated below, reflect the occupation of two operators on “a consolidated site”. Rental evidence and consultation with the industry indicates that that landlords have accepted this as being a standard condition.

A consolidated or RAN shared site will have two operators from either of the managing companies operating through a single set of equipment and the rents now being paid reflect these circumstances.

The rental evidence analysed assumes that the rent reflects the ability of the head tenant to operate their “family of providers” through the site.

Therefore where MBNL have developed a site it may have EE operating or EE and 3 and the basket of rental evidence reflects either of these scenarios.

4.2.5 Non Consolidated Sites

The analysed rents assume that the rent reflects the ability of the head tenant to operate their “family of providers” through a consolidated or RAN shared site.

There will still be instances where a site contains two providers from within the same management company. In these cases no addition should be made to the base rent.

4.3 Rental Basis - Tabulated

4.3.1 Outside M25 - Site Rentals

4.3.1.1 Greenfields

| TYPE/DEFINITION | HEIGHT | BASE RENT | CAP See section 2.1.3 above |

| Highways</p> "A non demised site of up to 15m in height located on a highway where no rent is paid</p> | up tp 15m | £5,250 | N/A |

| All Monopoles and Towers not located on a highway | Up to 30m | £6,600 | £19,101 |

| All Monopoles and Towers | between 30.01 and 45m | £12,000 | £27,001 (6 Major Sharers) |

| Towers | Between 45.01 and 60m | £16,500 | £34,001 (7 Major sharers) |

| Towers | Between 60.01m and 150m | £20,000 | £40,001 |

| Guyed Masts | Between 30.01 and 150.9m | £17,000 | |

| Towers and or Guyed Masts | Over 151 m | All valued individually | |

| Single Guyed Radiators | All Heights | £17,000 | N/A |

| Paired Guyed Radiators | All Heights | £25,000 | |

| Single & Paired Guyed Radiator with Monopole or Tower | All Heights | Value as a pair Guyed Radiator +25% of appropriate value attached to monopole/tower</p> If single +50% of appropriate value attached to monopole/tower</p> | N/A (Not agreed under working party) |

| Traffic Master | All Sites | £140 all inc of P&M | |

| Site Share Addition / (Greenfield Payaway) | - | £2,500 | |

| Minor Sharers | A company paying a rent less than or equal to £5,000 will be considered a minor sharer and therefore no valuation addition made for them being present on a site. |

Pico or Micro Cells where wall mounted on or in buildings /kiosks (including flag pole types on sides of buildings and forecourts)

| LONDON CENTRAL AND WESTMINSTER AREA | Value | Location |

| Pico or Micro Cells where wall mounted on or in buildings /kiosks (including flag pole types on sides of buildings and forecourts) | Category 1 £6,000 | Main Line Stations Termini and Shopping Centres |

| Category 2 £3,250 | Postal Districts W1 and WC2 | |

| Category 3 £3,000 | Postal Districts EC1,N1,N6,N7,NW1,NW3,NW5 NW6,NW8,SW1,SW3,SW5,SW7 SW10,W2,W8,W9,W10,W11,W14 WC1 | |

| Category 4 £2,750 | Postal Districts NW10,SW6,W6,W12 | |

| TV Repeater Stations “Broadcast Mast” with No sharers on Greenfield sites up to 45 M | N/A | |

| LONDON CENTRAL -CITY AREA ONLY | Value | Location |

| Category 1 | Valued separately, supported by individual rents. | |

| Category 2 £3,250 | (City) Postal Districts EC1,EC2,EC3,EC4 | |

| Category 3 £3,000 | (City Fringes) Postal Districts E1, E2,N1,N14, remainder of E14 | |

| Category 4 £2,750 | (Remainder) Postal Districts E3,E5,E8,E9,N5,N7,N16,N19 | |

| TV Repeater Stations “Broadcast Mast” with No sharers on Greenfield sites up to 45 M | N/A | |

| LONDON SOUTH AND NORTH AREAS OUTSIDE OF CITY AND CENTRAL AREAS (Former London South and North Groups) | ||

| Value at ALL Locations | ||

| Pico or Micro Cells where wall mounted on or in buildings /kiosks (including flag pole types on sides of buildings and forecourts) | £2,750 | |

| TV Repeater Stations “Broadcast Mast” with No sharers on Greenfield sites up to 45 M | N/A |

4.3.2.2 Rooftop Sites Inside M25

Reserved

Note these figure include rateable P&M unless the rateable equipment is similar to that found at mobile phone sites (such as towers or cabinets).

