LA Welfare Direct 11/2019 Appendix A: Final Report on LA review of self-employed Housing Benefit claimants

Updated 4 March 2024

© Crown copyright 2024

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/la-welfare-direct-bulletins-2019/la-welfare-direct-112019-appendix-a-final-report-on-la-review-of-self-employed-housing-benefit-claimants

Summary

Based on analysis that found that 52% of self-employed Housing Benefit (HB) claimants had not updated their earnings figures for at least 12 months, Fraud, Error and Debt Analysis (FEDA) and Housing Delivery Division (HDD) worked with Local Authorities (LAs) to perform a review of working-age, self-employed HB claimants, with the intention of reducing the level of fraud and error arising from this issue.

Running from September 2018 to April 2019, a total of 72,000 cases were sent out. During this time, the percentage of working-age self-employed HB claimants with unchanged earnings fell from 52% to 21%.

LAs actioned 82% of the referrals generated, resulting in a total weekly net reduction to HB entitlement of £1.02 million, and a total reduction to Annually Managed Expenditure (AME) expenditure of £73 million.

With a Departmental Expenditure Limit (DEL) cost of £5m, that gives a return on investment (ROI) of around 15 to 1.

Introduction

1. Earnings and employment issues are the largest cause of overpayments across the continuously reviewed benefits, accounting for £878 million in 2018 to 2019. Of this, around £110m can be attributed to self-employed, working age, Housing Benefit (HB) claimants.

2. Self-employed HB claimants are expected to regularly inform LAs of changes to their earnings, failure to do so may result in HB overpayments or underpayments.

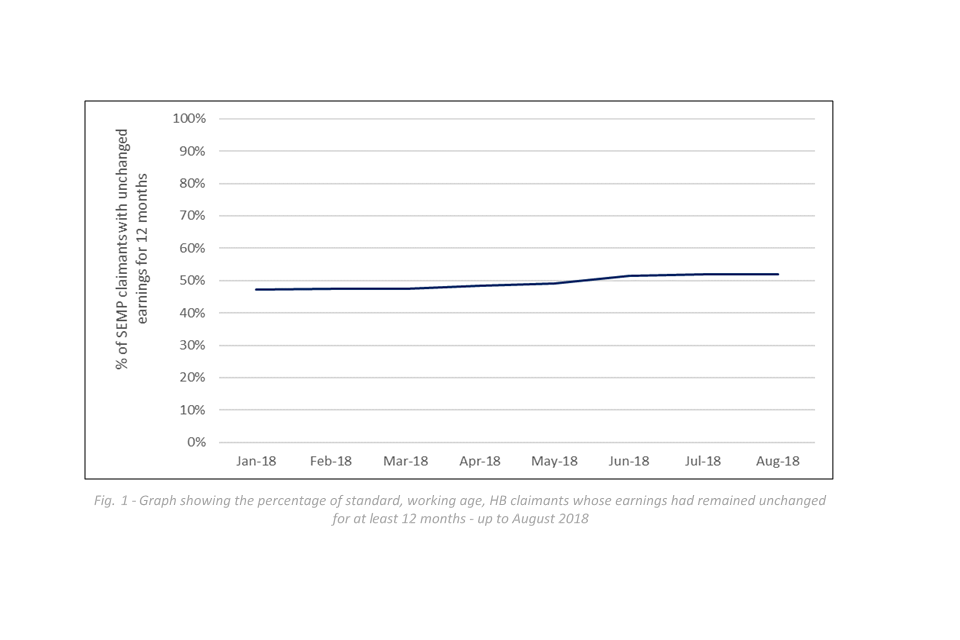

3. We would expect earnings to change at least once in any 12 month period. However, analysing the LAs’ SHBE returns, we found a large percentage of self-employed HB claimants had not reported earnings changes in over 12 months, peaking at 52% in August 2018.

Graph showing the percentage of standard, working age, HB claimants whose earnings had remained unchanged for at least 12 months between January 2018 and August 2018.

4. We put together a proposal for an intervention in which LAs would be provided with a list of eligible cases for review, they would contact the claimants and update the earnings information that they currently held. This was expected to lead to a reduction in both the number of cases with unchanged earnings figures, and HB overpayments.

