Guest and boarding houses

This publication is intended for Valuation Officers. It may contain links to internal resources that are not available through this version.

This section covers guest houses and bed and breakfast accommodation.

Special category code 122 should be used; as a generalist class the appropriate suffix letter should be G.

Guest houses and bed and breakfast accommodation are generalist classes to be dealt with by Rating Valuation Units (RVUs).

The Hotel Class Co-ordination Team has overall responsibility for the co-ordination of this class. The team are responsible for the approach to and accuracy and consistency of valuations. The team will deliver Practice Notes describing the valuation basis for revaluation and provide advice as necessary during the life of the rating lists. Caseworkers have a responsibility to:

- follow the advice given at all times

- not depart from the guidance given on appeals or maintenance work, without approval from the co-ordination team

- seek advice from the co-ordination team before starting any new work

Many properties in this class are occupied in conjunction with residential accommodation and may fall within the definition of domestic property. Such properties will not be rateable.

5.1 Statutory background

Short stay accommodation, which includes hotels, guest houses and bed and breakfast establishments, is rateable by virtue of Section 66(2) Local Government Finance Act 1988 [LGFA 1988]. S66(2A) LGFA 1988, which was inserted by S1 1991 No 474: The Standard Community Charge and Non-Domestic Rating (Definition of Domestic Property) (Amendment) Order 1991, introduced rules which are intended to ensure that certain types of “bed and breakfast” uses are not rated. This provides that such accommodation will continue to be domestic property (and therefore not rateable) if:

a. it is intended that within the coming year the short stay accommodation will not be provided for more than six persons simultaneously and

b. the proprietor intends to have his or her sole or main residence within the hereditament and the short stay use will be subsidiary to the use of the hereditament as the proprietor’s sole or main residence

5.2 The “Six Person” test

It may sometimes be difficult to establish the number of persons for whom the proprietor intends to provide short stay accommodation. Local and national tourist literature, which often contains appropriate details, may be a source of useful information. Another practical approach will be to ascertain how many bed spaces the premises contain in addition to those reserved for the private use of the proprietor and family. Any such count should be in relation to the number of adult spaces, and cots for babies and toddlers should normally be excluded. Beds which are provided and used on an exceptional basis in family rooms, and which are removed when not required, should not be included in the count. Where it is clear that there is sufficient accommodation for more than six persons but proprietors insist that they do not intend to make it available for more than that number, the subsidiary use test may be of particular assistance in determining rateability or otherwise. The DOE Consultation Paper of August 1990 recognised that a limit set at 5 or 6 persons only might exclude from rating significant business enterprises; the subsidiary use test is intended to prevent this happening.

5.3 The “Subsidiary” Test

The wording of the subsidiary use test in SI 1991/474, together with the above mentioned Consultation Paper suggest a number of criteria as a basis for this test.

a. Firstly, where the short stay accommodation comprises part of a hereditament which also contains other related non-domestic uses, such accommodation should not normally be regarded as being subsidiary to the use as the proprietor’s sole or main residence, but rather as being part and parcel of the business venture. Related non-domestic uses would include, for example, use of the hereditament as an inn, hotel or licensed restaurant, but would not include uses such as a village shop or a tractor repair workshop, which are unconnected with the short stay use. Another related use would be self-catering accommodation comprising part of the same hereditament. If the self-catering accommodation is not rateable by virtue of the 140 day rule, (see Rating manual: section 6 part 3 - section 480 Para 4 relating to the LT decision of Godfrey v. Simm (VO) RVR 2000/247) it should also be left out of account for the purposes of the “subsidiary” test because it will be shown as a separate dwelling and banded for Council Tax.