Appendix 1

EXAMPLES

The following scenarios are to assist the understanding of the above guidance note. They are illustrative only and in no way meant to be exhaustive as the individual circumstances of particular sites will need obtained.

Single Operator Site (Para 4.2.3)

Everything Everywhere (EE) is the single operator

Base Rent = £5,000

Sharer addition = ZERO as None present

Total Site Rent = £5,000

2 Consolidated Sites (Para 4.2.4)

Site is managed by MBNL, EE and 3 occupy the site and share one set of equipment (RAN Share)

Base Rent = £5,000

Sharer addition = ZERO

tal Site Rent = £5,000

Non Consolidated “Shared Site” (Para 4.2.5)

Scenario 1

Where the site is managed by one of wither MBNL or CTIL and historically both there providers are in occupation and transmitting e.g MBNL and EE and 3 are on site and have their own set of equipment.

Base Rent = £5,000

Sharer addition = ZERO

tal Site Rent = £5,000 - See Notes below

Scenario 2

As scenario 1 above but with a further sharing by Airwave and O2 (Telefonica UK Ltd)

Plus Sharing

Base Rent = £5,000

Airwave + £2500

O2 + £2,500

tal Site Rent = £10,000

4 Infrastructure Provided Sites

Scenario 1

Site is managed by Arqiva but only EE occupy and transmit from the site

Base Rent = £5,000

Sharer addition = ZERO No site sharing occurring

Total Site Rent = £5,000

NB: This is the same as 5.1 above

Scenario 2

Site is managed by Arqiva. Arqiva broadcast from the site and EE occupy and transmit as a sharer. They have their own rateable equipment

Plus Sharing

Base Rent = £5,000

EE + £2,500

Total Site Rent = £7,500

Notes:

3 Scenario 1

At Compilation Date (CLD) there will be some sites that due to historic agreements will continue to be operated on as a Non Consolidated sites i.e. they will have their own equipment.

It is evident from the majority of the new lease agreements that the preference of MBNL and CTIL would be to have one set of equipment and to RAN share.

In rating the hypothetical tenancy is considered at the Material Date with the tenant coming fresh to the scene.

Therefore in comparison with the 5.2 how it can be justified that where these circumstances exist the tenant would agree to pay an additional £2,500.

NB: All the rateable P&M would be valued.

1. Market Appraisal

Limited open market evidence exists.

Wifi/Bluetooth sites may be used in connection with a business conducted from the host property, such as a coffee shop. This is seen as an attraction to customers who can access the WiFi for free., Alternatively WiFi may be installed in vacant premises.

2. Changes From The Last Practice Note

These installations continue to be installed in both occupied and vacant buildings . However the duration of their presence within a fixed unit of accommodation varies according to the individual needs of both the operator and the landlord.

3. Ratepayer Discussions

No discussions with the industry as these types of WiFi/Bluetooth installations are generally installed at the request of Landlords whilst the host unit of accommodation is vacant.

4. Valuation Scheme

A site in an empty property will form a separate hereditament if it fulfils the criteria necessary to become a separately rateable hereditament. It is a common characteristic that sites are occupied for short, or transient, periods. When occupation exceeds 12 months the site becomes a separately rateable hereditament to the “host” property. The site is a new hereditament and should not be a split from the host hereditament.

The rateable value for the WiFi/Bluetooth hereditament is £100. This is irrespective of the number of pieces of WiFi/Bluetooth equipment within a single host property.