Child and Working Tax Credits Statistics: Quality Report April 2021

Published 23 June 2021

© Crown copyright 2021

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/statistics/child-and-working-tax-credits-statistics-provisional-awards-april-2021/child-and-working-tax-credits-statistics-quality-report-april-2021

1. Introduction

These statistics focus on the number of families benefiting from Child Tax Credit (CTC) and/or Working Tax Credit (WTC) in England, Scotland, Wales and Northern Ireland as at 2 April 2021.

This publication presents a breakdown of families by their profile position, age and gender, type of family and family size as well as the number of children in benefiting families, broken down by age.

It also includes statistics on families benefiting from each of the different elements of tax credits and provides information on the income used in calculating awards and the frequency of payments.

Tax credits were introduced in April 2003 replacing Working Families’ Tax Credit, Disabled Person’s Tax Credit and Children’s Tax Credit. They are an important part of the Government’s policy aims to provide adequate financial incentives to work, reduce child poverty and to increase financial support for all families.

WTC provides in-work support for people on low incomes, with or without children. It is available for in-work support to people who are aged at least 16 and meet a certain criteria.

CTC provides income-related support for children and qualifying young people aged 16 to 19 who are in full time, non-advanced education or approved training into a single tax credit, payable to the main carer. Families can claim CTC whether or not the adults are in work.

More information about tax credits eligibility can be found on GOV.UK.

2. Relevance

The provisional awards are currently published in January/February and June/July. These statistics are as close to real-time as possible and represent the picture as at the beginning of April and December.

These are National Statistics and the month of publication is indicated on HM Revenue Customs (HMRC) release schedule with the exact date being published at least 28 days before its release on HMRC statistics release calendar.

The statistics contained in this publication will be of interest to anyone who is looking for the latest possible data on tax credits. Specifically, there are aggregate statistics on who is getting what level of tax credits support as well as breakdowns by various subcategories - e.g. family composition, family income, work status, and geographical analyses.

It may be of interest to academics, think tanks and political parties interested in the twin aims of tax credits - eradicating child poverty and improving work incentives. Equally, it may be of interest to people considering wider questions on government support systems and/or others designing benefit systems.

Finally, the geographical analyses might be of interest at the more local level, giving some indication of the level of government support in each region and local authority in the UK.

3. Accuracy and Reliability

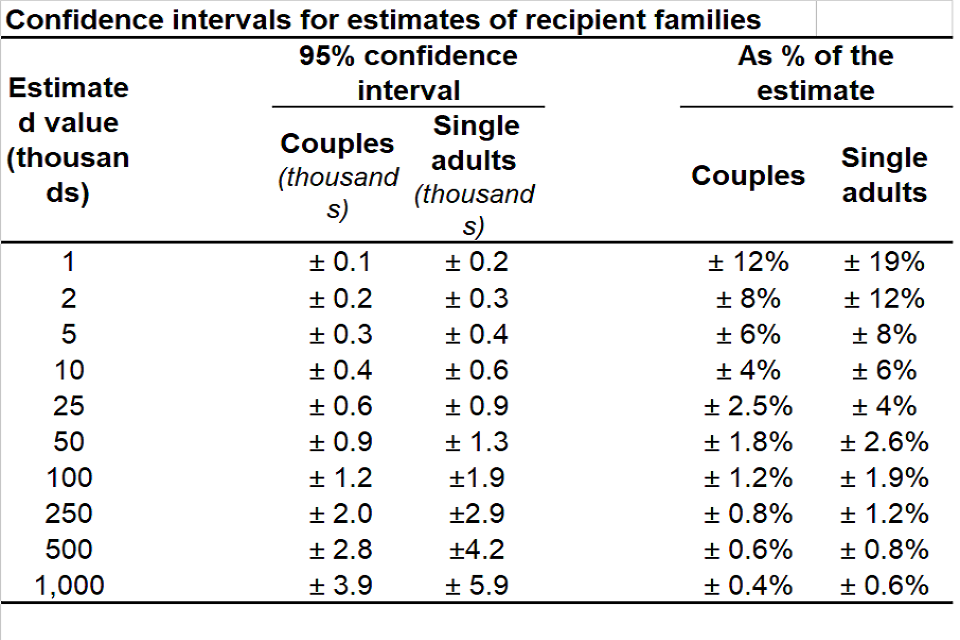

The published tables are based on a random sample of families receiving CTC or WTC at the reference date of 2 April 2021. The sample comprises 10% of such single adults (with or without children) and 20% of such couples.

Each figure in the tables is derived by weighting the relevant sample cases by the inverses of these sampling fractions. The figures in the tables are therefore estimates, but we know how accurate they are.

For example, suppose that there are 100,000 couples with a characteristic. This number is not known, and we are to estimate it via the sample. Each couple is sampled with a probability of 0.2.

Statistical theory says that there is a 95% probability that the number sampled will lie between 19,752 and 20,248, and that the resulting estimate will lie between 98,760 and 101,240.

At least approximately, then, where an estimate of 100,000 is derived from the sample, the true figure lies between these figures, with a 95% probability. That is, the “95% confidence interval” for the estimate is the estimate itself plus or minus 1,240. The width of the confidence interval varies with the size of the estimate and the sampling fraction, as shown in the table below.

