Civil Justice Statistics Quarterly: October to December 2021

Published 3 March 2022

© Crown copyright 2022

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/statistics/civil-justice-statistics-quarterly-october-to-december-2021/civil-justice-statistics-quarterly-october-to-december-2021

1. Main Points

| Covid-19 and associated actions are still having an impact on all civil actions | This quarter, civil justice actions remain below pre-Covid-19 levels. Following the marked recovery seen as a result of the impact of measures undertaken by the courts, volumes of all actions have stabilised in recent quarters. This publication will therefore focus largely on comparisons with the same quarter two years ago (as a pre-Covid-19 baseline). |

| Decrease in County Court claims driven by money claims and possession claims | In October to December 2021, County Court claims were down 21% on the same period in 2019, to 379,000. Of these, 309,000 (82%) were money claims (down 20%). Compared to the same quarter in 2020, County Court claims were down 5%. |

| Damages claims were up 2% at 31,000 | The increase in damages claims was driven by an uptick in Other damages claims (up 262% to 12,000) compared to the same quarter in 2019. This was offset by Personal Injury claims (down 30% to 19,000). Compared to the same quarter in 2020, total damages claims have fallen (down 2%). |

| The number of claims defended and number of trials is lower than 2019 | There were 65,000 claims defended (down 11%) and 12,000 claims that went to trial in October to December 2021 (down 29% compared to the same quarter in 2019). Compared to the same quarter in 2020, claims defended were down 5% and claims that went to trial decreased by 9%. |

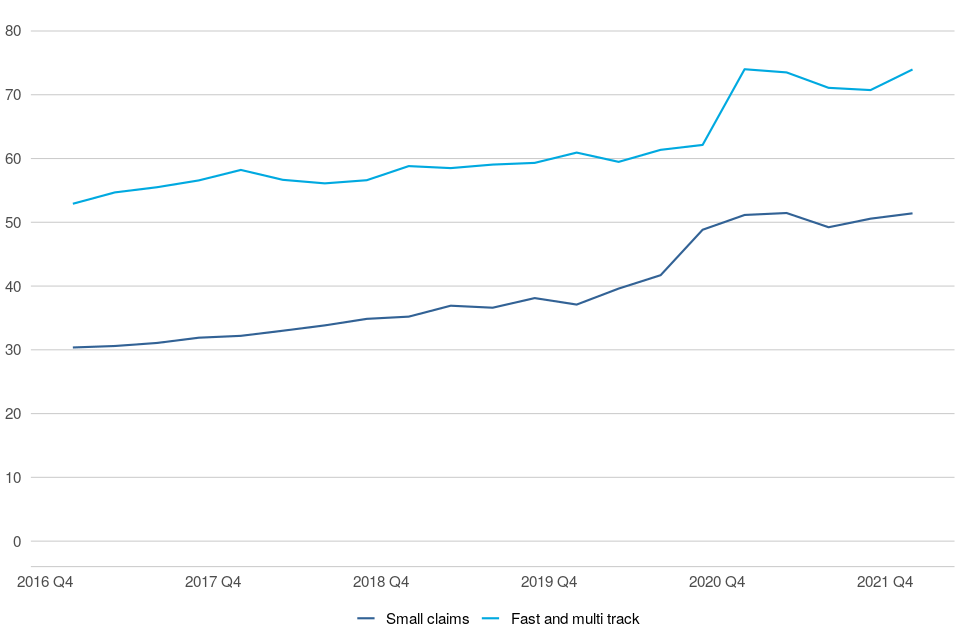

| Mean time taken from claim to hearing has increased | The mean time taken for small claims and multi/fast track claims to go to trial was 51.4 weeks and 74.0 weeks, 14.3 weeks longer and 13.0 weeks longer than the same period in 2019 respectively. These measures were 0.3 weeks longer for small claims compared to the same quarter in 2020 and the same as in this period for multi/fast track claims. |

| Judgments were down 32% and default judgments were down 31% | Judgments were down 32% (to 214,000) in October to December 2021, compared to the same period in 2019; with 90% of these being default judgments. Compared to the same period in 2020, judgments were down 3%. |

| 14,000 enforcement applications and 9,100 enforcement orders made | Enforcement applications were down 47% while enforcement orders were down 45% when compared to the same quarter in 2019. Compared to 2020, enforcement applications were down 11% while enforcement orders were down 1%. |

| 69,000 warrants were issued | Warrants issued were up 2% when compared to the same quarter in 2019 and up 103% compared to 2020. |

| 2,300 judicial review applications in 2021 | There were 2,300 applications for Judicial Reviews in 2021, down 18% on 2020 (here we are only comparing to 2020 as JR cases were not significantly impacted by Covid-19). Of the 1,300 cases in 2021 that reached the permission stage, 191 (15%) were found to be ‘totally without merit’. There were 570 applications for Judicial Reviews in Q4 2021, down 15% on Q4 2020 |

This publication gives civil county court statistics for the latest quarter (October to December 2021), compared to the same quarter in 2019 (pre-Covid19). Should users wish to compare latest outturn against 2020, they can do so using the accompanying statistical tables. The judicial review figures cover the period up to October to December 2021, and this quarter also includes data on privacy injunctions considered during the second half of 2021. For more details, please see the supporting document.

Statistics on the Business and Property Court for England and Wales have also been published alongside this quarterly bulletin as Official Statistics. For technical detail, please refer to the accompanying support document.

