Section 8

The Valuation Office's technical manual used to assess Capital Gains and other taxes.

8.1 The legislation

Relief from Capital Gains Tax on the disposal of a taxpayer’s private residence is provided under ss.222-226 TCGA 1992, as amended by subsequent Finance Acts.

8.2 The relief

S.222(1) of the TCGA 1992 provides relief for a gain realised by an individual in so far as it is attributable to the disposal of an interest in:

- ‘a dwelling-house’ or part of a dwelling-house which is, or has at any time in the taxpayer’s period of ownership been, his / her only or main residence, or

- land which the taxpayer has for his / her own occupation and enjoyment with that residence as its ‘garden or grounds’ up to the ‘permitted area’

S.222(3) and (4) of the TCGA 1992 provide that the ‘permitted area’ shall be 0.5 of a hectare or such larger area as is ‘required’ for the reasonable enjoyment of the dwelling-house as a residence, having regard to its size and character.

The 0.5-hectare permitted area referenced in s222(2) includes the site of the dwelling house.

8.3 Determining the permitted area and the amount of relief

To determine the permitted area it is necessary to go through the following five basic steps:

-

Determine the entity of ‘the dwelling-house’, that is, which buildings qualify for relief under Section 222 (1)(a). (See Part 2 of this Section). This is for HMRC to decide, with assistance from the Valuation Office caseworker.

-

Determine the extent of the ‘garden or grounds’, ie. which land occupied with the dwelling house can be described as garden or grounds (See Part 3 of this Section). This is for HMRC to decide, with assistance from the Valuation Office caseworker.

-

Determine the size of the permitted area, ie. if the ‘garden or grounds’ are in excess of 0.5 of a hectare how much of that land is ‘required’ for the reasonable enjoyment of the dwelling house as a residence (See Part 4 of this Section).

-

Determine the location of the permitted area, ie. which part of the garden or grounds would be the most suitable for occupation and enjoyment with the residence. (See Part 5 of this Section).

-

Apportion the proceeds of the disposal and the acquisition cost between the part of the property qualifying for relief and the remainder (See Part 6 of this Section).

These steps need to be followed in strict order avoiding the natural tendency to go straight to a conclusion at step 4. Problems sometimes arise by mixing up the ‘requirement’ test in step 3 with the ‘most suitable’ test in step 4. It is also particularly important to ensure that the HMRC has addressed steps 1 and 2 with larger estates where there may be cottages, stables or other outbuildings in addition to the main house.

8.20 General

HMRC will ask the Valuation Office to determine the extent and location of the permitted area where the garden and grounds of the residence exceed the statutory permitted area of 0.5 hectares set by s222(2) TCGA92 where there has been either:

- a disposal of the whole residence, together with its garden and grounds, and the owner contends that the permitted area should exceed the 0.5 hectare limit set by s222(2) TCGA92

- a disposal of part of the garden or grounds and the owner contends that some or all of that part falls within the permitted area

8.21 HMRC’s request for advice

In cases where the entity of the dwelling-house is not in dispute the HMRC caseworker will normally request an informal ‘not negotiated’ opinion of the permitted area. If on the information available the Valuation Office caseworker is able to accept the taxpayer’s permitted area then the HMRC caseworker should be advised accordingly and if any apportionments are required these may be provided on a not negotiated basis.

If on the information available, the Valuation Office is unable to accept the taxpayer’s permitted area then the case should be treated as a request for a formal ‘agreed’ opinion and the HMRC caseworker advised accordingly.

8.22 Information to be supplied to HMRC

HMRC’s instruction should contain details of the disposal, a plan, the tax computation, any valuation supplied by the taxpayer, a statement on HMRC’s view in respect of the entity of the dwelling house and the extent of the garden and grounds together with confirmation as to whether those aspects have been agreed by the taxpayer.

If this information is not supplied the Valuation Office should request that the HMRC caseworker provide it. In their response to the HMRC caseworker the Valuation Office should offer whatever additional information is readily available which may assist the HMRC in reaching a view. The case should be closed and re-opened when the information is provided.

8.23 Date at which the matter is to be considered

The Valuation Office caseworker should consider the size and location of the permitted area as at the date of the Taxpayer’s disposal. If there is a series of disposals, then it is necessary to go through the steps in paragraph 8.3 at each date.

HMRC may also request advice relating to the permitted area and required apportionments as at the date of the taxpayer’s acquisition of the property in order to calculate the chargeable gain.

8.30 Entity of dwelling-house

The first issue to be considered is the identification of the ‘dwelling-house’. This is a matter for the HMRC caseworker to determine. The Valuation Office caseworker may provide information to help the HMRC caseworker arrive at a decision.

This step in the process of determining the relief due is particularly important because:

- if a building is accepted as forming part of ‘the dwelling-house’ it must be included within the permitted area

- any buildings accepted as forming part of ‘the dwelling-house’ will have a bearing on its size and character, which should be taken into account when considering the permitted area that qualifies for relief under s.222(1)(b) TCGA 1992

Further practical guidance on cases where the entity of the dwelling is disputed can be found at 8.33. The information is intended to provide caseworkers with background knowledge necessary to gather facts and assist HMRC in arriving at their decision if required.