b. The second criterion relates to the proportion of accommodation within the hereditament used for short stay use compared with that used in connection with the proprietor’s sole or main residence. If the intention is that at any time during the forthcoming year, more accommodation will be given over to short stay use than will be retained for the private use of the proprietor and family, then the short stay use should not be regarded as subsidiary. This criterion should be applied to the total amount of accommodation within the hereditament, and not just to the bedrooms. This may avoid assessing proprietors providing a given amount of space in a small house, whilst those providing the same amount in a larger house might not be assessed. Where accommodation is used for both the proprietor’s private use and business use, a “wholly or mainly” test should be applied, in order to determine whether or not it should be treated as non-domestic property. In doing so, regard should be had to the nature of the furnishings and fittings, and to the extent and frequency of the non-domestic use. The provision of cable/satellite TV in rooms, telephones, separate room locks with keys etc may be suggestive of, but not necessarily conclusive, as to non-domestic use. If a dining room is permanently furnished with three or four dining tables it should be regarded as non-domestic even though the proprietor might take his or her own meals there. Conversely, if the guests are just provided with breakfast in the proprietor’s own living quarters, the latter should be treated as domestic property. The presence of a licensed bar or other facilities, which are not normally found in a private dwelling, may suggest business use.

c. a further indication that use of living accommodation for the provision of short stay accommodation is not subsidiary to the use of the hereditament as the proprietor’s sole or main residence might be the degree of physical adaptation which has taken place. If the character of the hereditament is such that it goes beyond that of a private dwelling house, then providing it is sufficiently utilised for short stay use, it should be possible to argue that such use amounts to a separate business venture rather than a use which is subsidiary to the dwelling house use. Such adaptation might include the provision of en suite bathroom facilities in each room, fire doors, fire alarms and fire extinguishers. It is not possible to give detailed guidance as to what precise coincidence of circumstances would lead to rateability, as each case will need to be judged on its merits. The emphasis must be placed on the use of the premises, whereas mere registration with the local tourist bureau would not be sufficient. It should be borne in mind that the intention of the “subsidiary use test” is to ensure, as far as possible, that whilst the provision of limited short stay accommodation in a person’s own home will not be subject to rating, this exemption will not extend to those where the main use of the property is clearly non-domestic. The case of Skott v Pepperell (VO) 1995 RA 243 where it was decided that the bed and breakfast accommodation was not subsidiary to the domestic use provides further guidance.

5.4 Unit of assessment

First, it may be helpful to clarify when a property is to come into assessment. It can only be included in the rating list when there is a rateable (non-domestic) use. This might be an actual use (for example, seasonal letting), a potential use (property housing furniture and fittings which are being kept pending the holiday season, and which is not otherwise occupied for domestic purposes), or it may be vacant non-domestic accommodation (part of a composite hereditament) which is liable to empty property rating. Once the property has been identified as rateable, in taking preliminary account of what might reasonably comprise the domestic accommodation and what the non-domestic (i.e. the letting part) might be, the VO should have regard to the likely pattern of use throughout the year. The Government’s intention is expressed in paragraph 24 of the Consultation Paper on composite hereditaments, and option 4 as there described is the one that is to be adopted (valuation by reference to general patterns of use i.e. ‘Notionality’). For the avoidance of doubt, it is not intended to vary the assessment to take account of (i) the length of season adopted by a particular occupier, if that is untypical, or (ii) the extent of the living accommodation which is made available by a particular occupier, if that is contrary to the usual pattern. Instead, it is the aim to assess the balance of use within the year having regard to the property that could be made available to let, and then to value that use both with regard to the extent of the non-domestic part and the duration of that use. For example, if a seasonal guesthouse is in business for an average of 16 weeks each year, and there are on average 3 bedrooms (with ancillary accommodation) which are made available for letting, the use to be valued will be that of 3 letting bedrooms for 16 weeks. The amount must be expressed as an annual value and entered in the rating list as the rateable value for the relevant part.

5.5 Seasonal property

When valuing hereditaments which are only rateable for part of the year (for example, for 20 weeks out of 52), it is necessary to consider both the way in which relevant information has been analysed and the way in which it is intended to apply the resultant values. It may help to consider some examples:

Example one A family house where there is holiday letting of a substantial part of the accommodation for a season which has an average length of 20 weeks, after which it all reverts to family use. It is rented, and the rent reflects the non-domestic potential. It is necessary to value the non-domestic potential (applying a “notional” pattern of use where it is not considered that the full potential is realised by the actual occupier). This requires the valuer to stand in the shoes of the hypothetical tenant and decide what the holiday letting potential is worth, out of the annual rent that is to be paid, compared with the residual value of the domestic occupation on the same assumed pattern of use. The value to be entered in the list is the sum of the value on a week-by-week basis for the whole of the potential non-domestic use.

