Annex G: Cost and charges statutory guidance

Updated 21 June 2021

© Crown copyright 2021

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/consultations/improving-outcomes-for-members-of-defined-contribution-pension-schemes/annex-g-cost-and-charges-statutory-guidance

Reporting of costs, charges and other information: guidance for trustees and managers of occupational schemes

October 2020

Draft statutory guidance issues pursuant Section 113(2A) of the Pensions Scheme Act 1993.

This guidance is produced for the purpose of consultation.

This updates previous statutory guidance for Occupational Pension Schemes (Administration, Investment, Charges and Governance) (Amendment) Regulations 2020.

Index of changes

We have amended the text from the previous guidance in the following paragraphs:

3-4, 10, 14-15, 17-18, 20, 22-23, 31, 33, 34, 36, 44, 51, 53, 56, 58-63, 65, 67, 69, 71-72, 76, 80, 82

We have added the following paragraphs to the previous guidance:

5, 6, 16, 19, 28-30, 32, 37-43, 45, 70 77-79

Background

About this Guidance

1. From 6 April 2018 the Occupational Pension Schemes (Administration and Disclosure) (Amendment) Regulations 2018 (“the 2018 Regulations”) introduce requirements relating to the disclosure and publication of the level of charges and transaction costs by the trustees and managers of a relevant scheme[footnote 82].

2. The 2018 Regulations amend the Occupational Pension Schemes (Scheme Administration) Regulations 1996[footnote 83] (“the Administration Regulations”) and the Occupational and Personal Pension Schemes (Disclosure of Information) Regulations 2013[footnote 84] (“the Disclosure Regulations”) to reflect these new requirements.

3. From 1 October 2019 the Pension Protection Fund (Pensionable Service) and Occupational Pension Schemes (Investment and Disclosure) (Amendment and Modification) Regulations 2018 (referred to in this Guidance as “the Amending Regulations”) introduce requirements relating to the disclosure and publication of the Statement of Investment Principles, alongside other related material. The Amending Regulations amend, amongst other Regulations, the Disclosure Regulations and the Occupational Pension Schemes (Investment) Regulations 2005[footnote 85].

4. Some of the duties inserted by the 2018 Regulations and the Amending Regulations, require trustees and managers to have regard to guidance issued from time to time by the Secretary of State in complying with the relevant requirements of those Regulations.

5. The Occupational Pensions Schemes (Investment and Disclosure) (Amendment) Regulations 2019 (“the 2019 Regulations”) introduce requirements relating to the disclosure and publication of the Statement of Investment Principles and other related material for non-relevant schemes. The 2019 regulations amend the Occupational and Personal Pension Schemes (Disclosure of Information) Regulations 2013 to reflect these new requirements.

6. The Occupational Pension Schemes (Administration, Investment, Charges and Governance) (Amendment) Regulations 2020 (“the 2020 Regulations”) introduce requirements relating to the reporting of investment performance and the assessment of value for members offered by a relevant scheme.

7. Apart from the elements described in this Guidance it is up to trustees and managers of occupational pension schemes to decide how, consistently with their legal obligations, to implement the requirements of the legislation based on the needs of their scheme’s membership.

Expiry or review date

8. This Guidance will be reviewed as a minimum every 3 years, from the date of first publication, and updated when necessary.

9. This document makes reference to a range of assumptions used in Actuarial Standards Technical Memorandum 1 (AS TM1) issued by the Financial Reporting Council (FRC), and used by the Financial Conduct Authority (FCA) in the Conduct of Business Sourcebook (CoBS).

10. In broad terms, the intention is to allow schemes to use the current assumptions set out for the production of illustrations in:

- CoBS[footnote 86] as at 6 April 2019, as amended by FCA Handbook Notice 51[footnote 87]; and

- version 4.2 of AS TM1, published in October 2016[footnote 88]. Subsequent references to CoBS and AS TM1 in this Guidance should be taken to refer to these versions

11. When relevant assumptions in AS TM1 or in CoBS are updated, our intention is to consult in good time to ensure that, where appropriate, alignment between this Guidance, AS TM1 and CoBS is maintained.