For general feedback related to the content of this publication, please contact us at: CAJS@justice.gov.uk

2. Statistician’s comment

Volumes across most Civil Justice actions remained relatively stable during 2021 following recovery from the impact of Covid-19 in the first half of 2020, although numbers remain below pre-Covid-19 levels. We continue to compare the data from this quarter with the equivalent quarter in 2019 (as a pre-Covid-19 baseline) for a more meaningful assessment of trends and performance and a better measure of how the civil process “returns to normal”. We expect to return to the usual practice for 2022 data. Should users wish to compare latest outturn against 2020, they can do so using the accompanying statistical tables.

There has been a decrease in volumes for most civil actions in Q4 2021 compared to the previous quarter, driven by seasonal effects resulting in a reduction in bulk users and processing completed in December. This trend is repeated in previous years but was not evident in 2020 due to the recovery seen over this period.

The recovery noted in the second half of 2020 has slowed in most areas across civil justice in 2021. Recovery in the volume of claims defended has also slowed, yet this remains an area where recovery is most evident with volumes just 11% lower than the equivalent 2019 quarter (pre-Covid). The mean time taken from claim to hearing remains significantly negatively impacted by Covid-19, although these measures have remained relatively stable in recent quarters.

Despite a dip in Q4 2021 due to seasonal trends, total claim volumes remained relatively stable during 2021, yet the number of “other” damages claims remain considerably above previous years (up 262% on the 2019 comparator and 68% on the same quarter in 2020). As noted previously, this increase is as a result of PPI-related claims that rely on a section of the Consumer Credit Act that relates to unfair relationships and follows a series of court rulings on the matter. Possession claims have also continued to increase, following the end of stays in possession actions in England (31st May) and Wales (30th June); however, these remain 46% below levels in the same quarter of 2019.

Looking ahead, as Covid-19 restrictions have come to an end, claim volumes are likely to return to historic trend levels over time but we expect timeliness measures to remain impacted for some time. As timeliness measures are taken from the initial claim date, data for the next few quarters is likely to continue to include some cases issued before or during the early stages of the pandemic. Measures implemented following the pandemic, such as the opening of Covid-secure courtrooms and the increase in hearings by remote means, will have benefited later cases and as such contributed to timeliness measures remaining stable during 2021 and not increasing further.

3. Claims Summary

County court claims were down 21% on the same quarter of 2019, driven by money claims and possession claims.

There were 379,000 County Court claims lodged in October to December 2021. Of these, 340,000 were money and damages claims (down 18% from October to December 2019).

Non-money claim volumes were at 39,000, down 37% when compared to the same quarter in 2019.

Mortgage and landlord possession claims were down 46% over the same period to 17,000, ‘other non-money claims’ were down 28% to 20,000 and claims for return of goods were down 7% to 2,300.

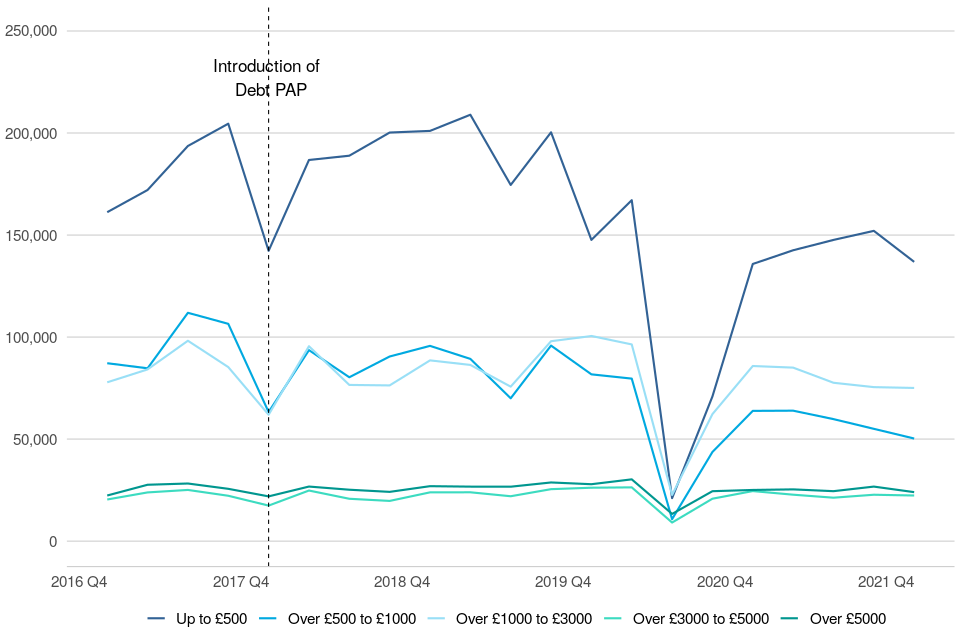

Figure 1: County Court claims by type, Q4 (October to December) 2016 to Q4 (October to December) 2021 (Source: table 1.2)

In the most recent quarter, total claims were down 21% compared to the same period in 2019 (from 477,000 to 379,000). Of these, 340,000 were money claims, down 18% from October to December 2019 (from 415,000). Money and damages claims made up 90% of all claims in October to December 2021, up 3pp on its share in October to December 2019.

Prior to the sharp fall in 2020, County Court claims had been generally increasing from 2015, reaching a peak of 565,000 claims in April to June 2017. This increase was driven by a rise in money claims, which make up the majority of claims received. Prior to 2020, claim volumes had been relatively unchanged but volatile, driven by a few “bulk issuers” slowing down and then ramping up their volume of claims. Claim volumes decreased significantly following the outbreak of Covid-19, with volumes this quarter remaining relatively stable after initial recovery towards pre-pandemic levels in the second half of 2020.

Non-money claims have been generally decreasing since 2015. While these showed less of an impact following Covid-19 in contrast to money and damages claims, the recovery to pre-Covid volumes has been slow. In the current quarter, these claims were down 37% (from 62,000 to 39,000) compared to the same period in 2019.

