FCDO Main Estimates Memorandum 2026 to 2027: Overseas Superannuation Account

Published 29 April 2026

© Crown copyright 2026

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/fcdo-main-estimates-memorandum-2026-to-2027/fcdo-main-estimates-memorandum-2026-to-2027-overseas-superannuation-account

1. Overview

1.1 Objectives

The overseas superannuation pension schemes cover the payments of pensions and grants under various unfunded defined benefit schemes relating to service overseas by former colonial public servants. Payments to entitled pensioners and their dependants are fully financed by the Exchequer.

1.2 Spending controls

The overseas superannuation pension schemes’ budgets are not subject to pre-set Departmental Expenditure Limit (DEL) control totals; they sit within a category of spending known as Resource Annually Managed Expenditure (AME), which can be revised and reforecast regularly. This is because net expenditure and cash payments are largely outside the control of the schemes’ administrators on a day-to-day basis, instead being affected by factors such as membership numbers; mortality rates; the age profile of members, and annual pension increases.

The Resource AME sought in this Estimate is primarily the interest cost arising during the year. The interest rate is charged on opening discounted provision for future pension payments adjusted for pension payments made in year.

In addition, the Net Cash Requirement represents the estimated net cash required for the year to cover payments of pensions.

1.3 Comparison of net spending totals sought

The table below shows how the totals sought for the pension schemes compare with last year:

| Net Spending total Amounts sought this year (Main Estimate 2026-27) |

Difference £m (+/-) compared to final budget last year (last year’s Supplementary Estimate 2025-26) | Difference % (+/-) compared to final budget last year (last year’s Supplementary Estimate 2025-26) | Difference £m (+/-) compared to original budget last year (last year’s Main Estimate 2025-26) | Difference % (+/-) compared to original budget last year (last year’s Main Estimate 2025-26) | |

|---|---|---|---|---|---|

| Resource AME | 11.1 | -0.5 | -4.3 | -0.5 | -4.3 |

| Net Cash Requirement | 31.5 | -6.7 | -17.5 | -6.7 | -17.5 |

1.4 Key drivers of spending changes since last year

The provision sought under Resource AME is lower than last year due to an annual decrease in the opening pension liability which will be a continuing trend year on year as the pension schemes get smaller.

This is also reflected in our Net Cash Requirement reduction as our annual forecasted pension payments decrease as the number of pensioners reduce.

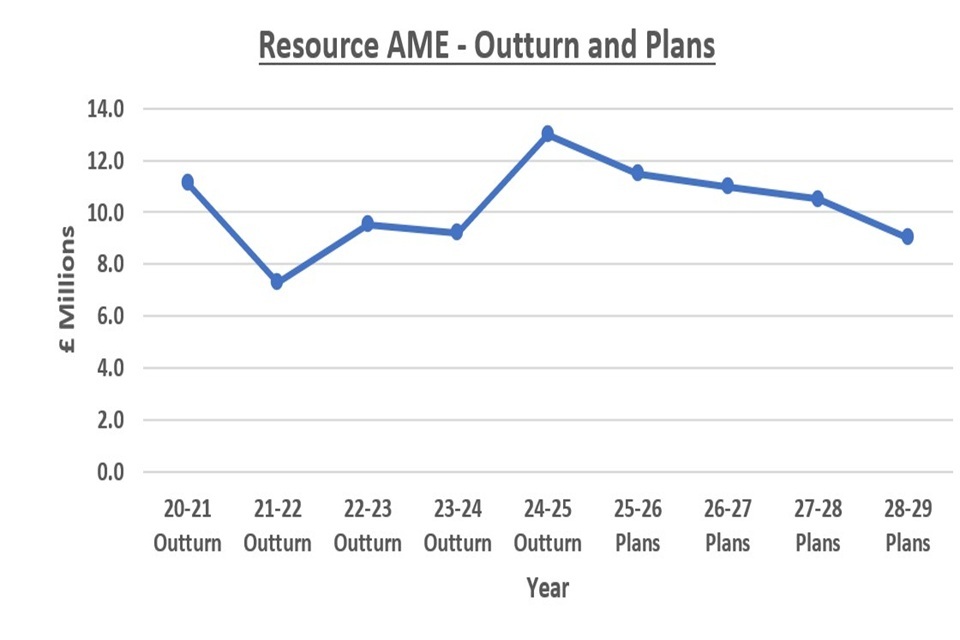

1.5 Spending trends

The chart below shows Resource AME spending trends for the last five years and plans presented in Estimates for 2025-26 to 2029-30.

1.6 Administration costs and efficiency plans

The costs of the administration of the schemes are borne by the Foreign, Commonwealth and Development Office and are forecast to amount to £0.6m in 2025-26 (2024-25: £0.6m)

2. Spending detail

2.1 Explanations of changes in spending

Resource AME

| Subhead | Description | Detail | This year £m | Last year £m | Change £m | Change % | Explanation |

|---|---|---|---|---|---|---|---|

| A | Interest on Scheme liability and other expenses | Interest on scheme liabilities | 11.0 | 11.3 | -0.4 | -3.1 | Paragraph 1.4 |

| A | Interest on Scheme liability and other expenses | Expected credit losses under I FRS 9 ‘Financial Instruments’ | 0.1 | 0.2 | -0.2 | -75.0 | N/A |

| Total | 11.1 | 11.5 | -0.6 | -78.1 |

Net Cash Requirement

| Description | Detail | This year £m | Last year £m | Change £m | Change % | Explanation |

|---|---|---|---|---|---|---|

| Use of pension provision | Pension payments | 31.5 | 38.2 | -6.7 | -17.5 | Paragraph 1.4 |

| Total | 31.5 | 38.2 | -6.7 | -17.5 |

2.2 Changes to contingent liabilities

As at 31 March 2025, there is a contingent liability of £234.77m for the Supplementary Pension for Overseas Service (SPOS) and £15.25m for the Hong Kong (Overseas Public Servants) Act 1996 – Sterling Safeguard Scheme. No new contingent liabilities are expected for 2025-26 or 2026-27.

2.3 Estimated scheme liabilities

The latest full valuation of scheme liabilities was performed with a calculation date of 31 March 2022, (using membership data as at 31 December 2021). The total valuation, including the Gibraltar Social Insurance Fund, was £635m. At that time there were a total of 6,290 pensioners.

The next full valuation will take place with a calculation date of 31 March 2026, using membership data as at December 2025.

3. Accounting Officer Approval

This memorandum has been prepared according to the requirements and guidance set out by HM Treasury and the House of Commons Scrutiny Unit, available on the Scrutiny Unit website.

The information in this Estimates Memorandum has been approved by myself as Departmental Accounting Officer.

Nick Dyer

Accounting Officer

Permanent Under-Secretary of State

Foreign, Commonwealth and Development Office

28 April 2026