12. The Guidance does not take precedence over, or try to direct, CoBS or AS TM1 in relation to the production of other projections.

13. When we review the Guidance, we will also consider, for possible inclusion, lessons from established and emerging best practice and user testing of the way in which cost and charge information is presented.

Audience

14. This Guidance is for trustees and managers of relevant occupational pension schemes (broadly, money purchase schemes and non-money purchase schemes in relation to their money purchase benefits, in both the accumulation and decumulation phases). Trustees and managers of non-relevant schemes may also find this Guidance helpful when meeting their publication requirements.

15. None of the publication requirements of the 2018 Regulations or the 2020 Regulations apply to:

- schemes where the only money purchase benefits offered arise from Additional Voluntary Contributions (AVCs);

- relevant small schemes[footnote 89]

- executive pension schemes[footnote 90]

- schemes that do not fall within paragraph 1 of Schedule 1[footnote 91] (description of schemes) to the Disclosure Regulations – most commonly single member schemes, schemes which are not tax registered and schemes which provide only death benefits

- public service pension schemes, as defined by section 318 of the Pensions Act 2004[footnote 92]

- In addition, the publishing requirements in the Amending Regulations and 2019 Regulations do not apply to:

- schemes to which the 2018 Regulations do not apply

- schemes with fewer than 100 members

- schemes established under an enactment or guaranteed by a public authority

- schemes not established under a trust

When this Guidance should be followed

17. The amendments made by the 2018 and the 2020 Regulations require occupational pension schemes which offer money purchase benefits (subject to the small number of exceptions above at paragraph 15) to, among other things:

- provide an illustrative example of the cumulative effect of costs and charges[footnote 93] incurred by the member as part of the Chair’s Statement

- publish that and certain other parts of the Chair’s Statement (or all, if a scheme wishes to do so) on a website for public consumption

18. The amendments made by the Amending Regulations require trustees of schemes with 100+ members offering money purchase benefits (subject to the exceptions in paragraph 16) to, among other things:

- from 1 October 2019, publish the Statement of Investment Principles (SIP)

- from 1 October 2020, publish an implementation statement on how they acted on the SIP

19. The amendments made by the 2019 Regulations require trustees of pension schemes with 100+ members not offering money purchase benefits (subject to the small number of exceptions at paragraph 16) to:

- by 1 October 2020, publish the Statement of Investment Principles (SIP)

- by 1 October 2021, publish an implementation statement on how they acted on the voting and engagement sections of the SIP

20. Trustees and managers of occupational pension schemes must have regard to this Guidance, where applicable, on meeting these legislative requirements.

Legal status of this Guidance

21. This statutory Guidance is produced under section 113(2A) of the Pension Schemes Act 1993 (“the 1993 Act”).

22. This Guidance replaces the previous Reporting of costs, charges and other information: guidance for trustees and managers of relevant occupational pension schemes statutory guidance, which was published in September 2018, and was issued under section 113(2A) of the 1993 Act.

Compliance with this Guidance

23. For occupational pension schemes, The Pensions Regulator (TPR) monitors compliance with the legislation and provides guidance about what employers and people running schemes need to do. The Department for Work and Pensions (DWP) is responsible for answering questions about the policy intentions behind the legislation. Neither DWP nor TPR can provide a definitive interpretation of the legislation which is a matter for the courts.

24. Trustees and managers and service providers should consider the Regulations to determine whether the new requirements apply to them, taking further advice where necessary.

25. Where the trustees or managers do not comply with a relevant legislative requirement of the Administration Regulations or the Disclosure Regulations by virtue of a failure to have regard, or to have proper regard, to this Guidance, the Pensions Regulator may take enforcement action which includes the possibility of a financial penalty.