Within non-money claims, ‘other’ non-money claims have shown a decline since 2018. In the most recent quarter, these were down 28% (from 28,000 to 20,000) compared to the same period in 2019.

The overall trend in Mortgage and Landlord Possession claims has been decreasing since a peak of 60,000 in January to March 2014. There were 17,000 claims in October to December 2021, down 46% compared to the same quarter of 2019 (32,000 claims). This decrease has been driven by a fall in all claims types since March 2020 due to actions following Covid19. Further details can be found in the Mortgage and Landlord Possessions publication annex here.

Claims for return of goods increased steadily to a high of over 3,000 in July-September 2018, with this trend stabilising in recent quarters. This quarter, as for other claim types, claims for return of goods were down 7% (from 2,500 to 2,300) in October to December 2021 compared to the same period in 2019.

4. Money Claims[footnote 1]

Money claims were down 20% (to 309,000 claims) in October to December 2021 compared to the same quarter in 2019, driving the overall trend in money and damages claims.

Money claims of up to (and including) £1,000 were down 18% over this period to 187,000, driving the overall trend in money claims.

Damages claims were up 2% at 31,000, driven solely by a rise in Other - damages claims (up 262% to 12,000) compared to the same quarter in 2019.

Personal Injury claims accounted for 61% of all damages claims in the most recent quarter, down 28pp on October to December 2019, when they accounted for 89% of all claims.

Figure 2: Money claims by monetary value, Q4 (October to December) 2016 to Q4 (October to December) 2021 (Source: civil workload CSV[footnote 2])

Historically, money claims reached a peak in October to December 2017, at which point the implementation of the Pre-Action Protocol (PAP) for Debt Claims in October 2017 led to a sharp drop in claims. An increasing trend resumed the following quarter, suggesting that the impact of the PAP on claim volumes was temporary. The main aim of the protocol is to encourage early engagement between parties to resolve disputes without needing to start court proceedings. In the most recent quarter (October to December 2021), there were 309,000 claims, down 20% on the same quarter in 2019 (384,000 claims).

This quarter, the majority (83%) of money claims were processed and issued at the County Court Business Centre (CCBC). There were 257,000 such claims at the CCBC in October to December 2021 (down 19% on the same quarter in 2019). CCBC claims have been particularly affected by Covid-19 and associated actions, with a more significant decrease than other money claims, but they have now returned to historic trend levels. For comparison, they also made up 83% of money claims in October to December 2019. This is as a result of bulk issuers almost completely ceasing their issue during the immediate response to the pandemic and now increasing these volumes.

The change in money claims is driven by lower value claims (under £1,000). These were down 18% to 187,000 claims in the period October to December 2021, compared to 2019, and account for 61% of total money claims in the most recent quarter. This is a return to historical levels following the previously noted significant decline, with this category making up 60% of total money claims in October to December 2019. When compared to the same quarter in the previous year, the next claim band (above £1,000 up to and including £3,000) was initially similarly affected but has now returned to around historic levels with 75,000 claims. As a result, this value bracket made up 24% of total money claims in the most recent quarter, similar to its share in October to December 2019 (26%).

Other than Q2 2020, damages claims have fluctuated between 30,000 and 40,000 claims each quarter over the last five years (since October to December 2016). More recently, the volumes were up 2% in October to December 2021 compared to the same period in 2019 (at around 30,000). This was driven by an increase in other damages claims, up 262% from 3,300 to 12,000; this is at its highest level since quarter 1 of 2012 (when there were 14,000 claims). That increase was offset by a fall in personal injury claims, down 30% compared to the same period in 2019 (from 27,000 to 19,000). The increase in other damages claims is a result of PPI-related claims that rely on a section of the Consumer Credit Act that relates to unfair relationships and follows a series of court rulings on the same matter. As the increase has been maintained for a few quarters, we intend to provide further analysis on this case type in the next few quarters.

4.1 County court claims by month and 5-year average[footnote 3]

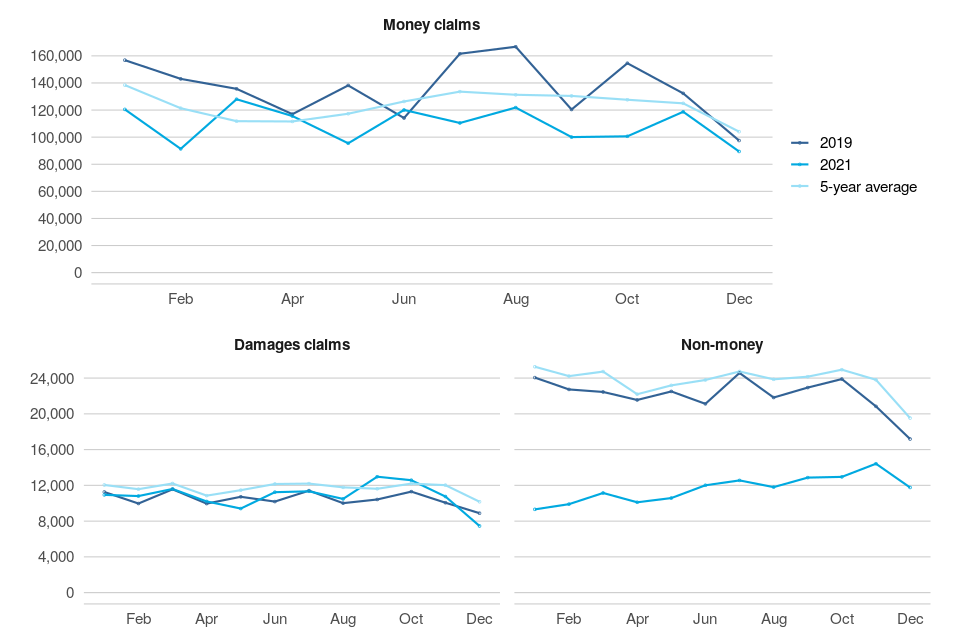

Claims for quarters 1 to 4 of 2021 – which cover the second peak Covid-19 period, have been shown by month (figure 3) to further examine the impact and recovery from the pandemic and related actions on claim volumes in county courts over this period.