8.31 Staff accommodation

The definitive judgement is contained in the Court of Appeal decision in Lewis (HMIT) v Lady Rook (EGCS21 1992). Nevertheless, it is worthwhile reviewing the significant judicial decisions building up to this case.

Prior to the decision in the Court of Appeal in Batey (HMIT) v Wakefield (EG5 December 1981 p.1003; RVR January 1982 p.11), HMRC took the view that the ‘taxpayer’s residence’ for s.222 purposes normally comprised only the dwelling-house in which the taxpayer resided and that separate dwelling-houses in which domestic servants exclusively resided were not part of it.

However, in Batey in the High Court Mr Justice Brown Wilkinson said that a literal construction of the words ‘a dwelling-house’ in s.222(1)(a) which excluded properties which were themselves dwelling-houses would lead to unacceptable conclusions. A self-contained servant’s flat within the structure of the dwelling-house would be part of the dwelling-house. It followed that a staff house in the stable yard would also be included, and if that were so to put up another structure closely adjacent to the house to provide staff accommodation ought not to produce a different taxation consequence. The test to be applied was ‘what is the dwelling-house which is the taxpayer’s residence?’ and this may comprise a number of different buildings. The Court of Appeal also asserted that there is “no logical reason why a house which is physically quite separate should not form part of another residence or dwelling-house”.

The Revenue derived two tests from the decision in Batey:

- the second house had to be very closely adjacent to the principal house

- the occupation of the second house had the purpose of enhancing the taxpayer’s reasonable enjoyment of the principal house

In the High Court case of Markey (HMIT) v Sanders in February 1987, Mr Justice Walton specifically approved the two-test analysis but re-phrased the ‘very closely adjacent’ test so as to include the concept of the relative size and scale of the buildings. “What would be very closely adjacent were one dealing with the sale of No 7 Paradise Avenue, Hoxton might very well be quite different from what those words mean if one were considering the sale of Blenheim Palace”. He therefore reconsidered this test in terms of “Looking at the group of buildings as a whole, is it fairly possible to regard them as a single dwelling-house used as the taxpayer’s main residence?” On the facts of the case, he decided that the Commissioners had reached an unsupportable conclusion that a staff dwelling some 130 meters from the principal house comprised one entity with it and the Commissioners findings were reversed.

In June 1987 a further judgement was given in the High Court by Mr Justice Vinelott in Williams (HMIT) v Merrylees. He declined to support the two-test analysis of Batey and preferred a single approach: “What one is looking for is an entity which can be sensibly described as being a dwelling-house though split up into different buildings performing different functions”. He added that “of course the propinquity or otherwise of the buildings having regard to their scale is a very important factor to be weighed” but it must not be isolated as a factor of particular importance.

In February 1992 the Court of Appeal in Lewis (HMIT) v Lady Rook (EGCS21 1992) decided that it was necessary to identify an entity which can be sensibly described as a dwelling-house, though split up into different buildings performing different functions. In cases where there is an identifiable main house it was held that no building can form part of a dwelling-house with the main house unless that building is appurtenant to, and within the curtilage of, the main house.

In the Lady Rook case the C of A quoted from the Leasehold Reform Act case of Metheuen-Campbell v Walters:

“For one corporeal hereditament to fall within the curtilage of another, the former must be so intimately associated with the latter as to lead to the conclusion that the former in truth forms part and parcel of the latter”.

They also referred to the Court of Appeal decision in Dyer v Dorset County Council (1989) which emphasised the smallness of the area comprised in the curtilage. In the Lady Rook case the main house was a substantial 8 bedroom house/mansion set in 10.5 acres of land. The cottage was 175 metres from the house and separated by a large garden. The Court came to “the inescapable conclusion that the cottage was not within the curtilage of, and appurtenant to, Newlands, and so was not part of the entity”.

As a result of these decisions the HMRC’s instructions adopt a broad approach to the relevant factors. These include the distance between the houses, the nature and quality of the access between them, their respective situations, their relative sizes, and their history of combined ownership and occupation. These considerations will assist in determining whether or not the building is appurtenant to and within the curtilage of the main house.

8.32 Other outbuildings

In the light of the Lady Rook case, HMRC’s instructions no longer distinguish between the nature of different outbuildings. The test is whether the building is appurtenant to and within the curtilage of the main house. Curtilage is defined in the Shorter Oxford Dictionary as ‘a small courtyard, or piece of ground, attached to a dwelling-house and forming one enclosure with it’. Emphasis is placed on the smallness of the area. Buildings standing around a courtyard together with the main house will be within the curtilage of the main house.

The other main factor to be considered by HMRC is that in accordance with S.224(1) TCGA 1992, relief shall not apply to any part of the dwelling-house which is used exclusively for the purpose of a trade or business, or of a profession or vocation.