Example two A family house where the potential letting use of the property is maximised by all-year-round letting, out of the holiday season to students, in season to holidaymakers. Here, the value of the letting accommodation has to be apportioned between the part which is rateable (for short-term letting to holidaymakers whose sole or main residence is elsewhere) and that which is not. First, the domestic use made of the residence by the proprietor and his family will have to be excluded from consideration. Then, the holiday season value (which will most probably be higher than that for out-of-season letting) needs to be isolated as the value which should be entered in the rating list. The period of time when the letting accommodation is occupied by students (or in other instances by long-term residents) as their sole or main residence will not be rateable. In ascertaining the value in the case of either of these examples, it should be apparent that when values are being imported from other classes of property (notably hotels and permanent guest houses), it will not suffice merely to take an arithmetical proportion of the value. For example, if the rental value of comparable guesthouse accommodation (which is in commercial use for 52 weeks of the year) is £250 per double bed unit per annum, it would not be appropriate to apply that to a seasonal composite hereditament using the formula £250 x 20 weeks 52 weeks assuming the seasonal use to be of 20 weeks’ duration. If the basis of value to be applied was itself seasonal (for example, a guest house where the business was confined to 20 weeks only), then the application of that value to seasonal use elsewhere would be more directly comparable. It may not be necessary to specify the assumptions that have been made about the length of the season, where it has been derived directly from other hereditaments enjoying a similar length of season, but there will equally be circumstances when it will be necessary to identify the underlying assumptions. For example, a judgement might have to be made to distinguish between accommodation (near the sea front) which has nothing but holiday potential, and that (near the sea front and a conference centre) where there is a demand for both holiday and conference use. There are bound to be some difficulties in establishing a uniform approach to this very varied category of property, but the aim is to establish an average pattern of occupation - perhaps that appropriate at the early or late part of the holiday season. It is expected that circumstances will vary between localities and that this will be an item for discussion as part of co-ordination procedures. It may be possible to obtain general information about the pattern of lettings from holiday bureaux in the locality.

Bed and Breakfasts and guest houses should be measured to Net Internal Area (NIA) in accordance with the VOA Code of Measuring Practice for Rating Purposes. The survey should include the following information: The type of premises, location, age, number of bedrooms (including type of room, e.g. double, family, single, whether en-suite or not) construction, services (including heating), the date when last refurbished, type extent and quality of ancillary facilities (areas for dining rooms, lounges and other guest accommodation should be separately shown), parking, details of bathroom and WC facilities, if any bar or restaurant is open to non-residents, the use of temporary marquees for wedding receptions and other functions. Details of any licence (see Para 8.3.3 below) should be obtained including details of the premises covered, e.g. whether the garden is included, the licensable activities covered, the operating schedule and details of the numbers and purpose of any Temporary Event Notices.

The inspection checklist is accessible and stored within EDRM.

8.1 General

Rental evidence should form the basis of valuation, although it may be necessary to cast the net wide for the rental evidence.

8.2 Units of comparison

For the small guest house, price per square metre of area may be a helpful and adequate basis of comparison although rents and assessments can also usefully be expressed in terms of a unit price per “converted” bedroom, or “equivalent bedroom”. The unit of comparison to be used is the Double Bed Unit (DBU) and the factors to be used when calculating the DBU are set out below. The extent to which separate values may have been ascribed to ancillary items such as car parks and swimming pools may affect the validity of a DBU comparison. It is therefore important to remember that adjustments may have to be made to exclude or include the value of some ancillaries before the calculation of a price per unit can be made on a common basis. Where rental evidence exists it should also be devalued by reference to receipts as a percentage of gross takings from all sources (GTAS) excluding VAT. Such analysis can be used as a further basis of comparison but percentages may vary according to the number of ancillary items provided.

8.3. Valuation considerations

Amongst other things consideration should be given to the following points, all of which may have a bearing on value.

8.3.1 Accommodation

It is not sufficient merely to take account of the total accommodation. The following matters also require to be considered:

-

whether the number of double and single bedrooms (with or without bathrooms) are in balance with the needs of the locality and the class of trade

-

do any public rooms provide adequate facilities for guests?

-

are any kitchens up to standard and convenient for economical working?