Figure 3: Monthly county court claims by type, 2019, January to December 2021, and 5-year average (2015-2019)

Money claims initially fell steeply in March 2020 (down 29% on 2019 - not shown in figure 3), coinciding with wide-scale closure of courts[footnote 4] across England and Wales as a result of Covid-19, and many bulk claim issuers “pausing” new claims following guidance from the FCA[footnote 5]. This was followed by further falls in April and May 2020 with just 21,000 and 22,000 claims respectively (down more than 70% on the five-year average in both cases).

The first significant uptick was seen in June 2020, and this continued into Q3 of 2020 with 55,000, 63,000 and 104,000 claims in July, August and September respectively (not shown in figure 3). Monthly money claim volumes have remained relatively stable in 2021 yet with levels generally remaining below both the 5-year average and 2019 levels. The latest three months (101,000, 119,000 and 89,000 claims respectively) have continued this trend. Claims in November 2021 were down 5% on the 5-year average and down 10% on volumes seen in 2019. The dip in money claims volumes in December is likely to be due to seasonal trends driven by bulk users and a reduction in processing over this period.

Damages claim volumes did not see such a significant decline; at the lowest point this reached 4,800 claims in April 2020, down 56% on the five-year average (not shown in figure 3). A partial recovery to pre-Covid levels had commenced by June 2020, with claim volumes only down 24% on the five-year average. The recovery reached levels consistent with previous years in August and September 2020 and this pattern has since continued (13,000, 11,000 and 7,500 claims for October, November and December 2021 respectively).

In contrast, non-money claim volumes had declined significantly by April 2020, reaching just 5,400 claims, down 76% on the five-year average. Following this, volumes rose slightly through May-July, reaching a high of 10,000 in July 2020, still down 59% on the five-year average. Claim volumes have generally continued to rise since then with 13,000, 14,000 and 12,000 claims respectively for October, November and December of 2021. December claim volumes were down 40% on the 5-year average and show no signs of returning to pre-Covid levels yet.

4.2 Allocations (table 1.3)

In October to December 2021, 32,000 money and damages claims were allocated to track, down 34% (from 49,000) on the same period in 2019. A decrease was seen across all tracks. Compared to October to December 2019, of these allocations:

- 20,000 were allocated to small claims, down 32% on October to December 2019. This accounts for 63% of all allocations (compared to 61% of all allocations in the same quarter of 2019);

- 9,700 were allocated to fast track, down 38% on October to December 2019. This accounts for 30% of all allocations (compared to 32% of all allocations in the same quarter of 2019);

- 2,100 were allocated to multi-track, down 33% on October to December 2019. This accounts for 7% of all allocations (compared to 6% of all allocations in the same quarter of 2019);

5. Defences (including legal representation) and Trials

The number of claims defended was down 11% to 65,000 compared to the same quarter in 2019.

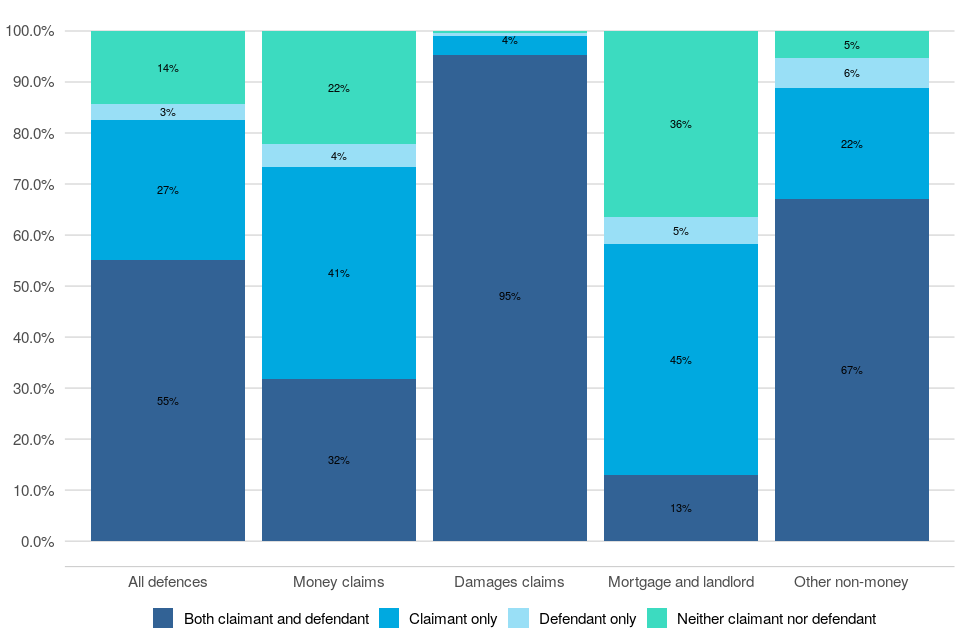

Of those claims defended, 55% had legal representation for both claimant and defendant, 27% had representation for claimant only, and 3% for defendant only.

The number of trials was down 29% to 12,000 compared to the same quarter in 2019

Average time taken for small claims was 51.4 weeks (14.3 weeks longer compared to the same quarter in 2019) and for multi and fast track claims it was 74.0 weeks (13.0 weeks longer than October to December in 2019).