26. Enforcement of Part V of the Administration Regulations, including the production and content of the Chair’s Statement, is currently provided for in Part 4 of the Occupational Pension Schemes (Charges and Governance) Regulations 2015[footnote 94]. Regulation 5 of the Disclosure Regulations sets out the penalties for failure to comply with any other requirement under those Regulations, including any failure to publish costs, charges and other relevant information in accordance with regulation 29A of those Regulations.

Production of an illustration

Overview

27. This section of the Guidance sets out the matters to which trustees and managers of relevant schemes must have regard when producing an illustration in accordance with regulation 23(1)(ca) of the Administration Regulations, as inserted by the 2018 Regulations.

28. The purpose of the illustrations is to communicate simply and clearly to members the impact of cost and charges on their pension pots, and the compounding effect of small differences in charges over the long term.

29. To show the effect of a range of charging levels, the illustrations should identify the default arrangement(s), lowest charging and highest charging self-select fund in which members are invested, and highlight to scheme members the difference in the compounding effect of the charges of each respective fund in which assets relating to members are invested during the scheme year.

30. If the charging levels or the defaults vary by employer, then each part of the scheme with a different default or charging levels should be treated as a separate scheme, and the three illustrations described above produced. This is to ensure that each employee who is interested can see the compounding effect of costs and charges on their default arrangement and a sample of other funds, regardless of the pension scheme’s pricing model.

31. Trustees and managers should present the costs and charges typically paid by a member as a figure in pounds, or pounds and pence.

32. Illustrations should be produced for the following sections of the scheme:

- default/s (schemes with more than one default, or a default whose price varies with employer, should produce an illustration for each)

- lowest charging self-select fund, by employer

- highest charging self-select fund, by employer

33. The illustration should be produced having regard to the Guidance, providing realistic and representative figures for the following elements:

- savings pot size

- contributions

- real-terms investment return, gross of costs and charges

- adjustment for the effect of costs and charges

- time

34. The examples below do not seek to be wholly prescriptive. Schemes are free to go further in the disclosure of additional illustrations based on the characteristics and diversity of their scheme membership, the fund or arrangement offerings where they feel an inclusion of these characteristics will improve the quality of the illustration.

35. When trustees and managers are deciding how best to present this data, they should consider the needs and preferences of their membership. Schemes are free to use a variety of different approaches which they believe to be more suitable for particular groups of members.

Examples

36. An example of how an illustration can be prepared which is consistent with this Guidance is shown below. This example uses assumptions which are based on CoBS as at 6 April 2019.

Figure 1

Projected pension pot in today’s money

Default arrangement:

| Years | Before charges + costs | After all charges + costs deducted |

|---|---|---|

| 1 | ||

| 3 | ||

| 5 | ||

| 10 | ||

| 15 | ||

| 20 | ||

| 25 | ||

| 30 | ||

| 35 | ||

| 40 |

Highest charging employee self select fund:

| Years | Before charges + costs | After all charges + costs deducted |

|---|---|---|

| 1 | ||

| 3 | ||

| 5 | ||

| 10 | ||

| 15 | ||

| 20 | ||

| 25 | ||

| 30 | ||

| 35 | ||

| 40 |

Lowest charging employee self select fund:

| Years | Before charges + costs | After all charges + costs deducted |

|---|---|---|

| 1 | ||

| 3 | ||

| 5 | ||

| 10 | ||

| 15 | ||

| 20 | ||

| 25 | ||

| 30 | ||

| 35 | ||

| 40 |

Notes:

1. Projected pension pot values are shown in today’s terms, and do not need to be reduced further for the effect of future inflation.

