Market Data Insights - August 2021

Published 13 September 2021

© Crown copyright 2021

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/market-data-insights-august-2021/market-data-insights-august-2021

Economic summary

This month the NHS began to offer COVID-19 vaccinations to 16 and 17-year olds. As of 29 August, 88% of people aged 16 and above in the UK have received their first dose and 79% had received their second dose.

Cases have risen steadily throughout August, possibly related to the legal limits on social contacts being lifted in July. The 7-day average number of cases stood at 25,887 as at 31 July which rose by 30% to 33,545 at 18 August. Cases are expected to rise further as pupils return to schools and universities and many begin to return to offices in September.

The furlough scheme will close by the end of September, which could lead to redundancies and cause unemployment to rise as a result. In contrast, there have been lorry driver shortages which have been attributed to multiple reasons such as summer breaks, Brexit and COVID-19 self-isolations. This has caused supermarkets to have supply issues and some have reacted by increasing joining incentives for new drivers. The reduced supply of supermarket goods and increased driver salary costs may cause an increase in inflation.

Credit spreads as at 25 August 2021

| AAA | AA | A | BBB | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 25 bps | 50 bps | 87 bps | 131 bps | ||||||

| 0 bps MoM | ▼2 bps MoM | ▼3 bps MoM | ▼3 bps MoM |

An asset’s ‘credit spread’ is the difference between its yield and that of a government-issued bond of similar maturity. It is an indicator of the perceived riskiness of the asset. It represents how much investors want to be rewarded for investing in it instead of a lower risk government bond.

Over the month up to 25 August, credit spreads held steady for most higher grades of bonds. However, the credit spreads on lower grade bonds fell. The lower the grade of bond, the deeper the decline tended to be.

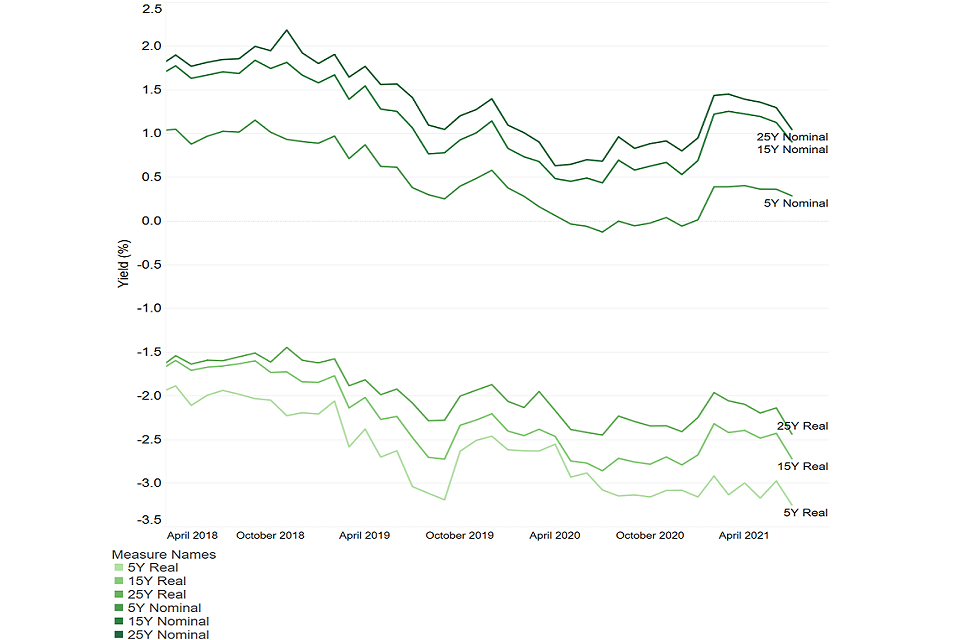

UK Gilts

UK Gilts are UK government bonds. These are related to the Bank of England base rate, which has stayed flat at an historical low of 0.1% since March 2020.

Both nominal and real yields fell over the month of July. The graph below shows how real yields have fallen to some of the lowest levels seen in recent years.