Of those claims defended in October to December 2021, 55% had legal representation for both claimant and defendant, 27% had representation for claimant only, and 3% for defendant only. Almost all (95%) damages claim defences had legal representation for both the defendant and claimant, compared with 32% of money claim defences.

Figure 4: Proportion of civil defences and legal representation status, October to December 2021 (Source: table 1.6)

The total number of claims defended was down 11% in October to December 2021 compared to the same quarter in 2019, from 73,000 to 65,000 cases. This was driven by decreases across all claim types, with the most significant impact from defended money claims (down 13% from 44,000 to 38,000). However, it should be noted that this is less than the fall in money claims issued (down 20%).

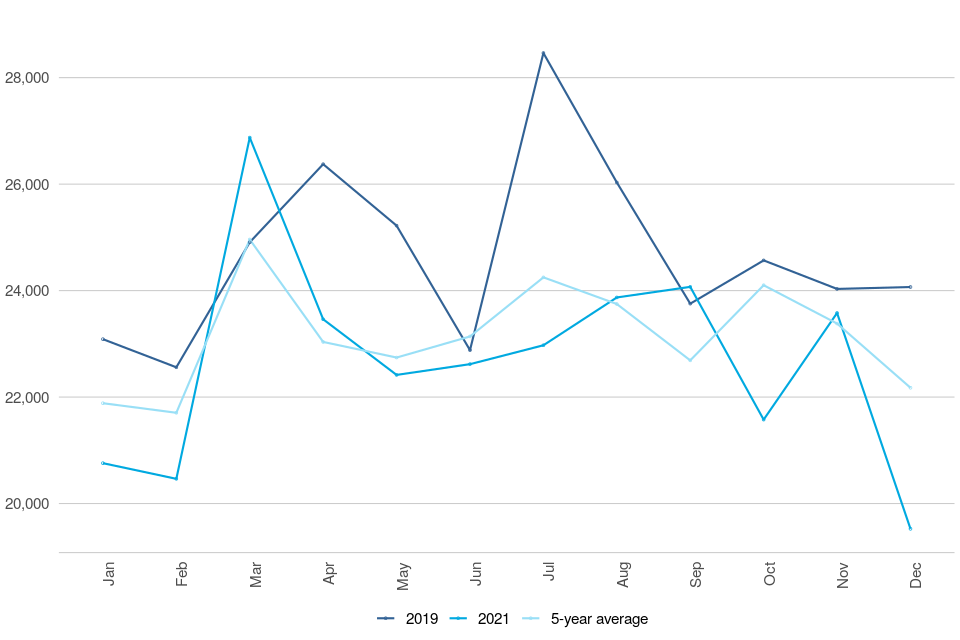

Figure 5: Monthly county court claims defended, 2019, January to December 2021, and 5-year average[footnote 3]:

As with total claims, the monthly breakdown of claims defended in figure 5 showed variance throughout the last year. Due to the time taken from claim to defence, the initial decline in defence volumes was not seen until April 2020, where claims defended were down to 19,000, followed by a more significant fall in May 2020 to 12,000 defences. Defence volumes then showed a steady recovery through June and July 2020 (14,000 and 17,000 defences respectively). These continued to rise, with September 2020 volumes (25,000 defended claims) being up 9% on the 5-year average, as well as up 4% on the higher volumes seen in 2019.

This recovery continued in Q4 2020 and has remained relatively stable since Q2 2021. Monthly figures for October and November (22,000and 24,000 defended claims respectively) showed a continued return to pre-Covid levels. Whilst monthly data is more volatile, November was stable compared to the 5-year average and down 2% on volumes seen in 2019. On the contrary defence volumes in December were 20,000, down 12% compared to the 5-year average. This fall is likely to be due to seasonal trends and a reduction in processing over this period.

5.1 Trials and Time Taken to Reach Trial (table 1.5)

Defended cases which are not settled or withdrawn, generally result in a trial. In total, there were 12,000 trials in October to December 2021, down 29% compared to the same period in 2019. Of the claims that went to trial, 8,400 (71%) were small claims trials (down 33% compared to the same quarter in 2019) and 3,400 (29%) were fast and multi-track trials (down 18% from the same quarter of 2019).

Figure 6: Average number of weeks from claim being issued to initial hearing date, Q4 (October to December) 2016 to Q4 (October to December) 2021 (Source: table 1.5)

In October to December 2021, it took an average of 51.4 weeks between a small claim being issued and the claim going to trial, 14.3 weeks longer than the same period in 2019.

Small Claims were impacted sooner than Fast and Multitrack claims by Covid-19, in terms of timeliness, for a number of reasons. These claims have shorter timeframes to begin with, and so delays were observed sooner in the timeliness figures. Small claims may also be less suited to remote hearings as they tend to be in person claims rather than professional users.

Measures put in place to help with the backlog of small claims include: Small Claims Mediation (re-referring cases back to mediation) and Early Neutral Evaluation (where a judge will try and engineer agreement without any finding on the fact). These measures, when successful, result in outcomes which are not used within the timeliness calculations. This means the final cases used in timeliness measures include a disproportionate number of more complex cases which take longer to dispose of.

For multi/fast track claims, it took on average 74.0 weeks to reach a trial, 13.0 weeks longer than in October to December 2019 – continuing to exceed the upper limit of the range 2009-2019 (52 to 62 weeks).

Covid-19 and associated actions have led to an uptick in time taken for all claims to reach trial. Prior to this, a sustained period of increasing receipts had increased the time taken to hear civil cases and caused delays to case progress. Additional venues have been provided to add temporary capacity to hear cases and help the court and tribunal system to run effectively.