2. The starting pot size is assumed to be £10,000 and contributions are £1000 per year.

3. Inflation is assumed to be 2% each year.

4. Contributions are assumed from age 22 to 68 and increase in line with assumed earnings inflation of 2.5% each year.

5. Values shown are estimates and are not guaranteed.

6. The projected growth rate for each fund or arrangement are as follows:

- default arrangement: 2.5% above inflation

- highest Charging Employee Self Select Fund: 2% above inflation

- lowest Charging Employee Self Select Fund: 1% above inflation

37. An example of how an illustration can be prepared for schemes with multiple defaults or variable charges which is consistent with this Guidance is shown below.

Figure 2

Projected pension pot in today’s money

Default – Employer Group A:

| Years | Before charges + costs | After all charges + costs deducted |

|---|---|---|

| 1 | ||

| 3 | ||

| 5 | ||

| 10 | ||

| 15 | ||

| 20 | ||

| 25 | ||

| 30 | ||

| 35 | ||

| 40 |

Highest Charging Employee Self Select Fund – Employer Group A:

| Years | Before charges + costs | After all charges + costs deducted |

|---|---|---|

| 1 | ||

| 3 | ||

| 5 | ||

| 10 | ||

| 15 | ||

| 20 | ||

| 25 | ||

| 30 | ||

| 35 | ||

| 40 |

Lowest Charging Employee Self-Select Fund – Employer Group A:

| Years | Before charges + costs | After all charges + costs deducted |

|---|---|---|

| 1 | ||

| 3 | ||

| 5 | ||

| 10 | ||

| 15 | ||

| 20 | ||

| 25 | ||

| 30 | ||

| 35 | ||

| 40 |

Default – Employer Group B:

| Years | Before charges + costs | After all charges + costs deducted |

|---|---|---|

| 1 | ||

| 3 | ||

| 5 | ||

| 10 | ||

| 15 | ||

| 20 | ||

| 25 | ||

| 30 | ||

| 35 | ||

| 40 |

Highest Charging Employee Self Select Fund – Employer Group B:

| Years | Before charges + costs | After all charges + costs deducted |

|---|---|---|

| 1 | ||

| 3 | ||

| 5 | ||

| 10 | ||

| 15 | ||

| 20 | ||

| 25 | ||

| 30 | ||

| 35 | ||

| 40 |

Lowest Charging Employee Self-Select Fund – Employer Group B:

| Years | Before charges + costs | After all charges + costs deducted |

|---|---|---|

| 1 | ||

| 3 | ||

| 5 | ||

| 10 | ||

| 15 | ||

| 20 | ||

| 25 | ||

| 30 | ||

| 35 | ||

| 40 |

38. This simple example is a scheme with only two default pricing structures. When producing the illustrations all defaults offered by the scheme must be included.

39. In relation to the self-select fund this example is of a typical scheme with variable charges which offer all the self-select funds at standard prices, less an employer specific discount. The identity of the lowest charging and highest charging self-select fund will typically, but not always, remain unchanged with the employer.

40. All members must be able to identify which employer group they are in, from their Annual Benefit Statement.

41. Members who didn’t make an active choice which fund they have been placed in by their employer are bearing the costs of being invested in that respective fund. Therefore, it is essential that they are able to calculate what they paid in costs over a saving lifetime as a result. Members of schemes with multiple defaults or variable charges have the same right to this information as those with a single price for employees of all employers.

42. This simple example is a scheme with two default pricing structures. All defaults offered must be included in the illustrations.

43. However, the illustrations for each respective employer group do not need to be presented alongside each other in the Chair’s Statement. Alternatively, Trustees can provide members with a bespoke link to the illustration for their specific employer group.

Required elements

Savings pot size

44. Schemes should use one or more typical savings pot sizes to illustrate the long-term effects of charges. These sizes should be broadly representative of the actual pot sizes of members of the scheme. For example, if trustees and managers chose to use just one pot size, the median pot size in the scheme should be used as a benchmark by which to set the value of the savings pot used in the illustration.

45. For schemes with multiple defaults or variable charges this should simply be a median across the whole scheme rather than producing a median for each default, or for each employer using the scheme.