5. Generally, an increase in earnings would result in a reduction to HB entitlement, and vice-versa. We assumed that the vast majority of the cases referred to LAs would lead to earnings increases, as it would be in the claimants own interest to report earnings decreases. Given that funding would be provided to carry out the case reviews, we also assumed that LAs would action all of the referrals they received. Based on these assumptions, we estimated yearly savings of £75 million would be achieved as a result of the review, comprised of £45 million of prevented overpayments and £30 million of recoverable overpayments.

Methodology

6. The review was proposed to all 379 LAs. Of these, 364 opted into the scheme, with 15 opting out. For those opting in, eligible cases would be identified by Data and Analytics and then would be referred to LAs. However, 16 of those opting in did not hold the data necessary for referrals to be generated. For these LAs, it was agreed that they would still receive funding, provided they identified and actioned eligible cases themselves.

7. Three scans were performed (in September 2018, December 2018, and February 2019) with the aim of identifying cases in which:

- either the claimant, partner, or both were self-employed and of working age

- the claim was non-passported

- there had been no change to earnings for at least the previous 12 months

8. A total of 72,000 referrals were generated, and LAs were provided with a list of the cases after each scan.

9. Because of their existing links to LAs, HDD were responsible for any communication with LAs. They sent out a template for the LAs to fill out, asking for 3 pieces of information for each referral that they actioned:

- local authority ID number

- Housing Benefit reference number

- date on which action began on the case

They were then asked to return the template to HDD on a regular basis, who collected them into a single Excel file, which was passed on to FEDA.

10. Each returned case was then identified in SHBE data by their LA ID and HB reference. This allowed us to capture an array of information, such as pre-entitlement, post-entitlement, earnings figures, change of circumstance records, and error records. These could be tracked over time, allowing us to track the progress of the scheme.

Results

11. We identified three key areas in which progress could be measured and which would provide us with a picture of the outcomes once the scheme had run its course:

- Number and proportion of referrals actioned by LAs

- Percentage of claims with self-employed earnings unchanged for at least 12 months

- Entitlement changes that had occurred following the review process

LA performance measurement

12. Of the 72,000 referrals generated by Data and Analytics across the 3 scans, to date 82% (59,000) have been reported as actioned by LAs. Of these, we were able to include only 55,000 cases in our analysis. The remaining 4,000 were excluded due to data quality issues.

13. Most LAs did a good amount of the work referred to them. Over 85% of LAs actioned at least half of the referrals generated for them, and over 60% actioned at least four-fifths. All LAs actioned at least some referrals.

14. There were, however, around 13,000 referrals that remained un-actioned by the time the scheme came to a close at the end of the 2018 to 2019 financial year. We are currently unable to comment on why this was the case.