6. Judgments

Judgments were down 32% compared to same quarter in 2019

There were 214,000 judgments made in October to December 2021, compared to 315,000 in the same quarter of 2019. Of these judgments, 193,000 (90%) were default judgments.

Figure 7: All claims, judgments and default judgments, Q4 (October to December) 2016 to Q4 (October to December) 2021 (Source: tables 1.2 and 1.4)

There were 214,000 judgments made in October to December 2021, down 32% compared to the same quarter of 2019. Of these, 90% were default judgments, up 2pp on its share in October to December 2019.

The second largest type of judgment was ‘judge’[footnote 6], of which there were 7,500 in October to December 2021, down 40% on the same quarter in 2019 (from 13,000). ‘Judge’ judgments accounted for 4% of all judgments.

7. Warrants and Enforcements

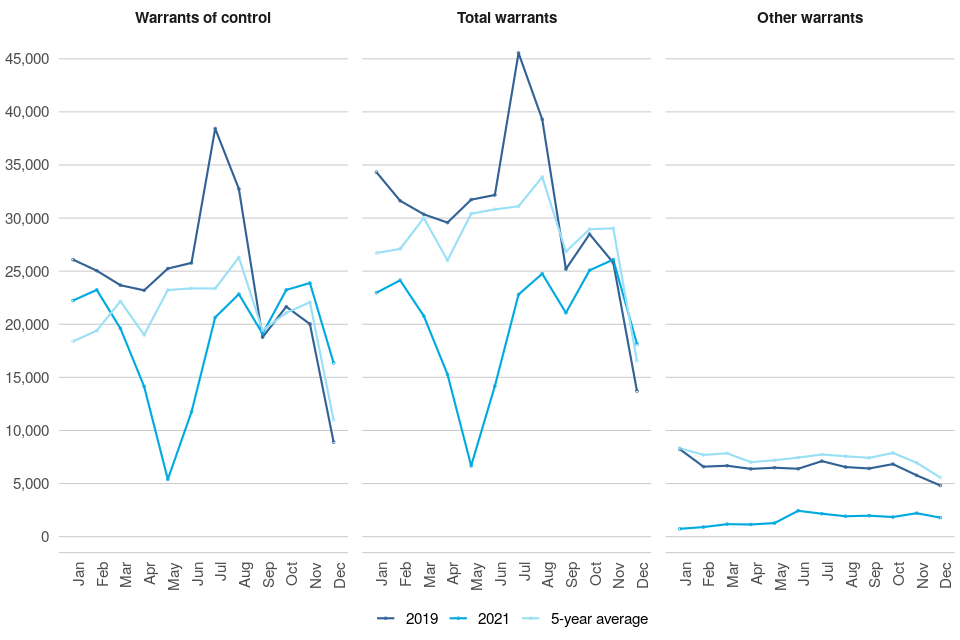

Warrants issued were up 2% when compared to same quarter in 2019

In October to December 2021, 69,000 warrants were issued, up 2% from 68,000 in the same quarter of 2019. Of these, 63,000 (92%) were warrants of control, up 26% compared to the same period in 2019.

Enforcement applications were down 47% and enforcement orders were down 45% when compared to October to December 2019

All application categories were down on October to December 2019. Attachment of earnings (AoE) applications were down 53% (from 17,000 to 8,000), while AoE orders were down 55% (from 7,500 to 3,400).

Figure 8: Warrants and enforcements issued – Q4 (October to December) 2016 to Q4 (October to December) 2021 (Source: tables 1.7 and 1.8)

7.1 Warrants (table 1.7)

In the latest quarter (October to December 2021) there were 69,000 warrants issued, up 2% (from 68,000) on the same quarter in 2019.

Figure 9: Monthly warrants issued by type, 2019, January to December 2021, and 5-year average[footnote 3]:

There was a particularly sharp decline in the monthly breakdown of warrants issued due to the initial impact of Covid-19. Following a significant decline in Q2 of 2020 (not shown), warrant volumes generally increased gradually from July 2020. Volumes fell back to 6,700 in May 2021, down 78% on the five-year average, but increased in June and July. These have continued to rise gradually since August 2021 with 25,000, 26,000 and 18,000 warrants issued respectively in October, November and December. These reached their highest level since February 2020 in November, down 10% on the five-year average. The decrease in warrants in December is likely to be due to seasonal trends and a reduction in processing in December.

However, different types of warrants have shown different patterns. As warrants of control are the majority of warrants issued, they have dominated the overall pattern and these also fell to 5,400 in May 2021, down 77% on the five-year average. This volatile pattern was caused by large backlogs being issued by key bulk issuers in August, as well as local Covid restrictions in September. These have generally increased since August 2021 with 23,000, 24,000 and 16,000 warrants of control for October, November and December respectively. These were up 10%, up 8% and up 49% respectively compared to the 5-year average. The fall in warrants of control in December is likely to be due to seasonal trends and a reduction in processing in December.

In contrast, other warrant types have remained low throughout the last year, although these increased slightly in June to 2,400 but have since decreased with 1,800, 2,200 and 1,800 issued in the latest three months (down 77%, down 68% and down 68% respectively compared to the 5-year average). The increase in June 2021 was led by warrants of possession and further details on this can be found in the Mortgage and Landlord Possessions publication annex here.

7.2 Enforcements (table 1.8)

In October to December 2021, there were 14,000 enforcement-related order applications (which include attachment of earnings orders, charging orders, third party debt orders, administration orders, and orders to obtain information), down 47% compared to the same quarter of 2019. All application types were down, in particular, attachment of earnings (AoE) applications were down 53% (from 17,000 to 8,000).