46. The pot size assumption should be clearly stated.

Contributions

47. Many members will be contributing to the pension scheme, and it is, therefore, often most meaningful for the illustration to show the effect of further contributions to the scheme. Contributions will generally increase in nominal terms, as they are typically a percentage of salary. Where salaries increase faster than inflation, there will be real-terms growth in contribution levels.

48. Where trustees and managers include further contributions to the scheme, the assumed initial future contribution level should be broadly representative of the overall level of contributions (including employer and employee contributions, and tax relief) and should be stated.

49. Where the product is being used for flexi-access drawdown, one or more expected representative future withdrawal rates should be assumed.

50. Future contribution level increases may currently be assumed to be zero in real (inflation-adjusted) terms, unless statute, scheme provisions or recognised practice require otherwise.

51. Real-terms contribution growth of 1.5% or more, taking into account expected real terms salary increases, may alternatively be assumed.

52. Where it is both disproportionately burdensome for schemes to show the effect of future contributions, and the scheme features no charges levied on contributions, trustees and managers may assume that no further contributions to the scheme will be made. This assumption should also be stated. Where the scheme levies a charge of any kind on contributions, at least one illustration including contributions should be shown.

Real-terms investment return gross of costs and charges

53. In line with AS TM1, we expect the real-terms investment return to take account of the expected returns, from the current and anticipated future investment strategy of each fund or arrangement over the period to the retirement date.

54. Alternatively, trustees and managers may, if they wish, use as a basis the intermediate rate real-terms investment return assumption currently permitted by CoBS.

55. An unrealistic expected rate of return should not be presented to the member, as this could distort the compounding effect of costs/charges. Schemes therefore should not use assumed rates of real terms investment returns gross of costs and charges which are higher than both those set out in CoBS or for AS TM1.

56. Both AS TM1 and CoBS refer to a category of costs named ‘dealing costs’. The CoBS investment return assumption is gross of charges, but the charges do not include dealing costs[footnote 95]. For schemes not subject to FCA rules on projections, the AS TM1 nominal investment return assumption is the ‘accumulation rate’ – the expected returns before the deduction of charges and other expenses – but again those charges and expenses exclude any dealing costs[footnote 96].

57. Neither the FRC nor the FCA define dealing costs, but for the purposes of producing these illustrations this Guidance treats them as equivalent.

58. Therefore, if the current CoBS investment return assumption is used, a maximum gross real-terms return of 3% plus the transaction costs is permitted.

59. If AS TM1 is used, a maximum gross investment returns of the ‘accumulation rate’ plus the level of transaction costs but minus the ‘inflation rate’ is permitted.

60. For the assumed level of transaction costs, see paragraph 63.

61. The real-terms investment return assumption only needs to be shown for each fund or arrangement for which an illustration is provided.

Adjustment for the effect of costs and charges

62. The effect of charges should be determined by an adjustment inclusive of all the charges, including performance fees, and transaction costs, which will have been taken from a member’s pot.

63. The transaction costs, as defined in regulation 2(1) of the Occupational Pension Schemes (Charges and Governance) Regulations 2015, should be based on an average of the previous 5 years’ transaction costs or, where data is available for less than 5 years, an average of transactions costs over the years for which data is available.

64. The charges (similarly defined in regulation 2(1) of the Charges and Governance Regulations) should be forward-looking and take into account all of those a client will, or may, expect to be taken after investment into the product. The percentage rate (or pound amount, in the case of flat fees) used should be stated.

65. Similarly, any change in flat fee in future should be taken into account. Where this is set to increase in line with inflation a figure of 2% (for Consumer Prices Index) or 3% (for Retail Prices Index) can be used.

66. Where trustees and managers choose to report the transaction costs associated with entering, exiting and switching between funds or arrangements, they should also show these effects in the illustration.