Where the Valuation Office caseworker is aware of any lettings or commercial activities at the property prior to the disposal, for example livery use of stables, they should advise HMRC as soon as possible.

8.33 Dispute over the entity of the dwelling

If the Valuation Office has any queries regarding the HMRC caseworker’s view on the entity of the dwelling-house or the information on which it is based, the HMRC Caseworker should be consulted before proceeding any further.

If the HMRC caseworker is unable to agree the entity of the dwelling-house with the taxpayer, the Valuation Office caseworker should base their opinion of the permitted area on the HMRC caseworker’s view but may in any negotiations explore the possibility of agreeing alternative permitted areas, without prejudice to the dispute over the entity. It should be remembered that providing an outbuilding is not excluded from being part of the dwelling-house by reason of its use, it may still qualify for relief if it falls within the Valuation Office’s permitted area (see Part 5). In such cases the fact that there is a dispute over whether or not an outbuilding forms part of the dwelling-house may be of no consequence from a valuation / tax payable perspective.

8.34 Relief for periods of letting

S.223B TCGA 1992 provides for some relief from Capital Gains Tax (CGT) on disposals made on or after 6 April 2020, where s.222 applies and a part of the dwelling-house has been let as residential accommodation, whilst the owner occupied the property as their only or main residence.

Where the disposal occurs before 6th April 2020, S.223(4) TCGA 1992 provides for some relief from CGT where a gain, to which s.222 applies, accrues to any individual and the dwelling-house in question or any part of it is or has at any time in the taxpayer’s period of ownership been wholly or partly let as residential accommodation.

In the case of Owen v Elliott (HMIT) the Court of Appeal held in April 1990 that rooms in a seaside guest house, although used mainly for short-term visits, were nevertheless let by the taxpayer as ‘residential accommodation’ within the relieving provisions of s.223(4) TCGA 1992.

The decision is based on the facts of the case as the taxpayers were found by the First Tier Tribunal (General Commissioners) to occupy the whole of the building together with their guests at certain times of the year.

HMRC may therefore seek the Valuation Office caseworker’s assistance as to the use/occupation by taxpayers in cases involving let residential accommodation, for example hotels and guest houses. Whether or not the relevant accommodation qualifies for relief is ultimately a matter for the HMRC to decide.

8.40 Introduction

Only land which is occupied by the taxpayer as ‘garden or grounds’ can qualify for relief under Section 222(1)(b) TCGA 1992. This issue must therefore be decided by HMRC before the Valuation Office caseworker considers the size and location of the permitted area.

Whether or not an area of land is occupied by the taxpayer as ‘garden or grounds’ is a question of fact and is for the HMRC to decide. The Valuation Office caseworker may provide assistance to enable HMRC to arrive at a decision.

This step in the process of determining the relief due is important because only if the site of the dwelling together with the ‘garden or grounds’ exceed 0.5 of a hectare can the permitted area exceed 0.5 of a hectare. For example, if a house and it’s land extends to 0.75 ha of land but only 0.25 ha of it is occupied by the house and ‘garden or grounds’ as the remaining land is used for a trade, then the permitted area will be restricted to 0.25ha. The Valuation Office caseworker cannot decide on the location of the permitted area until the land occupied as ‘garden or grounds’ has been identified because only land occupied as ‘garden or grounds’ can be included in the permitted area.

8.41 Meaning of ‘garden and grounds’

Garden and grounds are not defined in the statute but are taken to be any land occupied and enjoyed by the taxpayer with the dwelling and serving chiefly for ornament and recreation. The phrase ‘occupation and enjoyment’ in S.222(b) should be understood by reference to the legal meaning of the words used. ‘Occupation’ means possession of the land while ‘enjoyment’ means possession without contested claims from third parties.

Land used for agriculture, commercial woodland, trade or business purposes will not qualify as ‘gardens or grounds’.

Plots that are under construction for new residential or commercial building plots at the date of disposal will not constitute garden and grounds.

Paddocks and orchards may constitute ‘grounds’, provided that there is no commercial / agricultural use.

HMRC will not exclude land which is unused or overgrown at the date of sale but which traditionally has been part of the grounds of the residence.

To qualify for relief, gardens or grounds must be occupied and enjoyed with the house at the date of disposal.

Usually, the garden and grounds will be the land which surrounds the residence and is enclosed with it. Land which is separated from the residence by other land, which is not in the same ownership, will not normally be part of the garden and grounds of the residence.

However, if the facts show that land which is physically separated from the residence is naturally and traditionally the garden of the dwelling-house and it would normally be passed on as such on conveyance, the land may be classed as garden and grounds. For example, in some villages it is common for the garden to be across the street from the dwelling-house. This separation should not be regarded as a reason for denying relief if it can be shown that the land was naturally and traditionally the garden and grounds of that house.

Conversely, a keen gardener may buy a plot of land some distance from their dwelling-house because the dwelling-house itself may have an inadequate garden. Even though the plot of land may be fully cultivated and regarded as part of the garden by the owner, it will not qualify for relief.