-

the number of bathrooms (where these are not en-suite with the bedrooms)

-

are there adequate lifts?

-

whether there is sufficient parking available for guests (either on the hereditament or close by)

8.3.2 Double Bed Units (DBUs)

The method of calculating the number of DBUs should be the same as for hotels (see table below) and be standard throughout the network . Any minor local variation from the national guidelines will be exceptional. The layout, and actual use should be determinative in room classification. The number of DBUs should be expressed in accordance with the standard factors set out below:

DBU factors

| Room Classification | DBU Factor |

|---|---|

| a) Double or twin | 1 |

| b) Single | 0.7 |

| c) Family | 1.25 |

| d) Suite - standard - bedroom with large open plan sitting area | 1.5 |

These factors apply to ground and first floors and also basement and upper floors where served by passenger lift(s). The above factors should be reduced by 15% for rooms on basement and second floors without a passenger lift, and by 25% for rooms on the third floor and above if not served by a lift. Where rooms do not have en-suite facilities these factors should be reduced by 0.25. (For example, a ground floor double room without a bath/shower or WC would have a factor of 0.75.)

How the operator is trading in terms of DBU may provide assistance, but will be dependent upon factors such as type or quality of premises, location and age. For example the double or twin bed maybe larger or smaller, dependent on the quality of bedroom offered in a particular property/ locality.

8.3.3 Situation

The importance of situation cannot be overstated. Convenience to transport facilities or town centres will encourage tourist and commercial guest houses. At seaside holiday resorts the distance from the sea and views from the bedrooms will have a considerable bearing on the popularity of the guest house.

8.3.4 Liquor licence, catering and functions

Until full implementation of the Licensing Act 2003, guest houses may have possessed a “residential licence” (but this will not normally be value significant); and/or “restaurant licence” within the meaning of Part IV of the Licensing Act 1964. The latter may be value significant if the premises attracted non-residential trade. Following the coming into effect of the Licensing Act 2003 on 24 November 2005 in order to sell alcohol the premises will need a “Premises Licence”; there will also need to be a “Designated Premises Supervisor” (DPS) who will be named on the premises licence and who will require a “Personal Licence” under the Act. In addition to the sale of alcohol the licence may cover any provision of regulated entertainment (which includes the playing of recorded music and live bands {except bands playing at weddings}) and provision of late night refreshment. In addition any establishment, licensed or not, may apply for up to 12 Temporary Events Notices during a calendar year – this will cover marquees for wedding receptions, or other functions, among other purposes. If it is intended for alcohol to be sold the application must be made by a personal licence holder.

8.3.5 Fire safety

The Regulatory Reform (Fire Safety) Order 2005, SI2005/1541 introduced a new regime for fire safety replacing a raft of earlier regulation. Fire authorities no longer issue fire certificates and those previously in force have no legal status. The order applies to virtually all premises except private houses and flats. It applies to all guest accommodation properties, e.g. bed and breakfasts, guest houses, inns, restaurants with rooms, and farmhouses. Under the Order a responsible person who has control of the premises must carry out a fire-risk assessment of the premises which should identify fire hazards, identify people at risk, evaluate, remove or reduce and protect from risk, record findings and prepare an emergency plan, and regularly review.

8.3.6 Judges’ lodgings

These are accommodation provided for High Court judges when they try serious criminal and civil cases on circuit around the country. The properties concerned are large houses, often listed and/or with extensive grounds, and will normally provide 1 to 5 suites of accommodation for judges. A suite would normally comprise a double bedroom with en-suite bathroom and lounge /study for the judge and a single bedroom with en-suite for the judge’s clerk. In addition there will be ancillary dining and lounge facilities suitable for entertaining small parties of up to 12 or 15. There will also be domestic accommodation (comprising one or more composite CT assessments) for permanent staff – butlers, housekeepers or managers either in the main building or within the grounds. The accommodation is to provide physical security, privacy and an environment where the judges can undertake work out of court and is equivalent to, at least, 4* hotel accommodation. It is therefore essential that the DBU number correctly reflects the accommodation provided, and that the values adopted reflect the very high standard and amount of accommodation provided. It is expected that values applied will be substantially higher than those for other guest accommodation and should have reference to the best small 4* hotel accommodation (liaise with Hotel CCT as necessary). The description appearing in the Rating List should be overwritten “Judges Lodgings and Premises”.