For estimates that comprise a mixture of couples and single adults, the figures will lie between the two sets shown, according to the mix.

3.1 Sampling Uncertainty

As the figures are based on sample, therefore they are subject to sampling uncertainty. Values have been supressed for some where underlying sample counts are low. An entry of “[no data]” in a table indicates that the data has been rounded down to 0 or has been withheld in line with HMRC Dominance and Disclosure policy.

The provisional numbers relate to the caseload position at a snapshot point in time, based on the family circumstances we have been informed of by each family prior to that particular time.

The finalised awards (published in June/July each year) relate to the complete retrospective picture for the year, based on a finalised view of family incomes and circumstances.

The caseload population will be different, (so it should be noted that they are NOT a revision as such for this reason) between the two publications as a result of HMRC knowing the complete finalised picture of the award.

3.2 Revision Policy

This policy has been developed in accordance with the UK Statistics Authority Code of Practice for Official Statistics and Her Majesty’s Revenue and Customs Revisions Policy. The UK Statistics Authority Code of Practice can be found on the GOV.UK.

There are two types of revisions:

Scheduled Revisions

- regular, scheduled revisions due to the receipt of updated information since the previous statistical publication.

Unscheduled Revisions

- HMRC aims to avoid the need for unscheduled revisions to publications unless they are absolutely necessary and put systems and processes in place to minimise the number of revisions. Where revisions are necessary due to errors in the statistical process, an explanation along with the nature and extent of revision is also provided. The statistical release and the accompanying tables will be updated and published as soon as is practical.

4. Timeliness and Punctuality

The publication dates are published in the preceding publication and is produced with enough time to produce the analysis, carry out quality assurance and prepare the right format for publication. The release has since been published each year on the pre-announced date.

5. Accessibility and Clarity

HMRC has an increased focus on accessibility and all documents published for this release have met the Department’s accessibility requirements.

Provisional tax credits statistics are free and accessible to users via the UK National Statistics publication hub

Publications are available in PDF and Excel formats and can easily be downloaded by users.

The latest statistics publication is available in HTML and Open Document Spreadsheet (ODS) formats in compliance with the new accessibility requirements.

You can also access the previous publications by visiting the HMRC’s statistics on The National Archives website.

6. Coherence and Comparability

It is also difficult to fully compare this publication with any previous releases due to the numerous policy changes affecting CWTC over the past ten years. Changes in geographical boundaries and area codes have also had an impact on time series analysis which, where relevant, are explained in the publication itself.

7. Trade-Offs Between Output Quality Components

We are committed to ensuring these statistics are as accurate as possible and to minimise revisions due to errors, as such, the data will be published in a timely manner taking into account the time needed to carry out full and robust quality assurance.

The Provisional Tax Credit Statistics in April models entitlement for the whole year; even though they are a snapshot picture compiled using the data at April 2021.

It is not until finalisation (and thereby in the finalised award data publication) that a complete retrospective picture for the year, based on a finalised view of family incomes and circumstances, is known. So, the trade-off that should be considered is that figures for provisional awards are more up to date, but are subject to retrospective change.

The sizes of these changes can be seen by comparing the data for selected dates in finalised awards with data published earlier on provisional awards at the same snapshot dates.

The provisional award data tables classify families according to the levels of their entitlement at the reference date, modelled from data on their circumstances and their latest annual incomes reported and processed by that date. The actual amount being received at that date can be lower, due to the recovery of earlier overpayments.

The tables describe as “recipients” all families with positive modelled entitlement, though in some cases the payments are reduced to zero.

8. Assessment of User Needs and Perceptions

Users can provide feedback by contacting the relevant statistician whose details are provided in the publication.

HMRC launched a wide-ranging consultation on our official statistics on 8 February 2021. .

This includes changes to a number of tax credits statistics releases including a proposal to reduce the provisional award statistics from twice yearly to annually. An annual publication would be published each summer alongside or as one publication with the Child and Working Tax Credits Finalised Award statistics.

Any changes to the tax credit releases will take into account user feedback which we will respond to after the consultation.

9. Performance, Cost and Respondent Burden

Most of the datasets used for this analysis are taken from the tax credits administrative data and therefore the cost of carrying out this analysis is minimal. The compilation of these statistics does not impose any additional burden on employees or employers.

10. Confidentiality, Transparency and Security

All datasets used for these statistics are stored in a Controlled Access Folders (CAFs) which are accessible to only a few analysts who are part of the production team and therefore have business need to access the data.

HMRC is committed is to the efficient management of information as such our records are compliant with:

-

UK General Data Protection Regulation (UK GDPR) 2018

-

The Data Protection Act 2018

-

The Data Protection Act 1998

-

The Public Records Act 1968

-

The Freedom of Information Act 2000 (FOI) (in particular the Code of Practice on Records Management issued under s46 FOI which requires that public authorities have effective record-keeping arrangements in place).

Under the guidelines for pre-release access, information contained in the tables is not given out in final form one day before publication and then only to nominated officials and ministers whose names are published on the HMRC website.

To avoid the possible disclosure of information about individual families, values have been supressed when underlying sample counts are low. An entry of “[no data]’’ in a table indicates that the data has been rounded down to 0 or has been withheld in line with HMRC’s Dominance and Disclosure policy.