8.42 House retained and part of garden and grounds disposed of

It is possible to retain a dwelling house and sell off part of the garden and grounds and benefit from Private Residence Relief on the disposal. In order to qualify for relief, the land disposed of must have been part of the garden and grounds of the dwelling house at the time of disposal and have been within the permitted area, as per Varty v Lynes 1976 (51TC419).

Conversely, where the house is sold before the grounds are disposed of, the latter can no longer be regarded as occupied with the house and will not qualify for relief (Varty v Lynes). Relief will not however be denied where at the time of disposal of the grounds, the taxpayer remains in occupation of the house (for example in the interval between exchange of contracts and completion of the sale of the house).

8.43 Dispute over the extent of garden or grounds

If the Valuation Office is of the opinion that any of the land claimed by the taxpayer to be part of the permitted area did not comprise ‘garden or grounds’ then the HMRC caseworker should be advised of the facts and requested to resolve the issue with the taxpayer.

If the HMRC caseworker is unable to agree the extent of the land that was occupied as ‘garden or grounds’ the Valuation Office caseworker should base their opinion of the permitted area on the HMRC Caseworker’s view. However, they may explore the possibility of agreeing alternative permitted areas during any negotiations, without prejudice to the dispute over the extent of the garden or grounds.

8.50 Introduction

There is no automatic entitlement to relief on the full area of land if that land is not the garden and grounds of the residence at the date of disposal. For example, if a person has a house and 2 hectares of land but of that land only 0.2 hectares forms the dwelling house and garden and grounds with the remainder being used for the purposes of a trade, relief only extends to the 0.2 hectares.

Conversely, if it is considered that the dwelling house requires less than 0.5 of a hectare of the land occupied as ‘garden or grounds’, s.222(3) TCGA 1992 provides that the permitted area should be 0.5 of a hectare. The permitted area can only be less than 0.5 of a hectare if the ‘garden or grounds’ is less than 0.5 of a hectare.

If the land occupied as ‘garden or grounds’ exceeds 0.5 of a hectare then it is necessary to decide whether the permitted area should be restricted to 0.5 of a hectare or whether a larger area is ‘required’ for the reasonable enjoyment of the dwelling as a residence, having regard to its size and character.

This is a question for Valuation Office caseworker to decide and advise HMRC accordingly.

8.51 Meaning of ‘permitted area’

The size of the ‘permitted area’ of garden or grounds which qualifies for relief is defined in s.222(2) and (3) TCGA 1992. It is either:

- an area, inclusive of the site of ‘the dwelling-house’, of 0.5 of a hectare

- where the area required for the reasonable enjoyment of the dwelling-house as a residence, having regard to the size and character of the dwelling-house, is larger than 0.5 of a hectare, that larger area shall be the permitted area

This should be strictly interpreted, for example where a house might be reasonably enjoyed with 0.5 of a hectare or less although more pleasantly enjoyed with 1 hectare, the ‘permitted area’ should be restricted to 0.5 of a hectare. Relief for areas in excess of 0.5 of a hectare should be regarded as exceptional and must be clearly justified as ‘required’ for the ‘reasonable enjoyment’ of the house as a residence, that is, not as the actual owner’s residence reflecting their preferences, but simply as a residence and by general standards prevailing at the date of disposal having regard to sales evidence.

8.52 Meaning of ‘required’

Judicial guidance on the meaning of ‘required’ can be taken from the case of Geoffrey Longson v Victor Baker (HMIT) — [2001] STC 6, which was determined by the Special Commissioner Mr Everett and, on appeal, by Justice Evans-Lombe of the High Court.

Justice Evans-Lombe equated ‘required’ as used in this statute with ‘necessary’. He also approved of Mr Everett taking guidance on the meaning of this word from the judgement of du Parcq J in the High Court (KBD) case of Re Newhill Compulsory Purchase Order 1937, Paynes Application [1938] 2 All ER 163. The Newhill case concerned an application to quash the compulsory purchase of an area of pastureland in the same ownership as a mansion house where Section 75 of the Housing Act 1936 provided:

“Nothing in this Act shall authorise the compulsory acquisition for the purposes of this part of this Act of any land, which at the date of the compulsory purchase order, forms part of any park, garden or pleasure ground or is otherwise required for the amenity or convenience of any house.”

In giving his judgement Mr Justice du Parcq said:

I call attention to the word ‘required’. The use of it raises a question of fact which is necessarily a difficult one. Again, I do not wish to repeat myself, but one has to remember that it is pleasant, and, one may say, both an amenity and a convenience, to have a good deal of open space round one’s house, but it does not follow that that open space is required for the amenity or the convenience of the house. ‘Required’, I think, in this section does not mean merely that the occupiers of the house would like to have it, or that they would miss it if they lost it, or that anyone proposing to buy the house would think less of the house without it than he would if it was preserved to it. ‘Required’ means, I suppose, that without it there will be such a substantial deprivation of amenities or convenience that a real injury will be done to the property owner, and a question like that is obviously a question of fact.