67. Where the scheme offers funds or arrangements set at a range of different charges/total charge and cost levels, trustees and managers should again use a representative range of charges and costs, illustrating the default(s), lowest and highest charging default(s) and self-select funds for each employer or group of employers. It is not necessary to include every individual fund or arrangement offered by the scheme in the illustration.

Time

68. The illustration should show the cumulative effect of the charges and transaction costs on the value of a typical member’s savings pot over time. This should reflect the approximate duration that the youngest scheme member enrolled has saving until they reach the scheme’s Normal Pension Age set out in scheme rules.

69. Trustees and managers are only expected to present one starting point as a minimum. However, if the presentation method allows this to be easily understood, a scheme may also choose to present additional starting points depending on the generational demographic of the scheme membership. Trustees and managers should seriously consider presenting alternate start points if the level of costs and charges varies significantly by age – for example if younger members’ contributions are invested in a low-cost allocation of assets, but those members pay significantly more the closer they are to retirement.

Optional elements

70. Trustees may choose to provide additional illustrations where they believe these would be useful for members – for example for different time periods or contribution rates.

71. They may also choose to add extra information to the illustration and to present data in a more disaggregated format.

72. Examples of additional information trustees and managers may provide include:

- historic performance data about the funds or arrangements in which members are invested (although it should be made clear that this is no guide to the future)

- future charges data, if charges are expected to change

- percentage of gross investment returns lost over time

- percentage of the pot lost to costs and charges compared with a situation where no costs and charges were incurred. Trustees should provide an explanation of ‘negative transaction costs’)

73. Examples of greater disaggregation which may be provided include:

- a breakdown of charges into investment and administration costs

- a breakdown of transaction costs – for example into explicit costs (such as broker commission, settlement fees, and custody ticket fees) and implicit costs (slippage)

74. Where this additional or disaggregated information is provided, trustees and managers should carefully consider whether they believe that members would benefit from the information and whether it would prove distracting.

75. Provision of data in a more disaggregated form does not remove the expectation to also display it in aggregated form.

Publication of costs, charges and other information

76. This section of the Guidance sets out the matters to which trustees and managers of relevant schemes must have regard when publishing information under regulation 29A of the Disclosure Regulations, as inserted by the 2018 Regulations, and amended by the Amending Regulations, the 2019 Regulations and the 2020 Regulations. Trustees and managers of non-relevant schemes may also find this guidance helpful.

Required elements

Presenting the information

77. The Statement of Investment Principles, the Chair’s Statement (inclusive of charges and transaction cost information, value for money assessment and default SIP), and the relevant section of the Annual Report (the implementation statement) do not necessarily have to be produced as a single web-page or PDF document.

78. The information under regulation 29A can be published over a number of pages. When circulated in physical print the Chair’s Statement can then be a collation of these pages.

79. An example of how the documents in the annual report and accounts that can be presented as a series of linked web-pages or PDF documents which is consistent with regulation 29A is below:

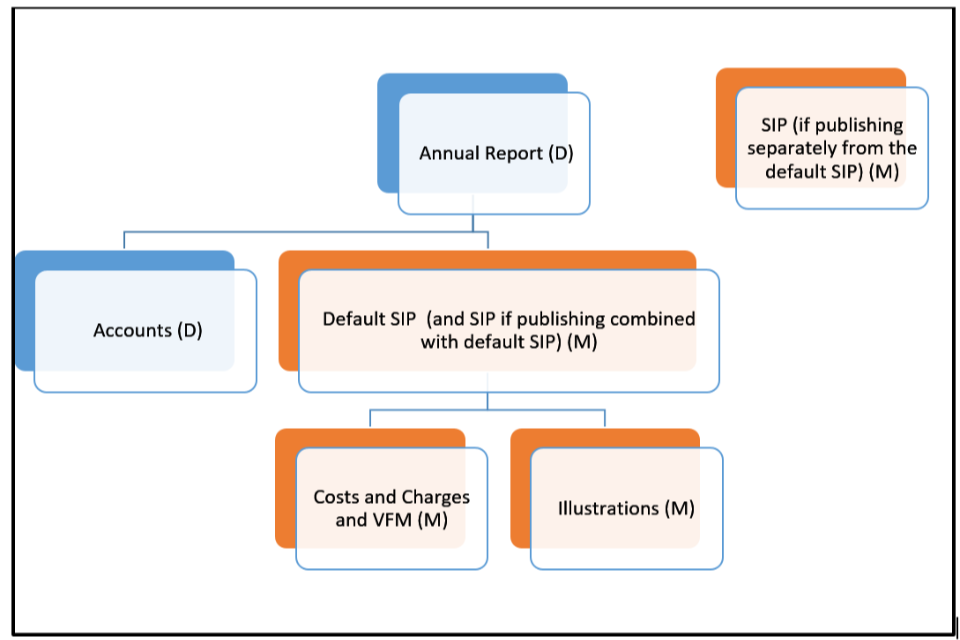

Figure 3 - illustration of a document chain which is consistent with Regulation 29A

1. Figure 3 depicts a flow chart showing how the documents can be presented.

2. At the top of the flow chart is a box labelled ‘Annual Report’.

3. Flowing out of this box is a box labelled ‘Accounts’ and a separate box labelled ‘Default SIP (and SIP if publishing combined with default SIP)’.

4. This illustrates that trustees can provide a link to the Accounts and Default SIP from their Annual Report and present them separately.

5. Flowing out of the box labelled ‘Default SIP (and SIP if publishing combined with default SIP)’ are two additional boxes, one labelled ‘Costs and Charges and VFM’ and another labelled ‘Illustrations’.

6. This illustrates that trustees can provide a link to their costs and charges and VFM information and the compounding illustrations from their Default SIP and present them separately.

7. Directly to the right of the flow chart is a box labelled ‘SIP (if publishing separately from the default SIP)’.

8. This is to illustrate the SIP can be presented separately from the default SIP.

9. Collectively all the documents referenced in the separate boxes of the flow chart are the Annual Report and Accounts.

10. The boxes labelled ‘Default SIP (and SIP if publishing combined with default SIP)’, ‘Costs and Charges and VFM’, ‘Illustrations’ and ‘SIP (if publishing separately from the default SIP)’ all have an additional label (M).

11. (M) stands for ‘Mandatory publishing requirement’. All boxes with this label represent documents which collectively are the published parts of the Chair’s Statement.

12. The boxes labelled ‘Annual Report’ and Accounts’ have an additional label (D).

13. (D) stands for ‘Discretionary publishing requirement’. This illustrates that there is no legal requirement to publish the documents labelled (D).

Finding and accessing the information

80. Whether produced as one document or separated out, the Statement of Investment Principles, the relevant sections of the Chair’s Statement (inclusive of charges and transaction cost information) and the relevant section of the Annual Report (the implementation statement) must be published on a publicly available website. The information should be published in a manner which allows for the content to be indexed by search engines:

- if published on the scheme’s or employer’s website, it should not include text which prevents the page from being indexed, and it should be linked to other pages which are found by web search engines

- if published via another website – for example, via a social media site, a blogging tool or a repository offered by a search engine provider – appropriate boxes should be selected to ensure that the document is public and can be indexed

81. Persons wishing to view the information should not be required to do so by:

- entering a specific user name and/or a specific password

- providing any other personal information about themselves

82. The Disclosure Regulations also require that a specific web address for the location of the published materials on the internet be included in a member’s Annual Benefit Statement. The web address should be appropriately titled so that members can readily re-type it into a web browser, and should clearly describe the information to be found at the location.

Needs of disabled people

83. Trustees and managers should satisfy themselves that they have adequately taken account of the needs of disabled people in publishing the Statement of Investment Principles, and relevant sections of both the Chair’s Statement, and the Annual Report.