8.3.7 Other considerations

Properties with other facilities such as bars, restaurants and function rooms with significant non-residential trade may need special consideration. In exceptional circumstances alternative valuation approaches may need to be considered reference should be made to the Rating Manual sections for Hotels, Public Houses and Restaurants.

8.3.8 Numbers of hereditaments in assessment

VOs should ensure as far as they are able that all rateable non-domestic use has been fully reflected. Periodically information contained in local holiday literature or websites together with any registers kept by the local authority should be monitored to identify any hereditaments no longer trading or not in assessment and worthy of further investigation.

Within RSA analysis and valuation scales specifically for this class enable input of factual data to achieve valuations that follow the recommended approach.

1. Market appraisal

1.1 The demand for guest house and bed and breakfast accommodation is largely driven by the numbers of domestic and international tourists and business travellers. Hence occupancy and turnover are heavily influenced by factors which impact on decisions to travel to and within the United Kingdom.

1.2 Since the last AVD (1 April 2021) the hospitality sector has benefited from the lifting of Covid-19 restrictions, these had a significant negative impact on the industry. Pent-up demand for holidaying saw revenues surge in hotels in 2021-22, though still below pre pandemic levels. The return of international tourism boosted the pace of the recovery in the sector while staycations increased within the UK also.

1.3 Revenue recovery has continued through 2023 into 2024 as tourism levels have increased. However, lower disposable incomes driven by inflationary pressures is a limiting factor on revenue growth.

1.4 Online Travel Agencies, social media networks and mobile technology have continued to have a big impact on the industry.

1.5 Following the pandemic there has been significant labour shortages in the hospitality sector which has had the effect of wage inflation. Other operating costs such as food and drink prices, and utilities have also impacted profit growth.

1.6 There has been increased competition both from budget hotel operators and aparthotels, and from hosting or sharing websites which have remained popular. Poorer guest houses have often seen revenue declining as rates are cut to maintain occupancy. Better properties, where operators have invested in maintaining and upgrading facilities, are more likely to have increased turnover despite the extra competition.

2. Changes from the last practice note

2.1 Market appraisal has been updated in line with economic and general market conditions.

3. Ratepayer discussions

3.1 There have been no ratepayer discussions in advance of preparing this Practice Note.

4. Valuation scheme

4.1 The majority will be valued based on local evidence/Tone/Scales/Sub locations. Any departure from RSA to the Licensed Property Application requires guidance from the Hotel CCT.

4.2 The approach will apply a price per Double Bed Unit (DBU). A DBU has an ensuite bath, or shower, and WC, and the basic scale assumes central heating. The DBU price, derived from rental evidence and consideration of accounts/receipts, will reflect the type (e.g. detached, terraced etc.) and class of guest house and its location (e.g. prime, good, fair, poor position). The DBU price will also reflect common areas such as residents’ lounge, dining room, bar (however see para 4.3 where there is significant trade to non-residents), and other normal ancillary accommodation.

4.3 If there is a bar, restaurant, or function room where there is significant non-resident trade, valuers must ensure that the valuation produced adequately reflects the additional income generated.

1. Market appraisal

1.1 The demand for guest house and bed and breakfast accommodation is largely driven by the numbers of domestic and international tourists and contractors travelling in the United Kingdom (UK). Hence occupancy and turnover are heavily influenced by factors which impact on decisions to travel to and within the UK.

1.2 The 12 months leading up to Antecedent Valuation Date (AVD), 1 April 2021, was dominated by the COVID19 pandemic. However, this market appraisal reflects the whole period since April 2015.

A. 2015 to 2019

1.3 Since 2015 the holiday accommodation industry generally experienced favourable market conditions. The increase in ‘staycations’ experienced during the last downturn was maintained, aided by exchange rate movements. This made the UK a cheaper destination for travellers from Europe and the USA in particular, whilst at the same time making foreign holidays more expensive for UK residents.

1.4 Online Travel Agencies (OTAs) and review websites increased their presence during this period. OTAs allow people to search for and compare guest houses and other holiday accommodation easily. However costs have increased following consolidation within the OTA sector. Review websites are also increasingly important, good reviews helping drive future business. However, one or two poor reviews can have a significant negative impact.