Clearly then the test of what ‘larger area is required for the reasonable enjoyment of it as a residence’ relates to ‘need’ or ‘necessity’ and is very far removed from what is merely ‘desirable’.

8.53 Objective Tests

The Valuation Office caseworker must be satisfied by objective tests that a substantial proportion of those likely to be in the market for the dwelling-house as a residence would require a minimum area of garden/grounds exceeding 0.5 of a hectare to be included with the residence and that any smaller area would substantially inhibit the reasonable enjoyment of the house as a residence.

An objective judgement must be made of the likely requirement of the typical person who would normally wish to live in a house of this size and character. No weight should be given to the special or individual requirements of the actual occupier insofar as they are not representative of, or consistent with, the market as a whole in relation to this residence. This is consistent with the decision of Mr Everett, the Special Commissioner in the Longson v Baker case, who said:

Accordingly, I am not permitted to take into account the particular requirements of the owner of the dwelling-house: it is the house to which I must look and not the wishes, desires or intentions of any particular owner of the house.

In considering the area ‘required’, the most obvious evidence to consider is the extent of the gardens/grounds enjoyed with houses of similar size and character in the locality at around the date of disposal. Evidence of sale prices is immaterial. Part of the character of a property is inevitably determined by its setting or locality and it is therefore important to consider only those properties, which are in the same or a similar locality. The extent of the locality will for this purpose depend upon the proximity of sufficient comparables to obtain a fair impression. It may be necessary to bear in mind:

-

that there is a general tendency towards smaller gardens because of development pressures coupled with, for example, local planning policies concerning density of development

-

that houses in urban localities are generally found to have smaller gardens/grounds than in rural localities.

It follows that houses which were built many years ago and/or are in districts which were once rural, but now more urban in nature, may no longer strictly require the area of garden/grounds which they retain. The lower end of the range of areas of garden/grounds occupied with comparable dwellings is evidence of requirement. Larger areas are often accounted for by historic reasons, or the owner’s preference. It should be sufficient to show that there are some closely comparable houses with 0.5 of a hectare or less. No value based test need be used.

8.54 Where stables form part of the entity of the dwelling

The case of Longson v Baker concerned a Grade 2 listed former farmhouse, where substantial brick and timber stables in a traditional courtyard setting were included as part of the entity of the dwelling. This together with 7.56 hectares of land was described as an equestrian estate and all the land was claimed to fall within the permitted area. The argument put forward on behalf of the taxpayer was that this was not just a house but a house with stabling and the extent of the stabling was such that its enjoyment required all the land to be included. On appeal it was contended by the taxpayer that the Commissioner had failed to take into account the equestrian aspect of the dwelling-house. In the High Court, Justice Evans-Lombe said that:

it is not objectively required, i.e. necessary, to keep horses at a house in order to enjoy it as a residence.

Thus the inclusion of stabling or equestrian facilities as part of the entity of the dwelling should not of itself give rise to the requirement for additional land on which to keep horses.

8.55 Inclusion of access

Where access to a public road would on the face of it require inclusion within the ‘permitted area’ of an undue area of land, other closer access possibilities should be considered, perhaps to another road. Where the residence enjoys an existing long access drive or, for example, is situated in an extreme corner of its land it could be argued that there is no need for the access to form part of the land required. If so, then an easement or right of way must be assumed to exist over the non-exempt access land and this should be considered in any apportionments. Often the effect of such an assumption will be the same as if the access land were included in the permitted area and caseworkers should adopt a pragmatic approach.

8.56 Approval for garden and grounds in excess of 2 HA

If Valuation Office caseworkers are considering agreeing a permitted area in excess of 2 hectares, they must first contact their Sector Leader or the Valuation Practise and Standards team to seek approval.

8.60 Introduction

If the Valuation Office caseworker decides that the ‘permitted area’ is less than the area occupied as ‘garden or grounds’, it is then necessary to identify on a plan exactly which part of the ‘garden or grounds’ should be taken to be the ‘permitted area’.

The location of the permitted area is a question for the Valuation Office caseworker to decide and advise the HMRC caseworker on. This step in the process of determining the relief is important because it may affect the valuation apportionments.

8.61 Identification of the most suitable location

S.222(4) TCGA 1992 provides that where only part of the garden or grounds qualifies for relief the part to be taken as the permitted area should be that which “if the remainder were separately occupied would be the most suitable for occupation and enjoyment with the residence”.

8.62 Features of the land

In identifying the ‘most suitable’ garden or grounds, consideration should be given to existing features such as the lie of the land, mature trees but the location of the permitted area should not be inhibited by the position of, for example, existing paths, gates, fences. A new layout of the notional grounds may be envisaged. It does not necessarily follow that the part of the garden/grounds which have actually been sold cannot prior to sale form part of the ‘required’ or ‘most suitable’ area since commercial motives or financial necessity might well have outweighed the resulting loss in enjoyment of the residence.