There were 9,100 enforcement-related orders made in October to December 2021, down 45% compared to the same quarter of 2019. Orders fell across all types, with the decrease driven by AoE orders, which were down 55% (from 7,500 to 3,400).

Over the longer term, there has been a decreasing trend in enforcement-related applications received and orders made since 2009, possibly due to claimants’ preference for using warrants instead to retrieve money, property or goods.

8. Judicial reviews[footnote 7]

Judicial review applications were down 15% compared to the same quarter[footnote 8] in 2020 and down 29% on Q4 2019 (pre-covid baseline).

Of the 2,300 applications received in 2021, 57% have already closed, and 190 were found to be ‘Totally Without Merit’ (15% of cases that reached the permission stage).

Of the 570 applications received in Q4 2021, 23% have already closed, and 16 were found to be ‘Totally Without Merit’ (13% of cases that reached the permission stage).

There were 2,300 judicial review applications received in 2021, down 18% on 2020 (2,800) and down 31% on 2019 (from 3,400).

There were 570 judicial review applications received in Q4 2021, down 15% on Q4 2020 (670) and down 29% on Q4 2019 (from 800).

Figure 10: Judicial Review Applications, by type; Q4 2014 to Q4 2021 (Source: JR CSV)

Annual JR receipts – Q1 to Q4 2021:

Of the 2,300 applications received in 2021, 800 were civil immigration and asylum applications, 1,400 were civil (other), and 140 were criminal, down 31%, down 9% and down 10% respectively on 2020. 48 of the civil immigration and asylum cases have since been transferred to the UTIAC.

Of the applications that were made in 2021 in the period January to December, 57% are now closed. Of the total applications, 1,300 reached the permission stage in 2021, and of these:

- 15% (190) were found to be totally without merit (TWM).

- 370 cases were granted permission to proceed and 870 were refused at the permission stage. However, 64 of the cases refused at permission stage went on to be granted permission at the renewal stage.

- 430 cases have been assessed to be eligible for a final hearing and of these, 93 have since been heard.

- the mean time from a case being lodged to the permission decision was 79 days, and the mean time from a case being lodged to final hearing decision was 178 days.

Quarterly JR Receipts – Q4 2021:

Of the 570 applications received in Q4 2021, 200 were civil immigration and asylum applications, 340 were civil (other), and 31 were criminal, down 26%, down 7% and down 14% respectively on Q4 2020. 6 of the civil immigration and asylum cases have since been transferred to the UTIAC.

Of the applications that were made in Q4 2021, 23% are now closed. Of the total applications, 120 reached the permission stage in Q4 2021, and of these:

- 13% (16) were found to be totally without merit (TWM).

- 38 cases were granted permission to proceed and 80 were refused at the permission stage. However, 2 of the cases refused at permission stage went on to be granted permission at the renewal stage.

- 40 cases have been assessed to be eligible for a final hearing and of these, 2 have since been heard.

- the mean time from a case being lodged to the permission decision was 40 days. Timeliness for cases being lodged to final hearing is not included for the latest quarter as this would be based on too few cases to be meaningful.

8.1 Applications lodged against departments (table 2.5)

This quarter’s tables include judicial review figures by defendant type (i.e. individual government department or public body) – table 2.5. This table, which is now published quarterly, provides the number of judicial review applications lodged, permission granted to proceed to final hearing, and decisions found in favour of the claimant at final hearing.

The information presented is derived from the ‘defendant name’ – a free text field completed by the claimant, which is automatically matched and grouped by department. All efforts have been made to quality assure the data presented. However, this is a manually typed field, and as such is open to inputting errors and should be used with caution.

The key findings for Q4 2021 are:

- The Home Office was the department/body with the largest number of JR applications lodged against them, with 190 applications. Of these, 13 were granted permission to proceed to final hearing (7% of applications) to date.

- The second largest recipient of JR cases was the Local Authorities, with 160 cases received, of which to date 17 were granted permission to proceed to final hearing (11% of applications).

- The third largest recipient was Ministry of Justice, having 100 applications lodged against them. Of these, 3 were granted permission to proceed to final hearing (3% of applications) to date.

A more granular view of the JR data by department and case type can be found in the newly developed data visualisation tool found here. Feedback is welcome on this tool to ensure it meets user needs.

9. Privacy Injunctions[footnote 9]

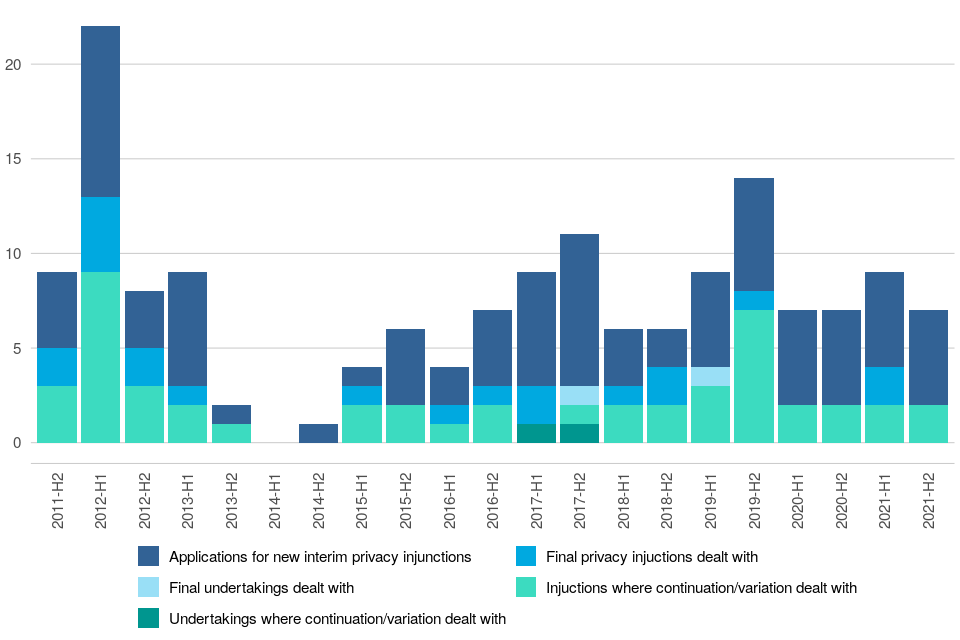

In the final six months of 2021, there were 5 proceedings where the High Court considered an application for a new interim privacy injunction.