UK Gilts

Bond yields fall when there is an increased demand for them. This implies there is an increased demand for gilts, as they have become comparatively more attractive investments.

Investors may have a more pessimistic view of economic growth or perceive that the markets are becoming increasingly uncertain and want to move towards safer investments, such as gilts. Alternatively, investors may have an improved view of the UK government’s ability to honour their bonds.

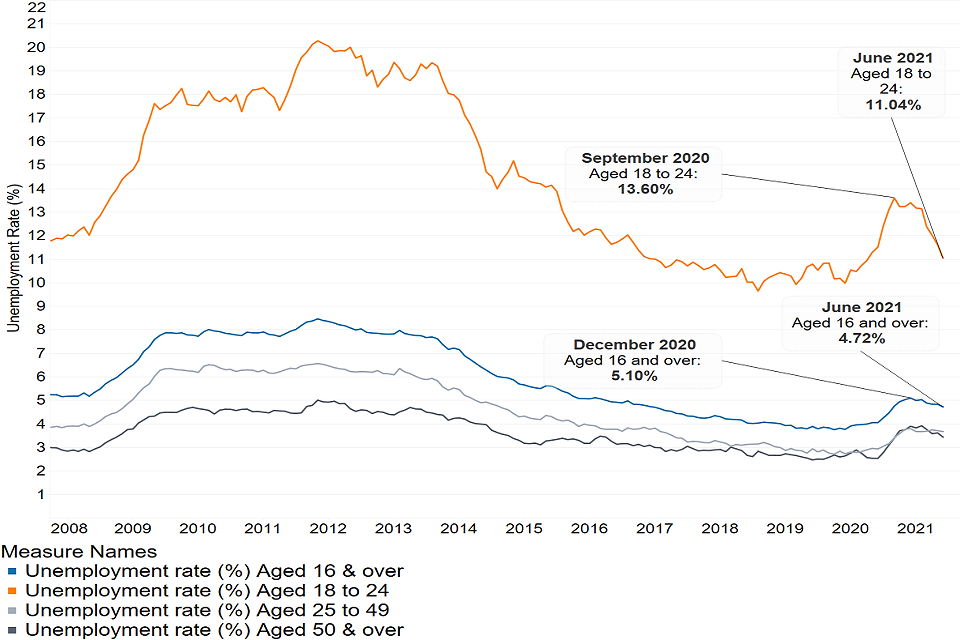

Unemployment rates

Unemployment is broadly defined as those aged 16 and above who are without work and who have actively been seeking work. The unemployment rate is defined as the number of unemployed divided by the sum of those who are either employed or unemployed.

Unemployment rates for those aged 16 and above have shown a slight decrease in recent months. However, the most marked decrease in unemployment is in those aged 18-24. This could be attributed to hospitality and retail re-opening as social distancing measures were relaxed.

Unemployment rates

Since 2016, unemployment rates for the 25 to 49 age group began to converge to the 50 and above age group rates. It is difficult to give a definitive explanation on this without looking closer at employment by industry and changes to employment laws and state benefits.

Inflation

The Consumer Price Index (CPI) measures the average change in prices over time that consumers pay for a basket of goods and services. CPIH is similar to CPI, in that it also measures inflation, but it also factors in owner occupiers’ housing costs.

So far, this year has seen inflation increase quite significantly compared to recent years. In July, CPIH stayed above 2% for the third consecutive month. The primary driver in inflation came from increased transport costs.

Inflation

As a barometer, the Bank of England has a government mandate to set its base rates to target an inflation rate of 2%.

If this level of inflation is sustained or continues to rise, it might prompt an increase in the base rate. However, increasing base rates is often seen as stifling the economy as it causes borrowing costs to rise, reducing spending and investing.

The Bank of England’s decisions around future base rate changes, will therefore need to balance inflationary pressures against the impact on the UK economy as it attempts to recover from the effects of the pandemic.

Disclaimer

The information in this publication is not intended to provide specific advice. Please see our full disclaimer for details.

The Government Actuary’s Department is proud to be accredited under the Institute and Faculty of Actuaries’ Quality Assurance Scheme.

QAS Logo