In choosing the most suitable garden or grounds, no undue concern should be given to odd parcels of land falling outside the permitted area that may appear to become land-locked or unusable. This is not important as the test solely has regard to the enjoyment of the residence itself and does not relate to financial or other considerations.

8.63 Buildings on the land

Buildings which form part of the entity of the dwelling-house must be included within the ‘permitted area’ identified on the plan. Similarly, the sites of buildings which do not qualify for relief by reason of their use or occupation must be excluded from the ‘permitted area’. It is desirable for the boundaries of the most suitable location to be drawn so that islands where there is no relief within the most suitable location do not arise. It is however recognised that this will not always be possible. Outbuildings which are not excluded from relief by reason of their use or occupation but do not actually form part of the entity of the dwelling-house will qualify for relief if they are sited on the land identified as being the permitted area. The presence of any such buildings may be considered in deciding which part of the garden or grounds are the most suitable.

8.64 Adjustments to the size of the permitted area

Caseworkers should take care to identify the size of the permitted area prior to and separately from considering the most suitable location of the ‘permitted area’.

However, once the Valuation Office caseworker has determined the size and in general terms the location, marginal adjustments to the size of the permitted area may be made in order to produce a reasonable result.

8.70 Statutory requirements

Apportionment of values or of the actual consideration may be required for several purposes in connection with taxation and are specifically provided for in Private Residence Relief cases by s.222(10) TCGA 1992. Apportionments should be in accordance with the requirement in s.52(4) TCGA 1992, i.e. they should be ‘just and reasonable’.

8.71 Interpretation of the ‘just and reasonable’ method

No particular ‘just and reasonable’ method of apportionment is laid down, but the object should be to arrive at the contribution which each part makes to the sum to be apportioned, whether that sum is open market value as determined by the Valuation Office, or actual sale consideration in an arm’s length transaction.

Apportionment by area will only be appropriate where value is evenly spread throughout the land, as was stated in Salts v Battersby 2KBJ155 (1910). This case dealt with the method of apportioning rent and Darling J stated that the correct approach was by value, not area:

“It seems to me to be clear from the authorities that what you have to regard is not the bare acreage of the severed portions of the land demised, but their relative values…. You find the same principle running through them all…. The county court judge was of opinion that the proper way to apportion the rent was to have regard to the yardage and the yardage alone. Therein I think he was wrong. If it be shown that the land is of equal value throughout, no doubt the apportionment must be on the basis of yardage. But yardage cannot be a sufficient test of the relative value by itself, and here, so far from there being evidence that the land was of equal value throughout, the evidence was the other way….”

The Salts case makes clear that apportionment may often be by reference to the relative value of the constituent parts and that in cases where the value of the land runs evenly throughout the sum to be apportioned (whether market value or an actual sale price) an area-based apportionment will usually be appropriate. An example of a situation where an area-based apportionment may be appropriate might be where the development proposals are for the main residence to be demolished and value runs evenly across both the land qualifying and not qualifying for private residence relief. See section 8.74 for further context. In all other cases it will normally be necessary to find the constituent relative values of the parts to the apportionment following the provisions set out in 8.72.

8.72 Approach to valuations of constituent parts for apportionment purposes

The approach to valuations of constituent parts for apportionment purposes should normally be open market value as applied in other taxation contexts, subject to the following exceptions. These exceptions are required in order to produce a consistent result given we are seeking a just and reasonable apportionment of the market value or sale price of a property as a whole.

The exceptions in this section aim to reflect a situation where hypothetical vendors of each part act in concert for the sale of the whole rather than maximising one part to the detriment of the other.

In addition, the value of the parts should reflect any marriage value inherent to the land as a whole (see section 8.77).