Two proceedings were considered at the High Court on whether to continue or amend an interim injunction.

There were no proceedings considered at the High Court on whether to issue a final permanent injunction, no proceedings considered on whether to continue or amend an undertaking, and no proceedings considered a final undertaking[footnote 10].

Figure 11: Revised number of privacy injunction proceedings, by type of proceeding, from Aug-Dec 2011[footnote 11] to Jul-Dec 2021 (Source: tables 3.1, 3.2 and 3.3)

9.1 New interim privacy injunctions (Table 3.1)

All five of the proceedings at the High Court that took place in July to December 2021 were granted. In the previous six months (January to June 2021) five new interim privacy injunction proceedings took place, and all of these were granted.

9.2 Continuation of existing interim injunctions (Table 3.2)

The continuation of two existing interim injunction proceeding that took place in July to December 2021 were granted/varied. In January to June 2021, the continuation of one existing interim injunction proceeding was granted/varied and one was discharged.

9.3 Final privacy injunctions (Table 3.3)

There were no final privacy injunctions or final undertakings dealt with in July to December 2021. Of the two final privacy injunctions in January to June 2021, these were both granted.

10. Further information

10.1 Provisional data and revisions

The statistics in the latest quarter are provisional and revisions may be made when the next edition of this bulletin is published. If revisions are needed in subsequent quarters, these will be annotated in the tables.

10.2 Accompanying files

As well as this bulletin, the following products are published as part of this release:

- A supporting document providing further information on how the data is collected and processed, as well as information on the revisions policy and legislation relevant to civil justice.

- The quality statement published with this guide sets out our policies for producing quality statistical outputs for the information we provide to maintain our users’ understanding and trust.

- A set of tables providing statistics on the Business and Property Courts of England and Wales.

- A set of overview tables and CSV files, covering each section of this bulletin.

- A JR data visualisation tool (to provide a more granular view of the JR data by department and case type). This can be found here.

10.3 Rounding convention

Figures greater than 10,000 are rounded to the nearest 1,000, those between 1,000 and 10,000 are rounded to the nearest 100 and those between 100 to 1,000 are rounded to the nearest 10. Less than 100 are given as the actual number.

10.4 National Statistics status

National Statistics status means that official statistics meet the highest standards of trustworthiness, quality and public value.

All official statistics should comply with all aspects of the Code of Practice for Official Statistics. They are awarded National Statistics status following an assessment by the Authority’s regulatory arm. The Authority considers whether the statistics meet the highest standards of Code compliance, including the value they add to public decisions and debate.

It is the Ministry of Justice’s responsibility to maintain compliance with the standards expected for National Statistics. If we become concerned about whether these statistics are still meeting the appropriate standards, we will discuss any concerns with the Authority promptly. National Statistics status can be removed at any point when the highest standards are not maintained, and reinstated when standards are restored.

10.5 Future publications

Our statisticians regularly review the content of publications. Development of new and improved statistical outputs is usually dependent on reallocating existing resources. As part of our continual review and prioritisation, we welcome user feedback on existing outputs including content, breadth, frequency and methodology. Please send any comments you have on this publication including suggestions for further developments or reductions in content.

10.6 Contacts

Press enquiries should be directed to the Ministry of Justice (MoJ) press office:

Sebastian Walters - email: sebastian.walters@justice.gov.uk

Other enquiries about these statistics should be directed to the Data and Evidence as a Service division of the Ministry of Justice:

Laura Jones - email: cajs@justice.gov.uk

Next update: 1 June 2022

-

To align with new terminology within MoJ, specified money claims are now referred to as “Money Claims” and unspecified money claims are now referred to as “Damages Claims”. ↩

-

Following the alignment of the fees for online and paper civil money and possession claims in May 2021 (https://www.legislation.gov.uk/uksi/2021/588/pdfs/uksiem_20210588_en.pdf), figure 2 shows all data with the updated claim brackets for comparison, a further breakdown of these brackets is available within the CSV. The CSV shows updated claim brackets from 2021. ↩

-

The 5-year average is calculated using data from 2015-2019 as a pre-Covid baseline. Figures for the 5-year average have been recalculated due to a processing error in previous quarters. ↩ ↩2 ↩3

-

https://www.gov.uk/government/news/priority-courts-to-make-sure-justice-is-served ↩

-

https://www.fca.org.uk/publications/finalised-guidance/personal-loans-coronavirus-temporary-guidance-firms ↩

-

For a judgment classed as “judge”, the claim is settled by the decision of a judge following a hearing or trial. ↩

-

The judicial review data are Official Statistics ↩

-

Quarterly judicial review figures have been added to the bulletin this quarter for a more granular breakdown of this data. These figures are available in the accompanying CSV and data visualisation tool for judicial reviews and will be added to the main tables from Q1 2022. ↩

-

The privacy injunction data are Official Statistics ↩

-

An undertaking is different from an injunction, in that it is a promise given by the defendants, rather than an injunction which is an order of the court ↩

-

H2 2011 only covers the period August-December 2011 and is not a full half-year ↩