Percentage self-employed earnings unchanged

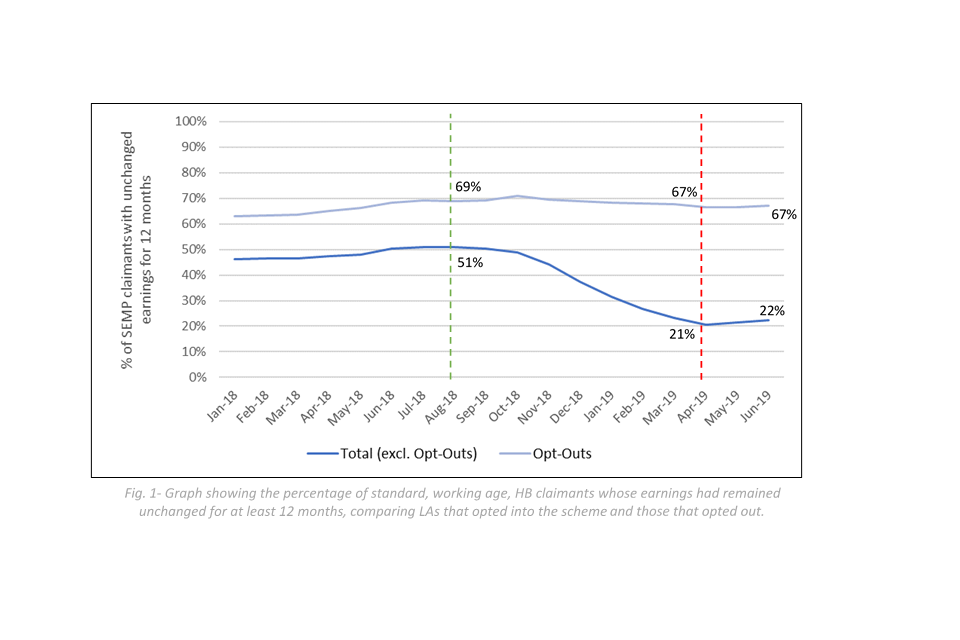

15. Among the LAs that opted in to the scheme, there was a significant fall in the percentage of cases with unchanged earnings, from 51% in August 2018 to 21% in April 2019. This was not the case for LAs that opted out. This group saw a reduction of just 2% over the course of the scheme, from 69% to 67%. This strongly suggests that the review process was the reason for the reduction seen among LAs that opted in.

16. In the months following the review, we have seen a slight reversal of this trend. From April to June 2019 there has been an increase of 1% in the percentage of cases with unchanged self-employed earnings. It remains to be seen whether this will continue, but when considered alongside the 21% of cases that remained unchanged at the end of the review period, this reversal may suggest there is value in repeating the scheme.

Graph showing that the percentage of standard, working age, HB claimants whose earnings had remained unchanged, between January 2018 and July 2019 for LAs that opted in or out of the scheme.

Effect on HB entitlements

17. Of the 55,000 actioned referrals that were able to be matched in SHBE, 19% (10,500) resulted in increases to entitlement, 44% (24,000) resulted in decreases to entitlement, and 11% (6,000) disappeared off SHBE, implying the claims were cancelled. The remaining 26% (14,500) saw no entitlement change.

18. While the original aim of the scheme was to identify earnings changes, this was not the outcome of all case reviews. Of the 55,000 actioned referrals, 67% (37,000) resulted in a change to earnings, with 24% (9,000) of these linked to entitlement increases, and 54% (20,000) to entitlement decreases. The remaining 22% (8,000) resulted in a change to earnings, but with no change to HB entitlement.

19. Of the 14,500 cases which saw no entitlement change, 55% (8,000) reported a change to earnings that did not affect entitlement. The remaining 45% (6,500) were recorded as having no change to either earnings or entitlement.

Estimated savings

20. In order to estimate the effect of the scheme on AME, we need to multiply the total weekly entitlement change, by the average number of weeks we would expect those self-employed earnings to have continued to go unchanged had the cases not undergone review. Our analysis indicates that to be 59 weeks for reductions to entitlement and 46 weeks for increases to entitlement.

21. As a result of LAs actioning the referrals generated for them, 40,500 cases had a change in their weekly entitlement with a total net reduction of £1,017,000, resulting in an estimated net AME saving of £63 million.

22. This is comprised of:

- 30,000 cases with a decrease in entitlement, with a total weekly reduction to entitlement of £1,232,000, resulting in an estimated £73 million decrease in AME expenditure

- 10,500 cases with an increase in entitlement, with a total weekly increase to entitlement of £215,000, resulting in an estimated £10 million increase in AME expenditure

23. These savings from prevention are higher than the £45 million predicted, despite proving wrong our assumption that only cases with increases to earnings would be found. This is primarily because of the larger than expected number of cases that had their entitlement terminated as a result of the review.

24. In addition to prevented overpayments, recoverable overpayments will also contribute to the AME savings.

Over the course of the scheme, past overpayments were detected in 39% of cases with changes to entitlement, with a total value of £16.5 million. Compared against the £73 million of future overpayment detected, this is lower than we might expect, and is lower than the £30 million predicted at the proposal stage. The reason for this seems to be that in most cases LAs opted simply to adjust the entitlement going forward, without identifying a past overpayment.

25. In accordance with subsidy rules, DWP will recover 60% of HB overpayments identified over the course of the scheme, which equates to £10 million. Combined with the £63 million of net AME reduced from prevented overpayments and underpayments, this gives a total AME saving of £73 million.

26. The DEL invested in this initiative in 2018 to 2019 was £5 million. The overall ROI is therefore estimated to be around 15 to 1.