Consistency of access and provision of access

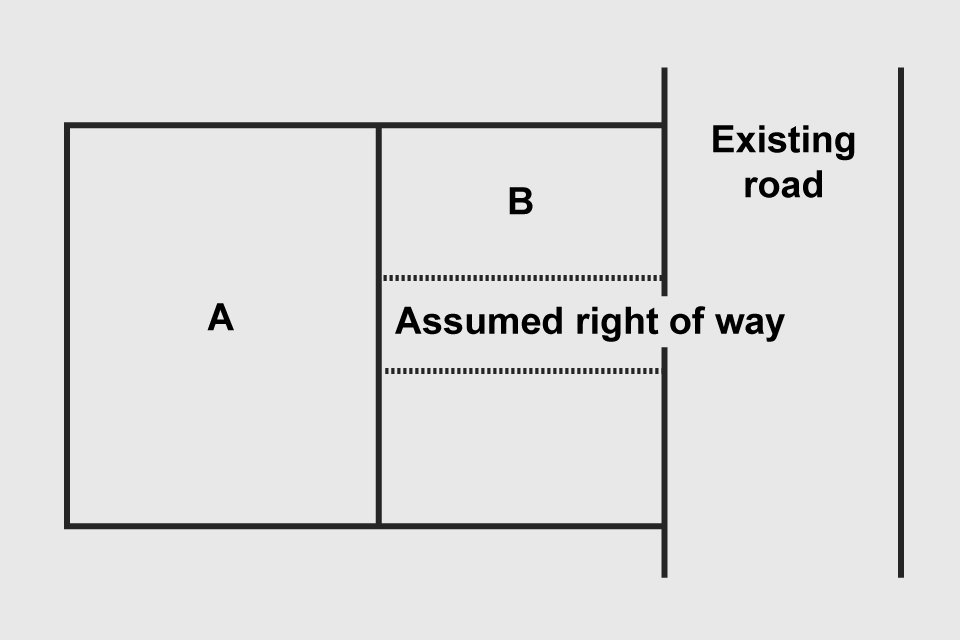

Example 1 — an area of apportioned land that has no existing road access

Area A does not have access to an existing road.

Area A shares a boundary with area B. Area B has access to an existing road.

It is assumed there is right of way to area A going through area B. This right of way allows area A to access the existing road.

Where one apportioned part of the whole land has no existing access, its constituent value should usually be found assuming a right of way across the other parts. In example 1, where the values of areas A and B are to be apportioned, the constituent value for the landlocked area A should be arrived at assuming a right of way across area B.

Consistency of layout

Where the sum to be apportioned (whether market value or an actual sale price) reflects development potential across all parts, the constituent valuation of those parts must be found assuming a consistent layout where appropriate. In example 1, if areas A and B benefit from planning permission for residential redevelopment it would be inconsistent to arrive at a higher constituent value for B by assuming development along the existing road frontage without allowing for the assumed access to landlocked area A. Site specific constraints for example flood risk could mean that in practise a proposed site layout in terms of development densities is inconsistent. It may be appropriate to take such factors into account when considering the values of those respective parts.

Consistency of type of development

Where the sum to be apportioned reflects a particular type of development, for example residential redevelopment, across the entire area. The valuations of the constituent parts should be found assuming a consistent type of development. In example 1, if the market value (or sale price) of the whole reflects residential development potential across both A and B, it follows that the constituent values of both parts A and B should also reflect that residential development potential. Any alternative, lower value development potential, say industrial, on area B should be disregarded as this would be unlikely to result in a just and reasonable apportionment.

If the Market Value or actual sales price itself reflects a mixture of different types of development, then it follows that constituent valuations of the parts should reflect those differences. In example 1, if area A benefit from planning permission for residential development whilst area B benefits from permission for industrial use then a just and reasonable apportionment of the constituent parts should generally reflect those circumstances.

8.73 Ransom value cases

Where it is necessary to apportion a sum which reflects overall development potential then an area-based apportionment will usually be appropriate. Valuation Office caseworkers should not attribute any ‘ransom value’ to part of a site because this could only arise if the land were valued as if it were a separate entity in different ownership from the rest of the site. The introduction of ransom value would not result in a just and reasonable apportionment. In example 1, it would not be appropriate to reduce the value of parcel A given it is landlocked by parcel B as both parcels were in the same ownership as at the date of disposal.

Example 2 — private residence within or connected to an area used for business

Area A is a piece of land used for business purposes as a plant nursery.

Area A contains area B, which a house the business owner lives in.

Area B contains area C, which is the private garden attached to the house.

Areas B and C qualify for Private Residence Relief.

Area A is sold for development together with area C which formed part of the garden of B but was included in the sale together with area A to provide an access visibility splay necessary for redevelopment. A separate, standalone valuation of C would normally reflect its ‘ransom value’ and a separate valuation of A would reflect the necessity to acquire C through negotiation. However, the ‘ransom value’ of C only exists if it is valued on the assumption that it is in different ownership from A. As A and C are all essential parts of the redevelopment scheme, an area-based apportionment is considered to be just and reasonable. It would not be appropriate to ascribe a value to area C that reflected the ransom value to the detriment of area B.

8.74 Where a private residence is to be demolished and garden and grounds or other land to be apportioned forms part of a site intended for redevelopment

Valuers should exercise caution when apportioning sales of residential property that will be demolished as part of a redevelopment scheme following sale.

Where it is necessary to apportion a sum which reflects overall development potential, then an area-based apportionment will likely be appropriate. In such cases, the sales price is driven by the purchaser’s valuation appraisal / residual methodology. If the whole site is to be developed and the lots are evenly spread across the site then a pro rata area apportionment may be appropriate and will not offend Salts v Battersby 2KBJ155 (1910).

A more considered apportionment may be required based on the development proposals having regard to site specific factors. For example, having regard to example 1 area B can be developed whilst area A cannot due to flood risk resulting in a planning permission that is not uniform across the site, the valuation of the constituent parts may need to reflect those relevant facts. Valuers should consider relevant statutory planning requirements where appropriate for example the necessity for Public Open Space or on-site Biodiversity Net Gain may mean that land not intended for development is an integral part of the development and should be valued as such.