1.5 Over this period there was increased competition both from budget hotel operators, who have been expanding rapidly, and from hosting or sharing websites which significantly increased in popularity. Guest house operators sometimes had to reduce rates to remain competitive. This was particularly the case where operators had not invested in their property. Poorer guest houses often saw revenue decline as rates were cut to maintain occupancy. Better properties, where operators invested in maintaining and upgrading facilities, were more likely to have increased turnover despite the extra competition.

1.6 Various tourism promotion bodies produce reports and statistics on UK tourism and the holiday accommodation sector.

B. Impact of the COVID19 pandemic

1.7 The COVID19 pandemic had a major impact on guest houses in the period leading up to AVD (1 April 2021). Details of the various restrictions implemented by statute in response to the pandemic, and of the vaccination rollout, can be found online. In February 2021 the UK Government published its Roadmap out of lockdown for England which set out four steps to relax restrictions. Step 1 had already taken place by the AVD, although at that point hotels and guest houses were still only allowed to open for restricted categories of guests, e.g. key workers, people quarantining, people attending funerals etc.

1.8 The later three stages of the Roadmap for England included

- the opening of outdoor hospitality and self-contained accommodation, and outdoor dining (Step 2, no earlier than 12 April);

- the opening of remaining accommodation types including guest houses, subject to social distancing measures (Step 3, no earlier than 17 May); and

- the removal of remaining restrictions on openings/events (Step 4, no earlier than 21 June).

1.9 Subsequent to 1 April 2021 Steps 2 and 3 took place as planned, but Step 4 was delayed four weeks to 19 July.

1.10 The regulatory situation in Wales, both leading up to and after the AVD, was similar although not identical.

Performance in 2020

1.11 Reports show that this performance in the accommodation sector varied significantly between locations. Once allowed to open, hotels in rural and tourist locations benefitted from the increase in ‘staycations’ through summer and early autumn 2020.

C. Future prospects at AVD

1.12 Various reports and commentary on the hotel industry published in late-2020 and early-2021 set out views on the likely recovery of the sector in the context of what was known at the time, including the UK Government Roadmap for England which, as noted above, specified the earliest dates for which each stage of the lifting of restrictions would occur. At AVD it was expected that domestic leisure business would recover first, with domestic business travel and international leisure business recovering more slowly.

1.13 It was also expected that some costs might increase. In particular it was reported that the impact of leaving the EU on staffing would become more apparent as the UK recovered from the COVID pandemic.

2. Changes from the last practice note

2.1 Market appraisal has been updated in line with economic and general market conditions.

3. Ratepayer discussions

3.1 There have been no central discussions in relation to guest houses and bed and breakfast accommodation.

4. Valuation scheme

4.1 For the 2023 rating lists, the effects of the COVID-19 outbreak need to be taken into account as they would have been anticipated by the parties at the AVD. Accounts or trade evidence that include long periods of lockdowns are unlikely to provide good evidence of the fair maintainable trade (FMT) at the AVD. The reasonable efficient operator (REO) will take a view not only on the trade immediately achievable at AVD, but the trade over a period of time ahead, as they are assumed to be taking a tenancy with a reasonable prospect of continuance.

4.2 Guest and boarding houses will still be valued on schemes adopting a price per double bed unit, based on local evidence/tone/scales/sub-locations. Valuation schemes should reflect the expected level of trade, as outlined at paragraph 4.1 above, and the level of risk and uncertainty experienced at the AVD. Any departure from RSA to the Licensed Property Application (LPA) requires guidance from the Hotel CCT.

4.3 The approach will apply a price per Double Bed Unit (DBU) – see Rating Manual Part 3 Section 125 paragraph 8. A DBU has an en-suite bath, or shower, and WC, and the basic scale assumes central heating. The DBU price, derived from rental evidence and consideration of accounts/receipts, will reflect the type (e.g. detached, terraced etc) and class of guest house and its location (e.g. prime, good, fair, poor position). The DBU price will also reflect common areas such as residents’ lounge, dining room, bar (but see below if there is significant trade to non-residents), and other normal ancillary accommodation.