84. Examples of factors they should take into account include, but are not limited to:

- whether screen reading software used by visually impaired and blind people can read the content and in a logical sequence

- whether the text can be enlarged, and whether the contrast in the pages is adequate so it can read by visually impaired people

- whether the text is simply and clearly written for the benefit of cognitively-impaired users

85. Standards which trustees and managers may wish to take account of, in verifying that the content takes account of the requirements of disabled people are:

- the web content accessibility guidelines (WCAG) 2.0[footnote 97], published by the Web Accessibility Initiative[footnote 98], established by the World Wide Web Consortium (W3C)

- BS 8878:2010 Web accessibility. Code of practice, published by the BSI Group

86. Section 29 of the Equality Act 2010[footnote 99] makes it unlawful for service providers to discriminate against people with disabilities. The “Services, public functions and associations: statutory code”[footnote 100] published by the Equality and Human Rights Commission to accompany the Act highlights that websites may in themselves constitute a service covered by the Act, for example, where they are delivering information to the public.

87. Although this section of the Guidance is about publishing information, the attention of trustees and managers is drawn to new regulation 29A(4) of the Disclosure Regulations concerning the provision of information in hard copy. Where the person has a disability which means that they are less able to access information on a website, this should be a key factor in deciding to provide that information in a different format.

Storage or printing of the information

88. The Statement of Investment Principles, and the relevant sections of both the Chair’s Statement and the Annual Report, whether published on a single page or across more than one page, should be published on a webpage in a way which enables the information displayed to be printed by the reader using widely used web browsers, using the menus available via the browser or functionality on the page itself.

89. In addition, the webpage on which the information is displayed should be such that the Statement of Investment Principles and any relevant sections of both the Chair’s Statement and the Annual Report should be capable of being downloaded and stored using a modern web browser, again either via the browser menus or the page’s functionality.

Optional elements

90. Pension schemes may additionally wish to publish the Statement of Investment Principles, and relevant sections of both the Chair’s Statement and the Annual Report in other locations, such as on the password-protected online servicing sections of their website. However, this does not remove the requirement to publish the information online in such a way that all can find the information without registration or entering any personal details.

-

Relevant scheme is defined in regulation 1(2) of the Administration Regulations. See paragraph 12 for more information about the scheme types which are excluded from the definition of “relevant scheme” ↩

-

The Occupational Pension Schemes (Scheme Administration) Regulations 1996 ↩

-

The Occupational Pension Schemes (Investment) Regulations 2005 ↩

-

FCA Handbook Notice 51 confirmed that the FCA Board had approved revised assumptions for projections following consultation in Quarterly Consultation Paper No 18 (CP 17/32). These changes, which are listed in pages 113-115 of the CP17/32, will come into effect from 6 April 2019 ↩

-

Actuarial Standard Technical Memorandum: AS TM1 Current Versions ↩

-

Also known as ‘Small Self-Administered Schemes (SSASs)’, a relevant small scheme is an occupational scheme with fewer than 12 members where all the members are trustees of the scheme or all the members are directors of a company which is the sole trustee of the scheme ↩

-

Executive Pension Scheme means an occupational scheme in relation to which a company is the only employer and the sole trustee; and the members of which are either current or former directors of the company and include at least one third of the current directors ↩

-

Actuarial Standard Technical Memorandum: AS TM1 Current Versions ↩

-

In practice, we are aware of no such schemes which meet this definition and offer money purchase benefits other than those attributable to AVCs ↩

-

‘Transaction costs’ and ‘charges’ are defined in the Occupational Pension Schemes (Charges and Governance) Regulations 2015 ↩

-

The Occupational Pension Schemes (Charges and Governance) Regulations 2015 ↩

-

CoBS 13 Annex 2 paragraph 2.6 (1) and (2) ↩

-

C2.4 and C2.9 of Actuarial Standard Technical Memorandum 1 ↩

-

Services, public functions and associations Statutory Code of Practice ↩