Where the garden and grounds are to be redeveloped Valuation Office caseworkers should avoid calculating the existing use value of the constituent parts and apportioning the remainder of the market value or sales price based on those relativities as this does not provide a just and reasonable apportionment. Valuation Office caseworkers should contact the Valuation Practice and Standards Team for further advice if taxpayers or their representatives adopt such an approach.

8.75 Land sold for development but house retained

If the house and permitted area are to be retained and land outside the permitted area is to be developed, each constituent part can be valued having regard to the Market Values. For the house and garden / grounds, that will involve valuing the property having regard to its existing use whilst the land would likely be valued reflecting the development potential associated with it.

Valuation Office caseworkers should refer to section 8.76 for guidance on building plots that bisect areas both inside and outside the permitted area.

8.76 Bisected plots and buildings

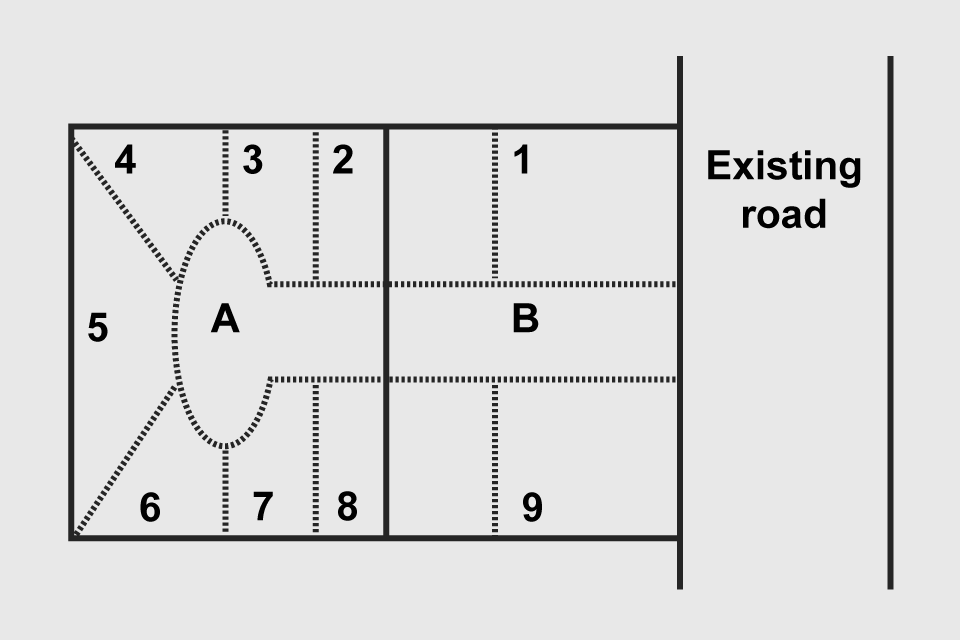

Example 3 — bisected plots of land

Area A shares a boundary with area B. Area B connects to an existing road. Area A does not connect to the existing road, but can access the existing road through area B.

Areas A and B contain plots 1 to 9.

Plots 1 and 9 are in area B.

Plots 3, 4, 5, 6 and 7 are in area A.

Plots 2 and 8 are bisected by the boundary between area A and area B so fall within both areas.

The boundary between parts of land to be apportioned may bisect plots or buildings. The constituent valuations for apportionment of the whole may have to be preceded by apportionments of the bisected parts. In example 3, where plots 2 and 8 are bisected, the Valuation Office should firstly arrive at separate valuations of these plots alone and then apportion those valuations between the parts falling within areas A and B. The apportioned values of the bisected plots should then be added to the constituent values of the remainders of areas A and B to arrive at an apportionment of the whole area.

8.77 Marriage value and apportionments

The individual values of the constituent parts may not always equal the value of the whole due to marriage value / synergistic value. In Private Residence Relief cases, marriage value may exist due to a property being a small holding or a country estate. The value of the property and land together could exceed standalone values of those parts. In such cases it will be necessary to apportion thus:

Open market value or sale price to be apportioned × (Constituent value of part ÷ sum of constituent values of all parts)

For example:

Bungalow and 2 HA sold for £500,000.

Constituent value of bungalow and permitted area of 0.5 HA £400,000 (A)

Constituent value of 1.5 HA £50,000 (B)

Total value of constituent parts £450,000

Marriage value / synergistic value £50,000 (£500,000 less £450,000)

A just and reasonable apportionment using the A over A+B formula from s42 TCGA92 will naturally apportion the £50,000 marriage value between the house and land as shown in this example:

1: Amount of sales price allocated to land:

£500,000 sales price ÷ (£50,000 constituent value land ÷ £450,000 total value of constituent parts) = 0.11

£500,000 × 0.11 provides £55,000 to land (B).

2: Amount of sales price allocated to house:

£500,000 ÷ (£400,000 constituent value house ÷ £450,000 total value of constituent parts) = 0.89

£500,000 × 0.89 provides £445,000 to house (A)

Note the figures have been rounded to 2 decimal places.