4.4 If there is a bar, restaurant or function room where there is significant non-resident trade, valuers must ensure that the valuation produced adequately reflects the additional income generated. In exceptional circumstances more than one valuation approach may need to be considered on the LPA. Reference should be made to the Rating Manual sections for Hotels, Public Houses and Restaurants as appropriate.

1. Market appraisal

The bed and breakfast association is the UK trade association for B&Bs and guest houses.

The Pink Book, produced by Visit England, is a guide to legislation relevant to accommodation providers in England. Attraction operators will also find legislation applicable to their business, such as regulations on hiring staff and health and safety.

According to the Bed & Breakfast Association the Bed and Breakfast sector consists of some 25,000 small owner-managed businesses generating £2.4 billion. This makes the sector 28% bigger than the ‘budget hotels’ sector and 35% of the size of the UK’s Hotel sector.

According to Visit England urban tourism is a significant growth area with the number of visits up by 2.9 million a year since 2006.

In 2013 British residents took 102 million overnight trips in England, totalling 297 million nights away with an average spend of £184 per trip.

Moreover, inbound tourism is said to be the fastest growing tourism sector with spend by international visitors forecast to grow by over 6% a year in comparison with domestic spending at just over 3%. So the value of inbound tourism is forecast to grow from over £21billion in 2013 to £57 billion by 2025.

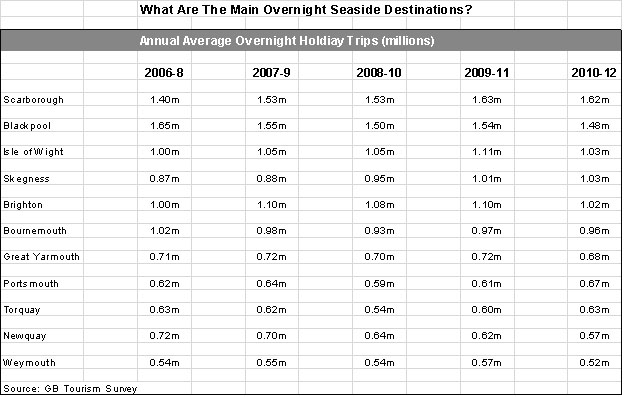

In 2012 there were 19.7 million seaside visits compared with 20.6 million seaside visits in 2006.

Trips to the seaside made up 31% (14.4 million) of the 46 million overnight domestic trips taken for holiday purposes in 2012. Almost half of overnight stays take place between July and September. The South West accounts for 40% of all domestic seaside trips which involve an overnight stay.

overnight seaside destinations

{kind=link}

The British bed and breakfast sector is set for a revival as there has been an increasing consumers ‘sense of localism and nationalism’ resulting in an increasing appetite for domestic experiences.

The conclusion is that the state of the industry is good and set for a revival both from the British residents’ appetite for short breaks/domestic experiences and the increase in inbound tourism.

2. Changes from 2010 practice note

For the 2010 Revaluation this class was valued using the Rating Support Application (RSA) except in certain cases (see below) when the Licensed Property Application (LPA) was used. The same approach should be adopted for 2017.

3. Ratepayer discussions

There have been no ratepayer discussions in advance of preparing this Practice Note.

4. Valuation scheme

The majority will be valued based on local evidence/Tone/ Scales/Sub locations. Any departure from RSA to the Licensed Property Application requires guidance from the Hotel CCT.

The approach will apply a price per Double Bed Unit (DBU). A DBU has an en-suite bath, or shower, and WC, and the basic scale assumes central heating. The DBU price, derived from rental evidence and consideration of accounts/receipts, will reflect the type (eg detached, terraced etc) and class of guest house and its location (e.g. prime, good, fair, poor position).The DBU price will also reflect common areas such as residents’ lounge, dining room, bar (but see below if there is significant trade to non-residents), and other normal ancillary accommodation.

If there is a bar, restaurant or function room where there is significant non-resident trade, valuers must ensure that the valuation produced adequately reflects the additional income generated.

In exceptional circumstances more than one valuation approach may need to be considered on the LPA. Reference should be made to the Rating Manual sections for Hotels, Public Houses and Restaurants.

If the premises are licenced for weddings and civil ceremonies then the Rating Manual section 6 part 3 - section 255.